SPANISH MARKET QUICK OVERVIEW - March 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SPANISH MARKET QUICK OVERVIEW March 2019

RETAIL MARKET OVERVIEW JANUARY 2019 2

QUICK OVERVIEW

KEY PORTFOLIO METRICS TOP 10 TENANTS BY CONTRACTUAL RENT

GAV (€M) 898M MEDIA MARKT 4.5%

ZARA 4.2%

ASSETS 19

BRICOR 3.6%

GLA (m2) 318k 3.1%

CARREFOUR

AVE. ASSET VALUE (€M) 47M AKI 2.9%

VACANCY 1.80% SPRINTER 2.4%

NATIONAL TENANTS 93% MERCADONA 2.2%

KIWOKO 2.2%

WAULT(1) 14.8 yrs

KIABI 2.0%

AVE RENT (m2/month) €13.96 1.9%

WORTEN

SECTOR SPLIT BY GAV TENANT MIX BY CONTRACTUAL RENT GEOGRAPHICAL SPLIT BY GAV

31% Fashion 43% Andalucia

GAV RENT 10% F&B GAV 23% Extremadura

€898M €4.3M 9% Services €898M 11% Castilla León

7% Electronics 10% Com. Valenciana

66% Shopping Centre

7% Sports goods 8% Madrid

31% Retail Park 6% 4%

Supermarket Asturias

3% Offices 30% 1%

Other Murcia

(1) To expiry of lease (4.5 years to break)

Note: All data as at 30 September 2018

RETAIL MARKET OVERVIEW JANUARY 2019 3

SPAIN PORTFOLIO PROFILE

9

4%

1 El Faro 10 Marismas de Polvorín

2 Bahía Sur 11 Edificio Alcobendas

4 11%

3 Los Arcos 12 Mérida

4 Vallsur 13 Villanueva

11

7 5 Habaneras 14 Pinatar Park

8% 17

16 23%

6 Granaita SC 15 Motril

12 10% 7 Parque Oeste de Alcorcón 16 Mejostilla

1

13 8 Granaita RP & LC 17 Ciudad del Transporte

5

9 Parque Principado 18 Edificio Bollullos de la Mitación

1%

3 18 14

10 6 8

43%

15

2

(1) Parque Oeste comprises two adjacent properties that were acquired in two separate

companies, but has been treated as a single combined property for reporting purposes

Property rank by value

(2) La Serena comprises two adjacent properties that were acquired in two separate

companies, but has been treated as a single combined property for reporting purposes

