AGRITECH IN BRAZIL Opportunities for Swiss SME's in the country's driving sector - January 2021 - Switzerland ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

AGRITECH IN BRAZIL

Opportunities for Swiss SME’s in the country’s driving sector

January 2021

Official Program In Cooperation With

Contents

INTRODUCTION ........................................................................................................... 6

BRAZIL & AGRICULTURE .................................................................................... 7

Brazil - where Farming is Big Business _____________________________________ 7

The Success Story of Tropical Agriculture ___________________________________ 8

Agriculture, Environmental Sustainability and the Amazon _______________________ 9

OVERVIEW OF THE BRAZILIAN AGRIBUSINESS............................................... 11

Key Numbers of the Brazilian Agribusiness __________________________________ 11

Global Leader for the Production of Main Commodities ________________________ 14

Cotton 14

Coffee 15

Soybean 15

Sugar 16

Orange Juice 16

Beef 17

Poultry 17

Livestock ________________________________________________________ 18

SWOT Analysis of Agritech in Brazil 2020 – 2024 ____________________________ 21

Challenges for the future _____________________________________________ 21

DIGITAL AGRICULTURE IN BRAZIL .................................................................. 23

Open Eco-Systems & R&D for Tropical Agriculture ____________________________ 23

Brazilian Agri-Tech Market____________________________________________ 26

TECHNOLOGY OPPORTUNITIES FOR SWISS INDUSTRY IN DIGITAL

AGRICULTURE ................................................................................................... 28

Meteorology & Risk Management _______________________________________ 28

Weather Stations 28

Weather Forecasts 28

Microclimate monitoring 29

Climate Risk Modelling 29

IoT, Sensor Technology & Platforms ______________________________________ 29

Livestock Automated Weight Monitoring 31

Behaviour and Feeding Monitoring 31

Crop Imaging Technology (Satellite, Aerial and Field) __________________________ 32

Satellite NDVI imaging 32

Aerial imaging 32

Deep Neural Networks for Image Recognitions 32

Multispectral or Hyperspectral Cameras 33

Pests & Diseases in Crops _____________________________________________ 33

Weather Related Disease Modelling 33

Biological Control Systems 34

Automatic Insect Traps 34

Irrigation, Soil & Plant Nutrition ________________________________________ 34

Irrigation Automation and Monitoring 34

Topsoil Mapping 36

In-Field Nutrient Analytics 36

Biological and Organic Soil and Plant Nutrition Products 36

Precision Farming __________________________________________________ 37

Geospatial Analysis Techniques 37

Prescription mapping 37

Management Zone planning 37

Smart Application or sensor-based VAR 38

Robotics and Drones ________________________________________________ 38

Mechanical Weed Control Robots 38

Milking Robots 38

Drones 39

Animal Genetics Market ______________________________________________ 40

Tracking & Supply Chains_____________________________________________ 41

Block Chain Driven Food Supply Chain Applications 41

Food Authentication Technologies 41

Animal Nutrition________________________________________________ 42

Bioactive ingredients 43

Alternative proteins 43

Insect Protein 43

Algal Protein 43

Niche Market Opportunities ___________________________________________ 44

Grape Market 44

Specialty Fruits 44

Agroforestry/ICLF (Integrated Crop-Livestock-Forest) 44

Bio Energy Market 45

Carbon Farming 46

Small Farmers/Risks Management 46

Tropical Agriculture 46

Farm-To-Consumer E-Grocery 46

Food Waste Reduction Systems 47

CONCLUSION ..................................................................................................... 48

RESEARCH METHODOLOGY AND SOURCES .................................................... 50

LITERATURE & INFORMATION SOURCES ________________________________ 50

DATA ANALYSIS AMAZON FIRES ______________________________________ 53

DIVERSE APPENDIX MATERIAL ....................................................................... 54

Real Case: Medium-Sized Soya Producer and IoT _____________________________ 54

Digitization in pig farming – Agriness Case _________________________________ 54

ABOUT S-GE ............................................................................................................... 56

CONTACT US .............................................................................................................. 56

Disclaimer The information in this report was gathered and researched from sources believed to be reliable and are written in good faith. Switzerland Global Enterprise and its network partners cannot be held liable for data, which might not be complete, accurate or up-to-date; nor for data which is from internet pages/sources on which Switzerland Global Enterprise or its network partners do not have any influence. The information in this report do not have a legal or juridical character, unless specifically noted.

Introduction In the following report, the reader will have an insight into this very important sector for the Brazilian economy. Agribusiness is and will remain for the upcoming decades the main driver of the economy of the country. The Swiss Business Hub Brazil, as responsible to foster the exports of Swiss companies to Brazil and aware of the level of innovation that Switzerland can offer to a sector that is increasing its digitalization at a fast pace and demanding niche technologies with the highest level of reliability, envisioned the strong positive impact a comprehensive report on the sector could have for both countries. It aims to provide a substantial overview of the subsectors, the most important trends and technological advancements highlight the level of sustainability that Brazil has already achieved and still pursuits in Agribusiness, outlining challenges and particularities and highlighting the most relevant opportunities for Swiss players in Agritech. To compile this report, the Swiss Business Hub Brazil engaged two experts from the sector and analysed an extensive collection of reports, interviews, market studies and articles issued by business associations, specialiazed research institutes, national and international market intelligence companies, as well as international trade organizations. The first chapter introduces and contextualizes the sector and its particularities. The chapter two aims to further provide figures of the most important subsectors, placing the relevance of the country and its globally forecasted growth and macro challenges identified. Chapter three is dedicated to the R&D ecosystem, whereas chapter four goes deeper in to every segment to outline the opportunities for Swiss players. The last subchapter of chapter four lists niche market opportunities and trends, also arising from Covid-19, not necessarily cross-referenced with Swiss technologies. The final goal of this report is to facilitate the connection between Swiss technical suppliers and the players in Brazil, enhancing the business between the two countries for mutual benefit and growth. AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 6 OF 58

BRAZIL & AGRICULTURE

Brazil - where Farming is Big Business

The Brazilian agribusiness does not have much in common with Swiss agriculture. In the world’s largest

tropical country, farming is big business. It is the business of feeding the world. Together with the other

agricultural superpowers - USA, China and India - Brazil is leading the production of most food

commodities, such as soya, corn, sugar, coffee, and orange. All these agricultural superpowers unite three

common factors, which make them naturally leading food producers: first, they all have large populations

to feed, which historically gives agriculture a priority in the country’s political agenda. Second, they

belong to the countries with the largest territorial extension on the planet. Third, in large parts of their

geography they enjoy a mild and wet climate, which makes their lands productive (i.e. this being the

reason why the largest and second largest countries, Russia and Canada, are not among the top food

producers).

