Tulsi Tanti - Suzlon's Green Warrior

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ecch: 310-286-1

Dr Dileep Saptarshi London Business School REF: CS-10-009

Date: 2008

Tulsi Tanti – Suzlon’s Green Warrior

Suzlon Energy Ltd. had recently completed two European acquisitions, Hansen

Transmissions (Belgium) and RE Power (Germany). Both were completed under

competitive bidding conditions, and many felt that this had driven the price up for the deals.

These were the largest purchases by an Indian company in Belgium and Germany

respectively. Would these acquisitions generate value and help take the company forward

in its plans to dominate the renewable energy generation industry?

Background

Tulsi Tanti started a textile business in Gujarat (India) in the 80’s when the economy was

booming. The business however soon took a beating because the rising cost of power and

its erratic supply drastically affected production and profits. This compelled Tanti to look for

an alternative supply of power. He secured two small capacity wind turbine generators to

produce captive electricity for his textile mill. This move was not appreciated by many of

his associates who thought of it as an avoidable expenditure. However, Tanti quickly went

on to acquire the technology and expertise to set up Suzlon Energy Limited, India’s first

home grown wind technology company. Today, the company is focused on the renewable

energy sector. “This is our core business and we have committed ourselves to grow in it”,

says Tanti.

At the global level, the wind energy industry was delivering roughly 20,000 - 25,000 MW of

electricity per year. At the global level a target had been set at a minimum 20% of energy

This case was prepared by Dr Dileep Saptarshi, MET League of Colleges, Mumbai, India as a basis for classroom

discussion rather than to illustrate either effective or ineffective handling of a management situation. The case study was

supported by the Aditya Birla India Centre at London Business School.

Copyright © 2008 London Business School. All rights reserved. No part of this case study may be reproduced, stored in a

retrieval system, or transmitted in any form or by any means electronic, photocopying, recording or otherwise without written

permission of London Business school.

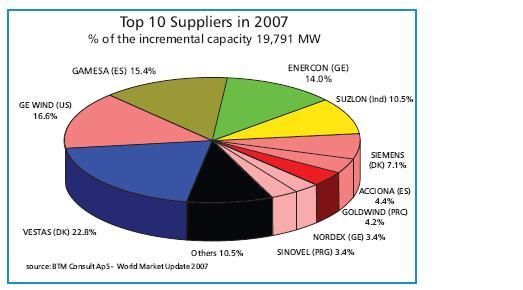

London Business School ecch: to come from renewable sources by 2020. By 2008, the contribution of Wind Energy was only 1%. To achieve the target in 12 years represented a great challenge and also a great opportunity. Source: BTM Consult ApS –World Market Update 2007 The Global Wind Market was growing by 20% to 25% per year. India was 10% of the size of the Global market and also the 4th largest market in the world. Europe was nearly 40% of the size of the total global market, the U.S.A., 20%, China, 15% and the balance was taken up by the rest of the world. The USA and China were large markets with the highest growth potential. In the United States, 26 states had made the Renewable Portfolio Standard (RPS) mandatory. This system used market tools to ensure that a certain percentage of electricity generated in a state came from renewable energy sources. The other support mechanism to the wind energy industry in the U.S.A. was the “production tax” concept. Both these popular measures leveraged the growth of the wind energy market in the U.S.A. to make it one of the fastest growing markets. The Chinese market was also growing very aggressively, with an ambitious target to be achieved by 2020 where 20% of their requirement would come from renewable sources of energy. Thus worldwide, the market for wind energy was growing rapidly. The major wind power installations were concentrated in USA, Europe, India and China, which accounted for 93% of the cumulative installed capacity. The global installed capacity was 94GW in 2008. It was expected to grow to 240GW by 2012. Copyright © 2008 London Business School 2

