The value creation journey A survey of JSE Top-40 companies' integrated reports - An analysis of company reporting in terms of the IIRC's ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

An analysis of company reporting in terms

of the IIRC’s Consultation Draft of the

International Framework.

August 2013

The value creation journey

A survey of JSE Top-40

companies’ integrated reports

www.pwc.com/corporatereporting

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers Inc, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Contents

Foreword 4

Executive summary 6

Introduction 7

Research methodology 7

Overview of findings 8

Emerging themes 8

Communicating value in the 21st century 10

Developments in integrated reporting 11

Findings 14

Organisational overview and external environment 15

Governance 18

Opportunities and risks 21

Strategy and resource allocation 23

Business model 25

Performance 29

Future outlook 34

Appendix 1: Companies surveyed 38

Contacts 40

PwC | 3

Foreword 4 | The value creation journey

The creation of value is at the heart of But what of the outcome of its product?

integrated thinking with the outcome In this regard, if it is alleged that the

being the annual integrated report. The beverage causes obesity the amelioration

process is known as integrated reporting. or eradication of such an outcome

should be included in the long-term

The integrated reporting process consists strategy of the company.

of integrated thinking which embraces:

the resources used by the company; This is an example of how integrated

its ongoing relationships with its key thinking must be from the input of the

stakeholders; its business model; its resources used by the company, the

output being its products or services; and relationships with its stakeholders, and

the impact that its products or services the outcomes of its products. It also

have on society, the environment and illustrates the interconnectedness and

its key stakeholders, such as customer interdependency of the resources used

satisfaction. by the company and its relationships

with its stakeholders with regard to its

This interconnection and functions and operations.

interdependency between the resources

used by a company and its relationships This survey by PwC on value creation

with its stakeholders, is critical in illustrates how the concept of value has

developing strategy. changed in the 21st century. It has to be

accepted that corporate reporting as we

At the beginning of the 21st century it have known it for years is no longer fit

was appreciated that some 80% of the for purpose because it does not deal with

value of companies was not represented the total value of a company.

by additives in a balance sheet according

to international financial reporting Integrated thinking deals with value

standards. To understand value, creation short, medium and long term

therefore, there had to be a shift in and the integrated report tells the story

thinking from a focus in value being seen of this value creation in clear, concise

in the context of future cash flows. Value and understandable language.

embraces the impact of the financial

aspects on the non-financial aspects and This survey will be extremely helpful

vice versa and how a board has applied to managers and directors in applying

its collective mind to the material integrated thinking and in preparing an

sustainability issues of a company in its integrated report.

long-term strategy.

For example, a beverage manufacturer

would have, as its long-term strategy,

reducing, reusing, replenishing and

recycling water, being the scarcest

natural asset. By embedding this

conservation of water into its strategy,

the company shows the investor that it Mervyn King SC

has a long-term plan to create value. Chairman of the International Integrated

Reporting Council

Integrated thinking deals with value creation

short, medium and long term and the

integrated report tells the story of this value

creation in clear, concise and understandable

language.

PwC | 5

Executive summary 6 | The value creation journey

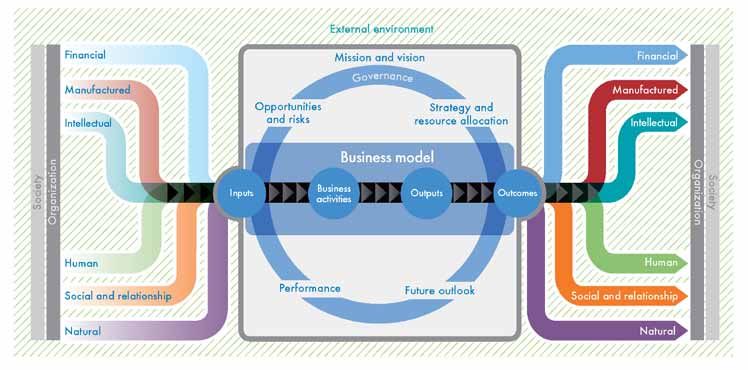

PwC’s model for integrated reporting

vers

Introduction

dri St

Corporate reporting is an ever-evolving l r

na

at

field as companies continually strive to Governance

eg

ter

improve their communication with their Technological

y

stakeholders. Societal Economic

Ex

Strategy &

One of the most important ways of doing objectives

so is through the annual integrated Geopolitical Competitive

report, which seeks to align relevant Environmental Remuneration Risk

information about an organisation’s

strategy, governance systems,

performance and future prospects

Corporate

ips

in a way that reflects the economic, contribution KPIs

environmental and social impact it has

Consumption -financial reso

Performance

Value drivers

on

on the environment in which it operates.

nsh

n

Social contribution

urc

Strategy

es

fin a n ci al r e

Business

Funding

model

For over a decade, we have invested

Pe

hip s

tio

Wealth creation

significant resources in understanding:

ns

ou ti o

rc e s

s

r ela

rf

la

or

• The information needs of preparers

re

and users; an

m

n d

ce

sa

• The economic benefits of

transparency; and

r ce

• Up-to-date reporting and best Resou

practices from around the world in

order to provide practical insights into

the critical building blocks of effective Source: PwC

corporate reporting.

