UK Commercial Property REIT (UKCM) - February 2021 Year End 2020 - Results Presentation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

February 2021 UK Commercial Property REIT (UKCM) Year End 2020 – Results Presentation Presented by: - Will Fulton, ASI - Graeme McDonald, ASI Picture – Ocado, Hatfield Aberdeen Standard Investments (‘ASI’)

Agenda 01. Overview 02. The Market 03. Financial Highlights 04. Portfolio and Performance 05. Concluding Remarks 1

Overview

UK Commercial Property REIT (UKCM) owns a diversified portfolio of UK real estate assets and aims to deliver an attractive level of

income together with the potential for capital and income growth

The Company has delivered robust returns in an unprecedented economic environment

Asset allocation firmly weighted to the industrial sector with a 58% exposure

Successful asset management has improved occupancy - notably letting Lutterworth on a 15 year lease which reduced void by 35%

Rent collection stronger than anticipated, and has improved each quarter since Spring 2020

Strong balance sheet with considerable financial resources available to invest and low levels of gearing has allowed the Company to pay

out a dividend throughout this pandemic*

Continued Environmental Social Governance (ESG) focus with an EPRA** “Gold” rating for Best Practice

Source: Aberdeen Standard Investments

(* please refer to 31 December 2020 NAV statement for more details; **The European Public Real Estate Association)

2 Past performance is not a guide to future results. The value of investments, and the income

from them, can go down as well as up and you may get back less than the amount invested

Agenda 01. Overview 02. The Market 03. Financial Highlights 04. Portfolio and Performance 05. Concluding Remarks 3

UK Forecasting

A renewed sense of optimism moving into 2021, with a no-deal Brexit averted and a vaccine roll out, is likely to be tempered, at least

initially, by the latest national lockdown

Retail and Leisure remain under significant pressure with the exception of supermarkets which are highly resilient

Industrial sector thriving and set to continue to benefit from accelerating structural changes

Continued measured-risk approach to the portfolio with income sustainability driving returns

Lower for longer interest rate expectations remain in place – supportive of real estate pricing

4

UKCM sector weightings against ASI sub-sector forecast returns

78% of the portfolio is in sectors forecast to outperform

Source: Aberdeen Standard Investments, December 2020. No assumptions around future performance should be made

Forecasts are not a reliable indicator of future results and there can be no guarantee that

5 these will be achieved

Logistics market outlook post-Covid-19

Mixed short-term signals but powerful structural drivers in the long-term

Short-term Economy Demand Supply Investment Relative Returns

performance

indicators

(1-2 years)

Volatile recovery expected E-commerce & groceries up Vacancy being absorbed Massive demand Outperform All Property

Online retail trends accelerated 5 years Investment considerations

Existing supply chains need to adapt

Major investment required by retailers • Intense pricing pressures. We anticipate

Urban fringe and mid-box critical significant volumes of capital to target this

E-commerce sector over the next decade

Long-term Long supply chains carry excessive risk • Urban fringe and mid-box should be most

Performance Labour cost arbitrage less pronounced relevant parts of the market

drivers Automation and robotics game-changing

Boost for major consumption markets • Fierce competition between operators – be

(next decade) Near-shoring certain your tenant is future-proof

• Maximise ESG potential to ensure

Supply chain risk has increased last 10yrs efficiency and employee welfare

Switch focus towards certainty vs. speed

Expected to drive storage requirements • Beware regulation – particularly urban

Will be very cost-sensitive – low rents key

Inventory building

Source: Aberdeen Standard Investments, January 2021

Short term indicators are relative to last 5 year trend, relative returns indicator based on three year outlook vs Global All Property

Forecasts offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed

6 and actual events or results may differ material.

