Current prospects for a strong European automotive supplier industry - Way forward - Steering automotive supply business through turbulent times ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Current prospects for a strong European automotive supplier industry Way forward – Steering automotive supply business through turbulent times Webinar 19 May 2020

Your contacts:

Dipl.-Vw. Christoph Stürmer

Autofacts Global Lead Analyst

Tel.: +49 69 8595 6269

christoph.stuermer@pwc.com

• Automotive market analysis and forecasting

• Business model assessment and risk analysis

• Market and brand strategy

• Product portfolio management

• Industry transformation scenario modelling

Dipl.-Ing. Henning Rennert

Partner Strategy&

Tel.: +49 160 9555 3583

henning.rennert@strategyand.de.pwc.com

• 12 years industry experience

• 13 years consulting experience

• Product- and technology strategy

• Efficiency improvement

• Product value management

19 May 2020

Strategy& 2

Today we report about two topics: OEM production prognosis and

corresponding supply chain dynamics

PwC perspective

1 We as PwC Auto practice operate our analyst expert team Autofacts …

2 ... delivering an independent market perspective …

3 … touching key questions of the industry, e.g. governmental incentives ...

4 … and regionalization of supply chains – a new trend?

5 In cooperation with CLEPA – Thanks

Current prospects for a strong European

automotive supplier industry 19 May 2020

Strategy& 3

Agenda 1. Global Production Outlook 2. Dynamics in the automotive supply chain - impulses for a new tomorrow Current prospects for a strong European automotive supplier industry 19 May 2020 Strategy& 4

Risk Assessment Status as of May 13, 2020

The prolonged COVID-19 mitigation measures have significantly

impacted global vehicle demand, production and value chains

Possible scenarios Risk assessment of global vehicle production1) 2020

Global vehicle production in mn

• Original Base Case

• After a decline in production due to plant shutdowns of 3-4 10

YTD April numbers

weeks that have originally been announced, production can

1 Impact be resumed without restriction for the most part 9

partially estimated

• Production shortfalls in the months February to April will not be 8

made up but merely return to expected rates in 2nd half year

7 6.7 6.6 6.7

• After the end of social measures, broad-based incentive 6.2 6.1 6.0

5.7 5.7 6.2

schemes unleash pent-up demand especially in China and EU 6 5.6 5.5 6.0

2 Incentive

• Due to coordinated planning, vehicle production and supply 4.8

5.6

4.9 5.5 5.6

chains are recovering rapidly – China up to 80% utilization 5 4.5 4.4 4.9

4.8 5.0

4.6 4.6

4 4.4 4.4

4.2

• Actual Base Case

3.5 3.6 3.6

• Based on prolonged measures, shutdowns continue into May 3

Deep 2.0

3 – with production recovering only slowly in Q2

Impact 2

• Disruptive effects on the demand side and suppliers/logistics 2.0

Base scenario (without influence of COVID-19)

lead to significant downturn over several quarters 1

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

• First wave of measures to be quickly relieved due to initial Total 2020 Base Impact Incentive Deep Impact Double Dip

containment successes (see “Impact” scenario) forecast

Double

4 • After summer, a second COVID-19 infection wave to follow, per

Dip contained more effectively with more targeted measures scenario 73.6 64.4 (-12%) 58.4 (-21%) 51.0 (-30%) 58.6 (-20%)

• Overall effect is structural and extends into the following year

Current prospects for a strong European

automotive supplier industry 1) Passenger Cars (incl. light duty LCV in USA) mn: million 19 May 2020

Strategy& Source: PwC Autofacts analysis V 5 as of May 13, 2020 Base case forecast: IHS Markit Release Q1 2020 5Europe:

COVID-19 measures are showing a scalable impact on demand

PC* sales: Risk assessment for sales 2020

2.0

• European demand was Actuals

increasingly stopped in March 1.5

2020, as a direct effect of the

1.0

measures to contain COVID-19.

On the basis of available data, 0.5

new car registrations in Western

0.0

Europe in March fell by about 53% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

compared to the previous year, the

quarter by 27%. Scenario Sales (in millions) Effect Result

• State incentive schemes if 2019 15.9 Basis of comparison

repeated from 2009 will create • -56% in May vs. 2019

Incentive 10.8 -32.1%

significant market distortions and • -7% in H2 vs. 2019

mostly sell pre-produced vehicles; • -35% in May vs. 2019

Impact 12.2 -23.6%

• Recovery in second HY

incentives on eco-cars only would

• -56% in May vs. 2019

fail to create significant volume Deep Impact 9.8 -38.4%

• -20% in H2 vs. 2019

effects. • -35% in May vs. 2019

Double Dip 11.1 -30.5%

• -53% in October vs. 2019

Current prospects for a strong European

automotive supplier industry Basis 2019 Impact Scenario 2020 Double Dip 2020 19 May 2020

Strategy& Incentive Scenario 2020 Deep Impact Scenario 2020 6Europe:

Could electric vehicles save the industry in 2020?

