CFA Institute Research Challenge - Hosted by - Asia-Pacific Research ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge Hosted by CFA Society Sydney Abercrombie & Co The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was submitted by a team of university students as part of this annual educational initiative and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report holds a financial interest in the securities of this company. The author(s), or a member of their household, of this report knows of the existence of any conflicts of interest that might bias the content or publication of this report. The conflict of interest is that one of the authors, or a member of their household, of this report holds stock in the company. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with CFA Society Sydney, CFA Institute, or the CFA Institute Research Challenge with regard to this company’s stock.

Abercrombie & Company Abercrombie Has the Golden Child Telecommunications Operators Australia | Australian Securities Exchange (ASX) & Company Lost Its Shine? Company: Telstra (“TLS”) Date: 19-Sep-2018 Closing Price: AU$3.21 Sell (-20.2% Total Return) Ticker: TLS-ASX Target Price: $2.67 Executive Summary TLS-AU Overview We initiate coverage on Telstra (TLS-ASX) with a SELL recommendation based on a 12-month price Target Price [A$] 2.67 target of $2.67, representing a -20.2% downside from the last close of $3.21 on 18 September 2018. Last Closing Telstra’s (TLS-ASX) substantial competitive moat as the nation’s wholesaler has been eroded via the [A$] 3.21 introduction of the National Broadband Network (NBN). The reduction in barriers to resell broadband 18/09/18 opened the competitive landscape for nimbler players to enter and grow market share. TLS is hanging Market Cap [A$m] 38,140 its hat on its ability to generate long-term value from the 5G rollout and recoup losses incurred due to Shares Out m 11,878.9 fierce competition in the mobile and NBN space. But this bet is not likely to yield sizeable returns amidst a hypercompetitive environment. Without this growth potential, other strategies like Telstra2022 cost cuts 52 Wk High [A$] 3.79 to improve margins will not sufficiently compensate for low mobile and NBN returns to drive up EPS. 52 Wk Low [A$] 2.60 1. Rising Mobile Competition | Prepare for the Game of Phones Table 1: Price History (Rebased) With 44% of TLS’s revenue derived from its mobile segment and the less attractive economic profile of ASX200 - Rebased TLS NBN, increased reliance is placed on their ability to capture market share in the mobile space. i) Tightening Competitive Landscape: The market believes the proposed merger of TPG (TPM) $8 and Vodafone (VHA) will lessen competition and concentrate the industry. Our analysis suggests that the merged entity will have the bundling benefits and intent to be a stronger challenger to TLS and will be able to compete for more than their 20% mobile market share. $6 The resulting competitive pricing in the mobile space could erode Average Revenue Per User (ARPU) and increase subscriber churn for the incumbent, triggering an earnings downgrade. $4 ii) Customer Flight: Reduced customer satisfaction from recent network outages has left TLS near all-time low Net Promoter Scores (NPS). This lays the foundation for customer flight in the run up to the NBN’s churn event, which could see TLS struggle to retain mobile market share. $2 2. All in on 5G | Hold the Door for Rivals to Enter 5G 2013 2014 2015 2016 2017 2018 Source: Abercrombie & Co Analysis Historically, the rollout of new mobile networks (e.g. 3G and 4G) marked TLS’s opportunity to boost mobile margins by commanding increased ARPUs as the first-mover of the superior network. This Graph 2: Returns Analysis expectation will not be met for the upcoming 5G rollout in a hyper competitive market as the telcos, Optus 8% and a potential TPM-VHA, will be as ready as TLS for 5G. WACC: 6.6% iii) Optus and TPM ready to go: TLS’s historically high mobile ARPU will subdue to 1% growth at 6% the commercial launch of 5G. Optus is committed to launch alongside TLS with sufficient spectrum and 5G trials, and the TPM-VHA merger could guarantee maximum spectrum since 4% without the merger, the individual entities were limited by their debt capacities. iv) Differentiation is King: The upcoming 5G release and NBN migration underscores a major 2% churn event. We believe TLS will lose 4% market share, as they struggle against Optus’ product differentiation (content-driven strategy) and TPM-VHA’s cost differentiation (product bundling). 0% 16 17 18 19 20 21 22 23 3. Commoditised NBN | Winter is Still Coming ROIC ROE The NBN rollout has triggered the migration of TLS copper customers to the new network. However, we Source: Abercrombie & Co Analysis expect more earnings pressure as competitors improve the quality of connections. Combating these rivals may compromise cost cuts that TLS relies upon to stave off a significant dividend reduction. TLS-AU Key Financial Data FY18 i) Incumbent’s Curse: Despite competition pushing down ARPU, TLS has always at least D/E 46.8% maintained their network quality advantage. New changes to the Connectivity Virtual Circuit (CVC) cost that telcos must pay to support bandwidth speeds will finally catalyse unprecedented Net Debt/Equity 1.6x quality convergence between competitors. The $2.5bn cost savings program is also unlikely to Dividend Yield 7.1% yield EBITDA relief amidst an unreliable record and accelerating cost of sales. ii) Indebted to the Dividend: TLS has always been viewed as a high dividend yield firm for an EV/EBITDA1 5.4x enormous retail investor base. But earnings headwinds from NBN, mobile and capex needs P/E(LTM) 10.6x mean a major dividend cut is imminent to retain an A credit rating. (1) EV/EBITDA (exc. NBN one-offs 6.3x) Financial Analysis FY18A FY19E FY20 2021 2022 2023 CAGR Revenue [A$m] 26,904.0 25,462.3 25,237.1 25,457.3 26,242.2 27,217.9 0.2% EBITDA [A$m] 9,656.0 9,372.1 9,264.0 9,319.4 9,580.5 9,909.5 0.4% EBITDA Margin [%] 0.4 36.8% 36.7% 36.6% 36.5% 36.4% 0.2% EBITDA Growth [%] (6.8)% (2.9)% (1.2)% 0.6% 2.8% 3.4% NPAT [A$m] 3,008.0 2,548.7 2,427.6 2,394.2 2,278.6 2,392.2 -3.7% NPAT Growth [%] (5.5)% (15.3)% (4.8)% (1.4)% (4.8)% 5.0% Postpaid Mobile ARPU [A$m] 58.05 55.73 54.62 53.53 53.53 53.53 -1.3% Postpaid Mobile ARPU [%] (4.4)% (4.0)% (2.0)% (2.0)% - - Growth 1

Diagram 1: Revenue Business Description Breakdown in FY18 Other (inc. General Overview Media) 6% Having transformed from its former status as a government owned natural monopoly, TLS is one of Global Connectivity Australia’s darling telecommunications companies. With dominant market positions in mobile and fixed- 6% line spaces, TLS boasts a 16.7m mobile customer base and provides access to 11m fixed-line services. These two segments collectively comprise 62% of TLS’s total revenue (TR) (See: Diagram 1). It has NAS recently come under a change in focus and structure in both areas. From 2014, it began disconnecting 14% fixed customers and moving them onto NBN representing a move from a wholesaler of broadband to a Mobile retailer. TLS also has footholds in more peripheral telco services. Whilst Data & IP (10% of TR), NAS 40% (14% of TR) and Global Connectivity (6% of TR) have promising, albeit historically volatile, growth, they Data & represent a small proportion of TLS’s TR. Despite the proliferation of its products in Australian homes Fixed IP (Exc. One- and enterprises, TLS’s historical performance over the last five years reflects that of a company forced 10% offs) to adapt rather than one undergoing a smooth transition. EBITDA margins have declined from 42.4% to Recurring 22% 35.9% between FY13 and FY18. The declining EBITDA figures are a result of (1) TR growth of 1.91% NBN DA over the same period on a CAGR basis, and (2) Increasing operating costs of 5% p.a (See: Diagram 3). 