COVID-19 Automotive demand post COVID-19 - Boston Consulting Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COVID-19 Automotive demand post COVID-19

Anticipate a prolonged Fight phase of 12-24 months

Scenarios and outcome driven by five key questions; shape varies based on regional assumptions

Illustrative

Flatten Fight Future

Shut down Restart Cure

Economic

activity 1a 2a

100% 3

2b Potential Pathways

1b

Critical care

patients

Five questions What will be the LENGTH of What will be the LENGTH of Where does the

1a 2a 3

will shape “Flatten”? “Fight”? economy return

the economic to relative to the

outcomes To what DEPTH does the What LEVEL of recovery does the pre-COVID era in

1b economy drop in “Flatten”? 2b economy achieve in “Fight”? “Future”?

Source: BCG AUTOMOTIVE DEMAND POST COVID-19

As of 15 May 2020

Fight: Auto sales in China on recovery path

Flatten Fight Future

2b | LEVEL of recovery

Vehicle sales Vehicle sales Vehicle sales

China1 Europe2 US3

-20% -46% -46%

-39%

+8%

-3%

-52%

~-80% 0%

-82% -7% -7%

Jan Feb Mar Apr Jan Feb Mar Apr Jan Feb Mar Apr

2019 2020

1. Passenger vehicles sales by month including Mini Vans; 2. New passenger car registrations by month, Europe = EU26 + UK + Iceland, Norway, Switzerland

2. 2020 estimate based on BCG analysis; 3. Light Vehicles (LV) include Passenger Vehicles (PV)

Sources: Marklines/China Association of Automobile Manufacturers (CAAM), ACEA actuals, Wards Automotive, BCG analysis and forecast AUTOMOTIVE DEMAND POST COVID-19

As of 15 May 2020

Economic forecasts deteriorating globally for 2020 while

remaining stable for 2021

Flatten Fight Future

2b | LEVEL of recovery

GDP growth forecast (YoY in %) GDP level forecast 2

2020 2021 EOY 2021 vs.

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% EOY 2019

China 1

1.2% 6.0% 5.8% 9.2%

107–112%

Europe2 -7.5% 1.3% 1.4% 4.7%

95–101%

US3 -5.9% Forecast 2.0% Baseline 1.7% 4.7%

97–100%

Forecast range

Forecast (IMF Apr 2020) Baseline (IMF Jan 2020) Forecast range (IMF & Banks3)

Note: As of reports dated 31 March 2020 to 05 May 2020, YoY forecasts 1. Announced by the German Federal Ministry for Economic Affairs and Energy on 29 Apr 2020

2. Range calculated with 25th & 75th percentile values of forecast range 3. Range from forecasts (where available) of International Monetary Fond, JP Morgan Chase; Morgan Stanley;

Bank of America; Fitch Solutions; Credit Suisse; Danske Bank; ING Group; HSBC Source: German Federal Ministry for Economic Affairs and Energy; Bloomberg; IMF; BCG analysis AUTOMOTIVE DEMAND POST COVID-19

As of 15 May 2020

Change in mobility behavior expected –

intentions stronger in China

Flatten Fight Future

3 | Return of economy in the FUTURE

Risk associated with mode of Mode of transport Change of likelihood to buy/

transport after lockdown usage after lockdown own car after COVID-19

Very Much more Much more

low risk frequent likely

-50%

>60% -60%

Very A lot less Much less

high risk frequent likely

Public transit Private car Public transit Private car Buying a car Owning a car

People see car as the safest Private car will be more preferred after Clear picture in China on trend towards

mode of transportation lockdown – especially in China buying/owning car while EU/USA are mixed

Source: BCG; Urban mobility study surveyed 5,000 people in large cities around the world AUTOMOTIVE DEMAND POST COVID-19

