CFA Institute Research Challenge Bahrain Polytechnic - CFA Society Bahrain

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge Hosted by CFA Society Bahrain Bahrain Polytechnic

Bahrain Polytechnic Student Research Company: Aluminium Bahrain (Alba) Sector: Manufacturing Sector Recommendation: BUY Exchange: Bahrain Bourse/London Stock Ex. Industry: Aluminium Industry Current Price (16th Jan 2018): BHD 0.620 Ticket Symbol: ALBH Valuation Date: 16th January 2018 Target Price: BHD 1.072 (+72.85%) SUMMARY Company profile Aluminium Bahrain (ALBA), established in 1968, was the first aluminium smelter in the 16th January 2018 Middle East with a total production of 981,016 metric tonnes as of 2017. The company Market Capitalization BHD 877,399,820 engages in manufacturing aluminium and aluminium related products. Market Share Price BHD 0.620 1.200 9 Outstanding Shares 1,415,161,000 52-Week High-Low 0.620 – 0.266 7 1.000 2-Year Average Beta 0.97 Average 3m Volume 223,188 5 0.800 3 Key Financials (Year ended 2017) 0.600 Dividend Yield 6.9% 1 EPS 24 fils 0.400 P/E Ratio 10.16 -1 EV/EBITDA 7.58 0.200 ROA 2% -3 Net Profit Margin 4% 0.000 -5 Debt Ratio 0.42 Jan 17, 2017 May 02, 2017 May 16, 2017 Aug 08, 2017 Apr 05, 2017 Apr 18, 2017 Feb 01, 2017 Feb 14, 2017 Feb 27, 2017 Mar 12, 2017 Mar 23, 2017 Jan 16, 2019 Aug 21, 2017 Sep 11, 2017 Dec 04, 2017 Dec 19, 2017 Jan 07, 2018 Jul 02, 2017 Jul 13, 2017 Jul 26, 2017 Oct 04, 2017 Oct 17, 2017 Oct 30, 2017 Jun 01, 2017 Jun 14, 2017 Valuation Summary Nov 14, 2017 Valuation Approach Weight Price DCF 50% 1.496 Change % Price Multiples 40% 0.668 Ben Graham 10% 0.643 The one year forward blended 50:40:10 target price of BHD 1.072, upside of 72.85% from 12-Month Target Price BHD 1.072 the current market price of 620 fils on 16th January 2018, is based on the following key Target Price Upside 72.85% factors; • Alba will become the largest single-site aluminium smelter in the world following the Source: Team Estimates & Annual Report operation of Line 6 expansion project. This will elevate their status and make them a prominent competitor in the aluminium industry. Alba Historical Stock Price since IPO Source: Bahrain Bourse • With the expectation of approximately 5% YoY growth for the next 5 years in demand 1.000 and decreasing supply by 2.2% of aluminium, Alba will benefit from higher aluminium prices. The forecasted market deficit will be driven by reduction in Chinese production 0.900 of aluminium for environmental purposes. 0.800 • The imposition of trade barriers on China’s aluminium will be giving Alba competitive 0.700 advantage due to FTA agreement with USA. 0.600 • Despite rising price of alumina, green petroleum coke, and carbon, the expected rise 0.500 in aluminium prices will increase Alba’s revenue on a yearly basis. Considering Project 0.400 Titan, costs are expected to remain low. 0.300 • Alba dominates a monopolistic position in Bahrain’s market, being the only producer 0.200 of primary aluminium locally. The high barriers of entry shield them from competition 0.100 locally. Also, 41% of their products are secured by the downstream industries in Bahrain. 0.000 • Alba pays yearly dividends, except for 2018 which will be zero given self-financing of 11/20/2013 07/19/2016 12/01/2010 07/05/2011 02/13/2012 09/10/2012 04/16/2013 06/19/2014 01/29/2015 08/27/2015 03/31/2016 11/14/2016 06/13/2017 Line 6 loan. However, dividends will be distributed thereafter given the rise in production, net income and cashflows due to operation of Line 6.

COMPANY ANALYSIS Table 1 Alba’s Facilities Source: Alba Website BUSINESS DESCRIPTION Facility Type # Facility Details Main Potlines 5 Potline 1-2-3-4-5 Cast Houses Carbon Plants 2 3 971,420 mtpa - COMPANY Fume Treatment 11 - Aluminium Bahrain B.S.C., widely known as Alba, is the effort of the output of the Kingdom Plants of Bahrain’s government to diversify production, reducing the reliance on oil and gas PS 1 (282MW) PS 2 (168MW) activities. Through the continuous advancement in its technological innovation and full Power Plant 4 PS 3 (860MW) involvement in enforcing CSR, training, safety, health and environment guidelines, Alba PS 4 (939MW) Petroleum Coke has managed to be one of the largest aluminium smelters globally (Table 1). Alba was 1 550,000 mt per day Calciner established in 1968 and officially launched its operations in May 1971, becoming the first Seawater Desalination Plant 1 41,000 m3 per day aluminium smelter in the Middle East with a total production of 120,000 tons per annum. 13 hectares 15,000 The company became public on 23 November, 2010 and launched its IPO at BD0.900 per Green Oasis - trees/shrubs ordinary shares and USD11.97 per GDR (1 GDR = 5 ordinary shares) which are traded Fruit/vegetable garden Artificial lake through the Bahrain Bourse and London Stock Exchange under the symbol “ALBH”. 75% of the total trading size were ordinary shares and Global Deposit Receipts (GDRs) through institutional investors, while 25% were ordinary shares available in retail offering. The Figure 1 Sales by product (2016) Company also has a subsidiary incorporated in the United States of America. The market Source: Alba's Website capitalization as of 16th January 2018 is BHD 877,399,820. Today, Alba produces over 14% 971,000 metric tons per annum (mtpa) promising the highest quality of aluminium. As of 2016, Bahrain is ranked as the 9th largest producer of aluminium globally and 2nd largest 30% aluminium smelter in the MENA region1. (Appendix 15) 11% PRODUCT MIX/PRODUCT RANGE Alba not only produces aluminium products, but other by-products as well. Primary 11% products include, standard ingots, rolling slabs, foundry alloy ingots, extrusion billets, t- ingots and liquid metal (Figure 1). Other products include, anodes, power, water, calcined 34% coke. Alba insures 99.86% purity of high-quality aluminium in all products (Appendix 17). The value-added sales accounted for 56% in 2016, a 12.5% drop from last year. Liquid Metal Extrusion Billet Furthermore, Alba imports raw material (alumina) from BHP Billiton, Alcoa and Hydro. Standard Ingots Rolling Slabs Foundry Alloys CONSUMER MIX/ CONSUMER SEGMENT The company’s main consumer sectors include; automotive, consumer products, commercial, residential, transport, and packaging industries. Alba’s main consumer base Figure 2 Sales Revenue by Geographic Location are regional clients and the typical length of the company’s commercial relationships with Source: Alba Annual Report 2016 its top five consumers is more than 28 years (Figure 2). Alba consistently work in collaboration with their customers through technical support services to update their 10% products and boost productivity. COMPANY STRATEGIES 18% 41% Adherence to safety and environment management Alba prioritizes safety in the working environment by conducting regular upgrades to its safety system through the company’s Risk Assessment Committee. Additionally, all 14% employees are trained in health and safety by OHSAS 18001 (Occupational Health and Safety) certified personnel. Alba is recognizable for being the first aluminium smelter in 17% the world to have not a single Lost Time Injury (LTI) in more than 9,200,000 work hours2. Since 1990, the company has invested over USD589million in environmental conservation in the form of fume treatment plants focusing on waste management and reduction of Domestic Asia MENA Europe Americas harmful gas emissions. Investment in training and development Alba has continued to provide training for over 40 years in order to develop the skills of Figure 3 Porter's 5 Forces its employees up to international standards. Alba’s commitment to human asset Appendix 11 development led to opening a Training Centre which consists of workshops and smart Degree of classrooms. The Centre offers training in leadership, automotive, mechanical, electrical, Competition 4 instrumentation and hydraulics and pneumatics. 3 Customer satisfaction Bargaining 2 Threat of Alba commits to maintaining strong relationships with its customers to build long-term Power of 1 New clientele. As a continuous effort to increase efficiency, Alba offers competitively priced Customers Entrants products yet retaining the highest quality of its aluminium with 99.86% metal purity. 0 Technological Development Constant upgrades in the technology used in production is implemented to further Bargaining increase production and improve efficiency. Alba’s recent upgrade from “EGA DX+” to Threat of Power of Suppliers Substitutes “EGA DX+ Ultra” for Line 6 project is expected to increase the company’s production by 540,000 mtpa. This technology improves energy efficiency allowing Alba to increase output by consuming less energy, thus, reducing the company’s production costs.

