A unique precious metals company - European road show, April 2018 - Swiss Resource Capital

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A unique precious metals company European road show, April 2018

Disclaimer

NOT FOR RELEASE, PRESENTATION, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A

VIOLATION OF THE RELEVANT LAWS OR REGULATIONS OF SUCH JURISDICTION.

This presentation is for informational purposes only and does not constitute or form a part of any offer or solicitation to purchase or subscribe for securities in the

United States or any other jurisdiction nor a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in which such offer,

solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

The shares to be issued in connection with the offer for Lonmin plc (“Lonmin” and the “New Sibanye Shares”, respectively) have not been and will not be registered

under the US Securities Act of 1933 (the “Securities Act”) and, accordingly, may not be offered or sold or otherwise transferred in or into the United States except

pursuant to an exemption from the registration requirements of the Securities Act. The New Sibanye Shares are expected to be issued in reliance upon the

exemption from the registration requirements of the Securities Act provided by Section 3(a)(10) thereof.

This presentation is not a prospectus for purposes of Directive 2003/71/EC (and amendments thereto, including Directive 2010/73/EU, to the extent implemented in

any relevant Member State) (the “Prospectus Directive”). In any EEA Member State that has implemented the Prospectus Directive, this presentation is only

addressed to and is only directed at qualified investors in that Member State within the meaning of the Prospectus Directive. This presentation is not directed to, or

intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such

distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction.

No statement in this presentation should be construed as a profit forecast.

Forward looking statements

This presentation contains forward-looking statements within the meaning of the “safe harbour” provisions of the United States Private Securities Litigation Reform Act

of 1995. These forward-looking statements, including, among others, those relating to Sibanye Gold Limited trading as Sibanye-Stillwater (“Sibanye-Stillwater”)’s

financial positions, business strategies, plans and objectives of management for future operations, are necessarily estimates reflecting the best judgment of the

senior management and directors of Sibanye-Stillwater and Lonmin. All statements other than statements of historical facts included in this Presentation may be

forward-looking statements. Forward-looking statements also often use words such as “will”, “forecast”, “potential”, “estimate”, “expect” and words of similar

meaning. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances and should be

considered in light of various important factors, including those set forth in this disclaimer. Readers are cautioned not to place undue reliance on such statements.

The important factors that could cause Sibanye-Stillwater’s and Lonmin’s actual results, performance or achievements to differ materially from those in the forward-

looking statements include, among others, economic, business, political and social conditions in the United Kingdom, South Africa, Zimbabwe and elsewhere;

changes in assumptions underlying Sibanye-Stillwater’s and Lonmin’s estimation of their current mineral reserves and resources; the ability to achieve anticipated

efficiencies and other cost savings in connection with past, ongoing and future acquisitions, as well as at existing operations; the success of Sibanye-Stillwater’s and

Lonmin’s business strategy, exploration and development activities; the ability of Sibanye-Stillwater and Lonmin to comply with requirements that they operate in a

sustainable manner; changes in the market price of gold, PGMs and/or uranium; the occurrence of hazards associated with underground and surface gold, PGMs

and uranium mining; the occurrence of labour disruptions and industrial action; the availability, terms and deployment of capital or credit; changes in relevant

government regulations, particularly environmental, tax, health and safety regulations and new legislation affecting water, mining, mineral rights and business

ownership, including any interpretations thereof which may be subject to dispute; the outcome and consequence of any potential or pending litigation or

regulatory proceedings or other environmental, health and safety issues; power disruptions, constraints and cost increases; supply chain shortages and increases in

the price of production inputs; fluctuations in exchange rates, currency devaluations, inflation and other macro-economic monetary policies; the occurrence of

temporary stoppages of mines for safety incidents and unplanned maintenance; their ability to hire and retain senior management or sufficient technically skilled

employees, as well as their ability to achieve sufficient representation of historically disadvantaged South Africans’ in management positions; failure of information

technology and communications systems; the adequacy of insurance coverage; any social unrest, sickness or natural or man-made disaster at informal settlements

in the vicinity of some of Sibanye-Stillwater’s operations; and the impact of HIV, tuberculosis and other contagious diseases. These forward-looking statements speak

only as of the date of this Presentation. Sibanye-Stillwater and Lonmin expressly disclaim any obligation or undertaking to update or revise any forward-looking

statement (except to the extent legally required).

