VOLSUNG MANAGEMENT - Rolls Royce Holdings plc (LSE:RR)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

VOLSUNG MANAGEMENT – Rolls Royce Holdings plc (LSE:RR)

June 12, 2014 – SumZero FactSet Non-US Idea Contest Submission

Investment Thesis:

Oligopoly aircraft engine manufacturer with insurmountable near-term barriers to entry and high-visibility,

recurring revenues thanks to almost total capture of aftermarket opportunity. Ramp-up of Trent

1000/XWB program will lead to surging revenues and potentially double margins as RR enters the lower

risk ‘sweet spot’ of a multi-decade product cycle. In-place product platforms offer 10+ years of high

visibility, high margin growth driven by a near 2xing of the installed engine base.

Business Summary:

Rolls Royce Holdings plc (LSE:RR) is one of the world’s leading manufacturers of complex, highly

engineered engines for aerospace, marine, and energy applications. Our investment thesis hinges on the

company’s civil aerospace business, which manufactures and services engines primarily for large

widebody commercial aircraft.

RR is significantly expanding its share of the widebody engine market thanks to the successful platform

wins of its newest series of engines, which will likely make the company the market leader in this segment

as it delivers on its current order book. RR’s benefits from stable, predictable economics, with almost ½

of 2013 revenues coming from long-term annuity-like service revenues earned on the existing installed

base of engines with useful lives exceeding 25 years. RR is in the final stages of the significant

investment spending program which will enable a surge in engine production starting in late 2014,

generating decades of high-margin, recurring revenues, even as this expense ramp temporarily

depresses current operating results. We believe this creates a highly compelling asymmetrical risk/reward

proposition and an attractive investment opportunity.

Despite the high quality of the business and its secure competitive moat, we believe that RR shares are

historically cheap for several reasons. Analysts are concerned by the degree of the contraction in the

company’s defense business in 2015 and are skeptical over management’s long-term guidance for the

segment. Defense concerns are magnified by management’s conservative guidance for the marine

business, which is coming down from a period of explosive growth in recent years. Finally, elevated costs

in advance of the deliveries of a new generation of engines create uncertainty as to the eventual

profitability of these engines, while a dearth of new orders has been created by the significant existing

backlog and delays by airframe OEMs in delivering the next generation of widebody. We believe that

these are transient factors which give little credit for the inherently defensive quality of the business, and

which unduly extrapolate short-term concerns against a business with a history of delivering on long-term

growth and value creation.

Rolls Royce Civil Aerospace – From Widebody Obscurity to Market Leader:

RR’s civil aerospace business manufactures large engines for widebody aircraft as well as smaller

engines primarily for corporate and regional jets. Despite being a distant third in the widebody engine

market as recently as 20 years ago, RR is today poised to become the market share leader in widebody

1

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019

aircraft engines and we believe the company is enjoying the strongest competitive position in its history.

We will briefly recap the company’s operating history in civil aerospace before discussing the economics

of the civil aerospace engine business and the company’s current product portfolio.

Rolls Royce was a pioneering giant of the reciprocating piston engine era, powering a significant portion of

the allied air effort in World War I and II, including designing the legendary Merlin engine which powered

the most successful variants of the Supermarine Spitfire and the P-51 Mustang. RR continued to develop

a significant portfolio of successful turboprop and jet engines for military aircraft in the post-war years but

was slow to enter the emerging civilian aerospace market. After missing out on the groundbreaking Boeing

747 and McDonnell Douglas DC-10, which were initially powered by General Electric and Pratt & Whitney

engines, RR belatedly responded in the ‘60s by winning an exclusive contract to provide the launch engine

for Lockheed’s proposed widebody competitor, the L-1011.

RR’s RB211 engine which was to power the L-1011, however, seemed to be an almost unmitigated disaster

at the time, suffering numerous delays and initial reliability problems. The cost overruns and delays

associated with engine’s initial development almost bankrupted the company, leading then Prime Minister

Ted Heath to nationalize RR in 1971. RR’s initial failures with the RB211 jeopardized the entire L-1011

program and were a decisive factor in Lockheed’s decision to abandon commercial aircraft production

altogether.

Despite its development problems and the damage done to RR’s credibility with customers and partners

by the RB211-L1011 fiasco, subsequent iterations of the RB211 would prove to be highly successful

engines. The reliable and cost-efficient RB211 would transform RR into a top-tier global competitor in

civil aerospace, and variants of the RB211 would win a meaningful share of orders as an alternative

offering on the Boeing 747-200 and 747-400, as well as on the later Boeing 757 and 767. The RB211-

524 variant in particular was to be a milestone for the company, becoming the first RR engine to be

selected by Boeing as a launch engine for the 757, first delivered to customers in 1983. The success of

the RB211-524 on the 757 led to the first major orders for RR-powered aircraft from an American airline

since the early days of the Lockheed L-1011.

While the RB211 returned RR to commercial significance, its widebody market share was still just 8% at

the time of its privatization by Margaret Thatcher in 1987, making the company a distant third to GE and

Pratt & Whitney, and questions remained over the company’s ability to continue to compete on future

aircraft platforms. However, having already achieved a foothold for RR in the widebody engine market,

the reliable RB211 would provide the foundation for its eventual successor, the Trent engine, which would

cement the company’s position in widebody engines and lead the company to new heights.

Development of the Trent series of engines was formally announced in 1988, with RR stating its intention

to use the versatile three-spool design of the RB211, which remained a departure from the two-spool

designs favored by GE and Pratt & Whitney. The three-spool design adds additional engineering

complexity, but allows each engine module to be more readily tailored to meet a range of performance

and thrust targets depending on the specific needs of airframe manufacturers, as well as offering potential

weight savings. Despite initial commercial setbacks with the aborted Trent 600, the subsequent Trent 700

iteration became the first RR engine to power an Airbus aircraft, becoming the launch engine for the A330

in 1990. The Trent 700 was to be the first major widebody success for RR, winning 57% market share on

the highly successful A330, and remains in production today.