London Business School ecch: Global Wind Energy Capacity expected to touch 240GW by 2012. Source: WWEA, GWEC, IIFL Research M&A as a Technology Development Strategy The Mergers and Acquisitions process deployed by Suzlon was a part of their growth strategy, aimed at developing leadership in technology. In this context an overall mapping of the potential assets available for acquisition in the wind power industry was carried out. Two likely candidates, The Belgian company, Hansen Transmissions, in the gearbox industry, and RE Power, a leading wind turbine company in Germany were identified as important strategic assets in the supply chain. The gear box was a key component in the turbine product line and reliability of the component is of utmost importance. It was decided internally that the green field expansion route was not viable, as it took about ten years to develop the product and test its reliability. So Hansen, the second largest gearbox company in the world, was the best available asset for Suzlon’s acquisition strategy. The second target company was RE Power based in Germany. It was a turbine manufacturing company which had a strong base of design teams and R&D engineers in turbine manufacturing. They had proven expertise and had developed the most successful product in the wind industry (the 5MW machine) which was the largest turbine in the world. Suzlon’s vision in acquiring Hansen and RE Power was to make a quantum leap in technical competencies and pole–vault its way into the technological leaders in the industry. In the gearbox industry there were very few companies to choose from. Hansen was the second largest company and the third company was Moventas, in Finland, but was a smaller organization. However, others had the same idea, there were four or five other bidders potentially interested in Hansen. Hansen Transmissions was owned by the Allianze Group - the German Insurance Company. To lay the foundation for acquiring the company, Tanti met the private equity investors of Hansen twice before acquisition. He also cultivated good relations with the management of Hansen. In the final bidding process four players remained. Ultimately, based on Suzlon’s ability and due to their continuous aggressive follow-up, they were successful in acquiring Hansen. In the end, the deal was a bit expensive and some felt that Suzlon ended up perhaps. But Tanti felt that this Copyright © 2008 London Business School 3

London Business School ecch:

acquisition of Hansen, for 371 million Euros, was an important necessary asset, in line with

Suzlon’s vision and growth strategy.

RE Power was a publicly listed company. French utility Areva, a French government

company owned 30% stock, Martifier, a Portuguese company owned 23% and the rest of

the stock was held by the public. Suzlon targeted it as it was the best available technology

asset and it complemented Suzlon’s market position, product portfolio and customer profile.

In the bidding process, Areva was already bidding for RE Power before Suzlon. Therefore

Suzlon had to rush in as a competitive bidder. There were multiple rounds of the bidding

process and finally with the good relations established with Areva, Suzlon was able to

convince them how RE Power was more important to Suzlon. It was a friendly deal closure

and Areva agreed to sell their stock to Suzlon after one year. Suzlon also acquired the

stock held by Martifier. After a prolonged prolonged bidding process of a year, Suzlon

acquired RE Power for $1.8 billion.

The Rationale

The growth of Suzlon on a year on year basis was in the range of 50-80%. For wind

turbine generators, (WTG’S) the supply chain is a bottleneck. Within the supply chain, the

gear box is the key bottleneck component in the wind industry. Thus as Tanti explained,

acquiring Hansen and expanding its capabilities rapidly on a global basis in low cost

geographies like India and China, helped Suzlon in three ways: 1) To get more supplies of

gear boxes. 2) Low costs of gear boxes and 3) Secured long term availability of supply

chain. At the same time, for investors at Hansen, it was a good investment opportunity, in

terms of capacity expansion. After the acquisition, the target was set to increase the

capacity from 3600MW to 15,000MW. The Belgium plant capacity was doubled from

3600MW to 7300MW. The new capacity which was developed in India gave 5000 MW and

another 3000 MW was installed in China. So the overall capacity was nearly expanded to

15,000 MW of capacity, which was lucrative from the investment point of view.

Suzlon added value to RE Power by providing it the much needed supply chain for its

expansion plans. Thus after acquiring RE Power, Suzlon doubled the growth of RE Power.

RE Power’s low margins were increased by the economies of the improved supply chain

provided by Suzlon. Therefore, both the increased rate of growth and the improved

margins resulted in excellent value creation for the stakeholders of the company. With

these two acquisitions, Tanti felt that Suzlon was closer than ever to delivering an end to

end integrated business model.

Integrated Business Model

Source: Suzlon Energy Ltd.