2

www.sibanyestillwater.com

Corporate overview

Shares in issue 2,178,647,129* Major shareholders*

Shares in ADR form 583,520,236*(ADR ratio 1:4 ordinary share)

Gold One Limited 19.43%

Market cap¹ c.R25 billion (US$2.1billion)

Listings JSE Limited share ticker: SGL Van Eck Associates Corporation 11.07%#

NYSE ADR programme share ticker: SBGL

Public Investment Corporation 9.61%

Net Debt R23 billion (US$1.88billion)3

at 31 December Net debt : adjusted EBITDA4 = 2.6x

Investec Asset Management 5.75%

2017 R4.1 billion (US$334 million) available

facilities

Black Rock Inc 4.34%

Reserves2 Gold Reserves of 25.7moz

at 31 December 4E SA PGM Reserves of 22.4moz

2017 2E US PGM Reserves of 21.9moz Shareholder geographic distribution*

Uranium Reserves of 96.1mlb China/ Gold One

Contact details James Wellsted

SVP: Investor Relations South Africa

29%

Tel: +27 (0)10 493 6923 /+27(0)83 453 4014 38%

ir@sibanyestillwater.com USA

Registered office: Constantia Office Park,

Bridgeview House, Building number 11, United Kingdom

Ground Floor, Corner 14th Avenue &

Potgieter Road, South Africa 19% 8% Europe excl UK

5%

*Shares in issue as at 14 March 2018, ADRs as at 23 February 2018

¹

Market cap as at 5 April 2018, sources: JSE, Factset Others

2 Refer to the Integrated Report or Mineral Resources and Reserves statement, issued on 29 March

1%

2018 at https://www.sibanyestillwater.com/investors/financial-reporting/annual-reports/2017

3 Converted using exchange rate on 31 December 2017 of US$/R12.36

4 Adjusted earnings before interest, taxes, depreciation and amortisation (EBITDA) based on the

formula included in the facility agreements for compliance with the debt covenant formula

*Shareholder information as at end February 2018

# As per Van Eck’s declaration on 23 March 2018

A leading global precious metal company 3

www.sibanyestillwater.com

Our vision and purpose dictates our actions

PURPOSE: Our mining improves lives

VISION:

SUPERIOR VALUE CREATION

FOR ALL OUR STAKEHOLDERS

Through mining our multi-commodity resources in

a safe and healthy environment

Underpinned by our C.A.R.E.S. VALUES

Commitment Accountability Respect Enabling Safety

Sibanye-Stillwater cares 4

www.sibanyestillwater.com

Location of SA region assets

ZIMBABWE

Mimosa

Rustenburg operations

Platinum Mile

Kroondal

JOHANNESBURG

South Rand project

(Burnstone)

West Wits operations

and projects:

• Driefontein

• Kloof

• Cooke surface

Key • WRTRP

Bushveld Complex SOUTH AFRICA Free State operations and projects

Great Dyke • Beatrix

• Beisa project

Witwatersrand Basin

• Bloemhoek project

Platinum operations • De Bron Merriespruit project

Gold operations • Hakkies project

• Robijn project

5

www.sibanyestillwater.com

Location of US region assets

Marathon project

(PGM-copper)

Stillwater mine

East Boulder mine

Columbus Metallurgical

complex

Altar project

(Copper-gold)

6

www.sibanyestillwater.com

Our three-year strategic goal

Maintaining

Deleveraging

our focus on

our balance

operational

sheet

excellence

Improving

Strengthen our position as a our position

Addressing

on the

leading international precious global

our SA

discount

industry cost

metals mining company by: curves

Pursuing value

accretive Consistently

growth based delivering on

on our market

strengthened commitments

equity rating

Well positioned to benefit from any upside in metal prices 7

www.sibanyestillwater.com

We have significantly transformed and grown

• Reduced costs

2013¹ Market • Improved flexibility and quality of

cap: R10 billion mining

Perceived high • Substantial increase in reserves

cost, short life SA enhanced by synergistic acquisitions

gold company • Significantly extended operating life

• Reduced debt/gearing

• Delivered consistent, industry leading

returns

• Significant PGM acquisitions at the bottom of

the PGM price cycle

Value accretive • Innovatively financed strategic growth enhancing

and high quality value

PGM acquisitions

• Implementation of operating model and realisation

of consolidation synergies yielding superior value

ahead of schedule

• Stillwater transaction transformative, creating a

globally competitive and unique SA mining

A major, global company

precious metal

• Unique commodity mix and global geographic

company presence

2018² Market • Proposed Lonmin Transaction concludes 4th step in

PGM strategy

cap: ~R25 billion • Will secure entire beneficiation chain in SA as well

as providing significant optionality to PGM prices

¹

11

February

2013,

Source:

