Studies in Applied Finance - INVESTMENT THESIS FOR ADVANCED METALLURGICAL GROUP (AEX: AMG)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SAF/No.20/July 2017

Studies in Applied Finance

INVESTMENT THESIS FOR

ADVANCED METALLURGICAL

GROUP (AEX: AMG)

Anshul Subramanya

Johns Hopkins Institute for Applied Economics,

Global Health, and the Study of Business Enterprise

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Advanced Metallurgical Group

Rating: Buy – Average Free Cash Flow per Share: $33.50

Company Name Advanced Metallurgical Group

Date 06/16/17

Fiscal year ends (Current Period) 12/31/2017 (Q2)

Current Price 26.42 Euros ($29.58 USD)

52 wk high (date) 27.90 Euros (06/09/17)

52 wk low (Date) 11.33 Euros (06/27/16)

Market Cap 788.67M Euros

Total Debt $173.8M

Cash $166.5M

Net Debt / Enterprise 4.38%

Dividend 1.01%

Shares outstanding / Float 29.04M

Current P/E 18.03

Bloomberg EPS Estimate (2018) $2.08

Bloomberg EPS Estimate (2017) $1.60

2018 P/E (EPS) 12.82x ($2.21)

2017 P/E (EPS) 16.57x ($1.71)

2016 EPS $1.45

2015 EPS $0.40

2014 EPS $0.79

2013 EPS -$1.51

EPS Estimates are consensus values from Bloomberg at the time of this writing

1

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Table of Contents

Executive Summary ........................................................................................................................... 3

Catalysts and Risks ........................................................................................................................... 4

Company Overview ............................................................................................................................ 5

Historical Performance ................................................................................................................... 10

AMG Model .......................................................................................................................................... 12

Monte Carlo Results ........................................................................................................................ 17

Capital Allocation.............................................................................................................................. 18

Management Compensation ........................................................................................................ 19

Conclusion........................................................................................................................................... 21

Appendix .............................................................................................................................................. 21

2

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Executive Summary

Advanced Metallurgical Group (Euronext: AMG) is a global critical materials

company headquartered in the Netherlands. AMG produces specialty metals, alloys,

and high performance materials such as ferrovanadium antimony, tantalum, and

niobium. They also engineer advanced vacuum furnace systems and operate vacuum

heat treatment facilities for the transportation and energy industries. The market

currently prices AMG at 26.42 Euros ($29.58 USD, market close 06/16/17, 0.89 Euros /

Dollar Exchange Rate, Figure 1) per share. By using a Probabilistic Discounted Cash

Flow Model (P-DCF), we estimate a free cash flow (FCF) per share of approximately

$33.50, or 29.82 Euros. This estimate is based on expectations of AMG’s current

product portfolio as well as their ongoing spodumene project, and suggests that the

stock is currently trading at a 13.25% discount. AMG has also provided an EBITDA

target of $200M+ by 2021,1 and reaching this target yields the estimated FCF per share

mentioned above. Our analysis shows that AMG has the opportunities, leverage, and

appropriate compensation metrics attain this target, so we rate AMG a buy.

Figure 1: Price Chart of AMG – AMG’s share price rose dramatically in 2016, yielding

a current price of 26.42 Euros per share

Source: Bloomberg Terminal Command ; Accessed 05/05/2017

1

Advanced Metallurgical Group (March, 2017). AGM CEO Strategy Update

3

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Catalysts and Risks

Catalysts

• Complete Deleveraging – During AMG’s austerity period (described below), the

company made steps to decrease its net debt and increase cash flows.2 These

measures successfully positioned the company for high cash flow growth moving

forwards. Subsequently, AMG is poised to take on debt in order to finance its

upcoming growth projects.

• Spodumene Mine – In July 2016, AMG supervisory board approved the

construction of a lithium concentrate (spodumene) plant at the Mibra mine in

Brazil. With the increase of mobile and portable devices, lithium’s importance is

growing rapidly. This plant aims to establish AMG as a cost leader in the lithium

market. Though this mine stands to produce substantial top- and bottom-line

growth for AMG, delays in operation or less-than-expected revenues pose a risk

to the company’s investment.