Copyright © 2008 London Business School 4London Business School ecch: Valuation &Due Diligence Hansen was not a listed company, and the valuation depended on the seller’s demand. The seller’s initial expectation was 400 million Euros, but after negotiation the deal was concluded at 371 million Euros. In case of RE Power, since it was a listed company, there was a prolonged bidding process. Areva, the French Government utility, started the bidding process, several rounds of which finally determined the valuation of RE Power at $1.8 billion. But before acquiring the target, Suzlon had conducted a comprehensive and vigorous due diligence process which involved technical, legal and commercial aspects. A series of meetings with the RE Power management were also carried out by Suzlon’s team to find out and understand the management team, their strengths and weaknesses and their vision for growth. Even before the bidding process, Tanti went ahead and met the shareholders of Areva and Martifier. By doing so, Suzlon was trying to understand the shareholders and their expectations. Suzlon made all possible efforts to convince the Areva management to agree to the RE Power acquisition. In case of the Hansen buyout, Suzlon’s finance team had 15 days to arrange for finance. It was a challenge to not only arrange funds in such a short time but to also transfer them while coordinating with a consortium of four leading global banks. Suzlon raised these funds in the international market on the strength of its balance sheet. In case of RE Power, it was an equity purchase and not a buyout. Suzlon had to purchase the majority equity stock of RE Power for acquiring it. The first thing Suzlon did was to acquire the 23% stake owned by the Portuguese Martifier group before putting its bid in the stock market. This was done with the condition that the payment would be made after two years. It then proceeded to acquire another 30% stock from the open market. During this process Suzlon convinced Areva and they agreed to sell their stock after 1 year. Therefore in a nutshell, Suzlon has acquired RE Power Company in installments. It was a very friendly deal closure executed without hurting any of the existing shareholders. Post Merger Integration “From the outset, we said that Hansen’s existing customers are more important. They helped Hansen grow, not us”. –Tulsi Tanti- Chairman and Managing Director, Suzlon Energy Ltd. After acquisition Suzlon decided to keep Hansen as a separate entity. In contrast RE Power was to be integrated into Suzlon. Before the acquisition, 100% of Hansen’s supplies were allocated to Suzlon’s competitors. In the wind energy business there were huge opportunities for everyone and very cordial relations among the top manufacturers. Suzlon saw no point in jeopardizing sales from these customers. Out of the top five companies in the world, the top three were buying their gear boxes from Hansen. First and foremost, Suzlon expanded Hansen’s capacity, so it could serve its original customers better on a Copyright © 2008 London Business School 5

London Business School ecch: priority basis. The remaining gear boxes would be available to service RE Power and Suzlon’s increased capacities. Thus there existed a unique relationship between Suzlon and Hansen. A new supervisory board was created above the management team of Hansen to manage the company independently. Moreover, Suzlon created a very good value proposition by listing Hansen on the London Stock Exchange. Suzlon had acquired Hansen for 371million Euros. Within 18 months, with the execution of strong growth plans and with listing on the London Stock Exchange, its market capitalization rose to 2.5 billion Euros. In the case of RE Power, Suzlon initially got only 66% stock. The balance stock was due to come from Martifier by 2009. Suzlon and RE Power were to be integrated as one organization after acquiring the Martifier stock and with the completion of some legal formalities. RE Power’s profits had started growing as a result of its expanding capacities and increased margins due to supply of low cost components by Suzlon. Augmenting the Management Teams After the acquisition of RE Power, the strategy adopted by Suzlon was not to merge their management teams, since both of them were in different geographies. The German team took care of the European markets and the Suzlon team after the Asian & US markets. While Suzlon had kept the same management team at RE Power It however increased its bandwidth to take up the extra load. They added two more European managers to efficiently take care of the larger size of business. Earlier there was a three member German management team. This was increased to five members by the addition of two more Danish members. This was done in order to make it a global management team. Both these new team members were from the wind industry. They were experienced and knowledgeable persons from Denmark and earlier they were working for Suzlon. They knew Suzlon’s strategy, future plans and work culture very well and thus they could help to integrate the RE Power team into Suzlon. No manager was transferred from India to Germany. Suzlon created a supervisory board to oversee the functioning of the company. Mr Tanti himself was one of the directors but without much control at the board level. In case of Hansen, after the acquisition, the same management team was retained, except for one change made by Suzlon. The existing CEO was promoted to the board level and a new CEO was selected from the existing team. No manager was transferred from India to Belgium. Suzlon strongly believed in local management. It chose a CEO from within Hansen, a person who had been working with Hansen for the last 25 years. The four member management team was also expanded to a seven to take up additional responsibility in an efficient manner. Dealing with the Broader Set of Stakeholders In case of RE Power, since it was a public listed company there was immediate attention from the shareholders, the media and also from the government on news of the acquisition. This company was partly owned by French utility Areva which is owned by the French government. Copyright © 2008 London Business School 6