IRESS

• Well positioned for further success

² 5

April

2018,

source:

JSE

Delivering growth and value while diversifying risk at the bottom of the cycle 8

www.sibanyestillwater.com

Becoming a leading precious metals company

Sibanye-Stillwater global PGM ranking Sibanye-Stillwater global gold ranking

2017A platinum 2017A palladium 2017A gold and gold

production (moz) production (moz) equivalents

production (moz)

1 Barrick 5,3

Amplats 2,4 Norilsk 2,8

Newmont 5,3

2

Sibanye-Stillwater

2.2 Amplats 1,6 AngloGold 3,8

(post-transaction)

2, 3, 4

Sibanye-Stillwater

2 3.7

Sibanye-Stillwater (post-transaction)

Impala 1,5 1.2

(post-transaction)

Kinross 2,7

Lonmin 0,7 Impala 0,9 Gold Corp 2,6

Newcrest 2,4

1

Norilsk 0,7 Lonmin 0,3

Gold Fields 2,2

Northam 0,3 Northam 0,1 Polyus 2,2

Agnico-Eagle 1,7

RBPlats 0,2 RBPlats 0,1

Sibanye-Stillwater 1,4

Lonmin’s contribution to Sibanye-Stillwater

Source: Company filings

Note:

1. Includes PGM by-products only

2. Rustenburg + Aquarius + Stillwater + Lonmin. Blitz at full ramp up.

3. Sibanye –Stillwater gold equivalents included

4. Gold equivalent ounces calculated as PGM basket price in the period / average gold price in the period multiplied by PGM production

Positioned globally as a leading precious metals producer 9

www.sibanyestillwater.com

We have a proven operating model

2017 SA gold industry UG operating unit costs (SA only)

3 500 3 344

3 300

3 100

2 900

2 700

R/tonne

2 466

2 500

2 224

2 300 2 111

2 100

1 900

1 700

1 500

Anglogold Gold Fields (South Harmony Sibanye-Stillwater

Deep)

2017 SA gold industry all-in sustaining costs (SA only)

1400

1.340

1350

1300

1.242

1250

US$/oz

1.195

1200

1150 1.128

1100

1050

1000

Gold Fields (South Anglogold Harmony Sibanye-Stillwater

Deep)

Source: Company reports for 12 months ended 31 December 2017

Sibanye-Stillwater is the lowest cost major gold producer in South Africa 10

www.sibanyestillwater.comPrecious metals strategy

• PGM industry in SA shares many operational similarities with gold mining

• Opportunity to leverage Sibanye’s successful operating model and hard rock,

tabular, labour intensive mining competency to realise further value

• Long-term PGM supply and demand fundamentals remain robust

• Low PGM prices and escalating costs (labour, utilities) had put balance sheets

under strain

• The SA PGM sector offered a number of consolidation opportunities

• Innovative approach to structuring transactions and projects

Platinum a logical first step 11

www.sibanyestillwater.comPalladium market outlook

2.500 1.100

• We are structurally bullish with palladium 2.000 1.000

1.500 900

set for sustained record deficits 1.000

800

500

700

– Palladium excess inventories already 0

600

-500

500

closing in on normalised levels -1.000

-1.500 400

300

– Gasoline expected to maintain a >70% -2.000

-2.500 200

2007A 2012A 2017E 2022E

market share through to 2025, supporting

Surplus / Deficit (koz) Ex-ETF market balance

demand Pall Price (US $ / oz) (rhs)

– Long term producer supply CAGR of

1.000

-1.2% significantly lags a net-demand 800

CAGR of 2.0% 600

400

– Over the long term substitution is 200

anticipated to provide more balance to 0

-200

the overall PGM basket

-400

-600

1992A 1995A 1998A 2001A 2004A 2007A 2010A 2013A 2016A 2019E 2022E 2025E

Platinum Palladium Rhodium

Source: Internal demand and supply model based on WPIC information, broker consensus and other sources

Palladium outperformance set to continue 12

www.sibanyestillwater.comPlatinum: Short term headwinds

• Despite ongoing diesel and EV concerns, 1.000 1.800

800

we believe platinum’s fundamentals 600

1.700

remain robust 400

1.600

200 1.500

– Limited primary and secondary supply 0 1.400

growth anticipated globally -200 1.300

– Demand remains well supported, even in -400

1.200

diesel markets -600

1.100

-800

• Decline in diesel penetration rates and -1.000 1.000

2007A 2012A 2017E 2022E

growth in EVs and hybrids already

factored in Surplus / (Deficit) Ex-ETF market balance Pt Price (US $ / oz) (rhs)

