DIVERSIFIED GAS & OIL PLC - INVESTOR PRESENTATION JANUARY 2018 - cloudfront.net

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DIVERSIFIED GAS & OIL P L C

I N V E S T O R P R E S E N TAT I O N

JANUARY 2018

CONFIDENTIAL

January 2018 Investor Presentation

DISCLAIMER

The information contained in this document has been prepared by Diversified Gas & Oil PLC (the “Company”). This document is being made available for information purposes only and does not

constitute an offer or invitation for the sale or purchase of securities or any of the assets described in it nor shall they, nor any part of them, form the basis of or be relied on in connection with, or

act as any inducement to enter into, any contract or commitment whatsoever or otherwise engage in any investment activity (including within the meaning specified in section 21 of the Financial

Services and Markets Act 2000).

The information in this document does not purport to be comprehensive. While this information has been prepared in good faith, no representation or warranty, express or implied, is or will be

made and no responsibility or liability is or will be accepted by the Company or any of its officers, employees, agents or advisers as to, or in relation to, the accuracy or completeness of this

document, and any such liability is expressly disclaimed. In particular, but without prejudice to the generality of the foregoing, no representation or warranty is given as to the achievement or

reasonableness of any future projections, management estimates or prospects contained in this document. Such forward-looking statements, estimates and forecasts reflect various assumptions

made by the management of the Company and their current beliefs, which may or may not prove to be correct. A number of factors could cause actual results to differ materially from the

potential results discussed in such forward-looking statements, estimates and forecasts including: changes in general economic and market conditions, changes in the regulatory environment,

business and operational risks and other risk factors. Past performance is not a guide to future performance.

The document is not a prospectus nor has it been approved by the London Stock Exchange plc or by any authority which could be a competent authority for the purposes of the

Prospectus Directive (Directive 2003/71/EC). This document has not been approved by an authorised person for the purposes of section 21 of the Financial Services and Markets

Act 2000.

The information contained in this document is subject to change, completion or amendment without notice. However, the Company gives no undertaking to provide the recipient with access to

any additional information, or to update this document or any additional information, or to correct any inaccuracies in it or any omissions from it which may become apparent.

Recipients of this document in jurisdictions outside the UK should inform themselves about and observe any applicable legal requirements. This document does not constitute an offer to sell or

an invitation to purchase securities in any jurisdiction.

1

January 2018 Investor Presentation

MARKETING PURPOSE

Acquire Two Transformative Packages for $180M* in Cash

Target: Alliance Petroleum Corporation - $95M Target: “Mountaineer”** - $85M

$180M Equity Capital Raise

Progresses Stated Strategy

Geographic Concentration Drives Enhances per share Further Positions DGOC

Efficiency Cash Flow & Dividend as Consolidator

Footnotes:

* Net of expenses

** “Mountaineer” is a code name

2

INTRODUCTION TO DGOC

Our Current Business

3January 2018 Investor Presentation

CORPORATE OVERVIEW: DIVERSIFIED GAS & OIL PLC

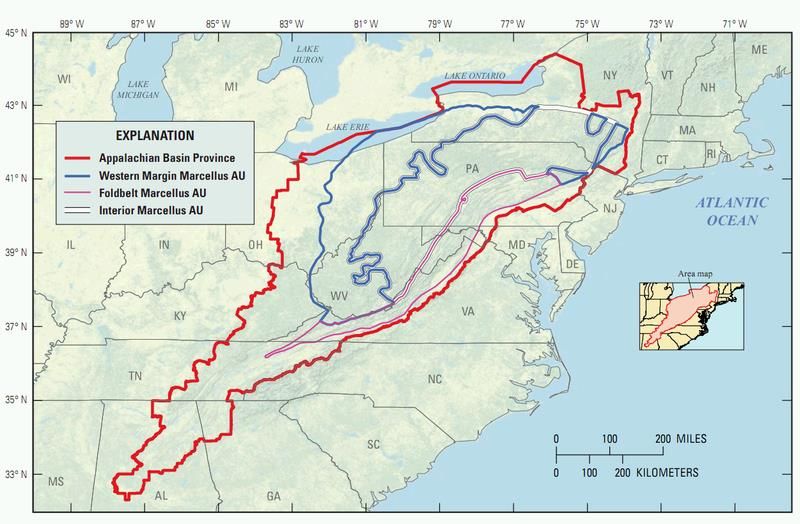

APPALACHIAN BASIN GAS AND OIL PRODUCER

Corporate Profile Today

Exchange Listing Details AIM DGOC

DGOC Focus Area

Net Daily Production MBoe per Day 10.3

(a)

