COGNIZANT 2ND QUARTER 2018 - Old Mutual Wealth

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COGNIZANT 2ND QUARTER 2018

JAPAN: THE LAND OF THE RISING ECONOMY | CHINA: ASCENDING | INDIA: THE TIME FOR GROWTH IS NOW

| THE MIDDLE EAST: ECONOMIES FULL OF ENERGY

TABLE

OF

CONTENTS

INTRODUCTION 3

JAPAN: THE LAND OF THE RISING ECONOMY 5

CHINA: ASCENDING 9

INDIA: THE TIME FOR GROWTH IS NOW 13

THE MIDDLE EAST: ECONOMIES FULL OF ENERGY 17

2

INTRODUCTION

CHRIS POTGIETER – HEAD OF PRIVATE CLIENT SECURITIES

The theme of this edition and the next is not see these technologies as threats its trading and investment with countries

“Around the World in 180 Days”. We will but as essential enablers. Labour force other than the US. Initiatives such as the

cover most of the globe with brief insights participation by women in Japan was One Belt One Road (OBOR) initiative is

into the major economies and trends negligible a decade ago and now a case in point.

shaping our collective future. At Private the percentage of women working in

Client Securities (PCS), we believe that Japan exceeds that in the US. Corporate From China we move on to India, the

wealth should be protected and grown governance and gender diversity at second most populous country in the

by diversification into global investment companies are improving rapidly and world. Its population is young, educated

opportunities. From the inception of PCS encouraging a shift of domestic savings and increasingly dynamic, connected

we made sure we had the capabilities to from bonds to stocks. and tech-savvy. India’s growth had long

enable this in bespoke personal portfolios disappointed investors who argue that,

We then move our attention to China. based on its demographics, it should have

in an efficient and a cost-effective way.

The most populous country on earth is outpaced China as the fastest-growing

South Africa represents less than 1% of

rapidly transforming from an export and large economy. But decades of erratic

the world economy and of the global

population and while many companies infrastructure investment-driven economy to economic policy, complicated tax laws,

listed on our local exchange do offer a domestic consumption-led economy, with inefficient infrastructure and bureaucratic

opportunities to get global exposure, its demographic dividend being replaced red tape have stymied its growth. However,

these are limited. For an investor to obtain by a consumption dividend coupled with there are tangible signs that things are

rightful exposure to global growth and rapid technological innovation. The country improving. Several meaningful fiscal

diversification opportunities, one has to has been able to produce a wide range of reforms are already playing out in the

look beyond the Johannesburg Securities products at compelling prices and become economy and the effects are evident in

Exchange. a leading exporter to the world. China’s the stock market. Increasingly domestic

growth was enabled by the technology savings are being driven out of bank

This edition covers the major economies of others. It copied these technologies accounts and into listed equities. This may

in the East. We look at Japan and its and applied them in new areas and on have been overdone recently, but booms

nascent revival from what some called a massive scale, but now it is coming and busts are part of the growing pains

a zombie economy to an economy that into its own in terms of creativity and that can be expected.

is changing from being export-led to home-grown innovation. With the Chinese

consumption-fed. Japan’s economy now economy forecast to match that of the US From the Far East we cross to the Middle

has such low unemployment that robotics by 2030, it is reasonable to expect the East – a fitting place to conclude this

and digitisation are necessary to keep up investable market to grow significantly. edition and to set the stage for the next.

with labour force demand. The Japanese, Trade wars with the US may slow this, The Middle East represents an ancient and

unlike some Western counterparts, do but won’t prevent China from expanding enduring link between East and West. It has

3

always been a contested region due to its

strategic geographic position in the world

and, from the late 19th century, because

it also represented a bountiful source of oil

and gas to fuel the world’s energy demand

as industrialisation and consumption

accelerated. With the world changing

its energy consumption habits towards

more sustainable sources, the economies

in this region have been reinventing

themselves also. This is probably most

obvious in Dubai and also the reason

for the planned listing of state-owned

oil company Saudi Aramco. Despite the

change in the energy landscape, the

new trade connections between East and

West will put the Middle East in centre

stage yet again.

Could the current bout of tit-for-tat raising

of trade barriers escalate into all-out trade

wars and spoil the opportunities we

highlight in this issue? It is possible, but not

probable. The price of an all-out global

trade war is arguably too high for any

of the world’s largest economies to bear.

Many would argue that the safest place to

be in a trade war is in the countries with

the strongest domestic economies that are

largely self-sufficient. The United States is

the leading economy in this regard, but as

new and renewed economies rise in the

East, it is no longer the only place to be.

New trade connections and relations are

being established and the scope and size

of these new relations have the potential

to far exceed what has gone before.

“We think of globalisation as a uniquely

modern phenomenon; yet 2 000 years

ago too, it was a fact of life, one that

presented opportunities, created problems

and prompted technological advance.”

Peter Frankopan, The Silk Roads: A New

History of the World

4

JAPAN: THE LAND OF THE RISING ECONOMY

JAPAN: THE LAND OF

THE RISING ECONOMY

ANDREW DITTBERNER – CHIEF INVESTMENT OFFICER

Japan and economic prosperity are two words that have not often been mentioned in the same sentence for the better part of nearly

three decades. The post-World War II economic miracle of Japan that came to a crushing halt in the late 1980s and early 1990s,

resulted in a prolonged period of economic malaise that became known as the Lost Decade. A lack of economic recovery through

2001 to 2010 resulted in the whole period becoming known as the Lost Score or the Lost 20 Years. Unsurprisingly, the Japanese

stock market suffered significant real losses during this period, as shown in graph 1.