2% Source: Abercrombie & Co Analysis Business Model Diagram 2: Mobile Revenue TLS’s business model follows a matrix configuration; six broad products that run laterally across three Breakdown in FY18 ($m) end consumer groups: Personal, Small Business, and Enterprise (See: Diagrams 2 and 4). $8,000 165 14 Mobile: Comprises 40% of TLS’s FY18 annual revenue. Over the previous 5 years, mobile revenue has 890 $7,000 958 grown at a CAGR of 1.97%. Revenue is generated via three channels: (1) through 20 simplified mass 7401 market pre-paid contracts that offer a range of phone, data and text/call combinations; (2) mobile $6,000 broadband solutions with three price points (See: Appendix 23); and (3) wholesale of mobile network $5,000 facilities to wireless communications providers such as Boost Mobile, Aldi Mobile and Lyca Mobile. 5374 $4,000 Fixed: The combined services (voice, data and other) comprise 22% of TLS’s FY18 total revenue. $3,000 Revenue is generated through: (1) fixed voiced plans across 4 price points, (2) fixed data from 100GB to Unlimited with a which can be bundled up with additional entertainment additions included from the $2,000 ‘unlimited data’ plans which includes a $100 Foxtel standard installation fee. Fixed voice and data plans $1,000 come with a $99 connection charge for new customers and (3) wholesale of broadband or NBN network $0 facilities follows the same Telstra Wholesale Agreement. Data & Internet Protocol: Provides solutions for fast and scalable Virtual Private Networks (VPN) e d 2M Pr d oa id l ta i llit an pa a To ep M te between a firm’s offices through ethernet connections. TLS is able to effectively cross-sell Cloud db st Sa Po Products, Security Services and Application Networking which contributed 10% to total revenue in FY18. Br Source: Abercrombie & Co Analysis Competitors like Evotec and other data network providers in higher ARPU Area Network connections Diagram 3: EBITDA Breakdown in have reduced revenue recently. FY18 Network Application Services (NAS): Represents TLS’s IT services segment providing Cloud solutions Recurring and other integrated services. NAS revenue increased 8.6% in FY18 with integrated service revenue NBN DA 5% driving this growth (39.5%) followed by Cloud services (14.4%), which has grown with TLS’s service of Data/IP 14% connecting users to the public or private cloud data centre partners. NAS has a steady EBITDA margin Mobile NAS 3% 38% of 10% and contributes 14% to TLS’s TR. Media: Entertainment packages can be purchased standalone, or in mobile bundles. TLS’s entertainment segment includes (1) Foxtel which operates on a per-month subscription model starting the most basic ‘Entertainment’ package for $26 per month to the ‘Platinum HD’ package for $111 per month, (2) TLS TV which can be bought for $192 outright; and (3) BigPond Movies including a library of movies and TV Global Fixed shows to rent as opposed to a subscription. In FY18 this segment has seen -1.2% revenue growth fuelled Connectivity Exc. partly by the mass migration of 18,000 subscribers. 8% Net One-Off One Off NBN DA NBN 17% C2C Other: Income growth in ‘other’ was largely due to increased NBN disconnection fees (and associated 18% Source: Company Filings one-offs) in line with the NBN network rollout. This category also includes Technology, Innovation and Strategy (including TLS Ventures and Ooyala), New Businesses (including TLS Health), and Media & Diagram 4: Heatmap of Relative Marketing. With FY18 revenue growing by 38.3%, this segment has been the fastest growing, albeit due Intensity of TLS’s Key Segments to NBN one-offs. This segment contributed 6% to total revenue in FY18. Personal Small Business Enterprise Industry Overview & Competitive Overview Industry Overview: Market Dynamics Mobile NBN Disruption: The government rollout of NBN has replaced the monopoly fixed-line internet network Fixed that TLS formerly commanded. The loss of this wholesaler position will cost TLS $3bn annually once the NBN completes. In contrast, the lower relative charges for retailers of NBN and negligible capex required NAS for competitors to resell NBN services has led to intense competition, with over 180 Retail Service Providers (RSP) now competing for NBN market share. RSPs are guaranteed uniform price and quality Data/IP by NBN Co, unlike when TLS, a competitor, was a wholesaler. Since consumers have wide access to comparable NBN providers, this has given rise to a period of intense churn. Despite this, NBN Co Media wholesale prices have not declined consistently. NBN Co recently reduced most wholesale prices to $45 but are still optimistic of achieving a $52 target by 2021. NBN ARPU remains sluggish (growing from $43 Other to $44 between FY15-18), so industry analysts expect higher access charges to remain unsustainable. With nearly 3m households and businesses currently connected, there is an activation rate of 45,000/week. By 2021, it is expected 75% of Australia will connect to NBN. Leader Neutral Competitive Source: Abercrombie & Co Analysis 2

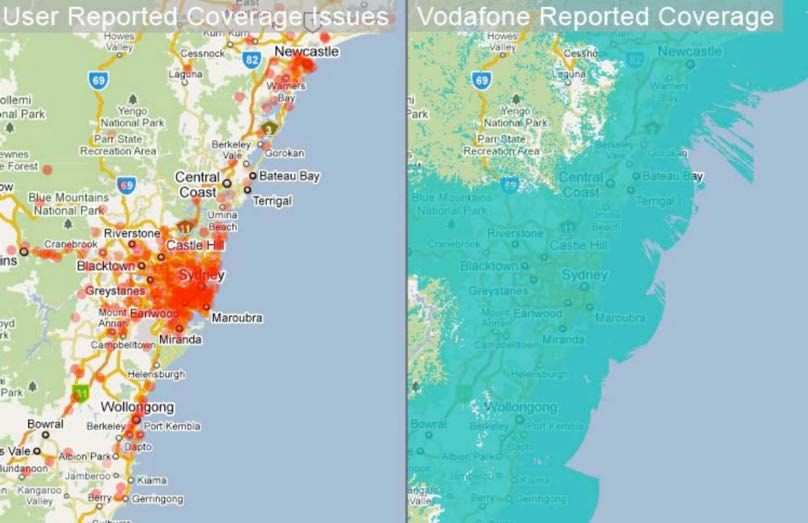

Mobile Competitors are Rising: Increasing competition between mobile service providers has fuelled Diagram 5: Data Allowances by downward pressure on TLS’s mobile ARPU, which is now $57.67. Industry mobile ARPU continued to Year decline 3.1% over the past year. Over the past 4 years, the mean annual ARPU decline has been 7.1%. 100% Whilst the 3 main players (TLS, Optus and VHA) have maintained fairly stable market share over the past 5 years, the rise of Mobile Virtual Network Operators (MVNOs) has contributed to price pressures. These 80% smaller players resell mobile services by leasing capacity from the big 3, and often provide prepaid plans at a cheaper price point with larger data inclusions (eg. Amaysim $40 15GB data for 28 days; also see 60% Appendix 23). The growth of data capacity has contributed to the popularity of affordable MVNOs, with 40% the total market share of Amaysim, Vaya and other MVNOs increasing whilst TLS market share has declined by 2% over FY17. 20% Lessons from Overseas: Globally, incumbent telcos have faced analogous pressures to TLS from rising 0% competition, technological disruption, and limited organic growth prospects. This highlights the difficulty Prior to FY14 FY16 FY18 for TLS to navigate beyond a low Average Margin Per User (AMPU) post-NBN world and retain mobile 2013 market share. For instance, consistent declines in mobile ARPU in the US, driven by competition and data usage spikes, drove: (1) merger frenzies to consolidate and seek higher growth and AMPU 20GB Wireless territories. This trend was also seen in the UK, when BT acquired EE in 2016 to create a 35m customer base. (2) Other incumbent telcos have opted to expand into adjacent operations or create Source: Abercrombie & Co Analysis bundled offerings to boost AMPU, such as AT&T’s merger with entertainment conglomerate Time Warner and Swisscom’s expansion into hospitality and cloud infrastructure. (3) Other telcos have faced further Diagram 6: Complaints to AMPU constraints and ARPU declines from aggressive competitors, which take advantage of a higher Ombudsman by Issue churn environment by undercutting. French telco Illiad disrupted the industry and claimed 