– Diesel’s global market share to decline to

14% by 2025, from 19% 140 25%

Millionen

! Light passenger diesel units expected 120

to remain relatively constant at c.18m 20%

100

units per annum 15%

80

– EV’s and hybrids to grow at a CAGR* of

60

25% through to 2020 (c.11m units) 10%

40

• Platinum likely to be mostly balanced for 5%

20

the remainder of this decade, thereafter

0 0%

reverting to material deficits as primary 2010A 2013A 2016A 2019E 2022E 2025E

production from SA contracts Diesel Gasoline

Hybrid (Mild and Full) PEV+PHEV

Diesel market share (%, rhs)

Source: Internal demand and supply model based on WPIC information, broker consensus and other sources

Despite declining diesel market share and EV concerns, we remain fundamentally bullish 13

www.sibanyestillwater.comImplementing a value accretive PGM strategy

• First entry into the SA PGM sector – April 2016

• Lean, well run company

Aquarius • Operational performance has increased further to record levels

since acquisition

• Effective from November 2016

• Smart transaction structure aligned with expectations of platinum

market outlook

Rustenburg • Significant synergies with Aquarius and the gold central services

• Realised synergies of ~R1bn pa in 14 months, well ahead of

previous target of R800m over a 3-4 year period

• Tier one US PGM producer acquired in May 2017

• High grade, low cost assets with Blitz, a world class growth project

Stillwater • Provides geographic, commodity and currency diversification

• 78% palladium content provides upside to robust

palladium market

• Attractive acquisition price at low point in platinum price cycle

• Combination with Sibanye-Stillwater SA PGM assets results in

significant potential synergies

Lonmin • Aligns with Sibanye-Stillwater’s mine-to-market strategy in SA and

adds commercially attractive smelting and refining

• Sizeable resources provide long-term optionality

A unique, leading precious metals mining company offering scale and sustainability 14

www.sibanyestillwater.com2017 – a transformative year strategically

• Concluded acquisition of Stillwater in May 2017

• Successfully refinanced US$2.65 billion bridge loan

– Oversubscribed US$1 billion rights issue

– Competitively priced US$1.05 billion Eurobond (two tranches)

– US$450 million flexible, low cost convertible instrument

• Proposed sale of certain WRTRP assets to DRDGold

– Realises immediate value and ensures continued exposure to the WRTRP

• Proposed acquisition of Lonmin

– Downstream processing business with a replacement value significantly higher than

acquisition cost

– Significant synergies between Sibanye-Stillwater and Lonmin’s contiguous PGM

assets

– Sizeable PGM Resources with potential upside from advanced brownfield projects

and greenfield project pipeline

Significant, value accretive transactions at an attractive point in the commodity price cycle 15

www.sibanyestillwater.comClear benefits from recent diversification

1200

US$/2Eoz PGM basket YTD ave = 23% higher than H1 2017

24.000

R/4Eoz PGM basket YTD ave = 6% higher than H1 2017

1100

22.000

Ave H2 2017: US

$946/2Eoz 1000

20.000

Ave 2018 YTD: US

$1,019/2Eoz

Ave H1 2017: US 900

18.000 $830/2Eoz

Ave 2018 YTD:

R/oz

US$/oz

R15,001/oz

Ave H2 2017: 800

16.000 R17,087/oz

Ave H1 2017:

R16,331/oz 700

14.000

Ave H2 2017: 600

12.000 Ave 2018 YTD:

R13,074/4Eoz

Ave H1 2017: R12,799/4Eoz

R12,063/4Eoz

10.000 500

Gold R/oz (LHS) PGM Basket R/4Eoz (LHS) PGM Basket US$/2Eoz (RHS)

Source: Inet BFA

*2E and 4E basket prices are based on Sibanye-Stillwater SA PGM and US PGM prill split

Dollar metal prices gains partially offset by rand strength – Stillwater basket price benefiting 16

www.sibanyestillwater.comLarge, low cost South African PGM acquisitions Source: Various companies’ disclosures Note: Bubble size represents PGM Resources A sizeable resource base at a compelling price 17 www.sibanyestillwater.com

2017 – a transformative year operationally

Adjusted

Ebitda*

contribu3on

(H2

2017)

• Integration of Rustenburg exceeding expectations

– Over R1 billion annual synergies realised over 14 months

US

PGM,

30%

– Operational results continue to improve – profitability

SA

Gold,

51%

restored

SA

PGM,

19%

– Sustainable move into lower half of industry cost curve

• Smooth integration of Stillwater

SA

Gold

SA

PGM

US

PGM

– Solid operational performance sustained

Produc3on

contribu3on

(H2

2017)