5

JAPAN: THE LAND OF THE RISING ECONOMY

GRAPH 1: THE NIKKEI 225 INDEX (DEC 1950 – MAY 2018) is that a normalisation of the Japanese

45 000

market has taken place and continues

40 000

to do so. Historically, the equity market

The Lost 20 Years

35 000 was very much driven by the yen/US

30 000 dollar exchange rate, given the Japanese

Nikkei Price Index

25 000 economy’s reliance on exported goods

20 000 such as motor vehicles (Toyota, Honda,

15 000 Nissan, Mazda, etc.) and electronic

10 000 goods (Sony, Canon, Fujifilm, Nintendo),

5 000 among others. This resulted in Japanese

0 companies producing very erratic earnings

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

growth profiles, in turn leading the market

to closely correlate with the exchange rate

rather than the underlying profitability of

With the Japanese economic miracle on this later. The profitability of listed

the companies that constituted the market.

parked in our very distant memory, companies, as measured by return on

This relationship began to break down in

and the oxymoron that is Japan and equity, has nearly doubled from mid-single

the lead-up to the global financial crisis

economic prosperity, today Japan is not digits to 9.2%. And most surprisingly, in

of 2008. This is highlighted in graph 2.

often considered an attractive investment local currency terms, the stock market’s

destination. The rise of China and the new Nikkei 225 Index has outperformed the Decomposing Japanese GDP numbers

technology age are viewed as far more other major stock indices of the US and into net exports and domestic demand,

exciting investment destinations. Yet, as Europe with a cumulative total return since 2010 domestic demand has been

all good things come to an end, so do of 135% to the end of May 2018. In a far larger contributor to total GDP than

periods of poor performance. US dollar terms, the Japanese market has exports and also far less volatile than

slightly underperformed the US market, exports. This theme is playing itself out in

Japan’s lacklustre economic performance

but remains materially ahead of the the equity market and is evident through

of recent decades aside, it remains the

European market. listed companies’ profitability becoming

third-largest economy, behind the United far less volatile, while at the same time

States and China, and constitutes the It is fascinating to dig a little deeper into increasing the overall level of profitability

second-largest weight in the global equity the Japanese equity market and get a as alluded to above. Graph 3 shows that

market, from a geographical point of better understanding of how the underlying over the past 10 years, the local stock

view. Given the sheer size of Japan, and market drivers have evolved in recent market has been driven more by earnings

their global economic significance, it is years. What becomes instantly obvious than the exchange rate.

imperative that Japan receives more than

just a passing glance. GRAPH 2: C

ORRELATION BETWEEN THE NIKKEI AND THE YEN/US DOLLAR

EXCHANGE RATE

If one were to take a bird’s eye view of

25 000 70

how Japan has progressed over the past

80

five years, it would be very difficult to 20 000

90

say that it remains in its economic slump

Yen/USD Exchange Rate

Nikkei 225 Price Index

100

of the 1990s and 2000s. Since the end 15 000

110

of 2012, economic growth as measured

10 000

120

by nominal gross domestic product, has

130

expanded by a cumulative 11.3%. The 5 000

140

unemployment rate has also improved Nikkei 225 (LHS) Yen/USD (RHS)

0 150

materially from 4.3% to 2.5%, but more

1992

1994

1996

1997

1999

2001

2003

2005

2007

2008

2010

2012

2014

2016

2018

6

GRAPH 3: T HE NIKKEI PRICE INDEX AND THE UNDERLYING EARNINGS LEVEL and efficient corporate sector and the

(MAY 2008 – MAY 2018) need to address the lack of corporate

200 governance was identified as a key

Nikkei 225 Earnings Base

area of concern. Second, labour market

Nikkei 225 Price Index

150 reform was required to reduce the level of

Index (May 2008 = 100)

unemployment and to attract women back

100

into the workforce. And last, addressing tax

collection issues that were putting further

50

pressure on an already strained fiscus.

0

Japan has more listed companies than

the US and therefore, given the size

-50

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 of the sector, it is vitally important that

corporate governance should be up

The recent five years has seen earnings Japan has been anything but stable with to date. The rights of minority investors

per share at market level growing 162%. 10 different prime ministers since the turn need to be protected, while also ensuring

This is slightly ahead of the market’s 135% of the century. This includes two terms by the independence of boards to reduce

total return over the same period, resulting incumbent Shinzo Abe, who first came to the likelihood of corporate troubles.

in a more attractively priced Japanese power in 2006, before returning again in Interestingly, Pakistan had a corporate

equity market (based on a price to 2012. The next elections are due to be governance code in place before

earnings ratio) than at the end of 2012, held in September, and while the feeling Japan did. Thankfully, Japan has now

despite the fantastic returns generated on the ground (at the time of writing) is addressed this issue and evidence shows

that Shinzo Abe will scrape through, he that corporate governance within Japan

for investors. The US and European

is currently facing a number of allegations has materially improved and is continuing

stock markets stand in stark contrast to

that are making the political landscape on this trend.

the Japanese market, given that over the

less certain than in recent history.

past five years, returns generated have Labour market reforms increased female

exceeded underlying earnings growth. Shinzo Abe has also played a significant participation in the workforce, to the

The net result is that both the US and the role in turning the Japanese economy point where there are now more females

European markets are more expensive around with the onset of what has become working in Japan as a percentage of the

today than they were at the end of 2012. affectionately known as abenomics. In total workforce than in the US. On a similar

short, abenomics was a three-pronged note, a record number of older people

Japan has struggled to wash itself of its old

approach which entailed a set of now also form part of the workforce. This

stigma, and as such international investors is in conjunction with the introduction of

aggressive monetary and fiscal policies

continue to refuse to pay a premium to minimum wages and a cap on overtime.

with the aim of revitalising the economy.

invest in Japanese companies. This is Currently, the job offer to applicant ratio

Four years down the line, it appears that

evidenced by the fact that roughly 40% sits at 1.6x, indicating that there are 60%

these policies have enjoyed an element of

of listed Japanese companies trade at more job offers than applicants. 97%

success, as the economy has managed to

less than their book value. Against the move out of the deflationary environment, of high school graduates are securing

above background, coupled with the while posting a number of consecutive jobs. The net result is that overall nominal

fact that consensus remains that earnings years of positive economic growth. employee income growth is rising at 3.3%.

growth will continue through 2018 and This all points to a labour market that is

2019, investors’ unwillingness to re-rate Completing the third prong of abenomics, very tight. Since household consumption

the market appears puzzling. was a number of structural reforms that makes up 55% of Japanese GDP, it augurs

were put in place to improve the overall well for the foreseeable future.