Risks

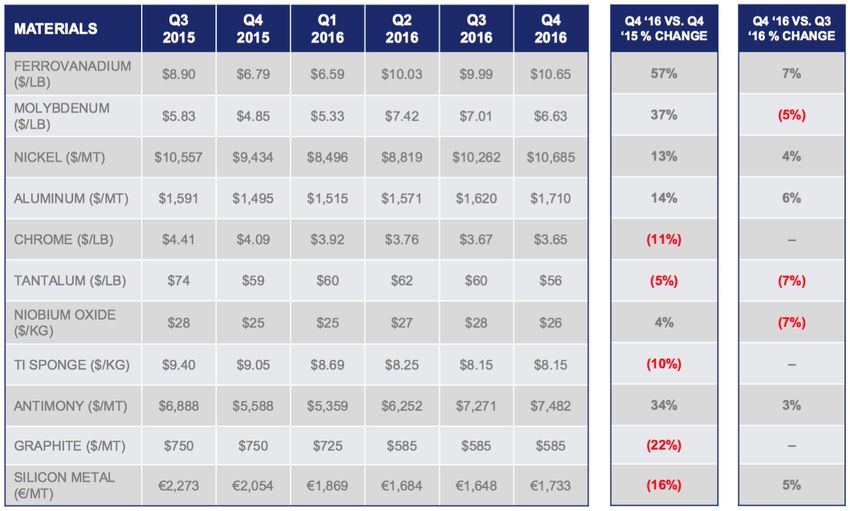

• Metal price volatility – The prices of metals that support AMG’s business

declined during early to mid-2016 but have recovered (Figure 2). Price declines

between Q4 2015 and Q4 2016 were led by chrome, graphite, and silicon.

However, unit prices of ferrovanadium, molybdenum, and nickel increased

between Q4 2015 and Q4 2016 instead. Since AMG’s products are primarily

refined metals or metal products, a decrease in the price of specialty metals

poses a risk to the business.

• Mining Risks – Risks inherent to the mining industry include safety and

regulatory concerns, geopolitical and environmental events, and unforeseen

accidents.

• Currency Risks – AMG’s global presence introduces foreign exchange (ForEx)

risk. AMG’s functional currency is the U.S Dollar, and the appreciation of the US

dollar compared to the Euro and other currencies caused ForEx loss of

approximately $500K in 2014.

2

Advanced Metallurgical Group (2016). AMG Annual Report.

4

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 2: Volatile Metal Prices – Metal prices dropped in early 2016, but have since

risen. Price declines between Q4 2015 and Q4 2016 were led by chrome, graphite, and

silicon.

AMG Investor Presentation 2016

Company Overview

AMG has two overarching business units, AMG Critical Materials and AMG Engineering.

Within the Critical Materials unit are multiple segments focusing on a particular metal or

metal product, while the Engineering unit has a single segment targeting vacuum

furnace systems. An in-depth description of each business unit can be found below,

followed by a bulleted description of the business segment hierarchy,

AMG Critical Materials

AMG’s Critical Materials unit produces a variety of specialty metals, alloys, and

high performance materials. Their most notable products are: lithium, ferrovanadium,

aluminum alloys, chromium metal, tantalum, titanium alloys/coatings, antimony,

graphite, and silicon metal. These materials need to be lighter, stronger, and more

resistant to corrosion and wear in order to meet the needs of a growing global

population. They are also in particularly short supply, as detailed in the 2014 Report on

Critical Materials for the EU.3 AMG views themselves at the forefront of global CO2

reduction trends, and delivers these high quality materials to the transportation, energy,

infrastructure, specialty metals, and chemicals end markets.

AMG Engineering

AMG Engineering designs, engineers, and produces advanced vacuum furnace

systems and operates vacuum heat treatment facilities. They primarily target the

3

EU Raw Materials Initiative (2014). Report on Critical Raw Materials for the EU

5

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

transportation and energy industries and provide systems designed for vacuum melting,

solar silicon melting, and vacuum heat treatment.

• AMG Critical Materials

o Ferrovanadium

o Lithium

o Aluminum Master Alloys and Powders

o Chromium Metal

o Tantalum and Niobium

o Titanium Alloys and Coatings

o Antimony

o Graphite

o Silicon Metal

• AMG Engineering

o Vacuum furnaces

History

AMG was incorporated in the Netherlands in November 2006 as a combination of

specialty metals businesses. The Critical Materials division had its origins in the

predecessor company Graphit Kropfmulh (GK), formed in 1870 to mine graphite in

Germany. GK was initially acquired by AMG in 2008 with 62% ownership, and AMG

acquired the remaining shares in 2010 and 2012.

The Engineering division originated with the predecessor companies of ALD

Vacuum Technologies Gmbh (ALD), founded in Germany during the mid-1800s.

