Horizons MARCH 2018 01 | - FROM THE EDITORIAL TEAM - HubSpot

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Horizons

CLIPPERMARITIME

C O N TA I N E R MARCH 2018

01 |

FROM THE EDITORIAL TEAM

02 |

GLOBAL OUTLOOK

03 |

TRADE LANE REPORTS

04 |

FLEET & VESSEL CASCADE

05 |

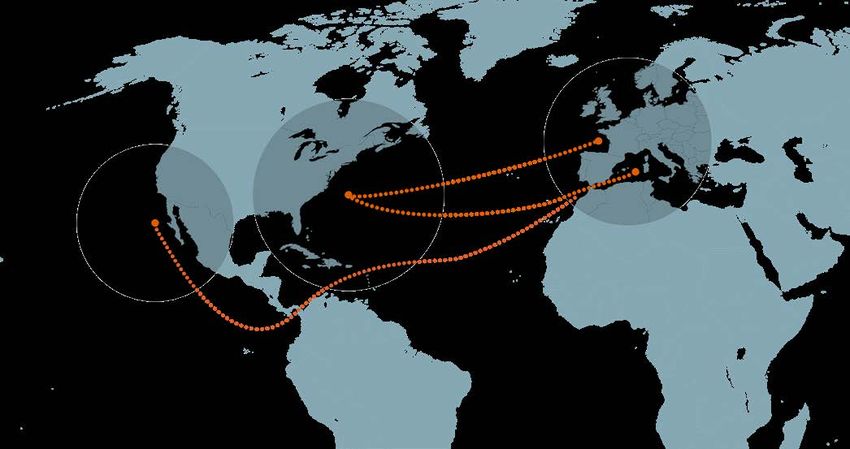

TRUMP –

WHAT’S THE BIG DEAL?

CLIPPERMARITIME Horizons

01

Contents

FROM THE EDITORIAL TEAM 03

02 GLOBAL OUTLOOK 04

03 TRADE LANE REPORTS 07

East-West

3.1: Asia-North Europe 08

3.2: Asia-Mediterranean 15

3.3: Transpacific-Asia-West Coast North America 22

3.4: Transpacific-Asia-East Coast North America 29

3.5: Transatlantic-North Europe / Mediterranean-North America 36

North-South

3.6: Asia-East Coast South America 42

3.7: Asia-West Coast South America 48

04 FLEET & VESSEL CASCADE 55

05 TRUMP – WHAT’S THE BIG DEAL? 63

06 APPENDICES & GLOSSARY 71

022

INTRODUCTION CLIPPERMARITIME Horizons

01

From the

Editorial team

After a successful launch in February 2018, the may strike, the impact of tariffs being placed on demand changes in key trade routes, including from

team at ClipperMaritime would like to thank the industrial metals in the US, are all factors that are Asia to North America, and addressing the latest

many subscribers from ports, terminal operators, going to impact international trade – and with it, the impact of the fleet and vessel cascade, we have

ocean carriers and the supply chain community that readership of Horizons. provided an assessment of this dynamic.

have kindly offered constructive and helpful feedback

Supply chain networks had been growing more We have seen that trade agreements are an

and comments.

global over time, and China’s entry into the WTO important facilitator of trade although it remains

One very interesting question received from the Port in 2001 greatly accelerated the addition of more necessary to consider other factors, such as the

of Montreal concerned how a free trade agreement far-flung nodes to these networks. Now, other level of development of a country, the state of the

can be quantified and what impact it might have emerging economies - Vietnam and Indonesia are international economy, commodity prices, exchange

on trade. On the back of Montreal seeing growth of the current stars - are fueling the growth in global rates and technological changes. Clearly, all factors

over 6% in 2017, and with January 2018 container trade, especially since 2008. Cheap labour and of interest to ports and shipping who help support the

handling volumes 11.7% higher than January 2017, access to raw materials have made these economies container supply chain globally

the future impact of CETA is an important factor as competitive, but it is the growth in global consumption

If, like the Port of Montreal, there is a topic of interest

the port continues to develop its facilities. that provides the pull maintaining the momentum.

impacting our industry that you feel would benefit the

With CETA provisionally effective from September So, what is the impact of a free trade agreement or growing and diverse readership of our publication,

2017, this is already an important and valid question. a tariff on products and on the container shipping please let us know. We welcome your thoughts at

Indeed, the threat to NAFTA, the fall-out from industry? Well, in addition to us providing a monthly horizons@clippermaritime.com and look forward to

BREXIT and its replacement by other deals the UK global outlook for the industry and outlining supply- hearing from you.

03

CLIPPERMARITIME Horizons

02

Global

Outlook

4

GLOBAL OUTLOOK CLIPPERMARITIME Horizons

Supply overview THE Alliance 13%.

Demand overview

• In late 2017, an estimated 1.6 million TEU was due Mexican volumes have been factored into our

to be delivered in 2018, but approximately 300,000 Asia to WCSA trade analysis which brings

TEU of this total has been delayed into 2019 as • For the seven trade lanes reviewed in this report, indicative head-haul load factors up to 60%.

carriers fear the impact of overcapacity. total loaded import and export TEU increased by

9% YoY in January 2018. • Our demand forecasts for 2018 point to

• New services have been launched (or are about continued growth. The two Asia to European

to be) in key East-West trade lanes by HMM, SM • For the head-haul trades covered in this report, trades lie between the 2-4% range with Asia

Lines and APL. We believe these are primarily for exports out of Asia grew by 8% YoY with South East to ECNA growth potentially reaching double-

individual company strategic reasons. Asian exports showing the fastest growth of 14%. digits for a second year. Risks remain later in

• European import flows were surprisingly quite weak the year if the East Coast port contracts are

• Two new Asia to WCSA services will be launched in

in January, down 1% YoY – in stark contrast to the not successfully concluded and we will monitor

2Q18 due to the regulatory re-structuring required

16% growth in volumes into North America. This trade flows carefully. The two trades from Asia

by Maersk Line’s acquisition of Hamburg Sud.

transpacific growth was driven by a 28% YoY surge into Latin America have recovered well in 2017,

• Largest vessel Maersk Line Hangzhou 15,282 TEU in flows to the US East Coast and highlights the but previous years of weakness must be put into

deployed on 2M’s pendulum service covering Asia strength of the pre-Chinese New Year cargo surge context. We are forecasting growth of 7-8% for

to North Europe and WCNA, but service will now be on this lane compared to the European trades. these routes in 2018.

de-coupled keeping smaller 13,500 TEU units in the

transpacific trade. • Indicative load factors on the head-haul trades are

higher than in November 2017 and in our last report

• New orders are being focused on 11,000 TEU due to the spike prior to Chinese factory shutdowns.

vessels and some are appearing in the Latin

American trades – these may now be replacing

smaller 8,000 TEU units which in turn will need re-

deploying in other trade lanes. A risk for shipowners

TRADE LANE STATUS - JANUARY 2018

and other trades. Trade No. Monthly Monthly Indicative Base Demand Ocean Carrier

Lane Operators Demand Nominal Nominal Forecast 2018 Short-Term

• Our latest assessment of the cascade highlights (TEU) Supply (TEU) Monthly Load Outlook

Factor (%)

that four Asia to North Europe strings will start to be

upgraded with another 14 ships of at least 18,000 Asia-ECSA 12 135,324 122,292 100% 7.0%

TEU in 2018, pushing out smaller 13-14,000 TEU

Asia-Med 13 543,550 632,546 86% 3.5%

vessels into the Asia-Mediterranean, transpacific

Asia-North Europe 12 920,201 1,173,842 78% 2.5%

and Asia to Mid-East trades. Despite pushing some

ships into 2019 delivery, the Ocean Alliance is most Asia-ECNA 14 638,162 693,413 92% 10.0%

affected by the orderbook and will have the largest Asia-WCNA 18 1,079,981 1,318,478 82% 4.0%

impact at the trade route and service level. Asia-WCSA 15 190,560 319,719 60% 8.0%

• An estimated 90% (by capacity) of ships over Transatlantic

16 402,695 648,579 62% 6.0%

10,000 TEU in the current orderbook are for the (ECNA & WCNA)

three major alliances. Ocean Alliance has the Load factors are indicative only based on nominal supply and do not account for wayport,

largest share (56%), followed by 2M (23%) and out of scope or deadweight adjustments.