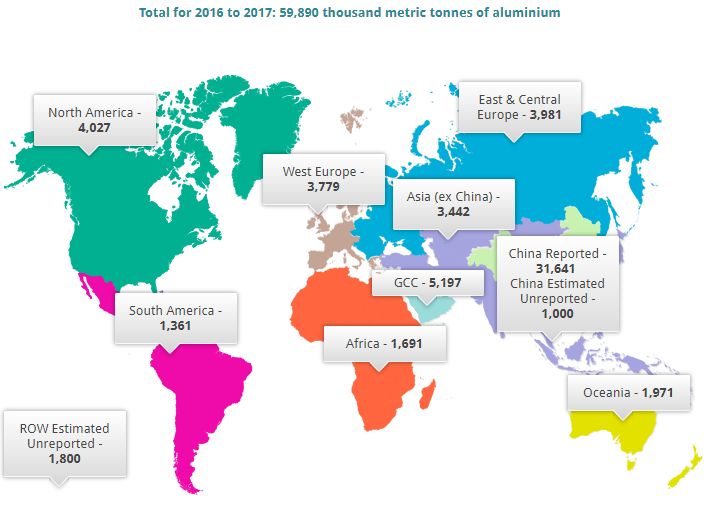

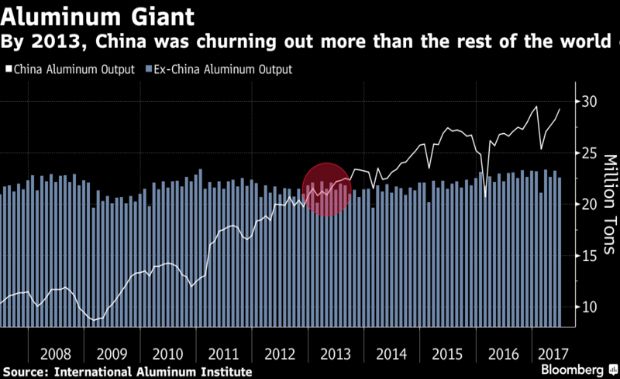

FUTURE DEVELOPMENT Table 2 Executive Managers Alba’s last expansion was completed in 2005 when the company introduced Line 5 to the Source: Alba's Website main site, increasing production by 307,000mtpa (total output=827,000 mtpa). Today, Name Current Position Alba’s line 6 is under development increasing production to 1,540,000mtpa (Appendix 16). Tim Murray Chief Executive Officer Ali Al Baqali Chief Supply Chain Officer Furthermore, Alba initiated plans of expanding its plant and work on developments to Khalid A.Latif Chief Marketing Officer further strengthen its operations within the nation by continuously supporting the non- Amin Sultan Chief Power Officer oil industry and Bahrain’s community to align with the Kingdom’s 2030 Vision. Waleed Tamimi Chief Admin Officer Hassan Noor Acting Chief Operations Officer CORPORATE GOVERNANCE CORPORATE STRUCTURE Figure 4 Alba's Shareholders Holding Board of Directors & Management Team Source: Alba’s Website The company has 10 members in the Board of Directors with diversified backgrounds and experience, 1 out 10 members of the board are non-independent, executives (Appendix 0.74% 6.79% 2.47% 13). Furthermore, the board works alongside with 3 sub-committees: The Board Audit Committee (BAC), the Board Executive Committee (BEC), and the Board Nomination and Remuneration Committee (BRC). The determination of Alba’s business operations 20.60% direction and its long-run strategy is the main responsibility of the BOD. The management team has 55 members inclusive of the 6 executive managers (Table 2 & Appendix 14). The 69.40% primary responsibility of executive managers in Alba is managing the daily operations and enacting strategies and polices set by Board of Directors. They receive compensation in the form of salaries, bonuses, gratuities, perquisites, pensions. Bahrain Mumtalakat Holding Co. BSC Shareholders Saudi Basic Industries Corp Alba’s ownership is majorly held by Mumtalakat Holding Company (a sovereign wealth Norges Bank Investment Management fund owned by Bahraini government) with 69.40% share, 20.60% is owned by Sabic Aluminium Bahrain BSC Public Industrial Investment Company (Saudi chemical manufacturing company), and remaining 10% of ownership is by the public, out of which 0.74% is held by Alba itself (Figure 4). Employees Figure 5 Aluminium Output in China vs. Rest of World Source: International Aluminium Institute The company provides a healthy environment for employees and is the first company in Bahrain to create a Union in 1975. Moreover, Alba has committed to Bahrainisation and is the largest employer in the Kingdom. As of 2017, it has a total of 2,681, of which 84% are Bahraini nationals. CODE OF CONDUCT Alba’s corporate governance structure is completely aligned with The Kingdom’s Commercial Companies Law and Corporate Governance Code issued by Ministry of Industry, Commerce and Tourism. Furthermore, Alba complies with the International Best Practices and Corporate Governance Module issued by The Central Bank of Bahrain. The company’s code of conduct outlines a set of rules that governs five main subjects: Valuing People: fair treatment, respect, non-harassment policies, providing equal opportunity. Safety, Health and Environment: commitment to environment and strict safety rules. Good Citizenship and Social Responsibility: key attributes towards the community and political relations with the government. Ethical Business: eliminate unlawful acts such as corruption, Figure 6 Refined Aluminium Demand and Supply bribery, conflicts of interest and frauds. Information and Confidentiality: protecting confidential Source: Wood Mackenzie, RBC Capital Markets estimates information and methods of representing Alba. 120000 20% SOCIAL RESPONSIBILITY Alba is determined to create a positive impact and improvement on the society and preserving the environment by contributing and initiating in wide array of activities. In 100000 458 15% sports field, Alba is the leading entity in supporting special needs athletes. Furthermore, 1507 716 Alba also participates in Gulf Air Formula One Grand Prix. Alba dedicated a community 80000 1454 services team that supports unprivileged locals financially by raising funds and creating 1719 10% charity events. As for healthier environment, Alba has contributed alongside the 60000 government in restoration of Malkiya beach as well as providing sponsorship for environmental entities and numerous events such as The International Garden show. Alba 5% has spent USD$589 million for environmental conservation. INDUSTRY ANALYSIS 40000 0% 20000 INDUSTRY OVERVIEW • Aluminium consumption increased 5% YoY in 2016; summing up to 59.6 million -376 0 -5% metric tons. Demand forecasted to increase 4-5% for 2018 and 5-6% for the next 5 2009 2010 2011 2012 2013 2014 years, reaching 65.9 million metric ton in 2020. • Rising demand from transportation, electrical and machinery sectors. -20000 -10% • Aluminium supply growth to 2.2% YoY due to Chinese production curtailment. Supply Demand • Increasing trade barriers against China could diminish world production supply. Surplus/Deficit % Change in Supply • China aims to reduce their reported production by 30% to lower pollution levels and aluminium oversupply in the market. % Change in Demand