Four scenarios of the crisis are simulated along Flatten-Fight-Future

1 Optimistic 2 Most likely I 3 Most likely II 4 Pessimistic

GDP level

ARCHETYPE

V-shape V skewed to a U U-shape W-shape skewed to an L

MACROECONOMIC

Positive surprise in virus properties Virus properties stay or worsen Virus properties linger with Occurrence of 2nd wave with severe global impact

continued fear of mutation

Rapid catch-up in mitigation measures Mitigation efforts are slow / unsuccessful Repeated shocks on regional/local

and their effectiveness and have to be extended Mitigation efforts are intense, yet ultimately level lead to frequent lockdowns

unsuccessful

Significant monetary and fiscal response Household & business confidence falls Severe depression of household

& remains depressed (08/09 crisis) Heightened incidents as economies reopen & business confidence

Household and business spending

necessitate new shutdowns

stays largely in tact Rebound through governmental Severe implications on labor, capital and

support in investments, business Household & business confidence remains productivity of the economy

Few businesses fail, unemployment

sector and households depressed

recovers from initial dip Economy increasingly embraces remote working

Financial system begins to show cracks

AUTO

Government backed incentives and cheap Confidence slowly increasing, supported by New vehicle sales remain depressed as market Auto supply chains severely disrupted

credit spur quick recovery government incentives moves into prolonged economic downturn

Continued shutdowns e.g., plants, dealers

Deferred automotive demand recovered Demand partly recovered, yet significant Significant portion of sales lost

Lingering change to consumer mobility

portion of sales lost in ‘20

patterns; Immense loss of sales

UNLIKELY COVID-19 CRISIS MOST LIKELY UNLIKELY

Source: BCG analysis

IN RANGE OF THESE SCENARIOS AUTOMOTIVE DEMAND POST COVID-19

As of 19 May 2020

Automotive Demand: Also in mid-term significant global impact

Sales forecast for CN, EU, US

(vehicle units in M)

Most likely scenario

-14% -6% -1% +4% +7% +9% -12% -3% +1% +7% +10% +12%

Most likely I Optimistic

68.4 70.2

scenario 62.5 61.8

65.0 66.8

scenario 62.5 63.1

66.6 68.6

59.0 60.7

53.4 55.2

27.4 28.4 29.4 28.0 29.1 30.1

24.8 25.7 24.8 26.2

24.8 25.4

22.8 23.4

20.5 19.8 21.0 21.4 21.8 20.5 19.8 20.3 21.4 22.0 22.5

16.8 19.2 17.5

17.1 13.8 15.0 16.2 16.7 17.1 17.1 17.1 14.2 15.4 16.6 17.1 17.5 17.6

2019 2020 2021 2022 2023 2024 2025 2019 2020 2021 2022 2023 2024 2025

-22% -7% -4% 0% +3% +5% -28% -15% -13% -11% -8% -6%

Most likely II Pessimistic

65.6 62.5

scenario 62.5

58.0 59.9

62.2 64.1

scenario 55.9 57.5 58.9

53.2 54.0

49.0 24.8

24.8 26.5 27.6 28.5 45.1

25.4

24.2 25.0 21.9 22.4 23.7 24.6

22.1 20.9

20.5 20.0 20.5 21.0 20.5

18.9 19.5 17.4 17.7 18.0 18.4 18.8

14.8 13.5

17.1 12.2 15.0 16.2 15.7 16.1 16.1 17.1 13.8 14.0 14.2 14.5 14.6

10.7

2019 2020 2021 2022 2023 2024 2025 2019 2020 2021 2022 2023 2024 2025

China Europe USA

Source: BCG Automotive Demand Model; IHS; BCG Analysis AUTOMOTIVE DEMAND POST COVID-19Next step: Please feel free to reach out regarding our tools/insights