Our focus has been on aligning the

interests of those who report on Research methodology

performance with those who use the

information to make critical investment

The mission of the IIRC is to create a The questions were based on the Content

decisions.

globally accepted integrated reporting Elements for an integrated report

framework that assists organisations presented in the IIRC’s Consultation

Our model has been developed following to recognise and present material Draft of the International

extensive stakeholder research and is information about their strategy, Framework.

closely aligned with the International governance, performance and prospects

Integrated Reporting Council (IIRC) in a clear, concise and comparable Each assessment was reviewed by an

Framework. format. experienced reviewer before being

approved for inclusion in the overall

We conducted our survey on the Top survey results.

40 companies listed on the FTSE/JSE

as at February 2013. For each of the

companies comprising the Top 40 (see

Appendix A), a detailed assessment of

110 questions was performed.

PwC | 7

Overview of findings

Survey findings by content element

Future outlook 23% 64% 13%

Emerging themes

Performance 13% 81% 6% Storytelling through

images

Business model 6% 59% 35%

Companies showed a definite willingness

to tell their value creation stories in

Strategy and resource allocation 3% 81% 16%

non-traditional ways. Use of information

graphics and images that combined

Opportunities and risks 3% 65% 32% words and pictures were common

throughout the reports.

Governance 39% 58% 3%

Governance in action

onal overview and external environment 6% 71% 23%

There was a definite tendency toward

‘constrained’ governance reporting.

Effective communication Companies seemed more comfortable

reporting on board charters and terms

Potential to develop reporting

of reference, rather than the actual

Clear opportunities to develop reporting activities undertaken by the board and

committees during the year.

Source: PwC analysis

Avoiding the ‘crystal ball’

Historical reporting remains the focus,

Findings were grouped by Content The most effective communication with companies shying away from

Element and then evaluated according to was found in reporting on strategy and broaching the topic of what the future

three broad categories: resource allocation, as well as reporting may hold for them.

on business models.

• Clear opportunities to develop

reporting; Reporting on governance activities ‘Silo’ reporting

showed the greatest room for It is evident that many companies

• Potential to develop reporting; and

improvement. are still taking their first steps on the

• Effective communication. integrated reporting journey. Stand-

alone sections of reporting often

provide excellent communication,

but opportunities to connect this

information to other areas in the report

are often missed, especially in the

segmental review.

8 | The value creation journey

Identify one or Report priorities Report their Integrate their risks

more material for their non-financial principal risks into other areas of

capitals capitals their reporting

55% 52% 97% 52%

Explicitly identify Average number of Discuss future Link market

their key measures market trends discussion to

performance

measures

22% strategic choices

Align measures with

strategy

84% 35% 90% 61%

Make reference to Integrate the Include strategic Base reporting on

their business model business model into priorities strategic themes

other areas of their

reporting 21%

Embed sustainability

in strategy

71% 60% 77% 29%

PwC | 9

Communicating value in the 21st century 10 | The value creation journey

Framework finalisation process

1st half 2012 2nd half 2012 1st half 2013 2nd half 2013

• Discussion • Prototype 16 April – 15 July: December:

Developments in Paper

responses

•

•

Examples

Benefits

Framework

consultation

Framework

version 1 launch

integrated reporting • Framework outline • Topics

Integrated reporting has been a

buzzword in recent years, but never

Pilot Programme (extended into 2014): Companies and investors

more so than in the first half of 2013.

The International Integrated Reporting

Council (IIRC) launched the eagerly-

anticipated Consultation Draft of the Engagement with regulators and other stakeholders

International Framework in April,

with 15 launch events held around the

globe. Source: Adapted from the Consultation Draft of the International Framework

The comment period for the

Consultation Draft closed in July 2013

and the IIRC is currently reviewing What’s the big deal? What are the benefits

comment letters in preparation for

the launch of the first version of the The world is changing at a rapid for businesses?

Framework in December 2013. pace and the global context in which

The organisations participating in the

businesses operate is changing along

Business Network have already begun

with it. The economic crisis was a sharp

What is the IIRC? reminder that financial measurement

to see the benefits of applying the

principles of integrated reporting in

The IIRC brings together leaders from all alone cannot provide sufficient insight

their businesses. Organisations have

the major international standard-setting into business performance.

benefitted from improving their ability

and regulatory bodies with companies, to tell their own stories and define what

investors and other key representatives Investors and other stakeholders are the business is trying to do through

to develop an internationally accepted now demanding that management teams management’s eyes.

integrated reporting framework. provide clear, unambiguous information

about issues such as external drivers

The application of integrated thinking

The IIRC’s mission is “to create the affecting their business, their approach

inside organisations has been a

globally accepted International to governance and managing risk, and

significant benefit for many businesses,

Framework that elicits from how their business model really works.

challenging them to question their own

organisations material information internal decision-making processes

about their strategy, governance, This paradigm shift is necessitating and break down silos within their

performance and prospects in a clear, businesses and other organisations to organisations.

concise and comparable format.”1 consider more than just the traditional

financial focus of thinking and reporting.

Since October 2011 the IIRC’s Pilot Why stakeholders like it

Programme Business Network,

comprising more than 90 businesses

What is integrated The Consultation Draft of the

International Framework

from 24 countries has been putting the reporting? identified investors, or ‘providers

principles of integrated reporting into of financial capital’, as the primary

Integrated reporting is “a process that

practice. audience for an integrated report, but

results in communication, most visibly a

periodic integrated report, about value emphasised that other communications

The Business Network has been creation over time. An integrated report resulting from integrated reporting

supported by more than 30 investor is a concise communication about how would be of benefit to all stakeholders

organisations that comprise the Pilot an organisation’s strategy, governance, interested in an organisation’s ability to

Programme Investor Network. performance and prospects lead to the create value over time.

creation of value over the short, medium

and long term.”2 The Pilot Programme Investor Network

has told the IIRC what they want: They

Integrated reporting is not just about want to see how companies perform

producing an integrated report; it is against their strategy and how strategic

about the journey that an organisation objectives actually support the long-term

has embarked on to create value. creation of value.