5.4% market share in their first 6 months. Orange, the incumbent, failed to achieve positive growth for the next 7 years. Industry Overview: Consumer Dynamics Landline Phone Rising Demand for Data: Over the past 5 years, data consumption has increased significantly for mobile Internet 27% 40% users and households (See: Diagram 5). Average monthly household data downloads over fixed-line connections have grown from under 10GB/month in 2010 to 95GB/month in 2016. This demand is projected to grow to 420GB/month by 2026 with technological advancements. Mobile trends follow a similar pattern, with 61% of mobile data plans comprising at least 3GB in 2017, compared to only 36% in 2013. Demand has been fuelled by the rapid uptake of subscription video on demand (SVOD) apps which Mobile Phone consume significant data. Netflix in particular, has demonstrated substantial growth in the Australian 33% market, averaging 100,000 new subscribers/month immediately following its launch. With mobile penetration reaching saturation levels ~96% and over 70% of 18-34 year olds regularly streaming videos Source: Telecommunications Industry Ombudsman on mobiles, telcos have upgraded their 4G networks to accommodate faster download speeds. Major investments in 5G technology are likewise expected as data demand grows. Diagram 7: Complaints against Over the Top (OTT) Disruption: OTT refers to applications and services provided to consumers over Telcos the internet without needing to be accessed via the telco providers. The growing popularity of OTT apps, 140,000 particularly messaging services like WhatsApp and Skype, have successfully deprived traditional revenues telcos received from their voice products. According to the Communications Department, 120,000 Facebook’s messaging apps now outnumber global SMS volumes 3:1. Our analysis suggests many OTT 100,000 apps are now seen as a cheaper alternative for traditional text and calls and have driven sharp declines 80,000 in mobile voice revenues across major Australian telcos. The growth of OTT services has forced telcos to invest in mobile data plans, though these have lower margins than voice. We believe this market trend 60,000 will continue, especially as telcos invest in data-centric products amidst diminishing mobile voice revenue 40,000 (TPM planned to enter mobile with data-only plans; TLS eliminated excess data charges). 20,000 Falling Trust in Telcos: Continual disruptions to coverage have contributed to falling trust levels between consumers and telcos. TLS in particular has the worst NPS score of all major telcos after 0 FY14 FY15 FY16 FY17 numerous NBN and mobile coverage issues (See: Diagram 12). The level of Australians who trust telcos has fallen to 53% in 2018. NBN problems relating to connectivity led to 23,000+ complaints to the Industry Telstra Optus Vodafone Ombudsman over 6 months in 2016, prompting a regulatory review. Complaints also rose 31.2% to iiNet TPG Primus Optus, 32.1% to Primus, 37.5% to VHA and 44.9% to TPM (See: Diagrams 6 and 7). Similar complaints spurred NBN Co to delay the NBN HFC rollout. In April 2018 TLS suffered major coverage outages of Source: Telecommunications Industry Ombudsman emergency hotlines. Optus also was forced into public apologies and free World Cup streaming after allocating insufficient bandwidth to subscribers. Diagram 8: NBN Wholesale Competitive Positioning: National Broadband Network Market Share TLS continues to lead with 48% NBN market share, compared to its closest rivals: TPM (26%), Optus Others Vocus 6% (14%) and Vocus (6%) (See: Diagram 8). However, our analysis indicates that relative to the pre-NBN 6% period, the rollout of the technology has noticeably increased competition and reduced market share, particularly in regional areas where TLS holds 55% market share compared to its traditional share near 70%. The setting of wholesale prices by NBN Co, instead of TLS, has created a $3bn earnings hole for TLS once the rollout is complete. As a result, bandwidth quality has generally been standardised, with Optus the exception of telcos who have not afforded purchasing CVC capacity to manage bandwidth during 14% Telstra 48% peak periods. We conducted a price survey (See: Appendix 23) across major telcos and identified that TLS charges substantially higher prices for their NBN50 services ($89 per month), compared to rivals like TPM VHA ($69) and TPM ($70). NBN churn rates have steadily increased over the past 5 years, and will 26% continue during the rollout, labelled a ‘once in a generation churn event’ by NBN Co. Competitive Positioning: Mobile Our telco price survey reveals that TLS’s basic SIM plan is substantially more expensive at $49 for Source: Abercrombie & Co Analysis 20GB/month compared to rivals like Optus ($36 for 30GB/month) (See: Appendix 23). This reflects TLS’s traditional focus on higher value consumers willing to trade cost for greater network coverage and TLS’s 3

Diagram 9: Postpaid Mobile superior brand equity. However, significant capex by competitors on improving network coverage ARPU Using BT/EE Acquisition including Optus’ $1bn upgrade of its regional network and TPM’s expected merger with VHA may further 62 increase competitive intensity and reduce mobile ARPU (See: Diagram 9). Whilst TLS has been the market leader in mobile, with 37.9% of total market share (postpaid and prepaid), this has fallen from 60 39.9% the year prior. Cheaper and higher data plans offered by smaller players like VHA and Amaysim 58 helped capture market share away from TLS and Optus. TLS’s prepaid market share declined from 41.5% 56 in FY17 to 34.8% in FY18, as lower cost prepaid plans have become more attractive during high churn 54 periods. Almost 50% of consumers switched providers in the past 3 years. TLS’s strategy has angled 52 towards investing in cloud services and upcoming 5G mobile networks to fill the $3bn NBN earnings hole. 50 If successful, demand for such networks could bypass fixed broadband connections, leading to a growth FY17 FY18 FY19 FY20 option for TLS earnings. However, we believe there are technological limitations and execution risks that Source: Abercrombie & Co Analysis; NB: see Appendix may hinder the expectation of filling the $3bn hole with these sources. 21 for further background regarding the case study Competitive Positioning: Telstra 2022 The Telstra2022 (T22) strategy was unveiled to improve competitiveness. It has 4 pillars: (1) simplifying Diagram 10: Comparing Equity products from 1800 to 20 plans, following efforts that have already been made by competitors like Optus and Debt of TPM, VHA and SPV to reduce redundant packages. The removal of excess data charges may have limited upside to improve TPG VHA 1 VHA 2 SPV TLS’s position since it primarily appeases existing customers facing unpopular charges. It may also $9 further reduce TLS mobile ARPU. (2) TLS aims to offset earnings loss by optimising operations with an ambitious $2.5bn cost reduction strategy. This represents a 35% cut on the underlying cost base of $7bn. 7.6 We hold concerns that the cost out will not be met, considering management’s record belying costs and $6 0 TLS’s hefty cost of sales growth. Even if the cost out is achieved, it will require reductions in customer- facing services. This will increase churn amidst a turbulent period of competition and depress ARPU 4.8 beyond any marginal gains in AMPU. (3) TLS will establish InfraCo as a standalone infrastructure $3 5.5 business InfraCo meanwhile, we believe is geared to either be set up to bid for NBN Co post 2021 or 5.4 provide transparency of TLS’s infrastructure-related earnings. (4) T22 will also aim to streamline the 1.9 organisational structure of the firm and focus on product leadership with new roles to build capabilities. 