05

GLOBAL OUTLOOK CLIPPERMARITIME Horizons

Key takeaways REGIONAL SUMMARY LOADED TEU (IMPORT/EXPORT),

JANUARY 2018/2017

• New service launches are mainly driven by individual

strategies and trade route re-structuring and the

remaining primary global operators are unlikely to

launch new strings in any key lane right now.

• The transpacific contracting season is imminent and

cargo owners will be signing new agreements from

May / June. From our cascade model, we see more

capacity entering the two key lanes this year and

into 2019. Together with increasing US intermodal

costs and current spot market conditions, we believe

these will help dampen the prospect of significant

rate increases for shippers.

• For the short-term, our trade lane indicators remain

quite positive judged on the existing supply/demand

balance. The two transpacific, trans-Atlantic and Asia

to ECSA lanes are green with strong recent demand

growth in evidence. However, the transpacific lanes

are certainly at risk from both additional capacity and

geo-political factors (US protectionism).

SUPPLY AND DEMAND OVERVIEW - MONTHLY TEU

JANUARY 2018

• The two primary Asia to Europe trades are not in

serious danger, but newbuild deliveries will continue

to be deployed in these routes throughout 2018

which will add pressure. The second cascade will

push larger vessels into the Mediterranean. The

fundamentals on the Asia to WCSA trade remain

strong for now, but capacity will be increased in the

immediate future and this will change the dynamics

for the worse.

• Our analysis of the impact of some Free Trade

deals that have been signed on overall trade flows

provides a mixed view on the relative success before

and after the deals were signed.

Actual supply (Bar) Supply forecast (Bar) High demand forecast

Actual demand Trend demand forecast Low demand forecast

Data refers to trade lanes analysed in this report-basis nominal TEU capacity and loaded TEU demand

06

CLIPPERMARITIME Horizons

03

Trade Lane

Reports

7

TRADE LANE REPORTS CLIPPERMARITIME Horizons

Asia–North Europe

Ocean carriers have minimised spot freight rate erosion,

but capacity increases are expected.

S U P P LY

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+13% +15%

DEMAND

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

-4% +7%

OCEAN CARRIER

SHORT-TERM OUTLOOK

08

TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Supply/demand balance and forecast

Alliances preparing for Q2 Section 4 Fleet & Vessel Cascade outlines that

around 400,000 TEU in total is due to be delivered

• Weekly nominal capacity to rise by 10%, with anot-

her five ships in the series due by the end of 2018.

network changes – demand after from the orderbook during 2Q18, which includes

Cosco

another eight ships of 20,000 TEU – all of these

Chinese New Year will be crucial. units will head into this trade. • A 20,000 TEU and 19,000 TEU ship will replace two

13,386 TEU vessels in the Alliance’s FAL2 service

In March 2018, the head-haul nominal monthly The seven ships of this size delivered up until the

in early April 2018.

capacity between Asia and North Europe was 1.2 end of February did not cause freight rates to crash

million TEU compared to 1.1 million TEU recorded as carriers voided a number of vessels during • Increased weekly nominal capacity estimated to be

for March 2017. With Chinese New Year falling later Chinese New Year. over 17% compared to Q3 2017.

in mid-February 2018, ocean carriers did not void The head-haul Asia to North Europe trade performed

Current vessel upgrades will up the pressure in the

sailings until well into February. well in 2017, although container flows in 2018 started

trade lane. This view is further reinforced by Ocean

The anticipated disruption likely to be caused by Alliance activities: rather weakly:

newbuild deliveries is yet to be factored into liner • January 2018 recorded 920,000 TEU, compared to

Evergreen

operating dynamics. 953,000 TEU for January 2017 – a decline of 3.5%

• The first 2 x 20,000+ TEU ships to be phased

and surprising given that Chinese New Year fell in

into Ocean Alliance FAL7 service in April and

mid-February.

June, respectively - a further nine units due in

2018 and seven in 2019. • Volumes in January 2018 were stronger than

Demand outlook and 2018 forecast December 2017 – up by 2.0%. This is in line with

the usual pre-CNY cargo surge.

Total volumes on the head-haul trade

reached just over 10 million TEU in 2017, a ASIA-NORTH EUROPE SUPPLY/DEMAND BALANCE AND FORECAST

4.1% rise on 2016. Our statistical analysis

of the last five years suggests a trendline

for this year of minus 1.9% which is skewed

by the recent weak figures for December

and January. Our 80% confidence interval Actual supply (Bar)

suggests a range of between minus 9% Actual demand

and plus 5.6%, but our latest assessment Supply forecast (Bar)

remains that growth will lie within the 2% Trend demand forecast

to 3% range. Ocean carriers are trying High demand forecast

to manage supply/demand balance by Low demand forecast

delaying the delivery of a number of ULCVS

till 2019.

NOTE: TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018

09

TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Supply/demand Supply

balance and Little change in March 2018, • Hamburg is also on the North Europe schedule.

forecast (cont.)

• Colombo to be utilised – to maximise regional

although “independent” HMM transhipment opportunities.

service confirmed. While the obvious conclusion here is that the

The lead-in to the Chinese New Year was strong with vessels are too small, HMM will not experience the

most major lines experiencing full ships (load-factors economies of scale enjoyed by its competitors. The

The early months of 2018 have seen little change in plan is regarded as a little optimistic, but an objective

of over 95% were recorded), with reports of small terms of vessel deployment:

pools of cargo rolling over in Asia to the next sailing. assessment will note the following:

This has helped to fill vessels and push up load • Largest ship size in March 2018 is 21,413 TEU – • With the demise of Hanjin in 2016, the presence

factors in early March after the Chinese holiday period same as in January/February 2018 of a strong and reliable South Korean shipping

finished and has helped keep spot freight rate erosion • Average ship size for March 2018 of 14,730 is a line with global coverage for shippers is very

to a minimum. minimal increase on the position at start of year important at both a strategic and political level.

Last year finished weak, with the SCFI reporting (of 14,696 TEU). • The new weekly AEX service is an opportunity

head-haul spot rates at $864 per TEU, against $1,200 • Number of ships in service has risen marginally for HMM to assess the viability of a longer-term

at the end of 2016. Ocean carriers have had some – from 199 in January/February 2018 to 201 for return to the key Asia to North Europe market as a

success improving rates in Q1 2018: March 2018. vessel deployer, rather than a mere slot charterer,

• January 2018 four-week average at $896 per TEU with the objective of providing BCO shippers

New HMM vessel deployment was verified on this

– a 3.6% rise over year end 2017. better assurances that it has the ability to cater for

key trade route in March 2018 (via PR News), with

their shipping requirements.