Net PDP Reserves MMboe 54.6

Ordinary Shares in issue #M 145.1

Share Price (18 Jan 2018) GBp/share 88.50

Market Capitalisation(b) US$M $178

Net debt (a) US$M $58

Enterprise Value(b)(c) US$M $236

Regional Profile – Appalachian Basin

Established Oldest hydrocarbon producing region in the US

Sustainable Long reserve life (~40 to 50+ years per well) with low plugging costs (~$10k/well)

Productive Basin produces ~24 Bcf/d Natural Gas with >1 million wells drilled (high success rate)

Active Abundant infrastructure that continues to attract new investment with conventional & horizontal development

Predictable Geologically prolific, long-life shale rock in Marcellus/Utica and conventional reservoirs

Stable Basin located within the continental United States with a stable and industry-friendly political environment

Growing Conducive environment; DGO ~80% Production CAGR since 2012; Significant pending acquisitions ($180M)

Footnotes: (a) Estimated as of December 31, 2017; (b) As of 18 January 2018 based on a closing price of 88.50 GBp; (c) Assumes a USD:GBP exchange rate of $1.38

4January 2018 Investor Presentation

COMPANY HISTORY MARKED BY GROWTH

Gross

Boe/

18,000 day

~80% Gross

‘17 Production

CAGR from 2012

to Jun17

Feb:

Floated on AIM raising

Gross $50m – largest UK O&G

Boe/ IPO since April 2014

4,333 day

Apr:

Gross Acquired producing wells in

Gross Boe/

Ohio and Pennsylvania for

Gross Boe/ 1,833 day ‘16 $1.75m

Boe/ 1,167 day

1,000 day

June:

Founded

‘15 Acquired producing wells

‘14

‘10 from Titan for $72.8m;

‘01 Successfully listed Raised add’l $35m through

Entered Ohio bond on ISDX secondary offering on AIM

Growth Market, which

Acquired producing raised £10.6m September:

wells from AB Acquired producing wells Closed on the remaining

Acquired assets of Titan wells held within

Resources for Acquired producing wells from Eclipse Resources

Diversified public partnership

$14.5m from Broadstreet Energy for $4.8m

Resources Inc. for structures (incl. 29 Hz

for $2.6m

$5.2m Acquired producing Acquired producing Acquired producing wells wells) for $11.4m

wells from Deep wells from Operated Acquired producing wells and pipeline assets from

Assets located in Resources, for Equity Investment and equipment from Seneca Resources for December:

West Virginia $5.5m (Fund 1) for $4.3m Texas Keystone for $725k $7.0m Acquired producing wells

from NGO for $3.1m

5January 2018 Investor Presentation

A UNIQUE OPPORTUNITY; ACHIEVING SCALE THROUGH ACQUISITIONS

Established, Profitable & Growing

• Founded in 2001 by the CEO with ~80% CAGR of production since 2012

• Over 10,300 net barrels of oil equivalent (“Boe”) production per day(a)

• 54.6 million Boe Proved-Developed-Producing reserves (significant, unrecorded PUD & 2P potential)(b)

Differentiated

• Low political and operational risk; 100% US onshore operations with stable, long-life production

• Low operating costs & maintenance capex; Averaging $7.46/Boe ($1.24/Mcfe) for the past six months(c)

• Cash-flow positive; +40% Adjusted EBITDA margins(c)

Proven Dividend Model

• Target dividend of ~40% of free cash flow (Paid $0.0398/share in 2017)

• Increasing Yield: 5.7% estimated yield on 2018 Dividends (before acquisitions)(d); 4.3% yield on 2017 Dividends(e)

• More than 75% above the average yield of the two other UK Listed independent E&Ps paying a regular dividend(d)

Value Creating

• Deep relationships in the industry support consistent and accretive deal execution

• History of success completing acquisitions; ~$135 million of transactions completed; $180 million expected in 1Q18

• Operational excellence & Strong balance sheet / liquidity position; Low unit OpEx cost; $50 million of liquidity(f)

Footnotes: (a) Net daily production rate is based on Dec17 “exit rate”; (b)Estimated as of 31 December 2017; (c) For the months June - November 2017; (d) Source: Bloomberg as of 18 Jan 2018; Peers include SEPL & SIA; Estimated yield excludes impact

of acquiring the two target acquisitions discussed within this presentation; (e) Assumes an average share price of $0.70 and $0.0399 total dividends; (f) At 31 December 2017 inclusive of $15 million cash + $35 available on credit facility.

