2021 Market Prospects and Sustainable Financial disclosure - Joint Investor Event from the Real Estate Investors Forum, PropertyMatch and AREF ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 Market Prospects and Sustainable Financial disclosure

Joint Investor Event from the Real Estate Investors Forum,

PropertyMatch and AREF

Thursday 7th January 2021

Moderator Welcome Melville Rodrigues Fund Services at Ocorian

Agenda for today

09.15 Webinar start

09.15 Welcome – Melville Rodrigues, Ocorian

09.20 Presentation from Ruth Hollies, CBRE Ltd

‘2021 market forecast, relevant to indirect real estate investors’

09.40 Presentation from Sasha Njagulj, CBRE Global Investors

‘How should investors address Sustainable Financial Disclosure

challenges?’

09.55 Final discussion and closing remarks from Melville Rodrigues

10.00 Close

Speakers

Sasha Njagulj, Ruth Hollies,

Global Head of ESG Head of European

CBRE Global Investors Forecasting

CBRE Ltd

Presentation

Ruth Hollies, Head of European Forecasting

CBRE LtdA TIME OF CHANGE ….AND MORE TO COME IN THE LONGER TERM

• Forecasts assumptions

• economy

• interest rates

• risk

• Sector outlooks – office, retail, residential &

industrial

• Comparison and conclusionUK GDP OUTLOOK USED IN NOVEMBER FORECASTS

Largest fall in activity in Q2

20 110

Bounce-back in Q3

15

105

Second lockdown Q4

10

100

5 Conditional on:

GDP level (2019q1=100)

95

per cent per quarter

0 • Lockdown 2.0 not being as

90 damaging to the economy

•

-5

Government support measures

85

being effective

-10

80 • Vaccine rollout

-15

Annual fall in GDP of 11.4% in 2020

75

-20 with a bounce to 5.6% in 2021

-25 70

Lockdown 3.0 will see 2021 output

2019Q4 2020Q1 2020Q2 2020Q3 2020Q4 2021Q1 2021Q2 2021Q3 2021Q4 2022Q1 2022Q2 2022Q3 revised down to circa 3%

Source: Oxford Economics, Macrobond, CBRELONG RATE (RISK FREE) AND ALL PROPERTY EQUIVALENT YIELD

14% long rate Equivalent yield

FORECAST

12%

10%

8%

6%

4%

2%

0%

Source: Oxford Economics, Macrobond, CBRECORPORATE BOND SPREAD (RISK PREMIUM) AND ALL PROPERTY EQUIVALENT YIELD

10% Equivalent yield Corporate Bond Spread (RHS) 6

FORECAST

9% 5

8% 4

7% 3

6% 2

5% 1

4% 0

Source: Oxford Economics, Macrobond, CBREALL OFFICE PERFORMANCE

25%

20%

15%

10%

5%

0%

-5%

-10%

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Capital Growth Rental Growth Total Return

Source: CBREEUROZONE & UK PRIME AVERAGE OFFICE YIELDS

%pa

7.5%

7.0%

6.5%

6.0%

5.5%

5.0%

4.5%

4.0%

European offices UK Offices ?

3.5%

3.0%

Source: CBREALL RETAIL PERFORMANCE

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Capital Growth Rental Growth Total Return

Source: MSCI, CBRERETAIL SEGMENT EQUIVALENT YIELD

10

9

8

7

6

5

4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Standard Shops Shopping Centres Retail Warehouse

Source: MSCI, CBRERETAIL SUB-SECTORS – CAPITAL VALUE CHANGE

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

-30%

-35%

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Standard Shops Shopping Centres All Retail Warehouses Supermarkets Department Stores

Source: MSCI, CBREALL RESIDENTIAL PERFORMANCE

14%

12%

10%

8%

6%

4%

2%

0%

-2%

-4%

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Capital Growth Rental Growth Total Return

Source: MSCI, CBREALL INDUSTRIAL PERFORMANCE

25%

20%

15%

10%

5%

0%

-5%

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Capital Growth Rental Growth Total Return

Source: MSCI, CBREFORECASTS & PRICING

Premium/discount to NAV vs 2021 capital growth forecast

10%

5%

%

NAV, %

vs NAV,

0%

price vs

growth, price

capital growth,

-5%

capital

-10%

-15%

-20%

-25%

Retail London Offices Industrials Generalist Long Income Other

1yr - CBRE 1yr - IPF High Average Low REIT pricing REIT pricing

Source: CBRE Research, November 2020; IPF Consensus Forecast, November 2020; PropertyMatch January 2021SUMMARY • ECONOMIC UNCERTAINTY Covid The evolving new EU relationship Scarring • REBOUND • STRUCTURAL RISKS nt up demand Working from home and Office usage Online shopping • REAL ESTATE OUTLOOK Income Hotels and leisure Residential Quality and function Adaptability Sustainability

DISCLAIMERS and WAIVERS This presentation has been prepared in good faith based on CBRE’s current views of the commercial real-estate market. Although CBRE believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE’s control. In addition, many of CBRE’s views are opinion and/or projections based on CBRE’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE’s current views to later be incorrect. CBRE has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change. Nothing in this presentation should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities – of CBRE or any other company – based on the views herein. CBRE disclaims all liability for securities purchased or sold based on information herein, and by viewing this presentation, you waive all claims against CBRE and the presenter as well as against CBRE’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein.