The success of the Trent series continued in the later years of the ‘90s with the Trent 800, designed for

the Boeing 777 and entering service in 1996, which won more than 40% market share against

competitive offerings from GE and P&W. Despite failing to win a place on Boeing’s long-range 777 (due

to GE’s willingness to subsidize the aircraft’s development in order to win exclusivity), the Trent 500 would

win exclusive positions on the competing Airbus A340-500 and -600 variants in 1997, being chosen over

a competing offering from Pratt & Whitney. These successes followed on the announcement in 1996 that

RR’s Trent 900 would power the gigantic Airbus A380.

2

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019Civil Aerospace Order Book (mms. of GBP)

£70,000

£60,000

£50,000

£40,000

£30,000

£20,000

£10,000

£-

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

RR’s surging order book in the late ‘00s has primarily been driven by the 787 & A350XWB

To date, RR claims that Trent engine has won some 40% market share on the platforms on which it

competes since its introduction. The successes of the ‘90s helped RR build lasting relationships with key

airline customers and made the company a legitimate contender in the wide body market, setting the

stage for the current generation of platform wins. Today, RR has won a place on 3 of the key widebody

aircraft offerings: the Boeing 787, the Airbus A380, and the Airbus A350XWB. With an exclusive position

on the A350XWB, the #2 position on the 787 program, and a modest market share lead for GE on the

A380, RR is poised to take a market share lead in the widebody engine market as production of these

platforms begins to ramp up in the coming years. RR will now have the scale and reach in the widebody

engine market it has heretofore lacked, and we believe the long-lasting impact of these successes will

bring about a step-change in the company’s financial performance over the next decade and beyond.

Jet Engine Economics, Customer Criteria, and the Revenue Lifecycle:

Jet engines generally have working lives exceeding 20 years and the development cycle for engines can

span more than a decade, comprising billions of dollars and millions of man-hours of development,

design, testing, and certification work. While this lengthy development process for new platforms involves

significant engineering risk and uncertainty as to whether an engine will ultimately be selected by the

airframe manufacturer, the relationship between engine and airframe manufacturers demands close

cooperation and is generally constructive. Furthermore, once an engine has been selected by one of the

two dominant airframe manufacturers and achieved final regulatory certification, the rewards are

significant and lasting. We believe that RR is currently at an attractive point in the cycle where it is poised

to benefit from the latest generation of widebody platform wins, having already incurred much of the

expenses necessary to deliver these engines, while the next round of major widebody bidding

opportunities is likely to be a decade or more away.

The long working lives of jet engines and the long development period creates a predictable, long-tailed

revenue cycle, with a single engine platform generally driving new equipment sales for 10+ years, and

then providing 20+ years of maintenance, repair, & overhaul (MRO) revenues. This is because jet

engines are generally sold on a ‘razor and blade’ basis, with manufacturers selling engines at a significant

discount to their list price (in some cases 80% or more) as long as the engine is sold bundled with lifetime

service agreements (LTSAs) and spare parts contracts, which are generally worth 2-3x the sticker price of

the engine. This “power by the hour” model, with revenue earned for every mile flown, allows engine

manufacturers to recover their investment over a period of several decades, lending an unusual degree of

persistency to revenues.

Customers ordering aircraft generally select an engine based on a number of factors. Interviews with

former engine executives suggest that the primary concern of customers is the initial upfront cost of the

3

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019engine, followed by the engine’s fuel efficiency, with the third factor being the possibility for financing,

either directly from the airframe or engine manufacturer or from a 3rd party bank or lessor. Maintenance

expenses, as generally encapsulated in “power by the hour” offers (including the prospective rate,

turnaround time guarantees, guarantees on availability of spare engines and parts, and included

warranties) are generally ancillary to the above factors, but play a significant role in decision-making as

they are also a determining factor in the initial upfront cost. Given that the practical differences in all of

the above elements between competing options are generally quite small or mutually offsetting, in

practice this decision can often come down to personal relationships between engine and airline

executives.

Once an airline has committed to an engine, it is very rare for an airline to attempt to shift orders from one

engine manufacturer to another, or to make additional aircraft orders with a different engine partner.

Doing so incurs incremental training costs for maintenance and flight personnel and may also incur

significant legal costs for backing out of previously agreed deals. This means that early order books for

airframes are generally indicative of future volumes and that the initial market share of an engine on an

aircraft platform tends to remain fairly stable over the platform’s life. Furthermore, once installed,

replacing an existing engine is generally regarded as uneconomical, meaning that engines under LTSAs

will generate revenues as long as the aircraft remains in service.

RR’s LTSA offering is branded as ‘TotalCare’ and charges customers a fixed cost per flight hour, with RR

responsible for almost all maintenance costs incurred, although in practice there is some ambiguity as to

what charges exactly are or are not included in power by the hour agreements due to the sheer

complexity of the contractual language. TotalCare is available either as a monthly billable service or

billable on service, with both offerings based on hours flown.

Customers find these LTSAs attractive for a number of reasons. they are able to lock in maintenance

costs up front (generally at a meaningful discount to what 3rd party or in-house MRO would cost) and

there is no possibility of being overbilled for service given the alignment of incentives. Furthermore, with

the majority aircraft opex comprised of engine maintenance, and the significant volatility associated with

customers’ other major line items (such as fuel & labor expense), carriers value the comparative certainty

provided by “power by the hour” service. “Power by the hour” also limits the direct financial losses from

engines plagued with reliability issues, although it obviously does not fully eliminate the possibility of

reduced availability associated with recurring engine maintenance.

Based on estimates from former engine executives, labor and repair revenues under LTSAs offer

comparatively low margins of approximately 5% and 10-20%, respectively, but spare and replacement

parts are highly profitable with margins of some 50-80%. This is largely because LTSAs typically discount

labor and repairs charges, but offer no such discounts for parts, which feature significant mark-ups on

cost. From a cost perspective, materials and parts are probably ¾ of MRO expense, with labor

accounting for the remainder.