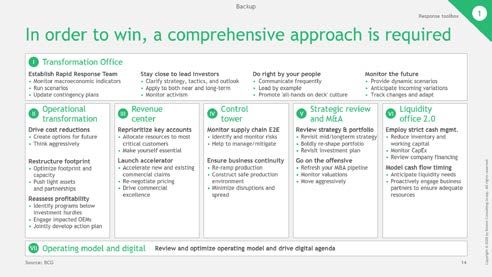

1 Response

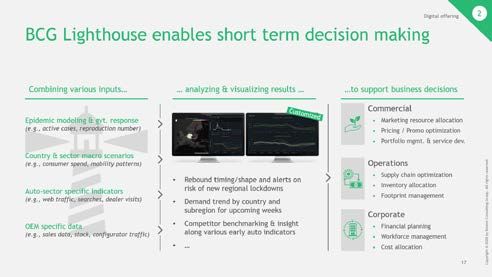

toolbox 2 Digital

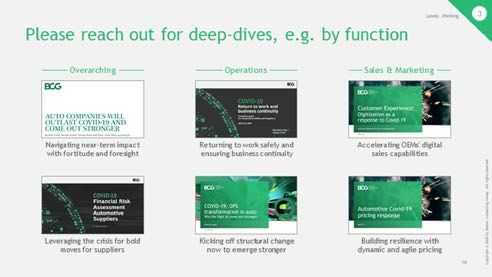

offering 3 Our latest

thinking

Comprehensive approach to Mid-long-term: Demand scenarios Overarching and functional deep-

managing COVID-19 response and P&L / cash flow wargaming dive material on demand

Handle immediate response Short-term: Monitor and analyze Regular publications on crisis,

and leverage crisis in long-term indicators for decision support necessary actions & impact on auto

Source: BCG AUTOMOTIVE DEMAND POST COVID-19COVID-19 Disclaimer

The situation surrounding COVID-19 is dynamic and rapidly evolving, on a daily basis.

Although we have taken great care prior to producing this presentation, it represents

BCG’s view at a particular point in time. This presentation is not intended to: (i)

constitute medical or safety advice, nor be a substitute for the same; nor (ii) be seen

as a formal endorsement or recommendation of a particular response. As such you

are advised to make your own assessment as to the appropriate course of action to

take, using this presentation as guidance. Please carefully consider local laws and

guidance in your area, particularly the most recent advice issued by your local (and

national) health authorities, before making any decision.

AUTOMOTIVE DEMAND POST COVID-19Disclaimer

The services and materials provided by Boston Consulting Group (BCG) are subject to BCG’s Standard Terms (a copy of which is available upon

request) or such other agreement as may have been previously executed by BCG. BCG does not provide legal, accounting, or tax advice. The Client

is responsible for obtaining independent advice concerning these matters. This advice may affect the guidance given by BCG. Further, BCG has

made no undertaking to update these materials after the date hereof, notwithstanding that such information may become outdated or inaccurate.

The materials contained in this presentation are designed for the sole use by the board of directors or senior management of the Client and solely

for the limited purposes described in the presentation. The materials shall not be copied or given to any person or entity other than the Client

(“Third Party”) without the prior written consent of BCG. These materials serve only as the focus for discussion; they are incomplete without the

accompanying oral commentary and may not be relied on as a stand-alone document. Further, Third Parties may not, and it is unreasonable

for any Third Party to, rely on these materials for any purpose whatsoever. To the fullest extent permitted by law (and except to the extent

otherwise agreed in a signed writing by BCG), BCG shall have no liability whatsoever to any Third Party, and any Third Party hereby waives any

rights and claims it may have at any time against BCG with regard to the services, this presentation, or other materials, including the accuracy or

completeness thereof. Receipt and review of this document shall be deemed agreement with and consideration for the foregoing.

BCG does not provide fairness opinions or valuations of market transactions, and these materials should not be relied on or construed as such.

Further, the financial evaluations, projected market and financial information, and conclusions contained in these materials are based upon

standard valuation methodologies, are not definitive forecasts, and are not guaranteed by BCG. BCG has used public and/or confidential data and

assumptions provided to BCG by the Client. BCG has not independently verified the data and assumptions used in these analyses. Changes in the

underlying data or operating assumptions will clearly impact the analyses and conclusions.

AUTOMOTIVE DEMAND POST COVID-19You can also read