2019 Edition SATELLITES TO BE BUILT & LAUNCHED BY 2028 - Euroconsult

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

22th Edition

2019 Edition

SATELLITES TO BE BUILT & LAUNCHED

BY 2028

A complete analysis & forecast of satellite manufacturing &

launch services

An Extract

A Euroconsult Research Report

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release

ABOUT THIS RESEARCH REPORT

SCOPE

Satellites to be Built & Launched by 2028 is a required reading for

anyone interested in the business generated by satellite systems

and their launches. The report is fully updated, providing all the

key figures and analysis needed to understand the global space

market, and the future opportunities & challenges.

EXTENSIVE FIGURES & ANALYSIS FOR THE COMING

DECADE

All Euroconsult research has, at its core, data derived from over

30 years of tracking all levels of the satellite/space value chain. To

this we add dozens of dedicated industry interviews each year,

along with the continual refinement of our data models, and the

collection and interpretation of company press releases and

financial filings. Our consultants have decades of experience

interpreting and analyzing our proprietary databases in light of the

broader value chain.

When you purchase research from Euroconsult, you receive

thousands of data points and the expert interpretation of what this

means for specific verticals and sectors of the satellite value

chain, including forecasts based on years of data and highly

refined models. 6,000€

INCLUDED IN THIS PRODUCT Single user report incl. efiles

• Forecast up to 2028 in units, mass and value

Enterprise license available

• All segments of the value chain reviewed

• Satellite forecast database included

Purchase the report at our online shop

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 2

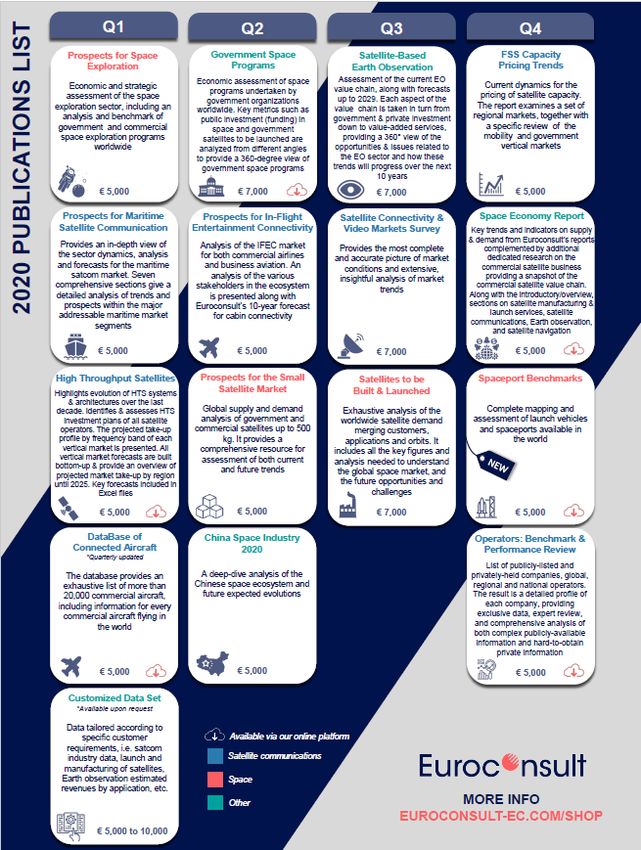

TABLE OF CONTENT 1/2

INTRODUCTION 02\ COMPETITIVE ENVIRONMENT AND PERFORMANCE OF MARKET PLAYERS

4 PURPOSE 42 THE SPACE INDUSTRY GLOBALLY

5 EXECUTIVE SUMMARY SATELLITE MANUFACTURING INDUSTRY

7 SCOPE & DEFINITIONS

8 LESSON LEARNED 45 2019 FOR THE SATELLITE MANUFACTURING INDUSTRY – NEW

9 METHODOLOGY 46 STRATEGIC ISSUES – NEW

10 METHODOLOGY : FOCUS ON CONSTELLATIONS – NEW 47 STRUCTURE OF THE INDUSTRY

11 RESULTS OF CONSTELLATION STATUS ASSESSMENT – NEW 50 THE COMMUNICATION SATELLITE INDUSTRY

12 RESULTS OF CONSTELLATION MATURITY ASSESSMENT – NEW 54 FINANCIAL PERFORMANCE

13 ACRONYMS 56 SATELLITE MANUFACTURERS MARKET SHARE

57 DISTRIBUTION OF SATELLITE MANUFACTURERS

01\ STRATEGIC ISSUES & TRENDS FOR SATELLITE 60 INNOVATIONS

MANUFACTURING AND LAUNCH INDUSTRIES 65 DIVERSITY OF PLATFORM – NEW

66 EVOLUTION OF PLATFORMS

15 2019 FOR THE SATELLITE INDUSTRY – NEW 70 NON GEO SATELLITE INDUSTRY

16 2019 FOR THE LAUNCH INDUSTRY – NEW 74 PROFILES OF 10 COMPANIES

17 WHAT TO EXPECT FOR 2020 – NEW 75 SATELLITE ORDERS BACKLOG – NEW

19 THE BIG PICTURE IN THE SATELLITE INDUSTRY

20 A NEW TYPOLOGY OF THE DEMAND