Agenda 01. Overview 02. The Market 03. Financial Highlights 04. Portfolio and Performance 05. Concluding Remarks 7

Financial highlights as at 31 December 2020

Strong Balance Sheet, Low Leverage and Significant Resources

Current combined debt positon

Overall Debt Position

Total debt available £350m

86.7p 2.7p Remaining available £150m

89.8p 3.5p

Weighted Average

8.2 years

NAV per share EPRA earnings Period to maturity

per share

All in rate 2.88% p.a

The combined facilities provide:

• Low LTV / risk

Net: 6.4% • Low cost

£218m* Gross: 15.1% • Good duration

£130m

N: 14.7%

• Flexibility

G: 17.7%

Capital available

to invest

Gearing • Significant covenant headroom

Source Aberdeen Standard Investments, December 2020. Light blue figures represent position

Source Aberdeen Standard Investments, December 2020

at December 2019 * Inclusive of £150m RCF

Past performance is not a guide to future results

8

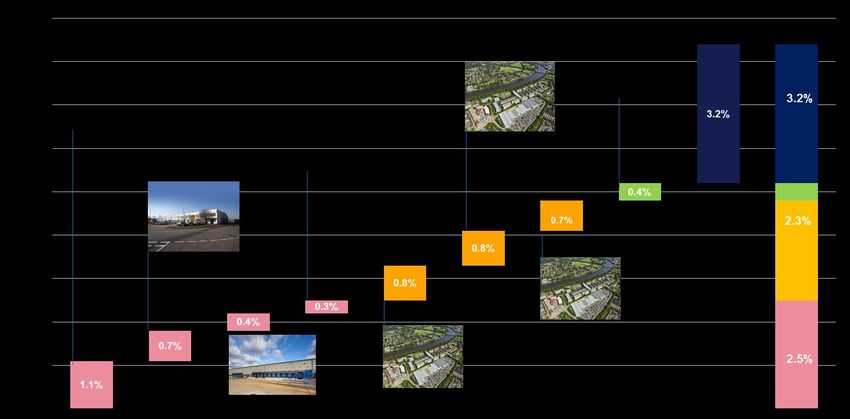

Financial highlights - NAV

NAV movement year to 31 December 2020

Source: Aberdeen Standard Investments, December 2020

Past performance is not a guide to future results. The value of investments, and the income from

9 them, can go down as well as up and you may get back less than the amount investedFinancial highlights – EPRA Earnings

EPRA Earnings movement year to 31 December 2020

Source: Aberdeen Standard Investments, December 2020

Past performance is not a guide to future results. The value of investments, and the income from

10 them, can go down as well as up and you may get back less than the amount investedAgenda 01. Overview 02. The Market 03. Financial Highlights 04. Portfolio and Performance 05. Concluding Remarks 11

Strategy

To provide shareholders with an attractive level of income with the potential for capital and income growth from

investing in a diversified portfolio of UK commercial property

• Continued focus on rent collection and reducing

Asset •

arrears

Drive down void level

• Enhance lease terms

Management • Engage with retail tenants to create sustainable

lease structures

• Focus on “future fit” modern economy and goods &

Accretive •

services distribution

Continue to explore strong operational opportunities in the

Acquisitions •

•

alternatives sector

Ability to repeat durable income streams

Lot Size target £20-50m

• Exit assets with significant capex requirement

Selective •

and limited return prospects

Selectively reduce retail and leisure exposure

Selling

12ESG Performance and Reporting GRESB 2020 • UKCM 2nd in UK Diversified (listed) peer group • Overall score of 67/100; Two Star rating Trust 2020 ESG Performance Headlines (EPRA sBPR) • EPRA Gold rating September 2020 • 100% of electricity sourced from renewable sources • 100% diversion of waste from landfill Current initiatives • Improve energy data collection at single let assets • Ongoing Solar PV feasibility at several industrial and retail assets. • Investigating potential for biodiversity projects including beehives • Installing enhanced bicycle facilities • Community activities at large format retail / leisure once practicable 13

Portfolio Structure

Portfolio sector weighting (by Market Value) UKCM sector breakdown

Urban Non - Urban

Industrial

60%

Rest of UK (light

Office London green SE)

Source: Aberdeen Standard Investments, Dec ember 2020; MSCI Balanced Quarterly & Monthly benchmark, September 2020

