Whiplash: 2019's Changing Fortunes - Kathryn Downey Miller, CFA February 28, 2019 - EnerCom Dallas

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Whiplash: 2019’s Changing Fortunes

Kathryn Downey Miller, CFA

February 28, 2019

www.btuanalytics.com

info@btuanalytics.com

BTU Analytics

BTU Analytics is a data-driven energy market analytics firm focused on

providing clear and timely information to industry decision makers

• Clientele is spread across private equity, producers, service companies,

power providers, midstream, traders, and marketers

Consulting capabilities include:

• Natural gas, oil, and NGL market analysis

• Infrastructure development analysis

• Producer strategy advisory services

Products:

• Upstream Outlook

• E&P Positioning Report

• Oil Market Outlook

• Natural Gas Basis Outlook

• Henry Hub Outlook Report

• Production Scenario Analysis Tool www.btuanalytics.com

info@btuanalytics.com 2

Volatility: 2019’s New Normal?

Entering Winter

Today

2018/2019

WTI WTI

$71 $55

WTI Midland WTI Midland

($12.85) $0.95

Henry Henry

Waha Waha

$4.60 $2.66

($3.60) ($0.55)

www.btuanalytics.com

info@btuanalytics.com 33

Source: BTU Analytics, Bloomberg.

Key Takeaways

• Geopolitical risk returns – Venezuela, Iran, Saudi Arabia, Tweets

all have potential to impact crude market’s precarious balance

• US production growth will be lumpy due to infrastructure timing.

Historical pricing relationships will be change as today’s

bottlenecks ease and new constraints emerge

• Permian Basin dominates US oil and gas production growth in

2019 and beyond, and new infrastructure timing will have

significant pricing implications in 2019/2020

• Peak Appalachia is near, several producers have already grown to

meet FT commitments on new projects and Appalachian gas is

becoming the swing supplier of gas in the US market

• US natural gas demand growth gap approaching as LNG wave one

crests in 2019 www.btuanalytics.com

4

info@btuanalytics.com

Breakeven improvement stagnating, but prices do cover

wellhead economics across all major basins

WTI Price vs. Shale Play Wellhead Breakevens

$120.00

$100.00

$80.00

$/Bbl

$60.00

$40.00

$20.00

$-

14

15

16

17

18

19

4

5

6

7

8

l-1

l-1

l-1

l-1

l-1

n-

n-

n-

n-

n-

n-

Ju

Ju

Ju

Ju

Ju

Ja

Ja

Ja

Ja

Ja

Ja

Bakken Delaware Basin DJ Eastern Eagle Ford Midland Basin WTI

www.btuanalytics.com

info@btuanalytics.com 55

Source: BTU Analytics, Bloomberg. Available on Bloomberg terminals at BTUS .

Global liquids market was long by over 1.5 MMb/d in 2H 2018, leading OPEC and

partners to cut production by 1.2 MMb/d in 1H 2019. These cuts are necessary to

balance global markets as shown by the oversupply once cuts expire in 2H 2019

Global Liquids Supply/Demand Balance

2.5

2.0

1.5

1.0

MMb/d

0.5

0.0

-0.5

-1.0

-1.5

14

14

15

15

16

16

17

17

18

18

19

19

20

20

20

20

20

20

20

20

20

20

20

20

1Q

3Q

1Q

3Q

1Q

3Q

1Q

3Q

1Q

3Q

1Q

3Q

www.btuanalytics.com

info@btuanalytics.com 6

Source: BTU Analytics’ Oil Market Outlook (February 2019)US/Canadian incremental liquids growth in 2019 could meet all incremental

global demand growth relative to December 2018, necessitating OPEC

production cuts or other supply disruptions for full year 2019

Incremental Global Liquids Demand vs Incremental

Liquids Production*

2.5

2.0

Implied oversupply

without OPEC and

1.5 Russia production cuts

MMb/d

1.0

0.5

0.0

1Q 2019 2Q 2019 3Q 2019 4Q 2019

US/CN Other Demand

www.btuanalytics.com

info@btuanalytics.com 7

Note: Assumes status quo production from December 2018 i.e. no OPEC/Russia production cuts