6January 2018 Investor Presentation

OUR BUSINESS MODEL

Value Balanced ~6% 2018E Dividend Yield(a)

6.0%

• Disciplined pursuit of cash producing • Finance acquisitions with a proper 36% Equity Return

assets available at low multiples balance of debt and equity to maintain since IPO (b)

a strong balance sheet

5.0%

Peer Average Yield:

3.3%

Stable Efficient 4.0%

• Maintain a strong balance sheet and • Maintain efficient cost structure by

low leverage at reduced commodity spending only what is necessary 3.0%

prices 5.7%

2.0%

3.8%

Consistent Returns 1.0%

2.7%

• Manage producing wells to maintain • Return meaningful cash to

shallow declines and maximize shareholders through the dividend

economic recoverable reserves

0.0%

DGOC Peer 1 Peer 2

Footnote: (a) Source: Bloomberg as of 18 Jan 2018; Peers include SEPL & SIA; (b) From IPO on 3 Feb 2017 (£0.65) to 18 Jan 2018 (£0.885)

7January 2018 Investor Presentation

TRACK RECORD OF DELIVERING STATED OBJECTIVES

Successful AIM IPO • Largest AIM E&P IPO since 2014

• One of only three UK Listed E&P (of 90) to pay a regular dividend(a)

• $160m of capital raised in 2017(b); maintaining low leverage profile

Financially Strong • $50m of liquidity at 31 December 2017 ($15 cash + $35 undrawn credit facility)

Significant Production • 2017 Exit rate of >10,300 net barrels of oil equivalent production per day

• Significant producer on AIM; Growing rapidly through acquisitions

• >90% of long-life, low-decline wells located within a radius of ~200 kilometers

Increasing Scale • Closed three acquisitions since February 2017 IPO, incl. one transformative

• Strong pipeline of compelling opportunities with others emerging

Reducing Costs • Adjusted EBITDA margin averaging >40% from June to November 2017

• Integration and optimization of Titan acquisition continues

• 5.7% estimated 2018 dividend yield before target acquisitions(c)

Dividend Paying • 4.3% 2017 yield

• 75% above the average of other UK Listed E&Ps regularly paying a dividend(c)

Footnote: (a) Dividend paying companies include DGOC, SEPL & SIA; (b) Includes $85m of equity capital and $75m of debt capital; (c) Source: Bloomberg as of 18 Jan 2018; Peers are listed in footnote (a).

8January 2018 Investor Presentation

STRATEGY: ACQUIRE, PRODUCE, DRILL

I Price acquisitions as a multiple of cash flows from existing production; Pay

N

nothing for undeveloped resource

O

R Source: Large energy players looking to reduce operating expenses and

G re-focus their limited financial & personnel resources on shale

A

N Target: Predictable production rates, long-life (50+ years), low declines

I

C Focus: On asset attributes & scale vs. location (Geographically agnostic)

Acquire and manage O

producing natural gas N

Deploying rigorous field management programmes

and oil properties to G

O Reduce unit operating costs and improve margins

generate cash flows, I

providing stability and N Optimize production by managing compression; perform low-cost workovers

growth for our G

stakeholders

O

R Focus on conventional formations

G

A

Strict control of drilling and completion costs

N Increased drilling in higher price environment

I

C

o Progressive dividend

o Improving gross margins

o Reduced unit operating costs

o Strong free cash flow generation

9January 2018 Investor Presentation

OUR ASSETS: LOW RISK, LOW COST, LONG LIFE

DGOC operates a large portfolio of producing wells driving stable cash flows

Low risk (political & operational; US Onshore) producing gas

and oil assets (Average Production Mix: +95% natural gas)

Shallow depth (~3,000’ to ~6,000’), vertical wells into low

permeability reservoirs sitting above the shale

Mature wells benefitting from:

• Low operating costs (~$1.24 LOE/mcfe(a); Ongoing optimizing)

• Low ongoing/maintenance capex (~$1.0m - $1.5m/year)

• Low water production (~1/3 Bbl per well per day)

Low decline rates averaging 3-5% per annum, enabling a high

quality and reliable stream of free cash flow

Long well life estimated from 40-50+ years with significant well control

Attractive fiscal regime further improved by recent US tax reform

as corporate tax rate drops from 35% to 21%

Footnotes: (a) Average for the months June - November 2017

10PENDING TRANSACTIONS

Further Transforming DGOC

11January

January

2018

2018

Investor

Investor

Presentation

Presentation

ESTABLISHED, LARGE, INDEPENDENT APPALACHIA PRODUCER

Addition of two strategic and accretive acquisitions achieves significant scale and economies in the Basin

Highlights

Pennsylvania

✓ Broad base of producing wells provides for

consistent, stable production, cash flows and

dividends

Ohio

✓ Tight geographical profile provides significant

economies driving down unit operating and

overhead costs through shared facilities, optimized

labor allocation, enhanced vendor management, etc.