Retail Retail Warehousing High Street (light

Capital value by geography

orange supermarket)

40% 37%

35%

30%

25%

19%

20%

15%

9% 9% 8% 8% Other Cinema Anchored Hotel/Student

10%

5%

5% 5%

Leisure Accommodation

0%

London

West Midlands

Scotland

Yorks and Humber

South West

North East

East Midlands

South East

Source: Aberdeen Standard Investments, December 2020 Source: Aberdeen Standard Investments, Dec ember 2020

14Portfolio Performance to 31 December 2020

UKCM direct portfolio total return outperforming Benchmark

Exposure Total return Income return Capital return

H2 2020

(%) (%) (%) (%)

Portfolio Benchmark Portfolio Benchmark Portfolio Benchmark

Industrial 58 10.3 8.9 1.7 2.2 8.5 6.6

Office 14 -2.5 0.3 2.2 2.2 -4.6 -1.8

Retail 17 -0.8 -1.6 1.9 3.2 -2.7 -4.7

Other (inc. Leisure) 11 -4.5 -0.2 -0.8 2.5 -3.7 -2.7

Total portfolio 100 4.6 2.6 1.5 2.5 3.1 0.1

Source: UKCM, Aberdeen Standard Investments, December 2020 - Benchmark: MSCI UK Balanced Portfolios benchmark to 30 September 2020 + 3 months MSCI UK Balanced Funds

Monthly index to 31 December 2020 . UKCM Figures are gross of Investment management fees, gearing costs and other fund related fees

15

Past performance is not a guide to future results.Rent Collection – Year to 01 January 2021

2020 Rent Collection

Source: Aberdeen Standard Investments, January 2021

Update on 17% Rent Outstanding over the four “COVID”

quarters as at 28/01/2021

Source: Aberdeen Standard Investments, January 2021

16Investment - Sales & Purchases 2020

Sales (5) Purchases (3)

£160m* £74m

£156m

Broadbridge Great Lodge R Park,

1 PBSA, Exeter PBSA, Edinburgh

R Park, Horsham 3 Tunbridge Wells 1 3

• £28m funding • £29.1m funding

• £46.25m** • 5.6% projected NIY • 5.5% projected NIY

• £18.1m

• Ahead of valuation • Strong university • Prime student location

• In line with valuation

• Mitigated short term • Located adjacent to the • High proportion of

• Selling down risk

income risk main campus cluster rooms

retail income

• Construction to • Construction to

complete for 2022/23 complete for 2022/23

academic year M8 Industrial Estate, Glasgow academic year

Eldon House, M8 Interlink Estate •£24.6m

Distribution Portfolio

M8 Industrial Estate, Glasgow •Topped up NIY 5.9%

ASDA Torquay

London•£24.6m Glasgow 2

2 4 •£85.4m

•290,104 sq ft across 20 units

•Topped up NIY 5.9% • £16.6m •Average

•Toppedrent

upofNIY

£5.25 psf

• £40m •290,104 sq ft across 20 units • £25.4m 5.5%

• 290,104 sq ft • NIY 5.25% in •909,030

2021 sq ft

•Crystallized profitrent

•Average fromof £5.25 psf

• Opportunistic & • 15 year income with rent of £5.52 psf

•Average

AM Activity

mitigate void risk indexed reviews

• Strong underlying trade

Source: Aberdeen Standard Investments, January 2021 * Includes Motorpark, Portsmouth, sold for £29.8m in March 2020; ** Less rent guarantee escrow.

17Industrial portfolio: Positive Leasing Activity

Xdock377, Magna Park, Lutterworth

Sector Weighting

• Newly refurbished cross docked facility in a prime

Golden Triangle location

• Let on a new 15 year lease to Armstrong Logistics.

• Agreed a rent of £2.45m per annum

• Mitigated the largest void in the portfolio

Dolphin Industrial Estate, Sunbury on Thames

Sector Occupancy

• High quality multi let urban estate with good

access to the M25

• Let Unit C to Avenue 51 on a 10 year lease with a

break at year 5 for £275,000 pa (£13.00 psf).

