2021 half-year results 5 August 2021 - Hammerson

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 half-year results

5 August 2021

1

The Oracle, Reading

Agenda

Overview

Financial results

Strategy update

Q&A

2

Overview

Progress against FY20 priorities

Balance sheet Strategy Operational

Strengthened capital structure Update on portfolio & organisational reviews Rent collection improving(1)

£403m of disposals, including French presented today: FY20 now at 90%

minority stakes Simplify organisation by more efficient HY 21 at 71%

Issue of €700m 1.75% sustainability- structures and platform

linked bond

Footfall c.80% pre-Covid levels

Redeemed €500m 2022 bond & 53% New leadership:

of 2023 €500m bond CFO with experience in transformation

Leasing volumes improving (+£5.4m on H1

£297m of private placement notes & technology

20, £+1.4m on H1 19)(2)

repaid Expertise in repositioning of assets and

Right categories and structures

£415m RCF maturing 2022 refinanced development

to £200m of facilities maturing 2026 Strong pipeline

Net debt reduced from £2.2bn to £1.9bn

No significant unsecured maturities until 2025

1

2

Rent collection was FY20 89%, HY 21 68% as at 9 July 2021

Flagships only

3

Half-year results

Westquay, Southampton

2021 half-year financial results

H1 headline results

30 June 2021 30 June 2020 Change

Income statement Adjusted net rental income (£m)(1) (2) 87.2 94.4 (8%)

LFL NRI (£m) 67.7 0 67.60 0.1%

Premium outlets earnings (£m)(3) (2.0) (7.4) 73%

Adjusted earnings (£m) 20.1 17.7 14%

IFRS loss (£m)(4) (375.5) (1,088.4) 65%

30 June 2021 31 Dec 2020 Change

Balance sheet Managed portfolio value (£m)(1) 3,596 4,414 (19%)

Value Retail net asset value (£m) 1,130 1,154 (2%)

Net debt (£m)(1) (1,879) (2,234) 16%

Value Retail value (£m) 1,902 1,924 (1%)

Value Retail net debt (£m) (690) (689) 0%

EPRA NTAPS (p) 69 82 (16%)

1 Figures on a proportionally consolidated basis excluding Value Retail.

2 Calculated on an adjusted basis to exclude the change in the provision for amounts not yet recognised in the income statement 5

3 30 June 2020 includes VIA Outlets earnings of £5.6m which was disposed of on 31 October 2020

4 Includes revaluation deficit on Group portfolio including Premium Outlets of £361.2m (30 June 2020: £939.6m)

2021 half-year financial results

Adjusted earnings walk

slide 41

H1 2021 Adjusted earnings walk (£m)(1)

Surrender premiums 11.3

20.0 Provisions 6.2

Tenant failure,

18.0 leasing, and void (9.2)

costs

16.0 Concessions (6.6)

14.0 11.3

7.8

Variable income

(1.6)

and other

12.0 LFL NRI 0.1

10.0 20.1

17.7

8.0

5.0

6.0

4.0

8.3 8.8

2.8

2.0 4.9

1.3

0.0 0.4 0.1

(2) (3)

H1

Jun 2020

2020 Disposals Other NRI D&O insurance Other net FX & tax LFL NRI Net interest Value Retail H1

H1 2021

2021

admin

1 At constant FX

2 Disposals include VIA H120 earnings of £5.6m and year on year change in NRI for H121 disposals 6

3 Other NRI reflects year-on-year non-LFL changes in NRI on Les 3 Fontaines, Cergy, which is undergoing a major extension, and assets classified as Developments and UK Other portfolio

2021 half-year financial results

Premium outlets earnings walk

slides 56-60

H1 2021 Premium outlets earnings walk (£m)(1)

5.0 (2.0)

3.0

5.6 1.3

1.0

2.7

-1.0 (2.0)

1.3 (0.3)

-3.0

(13.0)

-5.0

2.7

-7.0 2.5

-9.0

-11.0 4.8

-13.0

VIA Outlets Value Retail GRI Property operating Net administration Interest Tax Value Retail

H1 2020 H1 2020 costs costs H1 2021

Premium outlets H1 2020 -£7.4m

1 At constant FX 7

2021 half-year financial results

NTAPS walk

H1 2021 EPRA NTAPS walk (pence)

90

80

9

70 3 1

60

50

40 82

69

30

20

10

0

(1)

Dec 2020 Revaluation deficit Scrip dividend Loss on disposal Jun 2021

EPRA NTA EPRA NTA

1 On a proportionally consolidated basis including Value Retail 8

2021 half-year financial results

Rent collection performance(1)

slides 42-43

Total Demanded Total Waived, Total Due Total Collected Total Outstanding Collected of due

in Quarter Written Off and as at 30th July

Not Yet Due

£m £m £m £m £m %

FY20 261 28 233 210 23 90%

Q1 21 58 13 45 36 9 79%

Q2 21 54 - 54 34 20 64%

H1 21 112 13 99 70 29 71%

Q3 21 43(2) 2 41 27 14 65%

2021 YTD 155 15 140 97 43 69%

Collections:

• Key priority to maximise income and collection rates in H2 2021, good progress made since 9 July

• Trade receivables reduced in the UK as restrictions are lifted and concessions agreed, France and Ireland lagging at balance sheet date

• Extension of moratorium on rental collection ‘inexplicable’

Level of provisioning marginally increased from FY20:

• Maintain a prudent provisioning approach, and limitations on collection powers in UK.