LAUNCH INDUSTRY

SATELLITE FORECAST 90 2019 FOR THE LAUNCH INDUSTRY

21 TYPE OF SATELLITE OPERATOR 91 STRATEGIC ISSUES

22 APPLICATIONS 92 STRUCTURE OF THE INDUSTRY

23 REGIONS OF SATELLITE OPERATOR 93 GLOBAL DISTRIBUTION OF ORBITAL SPACEPORTS AND LAUNCH VEHICLES

24 ORBITS IN 2019

25 # OF SATELLITES – NEW 98 FINANCIAL PERFORMANCE

26 MASS TO BE LAUNCHED – NEW 90 LAUNCH SERVICE PROVIDERS MARKET SHARE

27 INDUSTRY REVENUES – NEW

28 MANUFACTURING REVENUES BY ORBIT & BY CLIENT 91 THE GTO LAUNCH INDUSTRY

29 LAUNCH REVENUES BY ORBIT & BY CLIENT 109 LEO LAUCH INDUSTRY

30 THREE DISTRIBUTIONS OF FUTURE SPACE INDUSTRY 110 LAUNCH RATES – NEW

REVENUES 111 INNOVATIONS – NEW

31 DEMAND AND SUPPLY DISTRIBUTION 2009 TO 2018 – NEW 112 LAUNCH BACKLOG – NEW

113 PROFILES OF 4 COMPANIES

MARKET DRIVERS

33 CONCENTRATION ALONG THE VALUE CHAIN

34 NEW USER REQUIREMENTS ARE DRIVING CHANGES – NEW

35 SATELLITE OPERATORS MITIGATING UNCERTAINTIES – NEW

36 FLEXIBILITY TO MITIGATE MARKET UNCERTAINTIES – NEW

37 INNOVATIONS ALL ALONG THE VALUE CHAIN

38 TECHNICAL RISKS ALSO PART OF THE ECONOMIC EQUATION

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 3

TABLE OF CONTENT 2/2

03\ COMPETITIVE ENVIRONMENT AND PERFORMANCE OF MARKET PLAYERS

120 TRENDS FOR COMMERCIAL DEMAND

121 DEMAND FOR COMMERCIAL SATELLITES

122 THE THREE ORBITS (GEO, MEO, LEO) ARE NOW COMMERCIAL

125 COMMERCIAL SPACE STILL MEANS COMMUNICATION SATELLITES

126 THE COMMERCIAL MARKET BY APPLICATION

134 GEO COMSAT MARKET DEMAND AT A TURNING POINT– NEW

140 GEO COMSAT DEMAND CYCLE – NEW

141 HIGH-THROUGHPUT PAYLOADS FOR BROADBAND COMMUNICATION

145 COMSAT MARKET DRIVEN BY CONSOLIDATION OF EXISTING OPERATORS & BY NEW ENTRANT

146 EIGHT COMSAT CONSTELLATIONS, OF WHICH SEVEN FOR BROADBAND COMMUNICATIONS

150 COMMERCIAL EARTH OBSERVATION

151 IN-ORBIT SERVICING OF COMSAT SYSTEMS

04/ GOVERNMENT SATELLITE DEMAND

153 TRENDS FOR GOVERNMENT DEMAND – NEW

154 GOVERNMENT MARKET HIERARCHY – NEW

155 MARKET HIERARCHY BETWEEN CUSTOMERS, APPLICATIONS AND REGIONS

161 GROWTH IN FUTURE GOVERNMENT DEMAND IS DRIVEN BY CIVILIAN SATELLITES

162 EARTH OBSERVATION DOMINANT FOR CIVILIAN SATELLITES

168 ASIA DOMINATES CIVILIAN SATELLITE MARKET AND THE USA THE MILITARY MARKET

170 NEWCOMER SPACE COUNTRIES

172 MARKET DYNAMICS BY ORBIT: LEO, MEO, GEO, ESCAPE

180 MARKET DYNAMICS BY APPLICATION: COMSAT, NAVSAT, METSAT, EOSAT, SECURITY …

05/ SATELLITE BACKLOG AND FORECAST

BACKLOG OF COMMERCIAL SATELLITES UNDER CONSTRUCTION TO BE LAUNCHED FROM JAN. 2019

EUROCONSULT’S FORECAST OF GOVERNMENT SATELLITES TO BE LAUNCHED OVER 2019–2028

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 4

EXECUTIVE SUMMARY

SATELLITE INDUSTRY EXPERIENCING DISRUPTION

Over the next 10 years, Euroconsult anticipates that anticipates an average of 990

satellites will be launched every year for the next ten years, regardless of their

2009 2018 2019 2028 mass*. The demand is experiencing a x4 increase with 9,900 satellites to be launched

by 2028 compared to the to 2,300 satellites launched during the last decade. With a 4Y