Austerity Period

As of 2011, AMG began austerity measures in an effort to deleverage, cut costs,

and prioritize their balance sheet (Figure 3). This was in response to warning signs that

the global economy had not yet recovered from the 2008-2009 crisis, and a belief that

markets would continue to remain down for the upcoming years. The decisions made in

2011 were extremely successful in eliminating AMG’s net debt in 2015 and 2016, and

place AMG far ahead of their peers, particularly in terms of FCF yield (FCF / Enterprise

Value, Figure 4). Their primary debt facility is a $400M multicurrency term loan and

revolving credit facility (Figure 5), and a 5-year term through 2021 allows the company

to increase debt by up to $160M.

Clearly, AMG has the option to obtain more debt in upcoming years, giving them

flexibility in how to finance growth opportunities. This aligns with our thesis that AMG

has the resources to attain their 2021 EBITDA goals.

6

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 3: AMG Reduction in Net Debt since 2012 - Net Debt is calculated as Total

Debt minus Cash and Cash Equivalents. AMG has been able to completely deleverage

during their austerity period.

AMG Investor Presentation 2016

Figure 4: Free Cash Flow Yield – AMG significantly outperformed its peers in this

metric over the last 12 months.

AMG’s Annual Report, 2016

7

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 5: AMG’s empty debt schedule – AMG’s primary debt facility is a $400M loan

and RCF expiring in 2021. AMG has significant room to increase debt in order to

decrease cost of capital and/or finance various projects.

Bloomberg Terminal Command ; Accessed 05/05/2017

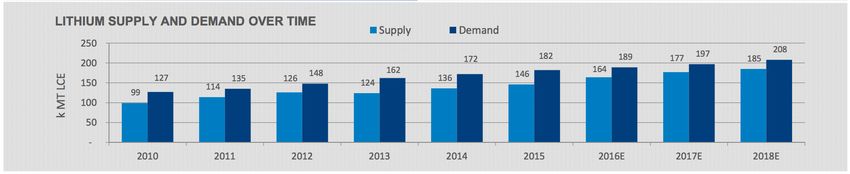

Spodumene Plant

In July 2016, AMG approved the construction of two spodumene (lithium

concentrate) plants at their Mibra mine in Brazil. These plants aim to make AMG a cost

leader in the rapidly growing lithium market (Figure 6), thus producing significant value

for shareholders. Spodumene production will be associated with a new business

segment, AMG Lithium, and will commence in mid-2018. Each plant is expected to have

a capacity of 90,000 metric tons (MT) of spodumene annually, and the full production of

180k MT is expected to occur in mid-2019.

Figure 6: Growing market for lithium – Demand for lithium is expected to continue to

grow and exceed supply through 2018. AMG aims to capture this market by becoming

the low-cost source of lithium.

AMG Lithium Presentation

8

Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Currently, the lithium project is progressing in line with expectations; a full offtake

agreement for mined spodumene has been established and production is expected to

commence mid-2018. For the purposes of the model, we assume that the first plant will

generate 45k MT in 2018 and 90k MT from 2019 onwards, while the second plant will

generate 45k MT in 2019 and 90k MT from 2020 onwards. Because of the low

production costs of spodumene (production costs are approx. 30% margin on sale

price), these plants are expected to generate significant EBITDA and bottom line

earnings for AMG, much to the benefit of the company’s FCF and to their shareholders.

The maximum output of 180k MT total per year generates annual revenue of

$144M and annual incremental EBITDA of $97.2M, and AMG estimates $96M EBITDA

from their non-lithium business in 2017. This leads to the extremely reassuring

conclusion that AMG could reach their EBITDA target of $200M by 2021 by simply

maintaining their non-lithium businesses and allowing their spodumene plant production

to ramp up. This does not even begin to consider the positive implications of rising metal

prices and any additional growth projects in the pipeline. As shown in the Monte Carlo

analysis, EBITDA of $200M from 2021 through 2026 yields an estimated FCF / share of

approx. $33, which is a significant gain over AMG’s current market value.

Organic Growth Projects

AMG’s management has mentioned that there are some promising organic

growth projects in the project pipeline. While details of these projects have not been

released, it should be noted that the BUY rating for AMG is not contingent on the

outcome of these projects. With only the spodumene project, AMG is expected to

generate enough EBITDA and cash flow to buoy their share price to over $33 per share.

Any additional top line or bottom line benefit from the organic growth projects is simply

additional upside.