Alternative Fuel Vehicle Sales

• Electrified vehicles are expected to secure growing market

shares due to high customer demand and an expanded 85,2% 8,4%

product offering. Targeted subsidies and sales support have

proven highly effective in overcoming buyer objections.

• Limited production flexibility, lacking product availability and 2,7%

oversold production volumes give AFV a more stable sales

performance, but limit the potential to support the total market. 3,7%

2020 Q1 Comparison to 2019 Q1 Top-5 (YTD March)

Total Sales 2,115,581 100%

BEV 79,000 +120%

of which AFV 312,626* 14.8%

PHEV 56,000 +149%

of which BEV 79,300* 3.7%

Hybrid 177,000 +27% of which PHEV 56,118* 2.7%

Total 313,000 +58% of which Hybrid 117,208* 8.4%

Strategy&Europe:

Vehicle production affected by the decline of local and global demand

PC* production: Risk assessment for production 2020

2.0

Actuals

• Short-term: Based on available 1.5

information, we estimate

1.0

production to have fallen by about

45% in March compared to 2019, 0.5

and to literally be at a complete

0.0

standstill in April at -97% versus Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019.

• Medium-term: Due to dramatic Scenario Production (in millions) Effect Result

pandemic effects, Italy decreed 2019 15.3 Basis of comparison

the closure of all factories on 22 • -58% in May vs. 2019

Incentive 11.0 -28.3%

March after FCA had already • -13% in H2 vs. 2019

stopped vehicle production, as Impact 13.0 -15.3%

• -10.7% in Version 4.1

• Stronger losses in April

well as in Spain.

• -58% in May vs. 2019

Deep Impact 10.0 -34.6%

• -26% in H2 vs. 2019

• -15.7% in Version 4.1

Double Dip 12.0 -21.2%

• -45% in October vs. 2019

Current prospects for a strong European

automotive supplier industry Basis 2019 Impact Scenario 2020 Double Dip 2020 19 May 2020

Strategy& Incentive Scenario 2020 Deep Impact Scenario 2020 8Risk Assessment Status as of May 13, 2020

Europe:

For the longer term, we assume a full recovery taking beyond 2021

Base Case: Deep Impact Scenario/ U-Shaped Crisis

Comments

18

• Starting in Q4 2018, European production was sent on a

downward trajectory due to (mismanagement of) certification

PC Production Western Europe [Mio].

16 16.7

changes and regulatory changes 16.2

15.3 15.1

14 14.5

• As the industry started to move into 2020 with uncertain

outlook, the COVID-19 freeze-up hit in the wake of numerous 13.3

12

critical product and production ramp-ups, specially of BEV and

PHEV variants which are still short in supply 10

10.3

• Impacts from COVID-19 measures are expected hit economies

8

across Europe deeply, to a level estimated larger than the global

financial crisis: unemployment, company failures, personal

defaults will have negative impact on private and corporate 6

purchasing power and willingness-to-spend

4

• Although state incentives may support short-term demand on

retail and OEM level, following increased taxes and restricted 2

Basis Impact Incentive Deep Impact Double Dip

infrastructure spending will slow down long-term growth and

civil development; changes in mobility preferences will require 0

rapid adaption of industry transformation strategies 2017 2018 2019 2020 2021 2022 2023

Current prospects for a strong European

automotive supplier industry 19 May 2020

Strategy& 9While markets in Europe collapse, USA and China show less decline

The year 2020 up to April

• Collapse of European new car registrations in April:

Sales Decrease vs.

Country

Decrease* YTD Apr 19 – UK, Spain, Italy all lose 99% of registrations to about 4,000 units

China -2,409,501 -35.9% – France loses “only” 89%, Germany 61% vs. April 2019

Japan -220,724 -13.9% – Full stop of sales as social distancing measures take hold

South Korea -18,637 -4.0%

– No alternative means of marketing, sales and registrations established

USA -976,308 -22.7%

– Registration offices mostly closed, so eventual sales not recorded

Rest of NA -271,839 -33.6%

– Used car markets and aftermarket impacted, but still working

Germany -368,605 -31.0%

UK -374,222 -43.4%

France -355,854 -48.0% • Resilience in USA and China:

Italy -361,380 -50.7% – Both markets operate on a stock-based sales model (build-to-stock)