1.7 $0 Investment Summary -0.8 -$3 Net Debt Equity 1. Rising Mobile Competition | Prepare for the Game of Phones Source: Abercrombie & Co Analysis; NB: See Merger Model; VHA 1 is the standalone VHA; VHA 2 is the merged entity The $15bn TPM-VHA merger could threaten TLS’s mobile earnings. We believe the market has reacted positively to the announcement and expect a consolidated TPM-VHA may alleviate ARPU pressure. But against the backdrop of higher competition and data demand, TLS is likely to lose customers to TPM- VHA with incentive and capacity to be aggressive, and to other competitors with better customer service. Every Person Has Their Price | Quality Premium < Price Premium Diagram 11: Debt Trends of TPM- VHA Entity vs TLS Bundling Exposes an Overrated Quality Premium: TLS’s mobile advantage relied on its actual and 5,000 2.50x perceived network superiority. Despite cheaper plans in the market, TLS maintained market share with high ARPUs because of customer preferences for quality networks. But the pace of VHA investments 4,000 2.00x into infrastructure (like investing $2bn in FY17 on mobile coverage) has spurred rapid improvements in network quality. VHA call success rate for instance has quickly caught up, improving 610 basis points to 3,000 1.50x 98.9% compared to TLS’s call success rate of 99.20%. VHA has a credible network with the opportunity to pierce TLS’s customer base on quality and price. We developed a quality-price divergence matrix by comparing network metrics of VHA and TLS as proxies for quality (e.g. active cell towers; See: Appendix 2,000 1.00x 15). Whilst TLS has superior quality metrics, our calculations reveal that the price that existing TLS customers were willing to pay for this quality advantage over VHA is only $23. However, the TLS plans 1,000 0.50x are $29 more expensive than comparable VHA plans (See: Table 7 and Appendix 15). This crossed the matrix point where TLS customers would migrate to VHA. We posit that this switching decision has not - 0.00x been triggered for many TLS customers because there are 3.1m customers on bundles, locked in with 20192020202120222023 lengthy broadband contracts, and switching to VHA does not fill a needed broadband replacement. The EBITDA TPM-VHA merger provides bundling of broadband and mobile and activates the gateway to capture these Net Debt customers. It exposes TLS’s overvalued quality premium and offers bundled broadband to trigger Net Debt / EBITDA migration. This is similar to the bundling impact after UK telco BT acquired mobile player EE. Postpaid TLS' Net Debt / EBITDA mobile ARPU declined from £25.9 to £23.4 from FY16-18 and the incumbent telco’s market share Source: Abercrombie & Co Analysis dropped 25% to 21% (Appendix 21). Further, whilst TLS has coverage over 99% of Australians, since 85% of the population stays within urban areas, which VHA already covers, TLS’s coverage premium is less compelling. Consumers spending most time in urban areas may be less likely to accept a $29 price Diagram 12: Comparison of NPS premium for negligibly different network quality within urban areas. This boosts the incentive to switch to across Telcos TPM-VHA. We project TLS market share will fall by up to 5% in FY19. We expect industry ARPU to fall, 25 as TLS and Optus fight on price to close the gap between the quality and price premiums. Rather than having 4 main telco players prior to the merger, our view is that there were only two main bundle 20 providers. With TPM-VHA, there are three quality bundle providers, enabling the price war to go on. 15 Clinging to Price Relief: We expect TPM-VHA to be aggressive in pricing as a merged entity contrary to beliefs that TPM-VHA would abandon an undercutting strategy. We believe TLS’s ARPU will decrease 10 to $55.73 in FY19, and TLS would miss EBITDA guidance of $8.7-9.4bn by 4%. We view VHA’s decision to create a Special Purpose Vehicle (SPV) (which involves VHA moving $4.8bn of debt and paying it 5 down with their half of the dividends from the TPM-VHA) as a means to ensure capex can be sustained 0 without hiking mobile prices (See: Diagrams 10 and 11). This is because in the absence of the merger, FY15 FY16 FY17 FY18 network investments placed TPM at risk of breaching their 3.5x Net Debt/EBITDA covenant and VHA’s -5 $7.57bn debt (at August 2018) inhibited its ability to raise more debt to fund mobile capex. Instead, TPM- VHA will have a combined leverage of 2.2x Net Debt/EBIDTA (See: Diagram 11). Our merger model also -10 Source: Company filings affirms that TPM-VHA will be deleveraged with greater debt capacity from the merger, as Net Telstra Optus Vodafone Debt/EBITDA declines across our model forecast (See: Appendix 22). This enables a sustainable annual 4

outlay of $898m in capex for mobile network and 5G upgrades, whilst allowing TPM-VHA to keep their Diagram 13: Average Customer prices low to capture market share. The prospect of TPM-VHA choosing an aggressive strategy is also Wait Times (hrs) supported by Mr Teoh’s claim after announcement that TPM-VHA will be a “leading challenger” and VHA’s motivation to reclaim the migration of customers from Vodafail. 1.3 1.3 Customer Flight | Unprecedented Attrition Rates 1 1 0.8 Customer Dissatisfaction: In a low trust environment, TLS customers may have reached peak dissatisfaction. A comparison of NPS reveals TLS is reaching an all-time low in customer satisfaction, 0.5 from a score of 13 to 7 in FY18 (see: Diagram 12). Rivals like VHA have a score of 20. Against more reliable alternative providers, we believe dissatisfied TLS customers could flee, contributing to the projected 6.7% fall in FY19 earnings. Our analysis reveals the causes are: (1) outages; with 174 reported outages since January 1; and (2) longer wait times than competitors (See: Diagram 13). On our testing, it took on average 1hr 31min to reach a human on TLS’s hotline, exceeding the industry median of 1hr. m ne ng in tra us rg si pt fo lo ls ay Vi Te O Be da Am Vodafail – the sequel? The previous two factors parallel the start of the ‘Vodafail’ saga in 2010, where Vo Source: Australian Communications Consumer Action Network VHA’s customers experienced outages and poor response rates. This reduced NPS by 250% from 2010 to 2012. VHA experienced churn of 8.4% in half a year and of 33% over the entire period. Given the Diagram 14: TLS’s Capex and current period of high churn and similarities with VHA in Dec 2010, we appropriate the abnormal impacts Gearing of ‘Vodafail’ churn in the 1st year (at a 50% discount) to arrive at our FY19 churn estimate at 16%. 