% Geographic profile by value

Note: All data as at 30 September 2018

RETAIL MARKET OVERVIEW JANUARY 2019 4

TOP 10 ASSETS 1/3

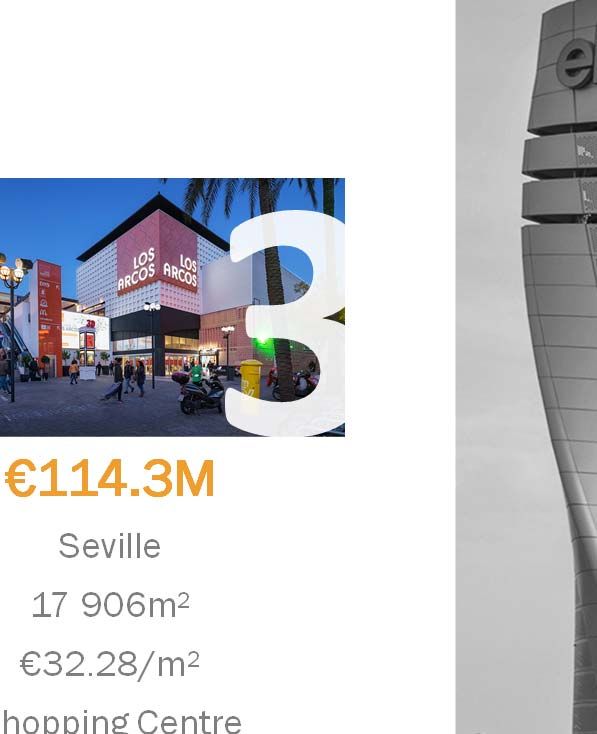

EL FARO BAHÍA SUR LOS ARCOS

GAV €161.5M €119.5M €114.3M

PROVINCE Badajoz Cadiz Seville

GROSS LETTABLE AREA 43 423m² 24 760m² 17 906m²

MONTHLY RENTAL €16.70/m² €24.72/m² €32.28/m²

SECTOR Shopping Centre Shopping Centre Shopping Centre

WALE 3.9 years 1.3 years 3 years

VACANCY 2.4% 1.9% 5.7%

Note: All data as at 30 September 2018

RETAIL MARKET OVERVIEW JANUARY 2019 5

TOP 10 ASSETS 2/3

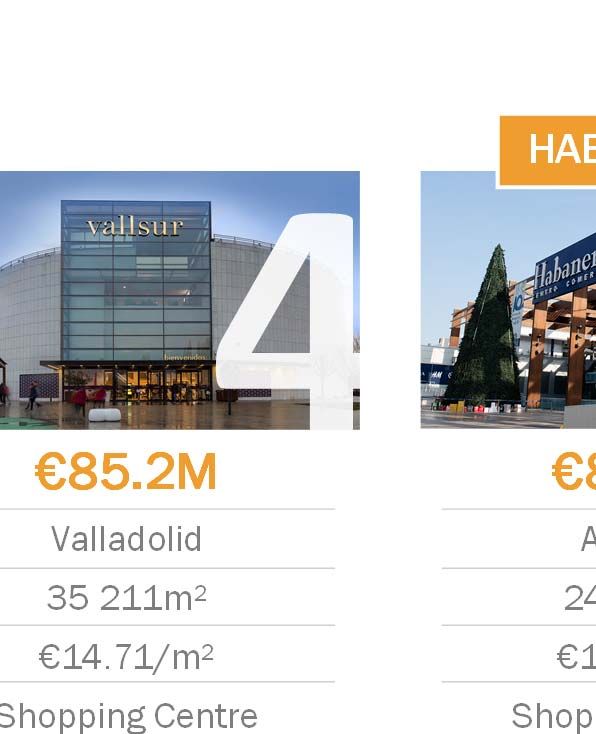

VALLSUR HABANERAS GRANAITA SC

GAV €85.2M €85.2M €59.8M

PROVINCE Valladolid Alicante Granada

GROSS LETTABLE AREA 35 211m² 24 158m² 27 913m²

MONTHLY RENTAL €14.71/m² €17.80/m² €10.70/m²

SECTOR Shopping Centre Shopping Centre Retail Park

WALE 10.1 years 4.6 years 2 years

VACANCY 2.9% 4.2% 2.2%

Note: All data as at 30 September 2018

RETAIL MARKET OVERVIEW JANUARY 2019 6

TOP 10 ASSETS 3/3

PARQUE OESTE ALCORCON(1) GRANAITA RETAIL PARK PARQUE PRINCIPADO MARISMAS DEL POLVORIN

GAV €52.7M €34.1M €32.8M €29.1M

PROVINCE Madrid Granada Asturias Huelva

GROSS LETTABLE AREA 13 604m² 18 508m² 16 396m² 20 000m²

MONTHLY RENTAL €15.69/m² €9.24/m² €9.52/m² €7.37/m²

SECTOR Retail Park Retail Park Retail Park Retail Park

WALE 4.2 years 7 years 4.9 years 3.3 years

VACANCY Fully Let Fully Let Fully Let Fully Let

(1) Parque Oeste comprises two adjacent properties that were acquired in two separate companies, but has been treated as a single combined property for reporting purposes

Note: All data as at 30 September 2018

RETAIL MARKET OVERVIEW JANUARY 2019 7

SALES & E-COMMERCE

*SPANISH SALES PER ACTIVITY IN SCs (1) **SPANISH E-COMMERCE / RETAIL CATEGORIES (2)

FASHION 0.1% Only 4.8% of total sales transactions are done online in

-0.8%

Spain (vs 9% average across EU)

1.5%

ACCESSORIES 1.1%

1.4%

Pure retail (excluding event tickets, transport etc)