• February 2018 four-week average at $912 per the following reported:

TEU – a 1.8% increase over the January 2018 • The ships to be deployed are small enough that

• AEX string to be launched in April 2018 –

average. they will not impact the short-term spot freight

an independent service offered outside the

rate market, While slot costs for HMM will be

However, any pick-up immediately after the Chinese agreement with 2M Alliance.

expensive, ships are likely to be chartered at low

holidays was not reflected in improved spot freight • Loop to be operated with 10 x 4,600 TEU ships daily rates of well under $10,000.

levels which by mid-March fell to $741 per TEU, (owned and chartered vessels).

the lowest recorded in 2018 so far. Ocean carriers • HMM does not need to aggressively under-bid

are seeking GRIs from April (CMA CGM’s FAK rate • First sailing leaves Busan on 9 April – ship size of competitors since it is already an existing operator

of $900 per TEU is an example), but this will be 4,728 TEU. in many major trades and will secure some former

challenging to achieve due to newbuild deliveries Hanjin business quite naturally – although not at

• First inbound port is Rotterdam (World Gateway)

and the revamped Alliance networks becoming the rate it did in 2017.

on 9 May, last outbound call from Felixstowe on

operational. Rising bunker costs are adding to the 15 May, 2018.

squeeze for ocean carriers, which are struggling to

ensure that fuel costs are factored into the rates.

10TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Supply

MONTHLY STANDING SLOT NOMINAL CAPACITY (MILLION TEU), OPERATOR SHARES AND MAJOR TRADE LANE SUPPLY DETAILS

APR 17 MAY 17 JUN 17 JUL 17 AUG 17 SEP 17 OCT 17 NOV 17 DEC 17 JAN 18 FEB 18 MAR 18

Maersk Line

MSC

Hapag-Lloyd

Cosco

CMA CGM

Average TEU 15,010 14,971 14,989 14,833 14,828 14,783 14,585 14,926 14,450 14,778 14,216 14,230

Max TEU 21,100 21,100 21,100 21,100 21,100 21,413 21,413 21,413 21,413 21,413 21,413 21,413

# deployed vsls 187 193 194 195 201 203 199 199 199 202 199 201

# services 17 18 18 19 19 19 18 18 18 18 18 18

• The new service will also help prepare HMM for • Present eight vessels to be increased to nine – • AE2/Swan – average weekly capacity of 18,900

future expansion plans. The company is poised although smaller units of 5,000 TEU to remain in TEU

to order a series of 20,000 TEU ships from South service.

• AE6/TP6/Lion/Pearl – average weekly capacity

Korean yards for 2020 delivery, but it certainly will

Despite the cessation of the Thailand origin call, the 13,500 TEU.

not be able to fill these ships by itself. After the

continuation of the service indicates that the operator,

current deal with the 2M lines expires in 2020,

CMA CGM, remains confident that targeting the

HMM will become more attractive as a potential

South East Asian market with smaller vessels and

partner of THE Alliance member lines.

a fast transit into North Europe remains a robust

It was reported in the February edition of Horizons strategy. However, a weak rolling 12 month volume

that the SEANES service operated by CMA CGM growth out of Thailand remains a warning for the

was using small ships and some changes were ocean carrier.

anticipated.

The number of void sailings in early 2018 was spread

The Ocean Alliance has now confirmed the following: amongst all Alliances - 2M (3 services), Ocean (4

services) and THE Alliance (3 services).

• New port rotation – Laem Chabang and Tangier

Med dropped, but Yantian, Le Havre, Algeciras However, in late February only the following had

and Beirut added. been reported for week 9 by 2M Alliance:

11TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Demand

Germany and UK volumes flat, In 2018 the UK economy is expected to slow as public

spending cuts and uncertainty over BREXIT continue,

In 2017 the port saw total box volumes rise by 24%

to 1.6 million TEU, supported by the introduction of

but Poland to see good growth, although inflation remains on track to fall to the Bank of the new T2 facility.

England’s 2% target.

again. The port is actively seeking to increase its share of

Yet, volume demand is likely to stay flat, as seen by non-transhipment traffic, and the country’s economic

China continues to represent the major source of the February 2017 to January 2018 trade from China position in 2018 should assist this process.

loaded imports into North Europe for the period falling by 0.6% (to 1.65 million loaded TEU).

Current EC forecasts predict that 2017’s 4.7% GDP

February 2017 to January 2018, and is considerably

Similar trends were noted for Germany over the same growth in 2017 will be about matched this year with

larger than all other origins combined:

period: 4.2% expected due to good domestic demand and

• China - 7.3 million TEU in total, but by sub-region: public investment fully recovered from the decline of

• Loaded containers from Asia were down 2% to 1.8

2016.

• PRC East – 3.9 million TEU, up by 6% million TEU

The ability of DCT Gdansk to continue to receive

• PRC South – 1.9 million TEU, down by 2.5% • China to Germany cargo flows declined 1% to 1.3

some of the largest container ships in service

million TEU.

• PRC North – 1.5 million TEU, a rise of 5% remains a crucial factor of the port’s competitiveness.

However, the European Commission (EC) is predicting

• South Korea – 524,000 TEU, a rise of 8%

that the German economy will see slightly faster GDP

• Vietnam - 498,000 TEU, an increase of 5% at 2.3% in 2018 (up on the 2.2% in 2017), driven by

strong private consumption, higher investment and

For the leading destinations in North Europe from

growing foreign demand.

Asia, UK growth remained flat, while the East Europe

region continues to see higher growth, consistent Yet, one of the country’s leading container ports,

with the position reported in the February edition of Hamburg, continues to struggle with draught

Horizons, as the following number show: restrictions due to dredging issues, and trade flow for

the Baltic and Russia is drifting away, primarily to DCT

• UK – 2.2 million TEU – negligible growth

Gdansk in Poland.

• Netherlands – 1.7 million TEU – up by 3%

Loaded container demand for Poland did increase by

• France – 677,000 TEU – rise of 10% 16% to 666,000 TEU in the February 2017 to January

• Poland – 666,000 TEU – strongest increase, 2018 period, which is primarily due to the successful

with 16% growth of DCT Gdansk( helped by two direct calls from

2M and Ocean Alliance lines).

• Russia – 564,000 TEU – improvement of 10%

12TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Demand

TOP ROUTES BY VOLUME, TOP ORIGIN COUNTRIES,

GROWING / DECLINING ROUTES TOP DESTINATION COUNTRIES

TOP ROUTES BY VOLUME TOP ORIGIN COUNTRIES BY VOLUME

TEU %YoY TEU %YoY

China to United Kingdom 1,653K -0.6% PRC East 3,941K 5.9%

China to Netherlands 1,270K 4.0% PRC South 1,922K -2.5%

China to Germany 1,341K -0.9% PRC North 1,407K 4.8%

China to France 540K 12.8% Vietnam 498K 4.8%

China to Poland 520K 16.4% South Korea 522K 7.1%

China to Belgium 517K -0.3% Thailand 316K -0.9%

China to Russia 317K 3.2% Malaysia 232K 12.3%

China to Sweden 231K 4.9% Indonesia 249K -0.4%

China to Denmark 173K 9.1% Japan 264K -6.5%

Vietnam to Germany 106K -4.1% Taiwan 206K -10.4%

TOP GROWTH ROUTES TOP DESTINATION COUNTIRES BY VOLUME

TEU %YoY TEU %YoY

China to Lithuania 59K 22.4% United Kingdom 2,164K 0.1%

South Korea to United Kingdom 49K 22.0% Netherlands 1,742K 2.7%

South Korea to Russia 106K 20.9% Germany NWC 1,836K -2.1%

China to Poland 447K 16.4% Belgium 805K 0.9%

China to France 479K 12.8% France NWC 677K 9.8%

Poland 666K 15.5%

ROUTES IN DECLINE Russia 564K 9.9%

TEU %YoY Sweden 310K 5.8%

Indonesia to Germany 55K -4.5% Denmark 221K 8.4%

Vietnam to Germany 106K -4.1% Finland 139K 2.1%

Thailand to Netherlands 67K -3.1%

China to Norway 88K -3.1%

China to Germany

13

1,341K -0.9%

TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–NORTH EUROPE

Cascade

• We anticipate operators upgrading several services to c.20k TEU

over the course of 2018: these include 2M’s Condor, and the NEW BUILD / EXISTING FLEET BREAKDOWN OPERATOR SHARE TODAY