1+2

“Consultation Draft of the International Framework”, IIRC, http://www.theiirc.org/wp-content/uploads/Consultation-Draft/Consultation-

Draft-of-the-InternationalIRFramework.pdf (accessed August 2013)

PwC | 11Organisational capital

Financial capital Manufactured capital

Includes cash, debt and equity that Includes physical objects such

enable an organisation to produce as buildings, equipment and

Only approximately 20% of the market goods or provide services. infrastructure.

value of a company today relates to

its tangible assets and investors want

businesses to account for the 80%

intangible value as well.

Intellectual capital Human capital

What does the Includes knowledge-

based intangibles of

Financial Includes people’s

competencies and

capital

Framework say? an organisation. capabilities.

Fundamental concepts Manufactured

capital

The Draft Framework focuses on Intellectual Human

the various forms of capital that an capital capital

Social and

organisation uses and affects, the relationship

organisation’s business model and the capital

creation of value over time.

Natural

The business model is the vehicle capital

through which an organisation uses its

capital to create value.

Social and relationship capital Natural capital

Includes the relationships between Includes all renewable and

Value in the context of is not an organisation and communities non-renewable environmental

limited to monetary or financial value, and other stakeholders. resources.

or a set time frame. Value can be tangible

or intangible, it can be created over the

short, medium and long term, and is not

Source: Adapted from the Consultation Draft of the International Framework3

limited to the organisation but can be

created for others as well. It is important

to acknowledge that value creation is Guiding Principles and The Framework provides the following

Content Elements:

complex and arises from the interaction Content Elements

between a wide range of factors.

While the purpose of the Framework is • Organisational overview and external

to assist organisations with the process environment

of integrated reporting, the requirements

of the Framework are principles • Governance

based and do not focus on rules for • Opportunities and risks

measurement or disclosure of individual

matters or the identification of specific • Strategy and resource allocation

key performance indicators. • Business model

The Framework puts forward Guiding • Performance

Principles and Content Elements to give • Future outlook

direction to the content of an integrated

report. The Guiding Principles inform These elements are not intended to

the content of the report as well as how appear as independent sections of

the information is presented. the report. Rather, the purpose of the

report is to integrate these elements

The Content Elements outline the in a meaningful way by answering the

categories of information required question posed by each element.

to be in an integrated report in order

to communicate the organisation’s

particular value creation story.

3

Copyright © April 2013 by the International Integrated Reporting Council. All rights reserved. Used with permission of the International

Integrated Reporting Council. Permission is granted to make copies of this work to achieve maximum exposure and feedback.

12 | The value creation journeyGuiding Principles and Content Elements

The information in an An should provide An should show a

should be insight into the comprehensive value

presented on a basis organisation’s strategy creation story, the

that is consistent over and how that relates to combination,

time and in a way that its ability to create inter-relatedness and

enables comparison with value in the short, dependencies between

other organisations to medium and long term. the components that

the extent it is material to are material to the

the organisation’s own organisation’s ability to

value creation story create value over time.

Strategic focus and future orientation

ity

bil

Co

ra

n

pa

ne

om

Organisational

cti

vit

overview and

dc

Governance

yo

external

an

f in

environment

cy

for

ten

ma

sis

tio

n

Co

n

Strategy and

Opportunities Business model resource

and risks

Re

ss

allocation

ne

liab

ive

ility

ns

po

a

nd

es

Co

rR

mp

lde

let

ho

Performance Future outlook

en

ke

es

Sta

s

Materiality and Conciseness

An should An should provide

include all material insight into the quality of the

matters, both organization’s relationships

An should provide

positive and with its key stakeholders

concise information that

negative, in a and how and to what extent

is material to assessing

balanced way and the organisation

the organisation’s ability

without material understands, takes into

to create value in the

error. account and responds to

short, medium and long

their legitimate needs,

term.

interests and expectations.

Source: Adapted from the Consultation Draft of the International Framework4

4

Copyright © April 2013 by the International Integrated Reporting Council. All rights reserved. Used with permission of the International

Integrated Reporting Council. Permission is granted to make copies of this work to achieve maximum exposure and feedback.

PwC | 13Findings 14 | The value creation journey

Organisational overview and external environment

61%

What it means

An integrated report Communicating the context within

should answer the which an organisation operates is often

the first step in enabling stakeholders

question: to understand how that organisation

creates and sustains value. of companies linked

What does the An integrated report should therefore strategic choices to

organisation do communicate information to enable

stakeholders to understand the markets external drivers

and what are the the organisation competes in, why it

has chosen to compete in that market,

circumstances under and the impact of trends that are

which it operates? driving strategic choices. This involves Reporting on organisational overview

communicating about the general and external environment

Source: Consultation Draft of the market environment including the key

International Framework para markets and environments that an

4.6 organisation operates in, key underlying

6%

drivers of market growth historically

and in the future, and the organisation’s

competitive landscape. An organisation 23%

should recognise the opportunities and

risks presented by the external market

that, through its strategic choices, the

organisation is adapting itself to meet.

Findings

71%

The majority of companies surveyed

displayed potential to develop their

reporting further.

