THE ECONOMIC PROSPECTS FOR THE CITY OF LEEDS - Report to: CEG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE ECONOMIC PROSPECTS FOR THE CITY OF LEEDS Report to: CEG pt23@cam.ac.uk 1

Acknowledgements

This study has been undertaken by Professor Pete Tyler (Project Director, St Catharine’s College),

Ben Gardiner (Cambridge Econometrics), Jon Stenning (Cambridge Econometrics) and Dr Adam

Brown (Cambridge Econometrics). It has been guided by Richard Crabtree, Strategic Development

Manager at CEG.

Issue

10 March 2017

2

Contents

Executive Summary

1. The aims and scope of the study

2. The growth of the Leeds economy since 1990

3. The relative competitiveness of the Leeds economy

4. The potential for future growth, key constraints on growth and

the agenda for policy

Annexes

3

Executive Summary

The aims and scope of the study

Leeds has undergone an economic transformation in recent years, shaking off the legacy of industrial

decline and developing economic opportunities and thus jobs in new and growing sectors, most

notably in financial services. The economic future for Leeds looks brighter than it has for many years

but there is a shortage of evidence on what that future might hold and the key opportunities and

challenges that exist as Leeds moves to consolidate its position as the leading centre of economic

growth and vitality in the North of England.

To understand more about the growth of the Leeds economy this Report considers:

How the Leeds economy has performed in the period since 1990 compared to the UK;

How the pace of change has varied across different economic sectors in which the Leeds

economy tends to specialise;

How the relative competitiveness of the Leeds economy compares with that of other cities

with which it competes for investment, most notably Manchester and Birmingham, and the

possible impact of the Northern Powerhouse and HS2;

The potential for the growth in the Leeds City Region; and

The key policies/ investment initiatives that could help to unlock the growth potential and thus

underpin the growth of the Leeds economy, particularly as they relate to land use and skills.

The growth of the Leeds economy since 1990

Population growth in much of the North of England including Leeds was relatively weak

compared to the South until the turn of the century. However, since then the position has

strengthened considerably. In Leeds, Birmingham, Manchester and Sheffield there is now

quite rapid growth;

Leeds has demonstrated an ability to grow faster than other leading centres with which it is

often compared; most notably Manchester and Birmingham. However, its momentum has

varied, falling back somewhat in recent years;

The Leeds economy has undergone significant economic restructuring. It been successfully

repositioning from a past industrial base and begun to build its position as probably the

leading financial and business services centre after London. It also has seen growth in

education, health, IT services and other professional services.

4

The relative competiveness of the Leeds economy

The Leeds economy is restructuring away from its traditional manufacturing sectors and

increasingly towards Knowledge Intensive Business Services (KIBSs);

It has a particularly strong competitive advantage in Business Support Services, Finance and

Insurance, but it is also well-placed in a number of other mainly service related sectors;

Whilst its overall level of productivity is below that of the United Kingdom as a whole it is

relatively high compared to other cities in the Northern Powerhouse and only slightly below

that of Manchester;

Whilst the productivity levels of some of its key sectors continue to lag behind the UK, there

is evidence for relative improvement and it is essential that Leeds does all it can to enable its

core businesses to access the labour, premises and finance they require to grow;

The importance of investing in the skill base cannot be overestimated. But it is also

necessary to invest in new transport infrastructure that will allow more commuting and

business travel into the City from the surrounding region and from other cities in the North.

Improving connectivity requires substantial investment in new road and rail infrastructure

between the east and west in addition to the current proposals for HS2;

Leeds as a city has powerful knowledge-based assets and economic activity associated with

this will become an increasing part of what Leeds does. There is substantial investment in

the regional innovation system and strong collaboration and networking between the main

knowledge-based institutions. This is a strong and rapidly growing digital economy. The

increasing concentration of KIBS in the Leeds economy reinforces the importance of a good

access to quality floor-space in Leeds that will enable businesses to benefit from close

proximity to one another.

The increasing concentration of KIBS employment in the Leeds economy reinforces the

importance of a good access to quality floor-space in Leeds that will enable businesses to

benefit from close proximity to one another.

The potential for future growth, key constraints and the agenda for

policy

On the baseline forecast the Leeds economy will grow over the period 2015-2030 at a rate

that is 69% above that which it achieved in the period 2000-2015. However, building on

forecasts made for the Northern Powerhouse, and assuming some enhanced productivity

growth, GVA could grow substantially more, by some 140% on its historic performance.

Employment growth would also be substantially improved in relation to the historic position at

26% above.

The strength of the Leeds financial sector is such that it is entirely plausible that Leeds, and in

particular its expanding City Centre area, could experience growth in office-based

employment towards the top end of our growth forecasts. This would create 47,000 extra

office jobs in the City Centre over 2015-30 and a corresponding requirement for 7.5 million sq

ft of new floorspace. On the basis of historic provision this is likely to prove challenging,

pointing to some key messages for those involved in land use planning and development;

To ensure that the projected growth in jobs can be met it is essential that there is also an

adequate supply of skilled labour. At the present time future recruitment need is greatest in

the high skilled and services sectors.

5

1. The aims and scope of the study

Aims

1.1 Leeds has undergone an economic transformation in recent years shaking, off the

legacy of industrial decline and developing economic opportunities and thus jobs in new and

growing sectors, most notably in financial services. The economic future for Leeds looks

brighter than it has for many years but there is a shortage of evidence on what that

economic future might hold and the key opportunities and challenges that exist as Leeds

moves to consolidate its position as the leading centre of economic growth and vitality in the

North of England in the years ahead.

1.2 Clearly, the economic future of Leeds and that of the United Kingdom cannot be

known with certainty. The growth of Leeds and its surrounding region will depend on how

quickly the United Kingdom can grow and in turn the prospects for the global economy, and

how Leeds is able to adapt. It will also depend on the quality of the decisions taken by those

in both the public and private sectors in the environment in which the United Kingdom now

finds itself following the result of the EU membership referendum.

1.3 It is essential that businesses and the public sector in and around Leeds respond to

the new opportunities that will emerge. At the present time central government in the United

Kingdom is devolving more power to combined authorities and local government to manage

local economic development and the provision of core public services. Following the

decision to leave the European Union there is a strong chance that central government will

accelerate this process and Leeds has to be ready to respond to the opportunities and

challenges that arise.

1.4 It is possible to make informed judgements as to what might happen to the growth of

Leeds on the basis of different assumptions about the pace of national growth. The resulting

growth scenarios can be used to help develop an economic vision for Leeds to inform land

use policy in Leeds and its city region. Doing this has a number of advantages. Firstly, the

process requires us to consider how Leeds has grown relative to the UK economy in the

past and the factors that have led to differences between them. Secondly, the approach

enables the impact of different national and local policy scenarios on the growth of the city

and its region to be quantified in terms of output (GVA), employment and population.

Changes in these variables will influence the demand for commercial floorspace, housing

6

and the provision of public and private services.

1.5 To understand more about the growth of the Leeds economy this Report considers:

How the Leeds economy has performed in the period since 1990 compared to the

UK;

How the pace of change has varied across different economic sectors and the

sectors in which the Leeds economy tends to specialise;

How the relative competitiveness of the Leeds economy compares with that of other

cities with which it competes for investment, most notably Manchester and

Birmingham and the growth potential associated with the development of

interventions to unlock growth potential associated with the Northern Powerhouse,

including HS2, HS3 and other transport improvements, and skills initiatives;

The potential for the growth in the Leeds City Region; and

The key policies/ investment initiatives that could help to unlock the growth potential

and thus underpin the growth of the Leeds economy, particularly as they relate to

land use and skills.

