Analyst presentation H1 2018/19 Half year ended 30 September 2018, 20 November 2018 - Lucas Bols

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Analyst presentation H1 2018/19 Half year ended 30 September 2018, 20 November 2018

Disclaimer

DISCLAIMER THIS PRESENTATION may contain forward looking statements. These statements are based on current expectations, estimates and projections of Lucas Bols’ management and

information currently available to the company. Lucas Bols cautions that such statements contain elements of risk and uncertainties that are difficult to predict and that could cause actual

performance and position to differ materially from these statements. Lucas Bols disclaims any obligation to update or revise any statements made in this presentation to reflect subsequent events or

circumstances, except as required by law.

Certain figures in this presentation, including financial data, have been rounded. Accordingly, figures shown for the same category presented in different tables may vary slightly and figures shown

as totals in certain tables may not be an exact arithmetic aggregation of the figures which precede them.

2

H1 2018/19

1. Lucas Bols at a glance

2. Highlights H1 2018/19

3. Operational highlights

4. Financials H1 2018/19

5. Outlook

3

Lucas Bols at a glance

13.4%

18.5%

20.0% 46.7%

22.7%

19.9%

Revenue EBIT*

€m €m

4

Global brands organic revenue growth of 3%

Global brands Revenue split H1 2018/19 Regional brands

Regional brands

Bols Liqueurs range € 10.2 mln. Liqueurs

21%

79% 29,8%

White Spirits Italian Liqueurs 70,2% Dutch Jenever portfolio

Global brands

€ 37.6 mln.

Gross Profit split H1 2018/19

Regional brands

€ 4.9 mln.

Passoã Nuvo 17% Value brands

83%

Global brands

€ 24.0 mln.

5

Strong and diversified global footprint, with around half

of the revenues coming from outside of Western Europe

Group revenue per geographical segment based on H1 2018/19

6

Clear strategy to capture the growing cocktail trend and premiumization

while maintaining the competitiveness of regional brands

Mission Lucas Bols

We create great cocktail experiences around the world.

Strategic framework Lucas Bols

Lead the Leverage

Build the Accelerate global

development of operational

brand equity brand growth

the cocktail market excellence

• To strengthen and grow our global brands in the international cocktail market

• To maintain the competitiveness of our regional brands in regional and local markets

7

H1 2018/19

1. Lucas Bols at a glance

2. Highlights H1 2018/19

3. Operational highlights

4. Financials H1 2018/19

5. Outlook

8

Highlights H1 2018/19*

Revenue Revenue of € 47.8 million, in line with last year

Global brands reported revenue growth of 3.0%, while revenue of the regional brands was down 10.5%

Brand

mainly as a result of temporary import restrictions in Western Africa and lower jenever/vieux sales in the

performance

Netherlands

North America achieved double-digit revenue growth on the back of a strong performance in the US. Asia-

Regional

Pacific showed healthy revenue growth, while both Western Europe and Emerging Markets saw revenue

performance

decline due to the performance of the regional brands

Gross margin The overall gross margin came in at 60.5% (down 110 bps) as a result of relatively lower shipments to

higher margin markets

EBIT EBIT amounted to € 12.9 million in line with last year

Net Profit Net profit came in at € 7.9 million, which is in line with last year

Dividend Interim dividend set at € 0.35 per share in cash, equal to last year

*All comparisons are on an organic basis, i.e. at constant currencies and excluding one-off items. In H1 2018/19 the one-off items consist of one-off restructuring