CAGR of 21% between 2019 and 2023 in number of satellites, the industry is

Average number of satellites launched per year experiencing a quick and radical transformation regarding the number of satellites,

value and mass highlighted by the following trends:

• From 2019 to 2028, manufacturing and launch services combined should reach a

market value of $292 billion of which 75% concentrated by satellite manufacturing

230 990 and 25% for launch activities.

• Commercial satellite operators are experiencing significant changes that are part of

a long term from a legacy GEO comsat broadcasting business to more data centric

use cases. Euroconsult estimates that the demand to build and launch Telecom

satellites will reach a yearly average of $8 billions.

Top 3 applications (satellite manufacturing and launch value)

• Constellations in LEO and MEO will concentrate 77% of the demand in satellites

36% 31% whilst GEO will only retain 4% but still concentrate 39% in value. 55 commercial

28% 27% constellations projects (of more than 5 satellites each) will launch a total of 6,600

13% 15%

satellites.

• Smallsat broadband mega-constellations are becoming a reality by entering

deployment phase after the successful in-orbit validation of prototypes and the

latest financing rounds of the most advanced projects, OneWeb and Starlink. Other

EO TELECOM SECURITY TELECOM EO SECURITY projects out of the smallsat range are gearing up too (Telesat, Kuiper) but have yet

to commit to their suppliers. These four mega constellations (Oneweb, Starlink,

Telesat and Kuiper) accounting for 39% of the demand (i.e. 3,900 satellites) with

different go-to-market and vertical integration strategies.

*Manned spaceflight application is not included in the scope of this report

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 5

EXECUTIVE SUMMARY • Civil government agencies* are the first customers of satellites, with 40% of the demand

in value, above defense and commercial operators. Expansion of space science,

exploration and earth observation are driving the demand. On the defense side, a

2009 2018 2019 2028 transformative period is starting with program replacement and enactment of new

strategies within each of the incumbent players like the U.S., China, Russia, Japan, India

and Europe.

Most dominant orbits • For manufacturers, the commercial GEO comsat market is showing signs of recovery

(# of satellites, mass and manufacturing & launch value) from the previous years’ downturn with 10 satellite orders to date, making 2019 better in

orders compared to 2017 and 2018. The market is also experiencing a growing diversity

of satellite platforms. Airbus or Maxar have secured first orders for fully reconfigurable

SSO LEO broadband payloads enabling satellite operators to mitigate evolution of their vertical

(920 sats) (6,630 sats) markets. At the lower end of the spectrum, a few smallsat missions are also under

integration for the same purposes.