• Estate is now fully let and a new rental tone has

been achieved.

• Significant valuation uplift in H2 2020.

Source: Aberdeen Standard Investments,

January 2021

Strategically Positioned – Urban Industrial Engine for Rental Growth

18Portfolio voids (by ERV) – significantly reduced

Ventura Park, Radlett

Remainder all

sectorsLease events over the next 12 months (by annual rent passing)

By rent passing

25 Moorgate,

Compagnie Fruitiere, Gap, Colmore Row,

Dartford Kew Retail Park

UPS, Emerald Park

H Tenens,

Sunbury

Remainder

0.4%Rent bridge

Potential Income Growth

Source: ASI, Dec 2020

Past performance is not a guide to the future. The value of investments and the

21 income from them can fall as well as rise and is not guaranteedAgenda 01. Overview 02. The Market 03. Financial Highlights 04. Portfolio and Performance 05. Concluding Remarks 22

Concluding remarks

UKCM has strong foundations to help it navigate through COVID-19

UKCM continues to have a portfolio aligned to sectors which aim to perform well on a relative basis

given current market conditions – it’s investment focus is firmly on “fit for the future” modern economy

assets

Maintenance of income is a key focus of the Board with a dedicated team at the Investment Manager in

regular contact with tenants

Diversified tenant base helpful in the current environment with a number of large household names

in the top ten such as Ocado and Amazon

The Company has continued to pay a dividend throughout this pandemic and with a further top up

dividend once audited results are announced*.

The Company remains one of the largest diversified REITs with a strong balance sheet, low gearing and

considerable financial resources. Overall UKCM has strong foundations to help it navigate through the

implications of Brexit and COVID-19 and be a beneficiary of the accelerated structural changes taking

place in the UK real estate market.

*(* please refer to 31 December 2020 NAV statement for more details)

Past dividends are not a guide to future dividends

2301

UK Commercial Property REIT

2020 – Results Presentation

Q&A01

UK Commercial Property REIT

2020 – Results Presentation

Data PackUK Commercial Property REIT

Experienced and dedicated fund management team with specialist support

Independent Board

Credit Management Research and

team Strategy team

Monitors financial Lead Manager Global macro

assumptions

health of existing Will Fulton

and prospective Quarterly real

Research / underwriting

tenants estate house view

Deputy Fund Manager

Risk management

Tom Elviss

Development Transactions

team team

Deal structuring Transactions

UKCM Real Estate Team support

Review/ negotiation

of funding David Fleetwood

agreements David Rodger

Sarah MacDougall

Gary Sleator

Finance & Tax

Wider ASI

team

Capabilities

Fund & deal

structuring Multi-Asset Investing

team, Global

Real Estate Finance Management Team

Tax planning Strategy, Global

Graeme McDonald Equity and Fixed

Banking

relationships

Michelle Reid Interest teams

Source: Aberdeen Standard Investments, Dec 20

26Global Performance Signals: Q1 2021

Vaccine offers hope for later in 2021 but first half likely to remain challenging

Performance Current

Outlook Comment

Signals Signal

UK to contract again in Q4 and Q1 after nearly 16% growth in Q3. Until a

Economic

fundamentals vaccine rolled out, lopsided “W” profile to growth expected. Thinness of Brexit

deal to reveal itself over time – financial services remain a concern.

Macro

Margin over bonds Real estate yields drifting outwards where risk has risen; gap narrowing for

securest income. Corp. bond spreads back in line with pre-Covid levels

Monetary policy Emergency cut to 0.1% and an expansion of QE has followed. More QE in

November but vaccine hopes may mean risk of negative rates has faded

Increasing number of segments may already be oversupplied through existing

Supply stock; conversions may offer more hidden supply. But logistics supply arguably

not keeping up with demand, especially in urban areas

Flows of capital Lockdown to hamper recovery in volumes but tentative improvement expected

Real Estate

in H1 2021, although focus of investor demand to remain narrow

Lending Traditional lenders hunkering down and pressured into forbearance; new

lending remains highly constrained with refinancing concerns mounting

Fund flows Flows relatively stable after initial outflows post re-opening. Lockdown could

weaken sentiment; proposed regulatory change a barrier to inflows.