costs of € 0.3 million (net) at Avandis. Pre-IFRS 15/16. 9

H1 2018/19

1. Lucas Bols at a glance

2. Highlights H1 2018/19

3. Operational highlights

4. Financials H1 2018/19

5. Outlook

10Operational highlights H1 2018/19 – global brands

Bols Liqueurs range: Revenue in line with last year

• Continued growth in the US, driven by increased distribution in retail chains

• Strong performance in China was off-set by a decline in Japan

• Bols Watermelon and Bols Cucumber successfully launched as LowBols heroes

• New flavours added to the ‘Add Flavor To Your Margarita’ program

• Multiple activation programs aimed at both on and off-trade

White spirits : Overall stable performance

• Bols Genever Red light Negroni expansion in the US, activation in several

other markets

• Continued double digit growth trend for Damrak Gin in both the US and the

Netherlands

• Damrak Gin launched in South-Korea and listed at Formula 1 in Singapore

• Bols Vodka under pressure in Canada and Argentina. Continued good

performance in the Netherlands

11Operational highlights H1 2018/19 - Global brands

Italian Liqueurs: Performance slightly below last year

• Highest score of Galliano L’Aperitivo in Wine Enthusiast Magazine bitter

test

• Social media campaign for Galliano L’Aperitivo in the US

• Solid performance of Galliano in core market Australia

• Strong performance Vaccari following global brand restyling

• Vaccari on-premise activation in key cities in Mexico

Passoã: Continued good performance with mid-single digit revenue growth

• Distribution expanded in the US to 35 states and new listings, both on- and off-trade

• Recovery in Puerto Rico, growth in Asia-Pacific

• New brand activations in Western Europe

• Signature cocktail “Porn Star Martini” expansion continues in the UK

Nuvo: Relaunch in de US

• Gradually building up the distribution with focus on a limited number of states

• First signs of activations are positive

• Strong retail activation program planned for H2 2018/19

12Operational highlights H1 2018/19 - Regional brands

• In Western Africa the company experienced temporary import restrictions into Togo and Benin

• Revenue Dutch domestic jenever/vieux portfolio was down as a result of the declining market

• Planned relaunch of Bols Jenever and Bokma with strong promotional activities in the second half of 2018/19

• Activation Bols Jenevers with new activation program “Bols komt met een biertje” in October

• New drinks strategy Coebergh in the Netherlands and activation programs Pisang Ambon in Belgium and Denmark

13Operational developments H1 2018/19 - US

Strong organic revenue growth of 12.9%

Continued strong performance Passoã, with additional retail and on-

trade listings secured

Further strengthened the retail position of Bols Liqueurs on the back of

the recent listings and continued growth of market share

Strengthened brand awareness Bols Genever through activations such

as #redlightnegroni during the Negroni week in the USA

Damrak gin - Accelerate distribution in the US by a Social Media

campaign “Ride like an Amsterdammer”

Relaunch of Nuvo with focus on a limited number of states .

14Awards

Galliano L’ Aperitivo

• Wine Enthusiast 94 points

Highest rated bitter

• Listed in the top 100 spirits of

2018

151. Lucas Bols at a glance

2. Highlights H1 2018/19

3. Operational review

4. Financials H1 2018/19

5. Outlook

16Revenue and EBIT in line with last year

Highlights

Revenue amounted to € 47.8 million, which was in line with last year at constant

currencies. The effect of currencies on revenue was € 0.9 million negative.

The gross margin stood at 60.5%, a decrease compared to 62.2% in the first half of

2017/18. This decrease is the result of currencies, relatively lower shipments to higher

margin markets and the introduction of Nuvo.

EBIT for the first half of 2018/19 came in at € 12.9 million in line with last year, at

constant currencies and excluding the one-off restructuring charge at Avandis of

€ 0.3 million (net of tax).

The EBIT margin came in at 26.9%, organically in line with last year.

* Excluding the impact of IFRS 15 and 16

Organic growth: at constant currencies, excluding one-off items

17Global brands showed an improvement in revenue of 3.0%

Revenue development (in €m)

-2.0% Group revenue structure

(H1 2018/19)

1.1 -1.2

48.8

-0.9 21%

47.8

79%

Global brands Regional brands

H1 2018/19* H1 2017/18 Reported Organic

Revenue (* €m)

growth % growth %

FY 2017/18 Δ Global Brands Δ Regional Brands Δ FX FY 2018/19 Global brands 37,6 37,4 0,7% 3,0%