Scope of the study

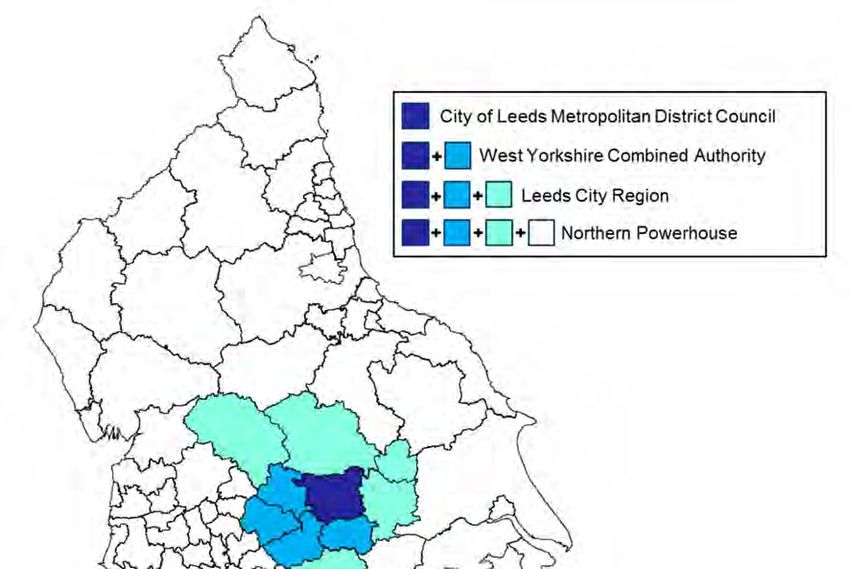

Geography

1.6 The city of Leeds can be defined in a number of different ways, based upon various

ways of considering the functional geography of the city. The narrowest definition of the city

is based upon the local authority district of Leeds, which covers the area for which the

metropolitan district council of the City of Leeds is responsible. This definition is also that

used by Centre for Cities in their Primary Urban Areas (PUA) analysis. With a similar (but not

identical) geographical footprint, the Travel to Work Area (TTWA) definition (calculated by

Newcastle University and the ONS and based upon census data that identifies those areas

where at least 50% of the working population both work and live in the same area) is only a

slight alteration. More radically different is the larger footprint covered by the West Yorkshire

Combined Authority (and which has agreed a devolution deal with the Government covering

skills, transport, housing and business support). The Combined Authority includes the

districts of Leeds, Bradford, Calderdale, Kirklees and Wakefield. A further (and even

broader) definition is that of the Leeds City Region (covering the area of operation of the

Leeds City Region Local Enterprise Partnership (LEP)), which includes all districts in the

Combined Authority plus Barnsley, Craven, Harrogate, Selby and York. The different scales

of these city definitions (in terms of area and total employment) are set out in Table 1.1 and

7

(except the TTWA) illustrated on the map below.

Table 1.1 Total employments in Leeds and associated geographies

Definition of Leeds Employment, 2015

City of Leeds Metropolitan district council / PUA 391,700

Leeds travel-to-work area 412,500

West Yorkshire Combined Authority 1,169,400

Leeds City Region LEP 1,435,200

Northern Powerhouse 7,787,100

Note: Geography as shown on Map 1 (except TTWA).

1.7 Leeds also sits within the area of the Northern Powerhouse. The area as a whole is

too broad to be the core area for the study, but it is necessary to place Leeds in the context

of the Northern Powerhouse (alongside comparison with other cities in the UK and beyond).

To do this the analysis has concentrated on the Leeds PUA, which also reflects the area

controlled by the City Council. The similarity between this definition and the travel-to-work

area shows that the majority of those commuting into Leeds also live within this area. The

table also highlights that a significant proportion of jobs in West Yorkshire are in Leeds

district (33%).

Methodology

1.8 The research has been undertaken in two stages. The first has involved an in-depth

analysis of how employment and output has changed on a sector by sector basis in Leeds

and its surrounding region relative to the United Kingdom as a whole since 1990. The

quantitative analysis has been undertaken using CE’s district data at a 45 sector level based

on ONS data. The data has been analysed to establish those sectors in which Leeds

appears to have something of a competitive advantage.

8

Map 1. Leeds and associated geographies

Source: CE

1.9 The second stage has involved forecasting what might happen to the growth of the

Leeds economy on the basis of different national assumptions. The national forecasts have

been taken from the CE national forecasting model and reflect different national and local

growth assumptions. A key objective has been to consider how the relative competitiveness

of the Leeds economy might affect its ability to attract investment. In the second stage of

analysis it has thus been possible to consider the potential for the Leeds economy if key

constraints are addressed to unlock the growth potential of the city, including the impact of

the policy initiatives associated with the Northern Powerhouse, delivery of HS2, and

associated improvements to the local and regional transport networks. This transformation

scenario is shared with the analysis underpinning the Northern Powerhouse Independent

Economic Review.

9

2. The growth of the Leeds economy since 1990

Population growth in much of the North of England including Leeds was relatively weak

compared to the South until the turn of the century. However, since then the position has

strengthened considerably. In Leeds, Birmingham, Manchester and Sheffield there is now

quite rapid growth;

Leeds has demonstrated an ability to grow faster than other leading centres with which it

is often compared; most notably Manchester and Birmingham. However, its momentum

has varied, falling back somewhat in recent years;

The Leeds economy has undergone significant economic restructuring. It been

successfully repositioning from a past industrial base and begun to build its position as

probably the leading financial and business services centre after London. It also has seen

growth in education, health, IT services and other professional services.

Introduction

2.1 This section examines how the Leeds economy has performed over the last twenty-

five years. It considers its growth in terms of Gross Value Added (GVA), employment,

population and GDP per head relative to the Yorkshire and Humber region as a whole and

the United Kingdom. Its performance is also considered relative to the Manchester and

Birmingham PUAs which are two cities with which it is frequently compared.

2.2 The section also assesses how the economic structure of the economy has changed,

seeking to identify those sectors which have either declined or expanded rapidly. It considers

whether the changes observed have been in line with that elsewhere.

Gross Value Added (Output)

2.3 Leeds grew relatively rapidly over the period 1971-2014. It has been in the top third of

British cities in terms of economic growth with a growth rate that has been quite close to that

of London and significantly higher than the other former industrial northern cities with which it

has traditionally been grouped (Figure 2.1). This reflects, in part, its particular strengths in

financial services but there have also been other factors that have meant it has been

performing somewhat better than many other British cities of similar size. However, analysis

presented in this Report shows that in recent years the relative growth performance of the

Leeds economy has been falling back somewhat compared to that of the United Kingdom as

a whole and in particular relative to that of Manchester, which is a city with which it is

frequently compared.