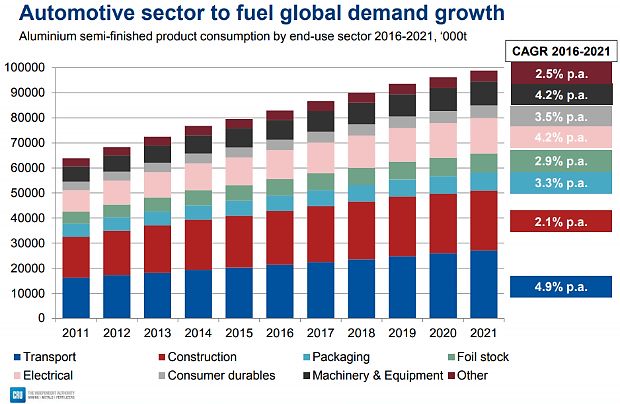

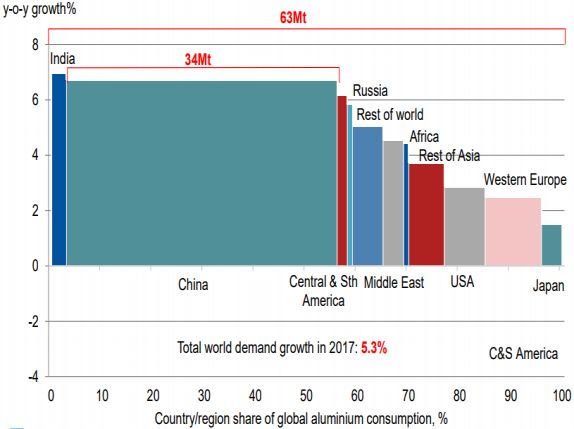

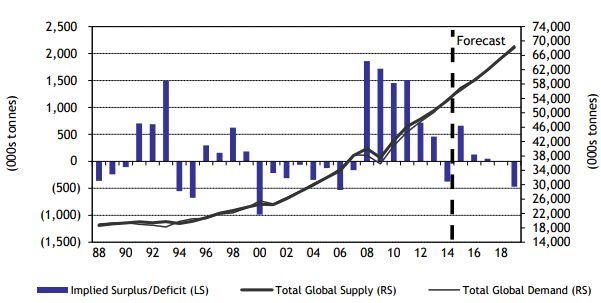

• Increasing raw material costs is pressuring the cost of production but marginal Figure 7 Global Aluminium Supply and Demand revenue exceeds marginal cost. Source: Bloomberg, RBC Capital Markets estimates GLOBAL ALUMINIUM INDUSTRY Direction of Market Balance: Is it a Deficit or Surplus? Alba operates in the aluminium industry that has faced challenging pressures on companies’ profits and valuations. The main reason behind such challenges is China, who started oversupplying aluminium mainly from 2013, more than the world producers, distorting aluminium prices and market balance (Figure 5). It could be observed from Figure 6; aluminium market recorded a surplus throughout the years except for the year 2014 (-376,000 tons) and 2016 (-913,000 tons)3. The year 2016, market deficit exceeded the 2014 deficit, which could be attributed to China’s unexpected trimming of production (Figure 7). A relative balance of 344,000 tons and global deficit of 538,000 tons for 2017 and 2018 is forecasted, a conclusion drawn based on the following: Assumptions: China’s output curtailment reaches 4.5 million tons in 2018. Curbing of China’s output for environmental purposes needs to be 600,000 tons in 2018 Figure 8 Global Primary Demand (YoY Growth % & mt) despite expansionary fiscal policies that will drive growth in short-run. Source: CRU Fall in growth of Chinese consumption by 4.5% in 2018 Rise in China’s net exports to 800,000 tonnes in 2018 from 500,000 tonnes in 2017. Risks: Pump of new projects mainly by China’s State-Owned-enterprises Fluctuations in aluminium prices following response to China supply policy Rise in prices of alumina, carbon and power due to cost-push inflation SUPPLY & DEMAND DRIVERS OF ALUMINIUM Demand Trend In 2016, the consumption summed up to 59.6 million metric tons that is approximately 5% YoY higher4 that than the world’s real GDP growth rate of 3.2% for 2016. The demand rate rises to 5.3% in 2017. China owned global demand share of 14% in 2000; exceeding 50% in 20175. United States, Germany, India and Japan are considered chief consumers of aluminium after China. Demand Outlook Aluminium is the 2nd most consumed metal, headed by steel, due to its intrinsic characteristics such as 100% recyclability, durability, versatility, conductivity, lightweight and strength without comprising safety and performance. Steel is being replaced by Figure 9 Demand of Sectors for Aluminium aluminium as per the EU emissions scheme and the Corporate Average Fuel Economy Source: CRU which supports steel substitution as it is considered more environmentally friendly since it is lighter which enhances fuel efficiency and reduces Co2 discharges (Appendix 17). Aluminium consumption is expected to reach 65.9 million metric ton in 2020 6 while demand is expected to further grow by 5-6% in the next 5-10 years (Figure 8)7. These demand growth rate exceed the world’s forecasted real GDP growth rate of 3.6%, 3.7% and 3.8% in 2017, 2018 and 2022 respectively8. The increase in demand growth is due transportation, electrical and machinery sectors (Figure 9). China is anticipated to adopt expansionary fiscal policies to achieve their target of multiplying their real GDP from 2010- to-2020 as it was expected to ease from 6.3% to 5.7% YoY; thus, driving demand for aluminium in real estate and transportation sector; while US has major infrastructure plans worth USD 1 trillion9. Regions, such as India, that are unable to produce aluminium locally due to high costs, rely on imports providing Alba with exporting opportunities especially since India would require large supply quantities which can be granted by the Line 6 expansion project. The reason being that India is viewed to boost aluminium consumption which increases from 3.3 million mt (2015/16) to 5.5 million from 2020 to 2021 as a result of government initiatives such as “Smart Cities”, “Make in India”, rural electrification, “Housing for All” and freight corridors10. Table 3 Top Aluminium Producers (August 2017 in Supply Trend million mt) The top individual aluminium producer is a Russian Company, UC Rusal, with total output Source: The Balance Producer Country Output amounting to 4,173,000 mt, followed by Alcoa in USA with 3,742,000 mt 11. However, UC Rusal Russia 4.173 China altogether is ranked the highest regional producer with a global aluminium output Alcoa Inc. USA 3.742 Aluminium Corp of China China 3.502 share exceeding 50%. The list of top producers as of August 2017 are listed in Table 312. China Power Investment Corp China 2.693 The 2nd highest regional aluminium producer is the GCC with a total output reaching Rio Tinto Alcan Inc Canada 2.174 5,197,000 mtpa, of which Alba contributes 17.4%; while Alba represents 1.64% of global Norsk Hydro ASA Norway 1.985 China Hongqia Group Ltd China 1.821 supply (Figure 10)13. It is forecasted that the share of aluminium production will decrease Shandong Weiqiao Aluminium China 1.715 and there will be a slowdown in supply growth to 2.2%. This slowdown is mostly due to; & Power Co Shandong Xinfa Aluminium & information collected regarding trade barriers and geopolitical tensions, China revamping Electricity Group Ltd. China 1.630 supply policies and the cost-push inflation in raw materials14. Dubai Aluminium Co. UAE 1.420 Trade barriers and geopolitical tensions The governments in Europe, India and US are enacting protective measures against exports from China by levying import duties or provision of subsidies to producers’