– Blitz project commissioned 3 months ahead of schedule

– Record recycling rates achieved US

PGM,

18%

• Gold operations restructured for sustainability SA

Gold,

44%

– Cooke closed, Beatrix West on watch list SA

PGM,

38%

– Expected R15,000/kg (U$S36/oz) (in 2017 terms) reduction in

total SA gold operation’s AISC in 2018

SA

Gold

SA

PGM

US

PGM

*Adjusted earnings before interest, taxes, depreciation and amortisation (EBITDA) is based on the formula included in the facility agreements for compliance with the debt covenant

formula. Full detail is contained in Sibanye-Stillwater’s 2016 Annual Financial Report

Transformational acquisitions balancing and de-risking the business 18

www.sibanyestillwater.comAquarius and Rustenburg realised synergies

Realised

Realised benefits

Initial benefits benefits since

Category Summary of key initiatives

identified (Rm) At 30 June acquisition at

2017 (Rm) 31 Dec 2017

(Rm)

• Employees and management configured to

reflect the Sibanye-Stillwater operating model 200

Resource

optimisation 246 456

• Consolidation of duplicated production and

support functions 237

• Improved procurement and supply chain

management 137

Sourcing and stores

management 26 166

• Owner Maintenance 98

Closure of • Rosebank, Centurion and Perth offices

corporate offices 69 62 62

• Property

Optimisation

• Consolidation of training footprint

268 68 164

• Engineering

• Other

Total Operating cost synergies R800m (over 3 R542m R918m

years) (over 8 (over 14

months) months)

Additional savings • Real capital savings realised (not deferred) 98 116

Realised integration synergies R800m (over 3 ~ R640m ~ R1,034m

years) (over 8 (over 14

months) months)

*Source: Company data

Kroondal baseline was 2016 actual (July 2015 to June 2016),Rustenburg: Baseline was the PFS – re-based as a standalone company

Savings identified include those related to decrease in labour numbers

Integration of Aquarius and the Rustenburg operations has exceeded expectations 19

www.sibanyestillwater.comMoving down the PGM AIC curves ‘16 – ‘17

20.000 Jun-16 all-in costs1 chart, by mine (R/6E ounce)2

18.000

Avg. basket price R12,699/ounce (6E)

16.000 Avg. all-in costs = R12,277/ounce (6E)

14.000

Cost R/Oz

12.000

10.000

8.000

6.000

4.000

2.000

0

Booysendal

Mototolo

East Boulder

Stillwater

Two rivers

Zimplats

Kroondal

Union

Marula

Modikwa

Amandelbult

Mogalakwena

Lonmin

Mimosa

Rustenburg

Impala

Boschkoppie

Unki

Zondereinde

20.000

Jun-17 all-in costs1 chart, by mine (R/6E ounce)2

Avg. basket price R12,128/ounce (6E)

18.000 Avg. all-in costs = R12,589/ounce (6E)

16.000

Cost R/Oz

14.000

12.000

10.000

8.000

6.000

4.000

2.000

0

East Boulder

Booysendal

Stillwater

Two rivers

Mototolo

Kroondal

Zimplats

Rustenburg

Mogalakwena

Modikwa

Mimosa

Union

Lonmin

Amandelbult

Unki

Impala

Boschkoppie

Zondereinde

Marula

Sibanye-Stillwater mines3 Other PGM mines

Source: Citi Research, Company reports,

Note:

1. Includes cash costs, all capex exploration, corporate costs, cash taxes and other operating costs

2. Excluding base metal credits

3. Mines acquired by Sibanye-Stillwater in the Aquarius acquisition include Kroondal and Mimosa

Clear cost benefits realised at Kroondal and Rustenburg operations from integration with Sibanye-Stillwater 20

www.sibanyestillwater.comStillwater acquisition

• High grade, low-cost PGM producer

• Favourable geographic location

• Steady state operations (~550,000 2Eoz)

with more than 20 year mine life Headquarters

(Littleton, CO)

• Near term growth from Blitz project

– first production in Q4 2017

Marathon

Stillwater Mine

– full run rate of ~300,000 2Eoz by (Montana)

(Ontario, Canada)

late 2021/early 2022

East Boulder Mine Blitz Development

(Montana)