REITs bounced on vaccine news but rental declines are still being priced into

360° view London specialists. Debt fund interest strong, as alternative lenders can

demand healthy margins; may also imply lack of faith in equity component

Sources: MSCI/IPD; Thomson Reuters Eikon; PMA; RCA; CBRE, Investment Association; Aberdeen Standard Investments, January 2021

Key: Trend: Performance signal:

27 Stable Supportive

Upward trend Neutral

Downward trend UnsupportiveIn a low rate environment, lower income yield is evident across asset classes

Real estate yields compare favourably in this environment

Low interest rate environment a global phenomenon Multi asset UK yield comparison

10

Policy Rate (%)

8

9

7

8

6 7

5 6

Yield (%)

4 5

4

3

3

2

2

1

1

0

0

Q1 2003

Q4 2003

Q3 2004

Q2 2005

Q1 2006

Q4 2006

Q3 2007

Q2 2008

Q1 2009

Q4 2009

Q3 2010

Q2 2011

Q1 2012

Q4 2012

Q3 2013

Q2 2014

Q1 2015

Q4 2015

Q3 2016

Q2 2017

Q1 2018

Q4 2018

Q3 2019

Q2 2020

Q1 2021

-1

Q4 2001

Q4 2002

Q4 2003

Q4 2004

Q4 2005

Q4 2006

Q4 2007

Q4 2008

Q4 2009

Q4 2010

Q4 2011

Q4 2012

Q4 2013

Q4 2014

Q4 2015

Q4 2016

Q4 2017

Q4 2018

Q4 2019

Q4 2020

UK 10 YR Gov Yield UK Corp. 10Y Yield (AA)

Ftse 250 (Div Yield) IPD Initial Yield

US ECB (Refi Rate) Bank of Korea BoE BoJ RBA UK Corp. 10Y Yield (BBB) IPD Equivalent Yield

Source: Refinitiv, MSCI, ASI, Jan 21

Source: Refinitv, Various Central Banks, ASI, Jan 21

For illustrative purposes only

Past performance is not a guide to future results.

28ASI Research – 3-Year Total Return Forecasts

Significant dispersion across property segments

Total return forecast (% p.a.), calendar years 2021-23

Supermarkets

London Distribution Warehouses

Rest of SE Distribution Warehouses

Healthcare

London Standard Industrial

Rest of SE Standard Industrial

Build to Rent (Rest of UK)

Rest of UK Distribution Warehouses

Rest of UK Standard Industrial

Build to Rent (London)

Solus Retail Warehouses

Bristol Offices

Edinburgh Offices

Retail Parks

Student Halls

Birmingham Offices

All Property

Rest of UK Offices

Leeds Offices

Manchester Offices

Glasgow Offices

Inner London Offices

Hotels

Rest of SE Offices

Mid Town Offices

City Offices

Dominant Standard Shops

West End Offices

Leisure

Rest of London Shops

Other Standard Shops

Dominant Regional Shopping Centres

Other Shopping Centres

Central London Shops

-8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0%

Source: Aberdeen Standard Investments, January 2021.

29 Forecasts offered as opinion and are not reflective of potential performance.

Forecasts are not guaranteed and actual events or results may differ material.Retail downgrades predominantly focused on rental value decline

Where is the floor? Threat of CVAs is real in fashion and F&B especially

Rental value growth forecast (% p.a.), calendar years, 2021-2023

London Distribution Warehouses

Build to Rent (Rest of UK)

Rest of SE Distribution Warehouses

London Standard Industrial

Build to Rent (London)

Rest of SE Standard Industrial

Rest of UK Distribution Warehouses

Rest of UK Standard Industrial

Student Halls

Healthcare

Edinburgh Offices

Bristol Offices

Manchester Offices

Supermarkets

Birmingham Offices

Rest of UK Offices

Leeds Offices

Glasgow Offices

Inner London Offices

All Property

Hotels

Solus Retail Warehouses

Mid Town Offices

Rest of SE Offices

West End Offices

Retail Parks

City Offices

Leisure

Rest of London Shops

Dominant Standard Shops

Dominant Regional Shopping Centres

Other Standard Shops

Central London Shops

Other Shopping Centres

-10.0% -8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0%

Forecasts offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual

Source: ASI, Jan 21.

events or results may differ material.

