COMPANY PRESENTATION SEPTEMBER 2020 - CIE Automotive

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COMPANY PRESENTATION

SEPTEMBER 2020

1

DISCLAIMER

• This document has been prepared by CIE Automotive, S.A. ("CIE Automotive"), and is for information purposes only. No reliance may or should be placed

for any purposes whatsoever on the information contained in this document or on its completeness, accuracy or fairness. This document and the

information contained herein are strictly confidential and are being shown to you solely for your information. The information may not be copied,

distributed, reproduced or passed on, directly or indirectly, in whole or in part, or disclosed by any recipient, to any other person (whether within or

outside such person's organization or firm) or published in whole or in part, for any purpose or under any circumstances.

• This document is an advertisement and not a prospectus for the purposes of applicable measures implementing EU Directive 2003/71/EC (such Directive,

together with any applicable implementing measures in the relevant home Member State under such Directive, the "Prospectus Directive") and as such

does not constitute or form part of any offer to sell or issue or invitation to purchase or subscribe for, or any solicitation of any offer to purchase or

subscribe for, any securities of CIE Automotive or any of its affiliates or subsidiaries, nor shall it or any part of it nor the fact of its distribution form the

basis of, or be relied on in connection with, any contract or investment decision. Investors should not subscribe for or purchase any securities referred to

in this advertisement except on the basis of the information contained in any prospectus eventually published in accordance with the Prospectus

Directive. The information and opinions contained in this document are provided as at the date of the document and are subject to change.

• This document is not an offer of securities for sale in the United States, Australia, Canada or Japan. The information contained herein does not constitute

an offer of securities for sale in the United States, Australia, Canada or Japan. Securities may not be offered or sold in the United States unless they are

registered or are exempt from registration. No money, securities or other consideration is being solicited and, if sent in response to the information

contained herein, will not be accepted. Copies of this document are not being, and should not be, distributed or sent into the United States. This

document does not constitute an offer of securities to the public in the United Kingdom or in any other jurisdiction. The distribution of this document in

other jurisdictions may also be restricted by law and persons into whose possession this document comes should inform themselves about and observe

any such restrictions.

• Certain financial and statistical information contained in this document is subject to rounding adjustments. Accordingly, any discrepancies between the

totals and the sums of the amounts listed are due to rounding. Certain management financial measures included in this document have not been subject

to a financial audit.

• The information and opinions contained in this document are provided as at the date of the document and are subject to verification, completion and

change without notice. Neither CIE Automotive nor any of its parent or subsidiary undertakings, or the subsidiary undertakings of any such parent

undertakings, or any of such person's respective directors, officers, employees, agents, affiliates or advisers, undertakes any obligation to amend, correct

or update this document or to provide the recipient with access to any additional information that may arise in connection with it.

• CIE’s management uses recurrently and in a consistent way during business management certain Alternative Performance Measures, APM which include

terms about results, balance sheet and cash flow. CIE understands that those APMs are helpful to explain its activity evolution, so they are presented,

defined and reconciled with financial statements in this presentation’s Appendix.

2

INDEX

1. WHAT IS CIE AUTOMOTIVE?

2. CIE CULTURE

3. UPDATE ON RESULTS

4. CIE IN STOCK EXCHANGE

5. APPENDIX

3

1.0 WHAT IS CIE AUTOMOTIVE?

CIE AT A GLANCE INTEGRATION AND MANAGEMENT OF PROCESSES IN A

SUSTAINABLE AND PROFITABLE WAY

EBIT 2019: CURRENT

SALES 2019: MKT CAP:

427.1 M€

3,461.1 M€ >12% over sales ≈1,900 M€

NET RESULT

EBITDA 2019: 2019:

594.4 M€ 287.5 M€

>17% over sales >8% over sales

Unique business model developed successfully since 1996, with a

solid track record and an IRR over 20%.

Carried forward in the context of the necessary consolidation of the

automotive Tier 2 sector.

5

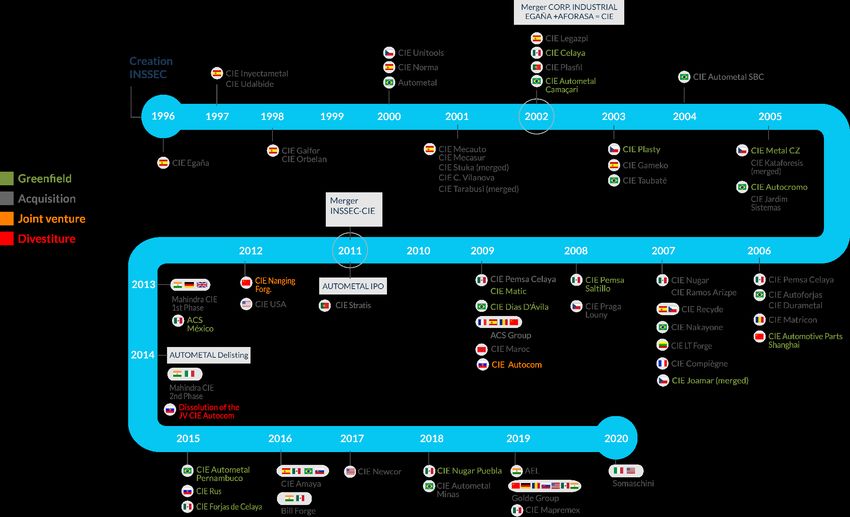

HISTORY A SUCCESSFUL INTEGRATION STORY OF > 20 YEARS

Almost 100 companies and over 28,000 people integrated in Europe,

North America, South America and Asia since 1996.