Analyst Recommendations

Three of three analysts covering AMG recommended a buy rating (Figure 7).

From the results of the Monte Carlo simulation, we see that analysts seem to be valuing

AMG slightly higher than the share price targeted in this thesis. This may be due to

optimism about organic growth projects, different discount rates, or a multiples-based

approach rather than a cash-based approach. ING and Kempen target 31 and 33 euros

per share respectively, and we target approx. 30 euros per share.

9Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 7: Analyst Recommendations of AMG – Target prices for ING and Kempen

are 31 and 33 euros respectively. These prices are slightly higher than our target price

of approx. 30 euros.

Bloomberg Terminal Command ; Accessed 05/05/2017

Historical Performance

AMG’s stock price hovered between 6 and 8 euros per share until mid-2016, at

which point share price rose to over 19 euros per share in late September (Figure 1).

This rise was spurred by extremely positive earnings reports throughout early-mid 2016,

as well as reassuring news about AMG’s progress with their lithium project. Share price

fell in late 2016, likely due to falling metal prices, but has since rebounded from less

than 15 euros a share in 2016 to over 24 euros a share as of 05/15/2017. Equity

markets took note of AMG’s nine business units each outperforming their EBITDA

targets, of the company’s consistently low net debt, and of the potential within the

company’s growth projects, and share price appropriately rose.

10Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Ratio Performance

Summary of Useful Life and LTAT for AMG

13.00 3.80

3.70

12.50

3.60

Useful Life

12.00

3.50

LTAT

11.50 3.40

3.30

11.00

3.20

10.50

3.10

10.00 3.00

2011 2012 2013 2014 2015 2016

UL LTAT

Figure 8: Asset Turnover Ratios – Both LTAT and UL were lower from 2013 through

2015 compared to their values in 2011. LTAT fell prematurely in 2012 because LTA had

a brief increase in property, plant and equipment (PPE)

AMG’s 10-K filings, 2011-2016

When we look at the Long Term Asset Turnover (LTAT, Revenue / LTA) and

Useful Life (UL, LTA / Depreciation & Amortization (D&A)), we see that both ratios

dropped around 2012-2013, since both top line revenue and total long term assets

decreased while D&A costs remained relatively constant (Figure 8). Going into 2016

and out of the austerity period, LTAT continued to shrink and UL continued to increase;

in this year, AMG grew its long term assets, lost revenue due to falling metal prices, and

maintained consistent D&A costs as a margin on revenue.

Historical performance of potential free cash flow yield (PFCFY, FCF / Revenue)

and free cash flow return on invested capital (FROIC, FCF / Invested Capital (Current

Assets – Current Liabilities – Cash + LTA) reveals similar trends as those seen in LTAT

and UL (Figure 9). These two ratios were lower from 2012 through 2015 compared to

their values in 2011 and 2016, reflecting AMG’s low-growth period. The growth of these

two ratios in 2016 can be largely explained, however, by a low price of crude oil

inducing lower operating costs. In addition, these two ratios saw a small rise in 2014 as

a result of a low income tax expense.

Looking forward, we could expect both of these ratios to rise relative to their 2016

values. Crude oil prices have risen since their low in 2016 and operating costs may rise

in turn, but AMG’s multiple projects are expected to generate significant EBITDA, and

as a result FCF. As we will see in the proxy statement, operating cash flow and return

on capital employed are significant portions of management compensation metrics as

well, so an emphasis is clearly placed on bottom-line rather than top-line growth.

11Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Summary of Historical Values of Potential Free Cash Flow Yield

(PFCFY) and Free Cash Flow Return on Invested Capital (FROIC)

12.00%

Margin on Total Sales

10.00%

8.00%

6.00%

PFCFY

4.00% FROIC

2.00%

0.00%

2011 2012 2013 2014 2015 2016

Year

Figure 9: Profitability Ratios – Both PFCFY and FROIC were lower from 2012 through

2015 compared to 2011 and 2016 values. A drop in crude oil prices and thus operating

costs in 2016 contributed to the rise of both ratios, but free cash flow generated through

projects and an emphasis on cash generation at the management level should maintain

or grow these values in the future.

AMG’s 10-K filings, 2011-2016

AMG Model

AMG separates its business units by metal or metal product. This is especially

useful for the model as trends in the spot price or futures price of the metal could be

indicative of the potential earnings of the respective business segment.