• Provisions for arrears at 30 June 2021 £77m, 67% (31 Dec 20: £80m, 64%)

• Provisions for tenant incentives at 30 June 2021 £55m, 24% (31 Dec 20: £68m, 22%)

1 Excludes Value Retail

2 Decline in total demanded in Q3 predominantly reflects disposal of retail parks portfolio to Brookfield completed on 19 May 2021 9

2021 half-year financial results

Portfolio valuation summary(1)

Sector Value H1 2021 ERV & other Yield Peak to ERV Yield shift Yield range

30 June capital impact impact date decline from 30 June

2021 return decline(2) from peak(3) 2021(3)

£m peak(2)

Managed portfolio

UK 1,320 (13.4%) (6.7%) (6.7%) (60%) (29%) +294bp 6.8% - 9.5%

France(4) 1,023 (4.2%) (2.0%) (2.2%) (25%) (4%) +59bp 4.6% - 6.3%

Ireland 679 (6.6%) (0.3%) (6.3%) (28%) (14%) +91bp 5.2% - 5.7%

Total flagships 3,022 (8.9%) (3.7%) (5.2%)

Developments &

UK Other

574 (9.5%) (9.1%) (0.4%)

UK RPs - (8.8%) (8.8%) -

Managed

portfolio

3,596 (9.0%) (4.6%) (4.4%)

Value Retail 1,902 (0.4%) (0.4%) - (7%)

slide 47-48

Total 5,498 (6.4%) (3.4%) (3.0%)

1

2

At Hammerson share, translated at 30 June 2021 FX rate

Like-for-like cumulative capital return since peak values (December 2017 – UK & France, December 2018 – Ireland, December 2019 – Value Retail)

10

3 Nominal equivalent yield

4 France includes Italik which has been reclassified to Trading properties as at 30 June 20212021 half-year financial results

Net debt analysis

Net debt analysis (£m)(1)

2,400

Adj. operating profit 62

2,300

Working capital

(14)

2,200 changes

2,100 Cash generated from

48

operations

2,000

396

1,900

50

1,800 2,234 77 103

1,700

48 13

1,829 1,879

1,600

1,500

1,400

Net

Netdebt

debt Disposals

(2)

Exchange and other Cash generated from Dividends Interest

(5)

Capital expenditure Net

Netdebt

debt

11Jan

Jan 2021

2021 flows

(3)

operations (4) 30

31Jun

Dec 2021

2020

1

2

On a proportionally consolidated basis, excluding Value Retail

Reflects net proceeds from the sale of eight retail parks portfolio, Espace St. Quentin and Nicetoile

11

3 Includes favourable foreign exchange translation of £80m

4 Includes withholding tax of £12m in relation to the 2020 interim dividend

5 Interest includes redemption costs of £14m and purchase of interest rate swap for £21m2021 half-year financial results

Debt maturity profile

Debt maturity profile - pro forma (£m)(1) (2) Refinancing achieved

1,200 Sterling Euro bonds

• €700m 1.75% 6 year sustainability-linked bond

bonds 1.8% avg

4.7% avg coupon

• 2022 bonds repaid (62% in H1, 38% on 8th July, €500m total)

coupon

• 2023 Euro bonds (53% repaid in H1, €265m)

New RCF(3)

1,000 Private Secured debt

placement 2.1% avg • £415m 2022 RCF refinanced (with two new facilities totalling £200m 3+1+1 year RCF)

2.4% avg coupon

coupon • Private placement notes due in June 2021 (£113m) repaid on maturity and 46%

800 (£184m) of notes prepaid at par

Revolving credit facilities

floating rate • O’Parinor JV debt (€55m at 25% share) refinanced with new €53m loan on 6th July

600

Liquidity position (£m)

400 £m

RCF – fully undrawn 1,030

Cash 587

200

Total liquidity 30 June 2021 1,617

July refinancing(2) (165)

0

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 Pro forma liquidity 1,452

1 Proportionally consolidated debt, excluding Value Retail. Interest rates are on a weighted average basis, post hedging derivatives

2 Pro-forma for final €190m repayment of 2022 Euro Bonds and refinancing and €2m partial repayment of O’Parinor JV debt in July 2021 12

3 New 3+1+1 year RCF shown at current maturity, with options to extend, subject to lender consent, to 20262021 half-year financial results

Balance sheet metrics

slide 50

30 June 2021 31 Dec 2020

Net debt £1,879m £2,234m

Value Retail net debt £690m 0 £689m 0

Group debt Headroom Internal 30 June 2021 31 Dec 2020

covenants guidelines

Gearing(1) 1.75x 1.83x 1.89x

Interest cover(3) >1.25x 40% NRI decline >2.00x 2.08x 1.81x

LTV – incl. Value Retail net asset value(4) no covenants IG rating 40% 40%

LTV – fully proportionally consolidated(5) no covenants IG rating 47% 46%

Net debt/EBITDA(6) no covenants IG rating 15.1x 14.1x

1 Covenant within the Group’s unsecured bank facilities, bonds and private placement notes

2 2021 Covenant within the Group’s unsecured private placement notes only. Covenant was temporarily amended to 1.25x between June 2020 and June 2021, before reverting to 1.40x in October 2021 and 1.50x in December 2021 13

3 Covenant within the Group’s unsecured bank facilities and private placement notes

4 Loan excludes Value Retail net debt and value includes Value Retail net asset value

5 Includes Group’s share of Value Retail net debt and property values

6 EBITDA calculated on a 12 months rolling basis as at 30 June 20212021 half-year financial results

Modelling assumptions

UK rental levels: declining c.35% peak to trough (29% to date), France and Ireland more stable

Rent collections: rates continue to improve, absent further lockdowns, 80-90% by FY21 –

provisioning rates flat

Net admin costs: assume same run rate in H2, 15-20% savings to come in FY22-23

Value Retail: H2 earnings to exceed H2 20 (£5.9m) – assume no cash distribution

Finance costs: annualised run rate saving of £10m

FY 21 capex guidance: £100m, of which £64m in H2 21 (c.50% Cergy and Italik)