10Figure 2.1 Growth across British Cities (PUAs), 1971-2014

8.0

Average Annual Growth Rate (%pa) 7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

-1.0

Coventry

Hastings

Cambridge

Plymouth

Glasgow

Newcastle

Rochdale

Portsmouth

Southampton

Bolton

Brighton

Bournemouth

Swindon

Telford

Chatham

Birmingham

Middlesbrough

Oxford

Luton

Edinburgh

Doncaster

Swansea

Manchester

Nottingham

Wigan

Warrington

Huddersfield

Norwich

Leeds

Wakefield

Mansfield

Worthing

Northampton

Hull

Grimsby

Bristol

Gloucester

Ipswich

Aldershot

York

Reading

Milton Keynes

Liverpool

Derby

Crawley

Dundee

Burnley

Barnsley

Southend

Cardiff

Aberdeen

Blackpool

Sheffield

Preston

Newport

Bradford

Stoke

London

Sunderland

Peterborough

Birkenhead

Blackburn

Leicester

GVA Employment

2.4 Leeds experienced particularly rapid economic growth during the 1990s and

early 2000s; growing faster in terms of GVA than both the wider Yorkshire and

Humber Region and the UK as a whole. However, in the past decade Leeds has

grown more slowly than the UK average (Figure 2.2). Figure 2.3 shows how the

Leeds economy has grown relative to that of both Birmingham and Manchester. Over

the whole of the last twenty-five years, its economy grew at a faster rate than both

Manchester and Birmingham. However, in the last decade it has tended to grow

relatively more slowly than Manchester and at about the same rate as Birmingham.

11Figure 2.2. GVA Growth of Leeds between 1990 and 2015 shown in comparison to

the UK and the Yorkshire and Humber Region

2.00

1.80

1.60

GVA (1990 = 1)

1.40

1.20

1.00

0.80

1990 1995 2000 2005 2010 2015

UK Leeds Yorkshire and Humber

Source: CE

Figure 2.3. The growth of GVA in Leeds since 1990 compared to Birmingham and

Manchester

2

1.8

1.6

GVA (1990 = 1)

1.4

1.2

1

0.8

0.6

1990 1995 2000 2005 2010 2015

Manchester Birmingham Leeds

12Employment

2.5 Figure 2.4 examines how employment has changed in Leeds. Leeds outperformed the

UK as a whole between 1990 and 2005, but then fell back relatively in the last decade. It did,

however, outperform the Yorkshire and the Humber region as a whole over the 25-year

period.

Figure 2.4. Employment Growth of Leeds between 1990 and 2015 shown in

comparison to the UK and the Yorkshire and Humber Region

1.20

1.15

Employment (1990 = 1)

1.10

1.05

1.00

0.95

0.90

1990 1995 2000 2005 2010 2015

UK Leeds Yorkshire and Humber

2.6 The growth of employment in Leeds and Manchester over the last twenty-five years

has been fairly similar; both have grown by about 18% (Figure 2.5). Birmingham’s

employment declined quite severely up until 2010 when it has tended to recover somewhat

but still ended the period with less employment than it had in 1990. Manchester’s

performance was initially relatively weak compared to Leeds but has been performing

relatively more strongly in recent years.

13Figure 2.5. The growth of employment in Leeds since 1990 compared to

Birmingham and Manchester

1.2

1.15

1.1

1.05

Employment (1990 = 1)

1

0.95

0.9

0.85

0.8

0.75

0.7

1990 1995 2000 2005 2010 2015

Manchester Birmingham Leeds

Population

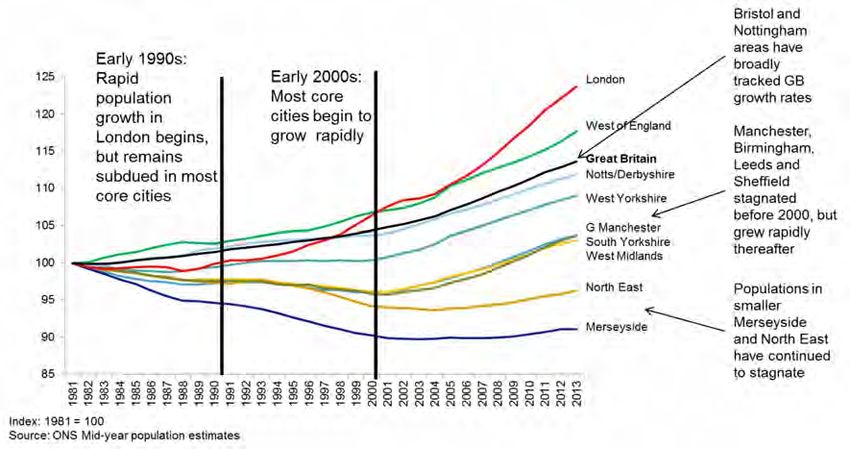

2.7 Population growth in the North of England was in general flat or declining up until

2000. This was quite different to that of the South of England. However, the position has

changed somewhat since then as Figure 2.6 shows. Since the turn of the century, the

population in Leeds, Manchester, Birmingham and Sheffield has begun to grow quite rapidly.

Figure 2.7 shows the population growth in Leeds, the wider region and the United Kingdom.

Leeds and its region began to experience rapid population growth from 2000 onwards.

Figure 2.8 compares population growth in Leeds with that of Birmingham and Manchester.

Over the last 25 years population has tended to grow at a somewhat faster rate in Leeds

than both Birmingham and Manchester. In fact, population actually declined in Birmingham

and in Manchester up until 2000, when it then turned around.

14Figure 2.6. Population Growth across Sub-Regions

Figure 2.7. Population Growth of Leeds between 1990 and 2015 shown in

comparison to the UK and the Yorkshire and Humber Region.

1.2

1.15

Index Population (1990 = 1)

1.1

1.05

1

0.95

0.9

1990 1995 2000 2005 2010 2014

UK Leeds Yorkshire and Humber

Source: CE

15Figure 2.8. The growth of population in Leeds since 1991 compared to Birmingham

and Manchester

1.1

1.08

1.06

Indexed Population (1990 - 1)

1.04

1.02

1

0.98

0.96

0.94

0.92

1990 1995 2000 2005 2010 2014

Manchester Birmingham Leeds

GDP per capita

2.8 Leeds currently has a GDP/capita that is higher than the national average reflecting

more favourable growth in the early part of the 2000s (Figure 2.9). It has a GDP per capita

that is substantially above the regional Yorkshire and Humber average.

Figure 2.9. GDP/capita of Leeds between 1990 and 2015 shown in comparison to

the UK and the Yorkshire and Humber Region

27.0

25.0

23.0

GDP/capita (£000)

21.0

19.0

17.0

15.0

13.0

11.0

9.0

7.0

1990 1995 2000 2005 2010 2015

UK Leeds Yorkshire and Humber

2.9 Leeds GDP/capita improved relative to its competitors between 1990 and 2005 (Figure

162.10) and still maintains a gap of about £3000 per person. Manchester and Birmingham

were in lockstep until 2005, since when Manchester has pulled ahead by approx. £2000 per

person as Birmingham was hit harder by the recession. However, this difference is partly

explained by the tighter spatial definition applied to Leeds PUA. Both Manchester and

Birmingham PUA cover a wider area and a larger population.

Figure 2.10. The growth of GDP per capita in Leeds since 1991 compared to

Birmingham and Manchester

27

25

23

21

19

GDP/capita

17

15

13

11

9

7

1990 1995 2000 2005 2010 2014

Manchester Birmingham Leeds

Sectoral growth

2.10 Figure 2.11 provides a decomposition of the Leeds economy into 6 macro-sectors for

the years 1990 and 2015. Whereas manufacturing output has fallen, this has been

outstripped by significant growth across the service sectors. Leeds has experienced rapid

growth in output from the service sectors over the past 25 years. The reduction in

manufacturing output has been more than offset by a substantial increase in economic

activity in its Knowledge Intensive Business Services (KIBS) and other private services,

although there was also an increase in the contribution of public services, which includes the

health and university sectors.