Effective communication

Principle in practice Potential to develop reporting

Clear opportunities to develop reporting

Good reporting should provide insight into:

Source: PwC analysis

• The organisation’s:

–– culture, ethics and values; Some of the most important information

–– ownership and operating structure; lacking in this area is comprehensive

–– principal activities, markets, products and services;

quantification of data such as expected

market trends or rates of market growth.

–– competitive landscape and market positioning (considering factors such This indicates that while companies

as the threat of new competition and substitute products or services, explain how markets have changed and

the bargaining power of customers and suppliers, and the intensity of grown historically, often only limited

competitive rivalry); information is provided on the key

• Key quantitative information (e.g. the number of employees, revenue and factors that will impact them in the

number of countries in which the organisation operates), highlighting, in future.

particular, significant changes from prior periods; and

• Significant factors affecting the external environment.

Source: Consultation Draft of the International Framework para 4.7

PwC | 15The competitive landscape is explained

39% 42% 20% 6%

Not accomplished To some extent Accomplished Exemplary

Source: PwC analysis

Competitive advantage What good reporting looks like

A tendency to avoid comprehensive

discussion of companies’ competitive

landscape was also identified. Less than Example 1: Discovery

a quarter (19%) of companies surveyed

succeeded in explaining market share, Operating structure, principal

Company culture is demonstrated activities, products and services are

positioning within key markets and

by explaining core values. illustrated in one graphic.

barriers to entry in specific markets.

Many companies shied away from

identifying key competitors.

Most companies surveyed did, however,

provide valuable information on how

strategic choices are directly linked to

external drivers and trends.

How reporting can be

developed

While it is often difficult to identify

forward-looking information and

quantify industry trends, this

information is crucial to investors in

assessing an organisation’s ability to

create value over the medium and long

term, as opposed to providing short-term

returns. Companies can therefore seize

the opportunity by including robust

reporting on the factors that may impact

on their ability to create value in the

longer term, as well as being specific

about the competitive landscape.

Key quantitative information.

Ownership percentage is disclosed

for each business unit.

Source: Discovery Integrated Annual Report 2012

16 | The value creation journeyExample 2: Aspen Pharmacare

Identity of competitors.

Market position

Comparison to peers

Source: Aspen Pharmacare Holdings Annual Report 2012

PwC | 17Governance

39%

What it means

Integrated reports “An organisation’s ability to create and

should answer the sustain value is determined inter alia by

how it’s led and its governance.”5

question:

Governance reporting provides the nexus

between the social, environmental,

of companies showed

“How does the economic and financial issues that clear opportunities to

organisation’s impact on the organisation’s business

and the development of strategy. develop governance

governance structure

support its ability to Effective communication about reporting

the governance of an organisation

create value in the is therefore integral to the user’s

appreciation of how those charged with

short, medium and governance are creating value. Reporting on governance

long term?”

Findings 3%

Source: Consultation Draft of the

International Framework para In analysing our overall results, the

4.10 governance element emerged as an area

where reporters did not provide much

insight into their governance practices. 58%

16%

The overall finding was that the majority

of reporters provide ‘boiler plate’

disclosures of their corporate governance 39%

practices, which do not reflect what

those charged with governance have

actually done in adding value to the

of companies describe company.

the actual activities Companies assessed are comfortable

reporting on board charters and terms Effective communication

of the board and of reference. There is an opportunity to

Potential to develop reporting

integrate the reporting of the actions

committees and responsibilities of those charged Clear opportunities to develop reporting

with governance with the operations and

strategies of the company to provide a Source: PwC analysis

holistic view of governance.

How integrated is the

Principle in practice governance reporting?

Good reporting should provide insight into: The integration of governance reporting

within the integrated reports was

assessed. Our research found that just

• An organisation’s leadership structure, including the diversity and skills of

more than half (55%) of integrated

those charged with governance;

reports were assessed to have not

• Specific processes used to make strategic decisions and to establish and accomplished integration as there was

monitor the culture of the organisation; minimal linkage between the narrative of

• Particular actions those charged with governance have taken to influence and the integrated report and the governance

monitor the strategic direction and risk management approach; reporting.

• How the organisation’s culture, ethics and values are reflected in its use of

and effect on the various forms of capital, including its relationships with key The balance of the reports were

stakeholders; and assessed to be linked to some extent

as cross references were provided to

• How remuneration and incentives are linked to value creation.

other aspects of the integrated report,

including risk management and strategy.

Source: Consultation Draft of the International Framework para 4.11

5

“Consultation draft of the international Framework”, IIRC, http://www.theiirc.org/wp-content/uploads/Consultation-Draft/Consultation-

Draft-of-the-InternationalIRFramework.pdf (accessed August 2013)

18 | The value creation journeyAre boards reporting on what

Governance reporting integrated into other reporting

they’re actually doing?

An emphasis has been placed on

reporting on the actual activities 55% 45%

undertaken by management and the

Not accomplished To some extent Accomplished Exemplary

board in discharging its responsibilities

rather than reporting on the

responsibilities, terms of reference and

charters of the board and its committees.

Source: PwC analysis

Thirty-five percent of reports disclosed

only the responsibilities of the board and Targets for gender diversity on the board are discussed

its committees and terms of reference

and therefore did not accomplish

effective reporting of governance 48% 39% 13%

practices.

Not accomplished To some extent Accomplished Exemplary

Some description of the actual activities

undertaken by the board was provided Source: PwC analysis

by 48% of reporters, while 16% of

reports were assessed as having

accomplished good reporting practice

by reporting the actual activities of the

board and providing examples or case

studies of these activities.