Dividends: assume further c.£210m of scrip by end of 2022 to cover REIT/SIIC obligations

14Strategy update

15

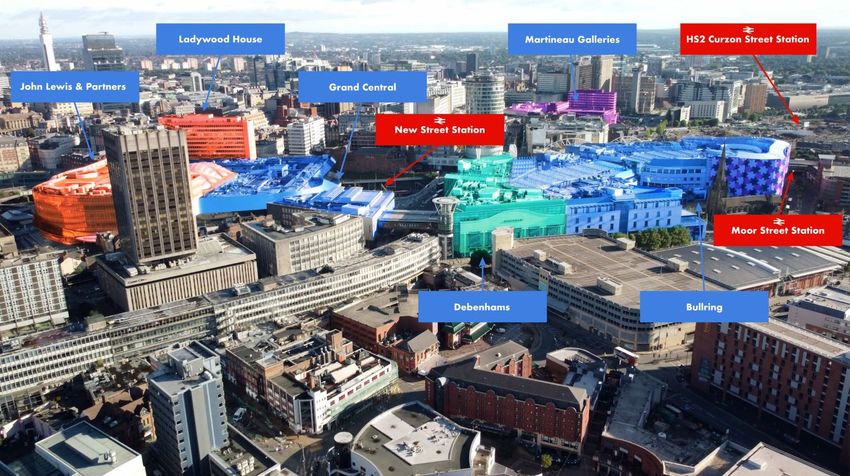

Martineau Galleries, BirminghamStrategy update

Future of Hammerson

Owner, operator, developer of focused, prime, urban estates

Indicative long-term core portfolio

Precarious capital structure Sustainable capital structure

Costly, complex organisation Agile, lean, streamlined platform

Complex, retail-only portfolio Reinvigorated mixed-use portfolio

Lack of focus on strategic

Accelerated development pipeline

opportunities

Department store Non fashion retail Fashion retail F&B and leisure Alternative use

16Strategy update

Existing asset footprint and structural shift in retail underpins our strategic choices

Area Strategic options

Disposals to focus

Scale Maintain status quo Consolidate

on core assets

Refocus / Enter logistics &

Mix Grow emphasis industrial

Re-enter office Enter lodging

rebalance

on residential at scale at scale

retail at scale

Footprint Concentrate footprint in set

Maintain status quo Enter new territories

of core urban estates

Model Develop, own,

Asset light Pure developer Financial investor

operate

17Strategy update

Covid-19 has accelerated existing structural change

DEMOGRAPHIC TRENDS CONSUMER TRENDS RETAIL TRENDS

Ageing population Value for money Polarisation of retail markets

Rise in single-person households Digitalisation Channel shift

Increased digital penetration Experience over things Evolving role of the store

Urbanisation Connected self Commercial model evolution

Changing consumer confidence Value of time Data & analytics

High and increasing avg. income Personalisation Importance of technology

Source: Accenture 18Strategy update

Prime urban retail has an important role to play in the omnichannel environment,

but reduction of space required

Forecasts for UK retail space reduction Encouraging re-opening sales despite restrictions

Low High

-6% -14%

Market CBRE Cushman & BNPP Savills

UK May & June France June overall

Net 16% Wakefield 30% 40% overall sales vs 2019 sales vs 2019

Vacancy (2021) 25-30% (2021) (2020)

14% (2019)

Physical sales & fulfilment remains key to profitability Role of physical space in omnichannel world

• c.70% of UK retail sales remain physical, c.80% in France & Ireland1 • Not only about legacy metrics, but also marketing and brand exposure

• Falling average retailer pre-tax profit margins in UK: • New technology = new metrics, comparable to online:

• Passing footfall = brand impressions

• Dwell time outside shopfront = click through

9.2% 5.5% 3.2%

2010-11 2019-20 2024-25 • Complementary to existing metrics:

• Conversion rates

• Customer acquisition costs

• Online costs rising through pandemic: delivery & fulfilment costs +20%;

fashion returns >40%; paid search +26%; social media +25% • Logistics returns costs

slide 40

19Strategy update

Hammerson today – high quality assets; strong locations; overexposed to fashion

and department stores

Asset quality by grade(1) Portfolio by city exposure(2) Portfolio mix by ERV and NIA(3)

Birmingham London Leeds Aberdeen

Other Value 7% 6% 3% 3% 1%

B Retail 7%

14%

17% Southampton By ERV

1% A++

B+ 3% 9% 6%

23%

20% Bristol 8%

26%

3%

By NIA

Reading

14%

2%

A- 79% of assets

10% graded A

A+ Leicester

15% Bicester 2% 28%

17% 19% 27% 41%

Glasgow

A

1%

31% Dublin

14% Paris

Marseille 12%

Black border indicates significant 10% Department store Fashion Non-fashion

JV/associate structures F&B / Leisure Other Vacant

Initial diagnosis stands: we will capitalise on the competitive advantage of the quality

and location of our core assets, with clear valuation upside from repositioning.