• Established large, low risk, recycling (Montana)

business Smelter & Base

Metals Refinery

• Acquired at a favourable time of the (Montana)

palladium price cycle Stillwater Recycling Altar

(Montana) (San Juan Province,

• Further growth potential in lower East Argentina)

Boulder and lower Blitz

World-class assets, stable jurisdiction, high-grade PGM operations 21

www.sibanyestillwater.comStillwater – a well-timed acquisition

100

76%

80 42%

Relative price performance (%)

Stillwater Transaction

concluded

60

Stillwater Transaction

announced

34%

40

Discussions with

Stillwater begin

20

0

-20

Gold (LHS) Palladium (RHS) Platinum (LHS)

Source: Inet BFA

Fundamental outlook for palladium remains robust 22

www.sibanyestillwater.comStillwater CPR – confirms value

• CPR released in November 2017

– NPV of US$2.7 billion vs acquisition price of US$2.2 billion confirmed, at assumed

palladium price of US$704/oz and platinum price of US$1,047/oz

– AISC and AIC converge to approximately US$530/2Eoz from 2021 as capital at

Blitz declines and production builds up

US

PGM

OperaMons

producMon

and

cost

profile

1.100

900.000

Ave

spot

2E

basket

price

YTD

~

US$1,019/2Eoz

1.000

800.000

19%

900

700.000

34%

800

50%

US$/2Eoz

600.000

2Eoz

700

500.000

600

400.000

500

400

300.000

300

200.000

2018

2019

2020

2021

2022

2023

2024

2025

2026

2E

producMon

(oz)

AISC

AIC

Spot

prices

for

2E

basket

Source: Stillwater CPR 2017

Note: Production and costs are in line with the published CPR for the Stillwater operations (available on https://www.sibanyestillwater.com/investors/documents-circulars)

The Stillwater operations have a PGM 2E prill split of 3.4 palladium: 1 platinum ounce

A value accretive and well timed acquisition 23

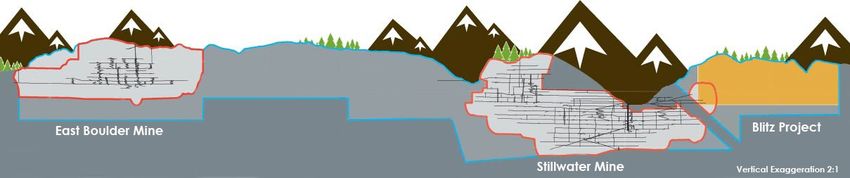

www.sibanyestillwater.comStillwater offers significant growth potential

• 2E PGM Mineral Reserves of 21.9Moz and Mineral Resources of 80.5Moz1

• Lower East Boulder and lower Blitz projects offer additional production growth

potential

• 12.2 kilometres of undeveloped mineralised section between Stillwater and

East Boulder mines

191

Sweet Grass Yellowstone 87

72

89

Big Timber

Yello

Metallurgical Billings

wsto

90 298

ne R

iver Complex,

Recycling Facilities

Columbus Laurel

Livingston McLeod

East

E. Bou

iver

a ter R

89 Stillw

Boulder

Absarokee

lder R

420

NYE

310

Fishtail 212

Mine

iver

419 Big Horn

Carbon

Park

Stillwater

Stillwater Mine 78

Bear Tooth Mo

untain Range Mine Red Lodge

12.2km

Source: Stillwater Mining

1. At 31 December 2017

Quality reserves with further upside 24

www.sibanyestillwater.comThe proposed Lonmin acquisition

• Sibanye-Stillwater has made an all

equity offer to acquire 100% of Lonmin 1. Northam

2. Anglo America

• Value accretive to Sibanye-Stillwater Platinum

2 1

shareholders 3. Siyanda Resources

4. Sedibelo Platinum

• Neutral to Sibanye-Stillwater debt 3 5. Wesizwe Platinum

6. Royal Bafokeng

profile – will not add debt to the Platinum

balance sheet 4 7. Impala Platinum

2 8. Eastern Platinum

• R1.5 billion in annualised pre-tax cost 9. Glencore Xstrata

and operational synergies* expected Sibanye-Stillwater

6

by 2021 Lonmin

5

• Should Sibanye-Stillwater shareholders 6

6

not approve the transaction, Western Bushveld

Joint Venture 7

agreement in principle to discuss asset 9 Sable project

acquisition 7

8 1

Pandora Joint

Venture

*For further information in relation to the expected synergies, please refer to page 17 and pages 58 to 60 of the offer announcement dated 14 December 2017, available on https://

www.sibanyestillwater.com/investors/transactions/lonmin/documents.