• The access to space industry is diversifying with new smallsat dedicated launchers

becoming a reality, such as Rocket. In this segment, dozens of launchers are under

T T development around the world, with different levels of maturity. A new generation of GTO

capable launchers will be entering the market within the next two years with a design to

GEO GEO LEO GEO cost focus. Meanwhile, SpaceX’s semi reusable launcher has been widely accepted by

(1,492 Tons) ($106 billion) (1,658 Tons) ($103 billion) satellite operators, and fully reusable launchers are entering their development phase.

THE WORLD’S SATELLITE MARKET OVER TWO DECADES (according to NEW SCOPE FOR THE 2019 EDITION

Euroconsult’s 2019 forecast) For this edition, the scope of the report was extended to include the global satellite demand,

2009–2018 2019–2028

Growth regardless of the satellites’ mass (previous editions included satellites with a launch mass

rate >50 kg). This new scope aims to provide a global overview of the satellite demand and

2,298 9,935 includes the impact of the growth of smallsat (LESSON LEARNED FROM OVER 20 YEARS

METHODOLOGY

Euroconsult’s satellite forecast versus market reality throughout

7 editions of its Survey The methodology and segmentation for this report has been consistent

throughout all editions of the survey since its first release 22 years ago. If

% of difference in number of satellites per comparable period between forecast and reality improvements have been introduced in the granularity of the forecast, the

two basic principles have remained the same:

90% • Mutually exclusive and completely exhaustive segmentation (see below)

Euroconsult surplus

Constellation in order to be representative of the whole space industry (but to avoid

Non-GEO overestimate vs.

double counting);

reality

70% GEO

• Large constellation projects (as of today or in the late 1990s) always

individualized for comparison to be consistent over the long term.

50% The quantitative forecast model includes three stages of assumptions:

• Number of satellites to be launched over the next 10 years—Some of

them are already under construction (see next page), but most of them

30%

remain to be funded, including commercial constellations;

Euroconsult deficit

• Mass of the satellites to be launched, according to a mass distribution

10% model by application/orbit presented in Parts 3 and 4; and

• Cost to build and launch the satellites, based on specific prices to build

1997-2006 1998-2007 2000-2009 2002-2011 2004-2013 2007-2016 2009-2018 and launch them. The price per kilogram varies according to the supplier

-10%

21 years of comparison possible origin, the mission of the satellite, the payload and the orbit.

SATELLITE LAUNCH MASS

-30% Average launch mass per application is assumed for satellites when it is

not otherwise known or easy to estimate on a case-by-case basis (see

satellites nominatively in part 5).

A reality check of Euroconsult’s forecast has been conducted in preparation for the

2019 edition of the survey. The number of GEO and non-GEO satellites launched in SPECIFIC PRICES ($ PER KG)

the past ten years (2009–2018) was compared with our forecast for that period. In Future satellite manufacturing and launch prices are estimated based on

the 2009 edition of our survey that covered that period, we had a non-GEO surplus historical price data points that allow correlating a given mass with a given

of 11% and a GEO deficit of -3%. price to derive specific prices, i.e., price per kilogram. Change in average

2010 Edition was the first one since 2000 to underestimate the non-GEO segment specific prices per satellite category or launch category were assumed for

(mainly commercial constellations) whereas previous editions corrected previous the next decade (2019-2028) relative to the past decade (2009-2018). The

over-estimates Our deficit in GEO forecast reflects a higher-than-expected resiliency revenues of satellite manufacturing and launch are annualized (i.e. not

of the GEO comsat market after crisis time. In the early 2010s, government comsat 100% of the revenue is recognized at launch year). Satellite manufacturing

systems compensated for the slowdown in commercial comsat more than expected. prices differ according to the application of the satellite system, the payload

and the origin of the satellite integrator. Satellite launch prices differ

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT according to the final orbit and the origin of the launch provider. The origin

© Euroconsult 2019 – Approved for public release of the supplier and the mass category are also considered. 72019 FOR THE SATELLITE INDUSTRY 500