Zooming into Brazil, it is possible to learn that in the period since 1990, the country has increased its

productivity in cereal’s yield per hectare from 1.76 tons to 4.81 tons per hectare. This increase of

productivity is unmatched among all major countries during the same period. However, this level is still

much lower than other major food producers (compare: USA = 8.69 t/HA, China = 6.08 t/HA,

Switzerland = 6.2 t/HA, Netherlands = 8.32 t/HA). This has enabled the increase of total grain production

by 217%, while the planted area has grown a mere 16% in the same period.

Against popular believe, the primary focus of modern Brazilian agriculture is not the territorial expansion,

but the productivity increase. However, despite this recent success, the importance of Brazilian

Agriculture lies much more in its future potential than in its past performance. Agronomists often use the

concept of Yield Gap to conceptualize how much a country could potentially produce and what are the

limiting factors. Thereby, the climate, the water and the crop genetics define the so-called potential yield

(Yp), i.e. the maximum potential yield per each planted hectare. Different studies show that Brazil has

still a Yield Gap of about 6.6 tons per hectare. In other words, the country can easily double its output

without extending its territory but mostly by adopting new technologies and efficient practices.

Apart from closing that yield gap, Brazil’s favourable tropical climate allows for two to three harvests per

year. In some regions, irrigation systems are needed to produce in the dry season, which is the ‘tropical

winter’, in other regions year-round farming is even possible without irrigation. This means that Brazil

has the potential to produce 3-5 times more than today without cutting a single tree from the Amazon

forest.

One could question why Brazilian farmers are so successful in increasing their productivity, while the rest

of the country’s industry remains largely uncompetitive. The answer is in the absence of government

subsidies and market protection, obliging the Brazilian farmers to adopt an entrepreneurial approach and

to sell their products at the world market price. Brazilian public spending for agriculture has gone mainly

into R&D, namely to EMBRAPA, the Brazilian Agricultural Research Corporation affiliated with the

Ministry of Agriculture. EMBRAPA has developed numerous agronomic innovations paving the path of

success of Brazilian farming.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 7 OF 58

At this point, two important conclusions can be made: first, Brazilian Agriculture has the potential to

increase its food production by factor three or more without accessing a single additional square-meter

of land and it is a matter of technology adoption. Second, local farmers are entrepreneurs and

businesspeople, who consistently seek innovations and productivity increase, while using the natural

advantage of their production site.

The Success Story of Tropical Agriculture

In spite of the favourable climate, farming under tropical climates is not an easy game. There are several

challenges.

Initially, while European soils freeze once per year and thereby interrupt the entire biological cycle, the

same does not happen in the tropics. This also means that pests and diseases can continuously develop.

Freshly seeded and vulnerable plants then encounter an entirely adult and aggressive population of pests

and pathogens. The humid and hot climate is generally favourable to these plagues. For the farmers, this

means a higher demand for chemical pesticides, which represents a cost to both environment and

financial budget. Biological and organic farming practices are generally very difficult under such

conditions. This is the main reason why the big Agrochemical corporations find interesting market

potentials in Brazil.

A second major challenge are the soils. Almost all tropical soils on earth are highly acid (i.e. ph. below

5.5) and nutrient poor due to frequent heavy raining and fast leaching. One of Brazil’s largest regions is

the so-called ‘Cerrado’, which covers a full 21% of the country’s territory. It is a grassland Savana with

unfertile and acid soils, normally ‘worthless’ for agriculture. Until the late 1960’s, Brazil’s food production

was limited to the territorially smaller Southern region. During the 1970’s, EMBRAPA has developed a

series of agronomic techniques and innovations to make the ‘Cerrado’ fertile and cultivable. The main

technique was the soil correction. By adding limestone or gypsum, a cheap prime material found in the

region, the pH value increases, the toxic soluble aluminium neutralizes, and valuable magnesium and

calcium is added to the soil. Through this technic, the entire Brazilian Savana was turned into fertile land.

Another breaking innovation was the Biological Nitrogen Fixation. Nitrogen is the main nutrient for plant

growth and is usually deficient in the soil while it is abundant in our atmosphere. EMBRAPA’s innovation

allowed the addition of specific microbes to the soil so that Gramineae crops (e.g. corn, wheat, rice,

sugarcane etc…) could uptake the Nitrogen of the atmosphere, fix it in the roots and use it for growth.

Hence, it resolved the problem of fertilizing and environmental hazard altogether, apart from an

important cost reduction. Today, about 75% of Brazil’s soya production uses this technique.

Other practices such as the direct planting system, a sustainable farming practice which avoids soil

erosion, and crop rotations, an important contributor to soil health and biological pest combating, are

other important techniques which may explain the ascension of the Brazilian agriculture in the last 40

years.

The growth of the global middle class in Asia and Africa will trigger food demand by more than 70% until

2050. While there is no exact plan for this challenge in place yet, it is certain that the growth must come

from the world’s tropical regions, given that Europe and the USA have no spare land and are close to their

potential yield. Originally, agriculture was a technique, which was developed and cultivated in temperate

climates during many centuries. Consequently, the agronomic techniques, practices and sciences were all

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 8 OF 58

developed for these climate and cannot be applied to tropical zones. This lack of an adequate and specific

science of food production is one of the factors that contributes to the underdevelopment and persistent

poverty of the global south. The work of EMBRAPA not only broke down this barrier for its own country,

but could be applied for many other countries in sub-Saharan Africa, Latin America and South-East Asia

that face similar issues like Brazil 40 years ago.

