The Wet Seal, Inc. (WTSL)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

RESEARCH REPORT:

PUBLISHED APRIL 21, 2014

It is no secret that the retail sector has struggled lately – most recently from a series of weather-related

issues, but also from persistently high unemployment that continues to dissuade consumer spending.

One of the harder-hit subsectors of retail though has been among teenage apparel, which has long been

a more fickle consumer group due to their ever-changing tastes, variety of available options, and volatile

spending habits. However, among teen spending, the largest portion of their budget is spent on clothing

(roughly 20%), followed closely by food, with accessories/personal care further behind. Although the big

three retailers in the teenage apparel space are clearly Abercrombie & Fitch, Aeropostale, and American

Eagle, the emergence of the so-called “fast-fashion” retailers have made significant strides in disrupting

that market over the years.

FAST-FASHION OVERVIEW AND COMPANY BACKGROUND:

The term fast-fashion is primarily used to describe fashion designs that move quickly from the catwalk

into retailers while being manufactured quickly and cheaply to allow mainstream consumers access to

these styles. Fast-fashion has also become associated with “disposable fashion” as these designer

products achieve mass market appeal through their relatively low prices. Since the more traditional

retailers place their orders much earlier in the season than fast-fashion retailers, the fast-fashion

retailers are able to stay more up-to-date on the most current fashion trends thus winning over more of

their target market (i.e. teenagers) than their competitors. Undoubtedly this strategy has been working

as these stores have continued to take market share from the bigger and more traditional teen retailers.

Some of the more common fast-fashion retailers are H&M, Forever 21, Zara, Peacocks, Urban Outfitters,

rue21, and Wet Seal.

Out of these retailers, one interesting example is Wet Seal, Inc. (WTSL), a specialty retailer that operates

stores across the US selling fashion apparel and accessory items designed for female customers aged 13

to 34 years old. The company operates two separate chains of retail stores (primarily mall-based)

nationwide under the names Wet Seal and Arden B. As of February 1, 2014, WTSL had 532 stores in 47

states and Puerto Rico, of which 475 were Wet Seal stores with the remaining 57 being Arden B stores.

While the Wet Seal segment targets more trend-focused and budget-friendly younger teenage girls

(mostly in the range of 13 to 23 years old), Arden B targets the more contemporary woman between the

ages of 24 and 34. The company also operates and continues to grow out its e-commerce divisions for

both their Wet Seal and Arden B business segments.

1

The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

RECENT STOCK PERFORMANCE:

While the vast majority of teen retailers/apparel stores have struggled over the past year, WTSL has

been among the hardest hit seeing its stock price fall over 60% since April 2013. In fact, as recently as

July 2013, WTSL shares were trading over $5 – a very far cry from their recent closing price of $1.17.

Looking at some of WTSL’s competitors, only shares of ARO have been hit as hard over the same time

period.

Source: Yahoo! Finance

Overall, the women’s retail apparel industry is highly competitive with fashion, quality, price, location,

and service acting as the primary competitive factors. Wet Seal has struggled more so than its

competitors as of late due to a combination of these factors, as well as company-specific issues. After

showing improvement in same store sales (SSS) from Q3 2012 through Q2 2013, the company began to

experience weakening SSS and margin trends during the latter portion of the back-to-school season.

These trends continued to intensify throughout the remainder of 2013 and into Q1 2014 due to several

factors. Chief among these factors were softness in mall traffic; an intense promotional environment

throughout the retail apparel segment; general weakness in fast-fashion merchandise and trends; still

challenging economic conditions (see: persistent high unemployment especially among teens); and

harsh weather conditions throughout much of the continental US over the winter months. As a result,

sales and margins suffered across both Wet Seal and Arden B stores, thus hurting share price

performance.

2

The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

TURNAROUND STRATEGY AND CATALYSTS FOR WTSL:

The majority of WTSL’s recent troubles began towards the end of 2011, and culminated in the firing of

their former CEO in July 2012 following the company’s first quarterly loss since 2007. The hiring of the

company’s new CEO, John Goodman, in January 2013 ushered in a re-branding of sorts and the

beginning of WTSL’s current “turnaround strategy” to re-establish their fast-fashion merchandising

practice through a more engaging shopping experience both in stores and online. Aside from Goodman’s

previous work experience in executive leadership roles at other retailers, additional expertise from other

senior members of the executive team will help expand and better market the company’s products in

the fast-fashion segment. Further, the recent additions of several board members will help aid WTSL’s

fast-growing e-commerce division, as well as the company’s branding campaign via social media.