6

GLOBALISATION GLOBAL FOOTPRINT WITH ESTABLISHED LOCAL PRESENCE

7

SUSTAINED AND PROFITABLE GROWTH Turnover (M€) EBITDA (M€)

CAGR 2002-2019: 12% CAGR 2002-2019: 15%

17% 17% 17%

3.461

700

16% 16% 16% 17% 18%

15% 15% 15% 15% 15% 16% 594

14% 14% 14% 16%

600

3.029

2.843 12% 529 14%

471

500

11% 12%

2.221

2.051 400 358 10%

320

1.811

300

276 8%

1.479 222 207 223

1.3221.3961.308 192 191

1.158 6%

1.057 200 156

893 969 116 131 120 4%

782 80 91

670

481 570 53

100

2%

0 0%

EBIT (M€) Net Income (M€)

350

8% 8% 9%

600

CAGR 2002-2019: 15% 13% 14%

CAGR 2002-2019: 31%

300

7%

7%

287 8%

12%

12%

11% 11% 6% 7%

12% 243

500

10% 250

10% 10% 427

10% 5% 5%

4% 5%

9% 399 202

6%

9% 8%

10%

4% 5% 4%

400

8% 200

8% 339 4% 5%

8%

3% 151

6% 6% 3% 4%

300

249 150

118

215 6% 2%

3%

172 1% 78

200

152

132 142

100

117 60 59

4%

112 1% 51 54 56 2%

73 90 42 41

100

59 59 50 35

42 2%

13 20 11

1%

3

0 0% 0 0%

Automotive Business comparable following 2018 accounting perimeter.

8

SUSTAINED AND PROFITABLE GROWTH

EARNINGS PER SHARE (€) DIVIDEND PER SHARE (€)

& EPS YIELD & DIVIDEND YIELD

CAGR 2016-2019: 21% CAGR 2016-2019: 22%

+19%

+19% 0,80 0,74 17,80%

2,50

+11%

17,80%

2,23

+13% 15,80% 0,70

0,62

15,80%

1,88

(1)

+37%

2,00

+33% 13,80% 0,60 0,56 13,80%

1,67

10,58% 11,80%

0,50

11,80%

1,50 0,41

1,26 8,77% 9,80%

9,80%

0,40

6,90% 7,80%

7,80%

1,00 0,30

5,80%

6,81% 5,80%

3,51%

0,20

2,21% 2,31% 2,89% 3,80%

3,80%

0,50

0,10 1,80%

1,80%

- -0,20%

- -0,20%

33% 33% 33% 33%

PAY-OUT

High double digit Earnings growth over the POLICY

+ A dividend in kind in 2018 valued in more than

period of the last Strategic Plan has allowed

400€ or more than 3€/share.

significant growth of dividends.

Note: EPS yield and dividend yield are calculated with year end closing share prices.

(1) EPS 2018 is calculated with the normalized automotive business net income (Dominion shares were paid as dividend in kind as of July 3rd, 2018).

9

2.0 CIE CULTURE

2.1 GEOGRAPHICAL BALANCE

2.2 COMMERCIAL

DIVERSIFICATION

2.3 MULTI –TECHNOLOGICAL

PORTFOLIO

2.4 INVESTENT DISCIPLINE

2.5 DECENTRALIZED

MANAGEMENT

2.6 ESG2. OUR BUSINESS MODEL

NON USUAL

MULTI-

A NECESSARY COMMERCIAL TECHNOLOGICAL

GEOGRAPHICAL DIVERSIFICATION, PORTFOLIO,

BALANCE AS A DEFENSE A FLEXIBILITY

TOOL INSTRUMENT

INVESTMENT DECENTRALIZED ESG

DISCIPLINE MANAGEMENT, INTEGRATED IN OUR

AND RETURN FOR VALUE BUSINESS MODEL

EXIGENCE GENERATION

112.1 GEOGRAPHICAL BALANCE SALES BY GEOGRAPHY 2019 • Healthy geographical balance in sales and

results.

• Defensive tool against different cycle

26,9% momentum in the diverse geographies.

26,5% EUROPE • Represents a key competitive advantage

NORTH AMERICA when servicing global platforms.

• 112 production sites.

• ≈ 28,000 employees.

• 10 R&D centres.

TOTAL • 4 main markets.

3,461.1 • > 7,000 references.

million euros

2018

18% 11%

BRAZIL

ASIA

9,4% 21,9%

BRAZIL ASIA TOTAL

25%

18% 3,029.5 NORTH

MCIE million euros AMERICA

EUROPE

15,3%

MCIE EUROPE 28%

EUROPE

EX MCIE

122.2 COMMERCIAL DIVERSIFICATION SALES BY CUSTOMER 2019

• Limited dependence on single customer,

platform or car model enabling price

defense.

• Both direct sales to OEMs and Tier 1s (circa

70% - 30%).