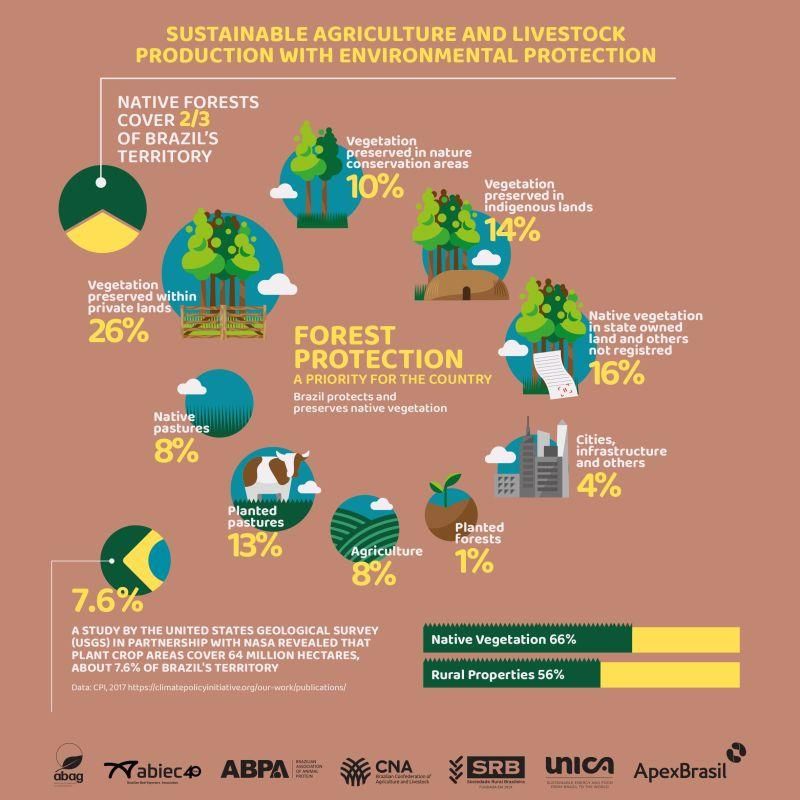

Agriculture, Environmental Sustainability and the Amazon

66% of Brazilian national territory is still covered with legally protected forest, which is by far the highest

number of all major and developed countries. 25.6% of this protected area are on farmers owned land,

10.4% are national parks, 13.8% are lands of indigene people and 16.5% are public lands.

Image 1 - Brazil: the second largest area preserved forests in the world

Source: APEX - Publication on the sustainability of the agriculture – LinkedIn Channel – August 2020

Nevertheless, it is impossible to discuss Brazilian Agriculture without doing a critical evaluation of the

topic of Amazon deforestation. The topic is multifaceted and extremely complex, involving many aspects

like environmental sustainability, crime and law enforcement, internal politics, bureaucratic regulations,

corruption, but also tradition, poverty and social aspects.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 9 OF 58

Apart from the deforestation, the fires that destroy mostly part of the “Cerrado” during the dry season are also regularly pointed out by the international community as a lack of willingness from the Brazilian government to address correctly this topic. Different reasons are at the origin of these fires, like the climatic reasons (dry season), the traditional practices but also illegal deforestation, which happens in remote places. Unfortunately, corruption and an excess in bureaucracy can help these criminals to ‘regularize’ later these territories and turn it into profit. The Brazilian government is defending its point, explaining that this internal issue is receiving the necessary attention from their part. Appropriate measures, like for example the creation of the council “Amazonia Legal” under the lead of Vice-President Mourao, have already been taken, aiming at solving the problem. Nevertheless, the lack of willingness from the government to discuss this issue openly with the international community and the satellite imagery showing an increase of the devastating areas, arouse suspicion about the capacity of the Brazilian government to correctly address this important topic. Recurrent declarations of members of the present government minimizing the problem also does not inspire trust from the international community. Existing strict environmental protection framework has not been changed by the current administration, but this attitude of shadowing the problem could have a negative impact for the country’s trade transactions and some Brazilian agribusiness associations and producers are worried to suffer boycotts in international markets. And in that sense it is worth adding that exporting agro producers are the ones least likely to be connected to fires, as they have to abide to strict current environmental protection framework from both the Brazilian government as well as the private stakeholders in order to maintain their exports. Associations of agro producers (such as the Soya, Beef and Citrus, for instance) already have their own very well adjusted and strict programs in place to monitor deforestation, using georeferencing tools and undertaking a close monitoring of all areas dedicated to production, also as a result from the pressure of the target countries they export to. Tools and guidelines exist and the challenges revolve around monitoring such a vast area as the Amazon, as well as the economic and social sustainability that also weigh heavily in this equation. AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 10 OF 58

OVERVIEW OF THE BRAZILIAN AGRIBUSINESS

Key Numbers of the Brazilian Agribusiness

Agribusiness is the sector that has protected Brazil from deeper downturn of the economy during the last

recession that hit the country in 2015. Over the past decade, labour productivity declined in the

manufacturing sector, stagnated in the services sector, and increased only in the agriculture. In 2017, this

sector was responsible for 4.5% of the GDP when narrowly defined and 23.5% when considering the

integrated agroindustry, including processed foods and beverages.

With 851 million of hectares, Brazil is the world’s 5th largest country and enjoys favourable conditions for

livestock and agricultural production (intensity of sunlight, availability of land and water resources).

The latest census undertaken by the Brazilian Institute of Geography and Statistics (IBGE) in 2017

identified 51’103 large farming operations with more than 1’000 hectares and 2’543’681 operations with

10 hectares or less. The small farms accounted for 2.2% of the land dedicated to agriculture. At that time,

the sector responded for 15.1 million of workplaces. Since 2017, the country has increased productivity

and, whilst shrinking the areas dedicated to farming, the sector accounted for 6.4% of 2019’s GDP, as

show in image 2, below.

Different studies tend to demonstrate that

when Brazil’s GDP contracts, the agriculture

sector usually grows. This seems to be once

again the case with the Covid-19 crisis, with

the agricultural sector taking advantage of

new market opportunities due to Covid-19,

by supplying foreign markets facing a

situation of product disruption. At the same

time, Brazil has not suffered from an internal

food supply shortage. Currently, the weak

Brazilian Real made the country’s

agricultural exports attractive on the

Image 2 - Importance of Agribusiness in Brazil’s GDP

international market, while the demand for

Compiled by the Swiss Business Hub Brazil with data from SECEA, 2020

imported food products is shrinking.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 11 OF 58As a result, while Brazil’s GDP was

forecasted to contract by at least 9% in

2020 during the same period, the

agricultural sector was expected to

grow by as much as 3% in August. But

it may surpass these expectations. As

per image to the right, up to mid-

November 2020, in spite of the Covid-

19 crisis, the agribusiness sector

accounted for US$ 85.8 billion, almost

46% of the country’s exports, an

increase of 5.7% in comparison to same

period of 2019 as shown below. Image 3 - Brazil Agricultural Exports vs. Total Exports - November 2020

Compiled by the SBH Brazil with data from CNA and SECEA – Period from Jan to Oct 2020

From 2017 to October 2020, Brazil’s agribusiness exports’ main destinations remained China, the

European Union and the United States as per image below. However, the percentages exported to China

increased almost 3%,

while the percentages of

the exports to the other

countries declined.

The agribusiness sector is

also responsible for

generating 102’467 job

openings from January to

October 2020, followed

only by civil construction,

whereas in the same

period, 558’597 job

positions across several

other sectors have been

extinguished.