17Figure 2.11. GVA levels in six macro-sectors in Leeds; 1990-2015

7000

6000

5000

GVA (£000 , 2010 prices)

4000

3000

2000

1000

0

Primary Manufacturing Construction and KIBS Other Private Public Services

Utilities Services

1990 2015

2.11 Figure 2.12 compares the sectoral changes in Leeds with wider national trends. The

Leeds economy has largely followed the same growth pattern of the wider UK, with falls in

the contribution of Primary Industries and Manufacturing, and growth in the Services Sector

and particularly KIBS and Public Services.

Figure 2.12. % GVA growth between 1990-2015; six macro-sectors in Leeds and UK

250.00

200.00

GVA (% change, 1990 - 2015)

150.00

100.00

50.00

0.00

-50.00

-100.00

Primary Manufacturing Construction KIBS Other Private Public Services

and Utilities Services

UK Leeds

18Figures 2.13 and 2.14 identify the top 10 more finely disaggregated sectors that have

experienced particularly strong GVA and employment growth over the period. Seven sectors

appear in both growth charts. These are:

Financial and Insurance

Education

Business Support Services

Health

IT services

Other Professional Services

Legal and Accounting.

2.12 All of these are knowledge intensive service sectors, whether privately or publicly

funded. These seven sectors have clearly been the strongest drivers of both employment

and output growth over the time period.

2.13 It is also worth noting at this point that despite its considerable % growth, Head

Offices and Management Consultancies does not appear in the top 10 due to its low starting

point.

Figure 2.13. Top 10 GVA growth sectors in Leeds by total additional output

2000.0

1800.0

1600.0

GVA (£000, 2010 prices)

1400.0

1200.0

1000.0

800.0

600.0

400.0

200.0

0.0

1990 2015

19Figure 2.14. Top 10 Sectors for Employment Growth from 1990 to 2015

60.0

50.0

Employment (1000 jobs)

40.0

30.0

20.0

10.0

0.0

1990 2015

Figures 2.15 and 2.16 show the sectors that have experienced negative GVA and

Employment growth over the period 1990 to 2015. There are five manufacturing sectors that

appear in both lists: The fall in manufacturing employment in recent years reflects wider

trends within both the Leeds City Region and the wider UK.

Metals

Printing and Recording

Wood and Paper

Textiles

Other manufacturing and Repair

2.14 Other interesting points of note are the reduction in employment in retail trade

occurring simultaneously with a significant increase in GVA. This may represent a

rationalisation of the business model of the retail industry to be less labour intensive.

20Figure 2.15. Bottom 10 GVA negative-growth sectors in Leeds; total decrease in

output

400.0

350.0

GVA (£000, 2010 prices)

300.0

250.0

200.0

150.0

100.0

50.0

0.0

1990 2015

Figure 2.16. Bottom 10 Employment GVA negative-growth sectors in Leeds by total

decrease in workers

40.0

35.0

Employment (1000 jobs)

30.0

25.0

20.0

15.0

10.0

5.0

0.0

1990 2015

Note ‘PAD’ refers to Public Administration and Defence

Leeds sectors compared with Manchester and Birmingham

2.15 Figure 2.17 shows that Birmingham has strengths in Manufacturing and Public

Services, whereas Leeds tends to specialise more in KIBS. The Manchester economy sits

between the two.

21Figure 2.17. Comparison Sectors; Manchester, Birmingham and Leeds, 2015

35

30

% of employment , 2015

25

20

15

10

5

0

Manchester Birmingham Leeds

2.16 When looking at employment growth from 1990 to 2015, we see that Primary and

Manufacturing have tended to fall, Construction, Utilities, Wholesale, Retail and transport

have remained flat and Private and Public Services have shown growth. Leeds and

Manchester have both seen significant growth in the KIBS sector. Whereas Birmingham has

lost manufacturing jobs at a rate similar to that in Leeds, it hasn’t been as successful at

replacing them with jobs in the KIBS sector.

22Figure 2.18. Changes in Sectoral Composition; Manchester, Birmingham and Leeds

25 year % change in employment

100

80

60

40

20

0

-20

-40

-60

-80

-100

Manchester Birmingham Leeds

2.17 Looking at the KIBS sectors in more detail, Leeds has a greater concentration than

the other two PUAs in IT services, Finance and Insurance, Other Professional Services, and

Business Services, which is by far the biggest KIBS sector in each city. Manchester’s

strengths appear to lie in Media, Real Estate, Legal and Accounting, and Architectural

Services. Birmingham lags behind the other two cities in all KIBS sectors.

23Figure 2.19. Comparison of Manchester, Birmingham and Leeds KIBS employment,

2015

12

10

Axis % of total employment

8

6

4

2

0

Manchester Birmingham Leeds

2.18 Over the last twenty-five years the biggest % gains in employment growth in Leeds

have been in the Head Offices and Management Consultancies and Other Professional

Services. These are clearly the two subsectors that have been driving KIBS growth in the

area. Employment in both finance and business services increased by 15% between 2009

and 2014, although over the longer time period its growth was more modest; this suggests

that the competitiveness of the sector (relative to the UK and comparator cities such as

Manchester and Birmingham) has improved in recent years.

2.19 Employment growth in Leeds has thus been concentrated in the service sectors,

which accounted for 363,000 jobs in 2015 – 88% of total employment.

Conclusions

2.20 The evidence presented in this section shows that the Leeds economy has

undergone significant economic restructuring over the last 25 years. It has transitioned from

an industrial base and is now defending its position as the second leading centre of financial

and business services next to London. It has shown an ability to out-perform other leading

centres with which it is often compared; most notably Manchester and Birmingham.

However, throughout the period its relative growth has tended to vary quite considerably. If

Leeds is to maintain its forward momentum it is essential that it continues to enhance its

economic competitiveness and it is to the determinants of this that we now turn.

243. The relative competitiveness of the Leeds

economy

The Leeds economy is restructuring its economy away from its traditional manufacturing sectors

and increasingly towards Knowledge Intensive Business Services (KIBSs);

It has a particularly strong competitive advantage in Business Support Services, Finance and

Insurance, but it is also well-placed in a number of other mainly service related sectors;

Whilst its overall level of productivity is below that of the United Kingdom as a whole it is

relatively high compared to other cities in the Northern Powerhouse and only slightly below that

of Manchester;

Whilst the productivity levels of some of its key sectors continue to lag behind the UK, there is

evidence for relative improvement and it is essential that Leeds does all it can to enable its core

businesses to access the labour, premises and finance they require to grow;

The importance of investing in the skill base cannot be overestimated. But it is also necessary

to invest in new transport infrastructure that will allow more commuting and business travel into

the City from the surrounding region and from other cities in the North. Improving connectivity

requires substantial investment in new road and rail infrastructure between the east and west in

addition to the current proposals for HS2;

Leeds as a city has powerful knowledge-based assets and economic activity associated with

this will become an increasing part of what Leeds does. There is substantial investment in the

regional innovation system and strong collaboration and networking between the main

knowledge-based institutions. This is a strong and rapidly growing digital economy. The

increasing concentration of KIBS in the Leeds economy reinforces the importance of a good

access to quality floor-space in Leeds that will enable businesses to benefit from close proximity

to one another;

The increasing concentration of KIBS employment in the Leeds economy reinforces the

importance of a good access to quality floor-space in Leeds that will enable businesses to

benefit from close proximity to one another.