Slido.com - ref: #2572 Discussion

Presentation

Sasha Njagulj, Global Head of ESG

CBRE Global InvestorsDATA IS CRUCIAL FOR INVESTMENT DECISION-MAKING

WHAT INVESTORS AND WHAT IS AVAILABLE?

NEED? DOZENS OF REPORTING FRAMEWORKS AND

RATINGS

COMPARABLE

ACCURATE

CLEAR

CONSISTENT

COMPREHENSIVE

Sustainable Finance

DATA Disclosure Regulation

Non-Financial Reporting

Directive(NFRD)

(SFDR)

Taxonomy Regulation

CONFIDENTIAL AND PROPRIETARY | CBRE GLOBAL INVESTORS| 22EU TAXONOMY

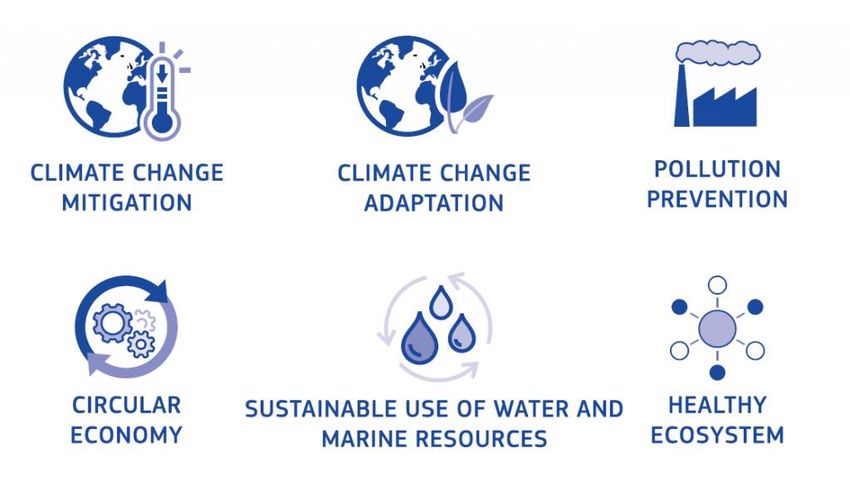

Six environmental objectives - Real Estate

CONTRIBUTE AND DO NO SIGNIFICANT HARM Sustainable urban

drainage systems

Smart buildings

Energy efficiency Air pollutant emissions

(EU EPC rating) Ozone depleting emissions

Carbon footprint/intensity Land and water pollution

Renewable energy

Waste management Biodiversity

Recycling rate Protected areas

Hazardous waste

Water

consumption

Water recycling

CONFIDENTIAL AND PROPRIETARY | CBRE GLOBAL INVESTORS| 23EU TAXONOMY

Governance safeguards – Real Estate

POLICIES PRINCIPAL ADVERSE IMPACT (do no harm)

Sustainability risks policy ESG violations/incidents

Remuneration policy Gender pay gap

Labour rights policy CEO pay ratio

Human rights policy Board diversity

Anti-corruption/bribery Exposure to suppliers/operations

policy Convictions and fines

D&I policy Accident/fatality rates

CONFIDENTIAL AND PROPRIETARY | CBRE GLOBAL INVESTORS| 24TIMELINE

1st reference period 2nd reference period 3rd reference period

Mar 2021 Jun 2021 Dec 2021 Dec 2022 Dec 2023

“Effective date” Latest date for Entity PAI Fund level PAI Reference

for PAI considering PAI disclosure disclosure periods

Funds publish Entity comparison

prospectus governance disclosure

disclosure

CONFIDENTIAL AND PROPRIETARY | CBRE GLOBAL INVESTORS| 25WHAT SHOULD YOUR MANAGERS BE DOING?

Review and align all policies

Review and align risk management/investment process

Identify products ‘captured’ by SFDR or Articles 8&9

Put in place robust data management system for entity and product data

Determine corporate data gaps & sources, and gather information

Determine investment data gaps & sources, and gather information (stakeholder engagement crucial)

Prepare website for disclosure AND compliance with other regulations (US Investment Advisers Act 1940, Rule 206(4)(1))

Keep monitoring technical developments for environmental screening criteria

Not wait for UK clarifications – prepare for the most stringent disclosure

CONFIDENTIAL AND PROPRIETARY | CBRE GLOBAL INVESTORS| 26Slido.com - ref: #2572 Discussion

Slido.com - ref: #2572 Thank you

Contact details Melville Rodrigues, Ocorian - Melville.Rodrigues@ocorian.com Ruth Hollies, CBRE Research - Ruth.Hollies@cbre.com Sasha Njagulj, CBRE Global Investors - sasha.njagulj@cbreglobalinvestors.com

You can also read