✓ Reserves are 100% PDP with estimated remaining

lives of ~50 years, with significant 2P & 3P potential LEGEND:

Legacy

West Virginia

✓ Large Undeveloped HBP Acreage position provides Alliance

a significant organic growth platform Mountaineer

✓ Successful execution of large transactions PRO FORMA INFORMATION:

establishes DGOC as the consolidator of choice in

Daily Production(a): ~28,000 BOE

the region

PDP Reserves: 173 MMBoe (PV10: $571M)

✓ Long history as an established operator provides

credibility among potential sellers of similar assets Strong Margins are Highly Accretive to EBITDA

Held by Production Acres: 4.0M

Footnotes: (a) Based on the combined midpoints of 26-30 Mboe/day estimate for the Alliance and Mountaineer acquisitions anticipated to close as detailed on the Expected Timetable slide

12January 2018 Investor Presentation

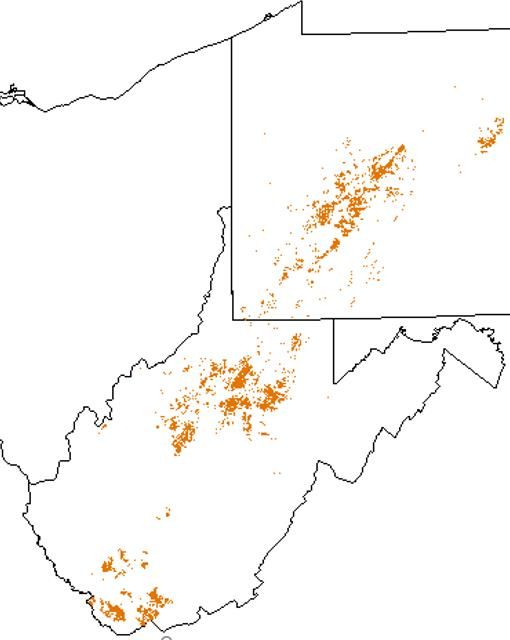

CONCENTRATED FOOTPRINT IN THE BASIN

DGOC Today Alliance Mountaineer

DGOC Combined

Pennsylvania

Ohio

Strategic acquisitions within

a tight focus area allow for >90% of DGOC wells in OH,

greater near and long-term PA & WV are within a

West Virginia

synergy potential 200km radius

13January 2018 Investor Presentation

TRANSACTION RATIONALE: ALLIANCE (STRUCTURE: STOCK PURCHASE)

Geographically Aligned with Existing Assets; Significantly accretive on evaluated metrics:

Acquisition Criteria / Valuation Metrics

($95M Purchase Price)

Net Daily production (90%+ Natural Gas) 53,000

Mmcfe / Boe 8,800

Reserves - PV10 ($Million) $168

PDP Reserves – Volumes (MMBoe) 49.3

Reserves – Long remaining life >50 years

High net revenue interest ~78%

Increases HBP undeveloped acreage (Millions) 1.5

Increases operational density; creates economies

Increases quality of skilled labor

PDP Reserves +90%

Accretive to EBITDA per share

Net Daily Production +86%

Accretive to cash flow per share

HBP Acres +94%

Funds progressive dividend

Anticipated closing date 07 Mar 2018 Significant Existing Hedge Book(a)

Footnotes: Estimated 70% of Alliance natural gas production is hedged at $2.35

14January 2018 Investor Presentation

TRANSACTION RATIONALE: MOUNTAINEER (STRUCTURE: ASSET PURCHASE)

Geographically Aligned with Existing Assets; Significantly accretive on evaluated metrics:

Acquisition Criteria / Valuation Metrics

($85M Purchase price)

Net Daily production (90%+ Natural Gas) 54,000

Mmcfe / Boe 9,000

Reserves - PV10 ($Million) $178

PDP Reserves – Volumes (MMBoe) 69.3

Reserves – Long remaining life >50 years

High net revenue interest ~73%

Increases HBP undeveloped acreage (Million) 0.9

Increases operational density; creates economies

Increases quality of skilled labor

PDP Reserves +127%

Accretive to EBITDA per share

Accretive to cash flow per share Net Daily Production +87%

Funds progressive dividend

HBP Acres +53%

Anticipated closing date 31 Mar 2018

15January 2018 Investor Presentation

INORGANIC GROWTH - CASH FLOW & EBITDA ACCRETIVE

20,000

Daily Production (Net Boe/d)

5.0x Multiple Paid of Op Cash Flow 17,833

18,000

Transformative Acquisition

(includes acquired G&A expenses)

16,000

Bolt-on Acquisition 3.9x

4.0x

14,000

Cash Flow Multiple Paid

3.3x

Net Boe per Day

12,000

2.8x

3.0x

2.4x 10,000

2.3x

7,250 8,000

2.0x

1.6x

6,000

4,000

1.0x

1,490 2,000

538 627

218

0.0x -

Eclipse Seneca EnerVest Titan NGO Current Targets

2016 2017 2018

16January 2018 Investor Presentation

NET PRODUCTION & RESERVE GROWTH

Stable production base with low (~3% annual) declines and long life (~50+ years remaining life)