25Introduction

3.1 The previous section examined the growth of the Leeds economy over the last twenty-

five years. The evidence suggests that it has been one of the relatively faster growing

Northern cities, although the pace has varied throughout the period. An analysis by sector

points to it being able to expand its presence in financial services to overcome relative

decline in its traditional manufacturing base. The sectors that have shown fast or moderate

growth (> 0.5%pa) between 1990 and 2015 in Leeds are:

Business Support Services

Education

Health

Finance and Insurance

Residential and Social

Head Offices and Management Consultancies

IT Services

Other Professional Services

Legal and Accounting

Recreational Services

Warehousing and Postal

Architecture and Related

3.2 An interesting observation, is that all of these sectors, with the possible exception of

warehousing and postal, are in the “non-routine” occupation sectors, meaning that they are

the least likely to be affected by automation in the next 20-30 years. Future growth depends

on the relative competitiveness of Leeds as a location for investment and it is to examine the

determinants of this that this section now turns.

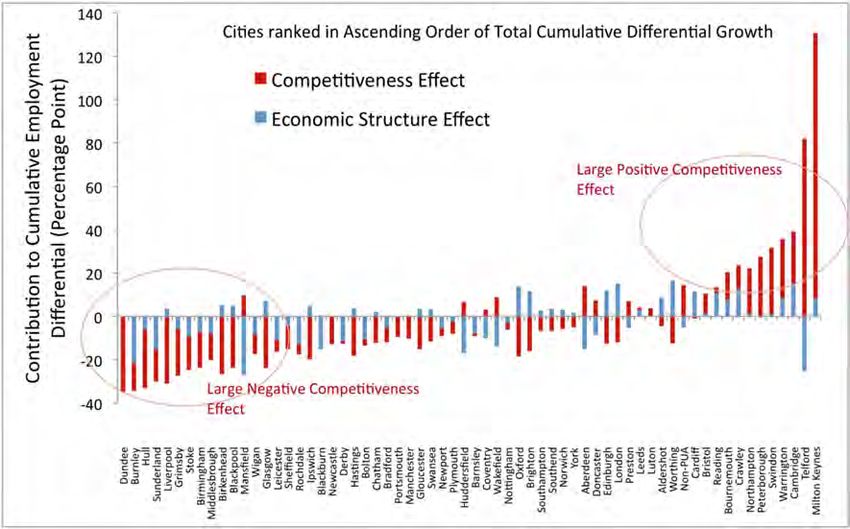

3.3 There are a number of different ways in which competiveness can be measured. The

findings from recent research by Martin, Gardiner and Tyler (2015) are shown in Figure 3.1.

This shows employment growth in the period across the British cities relative to the nation as

a whole. The difference between the national growth and that actually recorded by the city is

broken down into two components. The economic structure effect is the contribution to the

city’s growth that can be attributed to the difference in industrial structure as between the city

and the national economy; it reflects how far the city’s share of faster and slower growing

industries and activities differs from the nation as a whole, that is how far a region or city

specializes in more and less dynamic industries. The competitiveness effect is often

assumed to indicate the extent to which locally-unique factors have caused growth or decline

in a city’s industries: that is, it is assumed to point to some local competitive or comparative

advantage (or disadvantage). For this reason it is often referred to as the regional or city

‘competitiveness’ component, though it does not identify the causes of that competitive

advantage (or disadvantage). Martin, Tyler and Gardiner found that on the basis of this

measure of competitiveness Leeds was in the top one third of British cities.

26Figure. 3.1 The role of competiveness in the growth of employment across British

Cities, 1981-2013

Source: Martin, Gardiner and Tyler (2014)

3.4 Many factors have been identified as important determinants of urban

competitiveness. A relatively recent addition has been from the Economist Intelligence Unit-

“Hot Spots 2025: the Future Competitiveness of Cities”1. The emphasis is: ‘Competitiveness

is a holistic concept. While economic size and growth matter, several other factors determine

a city’s competitiveness, including its business and regulatory environment, its institutions,

the quality of human capital, cultural aspects and the quality of environmental governance.

These cities not only help a city sustain high economic growth, but also secure its future

competitiveness’ (Economists Intelligence Unit, 2013).

3.5 On this basis in its City Competiveness Index the Economist Intelligence Unit

benchmarked the competitiveness of 120 cities using 32 different indicators for each city.

The eight, distinct, thematic categories covered are economic strength (30%), Physical

capital (10%) and financial maturity (10%), institutional character (15%) and human capital

(15%), global appeal (`10%), social and cultural character (5%) and environmental and

natural hazards (5%).

3.6 One way to understand more about the relative competitiveness of the Leeds

economy is to adopt the pyramid approach shown in Figure 3.2.

1 Hot Spots 2025: benchmarking the Future Competitiveness of Cities.

27Figure. 3.2. The Pyramid Approach to Understanding the Determinants of City

Competitiveness

Source: Martin etc. adapted from Kitson, Martin and Tyler (2004)

3.7 Figure 3.2 shows that the economy of a city can increase its GDP per capita2 by

increasing their productivity, expanding their productive labour force (as indicated by its

employment rate) and the amount of wages and profits it can generate. The growth of

productivity in particular is affected by a number of factors including innovation, investment,

human capital, economic diversity/ specialization, the degree of connectivity and quality of

life and decision making. These, in turn, are influenced by the basic attributes of the city like

its business environment, its educational base, the quality of its physical infrastructure

including the degree of flexibility in its land and property markets, its socio-culture networks

and the quality of its institutional and governance structure.

3.8 Recently, an extensive body of research has been undertaken to examine the factors

responsible for the economic performance of the cities in the Northern Powerhouse3. This

research examined the relative contribution of the growth of productivity and the employment

rate to the growth of GDP per capita in the North of England.

Table 3.1 shows that although the contribution varied by sub-period, over the whole period

1992-2013 the most important factor contributing to the growth of GVA was the growth of

productivity.

2 It is necessary to consider the contribution made by Productivity (GDP/ Employee (sectoral hours worked), Total hours

worked / employment (Work-Leisure Trade off), The Employment Rate (Employment/ Working Age Population) and

Dependency Rate (Working Age Population/ Population).

3

Northern Powerhouse Independent Economic Review. Workstream 1: Analysis of the pan-Northern Performance Gap-Final

report. March 2016. Cambridge Econometrics and SQW.

28Table 3.1. The factors that contribute to growth in GVA per capita in the North of

England – average growth rate per annum (%)

1992/2013 1992/1997 1997/2009 2009/2013

GVA per capita 1.7 2.2 2.0 0.3

Productivity 1.5 1.7 1.6 1.0

Jobs per worker 0.0 0.4 0.0 -0.7

Employment 0.2 0.3 0.1 0.4

share

WAP share 0.0 -0.1 0.2 -0.5

Source: Northern Powerhouse Independent Economic Review, March 2016

How Leeds compares with other Northern Cities in relation to the

factors contributing to the growth of GVA per capita

3.9 Table 3.2 provides a detailed exposition by sub-region in the North of how the level of

productivity, the employment rate and the dependency rate (share of working age in total

population) varied. It should be emphasized that the analysis is for the Leeds City Region

taken as a whole (the LEP area). In 2004, GVA per capita was 7% above that of the North

as a whole. Its productivity was very close to the Northern average but its employment rate

was 3% higher and its dependency rate 3% lower than the North as a whole.