55% $7,000 2. All in on 5G | Hold the Door for Rivals to Enter 5G $6,000 50% 5G is the next generation of mobile internet connectivity (e.g. 3G and 4G), which is becoming a driving $5,000 factor of mobile uptake. TLS relied heavily on commercial 5G launch in 2020 reviving earnings. $4,000 Historically, TLS enjoyed the premiums available as a first-mover during 3G and 4G rollouts. We challenge management’s guidance that TLS will be the first to market and forecast subdued ARPU growth [A$m] 45% $3,000 of 1% in FY20 and declining growth afterwards. We premise this on a hyper-competitive landscape that will not subdue at commercial launch of 5G as Optus and TPM-VHA will be as ready as TLS. $2,000 40% 5G Rollout | Telstra No Longer First $1,000 ARPUs skydive against main Rival Optus: TLS may be forced to introduce expected plan prices for 35% $0 5G that will be unable to meet the premium investors expect. TLS increased capex with network upgrades FY11 FY13 FY15 during from FY11 and FY15 for 4G and 4GX (Diagram 14). These were offset by charging a premium for the new network with ARPU growth of 7.05% in FY11 and 5.51% in FY15 (Diagram 15). Having a Capex Gearing monopoly over 4G for a year before Optus turned on their networks and 4 years before allowing access Source: TLS Annual Reports to resellers (e.g. Woolworths Mobile, Boost) ensured TLS achieved perceived market leadership and could receive ARPU premiums before competitors caught up. However, as 5G rollout intensifies in FY19, our analysis affirms TLS will come to market at a similar time to Optus, eroding historical premium Diagram 15: TLS and Optus expectations. We modelled a -5% ARPU in FY19 and a subdued increase of +1% in FY20. These ARPU Growth Trends forecasts are premised on: (1) TLS’s plans to rush the “early 5G” stage by launching 200 5G-compatible sites this year has limited benefit as commercial 5G compatible devices only become available in 2020. FY11 FY13 FY15 FY17 FY19 Therefore, Optus’ plan to rollout out an identical 5G network in early 2019 will make them as ready as 11% TLS (See: Appendix 25) (2) Optus holds the most bandwidth in 5G spectrum at a population weighted average of 33.1% in major cities (See: Diagram 16). This allows trialling in capital cities where mobile 6% usage is most concentrated; (3) Thus, Optus has been able to accelerate successful 5G trials in July 2018 and matched similar TLS trials run in April 2018. We predict TLS will merely be equally placed with 1% competitors to rollout 5G. They would lose the ARPU premiums historically relied upon to recoup capex. -4% TPM-VHA together ensures guaranteed spectrum: The upcoming spectrum auction provides TPM- -9% VHA the opportunity to acquire the resources needed to continue initial 5G trials. We believe TLS investors will revise ARPU and subscriber growth downwards as a result. With TLS’s debt financing -14% capacity, we hypothesised that it could acquire all 60MHz of their spectrum allocation. Without a merger, TPM and VHA would be in fierce price competition to attain as much of the remaining 60MHz available -19% but would still be expected to stay below its debt covenant of 3.5x. However, the TPM-VHA partnership eliminates a bidding war and accelerates 5G rollout as it ensures the maximum spectrum of 60MHz will Telstra Optus be available to the combined entity and we estimate potential cost savings to be around $30m (Appendix Source: TLS and Optus Annual Reports; USR 28). We also forecast subscribers migrating from TLS. Though the rushed VHA Three partnership in 2011 Analysis could not manage mass migrating customers, TPM-VHA has better network and resource capacity to succeed since: (1) TPM-VHA has already started deploying small cells in Sydney which are 5G Diagram 16: 5G Spectrum infrastructure alternatives to macro sites of traditional mobile base stations. This reduces overall costs Ownership in FY18 for the combined entity as it expands on TPM’s 21,000km fibre networks, (2) the combined entity will extract learning economies of Mr Teoh’s experience in cost-cutting market entrance and Iñaki Berroeta’s 100% experience in mobile strategy; and (3) they have upgraded their towers to use 4.9G in preparation for 5G, allowing Western Sydney customers to use and be familiarised with VHA developments. 80% Aggressive Entrant | Three is Not the Magic Number Differentiation is King in the Face of Data Commoditisation: Intensified 5G rollout coinciding with 60% imminent NBN completion could trigger a major churn event for TLS. Consumers who are upgrading existing plans onto the new broadband and cellular network will become incentivised to join a new 40% provider with targeted offerings. Investors may infer an imminent rollout would lead to TLS ceding 4% market share to its competitors in FY20, contributing to a 6.7% decline in mobile revenue. Historically, 20% churn rates increase with each new network generation. The 4G rollout in FY11 caused a deviation from mean industry churn by 200bp (Diagram 17). With similar expected 5G rollout dates and data commoditisation (see Industry Overview), we expect product differentiation will drive market share 0% growth. We believe TPM-VHA’s merger allows for differentiation via cost leadership. By bundling mobile Sydney Melbourne Brisbane and broadband, we expect to see reduction in prices greater than if consumers purchased mobile and Available Optus NBN Co Telstra broadband separately. Further, we believe that Optus’ monopoly on international football streaming is an Source: Abercrombie & Co Analysis 5

Diagram 17: Industry Churn in enticing point of differentiation. Optus’ $63m exclusive license of the English Premier League proved to 19% the Postpaid Mobile Space be an effective acquisition strategy as these streamers were more likely to be Optus customers by ~290bp. We view the recent World Cup streaming failure as merely short term because football 16% subscribers increased after the failure and Optus has significant quality and quantity over previous providers of World Cup streaming. In contrast, TLS uses a sublicensing strategy where non-TLS 13% customers can access content, eliminating the differentiation benefit. For instance, their AFL, NRL and Netball streaming lack the same growth popularity and compete directly with free-to-air . 10% 3. Commoditised NBN | Winter is Still Coming The NBN has diminished AMPU for TLS over time. Wholesale access and CVC costs remain high, and 7% FY11 FY12 FY13 FY14 FY15 FY16 NBN rollout has enabled smaller, efficient competitors to offer parallel broadband to TLS. ARPU has Industry Average remained low at $44, sluggishly growing $1 since FY15. We believe impacts of NBN commoditisation are fully priced in by a pessimistic market. In FY19, catalysts relate to the difficulty of the incumbent to keep Source: Abercrombie & Co Analysis any remnant of quality advantage and meet their cost target, and an impending dividend cut. Diagram 18: CVC per User Incumbent’s Curse | Competition and Costs Catching Up Projects (mbps) 4 The churn will go on: In 2018, NBN Co began the progressive rollout of new wholesale NBN bundles. It encourages uptake of sufficient CVC, which enables telcos to support NBN peak speeds amidst 3 congestion. Bundles represent savings of 27% for 50mbps and 10% for 100mbps NBN. TLS’s prior NBN 2 competitive advantage was their investment in CVC above industry norms, which allowed them to achieve 85% of maximum service speeds during peak time. However, our analysis indicates these bundles will 1 spur improved competitor network quality as cheaper CVC bridges a previously unaffordable divide for smaller telcos. By modelling the resulting abnormal CVC uptake following other discount programs (See: 0 Diagram 18), we determined the new bundle prices almost double industry average CVC/user by the end 3/1/2017 3/1/2018 3/1/2019 of 2019 to 2.93mbps. At these levels, quality convergence of bandwidth across telcos reduces ARPU and Source: Abercrombie & Co Analysis keeps churn high as consumers benefit from choice. TLS’s connection quality advantage will decelerate quicker than expected, thus we forecast TLS fixed data revenue to fall 5%, and net income to fall $440m. Diagram 19: Cost Increases Outstripping Savings T22 Cost program – dubious at best: With competition set to rise further in FY19, we do not believe 2500 TLS’s $2.5bn productivity savings program will