30.0 +87% +173%

25.0 9.0 28

------------------

+86%

Net Boe per Day

20.0 54MMcf/d 97% Natural Gas

8.8

15.0

53 MMcf/d

10.0

10.3

5.0

62 MMcf/d 170 MMcf/d

-

DGOC Legacy(a) Alliance Mountaineer DGOC Combined

Reserves are 100% PDP; Offer significant PDP/Organic Development Upside(b)

200.0

180.0

+127% +217%

Net PDP Million Boe

160.0 69.3 173.2

140.0

120.0 +90% PV10: $178M

100.0

80.0 49.3

60.0 PV10: $168M

40.0 54.6

20.0 PV10: $571M

PV10: $225M

-

DGOC Legacy(b) Alliance Mountaineer DGOC Combined

Footnote: (a) 207 Exit Rate (December 2017); (b) Estimated as of January 2-12, 2018 using the current NYMEX strip

17January 2018 Investor Presentation

ACQUISITIONS SUBSTANTIALLY INCREASE SCALE & ECONOMIES

PDP Reserves(a) Net Daily Production (26-30 MBoe/d)(a)

200.0 $700 30.0

180.0

+217%

$600

160.0 25.0

PV10 ($Millions USD)

$572

MBoe per Day

140.0 $500

Millions of Boe

20.0

120.0 $400 +170%

100.0 15.0

80.0 $225 173.2 $300

60.0 10.0

$200

40.0

54.6 $100 5.0 10.3

20.0

- $- -

Legacy DGO Pro forma Legacy DGO Pro forma

Acres Held by Production(a) Accretive to EBITDA per share

4.5 $80.0

+147%

4.0

$70.0

3.5

$60.0

Millions of Acres

3.0

$ millions

2.5 $50.0

2.0 4.0 $40.0

1.5

$30.0

1.0

1.6 $20.0

0.5 $28.0

- $10.0

Legacy DGO Pro forma Legacy DGO Pro forma

Footnote: (a) Pro forma increases are calculated from the midpoint

18January 2018 Investor Presentation

LINE OF SIGHT TO LOWER COSTS

LOE per Boe (~$6.25-$6.75 per BOE)(a) G&A per Boe ($0.85-$1.15)(a)

$7.60 $2.50

$7.40

$7.20 $7.46 $2.00

$7.00 $1.99

LOE $ / Boe

G&A / Boe

$6.80 $1.50

$6.60

$6.40 $1.00

$6.20

$6.00 $0.50

$5.80 $1.24 Mcfe $0.33 Mcfe $0.17 Mcfe

$1.08 Mcfe

$5.60 $-

Legacy DGO Pro forma Legacy DGO Pro forma

Cash Operating Costs / Boe: Peer Comparison(b)

$45.00

$40.00 Peer Average:

$35.00 $20.43

$30.00

$25.00

$20.00

$15.00

$10.00

$5.00 $7.46

$-

DGOC

Peer 10

Peer 11

Peer 12

Peer 13

Peer 15

Peer 16

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Footnote: (a) Legacy DGO values are based on the average for the six month period June – November 2017 and the % declines are based on the midpoints of the ranges shown; (b) Source: Bloomberg and Peers include TLW, PMO, NOG, SEPL,

ENQ, GENL, SQZ, CNE, GKP, FPM, OPHR, SIA, ELA, LEK, AMER, SEX 19January 2018 Investor Presentation

SIGNIFICANT ORGANIC OPPORTUNITY SET

Infill Drilling Opportunities Single Gas & Oil Well IRRs

• Substantial ~4.0 million+ acre leasehold, estimated 80% 50%

45%

undeveloped based on 20 acre full-development spacing 45% 40%

40% 35%

• Low risk, low cost development. 150 wells drilled by DGO prior to 30%

2012 with no dry holes. $250k-$350k/well to drill & hook up 35%

25%

30%

• IP rates ~125 mcfepd per well, much shallower decline rates than 25%

21%

shale wells (~25% in year 1 vs. ~75%+ for unconventional)

20%

• Options to restart drilling activity when single well IRRs exceed the 15%

returns available from inorganic growth opportunities 10%

5%

• Opportunity to increase 2P & 3P reserves with a future engineering

0%

study of our largely undeveloped footprint $2.5/mcf $3.0/mcf $3.5/mcf $4.0/mcf $4.5/mcf $5.0/mcf

Four Million Acres Held by Production Significant Infill Development Opportunity

5.0 160

Acres Held by Production (Millions)