Ocean Alliance’s FAL1, FAL2 and FAL7. This is emphasised by (STANDING SLOTS TEU)

CMA CGM as it deploys the newly delivered CMA CGM Antoine

de Saint Exupery to its flagship service with two similarly sized

units due to follow within the year.

• String upgrades are also impacted by the specific geographies of

their rotations. In last month’s edition of Horizons, we highlighted

the differing growth rates of volumes between Northern, Central,

and Southern China (slower growth in the North): the Ocean

Alliance’s FAL3 which serves this northern region and currently

operating with an average of c.13k TEU, is therefore less likely

to receive the 20k ULCVS in the orderbook than routes calling CASCADE BY VESSEL VOLUMES

further south.

• Similarly, THE Alliance has two weekly services (FE1 and FE5) OPERATOR SHARE MARCH 2021

focused on the relatively small Japanese and South East Asian (STANDING SLOTS TEU)

markets. Despite its member lines’ 14,000 TEU newbuild orders,

they will not necessarily move straight into these services without

significant port call restructuring.

• These South East Asian trades are potentially at risk from the

imminent influx of capacity from new build deliveries to the North

Asia routes creating empty headhaul slots. With bunker costs

increasing the value of consolidating the moves currently served

by dedicated South East Asia – North European destinations

is increased. The only factor offsetting these benefits is the CASCADE BY OPERATOR

time-sensitivity of goods as adding calls to the main North

Asia – North Europe strings would inevitably add two to three

days to headhaul voyage durations. We will be monitoring the

supply:demand balance closely over the coming months to

provide further comment on this in due course.

• Directly resulting from new build activity, we see Maersk Line’s

market share cut to 19% and Evergreen entering the top 5

operators in terms of TEU deployed thanks to 16 deliveries

between now and 2021.

14TRADE LANE REPORTS CLIPPERMARITIME Horizons

Asia–Mediterranean

Cargo growth will be needed as trade prepares for

new Alliance networks and upgraded vessels.

S U P P LY

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+4% +5%

DEMAND

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+3% +7%

OCEAN CARRIER

SHORT-TERM OUTLOOK

15TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Supply/demand balance and forecast

Spot freight rates continue to For 2018, the key anticipated developments will focus

on the following, both of which represent potential

• The indicative trade lane load factor of 86% for

January 2018 was robust moving into the Chinese

trend below Asia to North Europe pressures on the supply-demand balance and spot New Year factory shutdown period

freight rates:

levels – but gap is narrowing. The trade route entered 2018 with SCFI head-haul

• Direct vessel deployment from revised Alliance spot rates at $738 per TEU. The following trends were

Head-haul liner capacity in the Asia-Mediterranean services evident:

trades has remained fairly flat for now, but we

• The continued threat posed by the cascade. • January 2018 four-week average of $758 per

anticipate this changing later in the year, and the trade

TEU.

receives larger vessels via the cascade. Based on the most up-to-date information available,

head-haul loaded container demand started positively • February 2018 four-week average of $794 per

• Total monthly nominal head-haul capacity in

in 2018: TEU.

March 2018 was 637,000 TEU – by comparison

March 2018 stood at 615,00 TEU • January 2018 demand was 544,000 TEU, up by These spot rates were higher than the $738 per TEU

2% on the 532,000 TEU for December 2017 and at the end of 2017, but were still around 20% lower

• The number of operational weekly services has

by 4% over the January 2017 total of 524,000 than a year ago. By mid-March, there was further

also remained constant, at 13.

TEU. erosion of rates to $665 per TEU as volumes had not

• Largest vessels in service have increased, but picked up after the factory shutdowns.

only marginally, from 16,652 TEU in March 2017

to the current 16,810 TEU (2M upgrading its Jade

service).

Demand outlook and 2018 forecast

ASIA-MEDITERRANEAN SUPPLY/DEMAND BALANCE AND FORECAST

Total volumes on the headhaul trade reached

5.87 TEU in 2017, a strong 5.3% uplift on

2016. Our statistical analysis of the last five

years suggests a trendline for this year of Actual supply (Bar)

2.8% with our 80% confidence interval giving Actual demand

a range of between minus 6% and plus Supply forecast (Bar)

11%. Our view is that demand growth in the Trend demand forecast

range of 3-4% can still be expected and the High demand forecast

momentum for the largest sub-trades into Low demand forecast

the Western Mediterranean and also Turkey

remain positive.

NOTE: TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018

16TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Supply/demand Supply

balance and Ocean carriers preparing • Other major providers of slots in March 2018 are

forecast (cont.)

CMA CGM (0.14 million TEU), Yang Ming (0.13

to introduce new Alliance million TEU) and Cosco (0.12 million TEU).

networks - trade remains at • In addition, Hapag Lloyd, Evergreen, Zim, K

Line and NYK Line are also active, but did not

The trend of spot rates being noticeably below risk from cascade. introduce any capacity adjustments in Q1 as

they wait for changes in Q2 when new Alliance

those in the much larger Asia to North Europe trade

have been in evidence since mid-2017 and there structures become operational.

are no immediate signs this will change moving into The Asia-Mediterranean trades continue to be split

into several sub-regions and liner networks build As identified in the February edition of Horizons,

Q2 2018. But the gap has narrowed a little mainly both THE Alliance and Ocean Alliance will amend

because North Europe rates have fallen faster during services around calls to both the West Mediterranean

and East Mediterranean (which includes the Adriatic their service in April 2018, although specific vessel

the Chinese New Year holiday. deployment details remain scarce:

and Back Sea areas) separately.

• Start of January 2018 difference - $150 per TEU • THE Alliance will offer three services, all

There is also a heavy use of transhipment in both

• Start of March 2018 difference - $106 per TEU sub-regions, and this enables operators to utilise commencing in the first week of April:

As 2018 progresses, gateway ports in the Central larger vessels making fewer calls and then onward • MD1 – links China and South Korea,

Mediterranean in particular, will continue to target feedering. However, the desire for direct calls also via Singapore, with West Mediterranean

cargo destined for Central European hinterlands. This remains, especially at ports that are able to offer (including Tangier-Med) ports of Barcelona

ocean carrier strategy is vital if upgraded ships are to good import-export cargo demand, such as at and Valencia, plus inbound/outbound calls

be filled on this route. Valencia (Spain), or Piraeus (Greece). at Damietta. Pusan, Hong Kong and Tangier

In terms of how the trade is developing on an Med are new calls.

individual liner basis, key conclusions from Q1 2018 • MD2 - from China and South Korea,

include: via Singapore, to Central and East

• MSC remains the biggest provider of TEU slots, Mediterranean, with calls at Piraeus, Genoa,

with 0.45 million in March 2018, showing a slight La Spezia and Fos. Here Qingdao, Shekou,

increase on its offering in January/February 2018. Fos and inbound/outbound calls at Piraeus

are new calls.