FOOD THE SPANISH DIFFERENCE

2.9% comprises c. 29% of total online sales

4.0%

HOUSEHOLD GOODS 2.8%

Spain unlikely to experience similar

3.8%

negative impact as in the UK & US

SPORTS & SPECIALITY 1% Health & Beauty

4.0%

3% Electronics RETAIL Spanish culture keenly geared

-2.6%

ELECTRONICS -2.4% 1% Department Stores 29% towards socialising, eating out –

3.2% 7% Enterteinment Spanish consumers spend the highest

SERVICES 1.3%

4% Leisure proportion of their budgets on eating

3.8%

LEISURE 1.0%

1% Hosehold out in Europe

2% Services

2.7%

FOOD & BEVERAGE 4.3% 1% Restaurants Favourable weather conditions and

1.1% 7% Fashion tourism also encourage increased

GENERAL REST OF

0.8%

2% Food F&B and Leisure offerings

CATEGORIES

71% Others

Average 2016-2017 2018 Q1 71%

* Source: “¿Qué le pasa a la moda?” report 2018 CBRE

** Source: Retail Market Presentation Jan’19 Savills Aguirre Newman

RETAILERS LANDSCAPE SPANISH MARKET March 2019

RETAIL MARKET OVERVIEW JANUARY 2019 9

FOOD CATEGORY

Discount supermarkets (Mercadona, Aldi, Lidl) growing faster than rest of market as consumers are MERCADONA HAS UPGRADED THEIR STORES IN

more cost sensitive HUELVA, VILLANUEVA AND MERIDA –

CURRENTLY UPGRADING STORE AT GRANADA

Discount retailers save consumers around €900 per annum on average in Spain

Consumers are visiting supermarkets less frequently but are spending more per visit AM TEAM IN DISCUSSIONS WITH KEY RETAILERS

TO IMPROVE FLOOR SPACE ACROSS THE

Consumers placing most emphasis on health benefits when shopping at supermarkets – key brands PORTFOLIO

offering more “bio” products in store

ALL MAJOR BRANDS ARE PERFORMING VERY

WELL ACROSS CASTELLANA’S PORTFOLIO

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

MERCADONA 31% CARREFOUR 1 (44%) 14,093 m2

CARREFOUR 14% MERCADONA 4 (37%) 12,045 m2

LIDL 6% ECONOMY CASH 1 (8%) 2,446 m2

ALCAMPO 3% MAXI DIA 1 (5%) 1,483 m2

EROSKI 3% ALDI 1 (3%) 1,100 m2

Lettable Area m2 (% for this category) Units

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018

RETAIL MARKET OVERVIEW JANUARY 2019 10

BEAUTY & HEALTH CATEGORY

Although hard hit by the crisis, health & beauty sector is showing strong signs of recovery

Rising incomes of female and adult consumers have led to sales growth for H&B retailers

Many new brands have entered the market with in-shop prices equivalent to online prices

Health & Beauty retailers are creating in-store customer experiences

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

PRIMOR 9% PRIMOR 4 (27%) 1,480 m2

DRUNI 7% MARVIMUNDO 1 (11%) 622 m2

SEPHORA 4% DOUGLAS 2 (9%) 478 m2

STRONG RELATIONSHIPS HAVE

CLAREL 4% KIKO 4 (8%) 422 m2

RESULTED IN TOP BRANDS LETTING

BODYBELL 3% DRUNI 1 (8%) 415 m2 LARGER BOXES AND INCREASING IN-

DOUGLAS 2% CENTROS UNICO 3 (4%) 245 m2 STORE PRODUCT OFFERINGS

PERF. JULIA 2% POEMA 1 (4%) 217m2

INCREASING HEALTH & BEAUTY

CENTROS UNICO 2% YVES ROCHER 3 (4%) 213 m2

OFFERINGS RESULTS IN INCREASED

KIKO MILANO 2% JEAN LOUIS DAVID 2 (3%) 163 m2 FOOTFALL IN PREVIOUSLY LOW TRAFFIC

RITUALS 2% NYX 1 (2%) 128 m2 AREAS

Lettable Area m2 (% for this category) Units

35 DIFFERENT BRANDS OCCUPY 56

UNITS ACROSS CASTELLANA PORTFOLIO

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 11

CINEMA CATEGORY

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

Strong and resilient cinema-going culture in

Spain CINESA 36%

12.1 million visits to the cinema in December YELMO CINES 25%

(highest single month figures in 9 years)