For illustrative purposes only

30Portfolio dashboard

Portfolio data Q4 2020 Q2 2020 Rent Collection

Portfolio Value £1,207m £1,219m

Rent Billing Mar June Sept Dec Mar June Sept Dec

Quarter 2019* 2019* 2019* 2019* 2020 2020 2020 2020

Rent collected

99% 98% 99% 93% 77% 83% 85% 84%

No. Properties 36 37 *21 days

No. of Tenancies 183 201

Lease expiry income erosion

Annual Rent Roll £56.3m £59.8m

Estimated Rental

£65.6m £69.6m

Value

Void Rate 6.5% 10.0%

AWULT* 8.9 years 9.7 years

NIY/ RY** 4.3% / 5.1% 4.4% / 5.4%

Gearing (gross) 6.4% (15.1%) 10.5% (18.7%) Source: MSCI, Sep 20. Green: MSCI Benchmark, Orange: Portfolio

Source: ASI, Dec’20

*Average Weighted Unexpired Lease Term

** Net Initial Yield / Reversionary Yield

Past performance is not a guide to future results

31Sector exposure over time

UKCM sector exposure by capital value versus benchmark Industrial

Retail-Industrial

inflection point

Material strategic overweight

position to industrial

Retail

17%

Maintained underweight positon

to retail

Offices

Source: ASI Dec 20 & IPD MSCI, Sep 2020

32Alternatives Portfolio: Rotunda – Asset Repositioning

The Rotunda, Kingston upon Thames

Sector Weighting

11%

Sector Occupancy

• Scheme closed entirely in March 2020 and January 2021.

• 18 year lease extension agreed with David Lloyd at

passing rent

• 15 year lease has been agreed with Odeon who are the

anchor tenant in the scheme

• Tenpin lease extended to 15 years in 2019

• Once stabilised we may look to progress with a significant

refurbishment of the scheme

• Have enhanced WAULT of the scheme and the

refurbishment will re position the asset

Source: ASI, Jan 21 Assisting tenants and creating long term value for Shareholders

33Office portfolio:

Sector Weighting

Sector Occupancy

Source: ASI, Jan 21 Controlled Low Exposure

Forecasts offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed

34 and actual events or results may differ material.Retail portfolio:

Sector Weighting

17%

Shopping Retail

High Street Supermarket Total

Centre Warehouse

Retail percentage nil 67% 18% 15% 100%

Portfolio percentage nil 11% 3% 3% 17%

Sector Occupancy

Source: ASI, Jan 21 Full exit from Shopping Centre Sector and limited High Street exposure

35Portfolio structure

Portfolio sector weighting (by Market Value) Capital value by geography

Source: ASI, Dec ‘20; MSCI Balanced Quarterly & Monthly benchmark Sep ‘20 Source: ASI Dec’20

Detailed sector weighting break down (by Market Value)

Source: MSCI, Sep ’20, ASI Dec’20

36Top 10 assets

By capital value 1 2

Sector Value Band (£m)