Existing Acres per Well

4.0 Full Development : ~80%

120 ~20 Acre Spacing 139 Undeveloped

0.9 4.0

3.0

80 92

1.5 85

2.0

64

40

1.0

1.6

- -

DGOC Alliance Mountaineer DGOC DGOC Alliance Mountaineer DGOC

Legacy Combined Legacy Combined

20January 2018 Investor Presentation

ACQUISITION STRUCTURE & FINANCING OVERVIEW

Highlights Low Net Leverage; Organically De-Leveraging

4.x Covenant Limit = 3.5x

✓ Continued commitment to balanced 3.5x

use of debt and equity capital to 3.x

Debt / EBITDA

2.5x

maintain low leverage and a strong

2.x

balance sheet 1.5x

1.x

0.5x

✓ Credit facility remains at $110M with 0.x

0.8x 0.0x

.x

DGOC Pro Forma DGOC Pro Forma

$35M available 2020

Capital Structure for each Target Purchase

✓ Leverage remains significantly

Equity

below covenant levels after funding $100

acquisitions $80

$ Million USD $60

✓ Strong cash flow profile of the $40

$95

$85

business generates cash to repay

$20

debt, reducing leverage over time

$-

Alliance Mountaineer

21January 2018 Investor Presentation

COMMITMENT TO A STRONG BALANCE SHEET

Pro Forma Capitalization ($M)(a) Pro Forma Liquidity ($M)

Cash & Cash Equivalents $ 15 $60

Credit Availability Cash

Borrowings 73 $50 Million

$50

Total Shareholders’ Equity(b) 276

$15

$40

$ Millions USD

Total Capitalization $364

$30

Liquidity

Cash & Cash Equivalents $ 15 $20

$35

Undrawn portion of Credit Facility 35 $10

Total Liquidity 50

$-

Pro Forma Debt Maturities ($M)(c)

$120 Outstanding Acquisitions Undrawn

$100

32% Undrawn $35

$80 $-

No Current Maturities(c)

$60

$40

$73

$20

$- $-

2018 2019 2020

Footnote: (a) Cash and cash equivalents reflects cash of $15M at 31Dec17 with no incremental cash build related to the $189M equity issuance net of closing fees (b) Shareholders Equity calculated as $87m at 30 June 2017 (last reported mid-year

results) plus $189M equity offering to fund the acquisitions;(c) Credit facility matures in 2020 with terms that include a principal cash sweep paydown provision whereby after dividends, taxes and all other operating cash flows, 90% of remaining cash is 22

used to paydown the facility. Under the terms of the facility, which is not a revolver, principal paydowns are not available for future draws.January 2018 Investor Presentation

EXPECTED TIMETABLE

2018

31 Jan Roadshow Complete

31 Jan ABB Announcement

31 Jan Book Closed

Placing Announcement & Circular Posted

1 Feb

2017 Final Dividend declared

19 Feb Shareholder Meeting

20 Feb Settlement & Admission of Placing Shares

Early Mar Alliance Acquisition Completed

Early Apr Mountaineer Acquisition Completed

23APPENDIX

January 2018 Investor Presentation

HEDGE PORTFOLIO PROTECTS CASH FLOW & THE DIVIDEND(a)

Crude Oil (bbl, $/Bbl) 1H18 2H18 1H19 2H19 1H20 2H20 1H21 Oil Hedges

Costless Collars 75,200 73,600 78,000 73,600 33,000 - 100,000

Ceiling $51.52 $51.45 $52.66 $52.40 $57.40 $50.00

80,000

Floor $41.41 $41.50 $43.25 $43.50 $42.50 $40.00

Swaps - - - - - 33,000 60,000

$30.00

Swap Price $50.78

40,000 $20.00

Total Hedge Volume 75,200 73,600 78,000 73,600 33,000 33,000 20,000 $10.00

Weighted Average Floor Price $41.41 $41.50 $43.25 $43.50 $42.50 $50.78 - $0.00

1H18 2H18 1H19 2H19 1H20 2H20 1H21

Hedged Volume (Bbl) Swap/Long Put Price ($/Bbl)

% of Forecasted Production Hedged 71% 72% 80% 78% 38% 39%

Natural Gas Hedges(b)

10,000,000 $3.00

8,000,000 $2.50

$2.00

6,000,000

$1.50

4,000,000

Natural Gas (MMBtu, $/MMBtu) 1H18 2H18 1H19 2H19 1H20 2H20 1H21 $1.00

Hedges & Physical Sales 8,267,375 8,114,807 5,641,176 5,661,085 5,647,812 5,388,085 2,970,000 2,000,000 $0.50