A word on gender diversity How reporting can be

In terms of providing more than basic Gender and race are important factors to developed

disclosures about the board effectiveness consider in achieving board diversity. In Organisations that integrate governance

review, 16% of reports were assessed as assessing the organisation’s leadership reporting into their integrated report

having accomplished good reporting. structure, we reviewed integrated provide a more holistic view of the

These reports included disclosure on reports to determine if policies and importance of governance to a business.

the logistics and process undertaken in targets for gender diversity have been

assessing the effectiveness of the board disclosed. Reporting on actual activities

as well as extensive disclosure of the undertaken by the board and the

outcomes of the review. No mention of a policy or a target for outcomes of these activities is more

gender diversity could be found in 48% insightful than simply providing

Brief mention of the logistics and the of reports, while 39% of reports provided information about committee agendas

process of assessment of the board’s brief reference to supporting policies on and charters.

effectiveness was made by 32% of gender diversity.

reporters, while the remaining 52%

of reporters were assessed as not Reporting assessed as accomplished

accomplished and provided a description in this area provided insight into the

of logistics, the process and a limited company’s policy, evidence of actions

discussion of the outcomes of the review. taken and targets set to achieve gender

diversity. This was demonstrated in13%

of the reports.

PwC | 19What good reporting looks like

Example 3: British American Tobacco

Summary terms of reference of the

board committee are provided and

are supplemented with details of the

actual activities of the board.

Board committees undergo an Actual activities undertaken by the

effectiveness review and the results board committee during the year

of the review are disclosed. have been disclosed.

Action points that have emerged

from the committee effectiveness

review have been provided.

Source: British American Tobacco Annual Integrated Report 2012

Example 4: FirstRand

An integrated approach to

governance of financial and non-

financial capitals is demonstrated

Source: FirstRand Annual Integrated Report 2012

20 | The value creation journeyOpportunities and risks

48%

What it means

An integrated report Value creation is significantly affected

should answer the by an organisation’s ability to embrace

opportunities and effectively manage

question: risk. An integrated report should

identify these opportunities and risks,

and explain the strategic direction the

of companies integrated

What are the specific organisation has chosen and the actions risks into other aspects

it has undertaken to manage these.

opportunities and of the report

risks that affect the Effective communication in this area

includes providing insight into the risk

organisation’s ability identification and management process Reporting on opportunities and risks

of an organisation, the specificity of the

to create value over risks identified to the organisation and

3%

the short, medium and clear discussion of the implications of 16%

the identified risks on the organisation’s

long term, and how ability to create value.

is the organisation

dealing with them? Findings

The vast majority of companies surveyed

Source: Consultation Draft of the showed potential to develop their

International Framework para

integrated reporting further.

4.13

81%

Principle in practice

Good reporting should provide insight into: Effective communication

Potential to develop reporting

• The specific source of opportunities and risks, which may be internal, external Clear opportunities to develop reporting

or, commonly, a mix of the two;

• The organisation’s assessment of the likelihood that the opportunity or risk Source: PwC analysis

will come to fruition and the magnitude of its effect if it does. This includes

consideration of the specific circumstances that would cause the opportunity While most companies included

or risk to come to fruition; and narrative information about identified

• The specific steps being taken to create value from key opportunities and to risks specific to the company, only 10%

mitigate or manage key risks, including the identification of the associated supported the discussion with quantified

strategic objectives, strategies, policies, targets and performance indicators. information, such as through key

performance indicators (KPIs).

Source: Consultation Draft of the International Framework para 4.15 Risk dynamics

A mere 13% of companies provided good

insights into the dynamics of their risk

Insights into the dynamics of the risk profile are provided

profiles by including information about

the impact and probability of identified

risks, as well as how risk profiles may

74% 13% 13%

change over time.

Not accomplished To some extent Accomplished Exemplary

Source: PwC analysis

PwC | 2123%

How reporting can be

developed

Opportunities and risks are fundamental Companies that include information

and pervasive to organisations’ value about the potential impact and

creation activities. It is therefore probability of risks occurring provide

paramount to integrate discussions stakeholders with valuable information of companies make

relating to opportunities and risks about those risks that may influence the

throughout the integrated report and company’s ability to create value over specific reference to risk

avoid limiting risk reporting to a stand- the short, medium and long term. This

alone section. could also include linking risks to KPIs or appetite

quantifying risks in a meaningful way.

What good reporting looks like

Example 5: SABMiller

Source of the risk is explained Risks specific to the company are Risks are linked to strategic

identified priorities

Impact on the business is identified Actions taken to mitigate the risks

are explained

Source: SABMiller Annual Report 2012

Example 6: Gold Fields

Risks are specific to the company

Risks are plotted based on severity

and probability

Only most material risks are

included

Source: Gold Fields Limited Integrated Annual Review 2012

22 | The value creation journeyStrategy and resource allocation

39%

What it means

An integrated report The importance of an organisation’s

should answer the strategy is highlighted by the fact that

strategic focus is one of the guiding

question: principles of the Framework, as

well as a Content Element.

of companies discussed

Where does the A good strategy is the frame of reference targeted time frames for

for all the value creation decisions and

organisation want activities that an organisation may implementing strategic

to go and how does it engage in. An organisation should

communicate what it is trying to achieve, objectives

intend to get there? where it is trying to compete, how it will

achieve its goals and how it will measure

Source: Consultation Draft of the progress.

International Framework para

4.18

Principle in practice

Good reporting should provide insight into:

Findings

Nearly half of companies surveyed • The organisation’s short, medium and long-term strategic objectives;

demonstrated effective communication • The strategies it has in place, or intends to implement, to achieve those

relating to strategy and resource strategic objectives;

allocation.