• Clients focused on different end market

segments which provides additional

diversification.

• Solvent, assorted and continuous quotation

requests, which allows us investment

choice by profitability return criteria.

TOTAL

3,461.1 2018

million euros

*OTHERS: JTEKT, TATA, DAF, MAN, AAM,

BMW, SCHAEFFLER GROUP, THYSSEN

KRUPP, ACI Y DACIA, TRW, KS,

KOLBENSCHMIDT, AUDI, MARUTI-SUZUKI,

BROSE, HYNDAI, KIA, OPEL, SCANIA,

LEAR…

*Includes 3% of BBAC (BAIC-DAIMLER JV) sales.

**Includes 1% of SGM (SAIC-GM JV) sales.

132.3 MULTI-TECHNOLOGICAL PORTFOLIO SALES BY TECHNOLOGY 2019

• One-stop shop for customers, offering the

21% whole range of the existing technologies

METAL to produce components.

STAMPING AND

• Enabling the selection of the technology

21% TUBE FORMING

that better fulfills changing customers

FORGING

needs.

TOTAL

18% • Allowing CIE to direct investments on

3%

3,461.1 MACHINING winning technologies anytime.

• Allowing to produce multi-technological

CASTING million euros parts.

10%

4%

ALUMINIUM CASTING 2018

16%

9%

11% ROOF SYSTEMS ALUMINUM

PLASTICS

26%

FORGING

16% TOTAL

PLASTIC &

ROOF SYSTEMS

3,029.5

million euros

TECHNOLOGY BY GEOGRAPHICAL AREA

TOTAL MACHINING STAMPING FORGING PLASTIC ALUMINIUM ROOF SYSTEMS CASTING

23%

EUROPE 44 15 5 6 5 7 6 22% MACHINING

STAMPING &

NORTH AMERICA 19 6 5 2 3 1 2 TUBE FORMING

BRAZIL 15 3 4 1 5 1 1

ASIA (INDIA & CHINA) 32 3 6 8 1 3 9 2

TOTAL 110 27 20 17 14 12 17 3

142.3 MULTI-TECHNOLOGICAL PORTFOLIO

FORGING CRANKSHAFT

Engine

CV- JOINTS

Transmission

CV- JOINTS

Transmission

AXLE SHAFT

Transmission

AXLE BEAM

Commercial

Vehicles

ALUMINIUM

GEARBOX HOUSING eREDUCER HOUSING LADDER FRAME STEERING HOUSINGS CAMSHAFT COVER

Gearbox xEV Gearbox Engine Steering Engine

CASTING

TURBO HOUSING CRANKSHAFT DIFFERENTIAL HOUSING BRAKE DRUM AXLE ARM

Engine Engine Transmission Brakes Structural Parts

MACHINING

HUBS, OUTER RINGS EPS COMPONENT DIFFERENTIAL CASE FLANGE AXLE SHAFT

Chassis Steering Transmission Transmission Commercial

Vehicles

152.3 MULTI-TECHNOLOGICAL PORTFOLIO

TUBE FORMING

STAMPING & STEERING COLUMNS BRAKE BOOSTER / BATTERY PACK COVER STRUCTURAL PARTS POWER ELECTRONIC

Steering I-BOOSTER xEV Chassis & Chassis & COVER

Brakes Structural Parts Structural Parts xEV Electronics

PLASTIC

EMBLEMS & INMOLD CONNECTORS & LOAD FLOOR ARM REST, CUP HOLDER, WHEEL COVERS,

DECORATION JUNCTION BOXES Composite Spray Molding & Thermoforming PILARS, GRAB HANDLES, REAR-VIEW MIRRORS,

Interior & Exterior Trim Electronics Interior trim SPEAKER GRILLS… DOOR HANDLES

Interior Trim Exterior Trim

TECHNOLOGY ROOF SYSTEM

ROOF SUNSHADES FIXED ROOF MODULES OPENING ROOF FLUSH WINDOWS SUNSHADES

Shading Roofs MODULES Doors & Windows Shading

Roofs

MULTI-

BATTERY BOX BATTERY BOX BATTERY BOX DIESEL & GASOLINE DIESEL & GASOLINE

PLASTIC - COMPOSITE STAMPING ALUMINIUM INJECTION RAILS INJECTION RAILS

FORGING AND TUBE FORMING

xEV Chassis & xEV Chassis & xEV Chassis & MACHINING

Structural Parts Structural Parts Structural Parts Engine

Engine

162.4 INVESTMENT DISCIPLINE

STANDARD Valid to produce for different customers and platforms,

allowing high saturation of productive capacity.

FLEXIBLE

MACHINERY ≈4% recurrent investment level that allows maintenance and

market organic growth.

STRICT Investment analysis discipline, always requiring high returns.

INVESTMENT Investments ≥ 20% ROI.

DISCIPLINE Operating Working Capital ≈0.

EBITDA Operational efficiency, together with capex control and

finance/tax strategies, enables a high average conversion of

CONVERSION the EBITDA into Cash.

INTO CASH

> 55% conversion level target.