Weighted Average Floor Price $2.57 $2.57 $2.60 $2.57 $2.56 $2.61 $2.91

- $0.00

1H18 2H18 1H19 2H19 1H20 2H20 1H21

% of Forecasted Production Hedged 84% 86% 62% 65% 68% 67% 38%

Volumes (MMBtu) Weighted Avg Floor Price ($/MMBtu)

Natural Bas Basis Hedges (b)

Natural Gas Basis (MMBtu, $/MMBtu) 1H18 2H18 1H19 2H19 1H20 2H20 1H21 7,000,000 $0.00

Hedges & Physical Sales 5,753,419 4,589,200 5,803,853 5,842,923 4,873,543 4,829,123 2,977,500 6,000,000 ($0.10)

Weighted Average Basis Price ($0.51) ($0.61) ($0.56) ($0.56) ($0.56) ($0.57) ($0.49) 5,000,000 ($0.20)

4,000,000 ($0.30)

3,000,000 ($0.40)

2,000,000 ($0.50)

1,000,000 ($0.60)

- ($0.70)

1H18 2H18 1H19 2H19 1H20 2H20 1H21

25

Footnote:(a)Existing hedge positions relate to legacy production and exclude all volumes to be acquired with the target acqui sitions; (b) Natural gas hedges reflected are Volumes (MMBtu) Weighted Average Basis Price

a blend of financial and physical hedge contractsJanuary 2018 Investor Presentation

RECENT TAX REFORM WILL ENHANCE CASH FLOW

➢ US Corporate tax rate significantly reduced Reduced Cash Taxes from Lower Corporate Rate

from 35% to 21%

40%

35%

➢ Reduction in corporate tax rate will reduce

Corporate Tax Rate

30%

cash taxes beginning in 2018 following the 25%

utilization of DGOC’s existing deferred tax 20%

34%

liability 15%

10% 21%

➢ Lower tax rate will reduce DGOC’s 5%

0%

deferred tax liability Pre-Reform Post-Reform

Gain to Recognize Lower Deferred Tax Liability

➢ 100% Bonus depreciation is now eligible

for used assets (as long as they are ‘first $16.0

Deferred Tax Liability ($Million)

use’ for the acquirer) $14.0

$15.1 Estimated Gain

$12.0 on Revaluation

$10.0

➢ Value allocated to discretely identified $8.0

personal property assets acquired as $6.0

part of larger asset deals become fully $4.0

deducted in the year of acquisition $2.0

$-

Legacy DGO Pro forma

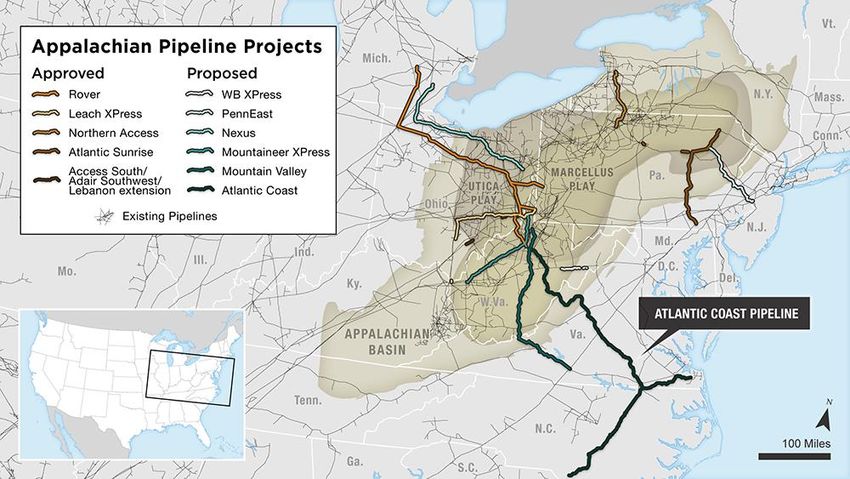

26January 2018 Investor Presentation ROBUST, EXPANDING DISTRIBUTION NETWORK Conventional Production Benefits Recent Pipeline Approvals: Low pressure gathering and transmission systems that Atlantic Sunrise: ~200 miles of pipe; 1.7 Bcf/day do not take Marcellus and Utica production Rover: ~500 miles of pipe; 3.25 Bcf/day Separation Units At Site: Oil trucked directly to market, gas delivered through flow-lines to processing facilities before using surrounding third party pipelines 27 Map Source: Energy company filings (shapefile), Energy Information Administration; Credit: Leanne Abraham, Alyson Hurt and Katie Park/NPR

January 2018 Investor Presentation

MANAGEMENT TEAM

Years of

Name Position Profile

Experience

▪ Founded DGO in 2001

Robert “Rusty” ▪ 4th generation oil and gas

CEO ▪ 13 years in finance and accounting in the banking industry, CPA 28

Hutson, Jr.