We gathered quarterly revenues since 2013 for all of AMG’s business segments

within its two business units. However, it is important to note that these data reflect

revenues from a period of 1) austerity by AMG and 2) weakening metal prices. Thus,

relying solely on these historical values to project into the future would yield extremely

conservative and inaccurate estimates.

We also calculated costs allotted to capital expenditures, change in working

capital, D&A and taxes. We estimated growth for each of the 9 business segments

based on trends in metal prices, and priced the company’s lithium project

Balance Sheet and Income Statement

All data can be found in the Balance Sheet tab and Income Statement tabs in the accompanying

spreadsheet

A cursory glance at the balance sheet and income statement reveals AMG’s

commitment to deleveraging and increasing cash flow. Total long-term loans decreased

12Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

from $265M in 2012 to $112M in 2015, and total short-term loans decreased from $20M

to $3M over the same time span. Goodwill steadily decreased from $24M to $18M over

that time frame, confirming that AMG has not gone out of its way to acquire additional

specialty metal companies. In addition, total inventories decreased from $211M to

$126M between 2012 and 2015. There is an overarching trimming of the balance sheet,

as total assets (and total liabilities + equities) decreased by $200M between 2012 and

2015.

Looking at the Income Statement, there were no restructuring costs or asset

impairment costs in contrast to previous years. In addition, costs of goods sold net D&A

(COGS net D&A) significantly decreased in 2016 compared to 2015, which

subsequently increased EBITDA and net operating profit after interest and taxes

(NOPAIT).

Value Drivers

All data can be found in the Value Drivers tab of the accompanying spreadsheet

From the value drivers, we first and foremost notice the consistently negative

revenue growth rate averaging -6.32% YoY since 2011.

In addition, we notice that the margin on revenue of COGS net D&A has been

remarkably consistent from 2011 to 2015 at around 80%, but dropped in 2016 to

77.69%. Realistically, this is likely because the price of oil bottomed in early 2016 and

has only gradually risen since then, and AMG relies on oil to fuel their plants, mining,

and refinery operations. The future of oil is uncertain, with both political and economic

factors affecting the trajectory of the price per barrel, so we hold this margin to 78.50%

in our models. Assuming the COGS margin is tied to the price of oil, this simulates an

increase in oil price compared to 2016.

In addition, EBITDA jumped from 6.73% in 2015 to 9.24% in 2016. This appears

to be directly due to the drop in COGS.

Finally, we can see that AMG’s CAPEX for the years of 2013-2015 was

extremely minimal, around .5% margin on revenue. In contrast, CAPEX was

approximately 5% in 2012, and 6.76% in 2016. We also see that D&A has been

relatively constant at approximately 3% margin on revenue since 2011. Change in

working capital has been consistently negative over the last five years, reflecting a

decrease in current assets and current liabilities but an increase in cash on hand.

Revenue Growth

All data can be found in the Revenue Growth M tab of the accompanying spreadsheet

The compounded annual growth rate (CAGR) for every business segment in

AMG Critical Materials has been negative since 2013 (Figure 10). While on first glance

this is worrisome, it should be noted that this revenue captures a period of both

austerities on AMG’s side and severely weakening metal prices in the global economy.

Revenues from titanium and antimony saw the biggest hits, with yearly revenues

from titanium decreasing from $120.7M in 2013 to $87.7M in 2016, and yearly revenues

from antimony decreasing from $113M in 2013 to $75.3M in 2016.

13Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

AMG’s Engineering unit saw relatively consistent performance since 2013;

revenues shrank between 2013 and 2014, but recovered the same amount between

2015 and 2016.

Figure 10: Revenue Growth – Revenues for almost all business segments shrank

between 2013 and 2016 as a result of weakening metal prices.

AMG’s Investor Presentations

P-DCF Assumptions

The P-DCF can be found in the PDCF tab in the accompanying spreadsheet

Assumptions made in composing the P-DCF can be broken up into three

categories: Cost Margin Assumptions, Base Business Assumptions, and Lithium

Assumptions. We briefly discuss our handling of Model Tuning Parameters such as

PFCFY, FROIC, etc. at the end of this section as well.

Cost Margin Assumptions

Cost margins refer to margins for operating costs, non-operating costs, CAPEX,

and D&A. As mentioned above, the margin for COGS net D&A was likely lower than

usual in 2016 due to bottomed oil prices, so we set this margin to 78.50% for the

entirety of our 10-year projection. This assumes a rise in oil price from present day

values.