1 As at 30 June 2021, UK, Ireland and France flagships, and Value Retail. Source: Green Street Advisors database July 2021, quality grade, 20

weighted by value as of FY20, at Hammerson share

2 As at 30 June 2021

3 As at 30 June 2021, excluding Value RetailStrategy update

Positioning Hammerson as an owner, operator, developer of focused, prime,

urban estates

Deliver Accelerate

Create agile Reinvigorate

sustainable development

platform the assets

capital structure pipeline

• Disposals of non strategic • Flatter organisation • Generate incremental cash • Disciplined capital recycling

assets: • Automation and digitalisation flow to scale development

• reduce net debt • Build skill sets for the future • Optimise use of space – opportunities

• generate capital for • Speed to value/opportunity minimise void • Explore different models

reinvestment ready • Repurposing & redevelopment • Create holistic prime urban

• IG credit rating estates

• Disciplined capital allocation

• Simplify portfolio & platform - focus on core assets • Net positive/sustainability lens over all initiatives

Capital redeployment & value

Stabilisation & simplification

creation

21Strategy update

A sustainable capital structure remains a core near term priority

FY 20 HY 21

€700m

£834m rights Recycling

£403m of sustainability- Further

issue & VIA Refinancing capital

disposals linked bond disposals

disposal Refinancing

issued

Approach through the cycle:

• Focus on total return

• IG credit rating

• Balance LTV & net debt/EBITDA depending on

phasing of disposals and redeployment of capital

22Strategy update

Strategic repositioning of portfolio

Near term disposals Optimise to sell Core

• Minority stakes (lack of control) • Opportunities to create more • Prime city centre locations in most attractive catchments:

value prior to disposal

• Better off in the hands of others • >250k people within 15 minutes / 1 mile

• More liquid assets • Not the right time to sell • >1m people within 1 hr walk/cycle/public transport or car

• Non core for the business • Opportunities for remix/repurposing/development

• Income growth potential

• Ability to scale: asset value potential c.£1bn for some, with at least

three non-retail uses with potential for >£100m value each

• Opportunities to consolidate ownership

• Support from central / local public leadership and policy

NEAR-TERM DISPOSALS MEDIUM-TERM DISPOSALS

depending on market conditions depending on asset conditions

Market conditions and third party interest will drive

individual assets and portfolio disposals

23Strategy update

Create agile platform for the benefit of all stakeholders

AMBITION

Create an efficient & agile, fit for purpose organisation

Develop a more empowered, accountable culture - conducive to delivering speed to value

Current organisation Future organisation

Capable, recognised platform Flatter organisational structure

High commitment from teams Asset-centric operations

Centralised core functions

New senior leadership in place

Fill capability gaps and build expertise

High cost

Explore strategic partnerships

Fragmented operating model

Increase automation & digitalisation

Complex and bureaucratic

Renewed focus on cost discipline

Nascent automation and digital capability

Net admin costs reduced by 15-20%

24Strategy update

Significant value creation opportunities from reinvigorating current prime portfolio

Generate incremental income Lease up & shift mix Repurpose

• Commercialisation • Minimise void • Capital light & more intensive options

• Last mile delivery • Try new concepts • Alternative use: residential; workspace;

• Operating services lodging

• Digitalisation/Data • Target categories: F&B; leisure; culture; services

Opportunity in underutilised space(1)

• 2m sq ft UK department store space, 800k sq ft department store space vacant or in temporary leases: £3/sq ft ERV; £9/sq ft value

• Ten UK car parks; four in France; one in Ireland: c.47k spaces

• 1.9m sq ft UK MSU space; 540k sq ft French MSU space; 220k sq ft Irish

• c. 600k sq ft targeted for repurposing/new lettings in UK

1 At 100% 25Strategy update

Leasing highlights

slide 35-39

Prime brands

New anchors

F&B, leisure, grocery, services

Digitally - native

26Strategy update

Wide variety of scale development opportunities, yielding returns and upscaling

existing assets to neighbourhoods

Retail F&B Leisure Residential Workspace Hotel Education Culture

Public spaces

Outline Earliest (k sq ft) (k sq ft) (k sq ft) (units) (k sq ft) (beds) (k sq ft) (k sq ft)

Key schemes Area planning/ start on

policy site

Les 3 Fontaines, Cergy 8,400m2 on site on site 10 20 45

The Podium at Dundrum, Dublin 10,000m 2

2022 1 107

Near term

Victoria Hotel, Leeds 8,400m 2

On hold 205

25,600m2

St Peters Lane, Leicester 2021 2022 305

Residential Quarter, Reading TBC- 2022 TBC

Victoria Phase 2, Leeds 10 acres TBC 50 50 50 1000 540 200 55 50

Martineau Galleries, Birmingham 7.5 acres H2 2023 90 70 20 1300 1100 200 10

Medium to long term

Callowhill Court, Bristol 9 acres 2022 TBC

Dublin Central 6 acres 2021 H1 2023 60 40 94 475 210

Dundrum Village, Dublin 6 acres 2022 H2 2023

Pavilions Phase 3, Swords 18 acres 2023 TBC

Brent Cross 15 acres TBC TBC

Croydon 22 acres TBC TBC

The Goodsyard, London 10 acres 2024 120 75 500 1400 150 40

TOTAL 103 acres 6m sq ft 4.5m sq ft 1m sq ft

27Case study:

Birmingham Estate

28Strategy update

Evolution of Hammerson: retail-centric assets to mixed use estates

Indicative evolution of identified core portfolio mix by NIA

Core portfolio by current mix Indicative mid-term core portfolio Indicative long-term core portfolio

Department store Fashion retail Non fashion retail F&B and leisure Alternative use

29Strategy update

Summary and priorities – Hammerson at inflection point

Clear direction of travel: owner, operator, developer of focused, prime, urban estates

H1 21 progress: Near-term priorities: Looking ahead:

• Balance sheet strengthened: • Disposals to reduce debt • Sustainable capital structure