▪ Field operations, investor relations, capital raise, acquisitions

▪ Joined DGO in 2016

▪ 25 years in finance, accounting and operations management, CPA

Bradley Gray FD; COO ▪ Commodities experience 28

▪ Capital management and operations oversight

▪ Joined DGO in 2017

CFO ▪ 17 years in finance, accounting and audit, CPA

Eric Williams ▪ 8 years in oil and gas 17

IR

▪ Capital markets, investor relations, financial reporting, controllership, audit

▪ Joined DGO in 2017 through its acquisition of Titan Energy

SVP ▪ 35 years in oil and gas production operations

Bob Cayton ▪ Experienced in multiple facets of producing well management including well tending, disposal 35

Ops

INDUSTRY AND CAPITAL MARKETSwellEXPERIENCE

management, drilling operations, etc.

▪ Joined DGO in 2017 through its acquisition of Titan Energy

SVP ▪ 36 years in oil and gas operations and environmental compliance

Jack Crook ▪ Safety policies, procedures, and training 36

EHS

▪ Exec Board Member & Secretary of the Board of PA Independent O&G Association

▪ Joined DGO in 2017

VP ▪ 21 years in audit and corporate finance for publicly traded US companies, CPA

Bryan Berry ▪ Investment banking experience with an emphasis in consumer services 24

Finance

▪ Deep experience in financial modeling, analysis and budgeting

▪ Joined DGO in 2017 through its acquisition of Titan Energy

VP ▪ 35 years in oil and gas

Bill Kurtz ▪ Experienced in energy marketing, field ops, land mgmt, acquisitions and reservoir engineering 35

Energy Marketing

▪ Active member of AAPL, OOGA (producers committee member), PIOGA and SPE.

Cumulative Management Team Experience 203

28January 2018 Investor Presentation

THE BOARD: ALIGNED WITH SHAREHOLDERS (SIGNIFICANT INSIDE OWNERSHIP >30%)

Name Position Profile Shares Held

▪ Joined DGO in 2005 as 50% owner with Rusty Huston

Robert Post Non-Executive Chairman ▪ Successful business entrepreneur and industrial operations experience 20.0 M

▪ B.S. degree in Accounting from Jacksonville State University, Alabama (13.8%)

▪ Founded DGO in 2001

Robert “Rusty” ▪ 4th generation oil and gas 20.0 M

Chief Executive Officer

Hutson, Jr. ▪ 13 years in finance, accounting and the banking industry, CPA (13.8%)

▪ Field operations, investor relations, capital raise, acquisitions

▪ Joined DGO in 2016

Finance Director and ▪ 28 years in finance, accounting and operations management, CPA 2.2 M

Bradley Gray Chief Operating Officer ▪ Commodities experience (1.5%)

▪ Capital management and operations oversight

▪ Long and successful career in the investment sector

▪ Worked at a number of leading city investment houses, as both an investment 0.1 M

David Johnson Non-Executive Director analyst, and more recently, in equity sales and investment management (0.1%)

▪ Roles with Panmure, Investec, Henderson Crosthwaite, Sun Life Assurance and

Chelverton Asset Management

▪ Partner in the corporate team at Watson Farley & Williams in London

Martin ThomasAND CAPITAL

Non-Executive Director ▪ 30 year legal career, including 7 years as the European Managing Partner of a global 2.0 M

INDUSTRY MARKETS EXPERIENCE

law firm headquartered in the United States (1.4%)

50.0 35%

31% Investors Holding >3% Shares

% of Shares Outstanding

As of 31 December 2017 30%

40.0 % O/S

Shares in Millions

25%

30.0 20%

13% 15%

20.0 10% 9%

10%

10.0

5% 4% 4% 3% 3%

5%

44.4 18.2 14.9 13.2 7.0 6.1 5.4 4.8 4.5

- 0%

Directors Sand Grove GLG Miton Janus Hadron Premier Hargreave River and 29

Henderson Hale MercantileContact Information

Company Brokers

Diversified Mirabaud Stifel

PO BOX 381087 MIRABAUD SECURITIES LIMITED STIFEL NICOLAUS EUROPE LTD |

BIRMINGHAM, ALABAMA 10 BRESSENDEN PLACE 150 CHEAPSIDE

35238-1087 (USA) LONDON SW1E 5DH LONDON EC2V 6ET

ERIC W ILLIAMS, CFO PETER KRENS ASHTON CLANFIELD

EWILLIAMS@DGASOIL.COM PETER.KRENS@MIRABAUD.CO.UK ASHTON.CLANFIELD@STIFEL.COM

+1-205-379-8321 +44 (0)20 3167 7221 +44(0) 20 7710 7459

WWW.DIVERSIFIEDGASANDOIL.COMYou can also read