• Maersk Line’s total monthly slots are 0.20 million

TEU in March 2018, although this is a very small • MD3 – is focused on the East Mediterranean,

rise on the 0.19 million TEU for January/February with South Korea and China, via Singapore

2018. Collectively, 2M has a dominant share on and stops at Jeddah, then calling to Ashdod,

the route and deploys the largest vessels Ambarli, Izmit, Izmir and Mersin. Shekou and

Izmit represent new port calls.

17TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Supply

MONTHLY STANDING SLOT NOMINAL CAPACITY (MILLION TEU), OPERATOR SHARES AND MAJOR TRADE LANE SUPPLY DETAILS

APR 17 MAY 17 JUN 17 JUL 17 AUG 17 SEP 17 OCT 17 NOV 17 DEC 17 JAN 18 FEB 18 MAR 18

MSC

Maersk Line

Cosco

CMA CGM

Yang Ming

Average TEU 10,369 10,493 10,669 10,519 10,629 10,914 10,658 10,499 10,900 10,540 10,112 10,548

Max TEU 16,652 16,652 16,652 16,652 16,652 16,652 16,652 16,652 16,652 16,810 16,810 16,810

# deployed vsls 134 141 140 139 139 140 140 140 140 140 140 140

# services 13 13 13 13 13 13 13 13 13 13 13 13

As the new service patterns are introduced, and the • Tangier- Med recorded a 12% increase in While the selection of ports of calls could change,

potential for further vessel upgrading is guaranteed 2017 total volumes, to around 3.3 million TEU, liner investment in facilities (whether directly or

via the cascade, successful ports will be those supported by both Maersk Line and CMA CGM through sister companies, such as APM Terminals

facilities (in all sub-regions) that can accommodate who together offer nine weekly services (across a / Maersk Line both part of the AP Moller Group) will

larger ships through a combination of water depths range of trade routes). play a significant role in dictating rotations and cargo

and infrastructure. Terminal ownership remains an flows. This will not change, irrespective of vessel

The terminals are able to cater for the largest

influencing factor too. For example: deployment or service upgrades.

ships in (and entering) service.

• Cosco subsidiary, PCT, operates container

• Other examples include CMA CGM

terminals at Piraeus, so in Q1 the line has been

concentrating its Central Mediterranean hub port

making regular calls with six different services in

focus at Marsaxlokk, MSC developing Asyaport

which it operates vessels. The port can receive

in Turkey and Maersk Line supporting East Port

ships of 20,000 TEU.

Said at the Eastern Mediterranean entrance to the

Suez Canal.

18TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Demand

Asian demand growth continuing • Spain volumes were 821,000 TEU, up by 4%, with

China continuing to provide a dominant 78%.

– locations in all sub-regions • Mediterranean French ports handled 343,000

benefitting. TEU, a rise of 5% - China is, once again,

dominant as it represented 76% over the period.

Chinese loaded container demand in the February

The European Commission expects Italy’s GDP

2017 to January 2018 period grew, while activity from

growth in 2017 of 1.5% to be matched in 2018, and

both South Korea and Vietnam also increased:

stated that the economy will become more self-

• Total demand from China reached 4.1 million sustaining, if somewhat limited in growth potential.

TEU, comprising: The fragile banking system remains a concern too.

• PRC East – 2.2 million TEU, up 6% The country’s ports will hope that key initiatives,

such as Contship Italia Group’s efforts to extend

• PRC South – 1.1 million TEU, marginal

hinterlands into Central Europe, southern Germany

increase of 1%

and locations such as Switzerland continue to gain

• PRC North – 849,000 TEU, a rise of 2% momentum.

• South Korea – 569,000 TEU, up by 5% For Turkey’s economy, the OECD is projecting a drop

• Vietnam – ships less than other countries at on the 7% GDP growth gained in 2017, but only to

194,000 TEU, but this up by 13% around 5%. In 2017, the government injected more

funds into the economy, and exports recovered, but

In terms of leading country destinations for Asian business and consumer confidence continue to lag in

loaded container demand, the market in the 2018.

Mediterranean is highly established, but will remain

split amongst West, Central and East sub-regions: The country’s ports compete with others in the

region, but for the highly competitive transhipment

• Italy is the largest market – 1.01 million TEU market, using larger ships, the ability to offer import-

(+2.8%) in the February 2017 to January 2018 export demand will remain crucial.

period, of which China accounted for 73% and

demand growth of 4.1%.

• Turkey is the second largest destination – 878,000

TEU (+7.2%) over the same period, which means

the volume growth has picked up favourably in Q4

2017 and into 2018. Chinese share is 54%, with

South Korea seeing higher growth of 12.6% to

132,000 TEU.

19TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Demand

TOP ROUTES BY VOLUME, GROWING / DECLINING ROUTES TOP ORIGIN COUNTRIES, TOP DESTINATION COUNTRIES

TOP ROUTES BY VOLUME TOP ORIGIN COUNTRIES BY VOLUME

TEU %YoY TEU %YoY

China to Italy 736K 4.1% PRC East 2,187K 5.6%

China to Spain 639K 4.8% PRC South 1,088K 0.5%

China to Turkey 474K 2.1% PRC North 849K 2.2%

China to France 259K 3.8% South Korea 569K 5.4%

China to Israel 261K -6.9% Vietnam 194K 12.9%

China to Algeria 226K -16.6% Thailand 209K 4.0%

China to Ukraine 188K 17.3% Malaysia 148K 10.9%

China to Slovenia 179K 15.6% Indonesia 152K 4.5%

China to Egypt 158K -11.6% Japan 152K -2.2%

China to Greece 164K 7.3% Taiwan 119K -3.9%

TOP GROWTH ROUTES TOP DESTINATION COUNTRIES BY VOLUME

TEU %YoY TEU %YoY

Malaysia to Turkey 44K 18.5% Italy 1,010K 3.8%

China to Romania 91K 18.0% Turkey 878K 7.2%

China to Ukraine 160K 17.3% Spain MED 821K 3.7%

Thailand to Turkey 43K 16.2% France MED 343K 4.9%

China to Slovenia 155K 15.6% Israel 336K -6.1%

Slovenia 322K 8.0%

ROUTES IN DECLINE Algeria 289K -8.5%

TEU %YoY Egypt MED 264K -13.2%

China to Algeria 226K -16.6% Ukraine 214K 17.8%

China to Egypt 158K -11.6% Greece 201K 6.2%

China to Israel 261K -6.9%

South Korea to Slovenia 97K -4.2%

South Korea to Spain 53K -3.9%

20

TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–MEDITERRANEAN

Cascade

• The Asia – Mediterranean trade lane is impacted by both new build

deployment and secondary vessel redeployment when the largest OPERATOR SHARE TODAY OPERATOR SHARE MARCH 2021

new build vessels are allocated to Asia – North Europe services. By (STANDING SLOTS TEU) (STANDING SLOTS TEU)

2021, our analysis shows 34 vessel upgrades split evenly between

these deployment categories.