A well-functioning equity market is very global competitiveness of the economy.

much reliant on a stable economic and Three of these structural reforms are One of the unintended consequences

political landscape. On the political front, highlighted here. First, a more competitive of some of the labour market reforms,

7

the cap on the amount of overtime per collection. As it stands, the tax base is well. Abenomics, which includes a number

week in particular, is that companies now far too narrow and should be a much of structural reforms under the watchful eye

have to find a way to boost productivity larger source of revenue. With marginal of Prime Minister Shinzo Abe, continues

to maintain the current level of output. income tax rates in the region of 55%, the to support and grow the economy on

The obvious answer to this is to turn problem does not lie in too low tax rates a sustainable basis. Coupled with the

to technology. Unlike the majority of but rather in the fact that not everyone normalisation of the equity market, which

the world, Japan embraces robotics, pays. A taxpayer identification system is supported by growing profitability

automation and artificial intelligence. was only put in place two years ago, on the back of improving domestic

which is almost unbelievable. Alongside

Given Japan’s highly indebted balance demand and much-improved corporate

this, 70% of Japanese companies pay no

sheet, it is imperative that the country governance, Japan is fast becoming an

income tax. These problems are currently

takes the necessary action to address attractive investment destination. Making

being addressed.

the problem, irrespective of whether the it even more appealing to the discerning

debt is held by locals or not. One way In conclusion, while flying under the radar investor is the fact that the equity market

identified to make inroads in this regard for the past few years, the Japanese remains relatively undemanding from a

was to address problems around tax economy has been performing exceedingly valuation perspective.

8

CHINA: ASCENDING

CHINA: ASCENDING

CHRIS POTGIETER – HEAD OF PRIVATE CLIENT SECURITIES

During my recent visit to Shanghai I made sure that I purchased, for posterity, a bottle of Kweichow Moutai at a local liquor

merchant. Moutai is a brand of baijiu – meaning “clear alcohol” – and is a prized and popular alcoholic beverage in China. In

fact, baijiu is by some measures the most consumed liquor in the world. This makes sense given that one in five people alive today

are Chinese! The company which owns this prized brand is partly state-owned, but the shares in Kweichow Moutai are listed on

the Shanghai stock exchange (as so-called “A-shares”, as opposed to Hong Kong-listed “H-shares”). With the gradual inclusion of

Chinese A-shares in the MSCI World Index starting June 2018, Kweichow Moutai will become a feature of many global portfolios.

The company has a market capitalisation of nearly CNY950 billion, or USD150 billion, which places it between the UK-listed

Diageo and Brussels-listed Anheuser-Busch InBev.

9

CHINA: ASCENDING

a reinvention of its imperialistic past.

Yet, the Chinese dream of a return to

greatness is real. In many important ways

the dream is already matched by reality.

China is rapidly transforming from an

export and infrastructure investment-driven

economy to a domestic consumption-led

economy. Much has been written about

its ageing population – the adverse

impact of the one child policy which

was introduced back in the 1970s and

only relaxed in 2013. However, its

demographic dividend is being replaced

by a consumption dividend. China will

probably “grow rich before it grows

old”. Personal consumption expenditure

Moutai, or Maotai, is named after become the world’s manufacturing hub

is still well below Western levels. Indeed,

the town with the same name in the and today it has risen to become the

it is well below some of its Near-Eastern

Guizhou Province, a mountainous province second largest economy in the world and

neighbours. The services sectors will benefit

in Southwest China with a very long is projected to overtake the US as the

most with financial services, technology,

history of distilling liquor. In fact, the world’s largest economy by 2030.

entertainment, healthcare and education

Moutai of today originated during the

Today, with China’s rapid ascendancy some of the top growth areas. Chinese

Qing dynasty (1644 to 1912), which

consumers are spending more on lifestyle

followed the Ming dynasty and was in areas of geopolitical power, trade

services and experiences while also

the last of the Chinese dynasties before and commerce, one cannot but wonder

moving from mass to premium segments.

the creation of the Republic of China. whether this is Qing Dynasty Version

The Qing was a multi-cultural empire which 2.0 in the making. From the expansion In Shanghai, as in all the major cities, the

lasted almost three centuries and formed of trade influence beyond its borders, influence and pervasiveness of Western

the territorial base of modern China. as evidenced by initiatives such as the One brands are very apparent. Everything

It was the fourth-largest empire in world “Disney” is loved by young and old

Belt, One Road (“OBOR”) to President

history. The Qing, like its predecessors, alike. The Disney Park in Shanghai is

Xi Jinping’s centralisation of power, it all

typically fully booked days in advance,

expanded trade and commerce well brings home many comparisons to what

while the brand’s influence is felt even

beyond the borders of China, into the was last seen during the Qing dynasty. at the top end of the market with co-

far reaches of the South China Sea and

Yet, the world is a very different place branded Disney products being sold in

beyond. The dynasty was vast in its

and the new dynamism and assertiveness high-end malls by luxury brands, such

reach and influence and its development

of China cannot be oversimplified as as Coach. Starbucks presents another

and expansion was set to continue.

Yet, the expansion of European states

into overseas territories and their rapid

DID YOU KNOW THAT PAPER CURRENCY WAS FIRST USED BY THE

industrialisation, coupled with the Opium

CHINESE, WHO STARTED CARRYING FOLDING MONEY DURING THE

wars of the 1840s, conspired against

TANG DYNASTY (A.D. 618 TO 907) — MOSTLY IN THE FORM OF

advancement of the Qing dynasty.

PRIVATELY ISSUED BILLS OF CREDIT OR EXCHANGE NOTES? IT WAS USED

China was the world’s largest economy

FOR MORE THAN 500 YEARS BEFORE THE PRACTICE BEGAN

in 1820 but it declined steadily in the TO CATCH ON IN EUROPE IN THE 17TH CENTURY.

150 years thereafter. Then it rose to

10example of a “magical” place where on the design of their high-end phones, companies such as Tencent and Alibaba is

Chinese consumers find escapement Apple still commands a premium in the evident. From Hong Kong to Beijing and

and fulfilment. Top sports apparel brands Chinese consumer’s mind. It may be the everywhere in between, taxi drivers use

such as Nike, Puma and Adidas are power of Western idealism, or idolism? an app via Tencent’s platform, WeChat,

competing head-on for top spot in the But things are changing as the Chinese to navigate and keep records. Purchases

Chinese consumer’s mind. Even though become more self-aware of their status are made and paid with WeChat Pay

domestic competition is tough with the likes and achievements on the world stage. and Alipay. News, information and

of Huawei now partnering with Porsche entertainment are all accessed through

Technology is playing an ever-increasing

these platforms. Mobile gaming has

role in the services sectors. China may still

become a major source of revenue

DID YOU KNOW THAT THE lag the US in some areas of technology

for Tencent, never mind the fact that it is

MING “TREASURE” VOYAGES, research and development but it leads the default communications tool for just

COMMANDED BY ZHENGE the way in applying cutting-edge about everyone. Businesses connect

HE, INCLUDED SEVEN technology. It is a hotbed of technology with one another and with consumers

FAR-REACHING OCEAN innovation. In little more than a decade, through Alibaba and procurement and

VOYAGES BETWEEN 1405

China has come from almost nowhere payments are seamless and well governed.