• The resource allocation plans it has in place, or intends to put in place, to

implement its strategy; and

Reporting on strategy and resource

allocation • How it will measure achievements and target outcomes for the short, medium

and long term.

6%

Source: Consultation Draft of the International Framework para 4.19

35% Almost all companies (97%) surveyed More than half (64%) of companies

made some kind of statement relating surveyed reported on the outcomes of

to overall ambition, and nearly three strategic activities and clearly set out

quarters (74%) of companies surveyed performance measures that management

59% had comprehensive discussion use to monitor whether these are being

surrounding how strategic priorities are achieved.

aligned to overall goals.

Outcomes of strategic priorities are reported on

Effective communication

Potential to develop reporting 19% 17% 16% 48%

Clear opportunities to develop reporting Not accomplished To some extent Accomplished Exemplary

Source: PwC analysis

Source: PwC analysis

PwC | 23What good reporting looks like

Example 7: British American Tobacco

How reporting can be Performance measure is linked to Medium and long-term goals are

developed strategic objective of “Responsibility” communicated

Incorporating strategic priorities as a

common theme throughout a report

demonstrates how integrated strategy is

in a company’s value creation journey.

Including time frames and targets

for achieving strategic priorities also

enables stakeholders to assess whether

companies are making progress towards

achieving their ambitions.

48%

of companies reported

on specific actions Measure and rationale for use is

explained

Current year measure as well as

comparison to past

taken to achieve

strategic priorities Source: British American Tobacco Annual Report 2012

Example 8: Standard Bank Group

Strategic objectives are clearly

identified

Outcomes of specific actions taken in

the current year

Specific actions planned for the future

Source: Standard Bank Group Annual Integrated Report 2012

24 | The value creation journeyBusiness model

55%

What it means

An integrated report The business model is at the heart of

should answer the an organisation and draws from the

different capitals as inputs and converts

question: them into outputs by means of the

organisation’s business activities. of companies identify

What is the This process leads to outcomes that in and describe material

turn impact on the capitals, which are

organisation’s business not necessarily identical to those used in capital imputs into the

model and to what the input phase.

business model

extent is it resilient? This complex interconnection between

an organisation and its environment is An organisation should explain the

Source: Consultation Draft of the the core of value creation. resources and relationships that it relies

International Framework para on to deliver its strategy, how dependent

4.21 it is on them, how it manages them and

how it monitors success.

The value creation process

Source: Consultation Draft of the International Framework6

6

Copyright © April 2013 by the International Integrated Reporting Council. All rights reserved. Used with permission of the International

Integrated Reporting Council. Permission is granted to make copies of this work to achieve maximum exposure and feedback.

PwC | 25Principle in practice

Good reporting should provide insight into:

• Key inputs and how they relate to the capitals from which they are derived;

Findings • Key business activities, considering such factors as:

Most companies accomplished effective –– How the organisation differentiates itself in the market place;

reporting at some level. While the –– The extent to which the business model relies on revenue generation after

majority still have potential to develop, the initial point of sale;

a large number of companies clearly –– How the organisation approaches the need to innovate;

demonstrated effective communication.

–– How the business model has been designed to adapt to change;

Reporting on the business model • Key outputs, explaining the products and services that the organisation places

in the market, and material by-products and waste;

• Key outcomes in terms of the capitals, including both internal outcomes and

3% external outcomes.

Source: Consultation Draft of the International Framework para 4.22

32%

Insights given into dependency on certain resources and relationships

65%

23% 58% 19%

Not accomplished To some extent Accomplished Exemplary

Source: PwC analysis

Effective communication

Potential to develop reporting

Clear opportunities to develop reporting

Thoughts on dependency Many organisations neglect to discuss

the role of the corporate centre in the

Source: PwC analysis Less than a quarter (19%) of companies delivery of strategy. How an organisation

gave insight into their dependency on functions on a central level may provide

Many companies (55%) identified certain resources and relationships insights into how the different elements

material capital inputs into the business inherent in the business model. More of the business model are managed

model, as well as the differentiators than 90% of companies integrated their and monitored, as the corporate

and value-adding activities within the discussion of the business model with centre is often the main driver of the

business model used to execute strategy other elements of the report. different value-creating activities of an

and implement priorities. organisation.

How reporting can be

developed

Given the complexity of organisations’

45%

relationships with the external

environment, resources and

relationships, organisations should

carefully consider the communication

of this complexity to stakeholders. This

is especially true where organisations

are dependent on scarce resources or

of companies integrated significant relationships to create value.

discussion of their

business model with

other elements of the

report

26 | The value creation journeyKey inputs into the

Material capital inputs business model are Processes and outputs Key outcomes are identified

are addressed described are explained Example 9: Kumba Iron Ore

What good reporting looks like

Source: Kumba Iron Ore Limited Integrated Report 2012

How the company differentiates itself in

the market place Future plans are discussed

PwC | 27Example 10: Massmart

Role of the corporate centre is

described

Inputs and outputs are identified

Products that the company places into Clear description of the business

the market are identified activities of the company

Explanation of how the company

differentiates itself in the marketplace

Source: Massmart Annual Report 2012

28 | The value creation journeyPerformance

51%

What it means

Integrated reports Underpinning the focus on integrated

should answer the reporting is a strong appreciation

that the success of organisations

question: is inextricably linked to three

interdependent factors: society, the

environment and the global economy.

of companies provide

“To what extent has clear alignment

Performance reporting has similarly

the organisation evolved from reporting on financial between KPIs and

achieved its strategic measures of success to a more holistic

approach that includes reporting on remuneration policies

objectives and what are social and environmental performance.

its outcomes in terms

Findings Reporting on performance

of the effects on the

The overall results indicate that

capitals?” with only 6% of reporters effectively 6%

13%

communicating their holistic

Source: Consultation Draft of the performance to users, there is great

International Framework para potential to improve performance

4.27 reporting in integrated reports.