172.5 DECENTRALIZED MANAGEMENT

CASH FLOW

FOCUS

INDIRECT

TEAM PEOPLE

COMMITMENT PRODUCTIVITY

FAST AND DECENTRALIZED

OBJECTIVE:

SIMPLE MANAGEMENT

DECISION STRUCTURE

VALUE

MAKING

UNIVERSAL,

GENERATION NETWORK

SERVICES

FLEXIBLE,

MULTITASK SUPPORT

ENTREPRENEURS

VARIABLE AND

LEAN

LONG-TERM

HEADQUARTERS GLOCAL INCENTIVES

PRESENCE

AND

ORDERS

1819

2.5 DECENTRALIZED MANAGEMENT

ORGANIZATION CHART2.6 ESG - ENVIRONMENTAL

TRIPLE CERTIFICATION

Closing in Triple Certification at all factories: IATF 16949, ISO

14001 and OSHAS 18001.

ENVIRONMENTAL FOOTPRINT

Development of advanced calculations of the Environmental

Footprint of the company’s products.

CARBON EMISSION COST

Inclusion of the Carbon Emission Cost as a new environmental

performance indicator.

CIRCULAR ECONOMY MODEL

Moving towards a Circular Economy Model with the aim of

reducing the intake of materials and the production of virgin

waste by closing economic and ecological loops.

Balancing industrial activity with minimum environment impact:

Skilled knowledge on production processes enables us for

CONSUMPTION OPTIMIZATION AND MATERIALS REUSE

202.6 ESG - ENVIRONMENTAL SUSTAINABLE R&D

CIE Automotive collaborates with a number of associations on a range of research programs.

Every year we earmark approx. 2% of our revenue to this effort across its 10 R&D centers, taking

a multi-technological and multi-materials approach.

The R&D roadmap initiatives are focused on tackling the challenges posed by the transformation unfolding in the sector:

SLOW BUT

VEHICLE PRODUCT AND NEW MOBILITY STEADY

EMISSION PROCESS CONCEPTS ELECTRIFICATION

STANDARDS DIGITALISATION (COMFORT) OF THE

SECTOR

212.6 ESG - SOCIAL COMMITMENT TO STAKEHOLDERS

IDENTIFICATION OF NINE GROUPS OF STAKEHOLDERS

Stakeholders: shareholders, professionals, customers, business partners, suppliers, society, public

authorities, automotive sector and financiers.

GLOBAL ROLL OUT OF OUR CSR WORKSHOPS

• Attended by local executives and managers.

• External and internal analysis of the key issues in the ESG arena.

• Prioritization of the issues identified as relevant.

DECENTRALISED MANAGEMENT MODEL

• Model that eases community engagement decisions and aligns them with each country’s

specific needs.

• More than 90% of plant managers are local.

STRATEGIC ALLIANCE WITH SAVE THE CHILDREN

First community project at corporate level: “Caminando hacia el futuro” (“Walking towards the

future”). A collaborative agreement for training support to youth in Mexico.

222.6 ESG - SOCIAL HUMAN RESOURCES

ZERO TOLERANCE WITH DISCRIMINATION

• Work environment free of bias on the grounds of gender, race, religion, age, sexual orientation, nationality, civil

status or socio-economic background.

• Approval of Corporate Equality Plan in order to reduce the salary gap and to get closer to effective gender equality

by job category.

ZERO TOLERANCE STANCE ON CHILD AND FORCED LABOUR

COLLECTIVE BARGAINING AGREEMENTS

• Employees’ freedom of association and right to collective bargaining.

• All of the agreements make special mention of workplace health and safety matters.

PEOPLE MANAGEMENT MODEL

• Creation of employee skill profiles.

• Evaluation of executive, middle management and skilled workers' job performance.

• Identification of areas for improvement. Continuous training.

• Career Development Programme.

• Global training on human rights matters.

EMPLOYEE ASSISTANCE MEASURES

• In 2019, over €30 million spent in employee support measures in the areas of health, food services, transport and

education.

• Compliance with and often exceeding the minimum wage requirements in each country.

• Development of work-life balance measures.

232.6 ESG - SOCIAL

GREEN SUPPLY CHAIN

A SUPPLIER

PORTAL We share

to facilitate end- OVER 90% OF information Standardisation

to-end SUPPLIERS OVER 20% OF about our supply of the global

management and of the product SUPPLIERS chain and requirement to

to ensure that families deemed of productive FOSTER EMBED ESG

the procurement subject to material have TRAINING CRITERIA INTO

model is framed assessment are ENVIRONMENTAL at small and AUDITS OF

by the criteria of IATF 16949 or MANAGEMENT medium sized SUPPLIERS

OBJECTIVITY, ISO 9001 CERTIFICATIONS. enterprises by of productive

IMPARTIALITY CERTIFIED. leading by material.

AND EQUAL example.

OPPORTUNITIES.

242.6 ESG - GOVERNANCE

CORPORATE GOVERNANCE DRIVEN BY PRINCIPLES OF ETHICS AND

TRANSPARENCY.

Responsibility for oversight of due compliance with the Code of Conduct and the various emanating

corporate policies are vested in the Corporate Social Responsibility Committee, which reports to the Board

of Directors.

CIE Automotive, S.A. makes it possible for all people who are part of the organization and its stakeholders

to submit doubts and notify irregularities or breaches against ethics or integrity or that infringe the

guidelines established in the Code of Conduct through the Whistle-Blowing Channel.