AND 1433 TO THE COASTAL

to become the largest e-commerce market These platforms are pervasive and used

TERRITORIES AND ISLANDS IN

in the world, accounting for more than for everything, from conducting business

AND AROUND THE SOUTH

40% of global e-commerce transactions. to living everyday life. The billion+

CHINA SEA, THE INDIAN

China’s mobile payments are 11 times eyeballs connected to these platforms

OCEAN, AND BEYOND? THIS

the value of those in the United States attract online advertising and promotions

EXPANDED CHINESE TRADE

thanks to consumers’ early embrace of and it still seems to be early days. Every

RELATIONS FAR BEYOND THE

the technology. The extraordinary impact provider of services or products to the

LAND-BASED “SILK ROADS”.

of the technology platforms owned by Chinese consumer needs to be on these

11platforms. Revenues will continue to grow, these platforms. It has changed people’s the north and its rich and prosperous

the companies will continue to invest lives and connected the world in a very rice-growing areas in the south. China

in their technology, net income will go real way. This has been mostly positive has always been about commercialism

through cycles, but the trend is upwards. for society. These tenets are important to and trade. This has meant creating

Alibaba founder Jack Ma and Tencent ensure sustainability and avoid the pitfalls connections – within itself and with the

founder Pony Ma remain heavily invested of anti-competiveness, non-compliance or outside world. It is also about competition

in the fortunes of these companies – in social self-sabotage as seen elsewhere. of the highest order. With the Chinese

personal wealth and in time and energy. economy forecast to match that of the

The stakes are high. Their approach to While sitting in the departure terminal at

US by 2030, it is reasonable to expect

government regulations is pragmatic and Shanghai Pudong International Airport,

the investable market to grow significantly.

collaborative, as it has to be. They promote I watched with some amazement as the

aircraft constantly took off and landed in One can expect more capital liberalisation

an open architecture approach so that

the foreground while cargo ships moved as the economy opens up. Trade wars

consumers decide, for most part, which

up and down the mouth of the 6 300km- with the US may slow this, but it will not

services or suppliers reach “page one” on

long Yangtze river in the background. prevent China expanding its trading and

My mind then crossed to the Grand investment with countries other than the

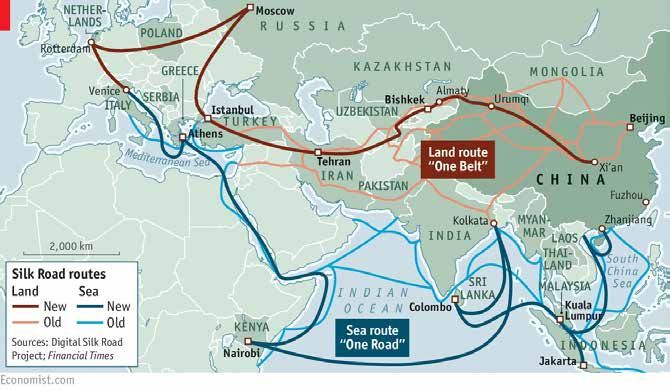

CHINA’S “ONE BELT, ONE Canal, not far from Shanghai. The Grand US. The Western developed world runs

ROAD” INITIATIVE COVERS Canal winds its way from Beijing in the the risk of falling far behind this rapidly

65% OF THE WORLD’S north to Hangzhou in the south and is at rising superpower in the East. Investors

POPULATION, 75% OF GLOBAL nearly 1 800km the longest and one of should no longer view China as an

ENERGY RESOURCES AND the oldest man-made waterways in the emerging market – it has “emerged”

40% OF GLOBAL GDP. world. The canal was a major conduit and is well on its way to, again, lead

for commodities between its capital in the developed world.

12INDIA: THE TIME FOR GROWTH IS NOW

INDIA: THE TIME FOR

GROWTH IS NOW

SAMEER SINGH – RESEARCH ANALYST

India has long been seen as the de facto leader-in-waiting among the ambush of Asian Tigers hungering to take over the global

economy. Through the rise of Asia during the 1990s, the commodity boom of the 2000s and the recovery post the 2008

global financial crisis, India’s decades of consistent upper-single-digit GDP growth remained behind that of its larger neighbour

to the East, and arguably, has left the expectations of many unsatisfied. As the oft quoted Chinese saying goes, “May he live

in interesting times”, most would agree that the present is the most interesting of times, and it is not only this current period of flux

and uncertainty, but also technological progress and marvel that present India with a stronger platform and greater opportunity

for growth than at any other time in the memorable past. In fact, not only do those in the know now assert that India will become

one of the three largest economies in the world by 20251, but also that India's growth rate should consistently surpass that of

China for at least the next decade2.

13INDIA: THE TIME FOR GROWTH IS NOW

HOW DID INDIA FIND ITSELF IN obligations3. After pledging 67 tons known as the “Liberalisation of India”.

THIS ENVIABLE POSITION? of the country’s gold reserves against The slew of reforms which followed

Well, it is not all demographics. India’s a US$2.2 billion emergency loan from the were a veritable overhaul of the way

path to the doorstep of world-leading International Monetary Fund, India, both India does business, both internally and

growth began from a position of ruin as as a government and a nation, awoke externally, including the devaluation

the country dealt with the after-effects of to the stark reality that open markets of the rupee; industrial deregulation;

the Balance of Payments Crisis in 1991. attracting foreign direct investment and

and structural reforms were needed to

Having managed both a trade and other capital flows; trade liberalisation;

get the economy back on track.

fiscal deficit for more than five years, the tax reforms and rationalisation of the

tipping point was reached when India’s A few months after the collapse, with taxation structure; reduction in financial

foreign exchange reserves could barely a new prime minister and finance repression; and continued modernisation

cover three weeks' worth of imports. minister (Manmohan Singh, later prime of monetary policy, including reducing

At the same time the government came minister over the 2000s) in charge, fiscal dominance4. Key industries that

close to defaulting on its financial benefited from liberalisation were largely

the government instituted what became

services related (leading to the strong

INDIA VS. CHINA GDP growth in business process outsourcing)

16 and included insurance, banking, and

China India

14 telecommunications. Previously, all of

12 these were subject to heavy government

intervention, if not outright control.