• All three major Alliances are actively varying their deployments,

specifically we envisage:

• 2M Alliance upgrading its Tiger service from c.13k TEU to 15.5k

TEU; and

• Ocean Alliance upgrading its MEX1 service from 11k TEU to 13.5k

TEU; and

• THE Alliance upgrading its MD1 service from 9k TEU to 14k TEU.

• Maersk Line is likely to strengthen its position as the second largest

operator in TEU capacity terms, increasing market capitalisation

from 13 to 19 percent, with MSC making the fewest upgrades (2x

redeployments of the MSC Venice and MSC London in the fourth

quarter of 2019 and no new build activity) resulting in a seven percent

loss of market share. However, as an alliance, 2M retains a dominant

position in this trade lane.

NEW BUILD / EXISTING FLEET BREAKDOWN CASCADE BY VESSEL VOLUMES CASCADE BY OPERATOR

21TRADE LANE REPORTS CLIPPERMARITIME Horizons

Asia–West Coast North America

Alliance stability expected, 2018 demand started strongly –

but vessel capacity upgrades expected.

S U P P LY

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+7% +4%

DEMAND

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+7% +7%

OCEAN CARRIER

SHORT-TERM OUTLOOK

22TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Supply/demand balance and forecast

Retailers replenishing stocks In early March 2018 the full impact of the Chinese

factory closures was strongly felt, and carriers must

• January 2018 total of almost 1.17 million TEU was

9% higher than December 2017 figure of 1.06

aiding short-term demand growth. be bracing for falling spot rates, especially following million TEU and 7% stronger than the 1.09 million

an increase in average ship sizes in 2017. The TEU for January 2017.

The start of a new year represents a time for anticipated cascade of vessels from current Asia-

• Indicative load factors were an estimated 85% in

replenishing of stock and inventories following the North Europe trades is expected as newbuilds from

January 2018, an increase on the December 2017

holiday season and Chinese New Year periods. the orderbook enter service, even allowing for some

ratio, but down on the 88% recorded for the same

Invariably this is followed by a drop-off in some delays from 2018 to 2019.

month in 2017 – reflecting the vessel cascade

demand into North America. This has clearly assisted

Despite the ongoing shift of container traffic from the process that occurred during 2017.

spot freight rates in head-haul Asia to WCNA routes,

West Coast to the East Coast in recent years, the

along with pre-Chinese New Year volumes and load In the February edition of Horizons, it was noted that

situation now looks to be reaching a ‘new normal’

factors (as reported in the February 2018 edition of head-haul spot freight rates started 2018 strongly,

with the West Coast now stabilising at 50% (of total

Horizons). with the $1,523 per FEU, a strong uplift on the

port handling volumes based on port statistics) for

$1,100 per FEU of the previous six weeks.

2015, 2016 and 2017 and the 1% gain (to 7%) by the

Demand outlook and 2018 forecast US Gulf Coast coming from East Coast ports (now at Indeed, compared to 2016, average weekly 2017

43% for both 2016 and 2017). rates were 20% higher, and the position remained

Total volumes on the headhaul trade positive, as the monthly averages from SCFI

reached 11.6 million TEU in 2017 (+5.6% Using our most recent (to January 2018) data, the

confirmed:

YoY) and the second successive year of following trends of head-haul loaded units can be

5% growth. Our statistical analysis of the identified:

last five years suggests a trendline for this

year of 3.5% with our 80% confidence

ASIA-WEST COAST NORTH AMERICA SUPPLY/DEMAND BALANCE AND FORECAST

interval giving a range of between -4% and

11%. Our view is that positive momentum

will continue in 2018, and annual growth

will lie within the 3-5% range. Geo-political

tension between China and the US could Actual supply (Bar)

impact trade flows, but it is too early to Actual demand

assess the severity of such a disruption. Supply forecast (Bar)

Should the negotiation of a new contract for Trend demand forecast

longshoremen on the US East Coast break High demand forecast

down in late September, this could trigger Low demand forecast

a temporary shift of cargo by shippers from

the East to West Coast.

NOTE: TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018

23TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Supply/demand Supply

balance and Further service upgrades on 6 x 4,253 TEU deployed and means a 50%

forecast (cont.)

increase in capacity. Dalian and Oakland have

transpacific WCNA routes as been dropped in favour of new calls in Prince

Rupert and Tacoma, with Los Angeles maintained

niche operator joins. in the rotation.

• January 2018 four-week average - $1,468 per • South Korea’s SM Line confirmed the launch of its

FEU. Some of the major operators in the transpacific new transpacific PNS service from mid-May 2018

WCNA trades continue to re-vamp and alter service using relatively small ships of 6 x 4,000 TEU –

• February 2018 four-week average - $1,484 per schedules, while a new entrant is also joining the 4,600 TEU. Vancouver (BC) and Seattle represent

FEU. route: the WCNA port calls, with Yantian, Ningbo,

As expected, some erosion has taken place leading Shanghai, Tokyo, Busan and Gwangyang filling

• Ocean Alliance is increasing capacity on the

into March after the Chinese New Year holiday the rotation. The operator is strategically targeting

Evergreen-operated PSW8 service, with 8,500

season, with the mid-March spot rates declining to the Pacific North West rather than the crowded

TEU ships replacing existing vessels of 7,000

$1,016, a 50% drop since the start of the year and southern California gateways of Los Angeles/Long

TEU in April and May 2018. Consequently, during

the lowest recorded weekly rate since June 2016. Beach.

Q2 2018 weekly capacity is set to rise by around

Given the strong overall cargo volume growth, this 10.5%. • HMM’s ‘premium’ services were launched in May

dynamic must be worrying for ocean carriers since 2017, PS1, PS2 and PN2, and the ocean carrier

at the moment they are heading for the dark days of • Ocean Alliance’s current PSW8 vessels will

is looking to increase its market share for the

mid-2016 when rates were stuck firmly below $1,000 switch to the PNW3 service led by Evergreen

future. The largest ships currently utilised are

per FEU. which currently uses 5,400 TEU units. Due for

6,800 TEU units - relatively small for the WCNA

completion in mid-June 2018, the change will

The annual contracting season could prove route now. Upgrading could be achieved via larger

see nominal weekly capacity in the PNW3 string

challenging for shipping lines if service changes bring ships from the charter market.

increase by almost 19%.

too much additional capacity, especially as there • APL launched a new service linking Asia, USWC

will be a need to factor in rises in fuel costs in 2018. • THE Alliance is adding 25% more weekly capacity

and Alaska. Named the Eagle Express (EEX), it

However, further positive demand growth is projected to its PS4 service during March and April 2018 by

will commence in July 2018 and offer a weekly

in this trade route for 2018. replacing the existing Yang Ming ships of 6,500

connection between the key Chinese ports of

TEU with vessels of 8,200 TEU – 8,600 TEU

Ningbo, Shanghai with Los Angeles and Dutch

capacity. The move will see an average weekly

Harbour with Yokohama and Busan. Outside

capacity of 8,300 TEU, an increase of 26% over

of the Alliance network it is focusing on US

the previous position, with Los Angeles and

Government cargo inbound to the US with the

Oakland still the two West Coast ports of call.

Dutch Harbour call handling reefer exports back

• The Alliance is launching a newly restructured to Asia. Small ships of around 2,000 TEU nominal

service, dubbed PS8, using Yang Ming’s ‘M’ Class capacity will be used, reflecting the specialist and

of 6,588 TEU vessels – these replace the existing niche nature of the routes and cargo linked.

24TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Supply

MONTHLY STANDING SLOT NOMINAL CAPACITY (MILLION TEU), OPERATOR SHARES AND MAJOR TRADE LANE SUPPLY DETAILS

APR 17 MAY 17 JUN 17 JUL 17 AUG 17 SEP 17 OCT 17 NOV 17 DEC 17 JAN 18 FEB 18 MAR 18

Maersk Line

Cosco

CMA CGM

MOL

MSC

Average TEU 7,358 7,466 7,649 7,605 7,615 7,710 7,877 7,932 7,966 8,089 7,691 7,971

Max TEU 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,568 14,000 15,282

# deployed vsls 272 273 283 283 283 283 283 284 283 284 283 286

# services 36 35 36 36 36 36 38 38 39 39 39 39

As reported in the February edition of Horizons, the • The largest ship upgrades occurred in 2017, • Maersk Line monthly standing slot capacity

largest contributor to additional supply remains the with the March 2017 figure of 13,568 TEU rising unchanged compared to one year earlier at 0.38

ongoing industry cascade, and this trend is expected to 14,000 TEU in April 2017, where it largely million TEU.

to continue. remained until March 2018. Maersk Line re-

• MSC has increased the March 2017 slots of 0.08

deployed the 15,282 TEU Maersk Line Hanoi to

In terms of the overall impact of the ongoing operator million TEU to 0.17 million TEU in March 2018,

the AE6/TP6 ttranspacific/Asia from the North

developments, the March 2018 position is: driven by vessel upgrades.

Europe pendulum loop, representing a major

• Total monthly nominal capacity of 1.23 million upgrade from the current 13,500 TEU vessels. • APL has been another major provider of additional

TEU in January 2018, a 7% increase on the In April 2018 the TP6 will be de-coupled into an slots, its 0.21 million TEU in March 2018

January 2017 position and an indication why spot end-to-end transpacific service deploying these compares with just 0.08 million TEU for March

freight rates have fallen since the beginning of the smaller vessels. 2017, reflective of network changes following

year CMA CGM’s acquisition (CMA CGM’s TEU slots

• The major transpacific WCNA operators remain

have fallen over the past 12 months). CMA CGM

• Average ship size reached 7,791 TEU in March unchanged now that the Alliance membership

and APL are now sister companies and so the

2018, 3% higher than one year earlier, when it process is resolved, and actual scheduled

combined share of the two carriers should be

stood at 7,586 TEU. services have been published and begin to

considered when reviewing trade shares.

adopt new formations. This will continue from Q2

2018, as the following dynamics at the end of Q1

represent the current position:

25TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Demand

China demand to WCNA Volumes from Thailand are growing rapidly (+14%),

but are less than half those out of Vietnam in total.

dominates – volumes at major Direct port coverage from Laem Chabang is also

strong, and should these trends continue, operators

Southern Californian gateways have a sound case to upgrade vessels on current

continue to grow. South East Asian loops. Direct services are a distinct

advantage for shippers.

For the February 2017 to January 2018 period, China This robust growth is reflected in the loaded box

remained the dominant origin of containerised goods volumes handled by the largest container ports on

shipped to the WCNA area, with 6.8 million TEU (a the Western seaboard. During the same February

rise of 7.4%). By contrast, volumes to Canada fell 2017 to January 2018 period, the following trends

by 0.5% (1.39 million TEU) – a disappointment for include:

the port of Vancouver. To put this dominance into

perspective, the next largest country-to-country pairs • Los Angeles – 4.3 million TEU, up 3%

over this same period were: • Long Beach – 3.3 million TEU, a rise of 8%

• Vietnam to US – 661,000 TEU, up by a strong • Vancouver – 1.3 million TEU, down 4%

20%

• Tacoma – 724,000 TEU, down 17%

• China to Mexico – 581,000 TEU, a rise of 9%

• Oakland – 665,000 TEU, an increase of 5%

• Taiwan to US – 430,000, an improvement of 5%

• Prince Rupert – 597,000 TEU, up 4%

The break-neck pace of demand growth from

Vietnam was reported in the February edition of • Seattle – 485,000 TEU, a strong improvement of

Horizons. The bilateral trade agreement in place is 23%

clearly influencing products being shipped to the US

and Canada, and the 19.7% growth that has occurred

over the past 12 months is expected to continue,

especially as revamped WCNA transpacific services

by the 2M Alliance, Ocean Alliance and THE Alliance

all schedule calls to Cai Mep port (Ho Chi Minh City) .

26TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Demand

TOP ROUTES BY VOLUME, GROWING / DECLINING ROUTES TOP ORIGIN PORTS, TOP DESTINATION PORTS

TOP ROUTES BY VOLUME TOP ORIGIN PORTS BY VOLUME

TEU %YoY TEU %YoY

China to USA 6,781K 7.4% Yantian 2,249K 7.9%

China to Canada 1,386K -0.5% Shanghai 2,233K 4.1%

Vietnam to USA 661K 19.7% Ningbo 1,062K 10.4%

Taiwan to USA 430K 5.1% Qingdao 730K 6.7%

South Korea to USA 405K -3.7% Xiamen 486K 13.0%

Japan to USA 492K 5.9% Busan 525K 1.5%

Thailand to USA 325K 13.7% Ho Chi Minh 403K 14.0%

Hong Kong to USA 208K -3.7% Xingang 415K 9.4%

Indonesia to USA 195K 0.2% Other China 373K -29.9%

Malaysia to USA 153K 1.3% Laem Chabang & Bangkok 349K 12.0%

TOP GROWTH ROUTES TOP DESTINATION PORTS BY VOLUME

TEU %YoY TEU %YoY

Vietnam to USA 553K 19.7% Los Angeles 4,268K 2.5%

Thailand to USA 286K 13.7% Long Beach 3,284K 8.0%

China to USA 6,313K 7.4% Fraser Port & Vancouver 1,285K -3.8%

Taiwan to Canada 76K 6.9% Oakland & San Francisco 665K 4.5%

Japan to USA 464K 5.9% Tacoma 724K -17.1%

Seattle 485K 23.2%

ROUTES IN DECLINE Prince Rupert 597K 3.6%

TEU %YoY

Japan to Canada 55K -9.4%

South Korea to USA 405K -3.7%

Hong Kong to USA 208K -3.7%

Philippines to USA 88K -2.8%

China to Canada 1,386K -0.5% TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018

27TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–WEST COAST NORTH AMERICA

Cascade

• The Asia – West Coast North America trade sees the largest influx

of redeployed vessels resulting from our predicted cascade. A OPERATOR SHARE TODAY OPERATOR SHARE MARCH 2021

key driving force behind this is the downstream impact of Ocean (STANDING SLOTS TEU) (STANDING SLOTS TEU)

Alliance’s expansion through new build vessel deliveries due in 2021.

This is most keenly felt with 23 of Evergreen’s vessels reallocated

here by the beginning of 2021.

• We also view this trade as the likely destination for 15 new build

vessels on order:

• 3x PIL New Panamaxes due in the third quarter of 2018;

• 3x NYK ULCVs (14k TEU), one due imminently with two further

deliveries in mid 2020;

• 3x Cosco New Panamaxes (13.5k TEU) due mid 2019; and

• 6x Evergreen Post Panamaxes (11k TEU) due at the beginning of

2021.

