The international role of the euro - SUERF webinar 14 June 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The international

role of the euro

SUERF webinar

Hans-Joachim Klöckers and Arnaud Mehl

14 June 2021

The views expressed here are those of the authors and do not necessarily represent those of the ECB or the Eurosystem

w ww.ecb.europa.eu ©

Outline

1. Key developments in the international role of the euro in 2020

2. Special features

A. EU and ECB policy responses to the pandemic and the euro’s global role

B. Central bank digital currency and global currencies

C. The euro as an invoicing currency for global trade

3. Conclusions

2 w ww.ecb.europa.eu ©The role of the euro remained broadly stable at a low level in 2020

Composite index of the international role of the euro

(percentages; at current and constant Q4 2020 exchange rates; four-quarter moving averages)

Constant exchange rates

Current exchange rates

24

23

22

21

20

19

18

17

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Sources: BIS, IMF, CLS Bank International, Ilzetzki, Reinhart and Rogoff (2019) and ECB calculations.

Notes: Arithmetic average of the shares of the euro at constant (current) exchange rates in stocks of international bonds, loans by banks outside the euro area to borrowers outside the euro area, deposits with banks

outside the euro area f rom creditors outside the euro area, global foreign exchange settlements, global foreign exchange reserves and global exchange rate regimes. Data at constant exchange rates are not available

f or global f oreign exchange settlements. The estimates for the share of the euro in global exchange rate regimes from 2016 onwards were obtained by ECB staff using the same methodology as Ilzetzki, E., Reinhart,

C. and Rogoff, K. “Exchange Arrangements Entering the 21st Century: which anchor will hold?”, Quarterly Journal of Economics, Vol. 134(2), 2019, pp. 599 646, complemented with ECB staff judgement. The latest

observ ations are for the fourth quarter of 2020.

3 w ww.ecb.europa.eu ©The euro remains the second most important currency globally

Snapshot of the international monetary system

(percentages)

US dollar Japanese yen

Euro Chinese renminbi

70

60

50

40

30

20

10

0

Foreign exchange International debt International loans Foreign exchange Global payment

reserves turnover currency (SWIFT)

Sources: BIS, IMF, SWIFT and ECB calculations.

Note: The latest data for foreign exchange reserves, international debt and loans are for the fourth quarter of 2020. Foreign exchange turnover data as of April 2019. SWIFT data as of December 2020.

4 w ww.ecb.europa.eu ©The US dollar punches above the US global economic weight

Global currency status vs. share in global GDP Global currency status vs. share in global exports

(percentages) (percentages)

30 30

25 25

Share of global GDP (PPP, %)

Share of glob al exports of goods

20 Chi nese 20

renmi nbi US dol lar Euro

and services (%)

Chinese

15 15renminbi

Euro

US dollar

10 10

Ja pa nese yen Japanese yen

5 5

0 0

0 10 20 30 40 50 60 0 10 20 30 40 50 60

Composite index of global currency status (%) Composite index of glob al currency status (%)

Sources: BIS, IMF, SWIFT and ECB calculations.

Note: The latest data for foreign exchange reserves, international debt and loans are for the fourth quarter of 2020. Foreign exchange turnover data as of April 2019. SWIFT data as of December 2020. The 45-degree

line is indicated as a red dashed line.

5 w ww.ecb.europa.eu ©The pandemic affected some indicators of the euro’s global appeal to

different degrees

Evolution of selected indicators of the euro’s international role in 2020 Euro exchange rates in 2020

(Q4 2020 – Q4 2019 changes, percentages, at constant Q4 2020 exchange rates) (end-2020 – end-2019, percentages)

10

1

8

0

6

-1

4

-2

2

-3

0

-4

EUR NEER-42 EUR/USD

International Foreign currency Foreign exchange International debt International loans Invoicing of euro

deposits debt issuance reserves securities area goods imports Source: ECB.

Notes: EUR NEER-42 refers to the nominal effective exchange rate of

the euro v is-à-vis the currencies of 42 major trading partners. An

Sources: ECB, BIS, IMF, national sources and ECB staff calculations. increase indicates an appreciation of the euro.

6 w ww.ecb.europa.eu ©The “dash for cash” that accompanied the pandemic also benefited the US

dollar as an international deposit currency

Currency composition of outstanding amounts of international deposits

(percentages, at constant Q4 2020 exchange rates)

Euro US dollar Yen Other

80

70

60

50

40

30

20

10

0

1999 2002 2005 2008 2011 2014 2017 2020

Sources: BIS and ECB calculations.