10

8 The results of these reforms are perhaps

6 most evident when looking at the ramp-up

in India’s trade share of GDP, from the

4

early 1990s to the global financial crisis.

2

Monetary and fiscal prudence, together

0

with open and greater participation

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

in the world economy, brought with

1

https://edition.cnn.com/2015/05/12/opinions/china-india-haiyan-wang/

2

https://www.forbes.com/sites/salvatorebabones/2018/01/02/india-will-outgrow-china-in-2018-but-must-invest-in-next-generation-value-chains/#30c88b744d87

3

https://en.wikipedia.org/wiki/1991_Indian_economic_crisis

4

India Development Update, World Bank, March 2018

5

https://www.yahoo.com/news/India-economy-stands-today-yahoofinancein-3798138905.html

6

https://en.wikipedia.org/wiki/Literacy_in_India#Post-Independence

14it crucial knowledge and technology barring two years of 4-5% GDP growth, Pradesh (largest agricultural producer in

transfers which, along with increased growing industrial output and increasing India) leading to the country’s net exports

capital and labour productivity, investment were the key priorities. In of agricultural products growing from

contributed to India’s economic expansion addition to targeting an annual growth US$5 billion in 2004 to US$39 billion

into the 2000s. rate of 8% from 2003 onwards, the in 2013.

government also set five-year goals

But it was not all plain sailing and avid AND THEN, A BLACK SWAN

for human and social development,

market watchers would be mindful The fallout from the global financial

which included reducing the poverty

to point out the 1997 Asian financial crisis had far-reaching ramifications for

rate by 5% by 2007 and increasing

all countries and India was not spared.

crisis. Fortunately for India, the Asian the literacy rate to 75% by March

In spite of limited ownership/exposure

financial crisis had a limited impact on 20075. It was also during this period

to sub-prime mortgage instruments

the economy with GDP growth shifting that the government set up an incentive

and the minimal presence of stressed

from 7.6% in 1996 to 4% in 1997 fund to encourage states to implement

international financial institutions in the

and back up to 6.2% in 1998. Owing fiscal reforms that could be monitored.

Indian banking sector, the economy

to much of the reforms taken since 1991, These reforms included improvement

was primarily affected by negative

India maintained a lower current account in the quality of life through provision

investment flows as foreign investors

deficit, had a lower reliance on foreign of basic public services; clustering

withdrew offshore cash to steady their

funding of the fiscus and greater control of of high-tech industries and services;

local balance sheets. Additionally, owing

capital flows allowing it to fare relatively setting up Special Economic and Agri-

to deteriorating investor sentiment, many

better than its Asian neighbours. Economic Zones to promote exports; and

Asian export-led economies suffered

formulating state-level industrial policies

current account imbalances as the

THE NEED FOR HUMAN AND to attract investments. Many of these

appetite for global trade diminished.

SOCIAL DEVELOPMENT policies and reforms can be credited

For India, a lower dependence on

The start of the 2000s for much of the for the specialised growth experienced

exports and large contribution to GDP

world was marked by the implosion of in states such as Bangalore (also known

from domestic sources helped lessen

the dot-com bubble. However, for India, as the Silicon Valley of India), and Uttar

the effects. However, growth did take

a knock. The following four years from

FACT: OVER 1991-2011 IS THE FIRST PERIOD DURING WHICH THE 2010 to 2014 saw India decelerate

ABSOLUTE NUMBER OF THOSE WHO COULD NOT READ DECLINED, from strong GDP growth of ~10% to

INDICATING THAT THE LITERACY RATE WAS OUTSTRIPPING THE ~6% as a multitude of factors took hold

POPULATION GROWTH RATE.6 on the economy. Not only was it the

strong aversion to emerging markets that

SHARE OF EXPORTS AND IMPORTS IN GDP HAS INCREASED worked against India, but the weakness

AS THE ECONOMY PROGRESSIVELY OPENED UP in global trade, high oil prices (India

35.00 is a net importer of crude oil) and an

30.00 enlarged fiscal deficit following the crisis

Exports (% of GDP) Imports (% of GDP) also played a significant role.

25.00

20.00 CHAK DE INDIA! (GO INDIA!)

Within two years, India had a new

15.00

prime minister in Narendra Modi, whose

10.00

appointment in 2014 marked a noticeable

5.00 shift in policy from the previous regime of

0.00

Manmohan Singh. Modi was appointed

with high expectations, having achieved

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

an overwhelming majority off the success

15of turning around the state of Gujarat’s Considering the majority of India’s and more transparent, which encourages

manufacturing base as well as promising population, around 62% are in the registration and adherence. Medium-term

a pro-socialist stance, inclusive of working age group of 15-59 years, expectations are for higher tax revenues,

substantial reforms. Much like past nearly 54% of the total population are higher exports and increased foreign direct

reforms, India continued to focus on below 25 years old and by 2020 the

opening up the economy and improving investment, all while increasing the ease

average Indian will be 29 years old.

the ease of doing business, for both locals of doing business 7. Over a sustained

Sustained improvements in digital literacy

and foreigners. However, differing from period, these are the key ingredients for

and inclusion will be a game-changer for

the past, embedding technology and high growth.

“digitising” the economy were integral the country that could super-charge the

to reform implementation. Besides well-documented demographic dividend. Pragmatically, the growth picture

the passage of reforms for improving is not all blooming lotuses. There have

GROWTH FROM WITHIN:

insolvency procedures (providing relief

UNBRIDLED TRADE been and will be teething issues. After

to India’s distressed credit markets) and

Growth over the coming years will also all, this is India, the world’s largest

liberalising foreign direct investment, two

of the most significant actions were the come from the introduction of GST, which democracy, second largest by population

launch of Digital India and the passing (much like South African VAT) will be levied (1.35 billion), seventh largest (for now)

of the Goods and Services Tax (“GST”). across all stages from manufacture to by GDP and land mass, and easily one of

Arguably, it is the scope of these two final consumption. This is significant as it the most diverse countries on the planet.

reforms that gives them the power to replaces up to 13 direct and indirect taxes

The country recognises 22 official spoken

transform the Indian economy by closing that often overlapped and existed across

languages, 6+ religious faiths and a mix

the digital divide and unlocking growth both federal and state administration.

in trade between states. of racial and ethnic groups; growth here

Beyond simplifying the status quo, the move

comes in starts and stops, spurts and

GROWTH FROM WITHIN: to a single GST widens the net for inclusion

of unregulated and unorganised industries stutters and with compromise. However,

A CONNECTED FUTURE

Digital India aims to overhaul the dated and improves the efficiency of logistics by as history would suggest, the path is

eGovernance project and is unashamedly limiting cross-state taxes and restrictions. undeniably upward and will continue to

ambitious, targeting nine key pillars: Furthermore, the whole process is online be so for the foreseeable future.