For operating costs of selling, general and administrative (SGA), restructuring,

environmental expense, and other income, historical margins are relatively consistent,

14Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

so these are projected at their historical average for the 10-year projection. We assume

asset impairment costs are 0, however, as the only significant asset impairment charge

occurred in 2013.

Interest expenses are calculated as a margin on total debt, and AMG’s interest

rate has hovered around 9% historically. Interest income, ForEx loss, and D&A are all

calculated as a margin on revenue and have been historically consistent as well. As a

result, margins for these four costs are held at historical averages for the DCF.

Income tax expense, on the other hand, is calculated as a margin on earnings

before taxes (EBT, EBITDA – Interest Expense + Interest Income – D&A) and has been

extremely volatile historically. Given AMG’s international presence, this may be due to

changes in the valuation of various currencies; management cites the volatile Brazilian

currency as one of the drivers behind its high income tax expense in 2015. An official or

targeted income tax rate is not provided by AMG, so a rate of 25% margin on EBT is

assumed for this model.

Finally, CAPEX is held at 6% margin on revenue through 2021, slightly lower

than its value in 2016. From 2022 onwards, it is held at 3%. Note that this does not

include CAPEX that will be directed towards AMG’s lithium project. Expenditures for that

item are added separately in the DCF; the CAPEX margin discussed here can be

thought of as AMG’s expenditures to grow its current business.

Base Business Revenue Assumptions

Trends in metal prices can be found in the Metal Spot Prices tab of the accompanying spreadsheet

We use the term ‘base business’ to refer to AMG’s current portfolio of business

units excluding the lithium project. We estimate revenues for AMG’s Critical Material

units by correlating business unit revenue with appropriate specialty metal spot prices.

For example, if the price of aluminum for 2017 is in line with prices from 2014, we can

expect AMG Aluminum to generate similar revenues as it did in 2014. Under this

assumption, we do not have to rely on historical growth rates to estimate future growth;

we can instead look directly at trends in the global economy and in metal spot prices.

For each business unit within AMG Critical Materials, we perform the following:

1. Identify the relevant specialty metal that supports the business unit (i.e. AMG

Chromium is supported by sales of chrome and chrome products).

2. Compare the present spot price of the metal to historical prices

3. Find the most recent year where metal price is comparable to the price in the

current year

4. Identify business unit revenue from the comparable year

5. In the P-DCF, input revenue growth rates such that by 2018, business unit

revenue approaches revenue from the comparable year

6. Assume revenue growth rate of 0% for every following year in the P-DCF.

15Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

If the current spot price of a metal is not available, we hold the revenue growth

rate at 0% YoY. This is a very conservative assumption as metal prices are increasing

as a whole in the global economy, and revenues should actually rise.

For AMG Engineering, we assume a constant 1% YoY growth in revenue for the

duration of our P-DCF.

After incorporating these assumptions, our model estimates EBITDA of around

$95M from AMG’s base business in 2021. This is in line with management’s EBITDA

target of $100M from the base business and the discrepancy can be explained by our

conservative growth estimates.

Lithium Business Assumptions

We use the term ‘lithium business’ to refer to AMG’s spodumene (lithium

concentrate) plants at the Mibra mine in Brazil. Management has offered significant

insight into their expectations for this business, namely:

- Production levels of 180k MT of lithium concentrate from 2020 onwards

- Two spodumene plants

o The first with capital investment of $50M, the second with capital

investment of $80M

o Production for the first plant begins mid-2018, production for the second

plant begins mid 2019

- Sale price that “exceeds $800 per ton of lithium concentrate”4

- Production costs of $211 per ton

- Expectations of $115M in incremental EBITDA by 2021

To price this project into the model, we project spodumene production 10 years

forward according to the plant ramp-up schedule as described above. A price per MT of

$800 is assumed in order to calculate top line sales generated from the plant, and

operating costs of $260 per MT are used to calculate EBITDA. We do make the

assumption that ‘production costs’, the term used by management, refers to all

operating costs, and that these costs exclude D&A. Lithium EBITDA is then added to

EBITDA generated from AMG’s base business. With these assumptions, our model

finds incremental EBITDA of approx. $97.2M in 2021. This is under management’s

expectations of $115M incremental EBITDA, but we elect to use our figure to provide a

more conservative estimate of free cash flow.

The CAPEX for the mines are handled as line items separate from AMG’s

expenditures for their base business. The first mine is expected to begin production mid-

2018, so we split the $50M investment into $25M spent in 2017 and $25M spent in

2018. The second plant is expected to begin production in mid-2019, costs an additional

$50M to build, and requires an additional $30M to expand the mining infrastructure in

the area. We allocate $55M of this expenditure into 2018, and $25M into 2019.