Source: BTU Analytics’ Oil Market Outlook (February 2019)Should oil prices fall, US oil plays will be disproportionately impacted based on

a combination of factors including breakevens, transportation costs, and

producer hedging portfolios

Bakken Oil

Permian Oil

1.6

7.0 1.4

1.2

1.0

MMb/d

6.0

0.8

0.6

5.0 0.4

0.2

0.0

4.0 2018 2019 2020 2021

MMb/d

Base Case $60 WTI $50 WTI $40 WTI

3.0 Eagle Ford Oil

3.5

2.0 3.0

2.5

MMb/d 2.0

1.0

1.5

1.0

0.0 0.5

2018 2019 2020 2021 0.0

Base Case $60 WTI $50 WTI $40 WTI 2018 2019 2020 2021

Base Case $60 WTI $50 WTI $40 WTI

www.btuanalytics.com

info@btuanalytics.com 8

Note: Includes $7.50/bbl of cash leakage to cover corporate costs like SG&A and interest.

Source: BTU Analytics’ Cash Flow Production Tool (July 2018) and BTU Analytics’ Upstream Outlook (August 2018)A buildup of Permian DUCs should allow for accelerated growth once

infrastructure arrives and soften the impact of drilling slow downs expected

throughout 2019

Permian Wells Drilled vs Wells to Sale

7,000

6,000

5,000

# Horizontal Wells

4,000

3,000

2,000

1,000

-

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

DUCs & COBs Wells Drilled Wells Turned to Sale

www.btuanalytics.com

info@btuanalytics.com 9

Note: DUC = Drilled Uncompleted; COB = Completed on Backlog

Source: BTU Analytics’ Upstream Outlook (January 2019)Rapid development of debottlenecking projects and new pipelines will eliminate

bottlenecks for Permian crude, significantly improving differentials with bottleneck risks

moving to downstream markets

Permian Oil vs Regional Demand and Pipelines

9.0

Proposed Liberty Pipeline or

8.0 reversals from Cushing could add

supply to basin boosting long haul

Potential for

7.0 consolidation

utilization to Gulf Coast.

6.0 of projects

5.0

MMb/d

4.0

3.0

2.0

1.0

0.0

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Existing Pipe + Refining EPD NGL Conversion & BridgeTex Expansion

Cactus II EPIC

Gray Oak Permian Gulf Coast Pipeline

Wink to Webster Production Projection (No Constraints or Completion Delays)

Note: Pipeline capacities are based on current design capacities and does not include expansion capacity on EPIC, Gray Oak, PGC

www.btuanalytics.com

of ~935 Mb/d. Also does not include JupiterMLP’s proposed 1 MMb/d pipeline. Does not currently include potential inbound supply from 10

info@btuanalytics.com

Midcontinent

Source: BTU Analytics’ Oil Market Outlook (February 2019)Plenty of Permian pipe has been proposed, and it will be needed to support long term

development from the Permian. New projects will increase connectivity to Gulf Coast

demand and increase the Permian’s sphere of influence

Permian Dry Gas Production vs Takeaway

22.0 Company Pipelines

Capacity Official

Estimated ISD FID

(Bcf/d) ISD

20.0 ONEOK ONEOK West Texas Reversal 0.45 N/A 1/2019 Yes

Kinder/Targa/DCP Gulf Coast Express 1.92 10/2019 10/2019 Yes

Kinder/EagleClaw Permian Highway (PHP) 2.00 3Q 2020 11/2020 Yes

18.0

Targa/NextEra/White

Whistler 2.00 4Q 2020 12/2020 No

Water/MPLX LP

16.0

Tellurian Permian Global Access Pipeline 2.00 4Q 2022 1/2023 No

14.0 Williams Blue Bonnet Pipeline 2.00 4Q2020 N/A No

12.0

Bcf/d

10.0

8.0

6.0

4.0

2.0

0.0

10

11

12

13

14

15

16

17

18

19

20

21

22

23

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Local Demand Transwestern El Paso