PILLAR DESCRIPTION

Broadband Highway Fibre-optic network covering 250 000 village councils; virtual network operators and smart

buildings in cities

Universal Access to Growing network penetration and coverage across the country

Mobile Connectivity

Public Internet Access National Rural Internet Mission – converting 1.5 million post offices to multi-service centres

Programme for service delivery

eGovernance Using IT to improve government transactions, workflow and databases

eKranti Electronic service delivery – using IT to improve service delivery, e.g. free wi-fi in schools,

digital literacy program and provision of Massive Open Online Courses

Information for All Massive open platform for citizens to communicate with government and vice versa

Electronics Through the development of incubators, specialised clusters and support from government

Manufacturing procurement

IT for Jobs ICT-enabled growth in smaller towns and villages – train 10 million people in towns/villages

in five years; support rural IT services businesses

Early Harvest Programs Quick-wins that cover standardisation of government communications, public wi-fi spots in

major metros, school books to become ebooks etc.

7

https://cleartax.in/s/impact-of-gst-on-indian-economy

16THE MIDDLE EAST: ECONOMIES FULL OF ENERGY

THE MIDDLE EAST:

ECONOMIES FULL OF ENERGY

MOOSA HASSIM – INVESTMENT ANALYST

The Middle East has always been a geographic region of great importance throughout human history. It is credited with being

the cradle of civilisation as its region of dry grasslands and fertile river plains made it the natural home to the first agriculture. Its

highlands were the natural habitat of wild grasses, such as wheat and barley, and it is from here that the first agriculture, based

on these crops, started around 10 000 years ago. Farming spread through the Middle East by around 6000 B.C. and from there

gradually spread westward into Europe and east to India and South Asia1.

17THE MIDDLE EAST: ECONOMIES FULL OF ENERGY

Beyond farming, the Middle East The adoption of the Paris Agreement What this analysis abundantly highlights is

contributed much to the development of marked a major step forward in global that the majority of Middle East economies

the civilised world. It was here where the efforts to address global warming. For the are heavily reliant on oil production and its

first codes of law were defined, where first time in history, both developed and related industries for both economic growth

the first writing systems were invented, developing nations committed themselves and socio-political stability. Unsurprisingly,

where engineering feats such as the wheel to pursue policies that would lower the reliance on a commodity that the

and the first surgical tools like the scalpel, their carbon footprint. This ensures that world is attempting to phase out presents

bone saws and forceps were crafted, these countries place larger emphasis on numerous issues for the future of the

where sciences such as astronomy and initiatives that would reduce their usage of region. These economies will come under

mathematics were first developed and hydrocarbon fuels as a source of energy. immense pressure as the global demand

studied, and it is even credited with for oil decreases. This is exacerbated by

Meanwhile, technological advancement

popularising the brewing of coffee, the fact that they subsidise energy in their

has improved the cost-competitiveness of

allowing you to get your morning fix2. home countries, providing it at prices that

low-carbon technologies such as wind and

solar energy generation, power storage are a fraction of the international market

More recently, the Middle East is known

technologies and electric vehicles. The value. In this process, the region incurs

for being the global energy storehouse,

global energy outlook sees the trend of massive losses, bloated and inefficient

with around half the world’s known oil

low-carbon technologies reshaping the public sectors and very high levels of

and gas reserves found in the region.

global energy generation mix. These two youth unemployment.

It is this fact that ensures the region will

continue to play a major role in global forces will ensure that the global reliance

SO WHAT ABOUT MIDDLE EAST

affairs, whether economic or political for on hydrocarbon fuels wanes and at some

STOCK MARKETS?

the foreseeable future. However, the rich point in the future we should reach a peak

With the geopolitical tensions and constant

deposits of “black gold” doesn’t come in global oil demand.

threat of war and proxy wars, why would

cheaply. There is a constant backdrop HOW WILL THIS AFFECT investors consider the Middle East as a

of geopolitical tension and the volatility MIDDLE EAST ECONOMIES? potential investment destination? The

of oil prices creates periods of economic The charts alongside analyse the answer is simple: long-term development

uncertainty. These tensions, along with the composition of specific countries' GDPs can and should continue irrespective of the

inefficiencies created by the monarchical to investigate the percentage that oil concerning structural dynamics surrounding

states, have left the Middle East largely contributes to their economy. Also oil and the geopolitical backdrop.

underdeveloped. compared are oil and non-oil fiscal

revenue and oil and non-oil exports. Although oil has in the past provided

GLOBAL DECARBONISATION these countries with great wealth and

Being considered the cornerstone of the These charts paint a clear picture. a certain measure of stability, growth and

global energy architecture, Middle Eastern For the major economies of the Middle income distribution have been uneven,

oil-producing countries have a vested East, oil and government activities (heavily coupled with a private sector that is unable

interest in ensuring oil prices remain high funded by oil revenues) constitute more to absorb the hundreds of thousands of

in order to support their economies and than 40% of their GDP. The amount of job-market entrants each year. To build a

the region as a whole. Traditionally, this fiscal revenue generated from oil in these more resilient and inclusive economy it is

was done by controlling the supply of oil same oil export-led economies is also imperative that these countries diversify their

(through OPEC). However, the latest dip disproportionately large. To provide an economies away from being completely

in the oil price is being driven by more example: Qatar reports its direct fiscal dependent on commodity exports.

than just an oversupply (although it is a big revenue from oil to be around 67% of total

component). Two forces that are playing a fiscal revenue, but practically all investment Revenues from hydrocarbon exports are

material role in the structural decline of the income and the bulk of corporate tax no longer guaranteed, which leaves

oil price are decarbonisation policies and come from Qatar Petroleum. In this case, policymakers in a pinch as to where

low-carbon technology advancements. their oil-related fiscal revenue is probably to obtain funds. With equity markets

closer to 90%, if not more. in bearish territory, this represents

1

History of The Middle East (n.d.), Accessed: June 2018,

2

Al-Hassani, S., 1001 Inventions: The Enduring Legacy of Muslim Civilization, 3rd ed., National Geographic, 2012