TotalCare requires that RR stand behind the quality of its engineering and manufacturing. We are

comfortable with the performance guarantees and contingent risks inherent to TotalCare for several

reasons: RR as a business already lives and dies by its the quality of its engineering work; the current

generation of engines are largely iterative improvements of designs with several million flying hours and

generally not wholly de novo products; and, even absent the explicit guarantees contained in LTSA

agreements, we believe that RR would likely be forced to stand behind any significant engineering and

manufacturing failures above and beyond its warranty guarantees in order to retain its relationships with

airline partners. Essentially, this is a risk already inherent to the business, and RR’s codification of this

risk in its LTSAs provides an attractive selling point for customers without adding much in the way of

actual incremental operational risk. It is the nature of such an engineering intensive business that

success is a function of design and manufacturing quality.

4

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019In any case, RR’s reputation for reliability is generally regarded as being best-in-class. Discussions with

engineers and mechanics suggest that RR has traditionally maintained a reputation for being reliability-

oriented in their engineering and has generally offered better performance retention over time than peers,

as well as the best maintenance monitoring program available, resulting in longer time on-wing and lower

lifetime cost of operation for RR engines. This has historically allowed RR to remain competitive against

engines with modestly better long-range fuel efficiency, although as we will further discuss, the respective

attractiveness of one engine over another depends on intended mission and usage, and there is not

necessarily one engine design that is universally better or more efficient than others for all potential

applications.

The insurance-like nature of the TotalCare product also provides ‘float’ to fund the business, as income

accrues ratably even as the bulk of maintenance costs are back-loaded towards the second decade of

operations. This makes the planned ramp-up in deliveries in the coming years especially valuable, as RR

will experience a surge in LTSA billings without a subsequent increase in service expense. Furthermore,

the complex tooling and assembly process associated with launching production of new engines (and

expanding attendant service capabilities) requires significant capital investments. This amplifies the initial

deferral of revenues by the “razor and blade model”, even as this incremental capital expenditure is

wholly success-based and therefore incurs limited risk.

RR is currently in the midst of its largest ever investment of this nature, incurring significant unabsorbed

fixed costs as it expands production facilities to prepare for deliveries of the Trent XWB later this year.

This will amplify the impact of the production ramp-up (with incremental service revenues being earned

without attendant service costs) due to the leverage of a significant amount of unabsorbed fixed costs.

We believe these complications magnify the analytical challenge for sell-side analysts trying to unpack

RR’s currently bloated cost structure, and we believe the consensus is underestimating the degree to

which the Trent 1000/XWB deliveries will radically alter RR’s revenue and margin profile.

TotalCare also introduces significant accounting complexity into RR’s accounts, and has presented some

challenges to the company and its auditors in deciding how to account for these agreements. These

concerns have resulted in a back-and-forth with the UK accounting regulator, with RR agreeing to adjust

certain accruals related to the accounting for entry fees on risk and revenue sharing arrangements with

partners[*]. We are comfortable with the manner in which RR accounts for TotalCare revenues, as we

believe the assumptions faithfully reflect the economics of the agreement and do not allow undue scope

for earnings management.

Current Engine Platforms:

Having addressed the economics of the civil aerospace engine business, we now turn to the company’s

current product portfolio, encompassing both the installed base of legacy programs as well as the core

growth programs which will drive near-term earnings growth. Our assumptions about the persistency of

each of these legacy programs will factor into our subsequent estimates of the value of current installed

base.

5

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019Civil Engine Installed Base - End of Year Totals

Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

RB211 22B 249 195 165 156 132 120 81 66 42 30 21 12 12 6

RB211 524 1,069 1,058 1,042 1,019 1,003 994 953 944 895 848 783 752 685 626

RB211 535 1,096 1,164 1,196 1,206 1,218 1,214 1,210 1,206 1,204 1,196 1,196 1,172 1,166 1,154

RB211 Total: 2,414 2,417 2,403 2,381 2,353 2,328 2,244 2,216 2,141 2,074 2,000 1,936 1,863 1,786

Trent 500 - 12 48 132 220 300 388 424 456 508 520 524 524 520

Trent 700 134 178 206 235 264 306 364 424 494 608 724 840 980 1,144

Trent 800 224 296 344 376 392 408 432 444 442 450 450 450 450 444

Trent 900 - - - - - - 16 20 36 68 96 152 216 252

Trent 1000 - - - - - - - - - - - 14 52 94

Trent XWB - - - - - - - - - - - - - -

Trent Total: 358 486 598 743 876 1,014 1,200 1,312 1,428 1,634 1,790 1,980 2,222 2,454

Large Engines Total: 2,772 2,903 3,001 3,124 3,229 3,342 3,444 3,528 3,569 3,708 3,790 3,916 4,085 4,240

Spey 1,472 1,442 1,408 1,376 1,342 1,246 1,204 1,158 1,132 1,056 1,000 892 848 768

Tay 1,640 1,714 1,772 1,830 1,847 1,866 1,890 1,903 1,951 2,017 2,057 2,077 2,119 2,155

AE3007 986 1,380 1,718 1,966 2,200 2,370 2,476 2,596 2,710 2,782 2,814 2,850 2,896 2,950

BR700 448 662 792 904 1,006 1,164 1,312 1,480 1,650 1,832 2,032 2,226 2,448 2,744

Small Engines Total: 4,546 5,198 5,690 6,076 6,395 6,646 6,882 7,137 7,443 7,687 7,903 8,045 8,311 8,617

V2500 638 759 872 971 1,080 1,217 1,361 1,496 1,650 1,794 1,949 2,119 - -

Civil Aerospace Total: 7,956 8,860 9,563 10,171 10,704 11,205 11,687 12,161 12,662 13,189 13,642 14,080 12,396 12,857

The widebody large aircraft engine business comprises the legacy RB211 engine family, dating to the

early ‘60s with significant numbers still in service, and the Trent engine family, which was originally

introduced in the early ‘90s and which represents the present and future of the company.