Upholding Spanish Law and international Directives on non-financial information and diversity.

CLOSING OF THE 2018-2019 CORPORATE STRATEGIC PLAN, DESIGNED TO

STANDARDIZE AND EMBED ESG CRITERIA ACROSS THE GROUP.

Consolidation of the compilation process of non-financial information.

External assurance for GRI indicators.

Development of ESG targets for each department.

Implementation of a CSR working methodology that can grow with CIE Automotive.

Development of a communication methodology with stakeholders.

252.6 ESG - GOVERNANCE

1 Signatory Member of the United Nations Global Compact and its Spanish Network,

for the implementation of the 10 Universally Accepted Principles to encourage

business social responsibility in the areas of human rights, labour, environment

conservation and anticorruption.

2 Pledge to contribute to sustainable development by upholding 8 of the 17

Sustainable Development Goals at the heart of the 2030 Agenda for Sustainable

Development.

3

Commitment to ethical and sustainable development in the management model.

262.6 ESG - FTSE4GOOD FTSE4Good INDEX SERIES CONSTITUENT

FTSE Russell confirms that CIE Automotive S.A. has been

independently assessed according to the FTSE4Good criteria,

and has satisfied the requirements to become a constituent of

the FTSE4Good Index Series.

Created by the global index provider FTSE Russell, the

FTSE4Good Index Series is designed to measure the

performance of companies demonstrating strong Environmental,

Social and Governance (ESG) practices.

The FTSE4Good indices are used by a wide variety of market

participants to create and assess responsible investment funds

and other products.

272.6 ESG - SUSTAINABLE FINANCING

CIE AUTOMOTIVE ARRANGED AN €80 MILLION

BILATERAL SUSTAINABLE LOAN WITH BBVA

Score provided by ESG performance A fresh milestone

Terms tied to

Vigeo Eiris an will be evaluated in our CSR

the ESG score

environmental during the life of commitment

consultant the loan

283.0 UPDATE ON

RESULTS:

3.1 RESULTS

3.2 BALANCE SHEET

3.3 CASH FLOW

3.4 FORECASTS 2020JUNE 2020 HIGHLIGHTS H1 2020

01 EBITDA Q2 2020

+13.2 €Mio CIE MARKET

QUARTER DROP >60%

02 Net Income

H1 2020 58.3 €Mio CIE MARKET

HALF-YEAR DROP >40%

03 Operating Cash +64.2 €Mio MANAGEMENT MODEL

FOCUSED ON

Generation H1 2020 46% OPERATING CASH / CASH GENERATION

EBITDA

04 TARGET PRICE

Analyst

recommendation

100% DO NOT SELL CONSENSUS

22.33€

1,130 €Mio

Cash and temporary financial

05 Liquidity Reserve investments: 568 €Mio

Undrawn funding: 562 €Mio

MAINTAINING OUR

06 Dividends and own

shares acquisition

106.5 €Mio COMMITMENT WITH

SHAREHOLDERS

07 Workforce

24,078

Vs 28.124

(Dec 2019)

EMPLOYEES

CIE Market: Motor vehicles production IHS JUNE 2020 (6 months 2020) (growth % in units), weighing the markets in which CIE has production plants

30JUNE 2020 HIGHLIGHTS H1 2020

JUST TWO CRITICAL MONTHS

April with 20% production(*) and May with 35%. In June, with 60% of production(*) we

achieve important net income

DEBT REDUCTION

The debt peak reached in May has already begun to decrease in June with the large cash

generation

FINANCIAL STRATEGY

With our income statement and our cash generation capacity, we have not had to change

the Group's financial strategy, focused on three areas:

• Remuneration of our shareholders: dividends and repurchase of own shares for

capital reduction

• Organic and inorganic growth plan: we are the integrating company in the sector that

will allow us to continue increasing our market share and value generation

• Net Working Capital Growth

WE ARE A BENCHMARK WITHIN THE INDUSTRY

At 60% of production level(*) in the first half of the year we have achieved Ebitda close to

13%, the standard margin of the sector in a normal situation

(*) Production on normalized conditions

31JUNE 2020 RESULTS SALES EVOLUTION 2020 – 2019

CONSTANT EXCHANGE RATE CIE MARKET CIE

NORTH

CHINA 68.0%

AMERICA

EUROPE

-34.3%

-19.6%

-39.9%

-31.5%

-40.5% INDIA

BRAZIL

-41.5% -40.8%

-51.2% -51.0%

CIE Market -40.4%

+12.6 P.P.

CIE -27.8%

Source: Motor vehicles production IHS JUNE 2020 (6 months 2020) (growth % in units).