London Business School ecch: Suzlon took the lead initially to discuss certain issues with the Indian Government, particularly with the Commerce and Finance Ministries, to understand the relationship of India with France and Germany. Then Tanti himself went to meet key people in the German government. He explained to them how he saw good value and synergy benefits for both countries. India had the market and RE Power, the technology. So if the two companies were integrated properly, it would create great value for both countries in line with Suzlon’s prime objectives. Suzlon also promised to protect the jobs of employees (i.e. no retrenchment of existing employees), expand the business and be a part of the renewable growth agenda of Germany. Thus, there was a positive reaction from the German government as they were convinced by the vision and the growth agenda of Suzlon Ltd. Since the French government was the owner of RE Power, Suzlon was not able to deal with them directly. Before submitting the bid, Tanti himself went to five different media houses, to put forward his vision for the deal. This gave a very strong message to the shareholders and also created a level of comfort amongst all stakeholders. Reaction of Stock Markets after Acquisition The immediate reaction of the stock market to the announcement of the Hansen deal was not positive. However, after 18 months, when it was listed on London Stock Exchange, it was valued at 2.5 billion Euros. This showed that there was good all-round acceptance of this acquisition. In the initial stages the market feared that Suzlon had overpaid. But after seeing the synergy and its growth plans, the market understood and reacted positively. In case of RE Power as well, initially when Suzlon had submitted the bid, the immediate reaction in the market was negative. Since it was not known at what price Suzlon would buy this company, many felt concerned that Suzlon would continue to bid higher and higher for RE Power and create more debt by leveraging its balance sheet. They reacted positively when Suzlon announced that the RE Power deal was concluded in a friendly manner for a sum of $1.8 billion, to be paid in installments. What have the Deals done for Suzlon? Suzlon Energy Limited planned to expand Hansen’s capacity from 7,300 MW to 14,300 MW through a combination of brownfield and greenfield expansions. It completed the brownfield expansion at its Belgian factory from 3,600MW as at end FY07 to 7,300MW. It set up greenfield plants in India and China, which would expand its production capacity to 14,300 MW by FY2012. This expansion, estimated to cost Rs 41 billion, (650m Euros), was to be funded partly by proceeds of Hansen’s recent IPO on the London Stock Exchange and partly by debt. The robust demand for gearboxes, clubbed with timely expansion, put Hansen in a sweet spot. At the gross margin of. 50,000 Euros/MW, the Belgian factory’s payback period was predicted to be less than three years. Suzlon Energy ltd. planned to run Hansen as an independent entity and allow it to service its customers such as Vestas, Gamesa – which were Suzlon’s competitors in the WTG market. Since Suzlon had a firm supply contract for Copyright © 2008 London Business School 7