Principle in practice 81%

Good reporting should provide insight into:

• Quantitative indicators with respect to targets, value drivers, and opportunities

and risks, explaining their significance and implications and the methods and

assumptions used in compiling them; Effective communication

• The organisation’s effects (both positive and negative) on the capitals, Potential to develop reporting

including material effects on capitals up and down the value chain; and

Clear opportunities to develop reporting

• Linkage between past and current performance, and between current

performance and future outlook.

Source: PwC analysis

Source: Consultation Draft of the International Framework para 4.28 Quantitative measurement

Quantitative indicators of performance

KPIs are explicitly identified such as KPIs can help increase

comparability and are particularly

helpful in expressing and reporting

16% 84% against targets.

Not accomplished To some extent Accomplished Exemplary

Our research found that 84% of

companies explicitly identified KPIs. On

Source: PwC analysis average, companies reported 24 KPIs in

their integrated reports, of which eight

were financial KPIs, 10 were operational

and six related to sustainability.

KPIs: Quantity vs quality

While inclusion of quantitative KPIs may

create the impression that performance

has been well disclosed, it is important to

assess the usefulness and quality of the

KPIs identified.

PwC | 29KPIs are aligned to strategic objectives

6% 43% 16% 35%

In providing a context for the KPIs Not accomplished To some extent Accomplished Exemplary

reported on, 81% of reports showed

room for improvement both in

Source: PwC analysis

qualitatively defining the KPIs and

providing a rationale for their use. The

remaining 19% of reports defined their

KPIs and explained within the context of Trend and comparable benchmark data Our overall assessment of KPIs indicates

their business why they had been used. is recognised as providing useful context that while most organisations are

for the results of the KPIs reported explicitly identifying KPIs and disclosing

It is encouraging to note that almost on. The majority of reports (84%) a large number of KPIs, the KPIs reported

half of all KPIs reported are aligned do provide trend data for their KPIs, on are not communicated on in the

to strategic priorities(51% of reports allowing users to make year-on-year context of the business.

assessed) that reinforce the principle comparisons.

of integrated thinking. Of these, three- Linking performance and

quarters explicitly linked their KPIs However, only 3% of the reports

to their strategic priorities and were provided industry benchmark data

remuneration

assessed as exemplary reporters. against which users can assess the A greater emphasis has been placed

performance of the company. on aligning KPIs with remuneration

policies to enhance the transparency of

71%

In the majority of cases, where trends management and board remuneration.

have been established, information has

not been provided regarding the reasons KPIs should be aligned to strategic

for movements from the prior year, priorities, which in turn drive the

particularly where targets have not been remuneration policies of the company.

met.

of KPIs are quantified Future targets for KPIs reported

on enhance the accountability of

management. An overwhelming majority

of reports (90%) do not provide future

targets for KPIs, or only partly provide

future targets for KPIs. Just 10% of

reports provide quantified future targets

for all KPIs.

Enhancing the quality of KPIs

• Tailor KPIs to be relevant to the organisation;

• Report KPIs that are consistent with measures used by those charged with

governance in assessing the performance of the organisation;

42%

• Present KPIs with targets, forecasts or projections over the short and medium-

term;

• Present for past periods to establish a trend and with industry benchmarks;

• Present against previously reported targets, forecasts or projections to

enhance accountability;

• Report consistently over periods;

of companies provide • Present measurement techniques and assumptions made with qualitative

information; and

comparable benchmark • Report on reasons for significant variations from targets, trends or benchmarks

data for KPIs and why they are or are not expected to reoccur.

30 | The value creation journeyHow reporting can be

Alignment of KPIs with remuneration policies

developed

Organisations can enhance the quality

35% 43% 16% 6% and usefulness of KPIs reported by

making them specific to their business

Not accomplished To some extent Accomplished Exemplary

and providing clear targets and industry

benchmarks against which they can be

Source: PwC analysis measured.

Where trends are provided to assist in

year-on-year analysis, management

An analysis of our findings found that Clear alignment between KPIs and commentary should accompany these

35% of integrated reports show no remuneration policies was demonstrated trends to enable users to understand the

meaningful alignment between KPIs in only 16% of reports. However, only movements in KPIs.

and remuneration policies, while 43% 6% of the reports assessed provided

demonstrate only some KPIs that align progress reports on whether targets Providing a clear link between KPIs

with remuneration policies. were actually achieved and if targets and the organisation’s strategy and

were not achieved, the reasons for the remuneration policies will enhance

underperformance. the quality of disclosure around

remuneration.

What good reporting looks like

Example 11: Gold Fields

Integrates the strategic requirement,

key stakeholders who would

be affected, stakeholder risk or

opportunity with performance,

strategic actions to be undertaken in The context of the KPI reported on is

the following year and remuneration in provided as well as its importance to KPIs are explicitly identified and

a format that is easy to follow. the organisation. quantified.

Reports on the key stakeholders Explains how the relative strength

driving the prioritisation of each of its value-adding activities and

strategic requirement. measures of success are determined,

i.e. use of performance measures and

the quantification of these.