32 The evolution of the production volume is calculated by weighing the markets in which CIE has production plantsJUNE 2020 RESULTS RESULTS H1 2020

(€ Mio) 30/06/2019 30/06/2020

Turnover 1,702.4 1,208.2

EBITDA 308.0 153.5

% EBITDA on turnover 18.1% 12.7 %

EBIT 226.6 90.2

% EBIT on turnover 13.3% 7.5%

Profit for the year 168.7 56.9

Net income 150.1 58.3

Despite the global paralysis of the economy, the strength of CIE model allows for positive closing

in all the lines of the income statement

Ebitda margin ≈ 13%, falls only 3 p.p. on CIE’s operating margins (Ebitda pro forma ≈16%; Ebit

Pro forma ≈ 11%)(*)

33 (*) Ebitda y Ebit proforma 2019, diluted after the last integrationsJUNE 2020 RESULTS RESULTS Q2 2020

(€ Mio) 2Q 2019 2Q 2020

Turnover 890.3 386.2

EBITDA 157.0 13.2

% EBITDA on turnover 17.6% 3.4 %

EBIT 113.7 (14.1)

% EBIT on turnover 12.8% -3.7%

Profit for the year 86.0 (20.1)

Net income 77.5 (14.5)

In the worst market context, CIE closes a second quarter with positive Ebitda

34JUNE 2020 RESULTS 2020 DIVISIONS CONTRIBUTION

6.5% 6.5%

25.3% 24.5% 25.6% 34.2%

TURNOVER EBITDA

3.5%

13.2%

30.5% 30.2%

Brazil North America Europe MCIE Asia (*)

Europe (India/China)

(*) China turnover: 182 €Mio.

35JUNE 2020 RESULTS 2020 DIVISIONS PROFITABILITY

NORTH BRAZIL EUROPE MCIE ASIA (INDIA &

AMERICA EBITDA EUROPE CHINA)

EBITDA 17.7% 12.6% EBITDA 12.6% EBITDA 3.4% EBITDA 12.9%

EBIT 12.5% EBIT 7.6% EBIT 6.6% EBIT -1.3% EBIT 8.2%

Despite the effects of COVID-19, half-year margins demonstrate the excellence of CIE's

management model and team

We have faced this great crisis with a socially responsible attitude, proof of our constant

and firm commitment to society

363.1 RESULTS 2014-2020 QUARTERLY EVOLUTION

Net income (M€)

1Q 2Q 3Q 4Q

History supports our growing path and our commitment to

growth: 25 consecutive quarters beating quarterly record

37BALANCE SHEET

BALANCE SHEET EVOLUTION

€ Mio 31/12/2019 30/06/2020

FIXED ASSETS 3,393.5 3,405.7

NET WORKING CAPITAL (275.5) (196.7)

TOTAL NET ASSETS 3,118.0 3,209.0

EQUITY 1,235.0 1,051.1

NET FINANCIAL DEBT 1,522.0 1,778.3

OTHERS (NET) 361.0 379.6

TOTAL NET LIABILITIES 3,118.0 3,209.0

Non-recourse factoring 222.2 € Mio 125.8 € Mio

38BALANCE SHEET CASH FLOW

EBITDA 153.5 (€Mio) 31/12/2019 30/06/2020

Financial Expenses (17.7)

Maintenance Capex (37.1) NFD 1,522.0 1,778.3

Tax Payments (21.4)

IFRS 16 Leases (1) (13.1) Adjusted NFD 1,505.3 1,770.8

OPERATING CASH FLOW 64.2

NFD/EBITDA

% EBITDA (4) 45.7% NFD/EBITDA NORMALIZED

3.91X 2.67X

Growing Capex (37.1)

Net Working Capital Variation (87.4)

Payments of Dividends (47.7) 18 months of covenant waiver for

Transactions with own shares (58.8) financial covenants up to 30/06/2021

Payments of previous acquisitions (2) (17.2)

Business Combination of the year (3) (79.0)

Exchange rate effect in NFD (12.4) LIQUIDITY RESERVE

Other movements 19.1 30/06/2020:

FINANCIAL CASH FLOW (256.3)

(1) Payment of rental fee accounted in EBITDA according to the new IFRS 16 regulation.

1,130 €Mio

(2) Pending payments from the acquisition of the solar roof systems of Inteva in 2019.

(3) Acquisition of the gear business of Somaschini S.p.A. (70 € Mio) and additional shares of Mahindra CIE Ltd.

(4) Operating cash flow on the Ebitda value corrected with the effect of IFRS 16.

(*) NFD and Ebitda data adjusted considering 50% of JV China SAMAP

39 39FORECASTS 2020

COVID-19 comes at an

optimal time for CIE, with all

the integrations finished and

the production plants with

high levels of profitability

and operating cash

generation.

40FORECASTS 2020

The worst of this crisis is over, our clients have returned to

business, and CIE is in a favorable competitive position

based on the strenghts of its business model:

FLEXIBILITY DECENTRALIZATION GEOGRAPHICAL

MULTILOCATION DIVERSIFICATION

We have the fixed The local Our global demand

cost structure and management of our does not depend

the management companies avoids the on the volume of a

model that best problems derived single country

adapt to variable from the lack of

volumes mobility of people in

all countries

41FORECASTS 2020

With current market estimates, the

second half of the year will be

better in sales and margins and

will allow us to continue with our

financial strategy focused on

shareholders’ remuneration

(dividend payments and

repurchase program) and debt

reduction

424.0 CIE IN STOCK

EXCHANGECIE IN STOCK EXCHANGE SHARE EVOLUTION VS NET RESULT EVOLUTION

CIE Share Price Evolution (Cumulative) CIE Net Result Evolution (Cumulative)

450%

413%

400%

334%

350%

300% 261% 249pp

250%

200% 170%

203%

150% 111% 168% 164%

100% 131%

39% 93%

50%

41%

0%

-50%

2013 2014 2015 2016 2017 2018 2019

…but a significant mismatch

has arisen during the 2017-

CIE’s share price evolution has performed almost in line with net

2019 period, with CIE’s

income evolution during the period from 2013 through 2017…

valuations severely and

baselessly decreasing.

