Economic Update July 2020 - Prepared for members of the Construction Industry Training Board - CITB

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SUPPORTING THE SOUTH AUSTRALIAN

BUILDING AND CONSTRUCTION

INDUSTRY AND WORKFORCE.

Economic Update

July 2020

Prepared for members of the Construction

Industry Training Board.

Contents

SUMMARY 01

IMPACT ON THE ECONOMY AND Australian Government – Economic and Fiscal Update 02

ON BUILDING AND CONSTRUCTION OF

COVID-19 — SUMMARY OF REPORTS

BUILDING AND CONSTRUCTION Summary of ABS Indicators - South Australia 04

INDICATORS ABS Building Approvals — June 2020 05

ABS Building Activity — March Quarter 2020 07

Construction Work Done and Construction Work

in the Pipeline — March Quarter 2020 08

Other Commentary on Building and Construction Indicators 09

Australian Securities and Investments Commission—

Companies Entering External Administration

by Industry 09

Cordell Construction Monthly — June 2020 09

ANZ/Property Council Survey —

September Quarter 2020 10

Sourceable: Housing Construction Trades

Remain in Balance 12

EMPLOYMENT AND UNEMPLOYMENT ABS Labour Force — June 2020, Cat. No. 6202.0 13

Vacancy Report — June 2020, Australian Government 14

COMMENTARY ON GENERAL ABS Retail Trade — May 2020, ABS Cat. No. 8501.0 15

ECONOMIC CONDITIONS CommSec — State of the States, July 2020 15

(VARIOUS ANALYSIS)

Note: See Disclaimer on last page.

These reports will be updated each month, reflecting data and

analysis that was released in that month. Note that this data may

in fact relate to activity some months prior depending on the data

collection methodology and timing.

This report provides commentary on data up to 3 August 2020.

Please refer all queries in respect of this publication to Eric Parnis,

Manager Research, CITB, (08) 8172 9509, email: ericp@citb.org.au

Contact: citb@citb.org.au | (08) 8172 9500

78 Richmond Road, Keswick SA 5035

Summary South Australia is ranked 6th overall of all the

states in economic indicators, according to

The impact of COVID-19 is affecting the the CommSec State of the State report.

construction sector in a number of ways:

More positively, non-residential building approvals

1. There has been a noticeable decline in are holding up in South Australia, and on some

apprenticeship commencements – see Chart 1 construction indicators, South Australia is

below. Comparisons for the April-June period performing noticeably better than other states.

for the past 5 years show that commencements

in 2020 are 55% lower than in the equivalent

period in 2018, with substantial declines across

all major qualifications.

Chart 1: CITB Supported Apprentice Commencements

— 3 Months to 20 June

700

600

500

400

300

200

100

0

2015 2016 2017 2018 2019 2020

2. The construction sector has had among the

highest take up of the JobKeeper program and

the program’s scaling back after 30 September

may provide a challenge to the sector overall.

3. Some of the major drivers of housing

construction – population growth and job

security are showing significant stress and will

negatively impact on construction activity until

the Home Builder stimulus starts to take effect.

4. Building activity data is only available to the

first quarter of 2020, before the full impact of

the pandemic was felt. Even at that stage were

downward trends in the value of construction

work done and work in the pipeline.

1

Impact on the Economy and on Building and

Construction of COVID-19 — Summary of Reports

Australian Government, Economic and Fiscal Update 23 June COVID-19 cases in Victoria and the corresponding

2020 measures implemented to contain the outbreak will

weigh on activity in that state. The increase in uncertainty

Source: The Hon Josh Frydenberg MP and budget.gov.au

about the spread of the virus is also expected to

• Note: this report was published before the COVID-19

dampen the recovery in other parts of the country.

situation in Victoria worsened considerably.

• Australia’s population growth is assumed to remain positive

• Australia’s underlying cash balance is forecast to decrease

but lower over the forecast period. This is mainly due to lower

from balance in 2018-19 to a $85.8 billion deficit in

net overseas migration. The fertility rate is also expected to

2019-20 and a $184.5 billion deficit in 2020-21.

fall due to the weaker economic conditions and outlook.

• Despite the support to the economy from the measures

• As a result, annual population growth is assumed to slow

the Government has taken, real Gross Domestic Product in

to 1.2 per cent in 2019-20 and to 0.6 per cent in 2020-

Australia is forecast to have fallen sharply in the June quarter

21 — the lowest annual rate of growth since 1916-17.

by 7 per cent. However, the easing of health restrictions in line

Future migration levels remain highly uncertain, due to

with the health advice is expected to deliver an increase in

the path of the pandemic and the nature and duration of

economic activity from the September quarter and beyond.

measures taken to contain its spread at home and abroad.