London Business School ecch: gearboxes, this strategy would allow Hansen to maximize value from its production in a supply-constrained market. As Suzlon expanded capacity in India and China, Hansen would supply part of its requirements, thereby shielding Suzlon from “tightness” in the supply chain. Suzlon identified two ways to improve RE Power’s operating metrics: supplying gearboxes from Hansen’s facilities, and supplying castings and forgings from Suzlon’s integrated manufacturing units in India. These initiatives could considerably ease margin pressure on RE Power. Tanti also reckoned that Hansen - Suzlon - RE Power together purchased bearings worth $200 million every year; a figure that was expected to go up to $600 million given their planned expansions. Tanti clubbed these orders together, took the CEO of Hansen along with him, and met the global CEO of SKF Bearings, and persuaded him to set up dedicated plants in Baroda and Chennai to meet his bearing needs. Before acquisition, RE Power found it difficult to grow on its own due to supply chain bottlenecks. Suzlon provided it with a ready solution to grow fast. It started to feed components to RE Power from its vertically integrated manufacturing facilities and well- oiled supply chain. Hence RE Power achieved a growth of 100% as compared to the previous year only due to the strong backing of Suzlon. At the time of acquisition, the EBIT margin was 2-3 %. This margin was projected to increase to 6% + because of the supply of low cost components, the economies of scale, and the addition of Suzlon’s brand value to RE Power. When Suzlon acquired RE Power its value was $1.8 b and then its market capitalisation rose to $3 billion. But it continued to pay money (in instalments) for the earlier valuation at the rate of $1.8b. Postscript By 2008 Suzlon Energy was emerging as a global giant in the wind energy market with a market capitalization of $10 billion. It had a successful IPO launch in October 2005. Since then in three years Suzlon grew by leaps and bounds at an astonishing rate of 126 percent per annum. In comparison with its competitors, the company has never incurred losses since its inception. Largely as a consequence of the twin acquisitions of RE Power and Hansen, the company had a new organizational identity where out of its 13,000 employees; more than 3000 were not of Indian origin. The fundamental shift was the transition from a small number of key people having direct control over everything in the company to an appropriate management structure that reflected the global nature of the business. Copyright © 2008 London Business School 8

London Business School ecch:

Exhibits

No 1: Suzlon’s Strategy, Mission and Vision

Suzlon: Strategy

Suzlon’s Vision Suzlon’s Mission

• Technology leadership in the Wind Energy • To contribute to sustainable development of

Space the Wind Energy sector through an integrated

• Be among the top 3 wind companies in all product design and manufacturing strategy

the key markets of the World • To increase the contribution of wind power to

• Be the global leader in providing profitable meet global energy demand

end-to-end wind power solutions • To create a better, greener tomorrow for all

• Be the “Stakeholders’ Choice” Company

Strategy

Focus on

Improving Growth

High growth

cost efficiency acceleration

markets

R&D • Strategic focus on

and Vertical integration customer needs

Innovation • End-to-end solutions

30

Source: Suzlon Energy Ltd

Copyright © 2008 London Business School 9London Business School ecch:

No 2: Structure of Suzlon’s Management Team

6 Experienced

management team &

strong employee base

Robust Employee Growth with

Experienced Top Management Team

Increasing International Mix

Mr.Tulsi Tanti,

Chairman and MD,

Founder and Promoter

Board Members 4419

2713

Group Management Team

9314

Mr.Toine van Megen 7764

CEO

Mr.Sumant Sinha Mr. T. Pradeep Kumar Mr. R. Sridhar FY07 FY08

COO CTO CMO Domestic International

Mr.Pascal de Roeck Mr.Wim Dufourne

CFO * CHRO

CLO

* Mr. Kirti Vagadia is the interim CFO

28

Source: Suzlon Energy Ltd

Copyright © 2008 London Business School 10London Business School ecch:

No 3: Capacity Expansion plan of Suzlon

Suzlon capacity expansion

plans

Suzlon’s Expansion Plans (1)

(1)

Panel facility in Tamilnadu, India @

@ WTG & Rotor Blade Unit in Foundry & machining unit in

Karnataka, India@

@ Tamil Nadu, India##

FY08 4Q FY09 1Q 2Q 3Q Future

Composites testing centre Generator facility in Forging & machining Gearbox facilities in Tower Unit in

in Gujarat, India Tamil Nadu, India@ @ unit in Gujarat, India## India and China Gujarat, India@

@

@ Capex planned for integrated wind turbine manufacturing facility is ~Rs.1,500 Crores

# Capex planned for Forging, Foundry and Machining units is ~Rs.1,100 Crores

Suzlon Planned Capacity

Suzlon (2) 5,700 Hansen (3) REpower (4) 1,700

14,300

1,250

Gearbox MW

7,300

MW

2,700

3,600 MW

Note: FY07/FY08 FY09 FY07 FY08 FY12 CY07 CY08

(1) Indicates expected date of commencement of operations

(2) Integrated capacity.