44CIE IN STOCK EXCHANGE CIE SHARE PRICE PERFORMANCE 2018-2020YTD

60%

CIE Automotive IBEX 35 STOXX Europe 600 Automobiles & Parts (1)

40%

20%

0%

-20%

-31 %

-32 %

-40% -32 %

-60%

Since mid-2018 and coinciding with the entry of CIE Automotive in Ibex 35, financial markets and Auto sector have been

heavily impacted both by geopolitical and macroeconomic issues (US-China and US-EU trade war, Brexit, global

economic slowdown) as well as Auto sector specific issues (new emissions regulations, postponement of purchases

due to lack of clarity in time horizons, drop in demand for economic uncertainty).

Despite this extremely complex context, CIE Automotive has delivered quarter after quarter outstanding financial

results, what, clearly, hasn’t been reflected in its share price performance.

But in beginning 2020, environment has become even more complicated due to Covid-19 worldwide crisis, which is

severely affecting both economic activity and financial markets.

STOXX Europe 600 Automobiles & Parts includes: OEMS: BMW ST, Daimler, Ferrari NV, Fiat, Peugeot,

(1)

Porsche, Renault & Volkswagen. SUPPLIERS: Faurecia, Michelin, Nokian, Plastic Omnium, Rheinmetall, Schaeffler,

Valeo.

45CIE IN STOCK EXCHANGE

EVOLUTION IN STOCK EXCHANGE

2020

2019 2018 2017(1) 2016(1) 2015(1) 2014(1)

Until 31/08

Market Cap (€ Mio) 1,871 2,719 2,766 3,123 2,388 1,993 1,453

Number of shares (Mio) 129 129 129 129 129 129 129

Last price of period (€) 14.50 21.08 21.44 24.21 18.52 15.45 11.27

Maximum price of period (€) 21.98 26.08 36.30(1) 26.20 18.98 15.46 12.29

Minimum price of period (€) 9.71 19.31 19.90 17.15 11.98 10.65 7.21

Volume (thousand shares) 57,266 57,296 87,149 59,318 59,065 60,619 62,970

Effective (€ Mio) 0,925 1,328 2,327 1,244 940 814 600

Source: Madrid Stock Exchange.

(1)Upon such dates, CIE Automotive’s subsidiary “Global Dominion Access S.A.” (Dominion) was still within CIE Automotive’s perimeter. CIE Automotive’s shares of Dominion where distributed as dividend

in kind to CIE Automotive’s shareholders upon July 3rd, 2018, with a consequential reduction in CIE Automotive’s share price from that date.

46ANALYSTS RECOMMENDATIONS

# COMPANY ANALYST RECOMMENDATION PRICE

1 Alantra Equities Álvaro Lenze BUY €20.60

2 Bankinter Esther Gutiérrez BUY €21.80

3 BBVA David Díaz Rico OUTPERFORM €24.90

4 Caixabank BPI Bruno Filipe Bessa HOLD €21.00

RECOMMENDATIONS

5 Exane BNP Paribas Francisco Ruiz HOLD €16.50

6 Fidentiis Enrique Yáguez UNDER REVIEW - Under Review Buy +

13% Outperform

7 Intermoney Valores Virginia Pérez BUY €22.00 67%

8 JB Capital Markets José María Cánovas BUY €31.00

9 Kepler Alexandre Raverdy BUY €20.00 Hold

20%

10 Link Securities Iñigo Isardo UNDER REVIEW -

11 Mirabaud Gonzalo De Cueto BUY €21.30

12 Nau Securities Pedro Baptista BUY €27.00

13 Renta 4 Iván San Félix OUTPERFORM -

14 Sabadell Alfredo Del Cerro BUY €20.97

15 Santander Robert Jackson HOLD €17.50

CONSENSUS - - €21.71

475.0 APPENDIX

APPENDIX I ALTERNATIVE PERFORMANCE MEASURES (APMs)

In addition to the financial information prepared in accordance with generally accepted accounting standards (IFRS), CIE Automotive Group uses in the

management of the business recurrently and consistently certain Alternative Performance Measures (‘APMs’), which include concepts about result,

balance and cash flow, understanding that they are useful to explain the evolution of their activity. Below is a breakdown of all the APMs used in this

document, as well as their definition and reconciliation with the financial statements.

PERFORMANCE MEASURES DEFINITION

EBITDA Net Operating Income + Recurrent Depreciation.

Adjusted EBITDA Annualized EBITDA of 12 last months in those companies incorporated to the perimeter during the period. It includes

50% of the Ebitda of Chinese JV SAMAP, which based on the current agreements with the partner, is consolidated by

the equity method.

EBIT Net Operating Income.

EBT Earnings Before Taxes.

Net Income Profit attributable to the company´s shareholders.

Net Financial Debt Debt with banks and other financial institutions – Cash and equivalents – Other current and non-current Financial

Assets.