Regional brands 10,2 11,5 -11,1% -10,5%

Total 47,8 48,8 -2,0% -0,3%

48.4% 60.5%

62.2% 63.7%

* Excluding the impact of IFRS 15 and 16

Organic growth: at constant currencies, excluding one-off items

Reported gross margin

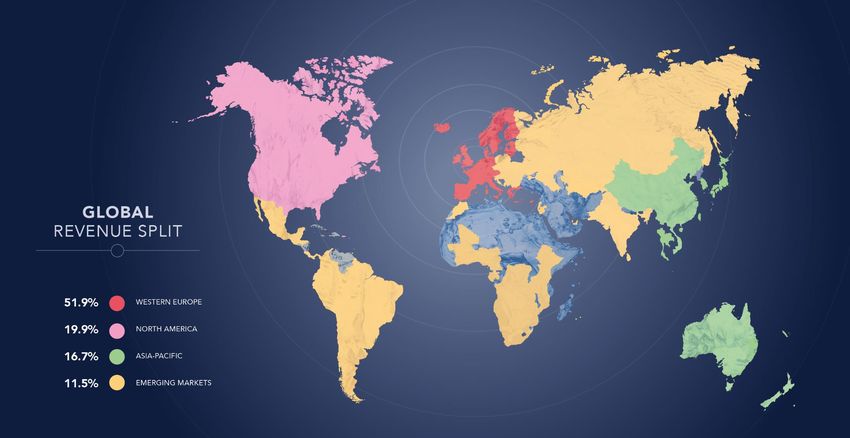

18Revenue by region

Revenue development at constant currencies (in €m)

Western

48.8 -0.5 Europe

0.9 Western Europe

-0.8

-0.9 • Revenue global brands broadly in line with last year

0.2

47.8 • Strong growth in the UK and the Netherlands, offset by

lower shipments to France

• Domestic jenever/vieux portfolio was down in line with the

51.9%

decline of the market

FY Δ Western Δ Asia- Δ North Δ Δ FX FY

2017/18 Europe Pacific America Emerging 2018/19

Markets

H1 2018/19* H1 2017/18 Reported Organic Asia-Pacific Asia-Pacific

Revenue (* €m)

growth % growth %

• At constant currencies revenue was up

Western Europe 24,8 25,8 -3,7% -3,1%

• Mainly driven by accelerated growth in China

Asia - Pacific 8,0 8,3 -3,7% 2,6%

North America 9,5 8,7 9,6% 11,2% • Japan is showing a decline due to challenging market

Emerging Markets 5,5 6,1 -9,5% -7,7%

conditions and related stock reductions

Total 47,8 48,8 -2,0% -0,3%

• Australia/New Zealand: a small growth in a stable market

* Excluding the impact of IFRS 15 and 16 environment 16.7%

Organic growth: at constant currencies, excluding one-off items

19Revenue by region

Revenue development at constant currencies (in €m)

North America

North America

48.8 -0.5

• Positive growth trend continues

0.9

-0.8 • Double digit growth in the US, mainly driven by Passoã and

-0.9 Damrak Gin as well as by the introduction of Nuvo

0.2

47.8 • Bols Liqueurs continues to gain market share 19.9%

• Lower revenue in Canada more than offset by growth of

Passoã in Puerto Rico

FY Δ Western Δ Asia- Δ North Δ Δ FX FY

2017/18 Europe Pacific America Emerging 2018/19

Markets Emerging

Emerging Markets Markets

• Global brands revenue at constant currencies is slightly up

H1 2018/19* H1 2017/18 Reported Organic

Revenue (* €m)

growth % growth % • Eastern Europe is showing a decline on high comps

• South America is showing growth. The positive impact of the 11.5%

Western Europe 24,8 25,8 -3,7% -3,1%

change in route to market more than compensates the decline

Asia - Pacific 8,0 8,3 -3,7% 2,6%

North America 9,5 8,7 9,6% 11,2%

in Argentina

Emerging Markets 5,5 6,1 -9,5% -7,7%

• The Caribbean is recovering from last year’s hurricane impact

Total 47,8 48,8 -2,0% -0,3%

• Regional Brands impacted by temporary import restrictions in

* Excluding the impact of IFRS 15 and 16 Western Africa

Organic growth: at constant currencies, excluding one-off items

20Gross profit margin influenced by country mix

Gross profit development (in €m)