Image 4- Main Agricultural Products Exported and its destinations

Compiled by the Swiss Business Hub Brazil with data from SECEA from Jan – Nov 2020 * RoW (Rest of the World)

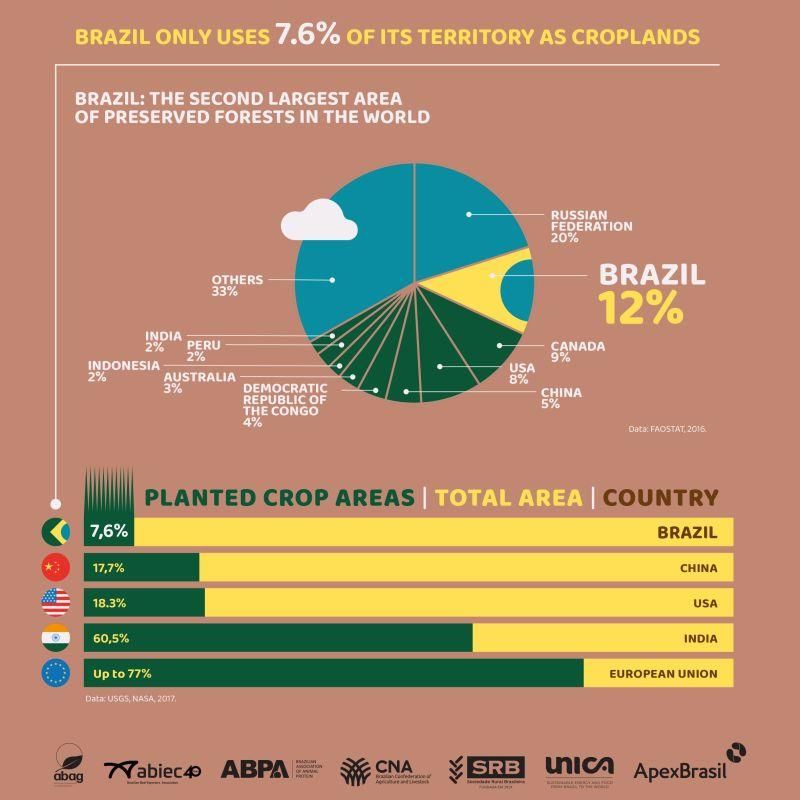

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 12 OF 58Currently, 30% of the

national territory is

dedicated to

agriculture, including

cultures mixed in

combination with

planted forests and

native forests, against

41% in 2017, with 2/3

of the territory

remains covered with

native forests, as

shown in image 5, to

the left. Plant crop

areas cover only 7.6%

of the territory.

Farmer groups in

Brazil are either

associations or

cooperatives. While

associations have

greater emphasis on

representativeness,

cooperatives seek

economic advantages

to the participants due

to economies of scale.

Image 5 - Sustainable Agriculture and Livestock Production with Environmental Protection

Source: APEX - Publication on the sustainability of the agriculture – LinkedIn Channel – August 2020

Despite the importance of cooperatives as an organizational tool, that enables small and medium farmers

to compete in a market, these organizations are still facing serious operational difficulties, ranging from

legal/regulatory to financing and management. Overcoming these difficulties, could greatly increase the

productivity of the Brazilian agriculture sector, in particular, the small and middle size farmers.

The expansion strategy of the Brazilian agriculture started during the late 70’s also had its downside.

Small farming lost its place and an enormous inequality was created. This inequality exists in all

dimensions - land ownership, productivity, access to technology, education, infrastructure, financing

services and market. A recent study shows that out of the 5 million landowners – not only agricultural

productive areas - a mere 15,686 people own 25% of the land, the same amount as the poorest 77% (3.847

Mio people). The picture in terms of productive land or farming areas is similar, where 8% of the farms

account for a full 85% of the total output. This is a level of inequality which can safely be declared as

extreme and unsustainable. Farming is a capital intense and risky activity, financing and insurance

services are an essential part of the value chain. Unfortunately, the traditional financial system in Brazil

is set-up in a way which effectively excludes smallholder farmers from these essential services. One simple

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 13 OF 58extreme weather event can push farmers to the verge of bankruptcy, and this has certainly been one of

the major factors of inequality and poverty.

Global Leader for the Production of Main Commodities

During the past three decades, Brazil’s agriculture sector has grown at an impressive rate. Brazil has

become the world’s largest producer of sugarcane, coffee, tropical fruits, orange juice, and it supports the

world’s largest commercial cattle herd with 210 million head. Brazil is also an important producer of

soybeans, corn, cotton, cocoa, tobacco, and forest products.

Image 6 - Brazil – A Leader in Global Agribusiness

Image compiled in October 2020 by the Swiss Business Hub with data from ABAG, ABIEC, CNA, APEX and USDA

Cotton

In 2019 Brazil became the 2nd largest world’s cotton producer

and the total production has reached 2.1 million of tons. The

main producing areas are Center West and Northeast of the

Country. 40% of the production supplies the domestic

market meanwhile 60% is exported, mainly to China.

Although shipments to China were significantly higher,

countries such as Vietnam, Indonesia, Bangladesh and

Turkey have also become important export destinations for

Brazilian cotton. Cotton producers are often also large

soybean and corn producers. Consequently, decisions

regarding which crop to plant are based on the expected

profitability for each crop.

The chart to the left is the result of a study elaborated by Image 7 - Cotton Production by Region - Growth from 2019 to 2029

FIESP (Federation of Industries of the State of Sao Paulo) Source: Outlook FIESP – Projections for the Brazilian Agribusiness

showing the outlook of the cotton’s production within the 2029 (July 2020)

next 10 years and the share of each region.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 14 OF 58Coffee

The Brazilian coffee harvested in 2019 was

approximately 44 million bags, resulting in a

decrease of 20% compare to the previous crop.

Generally, the fluctuation in production occurs due

to the biennial cycle of coffee trees with a higher

production within the first year. Brazil is 1st largest

producer and exporter of coffee worldwide. 70% of

the Brazilian production consists of Arabica coffee

and 30 % of Robusta coffee. 50% of the production

is exported, mostly to the European Union. The

main producing areas are located in the Southeast

of Brazil. Minas Gerais State concentrates the

Arabica coffee and Espirito Santo the Robusta

coffee.

Image 8 - Coffee, Production by Region - Growth from 2019 to 2029

Source: Outlook FIESP –Projections for the Brazilian Agribusiness 2029 (July

Soybean 2020)

Soybean is extremely important for the Brazilian economy and for the trade balance. The country is the

2nd largest producer and first largest exporter worldwide and, with 37 million hectares harvested in 2o20,

this will be Brazil’s largest soybean harvest. The biodiesel program plays an important role in soybean

demand. Last year, 5.9 million cubic meters of biodiesel were produced in Brazil, 70% of which used

soybean oil as raw material.

During the past decade, the soybean production has almost doubled and exports growth was the most

important market driver. 58% of the production is exported and almost 80% of the volume is sent to

China. Brazil is taking advantage of the ongoing dispute between USA and China, as China has

significantly increased their purchase of Brazilian soybeans and reduced imports from the USA.