meaningfully increase margins. We hold concerns over 1500 executing the remaining $1.8bn in fixed cost savings that the market expects. Under CEO Andrew Penn, costs ballooned $3bn since 2015 whilst EBITDA shrunk 4%. In contrast, mature telcos like VHA cut costs 500 by $600m over the past decade. Overseas, BT Group has cut costs by $2bn. TLS has problems executing cost efficiency programs. Plans to cut 30% of labour could impact customer satisfaction as NBN support -500 FY17 FY18 FY19 FY20 personnel reduce. In a high churn setting from NBN rollout, this compounds market share loss. Even if Cumulative TLS NBN the $2.5bn fixed cost target is reached, we think the market has overlooked the rapid increase in cost of Network Cost Increases sales in FY18, growing $1bn (13.6%), faster than the cost out which only progressed $480m. Greater Cost Savings Achieved (m) than expected payments to NBN made up $494m of this rise in cost of sales. The record 6.9m users Source: Abercrombie & Co Analysis connecting to NBN in FY19 and temptation to purchase more CVC to combat rivals could trigger cumulative cost of sales increases of $2.4bn by FY20, eviscerating the productivity savings (See: Diagram 20: Projected Ordinary Diagram 19). We project NBN cost of sales to increase by $773m, reducing EBITDA by 2.9% in FY19. and Special Dividends (c) 25 High Dividends to End | Not Enough Cash for Capex 20 Other concerns will take priority: Our analysis suggests a major dividend cut, beyond expectations, is 15 coming. In FY18 TLS paid 22c in dividends, 30% lower than the 5-year average. We believe the market 10 currently implies a 18c ordinary dividend/share in FY19, on a bare bottom 70% payout on lower end of TLS earnings guidance. This is still too optimistic. With capex and competition pressures posing 5 existential threats to TLS’s market leadership, we believe TLS will prioritise an A band credit rating (See: 0 Financial Analysis). In light of a recent A- downgrade, cofounding events in FY19 risk depriving NPAT. FY18 FY19 FY20 FY21 FY22 The looming $1.2bn capex outlay for their network program will lead to negative cash balances without Ordinary Special additional financing. Raising debt to cover this will breach the target debt servicing ceiling of 1.8x Net Source: Abercrombie & Co Analysis Debt/EBITDA. Other earnings pressures also strain TLS’s cash flow in FY19. Further NBN competition and aforementioned mobile declines both suppress ARPUs, losing $128m and $646m respectively. In Table 1: FY19 Upper and Lower our best-case scenario with zero premium for the 5G spectrum auction, TLS still commits $93m in capex Guidance with no recoupment until the 5G rollout. Thus, the dividend must give and we model that TLS will only have capacity to pay an ordinary dividend of 16c (See: Diagram 23), a 12.2% downside to expectations. FY19 FY19 Lower Upper With a 55% retail investor base, this retreat could spark a sell off. A bull case cut to 17c leads to a 4% Guidance Guidance fall in price from our base Discounted Cash Flow (DCF). A bear case cut of 13c triggers a 10% price fall. EBITDA 8800m 9500m Valuation NPAT off Historical Our price target of $2.67 was computed via three valuation methods: Consolidated Discounted Cash 2728m 2945m 31% Flow Model (DCF), Sum-of-parts (SoP) Maintainable EBITDA Model, and SoP relative valuation. The Ratio SoP approach rendered a more accurate valuation of TLS than on a consolidated basis, as it recognises Payout the dissimilar growth prospects and financial and operational risk profiles of each business. A Dividend Ratio off 70% Discount Model (DDM) was also calculated, although not weighted in the overall valuation. 70% Ordinary Div Consolidated Discounted Cash Flow Model [30% Weighting] Total 1909.60m 2061.50m Our DCF model was calculated using a Two-Stage Free Cash Flow to Firm (FCFF) with a five-year Dividend forecast horizon and a terminal growth rate (TGR) of 3%. We computed an intrinsic valuation of $2.74 Total per share. The five-year horizon represents the optimal period within which TLS’s cash flows, growth and Dividend risk assumptions can be projected without compromising the forecast accuracy. $0.17 $0.19 per Share Source: Abercrombie & Co Analysis 6

Table 2: Valuation Output Revenue: Since TLS’s business model operates on subscription contracts, revenue is a function of ARPU (contract price) × subscriptions: positively impacted by population growth and gross additions; negatively Share impacted by switching subscribers (churn rates). Method Weighting Price Mobile: [44%]: The primary driver of revenue is (73%) postpaid contracts. TLS’s postpaid ARPUs DCF $2.74 50% declined by a CAGR of 1.3% between FY11-18 with average churn rates of 10.88%. The current churn MEM $2.72 20% environment – further fuelled by ongoing NBN rollout – will see ARPUs further decline from $58.05-$53.53 (FY18-20) as competitors attract subscribers in the run-up to the next generation rollout. We forecast Multiples $2.44 30% increased net churn (gross churn less additions) of 4% in FY18 and 2% (FY19-20) given the same reasons, exacerbated by TLS’s low consumer satisfaction revealed by a 7 NPS score. Total mobile Target Price $2.67 revenue remains flat across the forecast: $9,468.7m (FY19) and $9,571m (FY23). The negative growth in postpaid is muted by moderate growth in the other 27% of mobile revenue (See: Appendix 14). Source: Abercrombie & Co Analysis Fixed: [18%]: Fixed revenues derive primarily from data and voice products. Fixed data revenue grew at 4.1% CAGR since FY14, but this obscures recent struggles to grow (1.6% FY17, -0.4% FY18). This stems from intensified competition with NBN. TLS’s lost wholesaler status and equal quality broadband Diagram 21: TLS’s Sales and available for 180 RSPs keep ARPUs low at $44. We project increased competitor capability and high EBITDA Margins churn through NBN activations will amplify revenue decline: -5% (FY19-20). Fixed voice fell 9.5% on 28 44% average over FY14-18 as growth of OTT and data alternatives usurped voice services. These revenues continued to fall -15% each year into the forecast, with no signs of a return to popularity for legacy voice. 27 42% NAS: [14%]: Annual revenue growth in NAS has been historically high yet volatile, with a mean of 20.2% 40% and standard deviation of 12.1%. NAS represents the ancillary growth engine of the company. Recent 26 38% growth may have been inflated, driven in part by the capture of clients transitioning from TLS’s own data 25 and IP networks, rather than capturing from rivals. Revenue is forecast to increase in line with reduction 36% in Data & IP, with additional 8% uplift in industry demand for cloud. 