Despite its increasing age, latter variants of the RB211 will likely remain a workhorse platform for a

considerable amount of time to come, with passenger service retirements being partially offset by

conversion of airframes to freighters. The venerable 22-B variant powers the L-1011, of which a handful

remain in service but which are uneconomic to operate today and which will soon be relegated to the

status of museum piece. The 524 variant powers the 747-200 and 747-400, as well as the 767-300, with

many of these aircraft being retired from passenger service or converted into freighters over the past 15

years. We expect the majority of the 524s to be retired by the end of the decade as the 787 enters

service with the key remaining operators of the 767-300, although a handful of -300s operated primarily

by Asian airlines could remain in service well into the 2020s. The most modern version of the RB211, the

RB211-535, powered the 757-200 and -300, of which new deliveries were still being made as recently as

2005, and a significant number of 535s will likely remain in service for a decade or more.

The Trent 500 powers the long-range variants of the Airbus A340, production of which peaked in the mid

‘00s. Despite being a comparatively recent platform, questions remain over the Trent 500’s future. Due

to sustained high oil prices, the four engine configuration of the A340 is no longer as economical to

operate as comparable twin-jet models like the 777 and A330, which have proven capable of operating in

the same role with greater fuel efficiency. With customers retreating from the platform and resale prices

plummeting, the A340 program has proven to be a costly mistake for Airbus. RR is unlikely to generate a

significant return on investment from the in-service Trent 500s, a handful of which have already been

retired after just 10 years of service, speaking to the potential risks to the LTSA model should the

airframe fail to live up to expectations.

The failure of the A340 program has been compounded by Airbus’ decision to offer customers significant

discounts as well as resale price guarantees to spur sales in the early ‘00s. With secondary market

prices as low as $20mm, against original list prices of more than $90mm and a scrap value of probably

$10mm, Airbus has recorded losses of hundreds of millions of dollars. RR has also faced pressure to

retool its LTSAs in order to level the cost of operation with the long-range variants of the competing

Boeing 777, which is powered by the GE90. Airbus believes the plane remains a compelling alternative

for customers looking to retire older 747s, and given the willingness of RR to make operating costs

competitive as well as the significant decline of purchase values, current lease rates for second-hand

A340s should more than offset the comparative lack of fuel efficiency. This potentially lends some

additional life to the in-service A340s as a stop gap for customers awaiting delivery of the 787 or

6

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019A350XWB, but we generally assume that the bulk of these engines will be retired in the next 5 years,

which we believe to be a conservative assumption.

The Trent 700 is available as an option on the Airbus A330, competing with the P&W PW4000 and the

GE CF6. The Trent 700 has been a tremendous success on the A330, becoming the preferred engine

option with market share of more than 57%. The success of the Trent 700 mirrors the failures of the

A340 with which it partially competes, and RR continues to deliver large numbers of Trent 700s, with a

significant order book which will be delivered through at least 2015. Given the operational success of the

A330, the comparatively recent vintage of the aircraft, and continuing deliveries of new planes and

engines, we expect that most Trent 700s will remain in service for more than a decade, with the potential

for a large number of engines to remain in service well into the 2030s. We believe the successes of the

Trent 700 and the contemporaneous Trent 800 more than compensate for the relative disappointment of

the A340/Trent 500, and offer a compelling illustration of what the prospective Boeing 787/Airbus

A350XWB sales lifecycles may look like. Furthermore, the success of the A330 has led some observers

to speculate that RR will secure an exclusive for the re-engined A330neo variant that Airbus is reportedly

developing.

The situation of the Trent 800, which powered the earlier variants of the Boeing 777, is similar. We

expect the service profile of the Trent 800 to largely resemble that of the 700, albeit with the potential for

greater numbers of retirements in the latter part of the current decade due to RR having lost its position

on the later, extended range versions of the 777, which are GE-exclusive. To date, the Trent 800 has

won 19% of total 777 family deliveries to date, but this ignores the fact that GE was awarded exclusivity

for the later 777-200LR, -300ER, and F variants, which account for just over ½ of 777s shipped. If one

considers solely the competitive portion of the 777 program, RR’s market share was 40%, comfortably

exceeding the 30% won by GE and P&W individually. We expect that the bulk of the Trent 800s will be

retired in the 2020-2025 timeframe, being replaced by 787s and A350XWBs.

Unfilled Orders - as of May 2014 While RR retains a significant installed base of

Trent 1000 458 Boeing 787 legacy engines, with the Trent 700 continuing to

Trent XWB 1,484 Airbus A350 XWB win new orders after almost 20 years since its

Trent 900 156 Airbus A380 first delivery to a customer, the current installed

Trent 700 292 Airbus A330 base pales in comparison to the prospective

Total: 2,390 weight of the current order book. The most

important airframe platforms for RR in the

coming decades will be the Boeing 787 Dreamliner and the Airbus A350XWB which are powered by the

Trent 1000 and Trent XWB, respectively. These engines power new long-range, twin-engine airframes

which, in the case of the 787, are just completing their first years of service and which still have their best

years ahead of them. The Trent 900-powered A380, on the other hand, has generated many of the

similar customer concerns as the A340, and orders have been weak, despite being a comparatively new

airframe. While Airbus will likely seek to keep the A380 as a viable platform for as long as possible, given

the significant investment in the platform to date, we do not anticipate significant incremental orders for

the Trent 900.

If the Boeing 777/Airbus A330 cycle offers any indication, new deliveries of these nascent twin-engine

widebody platforms will likely continue well into the 2020s, at which point the next generation of twin-

engine widebody aircraft will likely be announced, suggesting that the current order cycle is only 40-60%

complete. While orders for both platforms have tailed off after an initial pre-delivery surge, both

manufacturers will likely retain these designs as core platforms through the 2020s, and we expect

incremental orders to continue to mount as shipments begin to reduce the initial order backlog.

Furthermore, if, as anticipated, Airbus proceeds with the A330neo, RR will likely be able to leverage the

technology of the Trent 1000/XWB into a successor for the Trent 700, further enhancing the return on

investment of the company’s current generation engine programs.