locally 15 . This is due to low-cost input and artificially cheap loans given to Chinese Figure 10 Aluminium Production 2016-2017 producers, hindering the world’s aluminium capacity. India increased import duties for Source: The World Aluminium primary aluminium and aluminium products to 7.5% and 10% respectively 16 . US preliminary duties on all Chinese aluminium foil products are around 96.81% - 162.24%. Alba will have competitive advantage over China given their Free-Trade Agreement (FTA). China’s supply-revamp policies From April 2017 onwards, the shutting-down of unlicensed smelting capacity, could result in loss of 4 million tpa. Secondly, the introduction of environmental tax to reduce pollution will impact production significantly. China plans to reduce their reported production by 30% to lower pollution levels and aluminium oversupply in the market. Thus, reported production dropped by 2.3% within a month17. Cost-push inflation in raw material costs Cost of bauxite, alumina (extracted from bauxite), and anode baking capacities are pressuring raw material costs. China plans on trimming 30% of alumina production and 30% of anode baking and calcining capacities. This will reduce Chinese exports to aluminium smelters and will heighten costs for the whole world, including Middle East. These reforms will increase the aluminum marginal cost of production (exclusive of Figure 11 Alba’s Marginal Profit & Total Cost Estimate overheads, labor and management costs) over the years (Figure 11). Considering the main Source: Team Estimates components of production without the benefit of secured contracts, Alba still produces a positive margin due to rising aluminium prices. 5000 LONDON METAL EXCHANGE (LME): ALUMINIUM PRICES 4000 Aluminium prices dropped from 2013-2016, hitting rock bottom in 2015 with $1423.5 per 3000 1479.6 1466.3 ton. Aluminium became the 2nd best performing base metal in 2017/Q1 compared to 2000 488.4 535.7 being 2nd worst in 2016. If the bullish scenario continues as a result of expected global aluminium deficit in 2018, the LME aluminium prices will be as follows in 2018: 1000 1968 2002 Metal Bulletin Research outlook: Rise to an average of $2,090 to $2,195 per ton. 0 Banks & trading companies’ outlook: Rise to an average of $2,400 and $2,500 per ton. 2017 2021 Other’s outlook: Rise to an average of $2,000 and $2,200 per ton. LME Aluminium Total Cost Margin BAHRAIN MACROECONOMICS The lucrative growth in non-oil sectors, which generates 80.7% of Bahrain’s real GDP, powers Bahrain’s economy against benign international and national economic scene. The non-oil growth slipped down slightly from 5.2% to 4.3% in Q2 and Q1 of 2017 respectively18; this is partially attributed to power outage for 3 hours in Alba, decreasing approximately 3%-5% of the company’s entire aluminium output. Bahrain is expected to experience macroeconomic headwinds, where the foreign-exchange reserves in the Central Bank of Bahrain depleted by 75% since 2014. Without aid or lift in oil prices, Bahrain will struggle to be pegged to US Dollars at BHD 0.376. Hence, Bahrain could be withdrawing subsidies on energy products, increasing Alba’s cost of production. Also, financial aid is expected to be extended to Bahrain as it is viewed less costly compared with BH devaluing the currency that will reverberate regionally. Still, Alba is viewed as solid and financially stable; hence, it receives competitive offers from banks to finance Line 6 that will boost Bahrain economic position. (Appendix 12: PESTL analysis). Thus, its internal strength and Line 6 expansion will shield its stock price from any adverse event. LOCAL ALUMINIUM INDUSTRY The growth drivers of Bahrain’s industrial and logistic sectors are key infrastructure projects worth $33 billion. Among these projects, Alba initiated their Line 6 brownfield project to increase production capacity by 54%. With expectation of additional 250,000 Figure 12 Alba Yearly Production (mtpa) mtpa output sold domestically, local downstream firms plan to take advantage and Source: Alba Website expand their own businesses to accommodate the growing production, creating a wider consumer base for Alba. Furthermore, Alba’s major shareholder, Mumtalakat, entered into joint venture with synergies casting of India in 2015 for building a downstream aluminium plant in Bahrain worth $150 million that will commence operations with output capacity of 25,000 tons in Q4/2017 to absorb Alba’s output when line 6 starts in 2019. COMPETITIVE POSITIONING Monopoly in local aluminium industry & high barriers to entry Alba is the top manufacturer within Bahrain’s aluminium industry due to its monopolized position within the market for aluminium smelting. With the 54% increase in output to 1.5 million mtpa (Figure 12), Alba will have a more competitive edge in the market due to Line 6 expansion. Due to its monopolized market, it is difficult for new entrants to establish a position in the market. Alba has reached high levels of economies of scale due to its increased production and advanced technology levels (EGA DX+ to EGA DX+ Ultra). With the addition of line 6, Alba will be able to lower their costs even more due to operational efficiency and lower energy consumption due to technological advancement.