Within this e-commerce division, the company has been making remarkable strides in expanding their

online and mobile presence, which they recognize as the future of their business. Although only 6% of

WTSL’s sales in 2013 were generated through their online channel, the launching of their new

Demandware platform – which is optimized for mobile and tablets – should help the company achieve

their goal of being at 10% of sales by year end. Management’s desire to increase online sales is

compounded by the fact that online sales lead to double the profitability when compared to their brick

and mortar counterparts. Furthermore, considering that roughly 60-70% of teens indicate they prefer to

shop online at their favorite retailers1, WTSL’s push to expand their online store represents the future of

their business. Moreover, these numbers are only expected to grow as mobile adoption increases in the

future. Ultimately, the company should be able to continue to grow both of these segments out even

further by building on their existing presence on social media platforms, such as Facebook, Twitter, and

Pinterest – especially with the help of the newly added board members. Taking into account the fact

that “more than half of teens indicate that social media impacts their purchases with Twitter being the

most important,”2 the growing importance of social media branding has certainly not been lost on

WTSL’s management team.

In addition, WTSL has been developing a presence in the Junior Plus category, which was first launched

on their website and is now in several of their existing brick and mortar locations and even one

standalone location. The company is pleased with the results to date and has decided to grow this

segment through expanded online offerings and additional new store openings over the next several

years (including two planned for this year). Given the positive customer response thus far and the fact

that the plus-size apparel market is expected to reach close to $10 billion by 2017,3 the potential

certainly exists for significant revenue growth for the company.

Lastly, the company plans to expand their real estate options by opening stores primarily in outlet and

off-mall centers as some of their in-mall stores are closed this year due to lease expirations. These outlet

and off-mall store locations typically operate at higher productivity and profitability levels, and should

therefore help the company’s bottom line. In addition, these redesigned stores should also help with the

company’s current re-branding strategy as well.

3The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

In my opinion, while not nearly as dramatic as with JCP, this new strategy should help the company

improve upon their recent poor performance and serve as a catalyst for the shares to go higher over the

coming quarters.

FINANCIALS AND VALUATION:

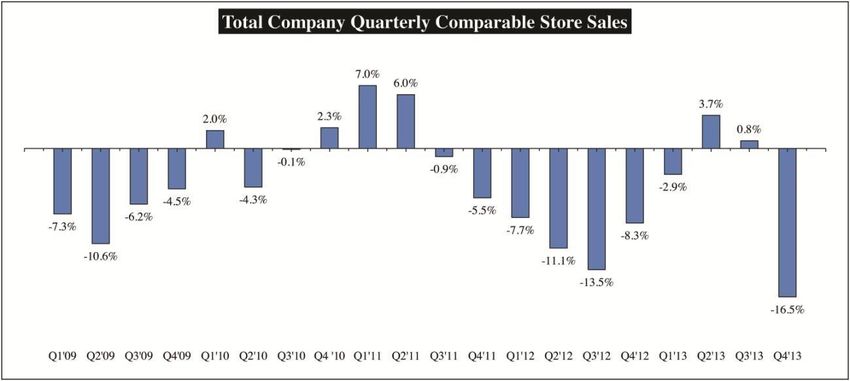

Overall, the financials of WTSL paint a very mixed picture with several positives and negatives. There is

certainly no arguing that over the years, SSS have been volatile, mostly disappointing, and somewhat to

blame for the recent performance of WTSL shares.

Source: WTSL Form 10-K, February 1, 2014

As expected, the negative and declining SSS have led to fairly poor revenue and earnings numbers –

especially over the past several quarters. For the most part revenue growth has been decidedly negative

leading to negative earnings in the form of EBIT, NI, and EBITDA in the company’s two most recent years.

Further, this appears to be somewhat of a trend over the past decade as revenue growth has been

volatile – growing only 2.5% on average. Moreover, gross margins have also been in somewhat of a

decline over the same time period and most recently stood at roughly 25.5% – slightly higher than last

year’s 24.3% but down from the 30%+ range in nearly all the years prior to 2013.

4The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

Meanwhile, despite being negative over the past two years, free cash flow has generally been positive

over the years, growing an average of roughly 23% per year. Furthermore, the same is true for operating

cash flow, which has expanded at an average of greater than 30% per year over the past decade (but

was also negative the last two years). Overall, these are fairly positive for the future of the company,

especially considering the fact that the dismal performance in FYE 2012 was aided mostly by a $71

million increase in the company’s valuation allowance against their deferred tax assets which was seen

in a $43 million increase in the provision for income taxes. In this instance, management concluded that

“it was more likely than not that they would not realize their net deferred tax assets.”4 It should be

noted that changing a valuation allowance is one way that management can potentially manipulate a

company’s earnings so it is necessary to consider that and keep an eye on future instances going

forward. To be clear, I am not saying management is manipulating earnings, but simply pointing out that

valuation allowances are one tool that could be used to that end. Also, in the same year, an asset

impairment charge of $27 million (nearly 440% more than the prior year’s $5 million charge) further

compounded the company’s troubles.