7

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019The Trent-900 powered A380 is worth mentioning as another potential source of future orders, but faces

many of the same issues that plagued the A340 program due to its 4 engine configuration and sheer size,

and is generally regarded as being something of a troubled platform of little interest to all but a handful of

premium long-haul operators. Despite winning an order at the end of 2013 for an additional 50 aircraft

from Emirates, A380 orders appear to have peaked and the aircraft’s future is generally regarded as

being in doubt unless a re-engined A380neo enhances the plane’s economic appeal. The prospective

challenge of re-leasing these aircraft after their initial lease terms expires has been a concern, as has the

potential near-term competition raised by the prospective revamped Boeing 777, the 777x. Airbus and

RR have reportedly held tentative discussions over the possibility of a re-engined A380neo, allegedly at

the urging of Emirates, but there has apparently been some skepticism as to whether it will be possible

for Airbus to pursue an A380neo and an A330neo simultaneously.

Barriers to Entry:

The primary attraction of RR’s business is the sheer size of its competitive moat. All of the current major

competitors in the aircraft engine market date to the early days of aviation in the early 20 th century, and

we believe that a new entrant would likely require state backing and several decades to reach competitive

parity with existing competitors. Indeed, RR itself has been a recipient of government aide over the

years, having received more than £450mm in subsidies from HM Treasury to kickstart the development of

various models of the Trent engine in the ‘90s, and we believe that significantly larger sums would be

required for a greenfield entrant building a wholly new engine architecture. Unless you are an especially

slow-moving endowment investor, this is likely to significantly exceed your investment horizon, and we

think there is little risk of any surprise entrants suddenly disrupting RR’s core markets in the medium term.

Furthermore, in the short term the range of competing products is fixed, being limited to the other

available engine options on each airframe. The long nature of the product cycle means that prospective

competitors can only enter the market once a decade or so, as manufacturers generally design airframes

in close cooperation with engine makers. This means that for any given product cycle, RR faces a fixed

constellation of 1 or 2 competitors at most. This offers an unusual degree of visibility into what the next 5-

10 years will look like for RR, and, given the size of the current order book, we believe a current investor

need not be especially concerned about RR’s success in bidding for the right to power any given future

airframe platform.

Indeed, it will likely not be until the 2020’s that Airbus and Boeing begin to develop replacements for the

787 and the A350XWB, although niche variants, re-engined upgrades, and other incremental bidding

opportunities may materialize, with a re-engined A330neo being the most likely near-term potential

project. Recent comments from Airbus to the effect that they will not be pursuing wholly new airframes,

and instead developing derivatives of existing platforms, have been mirrored by comments from Boeing’s

CEO that there will be no more “moonshots”. These comments and the apparent shift in strategy they

reflect seem to discount a period of tentative retrenchment after the ambitious, and often troubled,

development of this most recent crop of wide-body aircraft.

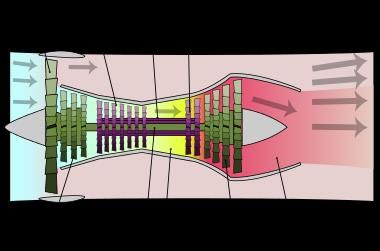

This long product cycle is driven by technical complexity. Jet engines are extremely complicated pieces

of machinery with tens of thousands of moving parts, complex to the point that no single engineer retains

a comprehensive understanding of any individual engine, with individual component assemblies being the

province of separate teams of engineers working in tandem. The sheer complexity of jet engines means

that current engine designs are generally the iterative evolution of several decades of design work,

reflecting billions of R&D investment and millions of running hours, with truly revolutionary leaps in design

coming only once every few decades. The Trent XWB, for example, took some 2,000+ engineers 10

years from conception to delivery, while the development of the RB211 engine which has formed the

basis for every of RR’s successful widebody engines to date nearly bankrupted the company. P&W’s

more revolutionary recent engine design, the geared turbo fan PW1000G, will likely have taken almost 20

years to deliver if it is delivered on schedule, and itself draws on concepts that were familiar to engineers

as far back as the ‘60s.

8

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019This technical complexity, and the confidence offered to customers from this iterative development from

the basis of proven platforms, presents a highly significant barrier to entry but also creates risks. While

the sheer cost of developing engines creates a risk that an engine may fail to win eventual acceptance

with an airframe manufacturer, these investments are not generally permanent losses, as the orphaned

architecture can generally be reused to bid for subsequent platforms. This is indeed what RR did with the

failed Trent 600, which was to become the launch engine for the Airbus A330 in a revamped configuration

as the Trent 700, or with the failed Trent 8104, which would evolve into the Trent 900. Indeed, the

process of technological evolution is a constant one (a 1% p/a increase in fuel efficiency is a commonly

cited ‘Moore’s Law’ of the jet engine industry), and manufacturers persistent R&D spending means that

engines offering incremental improvements are generally able to be developed when bidding

opportunities arise. However, there is risk surrounding any individual aircraft platform program, as the

airframe manufacturer’s shifting requirements may be out of step with an engine manufacturer’s

development cycle, as happened to GE’s attempts to power what would become the Airbus A350XWB

illustrate.

We believe these R&D risks are further mitigated by the range of bidding opportunities offered in an

oligopoloy sector with only 2 other real competitors, none of which have the ability to simultaneously

compete effectively in all segments at once. Combined with structural factors favoring aircraft platforms

with more than 1 engine option, we believe the risk of RR permanently losing its place in the commercial

aerospace engine market is quite small, although a partial loss of market share is certainly possible. If

the example of Pratt & Whitey and McDonnell Douglas are relevant, the most likely factor which would

lead to a partial loss of share is inadequate investment in R&D and attempting to over-stretch dated,

derivative technology past its obsolescence. We do not believe that RR’s current strategic direction

exposes the company to this risk.

Technical barriers to entry are enhanced by the demands of customers. The preference of customers for

purchasing engines bundled with LTSAs means that customers (not to mention the airframe OEM

choosing its engine partners) are making a bet that the engine OEM will not only successfully deliver

engines on time, but will still be around to provide service and replacement parts for several decades.