Adjusted Net Financial Debt Net Financial Debt including 50% of Chinese JV SAMAP net financial debt, consolidated by the equity method as per the

current partner agreements reached.

Normalized NFD/EBITDA Net Financial Debt including 50% of Chinese JV SAMAP net financial debt, on the las 12 months Ebitda, eliminating the

negative effects of 1Q due to Covid-19.

RONA = “Return on Net Assets” EBIT last 12 Months/ Net Assets (Fixed Assets + Net Working Capital - Goodwill not associated to cash outs).

Fixed assets Tangible assets and Intangible Assets, including Goodwill and without including rights of use over leased assets (IFRS

16).

Maintenance CAPEX The one related to the renovation of the facilities to face market growth.

Operating cash flow (%) EBITDA – Financial expenses paid – Tax payments – Maintenance CAPEX – Leases under IFRS 16

49APPENDIX II – 2019 ACQUISITIONS CIE GOLDE

PROFILE TRANSACTION

Specialisation Rationale

Design, engineering and • To reinforce its commitment to comfort systems and

manufacture of roofs for vehicles. increase its presence in the roof system segment. The

Footprint target company’s customers, markets and products

United States, Mexico, Germany, notably complement those of Advanced Comfort Systems

Slovakia, Romania, China and India. (ACS), the roof system unit CIE Automotive acquired in

No. of facilities 2009, since when it has doubled its revenue and boosted

12 factories. its EBITDA margin by 10 points.

6 R&D centres. • To become one of the top three global players in the

No. of employees roof system niche, which has been growing consistently

in recent years and not been affected by the

>2,700 employees.

hybridisation/ electrification processes.

Customers • To consolidate its strategic commitment to innovation

Top automotive OEMs.

and high-tech engineering by gaining access to new

2018 revenue highly complex and sophisticated products and

Almost 850 M€, including 50% of processes.

the SAMAP joint venture Price paid

Approx. 741 M€ (Enterprise Value ≈ 670 M€).

Transaction announcement date

17 September 2018.

CIE Transaction close

6 May 2019.

GOLDE

Roof Systems

Division of Inteva

50APPENDIX II – 2019 ACQUISITIONS AEL

PROFILE TRANSACTION

Specialisation Rationale

Aluminium injection • To add aluminium injection moulding technology in one

moulding. of the most promising markets - India - and diversify

Footprint MCIE India’s business, strengthening its presence in the

India. two-wheel segment.

No. of facilities • AEL is a key supplier for a considerable number of

3 factories. OEMs and Tier 1 suppliers in the passenger and two-

wheel vehicles segments in India and internationally. It

No. of employees

makes a large variety of bodywork, brake and engine

>2,300 employees.

parts using high-pressure and gravity injection processes.

Customers AEL also has machining, thermal treatment, coating,

OEMs and Tier 1 suppliers. assembly and leak testing capabilities, as well as modern

Passenger and two-wheel vehicles. tools and moulds.

2018 revenue Price paid

Approx. 108 M€ Approx. 111 M€ (Enterprise Value ≈ 111 M€).

Transaction announcement date

12 March 2019.

Transaction close

9 April 2019.

AEL

Aurangabad

Electricals Ltd.

51APPENDIX II – 2019 ACQUISITIONS CIE MAPREMEX

PROFILE TRANSACTION

Specialisation Rationale

Machined parts. • To leverage the acquired companies’ universe of

Footprint productive assets to complement CIE Automotive’s

México. existing manufacturing activities in Mexico and enable

No. of facilities physical and customer expansion going forward.

1 factory. Price paid

No. of employees Approx. 37 M€ (Enterprise Value ≈ 59 M€).

≈ 400 employees. Transaction announcement date

Customers 24 June 2019.

Tier 1 suppliers. Transaction close

2018 revenue 19 September 2019.

Almost 36 M€.

CIE

MAPREMEX

Maquinados de Precisión de

México S. de R.I. de C.V.

Cortes de Precisión de

México S. de R.I. de C.V.

52APPENDIX II – 2020 ACQUISITIONS CIE SOMASCHINI

PROFILE TRANSACTION

Specialisation Rationale

High precision gear systems and • Becoming a top global player within the

transmission solutions. precision gears segment, having presence within

Footprint the world’s largest 3 markets (Northamerica,

Italy and United States. Europe and Asia) and within various segments

No. of facilities (trucks, passenger vehicles, offroad, etc.). Being a

3 factories. global player means a clear competitive

No. of employees advantage when dealing with our clients.

• Somaschini provides further geographical

≈ 300 employees.

diversification and best in class technology with a

Customers very high degree of automatization.

OEMs, Tier 1s and Others │ Trucks,

passenger vehicles, industrial, and

Price paid

Approx. Enterprise Value 77 M€.

robotics.

2018 revenue Transaction announcement date

25 September 2019.

Almost 70 M€.

Transaction close

9 January 2020.

CIE

SOMASCHINI

SOMASCHINI-Somaschini

S.p.A.

SOM_NA-Somaschini North

America

SOM_SRL- Somaschini

Automotive SRL

53M A N A G I N G H I G H VA LU E A D D E D P R O C E S S E S 54

You can also read