(3) Wind gear box capacity

(4) Suzlon Group controls or influences, either directly or through voting pool agreements, approximately 89% of the votes in REpower 31

Source: Suzlon Energy Ltd

No 4: Suzlon Balance Sheet

Balance sheet (Rs crore)

Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05 Mar ' 04

Sources of funds

Owner's fund

Equity share capital 299.39 287.76 287.53 86.92 24.35

Share application

money - 0.02 - - -

Preference share

capital - - 15 115 15

Copyright © 2008 London Business School 11London Business School ecch: Reserves & surplus 6,648.27 3,425.53 2,519.72 727.65 377.48 Loan funds Secured loans 672.26 771.78 276.61 285.46 172.38 Unsecured loans 2,412.48 364.86 58.76 37.08 48.28 Total 10,032.40 4,849.95 3,157.62 1,252.11 637.49 Uses of funds Fixed assets Gross block 779.2 567.04 400.41 217.88 159.09 Less : revaluation reserve - - - - - Less : accumulated depreciation 266.98 178.57 104.73 57.61 23.77 Net block 512.22 388.47 295.68 160.27 135.31 Capital work-in- progress 134.63 92.71 76.25 17.93 12.43 Investments 4,919.48 805.26 292.74 126.01 53.33 Net current assets Current assets, loans & advances 7,048.40 5,068.61 3,754.36 1,665.88 821.11 Less : current liabilities & provisions 2,582.33 1,505.10 1,261.41 717.97 384.75 Total net current assets 4,466.07 3,563.51 2,492.95 947.91 436.36 Miscellaneous expenses not written - - - - 0.06 Total 10,032.40 4,849.95 3,157.62 1,252.11 637.49 Notes: Book value of unquoted investments 4,919.48 805.26 292.74 126.01 52.96 Market value of quoted investments - - - - 0.37 Contingent liabilities 7,584.65 3,607.72 251.63 78.61 54.24 Number of equity sharesoutstanding (Lacs) 14969.34 2877.65 2875.31 869.23 243.48 Source: http://money.rediff.com/money/jsp/balancesheet.jsp?companyCode=15130070 Copyright © 2008 London Business School 12

London Business School ecch:

No 5: Suzlon Cash Flow Statement

(Rs

Cash flow crore)

Mar ' Mar '

Mar ' 08 Mar ' 07 Mar ' 06 05 04

Profit before tax 1,506.96 1,119.58 902.66 392.45 122.03

Net cash flow-operating

activity 484.8 747.35 -389.78 63.23 78.48

Net cash used in investing - - - -

activity 3,946.55 1,165.54 -480.41 252.67 182.53

Net cash used in fin.

activity 3,985.86 453.34 1,098.23 217.29 112.17

Net inc/dec in cash and

equivlnt 524.11 35.15 228.04 27.84 8.12

Cash and equivalnt begin

of year 351.39 316.24 88.2 60.36 52.24

Cash and equivalnt end of

year 875.5 351.39 316.24 88.2 60.36

Source: http://money.rediff.com/money/jsp/cashflow.jsp?companyCode=15130070

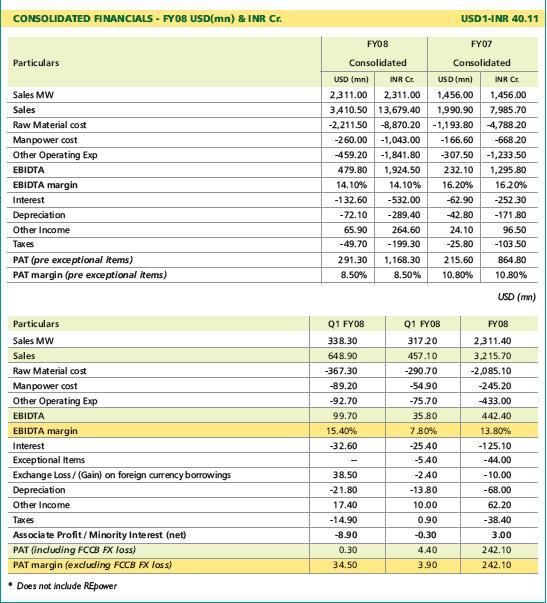

Copyright © 2008 London Business School 13London Business School ecch: No 6: Consolidated Financial Statement Source: Suzlon Energy Ltd Copyright © 2008 London Business School 14

You can also read