The nature of LTSAs also requires that a new OEM would have to build a global network of a dozen or so

MRO shops to service customer engines. LTSAs and the current preference for the “razor and blade”

revenue model extend the break-even point for new engine programs by stretching revenues out over

several decades, which further strains the case for a privately-funded new entrant.

The long pay-back period of engine development programs creates some risks should a platform fail to

live up to expectations, but the sunk-cost of the customer in purchasing the aircraft and the limited

secondary market for such commercially challenged aircraft means that these engines will generally

remain in service for sufficient time to remain economic, with pressure instead being reflected from

smaller than anticipated sales volumes. In these circumstances, it is possible that RR would face

pressure to reduce the per mile cost of TotalCare, as has been the case with the largely failed A340

program.

All of these combined factors mean that a new entrant would require decades of sustained losses, which

would likely prove impossible for any democratic government subject to the vagaries of electoral politics

to successful maintain, reducing the range of potential entrants to likely mean one backed by an

authoritarian government. In fact, the Chinese government already has such a plan underway, and

represents the only potential long-term threat to the currently cozy engine oligopoly worth mentioning,

even though we believe it faces a long uphill battle to commercial acceptance.

Aviation Industry Corporation of China (AVIC), although traditionally focused on high-performance

engines for combat aircraft, is reportedly looking to capture share in the civilian aerospace market, and

some analysts reckon that the company could win as much as RMB 100-300bn (~$16-48bn at current

exchange rates) in state subsidies to enhance its development programs. Although we are extremely

skeptical of the Chinese economy, the state of the national balance sheet, and, by extension, the

9

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019government’s ability to continue fund such an extravagantly ambitious long-term program, the potential

political issues for western customers in purchasing engines from a company controlled by the Chinese

military suggest that AVIC’s plans should be regarded with skepticism. These concerns can be

somewhat offset, or perhaps magnified, by the likelihood that AVIC can (and reportedly already has)

resorted to industrial espionage, allowing it to close the competitive gap by the theft of intellectual

property from western competitors. In either case, we believe that even if AVIC were to successfully win

share, it would not until the mid-2020s at the earliest, placing this risk well outside of the time horizons of

most current investors.

Competitive Dynamic – Civil Aerospace:

The aircraft engine business has been an oligopoly since the 1970s, and RR’s competitors are

subsidiaries of large industrial conglomerates: GE Aviation, a subsidiary of General Electric, and Pratt &

Whitney (P&W), a subsidiary of United Technologies. Both companies have histories stretching back into

the early 20th century infancy of aviation, reflecting the significant barriers to new entrants which have, if

anything, grown larger over time. As part of larger conglomerates, both competitors enjoy access to

greater financial resources and, in the case of GE, from the parent’s captive aviation finance unit. This

has historically meant that RR has had to rely solely on its engineering prowess and has been unable to

fall back on the ability to subsidize customers or airframe OEMs in order to win orders. While RR’s

comparative lack of scale creates some risks, we believe these are mitigated by the significant expansion

of the business currently underway, which will give the company the strongest market position, and by

extension the greatest breadth, in its history.

The structure of the aerospace industry means that airframes are generally offered with 2-3 engine

options at launch, although there have been notable exceptions, such as RR’s currently exclusive position

on the A350XWB (although this was more reflective of disagreements with GE rather than a choice by

Airbus). This is because airframe manufactures generally want multiple engine options in order to reduce

development risks (in case a partner fails to produce a viable engine on time, a situation Lockheed faced

when RR teetered on the brink in the early ‘70s), while customers generally want multiple options so as to

enhance negotiating leverage, or to be able to choose an engine with performance parameters that most

closely match the plane’s intended mission. Customer pushback reportedly led Boeing to abandon its

initial plans to offer the 787 with GE as an exclusive engine partner, which offers some certainty that RR

is unlikely to be wholly shut-out from future widebody airframe platforms.

Indeed, we believe that the power of engine manufacturers relative to airframe manufacturers is

increasing over time, as engines comprise the bulk of the operational costs of the aircraft given current

fuel prices. With the bulk of performance improvements increasingly dependent on the innovations of

engine manufacturers, and new engines able to breathe life into largely decades old airframes (as has

been the case with the A320neo), engine manufacturers are ever more critical partners for Boeing and

Airbus. We believe this dynamic has been visible in the case of the A350XWB, where Airbus’ attempts to

solicit bids for engines offering an unusually wide range of thrust options led to GE balking at the potential

development costs and RR committing only after receiving exclusivity.

Engine manufacturers routinely engage in coopetive behavior in order to reduce the risk associated with

individual development programs. RR regularly enters JVs in its defense aerospace business (such as

for the EJ2000 engine provided for the Eurofighter Typhoon, or the TP-400-D6 which powers the Airbus

A400M Atlas), and previously was a participant in the narrowbody aircraft International Aero Engines

(IAE) JV with P&W, MTU Aero Engines, and Japanese Aero Engine Corporation. IAE developed and

produced the highly successful V2500 engine, which powers the Airbus A320, but RR sold its stake in

2012 in order to concentrate the company’s focus on its core widebody engines. We believe the

presence of a number of significant joint ventures between otherwise direct competitors speaks to a

rational industry environment capable of sustaining abnormally high returns on capital.

10

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019Return on Assets (EBIT)

20.0%

18.0%

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

2010 2011 2012 2013

Rolls Royce Aerospace GE Aviation Pratt & Whitney

Prior to 2011, GE Aviation’s results were disclosed along with the company’s healthcare & transportation operations in the

"Technology Infrastructure" segment

It is important to distinguish between the narrowbody and widebody aircraft engine markets when

evaluating the industry’s competitive dynamic. While narrowbody aircraft significantly outnumber

widebody aircraft, the dollar value of the narrowbody market is slightly smaller, while regional and

commercial aircraft are almost wholly insignificant in comparison. Boeing recently estimated the value of

the widebody aircraft market at more than $2.3trn over the next 20 years, against a $2.0trn narrowbody

market and a $80bn regional & commercial market. The narrowbody market is generally more

competitive, with a greater number of second-tier airframe OEMs attempting to compete with the

dominant Boeing and Airbus, including comparatively new, heretofore irrelevant upstarts Bomarbdier

(Canada), Embraer (Brazil), Mitsubishi Aircraft Corporation (Japan), COMAC (China) and United Aircraft

Corporation (Russia). We believe the size of the market opportunity is more than enough to comfortably

sustain 3 engine manufacturers, and that the breadth of the industry precludes domination of all

segments by any given competitor. Furthermore, we believe that it would not be in the interest of

airframe manufacturers to let one of the 3 engine manufacturers disappear, thereby further increasing the

already significant market power of the surviving 2 manufacturers.