• net debt reduced; • IG credit rating

• refinancing achieved • Create agile platform

• cost reduction 15-20% • Focus on core - simplify the

• Business transformation underway: portfolio

• new leadership in place • Improve rent collection

performance • Maximise existing and incremental

• Improving operational performance: cash streams

• rent collection up; • Maintain leasing momentum

• encouraging leasing volumes • Commence recycling of capital to

& pipeline value creation opportunities

• Seek options to accelerate scale

development pipeline

30Questions

Dundrum, DublinAdditional disclosure

32

Cabot Circus, BristolContents

Managed portfolio

Net Positive

Value Retail

33Managed portfolio

34

The Oracle, ReadingAdditional disclosure: Managed portfolio

Leasing cumulative activity – managed portfolio

H1 2021 managed portfolio leasing and cumulative vs. H1 2020 and H1 2019 (£m) Leasing volumes H1 21 H1 20

£m £m

5 12

UK 4.3 2.7

4.5

10 France 5.1 1.4

4

3.5 Ireland 0.4 0.3

8

3

Total 9.8 4.4

2.5 6

2

4 UK retail parks 1.2 1.6

1.5

1 UK other 0.2 0.5

2

0.5

Managed portfolio 11.2 6.5

0 0

March

May

February

January

June

April

Monthly leasing H1 2021 (LHS) Cumulative leasing activity 2019 (RHS)

Cumulative leasing activity 2020(RHS) Cumulative leasing activity 2021 (RHS)

1 Monthly leasing LHS axis, cumulative leasing RHS axis 35Additional disclosure: Managed portfolio

Leasing cumulative activity – UK flagships

H1 2021 UK flagships leasing and cumulative vs. H1 2020 and H1 2019 (£m) H1 2021

leasing

5 5 £m

4.5 4.5

Principal leasing 2.5

4 4

3.5 3.5

Reconfigurations 0.5

3 3 Flexible and other 1.3

2.5 2.5

Total 4.3

2 2

1.5 1.5

1 1

0.5 0.5

UK flagships leasing key facts(1)

0 0 Leasing vs. Dec 20 ERV -24%

March

May

February

January

June

April

Leasing vs. previous passing -26%

Monthly leasing H1 2021 (LHS) Cumulative leasing activity 2019 (RHS) Average lease term: 8 years(2)

Cumulative leasing activity 2020 (RHS) Cumulative leasing activity 2021 (RHS)

Average incentive: 11 months(2)

1

2

Principal leases only

FY 2020: average lease term 6 years, average incentive 5 months

36Additional disclosure: Managed portfolio

Leasing cumulative activity – France flagships

H1 2021 France flagships leasing and cumulative vs. H1 2020 and H1 2019 (£m) H1 2021

leasing

£m

1.2 4.5

Principal leasing 4.0

4

1.0

Reconfigurations 0.5

3.5

Flexible and other 0.6

0.8 3

Total 5.1

2.5

0.6

2

0.4 1.5

France flagships leasing key facts(1)

1

0.2 Leasing vs. Dec 20 ERV 3%

0.5

Leasing vs. previous passing 0%

0.0 0

Average lease term: 10 years(2)

March

April

May

February

January

June

Average incentive: 2 months(2)

Monthly leasing H1 2021 (LHS) Cumulative leasing activity 2019 (RHS)

Cumulative leasing activity 2020 (RHS) Cumulative leasing activity 2021 (RHS)

1

2

Principal leases only

FY 2020: average lease term 7 years, average incentive 1 months

37Additional disclosure: Managed portfolio

Leasing cumulative activity – Ireland flagships

H1 2021 Ireland flagships leasing and cumulative vs. H1 2020 and H1 2019 (£m) 2021 leasing

£m

0.1 1.2

Principal leasing 0.1

0.1

1 Reconfigurations 0.1

0.1

Flexible and other 0.2

0.1 0.8

Total 0.4

0.1

0.6

0.0

0.0 0.4

Ireland flagships leasing key facts(1)

0.0

0.2 Leasing vs. Dec 20 ERV 16%

0.0

Leasing vs. previous passing 72%

0.0 0

Average lease term: 9 years(2)

March

April

May

February

January

June

Average incentive: 4 months(2)

Monthly leasing 2021 (LHS) Cumulative leasing activity 2019 (RHS)

Cumulative leasing activity 2020 (RHS) Cumulative leasing activity 2021(RHS)

1

2

Principal leases only

FY 2020: average lease term 6 years, average incentive 2 months

38Additional disclosure: Managed portfolio

Leasing analysis by type – flagships

UK France Ireland

% vs previous % vs previous % vs previous

£’000s % vs ERV £’000s % vs ERV £’000s % vs ERV

passing passing passing

Principal 2,470 -26% -24% 3,958 0% 3% 119 72% 16%

Other 1,873 -76% -76% 1,125 -49% -28% 263 -75% -80%

Total 4,343 -53% -63% 5,083 -13% -5% 382 -38% -72%

UK France Ireland

% vs previous % vs previous % vs previous

£’000s % vs ERV £’000s % vs ERV £’000s % vs ERV

passing passing passing

Fashion 2,446 -47% -57% 2,596 -15% 0% 114 -79% -89%

Non Fashion 1,479 -68% -70% 2,079 -6% -12% 266 60% -6%

F&B 418 -54% -58% 408 -23% -1% 2 n/a -97%

Total 4,343 -53% -63% 5,083 -13% -5% 382 -38% -72%

39Additional disclosure: Managed portfolio

White box leasing – new metrics relevant to digitally-native brands

Use of physical space is evolving in omnichannel world

• Hammerson “white boxing” initiatives encouraging digitally native

brands into physical space

• Not only about legacy metrics, e.g. sales and OCRs, but also

marketing and brand exposure

• New technology, e.g. AI in CCTV, is allowing development of new

metrics, comparable to online:

• Passing footfall = brand impressions

• Dwell time outside shopfront = click through

First store outside of London for omnichannel retailer of rare sneakers

• Complementary to existing metrics:

Additional 9% footfall in store zone in first week

• Conversion rates

3.5p cost per walk by / brand impression

• Customer acquisition

15% of passing visitors entered store

• Logistics returns costs

3x footfall/sq ft of neighbouring leading brands

High average basket size

Cost of acquisition only 3% of sales

40Additional disclosure: Managed portfolio

LfL NRI analysis - flagships

H1 2021 LfL NRI analysis Ireland flagships Total

UK flagships France flagships

(2.7%

Surrender Premiums 27.0% 6.2%

)

16.7%

(7.8%

Provision for incentives and arrears(1) 15.2% 9.9%

)

9.2%

(0.9%

Other 2.1%

)

0.7% 1.3%

(2.8%

Variable income (5.5%) 1.4%

)

(3.6%)

(10.8 (0.6% (0.3%

Tenant failure (CVAs/Administrations) %) ) )

(6.7%)

(13.7

Leasing and void costs %)

2.0% 4.1% (6.9%)

(12.0 (4.2% (8.2%

Concessions %) ) )

(9.8%)

Total LfL NRI (£m) £41.5m £13.8m £12.4m £67.7m

Change LfL (%) +2.3% +13.6% -17.0% +0.1%

Change LfL (£m) +£0.9m +£1.7m -£2.5m +£0.1m

1 Excludes provisioning for arrears from tenants subject to CVA or administrations which have been included in the tenant restructuring category 41Additional disclosure: Managed portfolio

Rent collection performance - flagships

UK France Ireland

Collected at 31 July Collected at 31 July Collected at 31 July

(%) (%) (%)

FY20 91 93 83

Q1 21 92 67 64

Q2 21 71 43 66

H1 21 79 56 65

Q3 21 67 60 67

2021 YTD 76 57 65

42Additional disclosure: Managed portfolio

Provisions for arrears – managed portfolio

H1 2021 provisions vs FY 2020

Provision as % Provision as %

Net trade Change since Change since

Provisions at Provisions at of net trade of net trade

receivables 31 December 31 December

30 June 2021 31 Dec 2020 receivables receivables

at 30 June 2021(1) 2020 2020

at 30 June 2021 at 31 Dec 2020

£m £m £m £m % % ppts

UK 64.1 42.1 53.1 -11.0 66 65 +1

France 34.9 24.4 18.9 +5.5 70 66 +4

Ireland 15.9 10.9 7.8 +3.1 69 53 +16

Managed

114.9 77.4 79.8 -2.4 67 64 +3

portfolio

1 Net of VAT and deposits 43Additional disclosure: Managed portfolio

Tenant restructuring – leases in CVA/admin as at 30 June 2021

UK France Ireland UK Group NRI LfL impact of CVAs & admins (£m)

flagships flagships flagship other

H121 FY20 FY19

5

Passing rent impact of (0.6) (0.2) - - (0.8)

new units in CVA/admin 0

in H1 21(£m)

(5)

Number of units in 132 31 n/a 12 175

CVA/admin (10)

as at 30 June 2021

(15)

Passing rent subject to 5.1 2.1 n/a 0.3 7.5

CVA/admin as at (20)

30 June 2021 (£m)

(25)

% of Group passing rent 2.2% 0.9% n/a 0.1% 3.3%

as at 30 June 2021(1) (30)

(35)

(40)

UK flagships France flagships Ireland flagships UK Retail Parks

1 Group passing rent £227.3m 44Additional disclosure: Managed portfolio

Top 20 tenants exposure(1)

Rental Rental

% of passing % of passing

Retailer Exposure % of NIA Retailer Exposure % of NIA

rent rent

(£m) (£m)

Inditex 8.1 3.6% 2.7% TK Maxx 2.3 1.0% 1.6%

H&M 6.1 2.7% 2.5% Superdry 2.3 1.0% 0.6%

Next 4.5 2.0% 4.5% Signet 2.2 1.0% 0.2%

Boots 3.7 1.6% 1.3% Apple 2.1 0.9% 0.4%

Watches of Switzerland

JD Sports 3.3 1.4% 0.8% 2.0 0.9% 0.2%

Company

CK Hutchison Holdings 3.0 1.3% 0.7% Natl Amusements (UK) 1.9 0.8% 1.5%

River Island Clothing Co 2.9 1.3% 1.0% McDonald's 1.7 0.8% 0.5%

Marks & Spencer 2.9 1.3% 3.2% Etam Group 1.5 0.7% 0.2%

France Printemps (Borletti) 2.5 1.1% 1.8% Debenhams 1.5 0.7% 2.1%

John Lewis PLC 2.4 1.1% 6.5% Freedom Sportsline 1.4 0.6% 0.3%

Total 58.5 26% 33%

1 Ranked by passing rent as at 30 June 2021 45Additional disclosure: Managed portfolio

Top ten occupiers by region(1)

UK France Ireland

Rental % of Rental % of

Rental % of

Retailer exposure passing % of NIA Retailer exposure passing % of NIA

Retailer exposure passing % of NIA

(£m) rent (£m) rent

(£m) rent

Inditex 4.4 1.93% 1.60% Printemps 2.5 1.12% 1.83% Inditex 1.9 0.84% 0.39%

Next 3.6 1.60% 4.12% Inditex 1.8 0.79% 0.70% River Island 1.7 0.73% 0.24%

H&M 3.5 1.53% 1.78% H&M 1.8 0.78% 0.42% Marks & Spencer 1.1 0.49% 0.82%

Boots 3.0 1.32% 1.12% Etam Group 1.5 0.67% 0.22% Primark 0.9 0.39% 0.35%

John Lewis PLC 2.4 1.05% 6.53% C&A Europe 1.2 0.52% 0.51% Next 0.9 0.39% 0.34%

JD Sports 2.3 1.03% 0.60% Rallye 1.0 0.44% 0.42% H&M 0.8 0.37% 0.30%

Signet 2.1 0.93% 0.22% FNAC Group 0.9 0.39% 0.63% Boots 0.7 0.33% 0.19%

CK Hutchison Holdings 2.1 0.92% 0.55% Monoprix 0.9 0.38% 0.28% TK Maxx 0.7 0.32% 0.51%