Table 4 GCC Aluminium Production 2016 (mtpa) Value-added products are key priority Source: Aluminium Insider Alba is among the very few companies who have their own on-site calciner and carbon Emirates Global Aluminium, UAE 2,471,000 plant allowing them to control operations efficiently and maintain optimum production Aluminium Bahrain, Bahrain 971,420 Ma’aden Aluminium, Saudi Arabia 756,800 of value-added products which comprises of more than half the sales. Alba closed 2017 Qatalum, Qatar 643,500 with value-added sales averaging 57% of total shipments against 56% in 2016. Sohar Aluminium, Oman 386,396 Advantage of domestic natural resources & low production costs The initiation of the aluminium industry was due to availability of natural gas – a main component of aluminium production. Alba secured a 10-year gas supply contract in 2015 with NOGA (National Oil and Gas Authority) at a fixed price formula. Also, while electricity is provided at a lower price than the market, Alba generates their own electricity through their production process. With Project Titan and other advantage through the government Figure 13 Alba's Competitive Positioning (5-strong & 0-weak) Source: Team Estimates for land use, construction and utilities, Alba has high competitive advantage. Advanced human capital and government support Monopoly 5 Alba has invested greatly in their human capital through extensive workshops and 4 programs. Alba is the first aluminium smelter in the world to have zero lost time injury Regional 3 Value-added competition 2 products (LTI) in +9,200,000 working hours. Also, since the government owns 50%+ of the company 1 through Mumtalakat Holding Company (sovereign wealth fund), the government is 0 encouraged to continuously support the smooth process of Alba’s operations. Strategic Domestic Strategic location for logistics location natural resources Bahrain has a strategic location, next to Saudi Arabia (largest economy in GCC), connecting via a causeway. Bahrain has easy access to the Gulf and MENA region due to Human capital its prime location. Similarly, Alba has its own port facilities to receive shipment of raw & gov support materials. Furthermore, Alba has a valuable physical position within the industry as the downstream industry is located few minutes away making transportation easy and cheap. Regional competition ranks Alba at 2nd place Top 6 producers of Aluminium in the GCC are listed in Table 4. With UAE’s Emirates Global Aluminium taking first place, Alba is ranked at 2nd. While UAE poses to be competition for Alba, it is asserted that with the start-up of line 6, Alba will improve in its ranking further. GCC accounts for one-tenth of global production; where 60% of production is exported19. This indicates that Alba has access to a wider market, reducing concentration domestically. Table 5 Target Price Source: Team Estimates FINANCIAL ANALYSIS Target Price Weight Weighted Price INVESTMENT SUMMARY DCF We establish a BUY recommendation for Alba at a target price of BHD 1.072 per share, a 1.496 50% 0.748 Valuation 72.85% from the current market price of 620 fils as of 16th January 2018 (Table 5). DCF is Relative 0.649 40% 0.260 given highest weighting as it fully incorporates the impact of line 6 expansion. Relative Valuation Ben valuation has 40% since it highly reflects market perception of the stock using multiples. 0.643 10% 0.064 Ben Graham formula is given 10% as this method yields a value in the upper bound level. Graham 1-Year Forward Target Price BHD 1.072 INVESTMENT ARGUMENT Strong financial position Current Market Price (16th Jan 2018) BHD 0.620 Despite the line 6 loan and interest burden, the ROA (Appendix 5) has continued to rise indicating Target Price Upside 72.85% strong financial health. With the expectation of increased revenues and production, the profit margin increases to 11% by 2021 from 5% in 2016. The current ratio of Alba remains above 1 consistently showing its ability to pay-off any current liability obligations with its current assets. Table 6 Financial Analysis This is further supported by the 96.8% increase in cash and cash equivalent over 5 years from Source: Team Estimates 2016 to 2020, which is attributed to the line 6 production capacity increase. With boost in Financial Analysis (2016) revenue due to higher aluminium prices, effective cost reduction through Project Titan, secured contracts for important raw materials, and upgraded production process will help Alba Piotroski F-Score 5 strengthen their financial position. Beniesh M-Score -3.45 Company Financial Analysis Various analysis tools were employed to access the financial standing of the company Altman Z-Score 3.181 (Table 6 & Appendix 9). Firstly, the Piotroski F-score, which is used to determine the value of stocks through its financial strength, had average scores, representing resilient financial health. Secondly, the Beneish M-Score which is used to identify any manipulations within the financial statements; over the 5-year period, no manipulations were found. Lastly, the Table 7 Project Line 6 Altman Z-score which is used to access the probability of bankruptcy. With being highly- Appendix 16 leveraged for line 6 expansion it is vital to access the likelihood of bankruptcy. However, Line 6 Details with above average scores of 3, bankruptcy is highly unlikely. CAPEX USD$ 3 billion Line 6 Project Syndicated Loan $1.5bn Alba’s Line 6 project is the major driver in their forecasted valuation. With the expansion Project Funding Assuming 2nd loan of $1.2bn Equity financing of $300mn initiative of Line 6 and Power Station 5, it would make Alba the world’s largest single-site Output Adding 540,000 mtpa aluminium smelter as well as provide the largest and most efficient power station. Line 6 Valuation Collectively, it would improve Bahrain’s economic outlook by increasing aluminium Target Price BHD 0.374 per share sector’s GDP contribution from 12% to 15% and generate 500 jobs. Based on DCF Line 6 NPV BHD 530,832,000 valuation, line 6 is estimated to add 374 fils/share to the share price (Table 7).

Project Titan successful implementation Table 8 Valuation Variables (in BHD) Project Titan commenced in February 2014 as a two-year efficiency program to decrease Source: Team Estimates cash cost. Project Titan’s target was to save $150/mt; Alba managed saving $148/mt by Cost of Equity 2015. Followed by Project Titan II, with the aim of saving $100/mt by end-2017, Alba Risk-free rate 5.50% managed saving $78/mt in 2016 and $65/mt in 2017 (actual savings were low in 2017 due to line 5 recovery time). Project Titan will help Alba maintain sustainable growth, boosting Alba's Adjusted Beta 0.94 the economies of scale benefit while lowering its costs. We assume the continuation of Market Return 10.68% this program to reduce costs every year to maintain optimal efficiency and competitive Cost of Equity 10.37% advantage especially with rising raw material prices. Positive LME Aluminium Price Outlook Cost of Debt The average LME prices are listed in Table 8. After falling prices between 2015-16, LME 4.25% aluminium prices is seen to rise by 20% in 2017 at $1,929 from $1,604 in 2016. The WACC forecasted market deficit and higher LME prices in 2018 will support Alba’s growth in sales 8.96% volume and revenue. In 2019, Alba’s rise in production from Line 6 project will lead to higher revenue and income. The upward trend will continue in 2020-21. Demand by transportation, electrical/machinery and construction sectors for aluminium is expected Relative Valuation to increase at 4.9%, 4.2% and 2.1% CAGR respectively. Correspondingly, LME aluminium Alba EPS 0.024 U.S. premium that stood at $180/mt on January 2017, was $200/mt by year-end-2017. This is expected to reach $250/mt with changing industry dynamics. Industry P/E 17.79 Target Price 0.427 VALUATION Alba EBITDA 157,871,000 DISCOUNTED CASH FLOW VALUATION (DCF) Based on DCF, the 1-year forward target price achieved was of BHD 1.496, which is 141% Industry EV/EBITDA 9.71 above current market price of 0.620 fils (Appendix 6). Alba Enterprise Value 1,509,246,760 Free Cash Flows to Firm (FCFF) Less: Debt Value 749,498,000 To determine the fair equity value of Alba, the formula for Free-Cash-Flow-to-Firm (FCFF) Add: Cash 371,806,000 was used (Cash flow from Operating Activities – Capital Expenditure – Changes in Net Working Capital). FCFF was selected because Alba uses a combination of equity and debt Equity Value 1,131,554,760 to finance their expansion plans and debt plays a major role in the company’s financials Outstanding Shares 1,420,000,000 and the cashflow reflects all the major changes undergoing Alba. Target Price 0.797 Weighted Average Cost of Capital (WACC) WACC was used to determine the cost of capital at which to discount the FCFF. For the W of EPS 40% component of cost of equity, Capital Asset Pricing Model (CAPM) was used with the risk- W of EV/EBITDA 60% free rate of Bahraini Government 10-year Bond. The risk adjusted beta was derived by Blended Target Price 0.649 calculating it over a 2-year weekly average by comparing Alba’s stock prices to Bahrain All Share Index. The market return was calculated over a 5-year period by averaging the daily returns and compounding it annually. For the cost of debt, LIBOR rate of 3.25%+1% Table 9 Aluminium Price Sensitivity Analysis ($/mt) was used due to the syndicated loan secured for line 6 expansion project. Weightings Source: World Bank & Team Estimates were derived using historical 5-year average of debt-to-equity ratio (Appendix 6.2). Year 2017 2018 2019 2020 2021 Terminal Growth Value Worst 1873 1890 1908 1926 1944 Alba contributes 12% to the GDP as of 2016 and is expected to increase to 15% after line Base 1911 1929 1947 1965 1984 6. This indicates Alba’s important contribution to the GDP; thus, it is used as a mechanism Best 1950 1968 1987 2005 2024 Aluminium to determine the terminal growth rate for the terminal value. Conducting a sensitivity Price 1929 1946 1965 1983 2002 analysis available in Appendix 6.3, the growth rate was 2.25%. RELATIVE VALUATION Figure 14 Forecasted Revenue (BHD'000) and Aluminium prices (USD$/mt) To determine the financial worth of Alba, it is compared to 7 other similar companies in Source: Team Estimates the industry who are Alba’s competitors (Appendix 7). Using earnings multiples of P/E and 1,600,000 2020 EV/EBITDA, we derived a blended target price (40:60) of 649 fils. These multiples were 1,480,322 specifically selected since P/E ratio is a highly common ratio used to measure performance 1,400,000 2000 against competitors and EBITDA excludes non-cash items giving a more approximate 1,263,190 2002 value. The median value was used as it is a better measure of central tendency since it 1,200,000 1,077,907 1980 eliminates the outliers distorting the result. 1983 BEN GRAHAM VALUATION 1,000,000 919,801 1960 With use of a formula created by Benjamin Graham, we were able to calculate the intrinsic 784,886 800,000 1965 value of Alba at 643 fils which is our target price for 1-year forward. Appendix 8 outlines 1940 the variables used to calculate the target price. It is understood that Alba’s share price is 600,000 1946 undervalued in the market; while its fair value is 3.71% above market price. 400,000 1929 1920 ANALYSIS REVENUE & PRODUCTION CAPACITY 1900 200,000 Alba is expected to recover from falling revenues (13% decrease) caused by downward trend in LME aluminium prices, $1,665 and $1,604 in 2015 and 2016 respectively, despite 0 1880 increasing production. The forecasted revenue is based on production levels and LME 2017 2018 2019 2020 2021 aluminium forecast prices. The production is expected to increase by 4%-5% based on Sales Revenue Aluminium Price