• The net impact of these changes gives Evergreen a 14% market

share by capacity in 2021, while Maersk Line remain the largest

operator with a 15% share in 2021, down 2% from its current position.

NEW BUILD / EXISTING FLEET BREAKDOWN CASCADE BY VESSEL VOLUMES CASCADE BY OPERATOR

28TRADE LANE REPORTS CLIPPERMARITIME Horizons

Asia–East Coast North America

(via Panama Canal and Suez Canal)

Pre-Chinese New Year volumes strong, but freight rates S U P P LY

declined in March despite the positive demand.

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+29% +15%

DEMAND

ROLLING

MOM %

12 MONTH

CHANGE

% CHANGE

+32% +7%

OCEAN CARRIER

SHORT-TERM OUTLOOK

29TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–EAST COAST NORTH AMERICA

Supply/demand balance and forecast

East Coast ports looking for • Monthly nominal capacity in March 2018 was

691,000 TEU, unchanged from February

Bridge in New York/New Jersey and the results

of the Savannah Harbour Expansion Project

continued strong trade demand • The number of weekly services offered has not

(SHEP) at Savannah.

in 2018. remains at 20 in 2018 The enlarged Panama Canal has allowed operators

to re-deploy much larger vessels on the Panama

• The route is mostly served by the same fleet in

The Panama and Suez canal routes are key options All-Water routing, but these increases will not

2018 so far, but this fleet now represent a 15%

for Asian cargo destined for the East Coast of North continue indefinitely. Improving water depths and port

capacity increase compared to a year ago:

America, but also as an alternative to the transpacific infrastructure on the North American East Coast is a

West Coast for the hinterlands of Chicago, the Ohio • Average ship size in March 2018 is 7,984 distinct positive, but vessels beyond 14,000 TEU-class

Valley, Memphis and Atlanta. TEU, marginally higher than the February are highly unlikely unless services via the Suez Canal

2018 figure of 7,775 TEU – but significantly are re-structured and upgraded.

A summary of the competitive supply position in early

above the March 2017 figure of 6,928 TEU.

2018 leads to the following conclusions: Using the most up-to-date information available,

• The largest ship in service in 2018 has head-haul loaded container demand in the Asia-ECNA

remained at 14,414, which represents a major trades reflected a surprisingly strong cargo spike in

Demand outlook and 2018 forecast increase in size and operator strategy on the the two-month lead up to the Chinese New Year:

10,700 TEU recorded for March 2017.

Total volumes on the head-haul trade reached • January 2018 totals were 638,000 TEU, which

5.8 TEU in 2017, a very robust 11.4% rise on • The largest ship size reflects the step-change compares with 564,000 TEU for December 2017

2016. Not only does this highlight the strength of in infrastructure projects at key ports, such and 484,000 TEU for January 2017. An upturn in

the trade, particularly for volumes out of China, as the raising of the air draft of the Bayonne volumes is usual prior to the Chinese New Year

but it also reflects a shift in the trade away from

the West Coast. Lower spot freight rates will also

be attracting shippers. Our statistical analysis

ASIA-EAST COAST NORTH AMERICA SUPPLY/DEMAND BALANCE AND FORECAST

of the last five years suggests a trendline for

this year of 14.7% with our 80% confidence

interval giving a range between 6% and 23%.

Our view is that demand growth will continue to

Actual supply (Bar)

be strong this year and could reach double-digits

Actual demand

for a second year. The most serious threat to

Supply forecast (Bar)

this growth forecast is a trade war between the

Trend demand forecast

US and China. One other risk remains the re-

negotiation of new labour contract between the High demand forecast

International Longshoremens’ Association (ILA) Low demand forecast

and the United States Maritime Alliance (USMX),

which is to be renewed at the end of September.

NOTE: TEU volumes and percentage changes refer to 12 month period Feb 2017 to Jan 2018

30TRADE LANE REPORTS CLIPPERMARITIME Horizons

ASIA–EAST COAST NORTH AMERICA

Supply/demand Supply

balance and Influx of larger ships now One development in the US East Coast is the

forecast (cont.)

continued expansion of HMM’s direct involvement

being seen at ports – but in trades between Asia and North America, with the

following occurring by the end of May 2018:

more to come from April 2018. • Deployment of two of its own vessels (8,566 TEU

period, but these are higher monthly aggregate size) on Zim’s Seven Star Express service.

totals than in the normal peak season period The trend of successively larger ships calling at ECNA • HMM has been a slot charterer since May 2016.

running from June to October. The January 2018 ports was a feature of the trade from Asia in 2017, but

totals are preliminary figures from CTS. It remains the same level of increase is not expected for 2018, • This further outlines HMM’s desire to increase its

to be seen if these trends continue into 2018, and as the biggest ships on All-Water trades shows: direct operating involvement in activity from Asia,

if there has been a genuine shift of Chinese cargo to supplement Transpacific to North America West

• March 2017 – 10,700 TEU Coast developments.

to the East Coast.

• April 2017 – 13,208 TEU • HMM is about to confirm a newbuilding order

• The January 2018 indicative load factors were

an estimated 82%, consistent with the 81% in • August 2017 – 14,414 TEU – still the largest in involving 12 x 22,000 TEU ships and 8 x 13,000

December 2017, but lower than the 90% for service in March 2018 and not expected to change. TEU units, all due by 2022. While the larger

January 2017 – reflecting the increased supply of vessels are for Asia-North Europe, the carrier’s

To put the March 2018 positions into context, the

TEU slots during 2017. 13,000 TEU ships could be in the Asia-North

leading operators based on monthly TEU standing slot

America trade, but at this stage it is too early to

The positive start for 2018 was reflected in SCFI capacity are:

say which coast.

head-haul spot rates, which averaged $2,647 • Maersk Line (2M)– 0.33 million TEU

per FEU in January 2018 and $2,773 per FEU in At the same time, Boston is going to be the recipient

February 2018. However, by mid-March, rates had • MSC (2M) – 0.32 million TEU of a call from the Ocean Alliance (CMA CGM, Cosco,

fallen significantly to $2,009 per FEU, the lowest APL, Evergreen, OOCL) from the start of April 2018

• Cosco (Ocean) – 0.25 million TEU

since late 2017. This is partly driven by the fall-off as part of its service restructuring. This Alliance has

in cargo volume after the Chinese holiday. Another • Evergreen (Ocean Alliance) – 0.14 million TEU previously called at the port with its AWE 2 service

factor seems to be aggressive carrier pricing to that also linked to the WCNA.

• Zim– 0.14 million TEU

protect market share. In the lead-up to the annual The new call is on the established Vespucci/AWE1/

It is notable that 2M has a relatively large capacity

contracting period with BCOs, ocean carriers will AW4/NUE/ECC2 and is deploying 10 x 8,500 TEU -

share in this route as opposed to the much larger

not want further spot rate erosion. The general 9,000 TEU units (Evergreen x 7, CMA CGM x 2 and

WCNA trade and that Zim as an independent has

market consensus is that contract rates will stay OOCL x 1). Boston will be called after Savannah

clearly focused its strategy on serving East Coast

steady relative to 2017, and this also remains and Charleston, but before New York/New Jersey,

destinations rather than West Coast.

our view as ocean carriers jostle to retain clients. so although it will not benefit from the likely larger

Shippers are also very pre-occupied with rising inland exchanges of a first inbound or last outbound call,

costs, bunker costs, lack of trucking capacity and sufficient local demand is warranted to offer a weekly

demurrage/free-time issues. connection.

31You can also read