24 34% Data & IP: [10%]: Data & IP declined by a mean of 9% since FY16, due to cannibalisation by the NAS 23 32% FY13 FY15 FY17 segment, as legacy physical data networks have seen demand shift to replacement cloud networks. We project further discontinuance of legacy data VPNs with revenue declining 4.9% each year. Sales [A$b] Operating Expenses: Management forecasts the T22 $2.5bn cost cut regime by FY22. We expect a EBITDA Margin [%] disproportionate amount of costs to be reduced in the short-run as the company streamlines its 20 plan Source: Abercrombie & Co Analysis offerings and employee salaries reduced as per management’s guidance. Cost reductions may be unlikely to continue at this rate. Lack of NBN cost relief and capex for 5G rollout could also largely mitigate Table 3: Valuation Output any cost-reduction benefits. As such, we forecast moderate decline in OPEX as a percentage of revenue from FY19-FY20, which levels from FY21 across the rest of the horizon. Forecast WACC 6.60% Capex: Forecasted to increase on the assumption that TLS will bid for all its available spectrum Terminal WACC 7.01% allocations. The value of the spectrum auction with only two main telcos (TLS and TPM-VHA) may have a zero premium and should sum to ~$93m – contributing to the FY19 capex figure. The result is PV Forecast FCFFs ($m) 9,077.1 capex/sales ratio of 17.8%, the upper end of management’s 16-18% guidance. From FY20-23 we expect capex to increase from ~$5872m-$6633m with 5G infrastructure capex and new network towers. PV Terminal FCFFs 39,728.3 (Sm) Free Cash Flow to Firm (FCFF): FCFFs were discounted at the explicit WACC of 6.60%. Cost of equity Enterprise Value 48,805.4 of 8.39% was calculated via the CAPM, Fama-French Three Factor model and the DDM (Appendix 9). ($m) The cost of debt of 3.24% was computed via a triangulation of intrinsic and comparable methods Less: Debt ($m) (16,860) (Appendix 10). TLS’s terminal value, which stores 81% of the company’s DCF value, was discounted by a terminal WACC of 7.01%. This higher discount rate reflects greater risk associated with TLS’s terminal Add: Cash ($m) 629 cash flows against the backdrop of the firm restructuring, industry changes and intense competition. (Appendix 11). TLS’s terminal FCFFs are assumed to grow in line with our TGR of 3%. After summing Equity Value ($m) 32,574.4 FCFFs and subtracting net debt, we arrive at an equity valuation with an intrinsic price target of $2.74. Shares Outstanding (m) 11,878.9 SoP DCF Maintainable EBITDA Model [50% Weighting] Value Per Share $2.74 Separating InfraCo offers the financial transparency needed to value core operations (CoreCo) separate to the infrastructure business. CoreCo was modelled with similar assumptions as the consolidated DCF. Current Share Price $3.21 Maintainable EBITDA: This represents the EBITDA attributed to the CoreCo (ex InfraCo). One-off receipts associated with the NBN transition process were stripped out as were recurring securitised Source: Abercrombie & Co Analysis payments. The result is EBITDA trending from $5,499.2m to $5,209.9m (FY19-23) consistent with margin erosion discussed in the DCF payments. Table 4: Cost of Capital Output InfraCo Value Drivers: InfraCo’s value is a function of NBN recurring securities payments that can be Forecast Terminal forecasted accurately. Their EBITDA contribution grows 2% p.a. from $593m to $623m (FY19-23) where they plateau. One-off payments were stripped from InfraCo as they are a non-recurring item distorting Re 8.39% 9.95% TLS’s intrinsic value. InfraCo’s overall EBITDA is forecast to fall from $3,125m to $2,418m (FY19-23). Rd 3.24% 4.09% Risk Profiles: InfraCo’s value can be compared to a fixed annuity stream. An appropriate discount rate Net Debt 16,653 16,653 was implied using the BBB rated as a risk proxy and implying a spread above the 10-year government ($m) bond rendering a lower explicit and forecast WACC than CoreCo. Similarly, with InfraCo detached, Equity CoreCo’s WACC was increased proportionately to reflect the riskier cash flow profile (See: Table 5). 36,591 36,591 ($m) FCFF Valuation: Two-stage FCFFs were calculated for each entity and discounted by the appropriate D/V 0.31 0.31 discount rates. The resulting SoP valuation is consistent with a $2.72 price target, $1.04 contributed by E/V 0.69 0.69 InfraCo (23%) and $1.68 by CoreCo (73%). The (Maintainable EBITDA Model) MEM results in some valuation uplift in the standalone unit caused by recognising its attractive risk profile. Tax Rate 30% 30% WACC 6.60% 7.01% Source: Abercrombie & Co Analysis 7

Sum-of-Parts Output EV/EBITDA Forecast EV (DCF) ($m) FY19 EBITDA ($m) (FY19F) WACC FCFF CAGR InfraCo 15,195.9 3,125.6 4.9x 5.2% (7.7)% CoreCo 36,892.4 5,499.2 6.7x 7.2% (4.5)% Total 52,088.3 8,624.8 6.0x Relative Valuation Trading Multiples [20% Weighting] Debt ($m) (16,653.0) Trading multiples were used on the separate units and a consolidated basis, allowing differing growth Implied Equity Value and risk profiles to be assumed by the multiples. A merit of the valuation first depends on selecting robust 35,435.3 ($m) comparables that reflect the growth, risk and cash flow profiles of TLS (See: Appendix 7). We computed Shares on issue 11,893.3 a $2.44 target price comprised of SoP EV/EBITDA, EV/Sales, EV/EBIT and consolidated P/E. NTM Target price $2.44 multiples were used to reduce historical accounting biases, rendering a more forward-looking valuation. Current Trading Price $3.21 Lower quartile multiples were applied to CoreCo whilst upper quartile multiples were applied to InfraCo Implied Premium – recognising its more attractive risk and cash flow profile relative to the core (See: Appendix 8). (31.6)% (Discount) SoP EV/Sales: weighted 9% given that the ability to generate revenue, particularly in mobile, is a key Table 5: WACC Outputs driver of value for telcos in light of competition. Further, it allows for comparison across international CoreCo WACC companies with minimal distortions (besides revenue recognition criteria) arising from other line items. The upper quartile multiple for InfraCo and lower quartile multiple for CoreCo rendered a summated Forecast 7.16% share price of $2.09. TLS trades at a 2.1x EV/Sales ratio, representing a ~15.3% and ~31.7% premium Terminal 7.58% to its comparable median and lower quartile multiples (respectively). One drawback is it is an imperfect proxy for value as it fails to consider operating efficiency discrepancies between TLS and its peer group. InfraCo WACC SoP EV/EBITDA: We ascribed 50% weight as it is a capital structure neutral metric that encompasses Forecast 5.22% the operational efficiencies of each unit. InfraCo’s implied share price is $0.99 whilst CoreCo’s is $1.63, rendering a $2.62 price target on a consolidated basis. TLS’s current price implied a 6.41x EV/EBITDA Terminal 5.60% multiple (summated basis) which reflects a marginal discount of ~5.9% to comparable peers, yet a 20.5% Source: Abercrombie & Co Analysis premium to its lower quartile. Its attractive EV/EBITDA margin is due to InfraCo’s strong EBITDA margin. Table 6: Summary Output of SoP EV/EBIT: We ascribed this multiple a 20% weighting as it provides a proxy for comparison of asset-rich companies with high D&A expenses. InfraCo’s implied price using this multiple is $0.95 whereas OpCo’s price is $1.50 yielding a total share price of $2.45, a 31% discount to the current share price of $3.21. Mult- iples TLS SP Infra Co Op Co Weight- ing P/E: Was moderately weighted at 20%. As a multiple it lacks predictive value due to its reliance on the current share price as a metric of value and is most exposed to the distortions that can arise from differing accounting treatments and capital structures. Also, it was used on a consolidated basis which implicitly bundles InfraCo and CoreCo’s risk and growth profiles into the one multiple. The peer-implied share price EV/ $2.09 $0.45 $1.64 30% is $2.51. The current share price implies a 14.85x P/E ratio – a 18% premium to the comparable multiple. Sales Financial Analysis EV/ EBIT DA $2.62 $0.99 $1.63 50% Profitability | Competitive Landscape Supressing Profit Margins Mobile Revenue: Postpaid mobile ARPUs declined from $64.46 to $58.05 (FY12-18) due to increasing competition. The negative effect on revenue growth is muted by the overall subscriber growth profile: P/E $2.51 20% averaging 4% from (FY13-18) albeit at a decelerating rate (8.6% FY13 to 1.7% FY18). In determining the quantitative impact on future ARPUs we constructed a Quality Factor Model (QFM) that aimed to Value/ Share: $2.44 understand network quality gained per marginal contract price in the Australian market. Comparing TLS, VHA and Optus, ‘network quality’ was proxied using five-factors (See: Appendix 15). Our analysis Source: Abercrombie & Co Analysis indicates that TLS’s average contract is over-priced by $5.1 (7.98%) whilst Optus and VHA are fairly priced with