30.4 Gross margin development at constant

currencies

-0.7

0.4 -0.4

0.0

Total -110 bps

-0.9 Western Europe -80 bps

Asia-Pacific -160 bps

28.9

North America -130 bps

Emerging Markets -140 bps

Group gross profit structure

(H1 2018/19)

11,6%

18,9%

49,9%

FY 2017/18 Δ Western Δ Asia-Pacific Δ North Δ Emerging Δ FX FY 2018/19

Europe America Markets

19,5%

62.2% 58.2% 70.6% 57.4% 61.4% 60.5%

Reported gross margin

Western Europe Asia Pacific

North-America Emerging Markets

21EBIT in line with last year

EBIT development (in €m)

-6.5%

Highlights

-0.2

0.4

13.8 0.0

Organically, EBIT for H1 2018/19 was

up 0.7% to € 12.9 million 30.6%

-0.7

69.4%

FX negatively impacted EBIT by € 0.7

-0.3 million

12.9

In H1 2018/19, Lucas Bols recorded a

one-off € 0.3 million net restructuring

charge at Avandis

FY 2017/18 Δ Global Δ Regional Δ Unallocated Δ FX Δ One-offs FY 2018/19

Brands Brands

28.2% 42.5% 42.5% 26.9%

Reported EBIT margin

22Global brands

Highlights

H1 2018/19* H1 2017/18 Reported Organic At constant currencies the global brands were up 3.0%.

Reported (* €m)

growth growth

The Passoã brand continued its good performance with mid-

Revenue 37,6 37,4 0,7% 3,0% single digit revenue growth.

Cost of sales -13,6 -12,5

GROSS PROFIT 24,0 24,9 -3,5% -0,5%

Gross margin % 63,7% 66,6% 63,8% The white spirits segment showed an overall stable performance,

with the double-digit growth trend for Damrak Gin continuing in

D&A expenses -7,9 -8,5 -7,0% -5,8% both the US and the Netherlands.

% of revenues -21,0% -22,7%

OPERATING PROFIT 16,1 16,4 -1,8% 2,3%

Operating margin % 42,8% 43,9%

Revenue of the Bols Liqueurs range was in line with the year-ago

Share of profit of JVs, net of tax -0,1 0,1 period.

EBIT 16,0 16,4 -2,7% 2,2%

EBIT margin % 42,5% 44,0%

The Italian liqueurs performed slightly below last year as a result

of lower shipments of Galliano that were partially offset by positive

developments for Vaccari in both the Netherlands and Mexico

* Excluding the impact of IFRS 15 and 16 following the restyling of the brand.

Organic growth: at constant currencies, excluding one-off items

EBIT rose 2.2% to € 16.0 million year-on-year at constant

currencies (currencies had a negative impact of € 0.7 million in H1

2018/19) and excluding the one-off restructuring charge at

Avandis (€ 0.1 million allocated to the global brands).

23Regional brands

H1 Highlights

H1 2018/19* Reported Organic

Reported (* €m) 2017/18*

growth growth

The decline of regional brands was mainly related to

Western Africa where the company experienced

Revenue 10,2 11,5 -11,1% -10,5% temporary import restrictions for its brands into Togo

Cost of sales -5,3 -6,0

and Benin.

GROSS PROFIT 4,9 5,5 -10,4% -9,2%

Gross margin % 48,4% 48,0%

Revenue of the domestic genever/vieux portfolio in the

D&A expenses -0,6 -0,9 -26,9% -26,9%

first half of the year was down as a result of the

% of revenues -6,1% -7,4%

declining market.

OPERATING PROFIT 4,3 4,7 -7,3% -5,9%

Operating margin % 42,3% 40,6%

Share of profit of JVs, net of tax 0,0 0,2

Organically, excluding the one-off restructuring charge

EBIT 4,3 4,8 -9,9% -5,0% at Avandis of € 0.2 million in H1 2018/19, EBIT for the

EBIT margin % 42,5% 42,0% regional brands decreased by 5%.