Despite the company’s recent $27 million convertible bond offering, WTSL does not have any other debt

on their balance sheet and has sufficient cash on hand to continue with their turnaround strategy. In

fact, management has stated that it expects net capex to be in the range of $10.5 million and $11.5

million in 2014, which is about half of the amount that has historically been spent on capex each year.

Additionally, the company’s decision to raise capital through a convertible bond offering rather than

through a straight debt or equity financing should be viewed as a positive one for investors as it is

essentially a bond with a stock option hidden inside should the company do well, which I believe it will.

The convertible bonds pay an interest rate of 6% and mature in March 2017; and are convertible at a

price of $1.84 per share.

Although WTSL’s balance sheet indicates decreasing current and quick ratios, both levels are currently

over 1, and will likely be brought closer to their longer-term averages of 2.9 and 2.4, respectively, on

account of both increased cash positions (from the convertible bond offering) as well as through better

inventory management. By working closely with store operations management and merchandise buyers,

WTSL’s teams of planners and allocators will better manage inventory levels and coordinate the

allocation of merchandise to each store. The company utilizes both merchandise planning software and

size optimization software to further ensure proper planning and allocations across their stores.

Considering the fact that WTSL’s earnings and cash flow were both negative in their most recent periods,

it is most appropriate to look at both the P/S and P/B ratios, with the greater emphasis on the P/S ratio.

Over the years, WTSL’s P/S ratio has declined for the most part and currently sits at a 10-year low – as

does its share price. As such, it is important to note that sales are eventually expected to pick up as

economic activity returns to normal and pent-up demand following last quarter’s harsh weather

conditions are met. Furthermore, the company’s P/B ratio is currently lower than its 10-year average

(1.5 vs. 2.4) and should also be seen as an opportunity. Moreover, it should be noted that when

5The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

compared to their industry averages, both of these metrics are significantly less, thus indicating possible

undervaluation. However, it should not be discounted that shares of WTSL are extremely low –

especially compared to their historical trading range. Oftentimes, stocks that are cheap are cheap for a

reason. In this case, a lot of WTSL’s fate rests on the economy and consumer spending, as well as

management’s ability to fully execute on their turnaround strategy. It is for these reasons that shares of

WTSL are likely trading well below their industry and historical averages. Additionally, despite the recent

declines in gross margins and liquidity ratios (current and quick), WTSL still operates within an

acceptable range when compared to its industry averages.

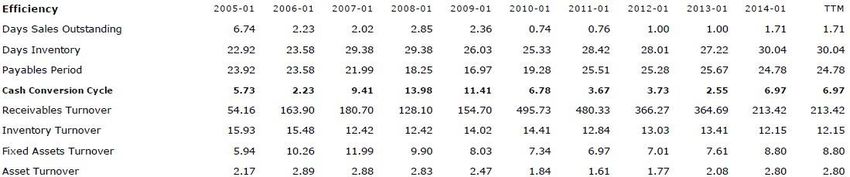

Lastly, the company has been, and continues to be, highly efficient in using its assets to generate sales as

evidenced by their relatively high and consistent turnover ratios and cash conversion cycle (CCC) as

shown below.

Source: Morningstar

ADDITIONAL ISSUES:

Aside from the aforementioned risks associated with WTSL and the retail industry in general, there are a

few other issues that should be considered before investing in shares of the company.

Although not explicitly mentioned earlier, the retail industry – especially teen apparel – is subject to

heavy seasonality issues. For example, for the past three fiscal years, nearly 30% of all sales at WTSL

occurred over the Christmas season (beginning Thanksgiving week and ending the first Saturday after

Christmas) and the back-to-school season (beginning the last week of July and ending during

September). These patterns are likely to continue and should be considered when looking at quarterly

sales and earnings, and making comparisons.

In addition, WTSL’s business could be negatively affected by activist shareholders, such as the Clinton

Group who currently owns over 7% of shares outstanding, and has in the past called for a sale of the

company. Additionally, activist shareholders could advocate for certain corporate governance and

6The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

strategic changes at the company (see: Bill Ackman and JCP) that could negatively impact existing

shareholders. However, anti-takeover provisions within the company’s charter documents (as well as

Delaware laws) might discourage or delay any acquisition attempts. One such measure permits the

Board of Directors to designate and issue (without stockholder approval) up to 2,000,000 shares of

preferred stock with voting, conversion, and other rights and preferences that could adversely affect the

voting power of existing shareholders of WTSL’s common stock.