YELMO 1 (100%) 2,282 m2

Cinema operators are trending towards KINEPOLIS 10% CINES

opening premium, luxury cinemas with a

OCINE 8%

higher number of screens per cinema complex

High quality cinemas positively impact footfall, FULL 3%

dwell time and cross selling in shopping Lettable Area m2 (% for this category) Units

centres

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018

YELMO CINEMAS HAVE RECENTLY OPENED

A LUXURY CINEMA COMPLEX IN VALLSUR

WHICH HAS SIGNIFICANTLY INCREASED

FOOTFALL TO THE CENTRE

AM TEAM IS PLANNING NEW CINEMA

OPENINGS ACROSS THE PORTFOLIORETAIL MARKET OVERVIEW JANUARY 2019 12

FASHION & ACCESSORIES CATEGORY

TOP FASHION BRANDS WISH TO

EXPAND THEIR STORES IN LOS

Fast fashion enable consumers to purchase the same amount of clothing at the same or lower price

ARCOS, BAHIA SUR AND HABANERAS

Climate change is affecting retailers ability to manage inventory levels

AM TEAM CONSISTENTLY FOCUSED

Spanish consumers are following global trends by dressing less formally at work and home

ON ADDING NEW, UNIQUE FASHION

Large flagship stores, click & collect and pure-play retailers are a large focus of retailers in the sector OFFERINGS TO ITS PORTFOLIO

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

ZARA 5 (12%) 8,869 m2

ZARA 12%

H&M 4 (11%) 7,887 m2

PRIMARK KIABI 4 (9%) 6,770 m2

9%

PRIMARK 1 (5%) 3,996m2

H&M 5% MERKAL 5 (5%) 3,910 m2

C&A 2 (5%) 3,515 m2

STRADIVARIUS 4% BERSHKA 5 (4%) 3,256m2

STRADIVARIUS 5 (3%) 2,223 m2

MANGO 4%

MASSIMO DUTTI 4 (3%) 2,130 m2

Lettable Area m2 (% for this category) Units

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 13

DIY CATEGORY

Iberian DIY sector continues to grow apace. Forecasted to reach 4.68 billion in sales in 2018 (+5.8%

from 2017)

Leroy Merlin/AKI merger will consolidate into a large player

Bricodepot has announced that they are exiting the Spanish market

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

IKEA 41% AKI 5 (51%) 19,231 m2 STRONG RELATIONSHIPS WITH ADEO GROUP DUE

TO LARGE PRESENCE IN CASTELLANA PORTFOLIO

BRICOR 1 (29%) 10,937 m2

LEROY MERLIN 37%

CURRENTLY IN NEGOTIATIONS TO TRANSFORM

BRICOMART 1 (19%) 7,051 m2 ALL AKI UNITS INTO LEROY MERLIN ACROSS THE

BRICOMART 6%

PORTFOLIO

CADENA 88 1 (0.4%) 161 m2

AKI 5% THE FIRST POP-UP IKEA STORE IN SPAIN HAS

IKEA 1 (0.2%) 68 m2

OPENED IN HABANERAS – IKEA TRADING WELL

BRICODEPOT 4% SO HAS EXTENDED THEIR LEASE AND LOOKING TO

ROLL OUT IN MORE LOCATIONS

Lettable Area m2 (% for this category) Units

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 14

FOOD & BEVERAGE

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

Spaniards expend the highest MC DONALD’S 18% BURGER KING 9 (26%) 5,616 m2

portion of their budget on eating BURGER KING 11% FOSTER HOLLYWOOD 6 (9%) 2,038 m2

out in Europe.

FOSTER’S HOLLYWOOD 6% MUERDE LA PASTA 2 (7%) 1,507 m2

Spanish culture, tourism, LA TAGLIATELLA 6% CITY WOK 1 (5%) 1057 m2

favourable weather contributes to

VIPS 4% LA TAGLIATELLA 2 (4%) 969 m2

strong performance of F&B

TELEPIZZA 3% 100 MONTADITOS 7 (4%) 871 m2

High consumer demand has

DOMINO’S PIZZA 3% POMODORO 2 (4%) 855 m2

resulted in attractive rental levels

GINOS 2% EL FOGON DE MARIANA 3 (3%) 622 m2

Fast - casual restaurant concepts

KFC 2% GINOS 2 (3%) 618 m2

have seen the most number of

openings in Spain in 2017 IKEA RESTAURANT 1% TACO BELL 2 (3%) 613 m2

Lettable Area m2 (% for this category) Units

F&B HAS BECOME ARE LARGE FOCUS AREA FOR THE AM TEAM

F&B OFFERING WILL BE EXPANDED AND IMPROVED IN LOS ARCOS,

EL FARO, VALLSUR AND BAHIA SUR

F&B OFFERINGS HAVE INCREASED DWELL TIME FOOTFALL AND

CROSS-SELLING SYNERGIES ACROSS THE CASTELLANA PORTFOLIO

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 15

ELECTRONICS CATEGORY

AM TEAM HAS SUCCESSFULLY RESIZED

Top electronics retailers highly focused on omnichannel strategies (online & physical stores) ELECTRONICS STORES AND RE-LET TO