NNG NGPL Eastbound*

Mexico ** Old Ocean & N TX Expansion ONEOK W TX Reversal

GCX Permian Highway Whistler Pipeline

Permian Global Access Dry Gas Production sans Shut-ins/Flaring

www.btuanalytics.com

Note: * Eastbound capacity is based on pipeline diameters and maximum daily flows. ** Mexico pipeline capacity is risked by timing of 11

info@btuanalytics.com

downstream pipeline bottlenecks in Mexico to connect inbound US supply to demand centers and based on expected outbound Permian flows

Source: BTU Analytics’ Upstream Outlook (January 2019)Marcellus and Utica production growth, once dictated by infrastructure build-out, will

move to become the marginal gas supply in the US and with production dictated by

macro supply and demand factors

BTU Analytics Appalachia Production Forecast

45

40

35

ain ed

nstr

30

C o US Marginal Supply

25 e line

Pip

Bcf/d

20

15

10

5

-

14

16

18

20

22

24

20

20

20

20

20

20

NE Appalachia SW Appalachia Pipeline Takeaway Capacity

12

www.btuanalytics.com

info@btuanalytics.com

Source: BTU Analytics (updated 1/2019)Appalachian producer guidance indicates a shift from rapid growth in

previous years to significantly slower growth in 2019

Average Production Growth YoY and Producer Guidance Actual

50% Production

Growth

40%

30%

20%

10%

0%

COG AR RRC EQT CNX SWN GPOR Average Basin

Growth

-10%

15 - '16 16 - '17 17 - '18 High Case '18 - '19 Low Case '18 - '19

13

www.btuanalytics.com

info@btuanalytics.com

Source: BTU Analytics’ Gas Basis Outlook, Bloomberg production data, investor materials (updated 2/2019)Significant inventory depletion of gas focused shale plays over the next

decade will drive the marginal cost of gas production higher without

continued efficiency improvements

Gas Focused Remaining Locations by Breakeven

20,000

16,000

12,000

8,000

4,000

0

Appalachia SW Appalachia NE Haynesville Cotton Valley Fayetteville

Sub $2.00 $2.00-$3.00 $3.00-$4.00 $4.00-$5.00 Over $5.00 2019-2024 Drilling Forecast

www.btuanalytics.com

info@btuanalytics.com

Note: Assumes futures strip of 12/31/2018; 5-yr wellhead oil average of $50.14/Bbl

Source: BTU Analytics’ E&P Positioning ReportDue to constraints, Permian associated gas has pressured adjacent basins,

depressing prices, and forced supply to compete for limited demand in the

Upper Midwest. However, now new supply is converging on Northern

Louisiana at Perryville

W. C

ana

da

Limited

Demand

Displaced Rockies Market

Appa l a

chia

n

e rmia

P

OK/

a

chi

a l a

Growing p

SCOOP/STACK Ap

ian

Perm

OK

Perm

i an

Permian Perryville

Perm

ia n

Growing

Demand

www.btuanalytics.com

info@btuanalytics.com 15

Source: BTU Analytics’ Gas Basis Outlook (updated 2/2019)With the start of Midship, MEP and Gulf Crossing will allow increased

flows into Northern Louisiana

Bennington

Tolar

Carthage Perryville

Waha

Katy

HSC

STX

www.btuanalytics.com

info@btuanalytics.com 16

Source: BTU Analytics’ Gas Basis Outlook (updated 2/2019)Midship capacity will help SCOOP and STACK producers, but congestion

unlikely to be completely alleviated as volumes grow to fill capacity

Oklahoma Capacity Changes in 2019

1.6 1.44 Bcf/d

1.4

1.2

1.0

0.45 Bcf/d

Bcf/d

0.8

0.6

0.34 Bcf/d 0.35 Bcf/d

0.4

0.3 Bcf/d

0.2

0.0

Midship Capacity ONEOK Reversal Pipeline Bottlenecks Volume Growth in 2019 Spare Capacity