A logical value accretive transaction 25

www.sibanyestillwater.comLonmin production and capex profile

• Significant capital investment required to maintain flat production profile

– Substantial capital hump

• Placing of generation one shafts on care and maintenance, which are coming

to the end of their lives, results in an expected retrenchment of approximately

12 6001 employees over the next 3 years

Lonmin LoM - 4E PGM ounces in concentrate Lonmin LoM - Total capital by category (real terms)

1.200.000 4.000

1.000.000 3.500

3.000

4E PGM ounces

800.000

R

million

2.500

600.000 2.000

400.000 1.500

1.000

200.000

500

0 0

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

K3 Saffy Rowland E3 Total Mining Capex Total Conc. Capex

4B K4 W1 E1

E2 Hossy Newman BTT Total S&R Capex Total Other Capex

Source: Lonmin’s company information

Note:

1. Numbers include contractors

Challenging financial requirements under current economic conditions 26

www.sibanyestillwater.comRevised Lonmin operational plan1

• Lonmin mining plan revised after detailed due diligence

• Planned for current economic and market conditions

– “Lower for longer” plan

• Conservative plan not contingent on expenditure of project capital thereby

ensuring affordability

• Generation one shafts to be put on care and maintenance as per Lonmin plan

• Flexibility to delay project capital investment

– Optionality to significantly extend operating life in a higher PGM price environment

Revised plan - adjusted 4E PGM ounces Revised capital by category compared to Lonmin

in concentrate plan (Real terms)

1.200.000 4.000

3.500

1.000.000

4E PGM ounces

3.000

800.000

R million

2.500

600.000 2.000

1.500

400.000

1.000

200.000

500

0 0

2018 2021 2024 2027 2030 2033 2036 2018 2021 2024 2027 2030 2033 2036

K3 Saffy Rowland E3 4B K4 Mining capex Concentrator capex Smelter and refinery capex

W1 E1 E2 Hossy Newman BTT Other capex New furnace capex Total LoM Capex

Lonmin LoM 4E PGM ounces in concentrate

1 Source: Lonmin’s company information and due diligence performed by Sibanye-Stillwater

Affordable mining plan with optionality 27

www.sibanyestillwater.comProcessing considerations

4E

PGM

oz

by

Source

• Ability to treat Rustenburg

2000

000

concentrate in Lonmin

4E

oz

in

conc

/

4E

oz

produced

processing facilities from 2021

1500

000

• Benefit of treating own

1000

000

concentrate through owned

facilities

500

000

• Optimising capacity positively

-‐

impacts processing unit costs

2018

2019

2021

2023

2025

2026

2027

2028

2029

2031

2033

2035

2036

2037

2020

2022

2024

2030

2032

2034

Lonmin

4E

contained

in

conc

Sibanye-‐SMllwater

4E

Produced

• Allows for better mine planning

flexibility enhancing profitable Concentrate

by

Source

mining mix

600

000

500

000

Tonnes

of

Concentrate

• Potential to build DC ARC

furnace (approximate capital

400

000

300

000

cost of R1bn) to cater for total

Rustenburg concentrate

200

000

100

000

– Other potential solutions also

being investigated

-‐

-‐100

000

2018

2019

2021

2023

2025

2026

2027

2028

2029

2031

2033

2035

2036

2037

2020

2022

2024

2030

2032

2034

Sibanye-‐SMllwater

Concentrate

tonnes

Lonmin

Concentrate

produced

tonnes

1 For

further information in relation to the expected synergies, please refer to page 17, 58 to 60 of the offer announcement dated 14 December 2017 available on https://

www.sibanyestillwater.com/investors/transactions/lonmin

Average processing synergies from 2021 to 2032 of approximately R550m per annum1 28

www.sibanyestillwater.comMaterial synergies with Lonmin operations

Pre-tax synergies of approx. R1.5bn per annum by 20211

Quantified synergies 2 Incremental synergy potential 2

• Overhead costs (R730m per annum by • Ability to mine through existing mine

2021) boundaries

– Corporate office rationalisation (closing • Optimal use of surface infrastructure

the London office and delisting)

• Optimising the mining mix

– Regional shared services

• Prioritisation of projects and new

– Operational (mining) services growth capital

– One-off R80m cost required to achieve • Capital reorganisation in line with new

these synergies

consolidated regional plan

• Processing synergies

– Differential cost benefits of R780m by

2021 and an average of approximately

R550 per annum from 2021

– Approximately R1bn of capex required

for the purchase of a new furnace

Note:

1. For further information in relation to expected synergies, please refer to page 17 and pages 58 to 60 of the offer announcement,

dated 14 December 2017, available at https//sibanyestillwarer.com/investors/transactions/lonmin/documents

2. For overhead synergies, total savings anticipated when fully implemented in FY21; varies per toll agreement production throughput

for processing synergies with average calculated between 2021 and 2032

3. Synergies which are unquantifiable at this point in time

Realisation of synergies will ensure operational viability 29

www.sibanyestillwater.comProduction profile for the next 20 years

Expected gold and PGM life of mine production (Next 20 Years)

Gold Operations, Gold oz

5.000.000

SA PGM operations, 4E PMG oz

4.500.000 US PGM operations (US), 2E PGM oz

Recycling (US), 2E PGM oz

4.000.000

Lonmin Operations, 4E PGM oz

3.500.000

Gold Fields Plan, Gold oz

3.000.000

Ounces

2.500.000

2.000.000

1.500.000

1.000.000

500.000

0

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

Source: Company information

Note: Profile is based on reserves declared as at 31 December 2017 and excludes the Burnstone project and the West Rand Tailings Retreatment Project

Ample mine life to sustain the Group in the long-term 30

www.sibanyestillwater.comLiquidity position robust – US$ RCF refinanced

• US$350 million RCF maturing in August 2018 refinanced and increased to US

$600 million on improved terms

• Strong support from group of various international banks – continued

confidence in Sibanye-Stillwater’s business plan

• Facility is not currently materially utilised but extended facility maturity, and

increased size, improves Group’s liquidity position

• Net Debt:EBITDA covenant remains as a maximum of 3.50x up to and including

31 December 2018, and a maximum of 2.50x thereafter

Debt

Maturity

ladder*

-‐

R

millions

R10

000

R5

000

R5

537

R5

945

R6

651

R5

451

R

0

(R1

545)

R1

137

2018

2019

2020

2021

2022

2023

2024

2025

(R4

124)

(R5

000)

(R3

090)

(R10

000)

Cash

(incl

GBF's)

Available

FaciliMes

ZAR

RCF

(R6bn)

New

USD

RCF

($600m)

2022

Bonds

($500m)

2023

ConverMble

($450m)

2025

Bonds

($550m)

*Balances as at 31 December 2017 adjusted for the New USD RCF

31

www.sibanyestillwater.comOUTLOOK

322018 Guidance

Production All-in sustaining costs Total capital

38,500 - 40,000 kg R475,000 - 495,000/kg R3,500 million

SA Gold operations¹

(1.24 - 1.29 Moz) (US$ 1,130 - 1,180/oz) (US$268 million)

R10,750 - 11,250/4Eoz (US R1,500 million

SA PGM operations¹ 1,100 - 1,150 koz (4E PGMs) $825 - 860/4Eoz) (US$115 million)

580 – 610 koz (2E PGMs

US PGM operations US$650 - 690/oz ~US$220 million

mine production)

Source: Company forecasts

¹ Estimates are converted at an exchange rate of R13.05/US$

Positive operational outlook 33

www.sibanyestillwater.comSouth African “green shoots” • The political environment in South Africa has recently undergone significant change and we anticipate this will be complemented by tangible actions • While the strong rand creates short term headwinds we have confidence in the longer term benefits • Starting to see an improvement in relations in contrast to the fractious environment of recent years • A policy and regulatory environment conducive to business competitiveness will promote investment and growth in the South African mining industry which remains a critical part of the national economy and a significant employer • Recent judicial ruling on “once empowered always empowered” another positive outcome for the industry • Sibanye-Stillwater is committed to support inclusive growth in South Africa through mining • Our recent South African investments provide significant exposure to South Africa and our company and its stakeholders stand to benefit significantly from this improving environment A vastly more favourable outlook for investment 34 www.sibanyestillwater.com

A unique value proposition

Largest Top 3 Stillwater – Leading

GLOBAL only sizeable

A leading precious producer primary GLOBAL

PRODUCER of

metal company of South platinum and producer of PGM

African gold palladium Palladium recycler

Copper

Delivery of superior Operational Gold mine life Proudly South The PURPOSE

value to all excellence >15 years African while of our mining

and innovative

stakeholders drives PGM mine life competing on is to IMPROVE

growth to create

strategy sustainability > 30 years a global stage LIVES

Source: Company information 35

www.sibanyestillwater.comContacts

James Wellsted/ Henrika Ninham

ir@sibanyestillwater.com

Tel:+27(0)83 453 4014/ +27(0)72 448 5910

Website: sibanyestillwater.com

36You can also read