Physical premises act as a point of sale, showroom and click and collect ADDITIONAL RETAILERS TO IMPROVE TENANT

MIX AND INCREASE RENTALS

Retailers are reducing GLA per store by 30% on average

Electrodepot looking to increase their store network in Spain STRONG RELATIONSHIPS HAVE RESULTED IN

PORTFOLIO EXPOSURE TO BEST-OF-BREED IN

SECTOR WITH FAVOURABLE LEASE TERMS

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

MEDIAMARKT 60% MEDIAMARKT 4 (65%) 17,743 m2

FNAC 13%

WORTEN 4 (23%) 6,290 m2

WORTEN 8%

ELECTROCASH 3 (10%) 2,582 m2

SATURN 4%

ELECTROFACTORY 1 (2%) 478 m2

MILAR 2%

Lettable Area m2 (% for this category) Units

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 16

SPORTING GOODS CATEGORY

Sportswear trend is gaining strength driven by trends towards healthy living and less formal attire.

Sports goods grew by 5% in 2018, up to 5.1 billion

Sector has benefitted from changing fashion trends towards more comfortable and casual attire and a

desire for a more healthier lifestyle

*MARKET SHARE IN SPAIN **TOP RETAILERS BY GLA FOR CPS

SPRINTER 7 (43%) 11,814 m2

DECATHLON 49%

DECATHLON 1 (26%) 7,046 m2

RETAILERS ARE REQUESTING

SPRINTER 4% FORUM SPORT 2 (11%) 2,990 m2

INCREASED GLA TO SECURE THEIR

INTERSPORT 2 (6%) 1,622m2 MARKET SHARE BECAUSE OF HIGH

NIKE 4% COMPETITION IN THE SECTOR

STOCKER 1 (4%) 1,150 m2

ADIDAS 3%

DECIMAS 4 (3%) 891 m2

SPORTING GOODS OFFERING WILL BE

JD SPORTS 2 (2%) 600m2 EXPANDED IN BAHIA SUR, LOS ARCOS

DECIMAS 3% AND VALLSUR

OTEROS 3 (2%) 564 m2

Lettable Area m2 (% for this category) Units

* Source: GFK Consumer Wallet from Jan – Dec 2018 (sample of 70,000 buyers. Purchases done by credit card in the stores)

** Source: Castellana Property Portfolio Sept’2018RETAIL MARKET OVERVIEW JANUARY 2019 17

KEY STRATEGIC OBJECTIVES OF REPOSITIONING PROJECTS AND ASSET MANAGEMENT INITIATIVES

CREATE ONE-STOP QUALITY VALUE-ADD ACCRETIVE

EXPERIENCES SHOPPING NODE ENHANCEMENT PROJECTS ACQUISITIONS

Improvement of leisure offering Creation of single shopping Each capex project will Asset management team are Investment team are

at Granaita Leisure centre node in Granaita through improve quality of external constantly analysing the portfolio constantly analysing new

integration of three adjacent and internal finishes for opportunities to improve the opportunities to:

Enhancing leisure and F&B retail centres (Retail park, tenant mix and create additional

offering on top floor of shopping centre and leisure Projects will improve natural income and value though • Increase exposure to key

Habaneras centre) to offer our customers light and overall look and feel tenants to improve

unparalleled choice to for the customer • Splitting low rent boxes to re-tenant relationships and

Improving F&B and leisure increase dwell time and at higher rentals performance of portfolio

activities in Bahia Sur, Los enhance cross selling Should lead to increased

• Introduction of new and better • Secure high quality assets to

Arcos and El Faro by synergies rentals and higher valuations

retailers into the centres enhance income and

introducing more fast and high- improve portfolio quality

end dining experiences

• Lease up of vacant units

• Find opportunities where

Castellana asset

management can add

additional value and income

• Organic growth through

increasing ownership of

existing high performance

assetswww.castellanasocimi.es

You can also read