18GRAPH 1: GDP COMPOSITION OF MENA COUNTRIES, 2016 a significant problem. What the region now

100%

requires is for the respective governments

90%

to push for much-needed reform in the

80% financial sector. The reforms would need

70% to be far encompassing: relaxing foreign

60% ownership rules would provide much-

50% needed market liquidity; development

40% of diversified asset classes would

30% present further investable opportunities,

20%

encouraging increased domestic

10%

investor inclusion, and strengthening

0%

the regulatory environment would ensure

Libya

Kuwait

Iraq

Oman

Saudi

Arabia

Qatar

Algeria

UAE

Bahrain

Egypt

Iran

Palestine

Yemen

Morocco

Israel

Lebanon

Jordan

more transparency and oversight in the

Oil Government Other market. While equity markets in and of

themselves cannot promote development,

GRAPH 2: O

IL AND NON-OIL FISCAL REVENUE IN SELECTED MENA

they provide the impetus for foreign capital

COUNTRIES, 2016 (% OF GENERAL FOVERNMENT REVENUE)

inflows and allow for greater transparency

100%

into the valuation of companies, which

90%

is vital for countries seeking funding and

80%

70%

sustainable economic growth.

60%

SOME STOCK MARKET

50%

CONCERNS

40%

Stock markets in the Middle East can be

30%

considered lacklustre. Even though their

20%

10%

stock market capitalisation as a percentage

0%

of GDP averages around 60%, which

Libya

Iraq

Oman

Qatar

Kuwait

Saudi

Arabia

UAE

Yemen

Algeria

Iran

Egypt

Palestine

Morocco

Lebanon

is roughly on par with global emerging

Oil Revenue Non-oil Revenue

markets, their market dynamics are dismal.

Turnover, a measurement of how often

GRAPH 3: OIL AND NON-OIL EXPORTS IN MENA COUNTRIES, 2016 shares change hands and an indication

100% of how vibrant and liquid a market is, has

90%

been pretty much stagnant over the past

80%

10 years. For 2017, Bahrain had an

70%

annual turnover of just 3.7%, with Abu

60%

Dhabi at 11% and Saudi Arabia at 49%.

50%

This is a fraction of the turnover seen

40%

in Asian markets, with China’s Shenzhen

30%

20%

Stock Exchange boasting a turnover

10%

of 264%.

0%

Not only are oil and gas the primary

Libya

Iraq

Algeria

Kuwait

Saudi

Arabia

Qatar

Oman

Iran

Bahrain

Egypt

UAE

Yemen

Tunisia

Morocco

Israel

Jordan

Lebanon

revenue drivers for the Middle East states,

Oil Exports Non-oil Exports but they also extend into stock market

Source: Bruegel based on International Monetary Fund, World Economic Outlook database, accessed in February 2017. returns. Saudi Arabian petrochemical

Note: Data on Libya refers to 2014.

and oil-related stocks make up over a

quarter of their market capitalisation

19and the Saudi financial sector makes Stock Exchange. Of further concern price slump has been the impetus that

up a further 39%. Analysis done by the is the fact that in June 2017 over 40% of these countries needed to accelerate

International Monetary Fund (IMF) has shares were held by government entities their systematic economic reform and

shown that banking profits in the Gulf in Saudi Arabia with only 27% belonging diversification strategies. By encouraging

Cooperation Council (GCC) are extremely to retail investors, which is indicative of a

the development and accelerating

positively correlated to the movement in very limited stock market culture.

privatisation, the respective domestic

oil prices. The net result is that the Saudi

Leaders around the Middle East and stock markets will allow these countries to

stock market, as a whole, is extremely

North Africa (MENA) region are now increase financing and promote a culture

susceptible to global oil prices, feeding

fully cognisant of the fact that higher of domestic saving and investing, which

volatility in the region’s markets.

oil prices cannot solve the fundamental will ultimately lead to economic growth.

Another complication is the limited number issues plaguing their economies.

Fortunately, many of these countries have

of investable opportunities available The abundant oil revenues will be unable

begun this process. We can see a list of

in the private sector. As of July 2018, to increase productivity in the public sector,

the various diversification strategies in the

only 50 companies were listed on the grow investment in the private sector

and improve the legal and regulatory table below. Whether these end up being

Abu Dhabi Securities Exchange, 40 on

the Bahrain Bourse, 62 on the Dubai environment needed to facilitate an open successful or not, remain to be seen but

Financial Market and 185 on the Saudi and improved business environment. it is the right course of action in creating

It can be argued that the extended oil an inclusive and a robust economy.

Iraq – Private Sector Development Strategy (2014-2030) (Launched in 2014)

• Increase the private sector up to a share of 60% of GDP by 2030

• Improve the country’s business environment, particularly for SMEs

• Reduce the unemployment rate to 4% or less by 2030

Kuwait – Kuwait Development Plan (2015-2020) (Launched in 2015)

• Increase the private sector up to a share of 40% of GDP by 2020

• Create public-private partnership to carry out infrastructure projects

• Increase the number of Kuwait employees in the private sector from 92 000 to 137 000 by 2020

Oman – Ninth Five-Year Development Plan (2016-2020) (Launched in 2016)

• Reduce the contribution of oil in GDP at current prices from 44% in 8th five-year plan to 26% by 2020

• Focus on the private sector and activate public-private partnerships

• Create job opportunities

• Focus on SMEs

Qatar – National Vision 2030 (Launched in 2008)

• Increase and diversify the participation of Qataris in the workforce

• Create a business climate capable of stimulating national and foreign investments

• Manage the optimum exploitation of hydrocarbon resources

• Expand industries and services with competitive advantages derived from hydrocarbon industries

• Create a knowledge-based economy characterised by innovation, entrepreneurship and excellence

Saudi Arabia – Vision 2030 (Launched in 2016)

• Increase SME contribution to GDP from 20% to 35% by 2030

• Increase foreign direct investment from 3.8% to the level of 5.7% of GDP by 2030

• Increase the private sector’s contribution from 40% to 65% of GDP by 2030

• Raise the share of non-oil exports in non-oil GDP from 16% to 50% by 2030

• Increase non-oil government revenue from SAR163 billion to SAR1 trillion by 2030

• Generate 9.5 GW of new renewable energy by 2030

Source: Bruegel based on Kingdom of Saudi Arabia (2016), People’s Democratic Republic of Algeria’s Prime Minister’s Office (2016), Republic of Iraq (2014), State of Kuwait (2015),

State of Qatar’s General Secretariat for Development Planning (2008) and Sultanate Oman (2016).