4

Advanced Metallurgical Group (March, 2017). AMG Reports Full Year and Fourth Quarter 2016 results and provides update on

lithium project. Retrieved from http://www.amg-nv.com/Investors/Press-Releases/Press-Release-Details/2017/AMG-Reports-Full-

Year-and-Fourth-Quarter-2016-Results-and-Provides-Update-on-Lithium-Project/default.aspx

16Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Model Tuning Parameters

For this paper, ‘model tuning parameters’ refers to PFCFY, FROIC, and percent

of invested capital in long term assets (LTA/IC). The typical procedure for modeling a

company using the P-DCF is to ensure that the ranges of these ratios in the model are

in line with their historical values. This ensures that a particular valuation is not reliant

on the company significantly changing their operational structure and efficiency.

We choose to not focus heavily on aligning estimated and historical model tuning

parameters for two reasons. First, the historical values of these metrics capture AMG in

their austerity period while we wish to model the company’s value after a period of high

growth. Second, we are already able to ensure that our model is realistic by basing our

assumptions for the lithium project, EBITDA, and CAPEX on management’s explicit

guidelines. These are more reliable than the company’s historical performance in

gauging their future performance.

Monte Carlo Results

These results can be found in the MC tab of the accompanying spreadsheet

To determine a margin of safety around the estimated FCF / share generated

from the P-DCF, we performed a Monte Carlo simulation.

A chart of the resulting distribution of share price is shown below. The resulting

distributions for almost every model tuning parameter was significantly out of historical

ranges, but this is because AMG will effectively be a different company in upcoming

years as it has been in the past. With EBITDA poised to double and over $100M in

capital expenditures planned, the asset base and earnings ratios for the company are

sure to change significantly in upcoming years. Comparing estimated values to historical

values, as a result, offers little insight.

Running the model yields an average estimated FCF / share of $33.50

compared to the current share price of $29.58 (Figure 12). This is an estimated gain of

13.25%.

17Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 12: Distribution of Expected Share Price with only the Lithium Project

priced in – The average estimated FCF per share is approx. $33.50, a gain of 13.25%

over the current share price. Even when ignoring any potential organic growth projects

in the future, AMG’s fundamental value is still greater than its market value.

The results of our Monte Carlo Simulation offer significant confidence in our

investment thesis. Management’s expectations of $200M EBITDA by 2021 result in the

distribution shown in Figure 12. So long as AMG completes their spodumene project,

consequently achieving management’s EBITDA goal, they will offer significant growth in

shareholder value.

Capital Allocation

Debt

As mentioned before, AMG focused a great deal on deleveraging over the last

three years and coined this strategy their ‘austerity measures’. These efforts succeeded

as the company’s net debt was negative in 2015 and rose to only $7.3M in 2016, a

debt-to-EBITDA ratio of 8.2%.

As a result, AMG has a significant amount of liquidity available to them in the

form of their RCF that expires in 2021 and their existing cash on hand (Figure 13). Just

the amount available in the RCF is enough to finance both spodumene mines, and

additional initiatives could be paid through debt if AMG decided to issue bonds as well.

This continues to align with our thesis that AMG has significant resources they

can use to fund their various value-driving projects. If desired, the company could issue

long term bonds, fund all upcoming projects through debt, and reduce cost of capital.

18Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Figure 13: AMG’s Leverage Opportunities – AMG still has approx. $243M available

in its RCF as well as $160M cash on hand.

AMG’s Annual Report, 2016

Management Compensation

AMG’s management board consists of CEO Mr. Heinz Schimmelbusch, COO Mr.

Eric Jackson, and CFO Mr. Jackson Dunckel. A full summary of their compensation can

be found in Figure 14.

Figure 14: AMG Management Board Compensation – Heinz Schimmelbusch, Eric

Jackson, and Jackson Dunckel are the three members of AMG’s management board. A

summary of their compensation is shown here.

AMG’s Annual Report, 2016

The annual bonus in the figure above depends on three key performance metrics

(weighting): return on capital employed (ROCE, 40%), operating cash flow (40%), and

individual performance (20%). AMG does not provide a definition of ROCE, and the

traditional definition of earnings before interest and tax (EBIT) divided by the sum of

19Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

shareholder equity and debt (Capital Employed) does not align with published values.