Image 9 - Soybean Production by Region - Growth from 2019 to 2029

Source: Outlook FIESP –Projections for the Brazilian Agribusiness 2029 (July 2020)

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 15 OF 58Sugar

As main producer and main exporter worldwide, Brazilian producers are suffering from the low prices of

sugar and many farmers are investing in ethanol production, where prices are more attractive. There are

good reasons to be optimistic about the growth of the ethanol market in Brazil in the coming years, due

to an increased demand for the product on international markets, mainly in Asia. However, the crisis

generated by the Covid-19 pandemic has drastically reduced fuel consumption in the impacted countries

and, consequently, oil prices began to decline in the foreign markets. There is a lot of uncertainty in this

industry, but the devaluation of the Brazilian Real is helping keep the prices at reasonable level.

Currently, 65% of the Brazilian sugarcane production is for ethanol. 71% of the sugar production is

exported.

Image 10 - Sugarcane Production by Region – from 2019 to 2029

Source: Outlook FIESP – Projections for the Brazilian Agribusiness 2029 (July 2020)

Orange Juice

Brazil is the world’s leading producer and exporter of

orange juice. The regions with the highest concentration

of citrus production, the state of São Paulo and southern

Minas Gerais, had an excellent performance in 2019,

reaching 386 million boxes. The 2020-21 orange crop is

estimated at 287 million boxes, a reduction of 25% due

mainly to adverse climatic conditions. Domestically,

prices paid to farmers per box of orange had remained at

profitable levels. The Coronavirus pandemic had a positive

impact on the industry and prices rose by more than 20%

since March 2020. The higher prices may be correlated

with greater global demand for the product, as people have

started seeking vitamin C rich products more intensively

as a way to boost their immune system. 51% of the

production is exported and 70% flows into the European Image 11 - Orange Production by Region - from 2019 to 2029

market. Source: Outlook FIESP –Projections for the Brazilian Agribusiness 2029 (July

2020

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 16 OF 58Beef

With more than 210 million head of beef cattle, Brazil is the world’s largest beef exporter and second

largest beef producer worldwide. Since 2018, China has been a significant importer of Brazilian beef and

the outlook is very promising for the next years. While representing just over 20% of national production,

foreign sales have played a decisive role in livestock chain dynamics.

In recent years, the domestic market is decreasing

due to difficult economic situation. Brazil has the

capacity to respond to an increasing global demand,

because of its potential to expand supply, in

particular, by increasing herd productivity.

Beef cattle slaughter continues to expand, although,

since late 2018, it has been supported more heavily

by increased male slaughter and lower female

slaughter. The veal proportion has increased

considerably due to strong demand for this

category. This also indicates the influence of

technology in speeding up the feeder stage, allowing

the earlier slaughter of the animals.

A positive outlook for the Brazilian beef industry

rises from the fact that some of Brazil’s foreign

competitors, such as the United States, Australia, Image 12 - Production of Beef by Region - Growth from 2019 to 2029

Argentina and Uruguay, continued with the Source: Outlook FIESP –Projections for the Brazilian Agribusiness 2029 (July 2020

slaughter of a high proportion of their females in the

last two years. Therefore, this suggests that meat supply is likely to drop in these countries due to veal

shortage. An outlook of the Federation of industries of the State of Sao Paulo shows that Brazilian exports

of meet could increase by 102% until 2029.

Poultry

As 2nd producer and major exporter worldwide, the

poultry industry in Brazil had a more positive

experience in 2019 than in the previous year. Feed

costs remain high and this impacts negatively the

profitability of the business for the farmers. The

increasing demand from international markets -

especially from China - could compensate the lower

economic growth on the domestic market. Apart

from China, Brazilian exports have also increased

in other significant countries where performance

had been weaker in the past year, such as Saudi

Arabia, Japan and Egypt. Sales to the European

Image 13 - Production of Poultry by Region - Growth from 2019 to 2029

Union, however, were even lower than those

Source: Outlook FIESP –Projections for the Brazilian Agribusiness 2029 (July 2020)

observed in 2019.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 17 OF 58Livestock

Brazil is the largest exporter of beef and poultry, and the third largest exporter of pork. Livestock farming

has experienced strong growth and transformation over the last three decades with the prioritization of

capital-intensive technologies. This has resulted in significant productivity gains. Poultry meat

production has increased by 22 times in the last 40 years; pork, 4 times; milk, 4 times; and beef

production, 4 times.

Image 14 - Evolution in Chicken Breeding Performance – Food Conversion X Body Weight X Slaughter

Source: APEX - Publication THE TECHNOLOGICAL INNOVATION PROMOTED BY BRAZILIAN FARMERS

There is a common misperception that the growth path of the Brazilian agricultural has been primarily

based on the expansion of the land area. According to a study by EMBRAPA, Martha, Alves & Contini

(2012), productivity gains explained 79% of the growth in beef production in Brazil from 1950 to 2006.

Between 1990-2019 productivity growth in cattle farming was estimated at 169%, whereas pasture area

has declined by 15.5% (Abimec and APEX).

Increased productivity with less animals, boosting continuous growth: the expectations for production

growth until the end of this decade are +27% in the case of beef, coming along with an increase of the

number of cattle by only 9%. Pork production (+39%) and poultry (+29%) will also grow strongly. A

particularly large increase in productivity is expected in the dairy farming: +39% in the amount of milk

produced with an increase by 5% in the herd.

The cattle industry has traditionally been very important in Brazil. According to the Brazilian

Confederation of Agriculture and Livestock (CNA), the gross value of livestock farming will reach 269

billion BRL (44.67 billion CHF) by end of 2020. Average productivity has increased from 1.6 @/ha/year

in 1990 to 4.3 @/ha/year 2019.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 18 OF 58It is important to emphasize that the

reality in Brazilian farms is marked

by enormous inequality in

production: some produce many

arrobas per hectare and the vast

majority produce very little. Large-

size specialized stocking and

finishing beef farms, typical of the

Cerrado region, exhibit cost

economies and high efficiency levels.

In the reality of many producers,

cattle ranching is still a low-tech

activity, quite extensive and with low

profitability, indeed.

The digital transformation in the

livestock segment began between 10-

20 years ago with a simple task:

replacing paper notes and graphs

built by hand with spreadsheets and

input of cards by direct registration

on cell phones and tablets. Real-time

information, greater variety of

Image 15 - Livestock productivity

graphics and data crossing facilitate

Source: APEX online publication, August 2020

the producer’s daily decisions about

production strategy, while reducing errors and saving physical space. Countless are the software solutions

that aim to offer these technological instruments. The apps have become increasingly accessible and

widespread.