20THE MIDDLE EAST: ECONOMIES FULL OF ENERGY

WITH DWINDLING OIL REVENUES, THE PRIVATE SECTOR NEEDS TO

BECOME THE ENGINE OF NON-OIL GROWTH AND JOB CREATION.

$96 $51 $51

Barrel Barrel Barrel

PRIVATE PUBLIC PUBLIC PUBLIC

CURRENT PUBLIC SECTOR-LED GROWTH MODEL RUNNING OUT OF STEAM

PUBLIC PUBLIC PRIVATE PRIVATE

NEW GROWTH MODEL NEEDED, WITH PRIVATE SECTOR AS THE ENGINE

2014 2015 2021

CONCLUSION

About a decade ago, returns in Gulf markets

were stellar and dazzling technologically

advanced exchanges were built across

the region with some analysts predicting

that the GCC markets (particularly Saudi

Arabia and the UAE) would soon rival

markets in East Asia. These predictions

may have been premature but sustained

low oil prices with rising debt and high

unemployment may provide the impetus for

the diversification required to reinvigorate

these economies.

21THE MIDDLE EAST: ECONOMIES FULL OF ENERGY

TOP EXPORT BY REVENUE IN MIDDLE EAST ECONOMIES

PETROLEUM &

PETROLEUM PRODUCTS

PETROLEUM PRODUCTS

& CHEMICALS OIL

VEHICLES

GOLD

OIL & GAS

CRUDE OIL

FOODSTUFFS & GAS

ALUMINIUM

OIL

OPIUM

JEWELLERY

CRUDE OIL

PETROLEUM

ELECTRONICS

CLOTHING OIL

OIL

PETROLEUM

CRUDE OIL

OIL METALS/MINERALS

ELECTRONICS TEXTILE APPAREL

OTHER MACHINERY/TRANSPORTATION

PRECIOUS METALS/MINERALS FOOD/DRINK

22CONTACT US

ANDREW DITTBERNER

CHRIS POTGIETER Chief Investment Officer VICTOR MUPUNGA

Head of PCS Tel: 021 524 4867 (CPT) Research Analyst

Tel: 021 524 4582 011 217 1945 (JHB) Tel: 021 524 4466

Cell: 082 827 9777 Cell: 083 296 6928 Cell: 072 838 2919

chris.potgieter@omwealth.co.za andrew.dittberner@omwealth.co.za victor.mupunga@omwealth.co.za

MOOSA HASSIM SAMEER SINGH

Investment Analyst Research Analyst

Tel: 021 524 4609 Tel: 021 524 4529

Cell: 072 448 6369 Cell: 072 383 4490

moosa.hassim@omwealth.co.za sameer.singh@omwealth.co.za

PRIVATE CLIENT PORTFOLIO MANAGERS

CAPE TOWN

DEREK ALTON SHANE LAWRENCE PAUL STEVEN

Tel: 021 524 4566 Tel: 021 524 4656 Tel: 021 524 4572

Cell: 072 290 4220 Cell: 079 526 6369 Cell: 076 719 3958

derek.alton@omwealth.co.za shane.lawrence@omwealth.co.za paul.steven@omwealth.co.za

JOHANN VAN ZYL MICHELLE MATTHEWS

Tel: 021 524 4574 Tel: 021 524 4421

Cell: 083 261 0140 Cell: 083 979 6391

johann.vanzyl@omwealth.co.za michelle.matthews@omwealth.co.za

JOHANNESBURG

DEAN GINSBERG VISHAL HURRICHUND TREVOR O’CALLAGHAN

Tel: 011 245 3818 Tel: 011 245 3812 Tel: 011 245 3801

Cell: 083 650 8223 Cell: 082 411 7798 Cell: 083 660 8321

dean.ginsberg@omwealth.co.za vishal.hurrichund@omwealth.co.za trevor.ocallaghan@omwealth.co.za

MIKE SITHOLE GARY SMITH ROY TOPOL

Tel: 011 245 3741 Tel: 011 245 3802 Tel: 011 245 3619

Cell: 083 352 9070 Cell: 082 464 3691 Cell: 082 809 5052

mike.sithole@omwealth.co.za gary.smith@omwealth.co.za roy.topol@omwealth.co.za

PRETORIA

LOUIS FOURIE GREGORY POTGIETER JACQUES THERON

Tel: 012 369 7232 Tel: 012 369 7234 Tel: 012 369 7235

Cell: 083 391 8610 Cell: 082 823 2731 Cell: 082 495 6465

louis.fourie@omwealth.co.za gregory.potgieter@omwealth.co.za jacques.theron@omwealth.co.za

DURBAN

HELMAR BREYTENBACH JAMES BUZZARD SCOTT LOGAN

Tel: 031 581 0773 Tel: 031 581 0763 Tel: 031 581 0768

Cell: 082 564 0223 Cell: 083 509 7640 Cell: 082 908 7679

helmar.breytenbach@omwealth.co.za james.buzzard@omwealth.co.za scott.logan@omwealth.co.za

BLOEMFONTEIN

BRIAN VERMEULEN

Cell: 083 408 0528

brian.vermeulen@omwealth.co.zaThis document is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice

before acting on any information contained herein. Old Mutual Wealth and its directors, officers and employees shall not be responsible and disclaim all liability for any loss, damage

(whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of or which may be attributable, directly or indirectly,

to the use of, or reliance upon any information contained in this document.

Old Mutual Wealth Private Client Securities (“PCS”) is a division of Old Mutual Wealth Trust Company (Pty) Ltd (“OMWTC”), an authorised Financial Services Provider, Reg No:

1925/002721/07. PCS is authorised to provide financial services on the OMWTC licence.

The Estuaries, 2 Oxbow Crescent, Century City 7441. Tel: +27 (0)21 524 4400, Fax: +27 (0)21 441 1060, Email: pcs@omwealth.co.za, Website: www.omwealth.co.za.

24You can also read