Figure 15 US$ Nominal Annual Average Price of Raw aluminium demand growth, more prominently from American and Asian regions. Materials Source: Consensus Economic Inc & World Bank Additionally, the continuous increase in LME aluminium prices also contributes to the rise 305 302 70 in Alba’s revenues with the forecasted LME prices between 2017-2021 to be at $1,929 in 60 60.9 2017; reaching $2,002 in 2021. This is due to the expected reforms in reducing China’s 59 300 56 60 production; thus, decreasing global aluminium supply. Collectively, Alba’s revenue is 53 expected to exceed BHD1 billion as Line 6 commences in 2019, a 37% increase from 2017 295 (Figure 14). 50 290 289.4 COST OF SALES Currently, Alba is under a long-term contract with Alcoa for raw material supply (alumina) 40 285 286.7 as a legal settlement since 2012. However, terms of the contract have not been disclosed; 280 thus, we assume continuation of contract for raw materials supply. Furthermore, with the 30 280.8 secured contract for gas prices with NOGA until April 2021, gas prices will become a major 275 concern by then as it can cause a $31 million fall in net income. However, it is highly 275 20 believed another contract for gas prices will be secured by then to prevent Alba from 270 incurring a loss considering the majority of the company is owned by the government. 13.7 13.7 14.5 14.5 15.3 10 Additionally, the government would take necessary measures to strengthen Alba since it 265 is one of the major contributor to Bahrain's GDP (12%) and would serve in the best interest 260 0 of the country. Crude oil price ($/mmbtu), which produces green coke, is expected to 2017 2018 2019 2020 2021 minimally increase over the next 5 years. Moreover, carbon, which is used to produce Alumina Carbon Crude Oil carbon anodes for aluminium production is forecasted to increase 5.5% (5-year-CAGR). With the assumption of further implementation of Project Titan every year to successfully reduce costs, cost of sales consistently reduces except for the last 2 years where the increasing prices of alumina (Figure 15) and gas price to more than USD$4/mmbtu Figure 16 Dividend per share and Pay-out ratio (increasing by USD$0.25/mmbtu yearly) after April 2021 will apply pressure on costs. Thus, Source: Team Estimates Alba has a competitive advantage in more than half the components of production. 100% 0.040 DIVIDENDS The dividend per share was calculated on the basis of compounded annual growth rate 90% 0.035 (CAGR) of -4.68%. Alba makes yearly payment of dividends but the dividend payout ratio 80% and dividend per share are moving in a downward trend (Figure 16). Alba is expected to 0.030 70% distribute dividends in 2017 with a pay-out ratio of 80.99% compared to 16.03% in 2016; 0.025 this is due to pick up in LME prices. Despite improved aluminium prices in the future, 60% Alba’s 10% self-financing plan for line 6 (USD$300 million) and higher capex (45% of line 50% 0.020 6 cost) will result in no dividend paid for 2018. The ratio will increase in 2019 to be 40.82% due to an expected higher income following the operation of Line 6 and lower capex 40% 0.015 (25%). The pay-out ratio will decrease YoY in 2020 and 2021 to be 25.59% and 16.92% as 30% Alba will still be constrained by its Line 6 debt repayment and finance cost obligations. 0.010 20% CASH FLOW GENERATION 0.005 Alba is expected to yield favorable liquidity measurements, with current ratio exceeding 10% 1.5, indicating the ability to settle current debt obligations using current assets, especially 0% 0.000 in 2017 recording the highest ratio (3.83) due to increase in cash (Figure 17). However, 2013 2012 2014 2015 2016 2017 2018 2019 2020 2021 2019 poses to be a difficult year for Alba considering its increased debt obligations and capex. With signs of recovery up till 2021, the company has a resistant liquidity standing Dividend Payout Dividend per share and has an upward trend overall. The cash ratio in 2017 will be the highest (2.06) given procurement of line 6 loan, and Project Titan-Phase II that will decrease cash-cost by US$ 100 per metric ton. Considering 2020 & 2021, the cash ratio will be low yet improved on Figure 17 Coverage Ratio a YoY basis (0.10 and 0.45) due to benefits of Line 6 expansion. Source: Team Estimates CREDIT PROFILE Syndicated term-loan from both conventional and Shari’aa compliant facilities was 27.03 acquired successfully mid-2017 worth $1.5billion (Appendix 16 for further loan details). Interest Margin is 325 basis point per annum over LIBOR for 7-year period, with a grace 22.97 period of 3 years for line 6 construction. The coverage ratio which indicates Alba’s ability 22.26 to pay-off its financial obligations, a ratio of over 3 depicts strong financial health. As seen 16.95 in figure 18, through the years, the ratio remains above 3 with a gradual increase as the burden of capex eases. 17.99 12.33 DUPONT ANALYSIS Return on Equity (ROE) is used as a measurement of Alba’s performance over the years. 7.81 Considering the 3 factors of ROE (Figure 19), historically, Alba’s ROE is decreasing over the years persistently with the most prominent between 2015-16 due to increasing 5.15 financial leverage and falling net profit margin. However, the ROE is expected to follow an 3.43 3.97 upward trend from 2018 onwards as profits from increased sales will increase the profit margin (as a result of rising production and increase in LME prices), efficient asset turnover and the major influx of cashflows increasing the equity multiplier reflecting the significant contribution of the Line 6 project. Therefore, Alba is expected to achieve an ROE of 13% 2013 2012 2014 2015 2016 2017 2018 2019 2020 2021 in 2021, the highest peak in past 5 years.