1. Ventura Park, Radlett South East Industrial Over 100

3 4

2. Hannah Close, London South East Industrial 60-80

3. Dolphin Estate, Sunbury-on-Thames South East Industrial 60-80

5 6

4. Ocado, Hatfield South East Distribution 60-80

5. Newton’s Court , Dartford South East Industrial 60-80

6. The White Building, Reading South East Offices 40-60 7 8

7. The Rotunda, Kingston-on-Thames Leisure 40-60

8. Kew Retail Park, Richmond Retail Warehouses 40-60 9 10

9. XDock377, Lutterworth RoUK Distribution 40-60

10. Junction 27 Retail Park, Leeds Retail Warehouses 40-60

Source: ASI Dec ‘20

37Top 10 tenants

By contracted rent % of MSCI Risk Band** December Rent Payment

Total

Income *

1. Ocado Retail Ltd 5.4 Low-Medium Paid in Full

2. Amazon UK Services Ltd 4.9 Negligible Paid in Full

3. Total E&P UK Ltd 3.8 Low Paid in Full

4. B&Q 3.3 Low Paying Monthly in Full

5. Cineworld 3.2 Low Unpaid

6. TK Maxx 3.1 Low-Medium Paid in Full (Kew)

/Monthly (Newcastle)

7. Public Sector 3.0 Negligible Paid in Full

8. Warner Bros Studios 3.0 Low Paid in Full

9. Dalata 2.8 Medium-High Paid in Full

10. Palletforce Ltd 2.6 High Paid in Full

Source: * ASI Dec ‘20 **MSCI, Sep ’20

© owned by each of the corporate entities named in the respective logos

38Debt Covenants

Barings 2027 Total debt available £100m Barings 2031 Total debt available £100m

Remaining to draw £0m Remaining to available £0m

Period to Maturity 6.25 years Period to Maturity 10.1 years

Margin 1.25% Margin 1.45%

All in rate 3.03% All in rate 2.72%

LTV/LTV Covenant (based LTV/Covenant (based on

50% / 75% 42.1% / 75%

on historical bank valuation) historical bank valuations)

ICR/Covenant 349% / 200% ICR/Covenant 312% / 200%

Source: ASI, December 20 Source: ASI December 20

ICR Forecast/Covenant 394% / 200% ICR Forecast/Covenant 367% / 200%

Barclays Total debt available £150m Overall Debt Position

Remaining to Draw £150m

Total debt available £350m

Period to Maturity 3.1 years

Margin 1.50% Remaining available £150m

All in rate 2.80%

Period to Maturity 8.2 years

LTV/LTV Covenant (December

0% / 60%

19)

ICR/Covenant 325% / 175% All in rate 2.88%

Source: ASI, December 20

ICR Forecast/Covenant 771% / 175%

Past performance is not a guide to the future.

39

The value of investments and the income from them can fall as well as rise and is not guaranteedNAV and share price performance

Share price Share price premium/discount to NAV

Source: ASI, December’20.

Source: Datastream, 29 January 2021

Past performance is not a guide to the future. The value of investments and the income from them

40 can fall as well as rise and is not guaranteedShare Price & NAV

UKCM Share Price & NAV

Source: Datastream, 29 January 2021

Past performance is not a guide to the future.

41Disclaimer

Risk factors you should consider prior to investing:

• The value of investments and the income from them can fall and investors may get back less than the amount invested.

• Past performance is not a guide to future results.

• Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

• The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset

Value (NAV) meaning that any movement in the value of the company's assets will result in a magnified movement in the NAV.

• The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult

to realise investments and may lead to volatility in the market price of the Company's shares.

• The Company may charge expenses to capital which may erode the capital value of the investment.

• There is no guarantee that the market price of the Company's shares will fully reflect their underlying Net Asset Value.

• As with all stock exchange investments the value of the Company's shares purchased will immediately fall by the difference between

the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

• The Company invests in real estate which is a relatively illiquid asset class, the valuation of which is a matter of opinion. There is no

recognised market for property and there can be delays in realising the value of assets.

• The value of property may fluctuate as a result of factors outside the Company’s control

• The Company’s ability to generate desired returns will depend on rental income generated and capital values of properties.

• Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends

and certain investors may be subject to further tax on dividends.

• The information contained herein including any expressions of opinion or forecasts have been obtained from or are based upon

sources believed by us to be reliable but are not guaranteed as to their accuracy or completeness.

• Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. You should

obtain specific professional advice before making any investment decision.