Watches of Switzerland 2.0 0.90% 0.20% Grand Vision 0.8 0.37% 0.16% JD Sports 0.6 0.25% 0.15%

Natl Amusements (UK) 1.9 0.83% 1.55% Happy Chic 0.8 0.33% 0.10% Staunton Sports 0.6 0.25% 0.19%

Total 27 12% 18% Total 13 6% 5% Total 10 4% 3%

1 As at 30 June 2020 46Additional disclosure: Managed portfolio

Valuation data (net initial & nominal equivalent yields)(1)

NIY (%) UK flagships France flagships Ireland flagships UK other Managed portfolio(2)

30 June 2021 6.7 4.3 4.9 5.3 5.5

31 Dec 2020 6.6 4.4 4.6 6.2 5.7

30 June 2020 5.9 4.3 4.6 5.9 5.4

Change 6m (pp) 0.1 -0.1 0.3 -0.9 -0.2

Change 12m (pp) 0.8 0.0 0.3 -0.6 0.1

NEY (%) UK flagships France flagships Ireland flagships UK other Managed portfolio(2)

30 June 2021 7.8 5.0 5.3 9.4 6.4

31 Dec 2020 7.3 4.9 5.0 9.0 6.3

30 June 2020 6.6 4.7 4.7 8.6 5.9

Change 6m (pp) 0.5 0.1 0.3 0.4 0.1

Change 12m (pp) 1.2 0.3 0.6 0.8 0.5

1

2

Yields as reported at period end, i.e. not like for like

Total portfolio for 31 December 2020 and 30 June 2020 include Retail Parks

47Additional disclosure: Managed portfolio

Valuation data (ERV)

ERV (£m) UK flagships France flagships Ireland flagships UK other Managed portfolio(2)

30 June 2021(1) 122.0 59.6 37.4 9.9 228.9

31 Dec 2020(1) 132.4 62.9 39.0 10.0 279.7

30 June 2020(1) 144.2 64.7 42.0 10.2 299.3

LfL change 6 months (%) -6.8 -0.3 -1.1 -3.5 -4.1

LfL change 12 months (%) -14.4 -1.0 -4.4 -5.3 -9.3

1

2

ERVs as reported at period end, i.e. not like for like

Total portfolio ERVs for 31 December 2020 and 30 June 2020 include Retail Parks

48Additional disclosure: Managed portfolio

Key disposals achieved 2019 – 2021 YTD

NIY Gross proceeds Buyer

(%) £m

2019:

Dallow Road, Luton 7.6 24 Private equity

Italie Deux, Paris (75%) 4.1 363 AXA

Abbotsinch, Paisley 7.8 67 Ashby Capital

St Oswald's Retail Park, Gloucester 8.5 54 Local authority

Parc Tawe, Swansea 4.7 22 Private investor

2020:

Abbey, Belfast 8.4 33 Slate Asset Management

SQY Ouest n/a 10 Société des Grands Magasins

Retention of exchange deposit for portfolio of retail parks n/a 21 Orion European Real Estate Fund V

VIA 6.5 277 APG

2021 YTD:

Brent South Shopping Park 6.2 22 London Borough of Barnet

Nicetoile 5.8 23 Allianz

Espace Saint Quentin 8.5 28 Allianz

Retail parks portfolio 8.6 330 Brookfield

Total 2019 – 2021 YTD(1) 1,288

1 Total annual gross proceeds (includes ancillary disposals): 2019 - £542m, 2020 - £343m, 2021 YTD (30 June 2021): £403m

49Additional disclosure: Managed portfolio

LTV methodology

30 June 2021 31 December 2020

With Value Fully proportionally consolidated With Value Fully proportionally consolidated

Retail net asset (£m) Retail net asset (£m)

Net debt value (£m) value (£m)

Managed portfolio 1,879 1,879 2,234 2,234

Value Retail - 690 - 689

Loan 1,879 2,569 2,234 2,923

Property values

Managed portfolio 3,596 3,596 4,414 4,414

Value Retail - 1,902 - 1,924

Value Retail net assets 1,130 - 1,154 -

Value 4,726 5,498 5,568 6,338

LTV 40% 47% 40% 46%

50Additional disclosure: Managed portfolio

Maintenance capex 2018- H1 2021: Flagships

H1 2020 2019 2018

2021

Service charge (maintenance)

Service charge income (£m) 24 55 69 73

Maintenance expenditure within service charge (£m) 3.5 13 13 13

Examples:

Painting, flooring upkeep, M&E: CCTV, wifi , IT systems maintenance

Capital expenditure

Gross rental income (£m) 102 229 282 306

Capital expenditure – no additional area (£m) 8 17 16 53

Yield on cost from capital expenditure – no additional area 0 0 3 6

(%)

Capital expenditure – no additional area: gross rental income (%) 8 7 7 17

Examples:

Income accretive: Repurposing and reconfiguration, recladding, CCTV upgrade, digital screens

Other (partly recoverable from tenants): Wayfinding projects, WC upgrades, LED relamping, seating upgrades, family rooms, smart metering

51Net Positive

Our Sustainability 2021 Half year update

Vision: Operations remain affected by COVID-19 but strong sustainability platform has supported

efficient operation and delivery of two key projects. We are continuing to focus on

To create retail destinations that delivering against out Net Positive carbon, water, waste and social impact targets through

deliver net positive impacts efficiencies and investment in technology and innovation projects and through our strong

relationships with community organisations.