* Excluding the impact of IFRS 15 and 16

Organic growth: at constant currencies, excluding one-off items

24Net profit in line with last year

Highlights

The effective tax rate was approximately 29% for the first half of

2018/19 (H1 2017/18: 27%), higher than the Dutch nominal tax rate as

profits of Passoã are taxed at a higher rate in France.

Given the envisaged reduction in the Dutch corporate tax rate, a

significant one-off gain is expected in the second half of the year,

related to the deferred tax liability.

Earnings per share (pre-IFRS 16) of € 0.64 (post-IFRS 16: € 0.63).

Excluding one-off costs the earnings per share came in at € 0.66.

Interim dividend set at € 0.35 per share in cash, equal to last year.

Number of shares outstanding are 12,477,298.

* Excluding the impact of IFRS 15 and 16

Organic growth: at constant currencies, excluding one-off items

25IFRS 15 and 16 impact

Extract from Interim report for H1 2018/19

IFRS15 & 16 adoption

Amounts in EUR '000 for the six months period ended 30 September 2018 reported 2018 pre-IFRS

impact

Revenue 45.208 2.618 47.826

Cost of sales (18.873) (33) (18.906)

Gross profit 26.335 2.585 28.920

Distribution and administrative expenses (13.331) (2.633) (15.964)

Operating profit 13.004 (48) 12.956

Share of profit of joint ventures, net of tax (81) - (81)

Finance income 46 - 46

Finance costs (1.816) 90 (1.726)

Profit before tax 11.153 42 11.195

Income tax expense (3.262) (10) (3.272)

Profit for the period 7.891 32 7.923

30 September 2018 IFRS16 adoption 30 September 2018

Amounts in EUR '000 as at

reported impact pre-IFRS

Assets

Property, plant and equipment 9.614 (7.084) 2.530

Other non-current assets 314.242 - 314.242

Total non-current assets 323.856 (7.084) 316.772

Total current assets 44.790 - 44.790

Total assets 368.646 (7.084) 361.562

Equity

Total equity 188.108 32 188.140

Liabilities

Loans and borrowings 40.976 - 40.976

Other non-current financial liabilities 75.245 (6.346) 68.899

Employee benefits 293 - 293

Deferred tax liabilities 45.242 10 45.252

Total non-current liabilities 161.756 (6.336) 155.420

Loans and borrowings 4.608 - 4.608

Trade and other payables 12.854 - 12.854

Corporate income tax payable 129 - 129

Other current financial liabilities, including derivatives 1.191 (780) 411

Total current liabilities 18.782 (780) 18.002

Total equity and liabilities 368.646 (7.084) 361.562

26H1 financing update: a new financing structure with ample

covenant headroom and significantly lower rates

Rationale for refinancing Refinancing results

• The current facilities have an aggregate of € 96m of committed • ABN AMRO to join the syndicate as new lender alongside

facilities with a tenor until February 2021, provided by Rabobank encumbered banks (Rabobank and NIBC)

and NIBC

• Annual interest costs assumed to be reduced by around

€ 0.4m

• Existing facilities provide little operational flexibility and no room • Additional liquidity headroom of € 34m

to fund potential add-on acquisitions

• Leverage Ratio covenant improved from 3.0x to 4.0x

• Pay-back of one year with capitalised fees write off of

• Main objectives of the refinancing: € 0.4m

• Achieve lower rates by benefitting from improved credit profile • One-off advisory costs and the accelerated amortization

and favorable loan market environment of the financing costs for the existing facilities will be

• Extend tenor by 5 years charged to the second half of the year

• Maintain sufficient covenant flexibility and liquidity to exercise

Passoã and be able to exercise Nuvo options

• Headroom under facilities to (partially) fund future add-on

acquisitions

• Increase operational flexibility by loosening of loan

documentation (information undertakings, acquisition criteria)