42Disclaimer continued

31/12/2020 (%) 31/12/2019 (%) 31/12/2018 (%) 31/12/2017 (%) 31/12/2016 (%)

NAV Total Return -0.9 0.1 4.5 12.2 3.8

Share Price Total Return -19.7 11.3 -2.0 9.4 3.8

MSCI Benchmark Total Return -0.1* 2.1 6.7 10.7 3.7

Source: Aberdeen Standard Investments, 31 December 2020 (*Benchmark: MSCI UK Balanced Portfolios benchmark to 30 Sept 2020 + 3 months MSCI UK Balanced Funds Monthly index to 31 Dec 2020)

Past performance is not a guide to future results

43Disclaimer continued Past performance is not a guide to future results. The value of investments, and the income from them, can go down as well as up and clients may get back less than the amount invested. Real estate is a relatively illiquid asset class, the valuation of which is a matter of opinion. There is no recognised market for property and there can be delays in realising the value of assets. The views expressed in this presentation should not be construed as advice or an investment recommendation on how to construct a portfolio or whether to buy, retain or sell a particular investment. The information contained in the presentation is for exclusive use by professional customers/eligible counterparties (ECPs) and not the general public. The information is being given only to those persons who have received this document directly from Aberdeen Asset Managers Limited or Standard Life Investments Limited (together “Aberdeen Standard Investments”) and must not be acted or relied upon by persons receiving a copy of this document other than directly from Aberdeen Standard Investments. No part of this document may be copied or duplicated in any form or by any means or redistributed without the written consent of Aberdeen Standard Investments. Copyright and database right MSCI IPD and its licensors 2021. All rights reserved. MSCI IPD has no liability to any person for any losses, damages, costs or expenses suffered as a result of any use of or reliance on any of the information which may be attributed to it. The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from marketing) any kind of investment decision and may not be relied on as such. Historical data and analysis, should not be taken as an indication or guarantee of any future performance analysis forecast or prediction. The MSCI information is provided on an ‘as is’ basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the ‘MSCI’ Parties) expressly disclaims all warranties (including without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages (www.msci.com).” 44

Disclaimer continued

FTSE International Limited (‘FTSE’) © FTSE 2021. ‘FTSE®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE International

Limited under licence. RAFI® is a registered trademark of Research Affiliates, LLC. All rights in the FTSE indices and / or FTSE ratings vest in FTSE and/or its

licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further

distribution of FTSE Data is permitted without FTSE’s express written consent.

No information, opinions or data in this document constitute investment, legal, tax or other advice and are not to be relied upon in making an investment or other

decision. Subscriptions for shares in UKCM may only be made on the basis of the latest prospectus, relevant Key Information Document (KID). These can be obtained

free of charge from Aberdeen Standard Investments, 1 George Street, Edinburgh, EH2 2LL, Scotland and are also available on www.aberdeenstandard.com

The information contained herein including any expressions of opinion or forecast have been obtained from or is based upon sources believed by us to be reliable but

is not guaranteed as to the accuracy or completeness.

Any data contained herein which is attributed to a third party ("Third Party Data") is the property of (a) third party supplier(s) (the “Owner”) and is licensed for use by

Standard Life Aberdeen*. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate, complete or

timely. To the extent permitted by applicable law, none of the Owner, Standard Life Aberdeen* or any other third party (including any third party involved in providing

and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Neither the Owner nor any other third party

sponsors, endorses or promotes the fund or product to which Third Party Data relates.

* Standard Life Aberdeen means the relevant member of Standard Life Aberdeen group, being Standard Life Aberdeen plc together with its subsidiaries, subsidiary

undertakings and associated companies (whether direct or indirect) from time to time.

Aberdeen Asset Managers Limited is registered in Scotland (SC108419) at 10 Queen’s Terrace, Aberdeen, AB10 1XL, Standard Life Investments Limited is registered

in Scotland (SC123321) at 1 George Street, Edinburgh EH2 2LL, and both companies are authorised and regulated in the UK by the Financial Conduct Authority.

GB-030221-141853-1

45You can also read