The Widebody Market – GE vs. Rolls Royce

RR’s primary widebody competitor is GE Aviation (GE). GE Aviation is the giant of the field for the time

being thanks to its current widebody market share lead as well as its strong competitive position in

narrowbody via the CFM International JV. Like both RR and P&W, GE also maintains a significant

defense aerospace business, with a strong legacy position in combat aircraft. Furthermore, GE has

historically been able to rely on the financial largesse of GE Capital Aviation Services (GECAS), which is

among the world’s largest aviation lenders, offering a competitive advantage in marketing. GE has also in

some cases offered significant direct subsidies to airframe OEMs, as it did with the long-range Boeing

777 variants, for which GE committed up to $500mm in exchange for exclusivity over the proposed Trent

8104, which was generally regarded as the more innovative and advanced engine at the time.

GE competes head to head with RR’s Trent 1000 on the Boeing 787 Dreamliner with its GEnx engine.

The GEnx engine builds on the previously successful GE90 engine and has so far won some 65% of

finalized 787 orders, although a significant number of firm orders remain uncommitted to an engine

supplier. The GEnx retains a somewhat more conventional core design as compared to its primary

competitors, favoring evolutionary, iterative improvements made possible by advancing materials science.

11

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019GE’s engine, at initial specifications, reportedly offers slight advantages compared to the Trent 1000 over

longer distances (>5,500km) due to a modest cruise fuel burn advantage, while the Trent 1000 offers

better fuel efficiency over shorter distances due to improved climb fuel efficiency, which is a product of

RR’s continued usage of three-spool architecture (first employed by RR as far back as the RB211) as

compared to GE’s more conventional two-spool design.

GE/P&W Revenue & Backlog (USD mms.)

50,000

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

-

2010 2011 2012 2013

Revenue - GE Revenue - P&W Backlog - GE Backlog - P&W

P&W’s backlog includes an estimate of future service revenues

The extent to which GE’s market share lead on the 787 platform is due to any apparent technical

superiority is questionable in light of the influence of GE Capital. RR maintains a higher market share

among better capitalized airlines as well as with large lessors, suggesting that sophisticated buyers may

believe that RR will retain a lower lifetime cost of ownership, absent any financial incentive provided by

GE’s largesse. Furthermore, as previously mentioned, the question of one engine over another also likely

hinges on the planned mission of the aircraft, meaning that each engine retains advantages for different

length routes and environments, as well as the engine’s reliability, which is obviously not wholly

determinable ex-ante.

The GEnx has not been without teething problems, and the engine suffered several low pressure turbine

failures as well as a serious but contained failure on a GEnx powered 747 freighter, which GE attributed

to weather issues. It is worth noting that these types of issues are not terribly unusual for a new engine

architecture (or for new airframes for that matter), and barring any catastrophic uncontained failures

leading to a high-profile crash, are unlikely to deter customers, as was the case with RR’s Trent 900,

which experienced similar issues on a Quantas A380 flight in 2011. This tentative process of

troubleshooting and tweaking is inherent to engineering challenges of this complexity.

GE reportedly attempted to sell the GEnx to Airbus as an alternative to RR’s Trent XWB for the

A350XWB, with talks supposedly breaking down due to GE’s unwillingness to offer a wholly new,

upgraded engine for the A350XWB for fear of cannibalizing sales of the GE90-115B powered Boeing

777-200LR/300ER on which GE has exclusivity. GE also claims that the commercial logic was strained

due to the gradual upsizing over time of the 350 program by Airbus, with necessitated an increasingly

large range of thrust requirements which effectively demanded a wholly new engine. Given GE’s

previous commitments to the upgraded 777 variants, this was an investment which GE was unwilling to

make, while RR was reportedly only willing to do so after receiving a promise of exclusivity.

GE also competes head to head against the Trent 900 on the Airbus A380 via its Engine Alliance JV with

P&W, which produces the GP7200 engine, and maintains a slight market share advantage over RR with

12

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/201955% of orders to date. The GP7200, originally an orphan engine developed for the failed 747-500/600x

platform, was re-designed for the 380 as the GP7270 and GP7277. P&W has reportedly been frustrated

by GE’s unwillingness to bid for more airframes for the GP7200, but this is perhaps unsurprising given the

success of GE’s wholly owned, partially competing GEnx, suggesting that the Engine Alliance JV is

unlikely to have much of a future.

GE’s GE90 engine is an older, legacy

product of note, contemporaneous with the GE/P&W EBITDA Margin

Trent 800, and which continues to win 24.0%

orders on Boeing’s durable 777 family of

22.0%

aircraft. The GE90 was originally offered as

20.0%

one of the 3 options on the early 777-200, -

18.0%

200ER, and -300 variants, and competed

16.0%

with the Trent 800 and the P&W PW4000.

14.0%

RR’s initial market share lead on the 777

12.0%

was due to offering a middle ground

10.0%

between the dated technology offered by 2010 2011 2012 2013

the PW4000 and the GE90, which offered

the most modern technology but which was EBITDA Margin - GE EBITDA Margin - P&W

plagued by reliability issues at the time.

However, as Boeing sought to extend the 777 family with several updated, re-engined long range

variants, GE won exclusivity for future 777s by agreeing to contribute some $250mm to airframe

development costs. This move has proven to be wildly successful, as the upgraded, re-optimized

versions of the GE90, such as the GE90-110B1L/115BL/115B, solved the early reliability problems of the

GE90 and have become among the most successful widebody engine platforms to date, exclusively

powering the -200LR, -300ER, and 200F variants.