PwC | 31Example 11: Gold Fields (cont.)

Trend data is provided for KPIs Strategic actions to be undertaken Explicit linkage is made between

reported on. in the following year have been achieving strategic priorities and KPIs

disclosed. and CEO remuneration

Source: Gold Fields Integrated Annual Report 2012

Example 12: Aspen Pharmacare

KPIs are explicitly identified. The implication of the actual performance as

per the disclosed indicator on the business

has been provided.

The relevance of the performance indicator for KPIs are quantified. A trend has been provided for the KPIs

the business has been discussed as well as an with at least two previous years of

explanation of what the KPI means. data reported on.

Source: Aspen Pharmacare Annual Integrated Report 2012

32 | The value creation journeyExample 13: Vodacom

Progress reported on targets identified As competitive performance is a

with an explanation of why results measure that may be subjectively

were ahead of targets. calculated, the report states what

competitive performance is in the

context of the results.

Weighting of targets is explicitly

provided

Description Financial targets used in

of how calculating remuneration,

bonuses are aligning strategic priorities

calculated is and remuneration are

provided explained

Source: Vodacom Annual Integrated Report 2012

PwC | 3329%

Future outlook

What it means of companies provided

Integrated reports In developing the Framework, it a comprehensive

should answer the was recognised that much of what is

currently reported tends to be backward- discussion of strategy

question: looking and fails to provide stakeholders

with sufficient information to make and priorities to ensure

What challenges and

a meaningful assessment regarding

the organisation’s ability to create and

the long-term viability

uncertainties is the

sustain value over the short, medium

and long term.

of the business.

organisation likely to Therefore, in addition to reporting

What is material?

encounter and what on performance during the reporting To provide a context for the future

period, the integrated report should viability of the organisation, it is

are the potential include a forward-looking statement important to understand the process

implications for its concerning the organisation’s

anticipated activities and performance

undertaken by management in

identifying material issues affecting its

business model and objectives, informed by its assessment of future viability.

recent performance and understanding

future performance? of trends in the external and internal A fifth (23%) of reports analysed did

environment, including stakeholder not discuss how material issues were

Source: Consultation Draft of the

expectations. identified, while 35% provided some

International Framework para

4.33 discussion of how material issues are

Findings identified.

Our research found that 13% of reporters The remaining 42% of reports provided

provided effective communication comprehensive reporting on identifying

of their future outlook and how the key issues such as descriptions of

company plans to create and sustain stakeholder engagement processes and

value over the medium and long term, outcomes.

while 87% of reports have the potential

to develop their reporting in this area. Reporting on the future outlook

Principle in practice 13%

23%

Good reporting should provide insight into:

• Anticipated changes over time;

• Information, built on sound and transparent analysis, about:

–– The expectations of senior management and those charged with

governance about the external environment the organisation is likely to face

in the short, medium and long term;

–– How that will affect the organisation; and

–– How the organisation is currently equipped to respond to the critical 64%

challenges and uncertainties that may arise.

Source: Consultation Draft of the International Framework para 4.34 Effective communication

Potential to develop reporting

The process for identifying material issues that impact future viability is Clear opportunities to develop reporting

explained

Source: PwC analysis

23% 35% 42%

The time frames of issues affecting future

Not accomplished To some extent Accomplished Exemplary viability and targets that an organisation

should consider in its reporting will

vary depending on its business and

Source: PwC analysis investment cycles, industry context,

strategies adopted and stakeholder

expectations.

34 | The value creation journeyWhile 32% of reports provided time

frames that are unclear, 68% do attempt Discussion of the future availability of material capital inputs

to identify the time frame in which future

viability has been considered, bearing

in mind the nature of the company’s 10% 71% 13% 6%

business and industry.

Not accomplished To some extent Accomplished Exemplary

Providing a future perspective

In assessing whether management Source: PwC analysis

discusses the expected availability

and its future access to the material

non-financial capital inputs that the The majority of reports assessed (71%) How reporting can be

organisation relies on to create value, provided only some or no information

only 6% of reports provided exceptional

developed

regarding specific strategic actions

disclosure and a comprehensive required to address future availability of The integrated report should provide

discussion of all material inputs material capital inputs. The remaining a clear and appropriate demonstration

supported with quantified data. 29% provided a comprehensive of the time frame over which future

explanation of strategy and priorities viability has been considered, in the

One fifth (19%) of reports provided a to ensure the long-term viability of the context of the nature of the company’s

discussion of all material inputs that the business. business and industry.

organisation is reliant on to create value,

while 71% of reporters provided limited Overall, the results of the future outlook Disclosing the specific strategic

or no discussion of the material inputs assessment show that integrated reports actions to be undertaken to address

and the availability of these, on which currently tend to provide information the availability of material non-

the organisation is reliant on to create that is mostly backward looking and financial capitals and provide future

value. which is of limited relevance to users. KPIs for strategic objectives identified

communicates the future prospects

and viability of an organisation to its

stakeholders.

What good reporting looks like

Example 14: AngloGold Ashanti

Where targets have not been reported on (social Explicit targets against The targets are aligned to strategy

performance), an explanation has been provided which KPIs are and cross-referenced to strategy

as to why the target has not been reported on and measured. disclosure.

when reporting on these targets will commence.

An explicit

time frame has

been provided

for achieving

the targets

identified.

Focus areas address both financial KPIs related to each focus area are

and non-financial strategic priorities. explicitly identified.

PwC | 35You can also read