KEY RISKS MARKET RISK LME Aluminium Prices (R1) Figure 18 Cash Ratio Alba’s commodity prices are exposed to changes in LME prices (quoted from the London Source: Team Estimates Metal Exchange) which are used as a basis to determine aluminium prices. Any negative movements in LME prices would risk the profitability of the firm. However, as seen in figure 2.06 20, in the case where LME aluminium prices are to drop by 20%, the impact on the 1-year forward target price is still a 52.9% upside from the current market price of 620 fils as of 16th January 2018. To manage this risk, futures commodity prices are considered to hedge selling price as per customers’ options. This approach can prove to be profitable if a proper strategy is adopted. However, Alba has been able to perform excellently despite 1.17 low aluminium periods over the last few years indicating towards Alba’s resilience during industry downturn. 0.58 Gas Prices (R2) 0.38 0.45 Generally, electricity accounts for 70% in cost variability of aluminium production and 0.29 since 2015, the rising gas prices from $2.25 per million British thermal units (MMBTU) can 0.21 0.10 be a disadvantage for Alba. The yearly increase of $0.25 in price could cost Alba 0.37 -0.14 approximately $31 million. Alba consumes 3,574MW in energy for production while the rest of Bahrain consumes 3,817MW. This depicts the high level of energy consumption 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 and dependency on gas for production. On April 2017, when Alba faced a power outage for 3 hours, they lost 3-5% of production. Following high dependence on gas, Alba secured a fixed gas price formula, effective till 1st April 2021. Furthermore, to offset fluctuating aluminium price risks, Project Titan, an in-house initiative, was introduced to reduce cash cost per unit. Currently, Alba aims to save $100 per unit on a production Figure 19 Return on Equity 1,000,000 mtpa for 2017. We assume the continuation of this project as it helps Alba Source: Team Estimates maintain its competitive advantage in the market. FINANCIAL RISK 250% 14% Interest rate risk (R3) 13% The company is exposed to interest rate risk which would affect its holding assets and 12% 200% 12% liabilities interest. Currently, the USD$1.5 billion syndicated loan for Line 6 is based upon 11% LIBOR + 3.25%. Therefore, Alba is subjected to high market risk since LIBOR experiences 10% 10% daily movements thus it will have a high impact on the profitability and cashflows of Alba. 9% 150% Foreign exchange risk (R4) 8% The operating activities is the main segment exposed to changes in foreign exchange 7% rates. The majority of Alba’s financial instruments are denominated in Bahraini Dinars, US 6% 100% 6% Dollars, Euros, Swiss Francs and Great Britain Pounds. In the past, the company entered 5% into forward foreign exchange contracts to hedge against forward foreign exchange 4% 4% contracts. Alba is not considered to have a significant exposure to US Dollar fluctuations 3% 50% as the Bahraini Dinar is pegged to the US Dollar at BHD 0.376. With this, the impact and 2% probability are relatively moderate. Credit risk (R5) 0% 0% Credit risk is applicable to Alba’s operating activities (primarily on trade receivables, financing activities including bank and financial institutions deposits), foreign exchange 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 transactions and derivatives instruments. A method in which the company reduces credit Net Profit Margin Asset Turnover Ratio risk is to deal with its investments dealt with reputable banks and assign credit limits to Equity Multiplier Return on Equity each counterparty. For trade and other receivables, 52% of its outstanding trade receivables consist of the company’s five largest customers account. In order to manage the credit risk, Alba prefers receiving advanced payments from customers, assess creditworthiness by obtaining letters of credit and other forms of credit insurance and Figure 20 Change in LME Aluminium Price impact on Alba's 1- track the customer exposure on a regular basis. When risks of default are identified, year forward target price provision for doubtful receivables are created. With the assumption of no derivative Source: Team Estimates contracts in the future, Alba is not subjected to credit risk for derivatives specifically. Liquidity risk (R6) 1.210 1.105 1.139 The company may be exposed to this risk when it is unable to sell its financial asset close 1.008 1.039 to or equal to its fair value. This risk can be decreased by ensuring the availability of 0.948 banking facilities. Additionally, Alba includes a sales term where it requires a payment to be made within 30 to 180 days of the date of sale. However, with a negative cashflow for 2019, liquidity risk remains high for the year. In the long-run this outlook is expected to change as Alba repays the line 6 loans and operates and maximum capacity to generate greater profits and cash flow in the future. -20% -10% -5% 5% 10% 20%

Figure 21 Bahrain Real GDP Growth Rate Source: World Bank OPERATIONAL RISK Raw Materials Risk (R7) 8.30% Alba is dependent on its suppliers for raw material supply. Any disruptions in the supply chain could lead to major drawback in the production process. Alba is currently under contract with Alcoa for raw material supply, and the government for gas supply. In the 6.20% 5.30% case these contracts no longer exist or are not renewed, Alba will be subject to major 4.30% fluctuations in market price of raw materials as alumina is expected to become expensive. 4.40% As contingency, Alba is assessing options to satisfy the demand for alumina which will rise 3.60% to 2.5M metric tons/year once Line 6 begins. Alba’s CEO also announced the consideration 2.90% of joint ventures with large alumina suppliers or off-take contracts with their refineries. 3% Operational Cost Risk (R8) 2.50% 2.10% By means of Project Titan II, Alba has been able to successfully reduce operational costs over the last 3 years which given them a competitive advantage in the market by selling at low prices. In addition, Alba close 2016 without any lost time injury. Constant initiative 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 by the CEO has increasing operational efficiency significantly. Strategic risk (R9) Figure 22 Risk Grid Alba manages its strategic risks by adjusting its capital structure and taking appropriate Source: Team Estimates actions in response to economic changes. This can be done by adjusting dividend payment to shareholders, return capital and issue new shares. The main objective of capital management is to sustain a healthy and sufficient capital base able to support its operations and maximize shareholders’ value. Since Alba is constantly on top of such factors to ensure smooth flow of operations, the risk is minimal. Historically, Alba has had many successful strategies (Project Titan I & II). ECONOMIC RISK Bahrain Macroeconomic Status Quo (R10) The economic slowdown of Bahrain since the financial crisis 2007/8, Arab Spring 2011 and declining oil prices has been gradually recovering (Figure 21). The non-oil sector (of which Alba is a part of) has remained resilient despite fiscal reforms such as VAT (5%) and subsidy removal. The introduction of 5% Value Added Tax on all sales by Q3 in 2018 might affect Alba's semi-final aluminium production indirectly, as there is the likelihood of VAT being applied to the downstream industry products. This will eventually affect Alba’s revenue as 41% is derived locally. Sovereign Credit Downgrade (R11) Bahrain’s credit rating is at a risk of another downgrade from B+. It was recently downgraded from BB- to B+ by S&P due to lack of fiscal reform plans and budgeting reports. However, with current reforms under process, the risk of downgrade is moderate since Alba already secured the syndicated loan for line 6 expansion. STOCK ANALYSIS 2015 Q3 - NOGA announced a 25% increase to oil and gas prices. This took an effect on April 1st. Increase in oil and natural gas prices caused a panic among public shareholder within the Bahraini Index. ALBH started dropping starting Q3. 2016 Q2 - ALBH reached its lowest point due to LME price decline, owing to the major increase in supply. The oversupply affected the global markets negatively. China started supplying the market with aluminum at lower price than the current market. 2017 Q1 - ALBH started to recover from the LME prices decline after adjusting to market fluctuations. LME started to resume its normal prices after China’s proposed 30% cut of production capacity. 2018 Q1 - Line 6 is one of the major drivers of share price increase; as the project nears its completion date, the future prospect for Alba is moving in a positive direction. Additionally, China production curtailment and expectation of higher LME prices has led to the increase. BHD 0.700 25000000 BHD 0.600 20000000 BHD 0.500 15000000 BHD 0.400 10000000 BHD 0.300 BHD 0.200 5000000 BHD 0.100 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 2014 2015 2016 2017 2018 Figure 23 Stock Valuation Volume Average Price