Pratt & Whitney – A Dormant 3rd Competitor in Widebody with a Narrowbody Foothold

Through the ‘80s and much of the ‘90s, P&W shared the widebody market with GE and RR was a distant

third to the American manufacturers. However, with the exception of its Engine Alliance JV which powers

the A380, P&W has not participated in a significant widebody aircraft platform since the mid ’90s when

the company experienced some limited success with modernized iterations of the older PW 2000 and

PW4000 engines. P&W’s example provides a cautionary tale of how a previously formidable competitor

lost its way by failing to be aggressive enough in investing in new engine architectures.

P&W’s travails started in the narrowbody market with its early failure to successfully win a position on the

Boeing 737 platform in the late ‘60s, losing out to the CFM56 in what was to become the most successful

commercial aircraft program of all-time. P&W would retain a significant foothold in the narrowbody

market, but did so only through the International Aero Engines (IAE) joint venture, of which P&W initially

held less than a 20% equity stake. This meant that P&W was a comparatively marginalized player in the

narrowbody market, a position which became increasingly problematic as the company failed to maintain

the initiative in its widebody engines.

P&W’s attempts to remain competitive in the widebody market by stretching the then-dated architecture of

the PW2000 and the PW4000 (which were contemporaries of the RB211) for the Boeing 757 and 777 in

the ‘90s resulted in these engines remaining 3rd choice options for carriers, winning only limited market

share compared to more modern engines offered by RR and GE. Following these setbacks, P&W took a

significant leap in opting to invest for the long-term in a comparatively radical ‘geared turbo fan’ (GTF)

architecture in hopes of restoring its commercial market share, a move which so far seems to have paid

off. This investment, along with its implications on the future of both the narrowbody and widebody

engine market, will be discussed more fully in the following section along with a more complete

discussion of the narrowbody market.

13

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019The Narrowbody Market – Present & Future

Outside of a handful of largely legacy engines powering small corporate and regional aircraft (some of

which remain in production), RR currently has no offering for narrowbody commercial aircraft, having sold

its interest in the highly successful IAE JV. The narrowbody aircraft engine landscape varies significantly

from the widebody market, and is primarily mentioned here to provide some insight into the possibility that

P&W is able to translate its recent success in narrowbody into future widebody engines with its potentially

revolutionary GTF technology. The narrowbody engine market is currently a duopoly between the

previously mentioned IAE JV and CFM International (CFMI), which is a 50:50 JV between GE Aviation

and SNECMA, a subsidiary of Safran SA. However, the competitive logic which sustained IAE has

dissipated and narrowbody will henceforth likely be a two-way contest between CFMI and P&W.

IAE’s sole commercial product was the spectacularly successful V2500 engine, which powers most of the

A320 family of aircraft and the now discontinued McDonnell Douglas MD90, first delivered to customers in

1988 and 1995, respectively. The V2500 competes on the A320 with the CFM International CFM56 and,

on a limited basis, with the P&W PW6000. CFM International’s CFM56, first delivered to defense

customers on a re-engined version of the KC-135R fuel tanker in the early ‘80s, has similarly been one of

the most commercially successful jet engine platforms of all time. The durable CFM56 was initially

developed commercially for the Douglas DC-8, but was to win its greatest success on the highly

successful Boeing 737 platform, as well as an option for variants of the Airbus 320 and as one of the

launch engines for the Airbus A340. These two engines will continue to power the majority of the global

narrowbody fleet for the immediate future.

RR’s widebody success with the Trent engine and the resurgence of P&W as a commercial aviation

competitor made the IAE joint venture a one engine proposition, however, and P&W is set to go it alone in

the narrowbody market with its potentially groundbreaking new engine, the PW1000G. The PW1000G’s

GTF concept, which has been in development since 1998, hopes to demonstrate the commercial

possibility of a concept that dates as far back as the ‘60s, and which has been used in a handful of small

commercial and regional aircraft to partial success. The GTF seeks to eliminate several intermediate

engine stages by the addition of a reduction gearbox, potentially offering significant fuel efficiency savings

through reduced weight at the potential expense of lower reliability.

The PW1000G seems to have won the tentative acceptance of customers so far, with P&W reportedly

recording more than 5,300 orders (including options) as of May 2014. P&W claims that its flight data

suggest performance modestly exceeding their own initial expectations and dismiss claims from CFMI

that its engine will be more expensive to operate due to higher maintenance costs. The acceptance of

the PW1000G by Lufthansa, generally regarded as being exceptionally diligent in its analysis of

prospective engine choices, has been highlighted as evidence that P&W has successfully solved the

engineering challenges of designing a gearbox capable of functioning effectively at the temperatures and

pressures demanded of it. P&W expects the PW1000G to enter service on the A320neo as an alternative

to CFMI’s proposed LEAP engine in Q4 2015 and as an exclusive on the second generation of Embraer’s

E-Jet series in 2018. The PW1000G will also be offered on the Mitsubishi Regional Jet, Bombardier

CSeries, and Irkus MS-21 platforms.

At the risk of oversimplifying, the two competing narrowbody engines are seeking to achieve similar

results by optimizing different criteria: propulsive efficiency in the case of the GTF, and thermodynamic

efficiency in the case of the LEAP engine (see our technical appendix for a more complete discussion of

these 2 engines). The two engines will compete head to head from the start on the Airbus A320neo, with

P&W so far maintaining a narrow lead over GE. It is worth noting that these technologies are by no

means mutually exclusive, and that if the GTF concept is sufficiently successful it is likely to be rapidly

incorporated by GE in future engine designs, on top of the existing thermodynamic efficiency gains made

by GE’s application of more advanced materials. Indeed, RR has already made announcements to this

effect, with its proposed Ultrafan concept incorporating elements of both of these engines for the next

generation of bidding opportunities in the mid-2020s.

14

Downloaded from www.hvst.com by IP address 172.20.0.10 on 09/10/2019You can also read