Examples include: JetBov, Procreare, and Bovcontrol. Typical features are financial control, weighing,

purchase and sale control, auctions, evaluation of cost/benefit of nutritional supplements, health or

vaccine control. BovControl also permits the monitoring of pregnant cows, a feature that allows the

farmer or veterinarian to monitor every pregnancy remotely, predict birth and send alerts. Some

softwares allow comparing inputs from different brands and distinguishing interventions on lots or the

individual animal.

Increased productivity in Brazilian livestock farming is the result of decades of investment in technology

and know-how. Around 80% of cattle is pasture-fed only. According to a study by Silva, Barioni et al.

(2017), more than half of Brazilian livestock production is on degraded pastures, what compromises the

profitability. Adequate fertilization of pastures, management and rotation of cattle in pastures and/or

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 19 OF 58irrigation of pastures, crop integration, livestock and forests are therefore very important. Image 16 - Results of Embrapa's Study 2018 on the priorities in the Management of Beef Cattle in Brazil Image compiled by the Swiss Business Hub Brazil, October 2020 Furthermore, a series of technologies such as nutritional supplementation, creep-feeding, pasture rotation, semi-confinement and confinement and a more professional farm and livestock management, e.g. in animal breeding, reproductive efficiency, and sanitary controls have helped to increase productivity and will play an increasingly important role in achieving the productivity goals mentioned in the introduction. The predominant driver of the digitalization and automation in livestock farming are cost concerns. According to an EMBRAPA survey with 1630 participants from all states of Brazil in 2018 (results are displayed in image 16 above) production cost turned out to be the main concern of the farmers. It was followed (with a clear gap) by capacitation of its workforce and concerns surrounding the quality maintenance of its means of production (degradation of pasture, conservation and fertility). Efficiency is pushed forward also through genetic research and optimization of the logistics along the entire value chain. Only recently consumer-related certifications such as labels for quality, environmental or animal-friendly productions have gained awareness in Brazil. They are best-established in the production of eggs and poultry. According to EMBRAPA, only around 6% of cattle are currently in quality programs. The market for premium meat is large and the potential therefore enormous. A backlog that is to be closed through closed efforts in this area – also in the declaration of origin. In general, Brazilian livestock is focused on quantity, not quality. But that can change. AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 20 OF 58

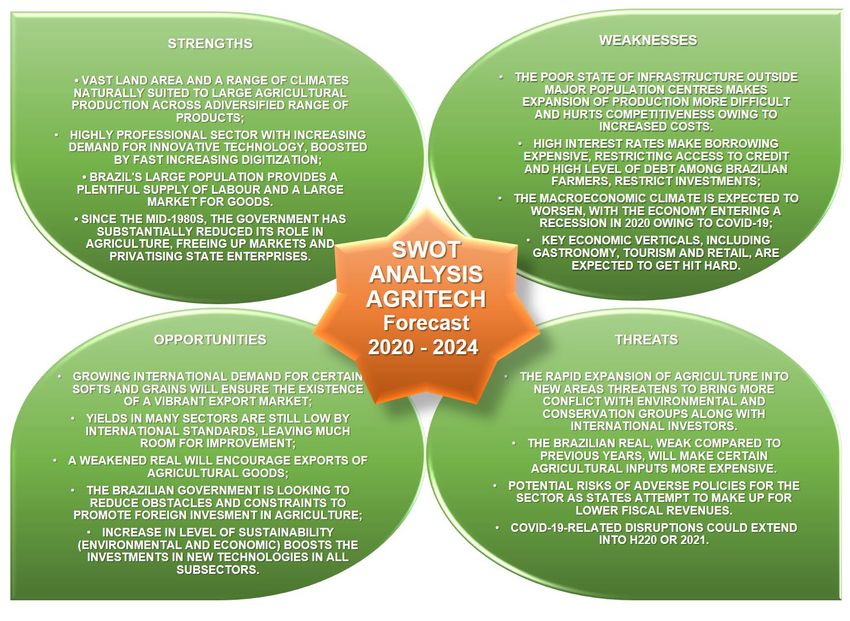

SWOT Analysis of Agritech in Brazil 2020 – 2024

Image 17 - SWOT Matrix of Agritech in Brazil - Macro 2020 – 2024

Source: Image compiled by the Swiss Business Hub Brazil – November 2020

Challenges for the future

By 2050 the world’s population will reach 9 billion and 70% of them will live in urban areas. In order to

feed this larger, urban and richer population, food production must increase by 70%. Brazil intends to

cover 40% of the global demand and therefore the agribusiness will always be one of the most important

drivers of the economy and gain interest and support from the central government.

In order to reach this ambitious goal, Brazil has to solve some challenges that the sector is facing, amongst

which are:

• Investment in transport infrastructure and additional modal options (roads, railways, ports) has

to be undertaken in order to reduce the cost of the freight;

• Increase the capacity of grain storage;

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 21 OF 58• Modernize systems for milk production in order to increase the productivity;

• Increase the access to credit lines for new investments aiming at improving production –

especially relevant considering the high level of debt among Brazilian farmers;

• Ensure better access to international markets for Brazilian agribusiness products through

enhanced trade policies;

• Improve internet connectivity across the country and rural areas (in coverage as well as in speed

and stability);

• Enhance and promote the level of sustainability (environmental, economic and socially)

characteristic of the Brazilian Agriculture, contrary to general perception in other markets;

• Avoid any expansion of the agriculture through deforestation in Amazonas, which will have a

strong negative impact for Brazilian products on the international markets;

• High dependency to China has to be leveraged, diversifying export markets.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 22 OF 58DIGITAL AGRICULTURE IN BRAZIL

Open Eco-Systems & R&D for Tropical Agriculture

In the path for a modern and developed agriculture, Brazil will have to invest in R&D and create an

innovation driven ecosystem. In this sense, EMBRAPA will have once again a major role in supporting

these activities in Brazil.

The goal followed by EMBRAPA is to support the technology transfer in the niches and segments left out

by the commercial companies and service providers. EMBRAPA has an enormous stock of scientific

papers and patents focused on agronomic, biological and technical problems specific to Brazilian

agriculture and actively seeks partnerships with commercial companies (national or foreign), to develop

joint offers for the market. A typical project can be a shared IP and joint venture, where the company

brings in its IoT hardware and cloud-based computing platform, while EMBRAPA develops the biological

algorithms to forecast a certain local disease and helps with market access.

If the reader now hoped to find a vast and technologically underdeveloped market, the expectations will

probably be disappointed. Digitization, of course, did not pass unnoticed by one of the world’s leading

food suppliers. The state of Sao Paulo, most notably the city of Piracicaba - about 150 from the city of São

Paulo - is in process of becoming one of the world’s major hubs for Agri-Tech ventures. Currently, the

Brazilian AgTech market map counts approximately 593 startups in the sector.