APPENDICES APPENDIX 1: CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F BD '000 BD '000 BD '000 BD '000 BD '000 BD '000 BD '000 BD '000 BD '000 BD '000 Sales 743,725 749,338 821,715 766,686 669,760 784,886 919,801 1,077,907 1,263,190 1,480,322 Cost of sales -638,515 -640,751 -673,947 -663,428 -587,381 -671,253 -777,438 -900,294 -1,042,415 -1,206,793 GROSS PROFIT 105,210 108,587 147,768 103,258 82,379 113,633 142,363 177,614 220,776 273,528 Other income 39,378 7,304 1,865 3,701 2,989 1,750 1,772 2,695 2,817 2,946 (Loss) gain on foreign exchange translation -17,838 211 671 728 -19 - - - - - Administrative expenses -27,347 -30,609 -29,546 -32,417 -22,548 -28,263 -33,121 -38,815 -45,487 -53,305 Selling and distribution expenses -1,346 -17,574 -19,885 -12,187 -11,259 -12,254 -14,360 -16,828 -19,721 -23,111 Finance costs -7,182 -5,823 -4,449 -3,176 -2,504 -40,391 -61,200 -52,548 -43,936 -35,157 Directors’ fees -190 -190 -190 -210 -210 -210 -210 -210 -210 -210 Net revaluation/settlement of derivatives 5,860 17,871 211 264 - - - - - - PROFIT FOR THE YEAR BEFORE TAX 96,545 79,777 96,445 59,961 48,828 34,265 35,244 71,907 114,240 164,691 Tax expense - - - - -438 - - - - - PROFIT FOR THE YEAR 96,545 79,777 96,445 59,961 48,390 34,265 35,244 71,907 114,240 164,691 ASSUMPTIONS: Sales Revenue: expected to increase with the boost in production due to line 6. Increasing worldwide demand for aluminium is another reason for the increase. 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Yearly Production 890,217 912,700 931,427 960,643 971,420 981,016 1,019,668 1,540,000 1,609,993 1,698,543 LME Aluminium Price: Based on World Bank forecasts, the team conducted a sensitivity analysis to produce realistic figures of the forecasted aluminium prices. 2017 2018 2019 2020 2021 Probability The rising LME prices will encourage Chinese producers to increase aluminium output, posing downside risk on LME prices. Still, the LME prices will rise due to weakening US dollar against other basket of World Bank Forecasts 1950 1968 1987 2005 2024 currencies, despite Federal Reserve interest rate hawkish hike from 1% to 1.25% this year (2017). Worst-case 1873 1890 1908 1926 1944 0.15 Moreover, the local premiums react to US Midwest premiums; and there is an impression that the US Base 1911 1929 1947 1965 1984 0.25 Midwest premium is increasing for P1020 aluminium, given the need for aluminium imports into US. Increase in freight rates will add to the premium prices; premiums will cushion aluminium smelters to Best-case 1950 1968 1987 2005 2024 0.60 some extent from fall in price. Furthermore, rising raw material costs will further drive the prices upwards. Incorporating all these factors, with the optimistic outlook in the aluminium market, the best- Team Estimates (in $/mt) 1929 1946 1965 1983 2002 case scenario has a higher probability of occurrence than the base and worse. Cost of Sales: With successful implementation of Project Titan Phase I & II, COS expected to decrease despite increase in Alumina prices due to Alba-Alcoa long-term contract Expenses: As the size of Alba increases with its production, its expenses are expected to increase as well as it caters to more orders around the globe. Finance Cost: With the line 6 loan of USD$1.5 billion and USD$1.2 billion at 3.25% LIBOR rate, the interest rate is calculated accordingly.

APPENDIX 2: CONSOLIDATED STATEMENT OF FINANCIAL POSITION (in BHD ‘000) 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F Assets Non-current assets Property, plant and equipment 901,779 868,318 837,757 811,377 847,500 1,102,685 1,513,794 1,679,390 1,582,116 1,482,947 Long term receivable 10,314 6,877 3,439 - - - - - - - Other asset - - 4,704 4,512 4,320 - - - - - Deferred tax asset - - - - 10 - - - - - 912,093 875,195 845,900 815,889 851,830 1,102,685 1,513,794 1,679,390 1,582,116 1,482,947 Current assets Inventories 143,564 144,930 152,469 146,404 163,422 157,823 164,042 247,751 259,012 273,257 Current of long terms receivables 3,438 3,438 3,438 - - - - - - - Long term receivable - - - 3,439 - 60,763 1,743 Trade and other receivables 108,299 85,375 92,888 100,698 92,065 100,684 117,991 138,273 162,041 189,894 Other assets - 4,800 - - - - - - - - Derivatives financial instrument 104 - - - - - - - - - Bank balances and cash 61,605 64,540 67,198 116,009 66,413 371,806 294,027 -30,814 24,500 130,726 317,010 303,083 315,993 366,550 321,900 691,077 576,059 356,953 445,552 593,877 TOTAL ASSETS 1,229,103 1,178,278 1,161,893 1,182,439 1,173,730 1,793,762 2,089,853 2,036,343 2,027,668 2,076,825 Equity and Liabilities Equity Share capital 142,000 142,000 142,000 142,000 142,000 142,000 142,000 142,000 142,000 142,000 Treasury shares -4,087 -5,157 -3,696 -4,905 -4,965 -4,965 -4,965 -4,965 -4,965 -4,965 Statutory reserve 71,000 71,000 71,000 71,000 71,000 71,000 71,000 71,000 71,000 71,000 Capital reserve 249 249 249 249 249 249 249 249 249 249 Retained earnings 600,683 629,381 687,387 731,698 779,813 806,322 755,508 827,415 910,982 1,046,437 Proposed dividend 19,773 30,978 21,200 7,768 - 29,658 - 30,673 29,237 27,868 TOTAL EQUITY 829,618 868,451 918,140 947,810 988,097 1,044,264 963,792 1,066,372 1,148,503 1,282,589 Non-current liabilities Borrowings 77,096 84,402 64,137 33,024 6,489 567,578 872,133 750,495 627,283 502,291 Employees’ end of service benefits 915 930 1,265 1,349 1,554 1,678 1,916 2,056 2,275 2,418 Derivatives financial instruments 23,996 5,313 - - - - - - - - 102,007 90,645 65,402 34,373 8,043 569,256 874,048 752,550 629,558 504,709 Current liabilities Borrowings 160,303 116,432 72,351 56,373 45,235 34,286 23,654 16,976 12,562 9,507 Trade and other payables 106,585 97,960 101,378 143,844 132,355 145,955 171,044 200,445 234,899 275,277 Derivative financial instruments 13,430 4,790 4,622 39 - - - - - - Short term loans 17,160 - - - - - 57,315 - 2,145 4,744 297,478 219,182 178,351 200,256 177,590 180,242 252,013 217,421 249,607 289,527 TOTAL LIABILITIES 399,485 309,827 243,753 234,629 185,633 749,498 1,126,061 969,971 879,165 794,236 TOTAL EQUITY AND LIABILITIES 1,229,103 1,178,278 1,161,893 1,182,439 1,173,730 1,793,762 2,089,853 2,036,343 2,027,668 2,076,825

You can also read