Notes: The latest observations are for the fourth quarter of 2020. International deposits are defined as deposits with banks outside the currency area from creditors outside the currency area

7 w ww.ecb.europa.eu ©Strong issuance of US dollar bonds by emerging markets led to a decline in

the share of the euro in foreign currency bond issuance

Currency composition of foreign currency- Regional breakdown of US dollar-denominated

denominated bond issuance international bond issuance

(percentages) (USD billions)

Euro area

Euro US dollar Other Japan

Other advanced economies

Emerging market economies

80% Non-euro area EU

700

600

60%

500

40% 400

300

20% 200

100

0%

0

1999 2002 2005 2008 2011 2014 2017 2020 1999 2002 2005 2008 2011 2014 2017 2020

Sources: Dealogic and ECB calculations. Sources: Dealogic and ECB calculations.

Note: The latest observations are for end-2020. Note: The latest observations are for the fourth quarter of 2020.

8 w ww.ecb.europa.eu ©The share of the euro in global foreign exchange reserves declined slightly in

2020 and that of the US dollar stands at a two-decade low

Evolution of the share of selected currencies in Average interest rates for major reserve

global foreign exchange reserves currencies in 2020

(percentages; at constant Q4 2020 exchange rates) (percentages)

Euro (right-hand scale)

5-year government bond yield 1-month deposit rate

US dollar (left-hand scale)

Other currencies (right-hand scale) 0.75

74 28

72 26

0.50

70 24

68 22 0.25

66 20

0.00

64 18

62 16

-0.25

60 14

58 12 -0.50

56 10

54 8 -0.75

1999 2002 2005 2008 2011 2014 2017 2020 EUR JPY GBP AUD USD CAD

Sources: Haver Analytics, Refinitiv Datastream and ECB staff calculations. Note: the 5-year government

Sources: IMF and ECB calculations. y ield f or the euro area is calculated as a debt-weighted average of 5-year euro area yields of sovereigns

Note: The latest observations are for the fourth quarter of 2020. with at least an AA credit rating according to Standard and Poor’s.

9 w ww.ecb.europa.eu ©The euro remained a key currency in international green bond markets

Currency breakdown of “global” issuance Currency breakdown of “international” issuance

of green bonds (all issuers worldwide) of green bonds (only non-national issuers)

(percentages) (percentages)

EUR EUR: Non-euro area nationality

USD USD: Non-US nationality

Other Other: Foreign nationality

100% 100%

90% 90%

80% 80%

70% 70%

60% 60%

50% 50%

40% 40%

30% 30%

20% 20%

10% 10%

0% 0%

2013 2014 2015 2016 2017 2018 2019 2020 2013 2014 2015 2016 2017 2018 2019 2020

Sources: Dealogic and ECB calculations. Source: Dealogic and ECB calculations.

Note: Bonds issued by all issuers, irrespective of their nationality or residence. The latest observations are Note: Bonds issued by non-national issuers. The latest observations are for 31 December 2020.

f or 31 December 2020.

10 w ww.ecb.europa.eu ©Summary Part 1

• Broad stability in the international role of the euro after the pandemic shock.

• This compares favourably to the developments after the GFC, reflecting a forceful

joint policy response in the EU this time

• Average share of the euro across various indicators remaining historically

relatively low, well below pre-Lehmann peaks

• Global trend towards reserve currency diversification continuing

• Euro has potential to strengthen its international role in green bond markets

11 w ww.ecb.europa.eu ©2. Special features

A. EU and ECB policy responses to the pandemic and the euro’s global

role

B. Central bank digital currency and global currencies

C. The euro as an invoicing currency for global trade

12 w ww.ecb.europa.eu ©EU bonds issuance under SURE well received by non-euro area investors

Geographical distribution of investors for SURE bonds issued in 2020

different EU bonds issued in 2020 Investor distribution at the time of allocation

(percentages)

Non-EA investors EA investors Of which domestic investors

Central banks

Maturity Value Insurance and Other asset Non-euro area

and official

Germany (Bund 15Y) (years) (€bn) pension funds managers inv estors

institutions

ESM (ESM bond 10Y)

5 8 30% 5% 65% 60%

France (OAT 20Y)

COM (SURE bond 10Y) 10 10 37% 6% 57% 49%

COM (SURE bond 15Y)

15 8.5 15% 14% 71% 45%

Italy (BTP 15Y)

20 7 13% 13% 74% 31%

COM (SURE bond 20Y)

30 6 15% 23% 62% 35%

0% 20% 40% 60% 80% 100%

Sources: ECB staff calculations based on data released by the European Commission (COM), the Source: ECB staff calculations based on data released by EU and national authorities. Data refers to

European Stability Mechanism (ESM) and national authorities. distribution at the time of the first allocation of SURE bonds. “Other asset managers” includes the following

Notes: data refers to the distribution at the time of first allocation of bonds. categories: fund managers, bank treasures, banks, hedge funds, others.