Diagram 22: Cash with 18c FY19 debt (A-) was due to muted earnings and increased competition. The profile is less attractive when Dividend applying Net Debt/EBITDA less Capex (1.2x – 3.4x) across the same horizon. We expect this to continue FY19 FY20 FY21 FY22 FY23 its decline as TLS rolls out the remainder of its $3bn commitment to 5G infrastructure investments, 2500 18.4 excluding expenditure related to spectrum auction which we forecast as ~$93m. We believe capex will 2000 continue to rise as adjusted Net Debt/EBITDA increases from 4.0x to 4.8x. 18 1500 Finance-Dividend-Investment Trade-off: TLS faces a three-way trade-off scenario between its 17.6 obligations (dividends and debt) and its goal to aggressively expand into 5G. Cash has rapidly decreased 1000 from ~$5.2bn in FY14 to ~$600m FY18. It has committed to two goals: (1) maintaining an A band credit 17.2 rating; and (2) implement the $1.2bn of growth capex to invest in network and digital intangibles for FY19. 500 With ~$600m of cash on the balance sheet, stagnant profit, and $825m of debt maturing in late 2018, 0 16.8 TLS will struggle to meet its twin aims whilst also satisfying its dividend hungry investors. Using historical yields on TLS’s stock we can impute that the market expects an ordinary dividend of 18c for FY19. -500 16.4 Funding the $1.2bn outlay (assuming no additional debt) leaves FY19 cash reserves at $600m, but by Cash Dividend Source: Abercrombie & Co Analysis FY22 cash reserves deplete to -$300m. With this projection, FY19 marks a decision point for TLS to avert negative cash balance. TLS has 3 options: (1) raise debt to fully fund the $1.2bn growth capex; but whilst we expect TLS to have no issues refinancing the $825m maturing loans in FY19, raising a further $1.2bn Diagram 23: Cash with 16c FY19 in debt brings TLS past its own upper 1.8x Net Debt/EBITDA target (1.86x) which may risk another credit Dividend rating downgrade (2) reducing capex; but this would compromise TLS’s ability to be competitive. Also, 2500 16.4 reducing growth capex to $1bn still leads to -$157m cash in FY21, (3) reducing their dividend payout to 2000 16 offset the debt required. We sensitised annual dividend against cash reserves over the forecast, implying that the minimum dividend cut from 18c required to avert negative cash was $0.02. We believe a base 1500 15.6 cut to $0.16 is warranted, with a bear case dividend cut to $0.12 emerging if competition is worse than expected or one-off NBN receipts are subdued impacting the special dividend. 1000 15.2 Investment Risks 500 14.8 Valuation Risk Analysis | Sensitivity, Scenario and Risk Analyses 0 14.4 FY19 FY20 FY21 FY22 FY23 Sensitivity: Three sensitivity analyses were conducted on the key drivers of TLS’s valuation (Explicit Cash Dividend WACC, Forecast WACC and TGR). These inputs were sensitised as they encompass growth and risk Source: Abercrombie & Co Analysis assumptions. Given 81% of TLS’s DCF valuation is stored in the terminal value, the share price is extremely sensitive to its terminal WACC and TGR assumptions (See: Appendix 11). Scenario: We conceived bull and bear scenarios that varied our valuation inputs based on the TPM-VHA merger Diagram 24: Monte Carlo Output outcome and success, TLS’s competitive positioning in the mobile/5G space, and the disruptive impacts of the NBN. The analysis reveals that our bear scenario renders a share price of $1.98, a 38% discount to the current price, whilst our bull case renders a share price of $3.53 (10% premium to market) (See: Appendix 17). Monte Carlo Simulation: The 10,000 simulations presented a probability-weighted depiction of bull and bear scenarios conceived above. By altering churn, ARPU and growth rate assumptions, we found a price target range of $2.10 - $3.55 with 90% certainty. The simulation reveals 72% of the potential outcomes are less than the current share price, resulting in a sell recommendation. Firm Specific Risks [F1] TLS Successfully Defends Its Market Share (Low Likelihood, Moderate Impact) Source: Abercrombie & Co Analysis Optus downside represents upside risk to our sell recommendation. Given subscriber growth is a key Diagram 25: Impact of Risk on driver of TLS’s mobile revenue, the upside risk will be material if it minimises growing attrition rates. While $4.00 Base DCF Value Optus appears confident that it can continue to increase subscription for its exclusive football streaming service, its World Cup streaming failure meant it could recoup little of its exclusive license for the World $3.00 Cup and the negative publicity would disincentivise TLS customers to switch. $2.00 Impact on Valuation: In this bull-case scenario, our analysis suggests that TLS’s churn in the mobile segment could decrease from 10.9% to 9.5% (FY18-19). Further, this will keep subscriber growth from $1.00 declining and TLS’s subscription will hold at 4% in FY19. This poses 2.4% upside to our base case DCF. $0.00 Mitigant: We believe Optus’ monopoly over international soccer in Australia, and better quality and quantity of viewing times (over SBS), will differentiate it from other phone/broadband bundling products. F F1 F2 1 2 1 2 M M C C C D [F2] Growth Risk - Telstra Enterprise (Medium Likelihood, High Impact) se Ba Source: Abercrombie & Co Analysis Any accelerated performance in TLS Enterprise will force upward share price revision. All telcos have been trying to pivot away from a ‘pure’ telco and avoid the fate of becoming ‘old pipe’ networks with Diagram 26: Investment Risk negligible other revenue streams. Success of business-related applications, 5G related business Matrix innovations and uptake of TLS’s Programmable Network which links all corporate solutions inside/outside High Impact on TLS in the of Australia serves as a risk with high impact. It derives value as an ‘optionality’ for underlying network capabilities and offers potential for TLS to adopt the trading multiple of an evolving tech company. Next Year M1 F2 Impact on Valuation: The growth of enterprise solutions could drag TLS out of a competitive commercial environment. We forecast Data and IP and NAS segment EBITDA growth to sustain revenue growth of 10% and 30% respectively from FY20-23. This poses 35.7% upside to our DCF value. Taking EV/EBITDA multiples of enterprise focused firms gives a valuation at 96% premium to the relative valuation. C1 Mitigant: We hold that TLS’s offerings in Enterprise will remain secondary to its core business as (1) the F1 10% margins are lower than the 40% earned in mobile and (2) the bureaucratic structure and multitude of offerings limits its manoeuvring ability relative to smaller start-ups. M2 Competitor-Based Risks C2 [C1] Merger Falls Short (Moderate Likelihood, Moderate Impact) If TPM-VHA accepts price stability, it reduces pressure on TLS’s mobile revenue, raising ARPU with an equilibrium state of 3 main telcos. This would greatly impact our valuation, as it quells the anticipated High Likelihood of Realising price war that TPM’s entrance into mobile with $0 unlimited data plans ($10 after 6 months) was expected in the Next Year 9 Source: Abercrombie & Co Analysis

You can also read