CONCLUSION:

The future of WTSL is heavily dependent on management’s ability to properly execute on their

turnaround strategy, as well as their ability to cater to their target market’s needs and wants going

forward. The apparel industry is a very tough market to operate in – especially in the female teenager

segment. In addition, high levels of unemployment (particularly among teens) are likely to improve over

time, and will ultimately translate into increased spending. Moreover, the recent weakness over the

winter months due to the harsh weather should abate and give way to stronger sales as consumer

spending catches up with pent-up demand. Despite the obvious challenges, I have confidence in the

management team at WTSL to navigate the tough waters of teen apparel, and therefore see shares of

the company as undervalued and poised for growth in upcoming quarters.

Sources

1 Piper Jaffray. “Taking Stock With Teens Survey.” 10 October 2013.

2 Ibid.

3 WTSL Q4 Conference Call Transcript. 21 March 2014.

4 WTSL Form 10-K. 1 February 2014. Page 33.

7The Wet Seal, Inc. (WTSL)

Rating: BUY

Capable Management Team Should Send Shares Higher

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself,

and it expresses my own opinions. I am not receiving compensation for it, and I have no business relationship with any company whose stock is

mentioned in the article.

Disclaimer:

The information contained herein is not intended to be investment advice and does not constitute any form of invitation or inducement by Michael Maggi,

CFA and Money by Maggi to engage in investment activity. Neither the information nor any opinion expressed constitutes a solicitation for the purchase

or sale of any security. Securities, financial instruments, strategies, or commentary mentioned herein may not be suitable for all investors and this

material is not intended for any specific investor and does not take into account an investor’s particular investment objectives, financial situations or

needs. Any opinions expressed herein are given in good faith, are subject to change without notice, and are only current as of the stated date of their

issue. Prices, values, or income from any securities or investments mentioned in this report may fluctuate, and an investor may, upon selling an

investment lose a portion of, or the entire principal amount invested. Past performance is no guarantee of future results. Before acting on any

recommendation in this material, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

This report may contain certain forward-looking statements and information, as defined within the meaning of Section 27A of the Securities Act of 1933

and Section 21E of the Securities Exchange Act of 1934, and is subject to the Safe Harbor created by those sections. This material contains statements

about expected future events and/or financial results that are forward-looking in nature and subject to risks and uncertainties. Such forward- looking

statements by definition involve risks, uncertainties and other factors, which may cause the actual results, performance or achievements of mentioned

company to be materially different from the statements made herein.

COMPLIANCE PROCEDURE

Content is researched, written and reviewed on a best-effort basis. This document, article or report is written and authored by Michael Maggi, CFA. An

outsourced research services provider represented by Michael Maggi, CFA, provided Small Cap Specialists, LLC this article or report. However, we are only

human and are prone to make mistakes. If you notice any errors or omissions, please notify us below. Small Cap Specialists, LLC and BrokerBank Securities,

Inc. are not entitled to veto, interfere or alter the articles, documents or report once created and reviewed by the outsourced research provider

represented by Michael Maggi, CFA.

If you wish to have your company covered in more detail by our team, or wish to learn more about our services, please contact us at

admin@smallcapir.com. For any urgent concerns or inquiries, please contact us at admin@smallcapstreet.com.

NO WARRANTY OR LIABILITY ASSUMED

WTSL has not compensated Small Cap Specialists, LLC, BrokerBank Securities, Inc., or Michael Maggi, CFA for the creation or dissemination of this report.

Small Cap Specialists, LLC and BrokerBank Securities, Inc., is not responsible for any error which may be occasioned at the time of printing of this

document or any error, mistake or shortcoming. Small Cap Specialists, LLC and BrokerBank Securities, Inc. do not hold any positions in WTSL. No liability is

accepted by Small Cap Specialists, LLC and BrokerBank Securities, Inc.

whatsoever for any direct, indirect or consequential loss arising from the use of this document. Small Cap Specialists, LLC and BrokerBank Securities, Inc.

expressly disclaims any fiduciary responsibility or liability for any consequences, financial or otherwise arising from any reliance placed on the information

in this document. Small Cap Specialists, LLC and BrokerBank Securities, Inc. do not (1) guarantee the accuracy, timeliness, completeness or correct

sequencing of the information, or (2) warrant any results from use of the information. The included information is subject to change without notice.

Small Cap Specialists, LLC is the party responsible for hosting the full analyst report. BrokerBank Securities in the party responsible for issuing the press

release and Michael Maggi, CFA, is the author of research report. Small Cap Specialists, LLC has compensated Michael Maggi, CFA two hundred dollars and

fifty dollars for the right to disseminate this report. BrokerBank Securities has been compensated one hundred dollars to issue press release by Small Cap

Specialists, LLC. Information in this release is fact checked and produced on a best efforts basis by Michael Maggi, CFA.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

8You can also read