economically, socially and

environmentally

Key projects delivered

Positive Places is our strategy

for making that happen • the connection of Les Terrasses du Port to the Thassalia geothermal system

• the successful launch of our sustainability linked bond (SLB)

EPRA LFL Portfolio (unit) H1 2021 H1 2019 % Change 2021

Target

Energy demand (MWh) 33,710 40,505 -17% -8%

Carbon emissions (mtCO2e) 6,442 9,101 -29% -17%

Water demand (‘000m3) 108 183 -41% -7%

53Additional disclosure: Net Positive

Sustainability-linked bond

Issued in June 2021 and confirmed as being beyond business as usual and Paris aligned, our sustainability-linked bond (“SLB”) links ambitious Scope 1,2 and 3 targets to financing without restricting our use

of proceeds. This was the first SLB to be issued by a real estate company and reaffirms the strength of our sustainability strategy.

KPI 1 – Absolute Emissions KPI 2– Absolute Emissions

16,000 80,000 71,742

14,000 13,357 70,000

12,000 60,000

10,000 50,000

8,000 40,000

6,000 5,343

30,000 35,527

4,000 20,000

60% reduction versus 50% reduction versus

2,000 2019 Baseline 10,000 2019 Baseline

0 0

2019 2020 2021 2022 2023 2024 2025 2019 2020 2021 2022 2023 2024 2025

BAU Scope 1, 2 & selected Scope 3

KPI 1 - Hammerson Scope 1, 2 & selected Scope 3 targets BAU Scope 3 tenant emissions KPI 2 Hammerson Scope 3 tenant emissions targets SPT 2

Sustsainability Performance Target 1

Performance to date:

During H1 2021, Scope 1 and 2 emissions for this portfolio* have fallen by 10% v 2020 and 36% v 2019 baseline. These reductions are significantly influence by the closure of assets during the pandemic. However we are

continuing to invest in energy efficiency measures and our procurement strategy and expect to revert to a more normal downwards trend in 2022. Scope 3 emissions performance will be calculated at year end. However, 50

units have been fitted out in accordance with our energy efficiency standards in H1 2021 and environmental data sharing clauses included in new leases as standard.

If these targets are not met, an additional margin will be payable of 37.5 basis points per annum for the last year of the bond between June 2026 to the June 2027 maturity date for each of the two targets, 75 basis points in

total, payable at the final interest payment date.

Notes: Emissions forecasts are location based and reflect a Steady Progress Future Energy Scenario

BAU reflects only forecast grid carbon emissions reductions for GB, Ireland and France, provided by Aurora Energy Research reflecting an adapted Steady Progress Future 54

Energy Scenario. It excludes any corporate carbon reduction activities.

The portfolio includes all assets under Hammerson ownership during the reporting period at equity share. The same portfolio is reflected in each trajectoryValue Retail

55Additional disclosure: Value Retail

H1 2021 operational update

30 June 30 June Change Value Retail value creation (£m)

2021(1) 2020(1)

Brand sales (£m) 626 585 +7%

Footfall (m) 8.5 8.8 -3%

Sales density (£/m2)

1,200 9 year IRR - 18%

3.1 3.3 -4%

Like-for-like NRI (£m) 24.9 16.8 +48% 1,000

Occupancy (%) 95.3 94.7 +0.6%

800

950

600

1,107

400 (147)

280

(190)

200

214

0 (2)

NAV Jan-12 Capital invested Distributions - Distributions - Valuation uplift NAV Jun-21

operating refinancing

1

2

With the exception of like-for-like net rental income growth, figures reflect overall portfolio performance, not Hammerson’s ownership share

Premium outlets NAV as at 30 June 2021 includes liabilities in respect of distributions received in advance of £23m which will be repayable upon disposal of stakes in Value Retail

56Additional disclosure: Value Retail

Tiered European outlet market

Sales densities €/m2

€30,000+ International fashion and

luxury brands

€2,000–€10,000

Mainstream fashion brand outletsAdditional disclosure: Value Retail

Value Retail villages

Bicester Village, Oxford

GLA: 28,100m2

Boutiques: 163

La Roca Village, Barcelona

GLA: 25,900m2

Boutiques: 148

Las Rozas Village, Madrid

GLA: 16,600m2

Boutiques: 100

La Vallée Village, Paris

GLA: 21,600m2

Boutiques: 105

Maasmechelen Village, Brussels

GLA: 20,000m2

Boutiques: 100 Portfolio value

Fidenza Village, Milan

GLA: 21,100m2

Boutiques: 116

£1.9bn

Wertheim Village, Frankfurt

GLA: 21,200m2

Boutiques: 118

Ingolstadt Village, Munich

GLA: 21,000m2

Boutiques: 114

Kildare Village, Dublin

GLA: 16,200m2

Boutiques: 97

58Additional disclosure: Value Retail

Hammerson’s total investment in Value Retail

Holding companies 25%

equity

Las Rozas La Vallée Maasmechelen Wertheim Ingolstadt Kildare

Bicester Village La Roca Village Fidenza Village

Village Village Village Village Village Village

37 29 25 14 14 22 33 2 29

50 41 38 26 27 34 45 15 41

Village ownership

via LPs (%)

Total Village

ownership (%) (1)

1 Total Village ownership calculated as economic entitlement of directly held and indirectly held interests 59Additional disclosure: Value Retail

Absolute sales growth delivered through active management,

acquisitions and extensions

Sales and Sales Growth 2012 – 2021 (€m)(1)

3,500

+9%

+8%

3,000 +8%

+8%

2,500 +11%

+11%

+12%

2,000 -45%

+13%

1,500

1,000 +7%

500

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

H1 Sales H2 Sales

1 Figures have been restated at constant FX rates

60You can also read