400

104 satellites >500 kg

300

The satellite industry

generated 200

386 smallsats**

$27.9 billion for 100

0

both manufacturing and 2008 2010 2012 2014 2016 2018 20

launch

Technology

29%

The U.S. accounted

for 57% of the demand

490 Telecom

35%

EO

277 launched* in 2019 17%

Telecommunication

in 103

satellites

was the 1st application with

173 satellites

LEO/SSO

10

concentrated both the

heaviest payloads (225

tons) and the highest

number of satellites 389 t

(438) commercial launched

GEO comsat ordered

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release * Inclusive of all missions **Satellites with a launch mass < 500 kg2019-2028 TRENDS FOR THE SATELLITE INDUSTRY

4,3

67%

x

Of future demand in

number of satellites driven

by 75 commercial

constellations By average

990

Growth in number of

2009 - 2018 38% 62%

71% 29%

satellites compared to

2019 - 2028 33%

77%

67%

23% last decade

62%

Single satellite Satellite within constellation (but only x 1,7 in mass)

satellites to

Projects of

Earth

be launched

every year by 2028 20 countries

will launch their first

Observation ever satellite

constellations

20 with more

than 10

¾

satellites each

of the satellite

In both # of satellites (4,842 demand in value

units) and mass (2,300 will be

tons) Telecom will be the concentrated

largest application by satellite

manufacturing

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release2019-2028 TRENDS FOR THE MANUFACTURING INDUSTRY

5 manufacturers have Smallsats** will account for 87%

5 fully reconfigurable

satcom payloads

are now marketed by suppliers

concentrated of the # to be launched but only

55% 13% in value

of the satellites

manufacturing revenues

between 2009-2018

Diversity of commercial 7.075 tons

i.e. $94 billions 300 kg

Astranis-1

GEO comsat satellite Telstar 19V

(2020) (2018)

In 2019 satellite

manufacturers generated Manufacturers looking

to address constellation’s

$21.4 needs by adapting capabilities

Billions to mass

production and

i.e. 77% of the satellite

industry’s revenues

standardization

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT **Satellites with a launch mass < 500 kg

© Euroconsult 2019 – Approved for public release2019-2028 TRENDS FOR THE LAUNCH INDUSTRY 100 Smallsat dedicated launchers at

Various development stage

In 2019 launch service

providers generated

2,298 $6.5

Billions

Satellites i.e. 23% of the satellite

industry’s revenues

Launched

in 754 launches

Between 2009 and 2018 satellites will need 4 new GTO

capable

67% launches in Low Earth launchers will be

Orbit i.e. 1,657 Tons available by 2021

(H-3, Ariane 6, Vulan, New Glenn)

¼ of the launch

vehicles lifted

3/4 9m

of the 6 methane fueled

rocket engines

19m

Starship

Satellites under Payload

launched development Fairing

with a focus on size

lowering cost,

reusability and

more efficiency

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release4 COMPLEMENTARY ACTIVITIES

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 12RESEARCH

Research products covering

Since its incorporation, Euroconsult has been the full satellite value chain

running permanent research programs;

collecting, updating and assessing detailed market,

industry, policy, program and financial information

to produce a range of high quality research

products:

Forecasts based on over three decades of data

and highly refined models,

Millions of data points with expert

interpretation of what this means for specific

verticals and sectors,

Key reference tool used by most public and

private stakeholders,

Full list of our research products available at

euroconsult-ec.com/research

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public release 13SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT © Euroconsult 2019 – Approved for public release 14

CONNECT WITH US

HEADQUARTERS | FRANCE

86 boulevard de Sebastopol

75003 Paris

Tel: +33 (1) 49 23 75 30 www.euroconsult-ec.com

U.S.A.

4601 n. Fairfax drive, suite 1200

Arlington, VA 22203

Tel: +1 (703) 520-6415

CANADA

465 rue McGill, suite 1103

Montreal (qc) h2y 2h1 consulting@euroconsult-ec.com

Tel: +1 (514) 750-9698

reports@euroconsult-ec.com

JAPAN

1-5-212, Iwaicho, Hodogaya

summits@euroconsult-ec.com

Yokohama, 240-0023

Tel: +81 80 2052 1348

training@euroconsult-ec.com

SATELLITES TO BE BUILT & LAUNCHED BY 2028 // AN EXTRACT

© Euroconsult 2019 – Approved for public releaseYou can also read