Table 3.2. Sub-Regional Performance Relative to the Northern Economy in 2004

GVA per capita Labour Employment rate Working-age

productivity share

Cheshire and 119 109 107 101

Warrington

Greater Manchester 107 102 99 102

Leeds City Region 107 101 103 103

Liverpool City Region 100 113 93 98

York, North Yorkshire 97 101 106 99

and East Riding

Cumbria 95 88 103 100

Humber 94 95 100 101

Lancashire 93 92 100 100

Tees Valley 91 93 95 101

North Eastern 90 99 95 99

Sheffield City Region 87 98 98 104

3.10 Table 3.3 shows how the key components that contribute to GVA performance

compare across the sub-regions of the Northern economy by 2013. The position of the

Leeds City Region had remained much the same as in 2004. However, it is noticeable that

the relative position of Greater Manchester has improved substantially. Table 3.4 shows that

Manchester has tended to increase its size relative to its city-region somewhat more quickly

than that of Leeds over the period 2010 to 2015 (just over 6% compared to 2.2%).

29Table 3.3. Sub-Regional Performance Relative to the Northern Economy in 2013

GVA per capita Labour Employment rate Working-age

productivity share

Cheshire and 118 101 111 100

Warrington

Greater Manchester 107 105 99 106

Leeds City Region 105 101 102 104

Liverpool City Region 102 113 94 102

York, North Yorkshire 97 100 109 100

and East Riding

Cumbria 104 92 109 95

Humber 91 97 104 99

Lancashire 91 91 100 99

Tees Valley 91 95 96 103

North Eastern 91 98 99 103

Sheffield City Region 88 93 101 99

Table 3.4. The growth of Leeds and Greater Manchester in relation to their

respective sub-regional economies 2010-2015

West Yorkshire Greater Manchester Leeds LAD Manchester LAD

(% City region) (% City region)

Employment 958,000 949,000 396,000 309,000

2010 (41.3) (32.5)

Employment 1,019,000 1,008,000 430,000 349,000

2015 (42.2) (34.6)

Growth in 61,000 59,000 34,000 40,000

Employment

% Growth in 6.4% 6.2% 8.6% 12.9%

Employment

3.11 Figure 3.3 picks up on the productivity issue further and shows how the level of

productivity in Leeds City (the PUA area in this case) compares with other cities across the

UK Great Britain in 2013 compared to 1981. It is encouraging that Leeds appears to have

been increasing its relative productivity over the last 25 years and at a slightly faster rate

than Manchester.

30Figure 3.3. How Productivity Varies across Cities, 1990 and 2014

140

Slough

Improving in Relative Productivity London

130

Productivity Level in 2014 (relative to GB = 100)

Milton Keynes

Swindon

120

110

100

Leeds

90 Birmingham

Manchester

Declining in Relative Productivity

Sheffield

York

80

70

70 80 90 100 110 120 130 140

Productivity Level in 1990 (relative to GB = 100)

3.12 However, as Figure 3.4 shows, it is important to recognise that Leeds has an overall

level of productivity that is still below that of the United Kingdom as a whole. The position for

the Yorkshire and Humber region is worse.

31Figure 3.4. Productivity of Leeds compared to UK and Yorkshire and Humber, 1990

to 2015

50.0

45.0

Productivity (£000 per worker)

40.0

35.0

30.0

25.0

1990 1995 2000 2005 2010 2015

UK Leeds Yorkshire and Humber

Growth in productivity by sector

3.13 Productivity growth in the largest sectors in Leeds (Figure 3.5) has not been

particularly strong (and in many cases slower than the UK average). This reflects the fact

that many of these sectors have seen substantial (and faster than UK) growth in employment

over the past 25 years, and more moderate increases in GVA. The IT and Financial and

Insurance sectors have seen some of the fastest growth.

3.14 Outside the top twenty largest sectors, GVA per employee in Textiles is above the

national average, reflecting a sector that has managed to achieve stronger growth in GVA

than employment (and, in more recent years, a more rapid decline in employment than

output).

32Figure 3.5 % Productivity Change in Leeds’ largest 20 sectors by employment

between 1990 and 2015

160.0

140.0

Productivity % Chnage (1990 to 2015)

120.0

100.0

80.0

60.0

40.0

20.0

0.0

-20.0

-40.0

The Drivers of productivity

3.15 The main drivers of productivity highlighted by HM Treasury4 are:

sectoral specialism;

skills;

connectivity;

agglomeration

knowledge and innovation;

governance.

3.16 In the rest of this Section we provide a brief review of what is known about the

relative strength of the Leeds economy in relation to the first five of these.

Sectoral specialisation

3.17 One way to assess the degree to which a city has a relatively greater concentration

of economic activity is through location quotients. Figure 3.6 shows employment location

quotients for Leeds in 2015. A Location Quotient of greater than one signifies that that sector

represents a larger proportion of employment within the Leeds economy than the total sector

4

HM Treasury (2006). Prosperity for All in the Global Economy-world Class Skills. Final Report of the Leitch Review of Skills,

TSO, London.

33employment within the total UK economy. When a local area has a relatively greater

concentration than the national average in a specific sector it can reflect that the area has

some form of competitive advantage in the sector, particularly if the sector is experiencing

relative growth over the study period examined.

3.18 Table 3.5 adds a further dimension by showing the location quotient by sector in

2015 alongside the growth of the sector over the period 1990-2015 in Leeds compared to

the UK. It can be seen that there was particularly rapid economic growth in business support

services, education, head office and management consultancies in Leeds, which were all

sectors in which Leeds had a relatively greater concentration by 2015 compared to the UK.

3.19 The main sectors in which Leeds appears to have a relatively higher concentration

than the national average are:

Electricity and gas;

Electrical equipment;

Air transport;

Printing and recording;

Financial and insurance;

Wood and paper;

Other professional services;

Legal and accounting;

Business output services.

Table 3.5. Leeds sectoral analysis; An analysis of the sectoral composition of

employment in Leeds is shown below

Sector Leeds LAD Growth, % pa, UK Growth % Location

Employment 1990-2015 pa, 1990 2015 Quotient, 2015

2015

Business support services 48,700 2.39 0.41 1.29

Education 44,000 3.30 1.55 1.11

Retail trade 34,000 -0.44 2.54 0.84

Health 30,700 1.49 2.20 0.96

Construction 23,800 -0.42 -0.29 0.83

Financial & insurance 22,100 0.98 1.62 1.44

Residential & social 21,500 1.27 1.15 0.88

Public administration and

21,500 -0.80 -0.75 1.09

defence (PAD)

Wholesale trade 18,900 -0.84 0.11 1.10

Food & beverage services 18,900 -0.45 -0.14 0.80

Head offices & management

14,900 9.94 2.56 1.17

consultancies

IT services 14,300 1.93 0.92 1.08

Other professional services 12,600 6.20 5.81 1.32

Legal & accounting 12,500 2.24 1.71 1.30

34Sector Leeds LAD Growth, % pa, UK Growth % Location

Employment 1990-2015 pa, 1990 2015 Quotient, 2015

2015

Recreational services 10,300 2.59 1.67 1.19

Warehousing & postal 9,400 1.45 2.13 0.87

Other services 9,300 -0.90 -0.35 0.72

Architectural & related 8,500 0.89 1.58 0.97

Land transport 8,400 -0.68 2.08 0.92

Motor vehicles trade 8,100 0.10 -0.66 1.04

Note: Only the top 20 sectors (with employment > 8,000 employees) are shown.