13 w ww.ecb.europa.eu ©NGEU first step towards an European safe asset but unlikely to change the

global status of the euro

Amount outstanding of general government Market capitalisation of Bloomberg Barclays

debt securities Global Aggregate Aaa Index

(USD trillions) (percentage of world GDP)

25

20

NGEU +

15 SURE

(Aaa)

Aaa

10 Aaa

Aa

5 A1

A1

A to

Aa3

Ba

0

US

UK

Japan

Euro area

China

Sources: BIS, Haver Analytics, Bloomberg, European Commission and ECB calculations.

Notes: The data refer to total debt securities issued by the general government. Planned issuance for NGEU. Sources: Bloomberg, IMF and ECB staff calculations.

Latest Moody ’s local currency long-term sovereign debt rating. The observations are for the third quarter of 2020 Notes: The Bloomberg Barclays Global Aggregate - Aaa Index is a measure of Aaa index rated debt

f or the amount outstanding of debt securities and for 2 March 2021 for credit ratings. including treasury, government-related, corporate and securitized fixed-rate bonds.

14 w ww.ecb.europa.eu ©The ECB´s monetary policy measures in response to the pandemic have

been swift and forceful and helped stabilise the euro area economy

• Launch of the pandemic emergency purchase programme (PEPP) in March

2020:

Initial envelope increased from €750 billion to €1,850 billion in December 2020.

• Expansion of longer-term liquidity refinancing operations (TLTRO III):

– Volume of outstanding take-up reached €2 trillion in May 2021

– Measures to increase attractiveness of TLTRO III

Lending interest rate reduced to up to -1%.

Increase in the borrowing allowance

Expansion of the range of eligible collateral

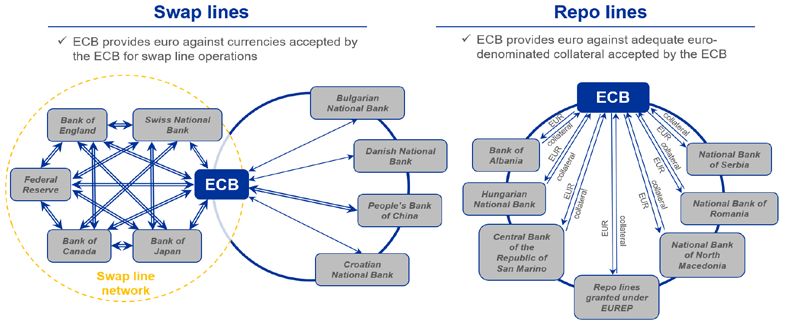

15 w ww.ecb.europa.eu ©Providing euro liquidity internationally through liquidity lines contributed to

forestall the pandemic’s potential adverse implications on the euro area

Estimated impact of ECB liquidity lines on

Eurosystem framework for providing euro funding cost of recipients (currency basis)

liquidity to other central banks (basis points)

0

-5

-10

-15

-20

-25

Announcement day 1 week after 2 weeks after

Source: ECB.

Note: Under the swap line arrangements, the ECB provides euro liquidity against currencies accepted

by the ECB for swap line operations. Under the repo line arrangements, the ECB provides euro liquidity

Sources: ECB calculations.

against adequate euro-denominated collateral accepted by the ECB. EUREP is the Eurosystem repo

Notes: The chart shows estimates from an event study of the effect of the liquidity lines obtained in 2020 by

f acility for central banks. The countries mentioned in the overview of the Eurosystem’s repo line

Bulgaria, Croatia, Denmark, Hungary and Romania on their corresponding currency basis, controlling for fixed

arrangements are only examples to illustrate the functioning of these types of agreements. A double

ef f ects, month effects and the VIX index. The estimates are obtained on daily data over the period 2010-2020.

line in the swap lines ov erview indicates that the agreement is reciprocal.