Image 18 - AGTech Valley Hub Piracicaba

Source: AG Tech Valley Piracicaba Website

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 23 OF 58These dynamics have multiple reasons. The most important is certainly the institutional and cultural

commitment to make Brazil an Agriculture powerhouse. The vital role of Embrapa was already discussed.

Apart from Embrapa, the University of Sao Paulo’s ESALQ (Escola Superior de Agricultura "Luiz de

Queiroz") is a unit of the University of São Paulo (USP – one of the world’s most renowned Universities

in Agronomic Science) and is another expression of this public compromise to foster R&D in Agritech.

Esalq was born in 1901, in Piracicaba, from the dream of the visionary Luiz Vicente de Souza Queiroz,

donor of Fazenda São João da Montanha to the government of the State of São Paulo, to create an

agricultural school. Until 1934, the Institution was part of the Department of Agriculture of the State of

São Paulo. From then on, it became part of USP, as one of its founding units. Since its creation, Esalq/USP

has constantly evolved, expanding its performance based on the teaching, research and extension pillars.

The strong inclination that Esalq has for differentiated teaching and quality research is contemplated in

130 laboratories installed in 12 departments, in a structure that employs more than 750 professionals

among teachers and technical-administrative servers.

Piracicaba has become an important hub for the generation of agricultural knowledge and technology in

Brazil, creating the basis for the birth of many AgTechs and boosting incubation initiatives (EsalqTec

incubator), acceleration, hubs and co-workings (PulseHub and AgTechGarage). This environment has

become very attractive for venture capitalists: from angel investors and accelerators to many others.

The Artificial Intelligence Hub Londrina was inaugurated in 2019 in order to foster big data, cloud

computing and machine learning solutions in different productive sectors, including agribusiness.

Lab analysis

Biological Control

Shared economy

Fertilizers, nutrients

Genomics and biotech

Animal Nutrition

Seeds

Finance services

Image 19 - Number of Startups in AGTech "before the farm"

Source AG Tech Survey 2020

The Londrina AI Hub project is an investment of Senai Nacional and partners such as the Fiep System

(Federation of Industries of Paraná). Some other partners such as institutions and companies in other

sectors also include IBM, Google and Microsoft, as well as MIT Computer Science & Artificial Intelligence

Lab (United States), Fraunhofer Institute for Industrial Engineering (Germany) and Vector Institute

(Canada), as well as ventures and angel investors.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 24 OF 58The Agri Hub Space - Mato Grosso is the first agroecosystem in the Middle west of Brazil. Main focus is

open innovation, startups’ programmes and business attraction.

Ag Tech Survey: Inside the Farm

Precision Land Management

Agriculture

Content, Education and social media

Images

Water and Residue management

Iot

Equipment

Irrigation

Image 20 - Number of Startups in AGTech "inside the farm"

Source AG Tech Survey 2020 Monitoring

Remote sensoring

Management

Telemetry

Drones

While the innovation in Agritech is booming, we also observe a typical phenomenon in the Brazilian

economy. Recently, the country went through economically difficult times with a recession, negative

economic outlook and the chronic problems of its institutions and industrial sector surfaced.

Agribusiness, which in the last years already accounted for a significant share of the Brazilian GDP, seems

to be immune against such problems. As a consequence, professionals and investors sought shelter in it,

causing a massive inflow of human and financial capital into the sector. Hence, we have financial capital,

human capital, a large domestic market and scientific support – all ingredients needed for a successful

innovation hub.

Despite these highlights, the general market climate can be characterized as ‘overheated’. There are many

startups on the market without a technically viable product (or even products at all), focusing more on

the marketing aspect than on the R&D. Given the availability of capital, many of these companies are well

financed, but struggle to find market acceptance as they fail to demonstrate technical benefits. It is not

uncommon to give customers a 12 months free trial for the services, only to learn later that the

subscription rate hoovers around 5%. Many of these ventures certainly may disappear in the mid-term.

Another group with challenges ahead are the startups that indeed bring breaking new technologies

solving real problems, but did not find a viable business model. This can happen if applying the

technology is so complex or technically demanding that end-users, i.e. farmers, are unable to handle it by

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 25 OF 58themselves and automation is not possible. This is typically the case for many technologies in the area of

laboratories, biotechnologies and fertilizers, but can be equally true for IoT companies and their

maintenance. In a country of continental proportions such as Brazil, it is hard to build up nationwide

business model, which requires physical presence of qualified labour. The reality of such startups is often

that they focus business in a few large sugarcane or soya producers around their hub in Piracicaba. A

working pilot in a sugar refinery next to the ESALQ is one thing. How to profitably serve a large farmer

in the south of Maranhao is a different challenge altogether.

Such models can indeed be very interesting for Swiss core technology. Despite all the efforts, investments

and innovation hubs, Brazilian industry continue showing some severe weak points. Fortunately, these

areas of expertise tend to be exactly the areas where the Swiss industry excels. Examples are sensor

technology, robotics and precision mechanics, electronics, camera and imaging technology, high-

performance computing and, of course, the entire field of data science and artificial intelligence. On the

other hand, Brazil counts on an excellent expertise in agronomics, especially tropical agriculture,

hydrology, biology and chemical engineering. Furthermore, Brazilian entrepreneurs usually know their

market very well, understand the particularities of their customers and are competent in dealing with

complexity, risks and social aspects, a crucial aspect of any successful business.

Given that off-shelf product sales are difficult, a partnership with a local company with complementary

technology and skills can be a promising alternative. If the focus is right, i.e. on the left-out market niches,

chances are that the venture may become part of a Public-Private Partnerships with EMBRAPA and

eligible for a financing support from the development bank (BNDES).

Brazilian Agri-Tech Market

Evaluating the entire Agri-Tech market would go beyond the scope of this paper, but it is worth

mentioning some innovative companies present in Brazil:

Strider www.strider.ag Metos Brazil www.metos.com.br

Strider is probably the most successful Metos Brasil is the local subsidiary of Austria-based

technology company inside the sector. IoT weather station manufacturer Pessl Instruments.

Strider is a digital agriculture platform, The company’s big strength is its market experience

whose objective is the improvement of the of 35 years, its robust quality hardware and its global

efficiency of pest and disease control. The innovation leadership in field sensor technology.

app includes a scouting function, which Recently, under the brand Data by Metos, the

uses photo recognition technology to company started its localization strategy, where it

detect and identify different pests and crop proactively seeks R&D collaboration with local

diseases. The company was acquired by players, such as EMBRAPA and Strider, in order to

Syngenta. adapt the technology to the needs of tropical farmers.