3.20 Figure 3.7 adds a further dimension to the analysis by considering if the sectors that

are relatively specialised in the Leeds economy have been increasing their relative share

over the period 1971-2014. It appears that the sectors in which Leeds has been increasing

its relative degree of specialism are Business Support Services, Education, Health, Finance

and Insurance and the Residential and Social sector. This suggests that the City has

strength across a wide range of office-based activities.

3.21 The analysis is extended further to add an analysis of how the Manchester economy

has performed to enable comparison (Figure 3.8). It is interesting to note that Manchester

like Leeds has been increasing its degree of specialisation in Business Support Services,

education, health and the Residential and Social sector.

35Figure 3.6 Leeds LAD Location Quotient (Employment)

0.00 0.50 1.00 1.50 2.00 2.50 3.00

Electricity & gas

Electrical equipment

Air transport

Printing & recording

Financial & insurance

Wood & paper

Other professional servi

Legal & accounting

Business support service

Recreational services

Machinery, etc

Head offices & manag co

Chemicals, etc

Education

Wholesale trade

PAD

IT services

Coke & petroleum

Other manuf. & repair

Motor vehicles trade

Architectural & related

Arts

Real estate

Health

Land transport

Textiles etc

Metals

Residential & social

Warehousing & postal

Retail trade

Construction

Food & beverage services

Water, sewerage & waste

Non-metallic

Other services

Accomodation

Food, drink & tobacco

Pharmaceuticals

Media

Agriculture etc

Mining & quarrying

Computers, etc

Motor vehicles, etc

Water transport

Other trans. equipment

2015 1990

36Figure 3.7. Sectoral concentration of employment in the Leeds economy in relation

to growth over the period 1971-2014.

Leeds: Employment Change x Share

8

Business Support Services

Education

6

Change in Employment Share (pp), 1971-2014

Finance & Health

4

Insurance

2 Residential & Social

0

0 2 4 6 Retail 8 10 12

-2

-4 Wholesale

-6

-8

-10

-12

Employment Share (2014)

Figure 3.8. Sectoral concentration of employment in the Manchester economy in

relation to growth over the period 1971-2014.

Manchester: Employment Change x Share

8

Business Support Services

6

Change in Employment Share (pp), 1971-2014

Health

4

Education

Residential & Social

2

Construction

0

0 2 4 6 8 10

Retail

-2

PAD

-4

-6

-8

-10

-12

Employment Share (2014)

373.22 It is clear from the evidence that the Leeds economy is increasing its relative

presence in KIBS and its ability to do this reflects its relative strength in this key area of

economic activity. Because of the importance of this sector in the Leeds economy an

analysis was undertaken to assess how productivity in this sector in Leeds compared with

other British cities with which it is competing for investment. Figure 3.9 shows that

productivity in this sector in Leeds has been increasing since 1990. Moreover, Leeds has a

higher level of productivity than cities like Manchester, Sheffield and Birmingham and

appears to be moving away from them to some degree.

Figure 3.9. Changes in Productivity in the Knowledge Intensive Business Services

sector across British Cities 1990-2014.

London

KIBS Productivity Level in 2014 (relative to GB = 100)

140

Improving in Relative Productivity

130

Slough

120

Milton Keynes

110

100

Swindon

90

Leeds

Birmingham

80 Manchester

York Declining in Relative Productivity

Sheffield

70

60

60 80 100 120 140

KIBS Productivity Level in 1990 (relative to GB = 100)

Skills

3.23 The ability of the Leeds economy to increase its productivity and grow is strongly

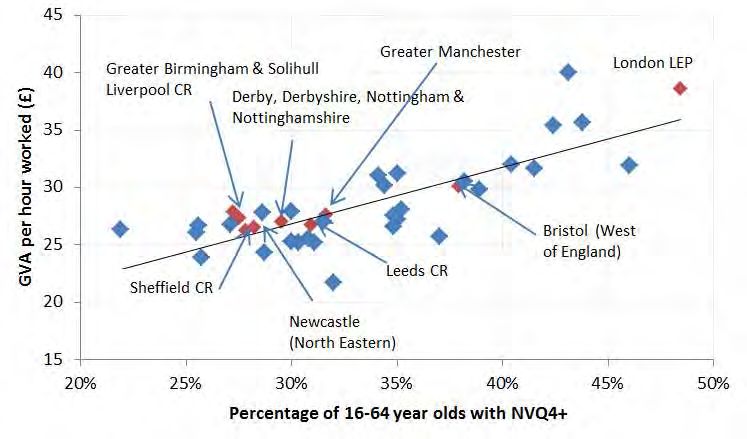

influenced by its ability to obtain skilled labour. Figure 3.10 shows the relationship between

skills (as proxied by the percentage of the areas workforce with NVQ4+) and the level of

productivity (as proxied by GVA per hour worked) for English Local Enterprise Partnerships.

There is a fairly positive relationship between the two variables as would be expected. Leeds

is bunched close to Manchester in its relative position and better placed than cities like

Sheffield and Liverpool. However, most Northern cities have a skill deficit compared to their

38Southern counterparts. The cities with the highest levels of productivity have the highest

proportion of better skilled workers and it is thus essential that Leeds seeks to increase the

level of skills in its workforce as it moves forward.

Figure 3.10. The relationship between GVA per hour worked and levels of skill in

English Local Enterprise Partnership areas.

Source: BIS (2015).

Agglomeration

3.24 In recent years there has been much attention given to the role of agglomeration as a

factor that enhances the economic competitiveness of cities. The argument is that the

spatial concentration of people and firms in cities leads to positive externalities that

provide increasing returns and thus falling average costs to the businesses located

there. Three main sources of the types of externalities are identified. These are ‘’input

externalities’ whereby there is a concentration of companies that produce specialised

services and products, lower transport costs and procurement economies. The second

embrace labour market externalities that arise from the geographic concentration of

workers with specialised skills of relevance to an industry. The third relate to knowledge

externalities that reflect the benefits of close proximity in sharing and exchanging

knowledge of relevance to an industry’. (BIS. 2009) 5.The benefits of agglomeration are

particularly strong for the financial services sector. Some idea of the relative size of the

potential agglomeration benefits available to Leeds compared to other cities in the North

of England can be gauged by considering Figure 3.11. This shows that Leeds City has

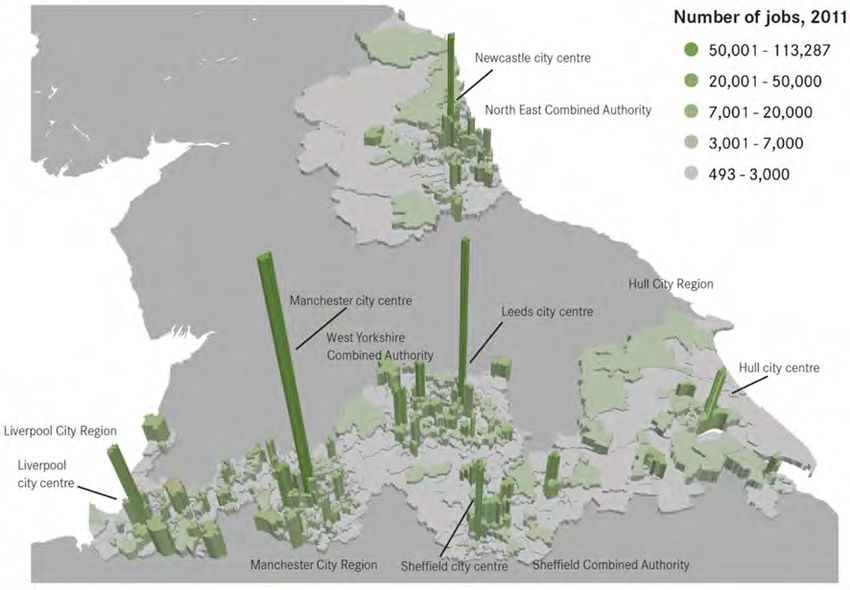

the second highest concentration of jobs in the North next to Manchester. Figure 3.12

5 BIS Occasional Paper No 1. Research to improve the assessment of additionality. October 2009.

39shows that private business services sector (KIBS, Real Estate and Business Support

Services) tends to dominate the demand for city centre office space and it is highly

concentrated in two centres in Manchester and Leeds having over 100,000 employees.