27Balance sheet and cash flow

Actual Actual Actual Actual

Reported (* €m) H1 2018/19* FY 2017/18

FY 2017/18

H1 2017/18

Highlights

Intangible assets 306,9 306,9 306 306,5

Investments in joint ventures 6,8 7,4 7,79 7,4 Net working capital € 19.6 million, traditionally higher in the first

Other 3,1 2,6 0,6 2,5

NON-CURRENT ASSETS 316,8 316,9 317 316,4 half of the year

Cash and cash equivalents 12,2 12,4 12,4 9,0

Net working capital

Other

19,6

0,0

14,4

0,1 0,05

18,4

0,7

Other non-current liabilities include an assumed debt of € 68.7 million

TOTAL 348,6 343,8 359 344,6 related to the call/put option related to Passoã

Funded by equity and liabilities

EQUITY 188,1 183,6 184 176,9

The net debt to EBITDA ratio is 2.9. The net debt to EBITDA ratio

Loans and borrowings 41,0 43,9 43,9 45,3 including assumed debt was 4.3

Deferred tax liabilities 45,2 43,1 43,1 48,4

Other 69,2 68,8 68,5 68,3

NON-CURRENT LIABILITIES 155,4 155,8 156 162,0

Loans and borrowings 4,6 4,0 4,04 5,4 Actual Actual Actual Actual

Derivative financial instruments 0,4 0,4 0,4 0,3 Reported (* €m) H1 2018/19* FY 2017/18 FY 2017/18

H1 2017/18

CURRENT LIABILITIES 5,0 4,4 20 5,7

Deferred tax assets 3,3 5,3 8,03 6,4

0

Deferred tax liabilities -48,6 -48,4 -54,5 -54,8

Total deferred tax -45,2 -43,1 -46,5 -48,4

TOTAL 348,6 343,8 359 344,6

Cash flow development (in €m)

13.0

0.3 -0.8

Cash flow was temporarily impacted by catch up on income tax

-3.8

-8.9% payable in France as well as CAPEX investments in our

6.7

headquarters and € 0.7 million negative currency impact

-3.1 6.1

0.5

Cash flows were used to pay dividends (€ 3.1 million),

and debt reduction (€ 4 million)

Operating Δ Δ CAPEX Δ Working Δ Income Δ Other FOCF H1 FOCF H1

profit H1 Depreciation capital tax 2018/19 2017/18

2018/19

28Important aspects of Lucas Bols’ currency effects

USD exchange rate JPY exchange rate

• 54% of revenue is denominated in foreign

currencies in H1 2018/19 (compared to 49.7% in FY

2017/18 and 50.6% in H1 2017/18 )

• Lucas Bols has a policy of hedging 60 - 80% of its

net cashflows in foreign currencies at the start of

the financial year

• In H1 2018/19, as a result of the stronger euro,

foreign currencies had a negative impact of € 0.9

million on revenue and € 0.7 million on EBIT

AUD exchange rate GBP exchange rate • Taking into account the foreign currency positions

already hedged and assuming the current level of

the euro, all foreign currencies combined are

expected to have a negative impact of around € 1.2

million on EBIT in FY 2018/19 vs. the 2017/18 rates

29FY 2018/19

1. Lucas Bols at a glance

2. Highlights H1 2018/19

3. Operational highlights

4. Financials H1 2018/19

5. Outlook

30Outlook

The underlying dynamics in the global cocktail markets remain healthy.

We expect revenue growth from the global brands to further increase in the second half of the 2018/19 financial

year, mainly driven by the strong growth in the US market.

The performance of the regional brands will remain under pressure in the second half of the year.

Currencies will have a negative impact of around € 1.2 million on full-year 2018/19 EBIT. Furthermore as stated

before, given the initially higher A&P investments and royalty payments, the revenue of Nuvo will translate into a

limited contribution to EBIT.

Taking into account the impact of the aforementioned items and the one-offs, we remain confident in delivering an

overall performance in line with our mid-term strategic ambitions.

31You can also read