Irriger www.irriger.com.br InCeres www.inceres.com.br

Owned by the US company Valmont, InCeres is a soil fertility cloud processing firm, with

Irriger is an irrigation management over five million hectares in primary data, evolved to

platform. It connects climate data, soil lead a data science revolution integrating the fertilizer

sensor data and satellite images to create supply chain. The system provides a data science

daily irrigation decision support, aiming at assistance for consultants in the field.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 26 OF 58a more sustainable and cost-efficient

agriculture.

Solinftec www.solinftec.com Agrotools www.agrotools.com.br

Solinftec is the dominating IoT platform in Agrotools is a platform system combining

the sugarcane industry, integrating and geomonitoring, data bases, competitive intelligence

digitalizing all aspects of the farming and strategic tools for better management of the

operation. Its main focus is on the territory. The algorithms analyze the complexity of

automation of farm equipment, the productive and preserved territory and create

application control and the integration of meaningful insights.

different third party information, such as

weather.

Systech Feeder www.systechfeeder.com.br Mobimilk ajagro.agr.br/mobimilk-ordenha-movel

Systech is a Brazilian startup company that Mobimilk is also the name of their first solution, a

won the Ideas for milk contest in 2017 for container which works as a ‘mobile milking room’.

the feed. Feeder supplies feed and Simply connect water and energy to start milking

monitors, in real time, intake and weight cows, without civil works. Moreover, the tool

gain of lactating calves. The remote device monitors somatic cell counting and animal’s

emits visual alerts during sudden change temperature, issuing alerts. The system can be

of consumption and time for weaning. operational within a few hours.

Agromarra www.agromarra.com.br BovControl www.bovcontrol.com

manages production in real time through

With an integrated platform that allows for the data

app or web interface, tracking each animal

collection and analysis, provides recommendations to

indexes and profitability operations. It is

farmers on how to enhance their performance in the

ready to connect to devices such as barcode

production of meat, milk and genetics. The Brazilian

earring, drone, scale and automatic

startup internationalized to the U.S. and is rapidly

milking solutions.

expanding to many other countries.

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 27 OF 58TECHNOLOGY OPPORTUNITIES FOR SWISS

INDUSTRY IN DIGITAL AGRICULTURE

Meteorology & Risk Management

Weather and climate are the first and most important risk factors of any farming activity. Most fields in

Brazil are rainfed, hence, obtaining enough and regular rain is critical. Furthermore, temperature and

humidity are variables that play an important role for the general growth climate, as well as for the disease

pressure. Most farming operations, such as pesticide spraying, tilling, field accessing, and planting can

only be executed under certain weather conditions. It is therefore clear that reliable weather data for past,

present and future are the farmer’s most important basis for operational decision taking. Note that under

tropical conditions, weather tends to be a more important factor, as it can change rapidly and it is difficult

to forecast.

Weather Stations

Weather stations are still very sparse in

Brazil. The public network from Inmet

(Instituto Nacional de Meteorologia) has

around 500 weather stations, which is by far

not enough, given the enormous size of Brazil.

In average, each station covers around 17’000

km2 and is 130km distant from the next. This

is about 10 times less than the ideal

distribution, which depends on the spatial

autocorrelation. It is typical that farmers buy

their own weather stations, which typically

come along with agrometeorological services,

such as weather forecast specific to each

Image 21 - IoT based field weather station in an irrigated corn field

agronomic task or crop disease modelling.

Source: Drawdown Labs Library

Weather Forecasts

Weather forecasts are available in Brazil. However, their precision is far from North American or

European standards. There are multiple reasons for that. Initially, while meteorology in Europe and

North America looks back on a long, scientific history, along with significant investments from both the

public and private sector, the same is not true for Brazil. There is only a hand full of local weather services

and most, if not all, do not have the precision required for farming. Second, there are very few good

weather models available. While the world’s leading Meteorological Institutions like NOAA, Deutscher

Wetterdienst and UK Met run very precise models for the Northern Hemisphere, Brazil is only covered

by their global models, which are usually much less precise. The third factor is the lack of accurate ground

data, which is crucial for the precision of weather models. The Swiss Precision Meteorological Institution

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 28 OF 58Meteoblue is one of the few exceptions, which runs two own, precise weather models for Brazil and use

weather data from farmers own weather stations to calibrate the models. The result is a much higher level

of accuracy and a highly successful market product, called ‘Hyper-localized Agrometeorological Weather

Forecast’. Meteoblue is currently extending this service to the so-called virtual weather station concept,

where the same service can be offered without the need of a physical weather station.

Microclimate monitoring

Microclimate monitoring is another challenge. Today’s weather models’ resolutions are not sufficient to

capture these microclimates. They need to be measured and, in fact, they are hardly understood

scientifically, but they can affect crops substantially. Ordinary weather stations are usually too expensive

to place on such a high density, even though recent communication technologies have brought new cost

drops. However, there is still a vast territory to be explored in how to measure, analyse, model and adapt

farming operations to microclimates.

Climate Risk Modelling

Climate risk modelling is another activity which is still largely underdeveloped. Given the lack of ground

data and precision weather models, it is very difficult to figure out the climate history of a certain field or

farm. This, however, is decisive for real estate valuation, crop insurance policy pricing and long-term crop

decisions. What is needed here is not clear. Some approach including weather data modelling, machine

learning approach and using the few ground data available could be one approach to recover a climate

history of the last few decades. Once this data is available, statistical techniques can help to understand

climate risks, make better decisions in real estate, crop insurance and crop decisions.

IoT, Sensor Technology & Platforms

The concept of the Internet of Things (henceforth IoT) has also been introduced in Brazilian Agriculture.

Indeed, the use of sensors in farming activities is nothing new. Be it tractors, sprayers, tanks, insect traps,

silos or soil moisture, rain gauges or thermometers, measuring has always been part of the farmer’s daily

routine. However, these sensors have usually been manual readings or, at best, island systems. It is not

unusual that larger farms still have entire teams of qualified people to go daily around the fields, gather

sensor readings and fill in Excel sheets.

The IoT is bringing a real revolution to this. Meanwhile, there is a complete eco-system of startups,

manufacturers and platforms that build, install and connect all kind of sensors on the farm. Most of these

companies unite hardware, connectivity and software platforms and are focused on a certain domain.

There are successful examples of companies providing systems that come with a large range of sensors, a

proprietary communication system and an intelligent platform, creating optimization recommendations

for farm management. There are also companies offering intelligent field stations connecting any kind of

climate sensors, soil moisture sensors and plant sensors, whose data all come together in a platform.

Further ahead, applications that integrate machine management, labour, inventory and production

control, logistics, financial management and climate data will set the trend. Treating farming as a

AGRITECH IN BRAZIL – REPORT – JANUARY 2021 PAGE 29 OF 58You can also read