www.btuanalytics.com 17

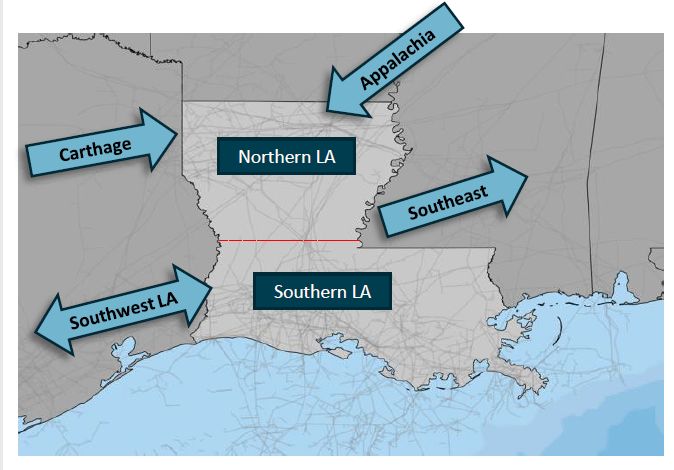

Source: BTU Analytics, Genscape, Updated December 12, 2018 info@btuanalytics.comMore supply can get to Northern Louisiana, but a bottleneck is

emerging in the middle of Louisiana

Bennington

Tolar

Carthage Perryville

Waha

Katy

HSC

STX

www.btuanalytics.com

info@btuanalytics.com 18

Source: BTU Analytics’ Gas Basis Outlook (updated 2/2019)Flows from Northern LA are creeping towards full utilization.

Expansion projects could add up to 1 Bcf/d of additional corridor capacity, BTU assumes

expansions likely entered service in 4Q2018 or 1Q2019

North LA to South Flows versus Capacity

10.0 100%

8.0 80%

Pipeline Utilization

6.0 60%

Bcf/d

4.0 40%

2.0 20%

0.0 0%

-2.0 -20%

5

6

7

8

15

16

17

18

l-1

l-1

l-1

l-1

n-

n-

n-

n-

Ju

Ju

Ju

Ju

Ja

Ja

Ja

Ja

CGT ANR TGP

Trunkline TGT GulfSouth

Acadian Capacity Utilization

www.btuanalytics.com

info@btuanalytics.com 19

Note: Pipeline capacities based on maximum north or southbound observed flows and compressor station capacities

Source: BTU Analytics, SONRIS, Data as of Dec. 31, 2018The Gulf Coast will continue to play a larger role in the US demand mix, but

‘LNG Gap’ is ahead

Louisiana and Texas Demand

40.0% 1

Exports Drive Shift in US

Demand Dynamics

TX and LA % of Total US Demand

30.0% 9

20.0% 6

10.0% 3

0.0% 0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Other Industrial LNG Mexican Exports TX and LA % of US Demand

www.btuanalytics.com

info@btuanalytics.com 20

Source: BTU Analytics’ Henry Hub Outlook (January 2018)Contact Us: 720.552.8040

info@btuanalytics.com

165 S. Union Blvd., Suite 410

Lakewood, CO 80228

BTU Analytics provides data-driven, market-risk assessments and due diligence analysis for acquisitions and divestitures of oil, NGL, and natural gas assets in

North America. We utilize our in-depth understanding of North American energy data to help clients determine the future value of upstream, midstream,

and downstream assets in the face of ever-evolving market conditions.

DISCLAIMER. THIS REPORT IS FURNISHED ON AN “AS IS”BASIS. BTU Analytics, LLC DOES NOT WARRANT THE ACCURACY OR CORRECTNESS OF THE REPORT OR THE INFORMATION CONTAINED THEREIN. BTU Analytics, LLC MAKES NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE USE OF ANY

INFORMATION CONTAINED IN THIS REPORT IN CONNECTION WITH TRADING OF COMMODITIES, EQUITIES, FUTURES, OPTIONS OR ANY OTHER USE. BTU Analytics, LLC MAKES NO EXPRESS OR IMPLIED WARRANTIES AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANT- ABILITY OR

FITNESS FOR A PARTICULAR PURPOSE.

RELEASE AND LIMITATION OF LIABILITY: IN NO EVENT SHALL BTU Analytics, LLC BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL, INCIDENTAL, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFIT) ARISING OUT OF OR RELATED TO THE ACCURACY OR CORRECTNESS OF THIS REPORT OR

THE INFORMATION CONTAINED THEREIN,WHETHER BASED ON WARRANTY, CONTRACT, TORT OR ANY OTHER LEGAL THEORY. 21You can also read