This reinforces the increasing agglomeration benefits to KIBS employers of locating in

Leeds City Centre.

3.25 Leeds is thus well positioned to continue to exploit its substantial agglomeration

benefits as they relate to the KIBS that are becoming an increasing part of its economic

landscape. It is thus very important for Leeds that it ensures that there is a strong supply

of high quality of offices in and around its centre core.6

Figure 3.11. Distribution of jobs across and within the cities of the North of England

(Source: Centre for Cities, 2015)

6Recent research undertaken by the Centre for Cities shows that jobs growth, and particularly in

KIBS, is concentrating in Leeds City Centre ( http://www.centreforcities.org/publication/leeds-city-

centre/ ).

40Figure 3.12. The concentration of the private business services sector (KIBS, Real

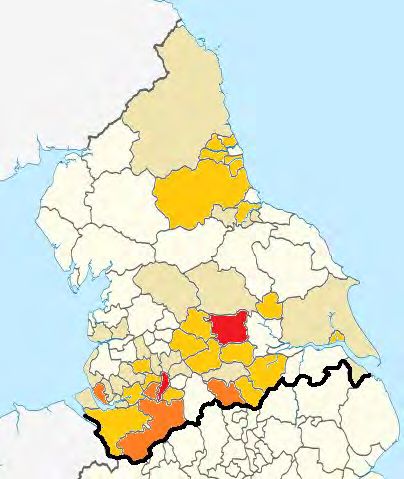

Estate and Business Support Services) in the North of England.

Total Employment

The importance of connectivity

3.26 In recent years HM Treasury has been highlighting the need to increase the degree

of connectivity between northern cities. They argue that better connectivity would be good

for the labour market in the North since it would allow KIBS employers in cities like Leeds to

realise the benefits of agglomeration whilst enabling some part of their workforce to

commute from their homes elsewhere in the city-region. Businesses in the North could

obtain labour from a wider labour pool, in the way that businesses in London are able to do

because of very good rail infrastructure to surrounding cities in the South East of England. At

the present time connectivity is relatively poor and there are very weak levels of commuting

flow between cities in the North. HM Treasury comments: ‘it is currently quicker to travel the

283 miles from London to Paris by train than it is to travel less than half that distance

between the two Northern cities of Liverpool and Hull’7. The British Treasury stated that

increased connectivity would enable more trade to occur and enable businesses to interact

and collaborate more effectively. Figure 3.13 shows recent evidence assembled by HS2

that illustrates just how disadvantaged the cities are on the basis of rail connections. There is

much evidence to reinforce the view that the motorway system is also heavily compromised

and for Leeds a key area remains the need for it to increase its relative connectivity to the

East, West and North of England. HS2 clearly offers major opportunities with respect to the

7 HM Treasury (2015). Fixing the Foundations: Creating a More Prosperous Nation. Cm 9098.

41South of England although even here there is an urgent need for more research and insight

into how even investment in this major infrastructure project can be developed so as to

maximise the economic benefits for Leeds and other northern cities.

Figure 3.13. East West and North South Connectivity in the United Kingdom.

Source: Rebalancing Britain, HS2, 2014

Enhancing the knowledge and innovation system

3.27 An increasingly important factor in the growth of cities is their ability to develop their

knowledge-based assets including their universities and major research institutions. Leeds

and the other major cities in the North have extensive knowledge-based assets. Recognising

the significant benefits that arise from collaboration and interaction across their regional

innovation system the universities have formed the N8 Research Partnership which is a

‘collaboration of the eight most research intensive universities in the North of England:

Durham, Lancaster, Leeds, Liverpool, Manchester, Newcastle, Sheffield and York. Working

with industry, N8 aims to maximise the impact of this research base by identifying and

coordinating powerful research collaborations across the North of England and beyond’

(http://www.n8research.org.uk/). The N8 universities have an extensive combined research

capability and argue that they ‘represent a significant cluster of research power among the

130 universities in the UK’. Their website shows that they have almost 15,000 academic

staff–12% of UK total, over 38,000 postgraduate students–11% of UK total (taught and

research) and a total research income in 2010/11 of £747m–17% of UK total. They received

42almost £500m of Government research funding-18% of UK total, £72m of UK industrial

research funding–16% of UK total and £120m from overseas research partners. All eight

universities are in the top 1% of institutions in the world.

3.28 The importance to Leeds of developing its knowledge based assets and the

enterprise associated with it cannot be overemphasised. If it is to be successful in this

respect then it will have to re-orientate its land uses, resource bases and institutions

accordingly (Tyler, 2015). Recent support by HM Government to technology incubators in

Leeds is reflective of the investment that has to be attracted.

3.29 It should also be mentioned that Leeds has performed well in recent years in

developing its presence in the digital economy as the growth of the Leeds Digital Festival

illustrates. In 2016 over 6,000 people attended 56 events across 28 venues featuring over

175 speakers; over 10,000 attendees are expected in 2017. The local authority in

partnership with business, universities and education providers has developed a Leeds

Digital Skills Action Plan8.

Conclusion

3.30 The Leeds economy has been restructuring its economy away from its traditional

manufacturing sectors and increasingly towards KIBS. It has a particular strong competitive

advantage in Business Support Services, Finance and Insurance where it is now probably

the second leading centre of such activity in England. However, it is also well-placed in a

number of other mainly service-related sectors like tourism, retail and leisure. Continued

growth in these sectors will provide jobs for those who may have lower skill levels than KIBS

workers and may be having difficulties in finding employment elsewhere in Leeds.

3.31 The ability of the Leeds economy to continue to attract new investment in KIBS

sectors depends increasingly on the strength of its offer compared to cities like Manchester

and Birmingham with which it competes for this type of activity. Whilst its overall productivity

levels are behind that of the United Kingdom it is relatively high compared to other cities in

the Northern Powerhouse and only slightly below that of Manchester.

3.32 Whilst the productivity levels of some of its key sectors continue to lag behind the

UK, there is evidence for relative improvement and it is essential that Leeds does all it can to

enable its core businesses to access the labour, premises and finance they require to grow.

3.33 The importance of investing in the skill base cannot be overestimated. But it is also

necessary to invest in new transport infrastructure that will allow more commuting into the

City from the surrounding region and from other cities in the North. Improving connectivity

requires substantial investment in new road and rail infrastructure between the east and

west in addition to the south as envisaged in the current proposals for HS2.

8 see: http://www.leeds.gov.uk/docs/The%20Leeds%20Digital%20Skills%20Action%20Plan.pdf

43You can also read