Spain -213,441 -48.9%

– Dealers operate independently and bill their own cars

Remaining EU -584,252 -37.2%

– Ad-hoc online marketing, sales and alternative delivery sprung up

ROW -1,670,742 -32.0%

– More digital-savvy clients and easier legal prerequisites in China

Total -7,866,414 -31.9%

– Sales reported by wholesale/ retail companies, not registration offices

Current prospects for a strong European

automotive supplier industry 19 May 2020

Strategy& 10A few do‘s and don‘ts of incentive programs

Comparison of 2009 to 2020

• Incentive Programs 2009 • Recommendations for 2020

– Different programs in different European countries – Coordinated approach across all countries

– Small programs proved ineffective – Significant billion-Euro size required for credible effects

– Included in-stock and pre-registered vehicles – Only effective for suppliers if focused on new vehicles,

while aftermarket offers complementary opportunities

– Full focus on just automotive retail created a time lag for

effects on production – Overstocking not as pronounced as 2020 allows for

quicker transmission into new-car production

– Scrappage schemes lead to over-proportionate demand

for lowest-price vehicles and import production – Incentives should focus on potential average new-car

buyers in order to focus on demand creation

– General support of “up-to-date” vehicles without

technical discrimination (France offered CO2 bonus) – Too narrow focus on e.g. electric/ plug-in vehicles would

aggravate supply shortages but not support total market

– Showroom traffic was greatly increased due to possible

bargains after the immediate effects of the crisis – Positive secondary effects only to be expected when

overall consumer confidence has stabilized

Current prospects for a strong European

automotive supplier industry 19 May 2020

Strategy& 11Agenda 1. Global Production Outlook 2. Dynamics in the automotive supply chain - impulses for a new tomorrow Current prospects for a strong European automotive supplier industry 19 May 2020 Strategy& 12

The COVID-19 outbreak makes transparent that the automotive supply

chain is far from invulnerable – will the structure change?

Takeaways

Rethinking the global supply chain

1 The current COVID-19 crisis has made the European automotive industry aware of its dependence on Asian suppliers - current supply

chains are being questioned and rethought

Additional cost down push by OEM

2 In addition to the strategic considerations, the redesign of the supply chain comes together with an additional price push by the OEMs

Insourcing an option again?

3 In addition to direct dependency, topics such as intellectual property, strengthening core competencies and the utilisation of the

company's own workforce are coming back into focus - insourcing seems to be an option in selected cases again

Restructuring as chance for a new tomorrow

4 Combination of relocation and upstream product cost reduction and product qualification: Using the crisis for success!

Current prospects for a strong European

automotive supplier industry 19 May 2020

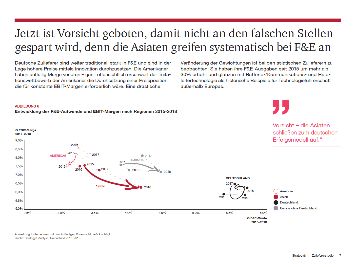

Strategy& 13The crisis demonstrates the high dependency on global suppliers and

might lead to a trend towards more regionalization

Trend towards regionalization after the crisis Calls for more regionalization after the crisis

Foreign trade and dependency on China - quote from Automobil-Industrie

Germany’s auto parts exports to China (in k USD)1)

2015

21.04.2020

2016

+3.7% “Manufacturing in the market for the market and

2017 purchasing components there. We will certainly

CAGR

2018

Dr. Holger

continue to optimize this principle and thus operate

2019 Engelmann, CEO even more regionally. …. taking greater account of

of Webasto SE the regional aspect in the future.”

0 2,000,000 4,000,000 6,000,000 8,000,000 10,000,000 12,000,000

Germany’s auto parts imports from China (in k USD)1)

2015

2016

2017

+11.0%

CAGR 24.04.2020

2018 “The Corona crisis has shown that supply chains in the

2019 automotive industry are heavily dependent on Asia.

0 2,000,000 4,000,000 6,000,000 8,000,000 10,000,000 12,000,000 Dr. Stefan Wolf,

In my opinion, adjusting supply chains more locally

Chairman of the and relying more on solid suppliers in Germany or

board of Elring Europe would be the right way to get out of the one-

Klinger sided dependence on individual regions.”