However, management states that ROCE and operating cash flow in 2016 were

significantly above targets set by the supervisory board. In addition, the first two metrics

are measured against agreed target ranges, and performance under the target range

yields 0% payout. Measurement of ‘individual performance’ is done at the discretion of

the Supervisory Board.

These particular metrics indicate that compensation is not particularly tied to top-

line revenue, but rather to cash and earnings after operating costs. We have already

shown that AMG has the growth potential to attain the $200M EBITDA target by 2021,

but this compensation scheme shows that management is also incentivized to do so.

EBIT should be an appropriate proxy for EBITDA, as we have seen that AMG’s D&A

expenses have been remarkably consistent historically. As a result, we can further

increase our confidence in our investment thesis.

Long Term Incentives include stock options and performance share units (PSU).

The number of PSUs vested is subject to a minimum average ROCE over the

performance period and the relative total shareholder return (TSR) compared to the

Bloomberg World Metal Fabricate/Hardware index. The reliance of vested PSUs on TSR

compared to the Bloomberg World Metal Fabricate/Hardware Index is reassuring. This

metric isolates AMG’s performance from global market conditions and incentivizes the

development of competitive advantages against AMG’s peers.

AMG’s peer group can be found below (Figure 15). The group follows a US-

centric approach, and was revised for this year.

Figure 15: AMG’s Peer Group

AMG’s Annual Report, 2016

20Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Conclusion

Our investment thesis for AMG is rooted in explicit guidelines released by

management regarding EBITDA targets and return from the spodumene plants. The

particular target of $200M+ EBITDA by 2021 has been stated numerous times; our

model finds that achieving this goal yields an expected FCF / share significantly above

the current market value (Figure 12). In addition, by pricing only the lithium project into

our model according to the public production schedule, our model finds that AMG is

clearly able to reach this target. We find that the stock is currently trading at a 13.25%

discount from their fundamental value, even when we ignore the impact of upcoming

organic growth projects, use conservative revenue growth assumptions for AMG’s base

business, and model the spodumene CAPEX using cash rather than debt, which would

offer a lower cost of capital. AMG’s clear debt schedule and steady cash flow allow

them to finance these opportunities as they see fit, and management’s compensation is

tied to EBIT, an effective proxy for EBITDA, that ensures they prioritize the achievement

of these targets.

In summary, AMG has the resources to fund their growth opportunities en route

to their financial targets, which, when met, should in turn buoy the company’s share

price compared to the present value. Any additional upside from future growth projects

or from more effective financing is simply an added bonus. As a result, we rate AMG a

BUY.

Appendix

21Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

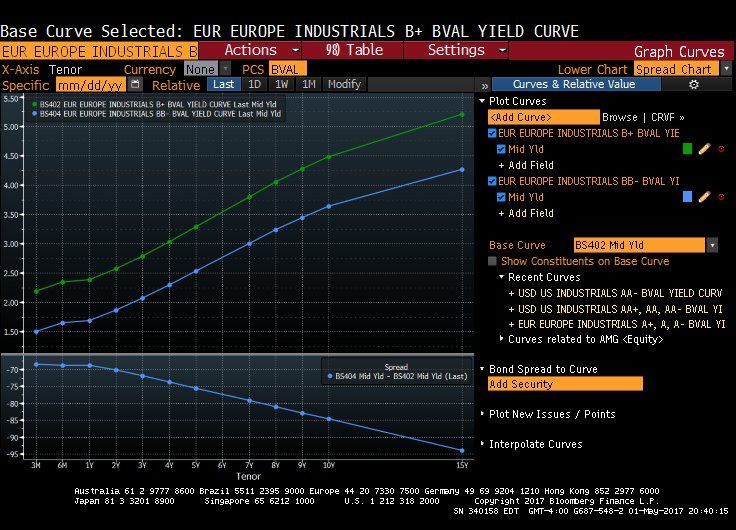

Appendix 1: Yield curves for B+ and BB- bonds

Bloomberg Terminal ; Accessed 05/05/2017

Appendix 2: AMG’s deleveraging over the last five years

Bloomberg Terminal ; Accessed 05/05/2017

22Investment Thesis: Advanced Metallurgical Group (AEX: AMG)

By: Anshul Subramanya

Last Updated: 06/16/17

Appendix 3: Ownership Summary

Bloomberg Terminal ; Accessed 05/05/2017

Appendix 4: Ownership Summary, cont.

Bloomberg Terminal ; Accessed 05/05/2017

23You can also read