16 w ww.ecb.europa.eu ©2. Special features

A. EU and ECB policy responses to the pandemic and the euro’s global role

B. Central bank digital currency and global currencies

C. The euro as an invoicing currency for global trade

17 w ww.ecb.europa.eu ©Central bank digital currency supports use of a currency in cross-border

payments, depending on its design

• Issuing a digital euro may become important if foreign digital money (foreign

CBDC or stablecoins) largely displaced existing means of payments in the

euro area.

• A digital euro will mainly serve domestic payment purposes. But it could

also reduce frictions and costs of euro-denominated cross-border payments

and thereby support the euro’s global role.

• Features specific to digital means of payment could ease international

adoption of a central bank digital currency:

Safety, low transaction costs, bundling effects and programmability, potential

feedback loops in use as means of payment and store of value.

• Design choices matter for the global outreach of a central bank digital

currency:

Interoperability, restrictions on non-resident holdings, remuneration.

18 w ww.ecb.europa.eu ©CBDC supports global use of a currency but not necessarily a game changer

Model simulations on the impact of CBDC for international currency use

(Currency breakdown of global export payments in alternative simulations, percentages)

Currency 1

Other currencies

100

90

80

70

60

50

40

30

20

10

0

Baseline without CBDC Baseline with CBDC

Source: ECB calculations.

Notes: The lef t panel shows simulations based on a three-country DSGE model in the spirit of Eichenbaum et al. (2020) with no capital controls, a 1% liquidation cost for debt securities, symmetric 33%-weights for all

countries and the same volatility of the exogenous shocks in both simulations.

19 w ww.ecb.europa.eu ©2. Special features

A. EU and ECB policy responses to the pandemic and the euro’s global role

B. Central bank digital currency and global currencies

C. The euro as an invoicing currency for global trade

20 w ww.ecb.europa.eu ©The US dollar is a globally dominant invoicing currency while the euro is a

regionally dominant currency in Europe and some parts of Africa

Trade and invoicing currency shares at the country level: US dollar vs. euro

(percentages)

100 100

Serbia

Montenegro

West Af rican

80 80 f ranc zone

EUR export inv oicing share

USD export inv oicing share

Moldov a

60 60

40 40

20 20

Russia

Kazakkstan

Algeria

Azerbaijan

0 0

0 20 40 60 80 100 0 20 40 60 80 100

Export share accounted for by the United States Export share accounted for by the euro area

Source: Boz et al. (2020).

Notes: The chart presents scatter plots of the share of countries' total exports accounted for by the United States and the share of total exports invoiced in US dollars (left panel), as well as the share of total exports

accounted for by the euro area and the share of total exports invoiced in euro (right panel). The 45-degree line is shown as a black dashed line.

21 w ww.ecb.europa.eu ©3. Conclusions

• Broad resilience in the international role of the euro despite the pandemic

shock, in contrast to the euro area sovereign debt crisis episode.

• This may reflect, to some extent, the effectiveness of the unprecedented

policy support measures and coordinated approach prevailing in the euro

area.

• Stability of the role of the euro at a low level suggests that only further

resolute policy measures and reform efforts would enable to realise its

global potential.

22 w ww.ecb.europa.eu ©3. Conclusions (cont’d)

• Policy implications stressed by the Eurosystem in the past still valid:

“The international role of the euro is primarily supported by a deeper and more complete EMU, including

advancing the capital markets union, in the context of pursuing sound economic policies in the euro area.

The Eurosystem supports these policies and emphasises the need for further efforts to complete EMU.”

• Euro area capital markets less deep and liquid than in the US

Progress towards Capital Markets Union

• Other positive factors for the euro’s role:

NGEU, and creating a common safe asset

Green bonds, setting global standards and deepening the market

• Digital euro work in early stages, unlikely to be a game changer

23 w ww.ecb.europa.eu ©History offers lessons for the euro

Currency composition of globally disclosed foreign exchange reserves: 1899-2020

(percentages; at current exchange rates)

Pound sterling Japanese yen

US dollar Euro

French franc Chinese renminbi

German mark

90

80

70

60

50

40

30

20

10

0

1899 1909 1919 1929 1939 1949 1959 1969 1979 1989 1999 2009 2019

Source: Updated from Eichengreen, Barry, Arnaud Mehl and Livia Chiţu (2017), How global currencies work, Princeton University Press.

Notes: Data available for only 1899 and 1913 prior to the World War I. No data available for 1914-1927 and 1937-1946 due to incomplete archival records. The latest observations are for the third quarter of 2020.

24 w ww.ecb.europa.eu ©You can also read