Dependence on China increases

Current prospects for a strong European

automotive supplier industry 1) Source: ITC – Bilateral trade statistics between Germany and China: Parts and accessories for tractors, motor vehicles for the transport of ten or more persons, motor cars 19 May 2020

Strategy& and other motor vehicles principally designed for the transport of persons, motor vehicles for the transport of goods and special purpose motor vehicles 14To fundamentally understand if there is a trend or not, we conduct a

joint survey. Please join

Dynamics in the Automotive Supply Chain – Impulses for a new tomorrow

Intention of the survey Your participation in our survey

The COVID-19 outbreak makes transparent that the

Survey consists of 12 questions

supply chain is far from invulnerable. It has triggered a

discussion whether the current supply chain needs to

evolve towards a more regional and diversified setup. Takes about 15 minutes of your time

CLEPA and PwC Strategy& collects firsthand We kindly ask you to indicate your company

information to better understand the current situation.

We ensure that data is kept secure

The anonymized results of the survey will be Scan this QR-Code

published in the form of a study.

to get to the

survey!”

Source:

PwC Strategy& https://pwc.qualtrics.com/jfe/form/S

Automotive Supplier

Study 2019

V_77i7TTtrNKpz3yB

Automotive Supplier Study 2020 How to get to the survey?

Current prospects for a strong European

automotive supplier industry 19 May 2020

Strategy& 15Global:

In consequence, vehicle demand is heavily impacted by the shutdowns

PC* sales: Risk assessment for sales 2020

10.0

Actuals

8.0

6.0

• Demand is returning to the end of 4.0

local restrictions at different rates, 2.0

with labour market effects 0.0

amplifying the impact Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

• Production bottlenecks caused by

Scenario Sales (in millions) Effect Result

logistical and financial problems of

global suppliers determine the 2019 75 Basis of comparison

production ramp-up in Q2 2020 • -14.3% in Version 4.1

Incentive 60.4 -19.4%

• Lowered expectation for China

• -13.7% in Version 4.1

Impact 65.0 -13.2%

• Recovery in the 2nd HY

• -36.8% in Version 4.1

Deep Impact 53.0 -29.2%

• More positive outlook for China

• -19.5% in Version 4.1

Double Dip 59.3 -20.9%

• -33% in October vs. 2019

Current prospects for a strong European

automotive supplier industry Basis 2019 Impact Scenario 2020 Double Dip 2020 19 May 2020

Strategy& Incentive Scenario 2020 Deep Impact Scenario 2020 16USA:

Extended containment follows the Deep Impact scenario path

PC* sales: Risk assessment for sales 2020

1.4

Actuals

1.2

• After initial slumps in California 1.0

and New England (New York, 0.8

0.6

Boston), vehicle retail showed

0.4

surprising resilience in April.

0.2

• The sharp rise in unemployment is 0.0

dampening purchasing power. Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

• In April, vehicle production came

Scenario Sales (in millions) Effect Result

to an almost complete standstill.

2019 13.5 Basis of comparison

• In the meantime, we don‘t expect • -42% in May vs. 2019

Incentive 9.6 -28.9%

a restart before mid-May (Deep • -29% in H2 vs. 2019

Impact Scenario), so that a catch- Impact 12.0 -11.3%

• -33% in May vs. 2019

• Recovery in the second HY

up process lasting several years is

to be expected, as after 2008/09. • -42% in May vs. 2019

Deep Impact 9.0 -33.4%

• -38% in H2 vs. 2019

• -32% in May vs. 2019

Double Dip 11.0 -17.7%

• -8% in October vs. 2019

Current prospects for a strong European

automotive supplier industry Basis 2019 Impact Scenario 2020 Double Dip 2020 19 May 2020

Strategy& Incentive Scenario 2020 Deep Impact Scenario 2020 17China:

Demand shows surprising resilience while production returns

PC* sales: Risk assessment for sales 2020

3

Actuals

• Judging from the example of 2009, 2

incentives on car taxations and

financing can unleash pent-up 1

demand from 2017-18, while

installed capacity allows for 0

production of up to 5 million units Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

per month.

Scenario Sales (in millions) Effect Result

• The release of the supplier and

2019 21.1 Basis of comparison

manufacturer plants allows a rapid

• +16.6% in Version 4.1

start of production; however, JV Incentive 20.4 -3.4%

• +22% in H2 vs. 2019

plants of foreign brands still suffer • -12% in May vs. 2019

Impact 18.6 -12.3%

in part from a lack of supply from • Recovery in the second HY

international suppliers. Deep Impact 17.0 -19.5%

• -37.3% in Version 4.1

• -Takeover of PwC China

• -12% in May vs. 2019

Double Dip 15.7 -25.9%

• -49% in October vs. 2019

Current prospects for a strong European

automotive supplier industry Basis 2019 Impact Scenario 2020 Double Dip 2020 19 May 2020

Strategy& Incentive Scenario 2020 Deep Impact Scenario 2020 18You can also read