• On a calendar-year basis, real GDP is predicted to grow by

• As is the case globally, the evolution of the virus is the

2½ per cent in 2021, after a fall of 3¾ per cent in 2020.

greatest uncertainty for the domestic outlook. Additional

• There are some positive early signs in the recovery with significant outbreaks in Australia, or a noticeable worsening

indicators suggesting that the unwinding of containment of existing outbreaks, would lead to a further contraction in

measures in the latter part of the June quarter has economic activity and employment, especially if accompanied

led to a noticeable recovery in activity and jobs. by the reintroduction of containment measures.

• As a result of the pandemic, around 709,000 jobs • Even if Australia is able to prevent a major regression

were lost across the country in the June quarter. in health outcomes as containment measures are

relaxed, further outbreaks in our major trading

• The unemployment rate is forecast to peak in

partners also pose a risk to Australia’s recovery.

Australia at around 9¼ per cent in the December

quarter 2020 although labour market conditions • There is also significant uncertainty around the pace and

are expected to strengthen beyond 2020. shape of the recovery, given the unprecedented nature of

this crisis. The economic recovery is forecast to be relatively

• Even with the current outbreak and reintroduction of

fast by historical standards. The economy could recover

more significant containment measures in Victoria,

more quickly than forecast if firms rapidly adjust to the new

the Australian economy is expected to perform better

environment and household spending returns to usual levels.

than all major advanced economies in 2020.

• However, the recovery could be more protracted if confidence

• Economic activity is expected to pick up nationally in the

remains subdued or more people than expected lose their

September quarter, by 1½ per cent. Activity in the quarter

jobs, including from changes in the structure of the economy

will be supported by the gradual easing of restrictions

or a larger-than-expected wave of business closures.

around most of the country that began in the latter part

of the June quarter, which was accompanied by a partial • Structural change is a significant source of uncertainty;

recovery in consumer confidence, a rebound in business the health and economic shock has changed many

confidence and some improvement in the labour market. aspects of the way people live, including the way people

work, shop and socialise, and it is unclear how large

• However, the recent increase in locally acquired

and persistent some of these changes will be.

2

• Dwelling investment is forecast to fall by 16 per cent in the outlook for non-mining investment, which is

in 2020-21 nationally. The fall in the June quarter is forecast to fall by 25½ per cent in the June quarter.

forecast to be 7 per cent, given cancellations and delays

• Real-time data suggest that around three-quarters of

in residential projects reflecting reduced demand, health

firms have been operating under modified conditions as

restrictions on construction sites and some supply-chain

a result of the pandemic, including changed workplace

disruptions. A further 11 per cent decline in dwelling

practices, payment methods, operating hours and

investment is anticipated in the September quarter.

suppliers. Business solvency is also at risk with around

• The HomeBuilder program is expected to provide a significant two-thirds of all businesses reporting decreases

boost to the future pipeline of work, and there are early in revenue and a number of firms deferring loan

indications that it has already improved confidence and repayments and renegotiating lease agreements.

incentivised some buyers to return to the market. The

• Elevated uncertainty, downgrades to investment intentions

program is expected to contribute around $1.6 billion

and lags between approvals and activity in the construction

to activity in 2020-21, but total residential construction

sector are expected to result in a more gradual recovery

activity is expected to remain subdued for some time.

in business investment than in household consumption.

• New business investment is forecast to fall by 12½ per

cent in 2020-21, driven by a significant deterioration

3Building and Construction Indicators

Summary of ABS indicators

South Australia

Compared to Compared to a

Monthly data Latest month previous month year earlier

Dwelling approvals (Seas. Adj., June 2020) 890 -4.6% -2.4%

• Private houses 648 -2.3% -1.2%

• Private ‘other’ dwellings 182 -10.8% -16.1%

Compared to Compared to a

Quarterly data Latest quarter previous quarter year earlier

Dwelling commencements (Mar qtr 2020, seas. adj.) 2,845 -1.2% 16.7%

Construction work done (Mar qtr 2020, chain vol. seas. adj.) $2.9b 1.1% -8.3%

• Residential $0.9b 1.8% -0.1%

• Non-Residential $0.7b 5.5% 11.9%

• Engineering $1.4b -1.4% -19.7%

Construction work in the pipeline (Mar qtr 2020, original) $6.6b 4.3.% -1.7

• Residential $2.8b -0.5% -1.0%

• Non-Residential $2.3b -11.0% -9.2%

• Engineering $1.6b 53.2% 9.4%

• Construction industry employment (Year to May qtr 2020) 70,898 na -3.5%

SOURCE: ABS DATA, VARIOUS PUBLICATIONS

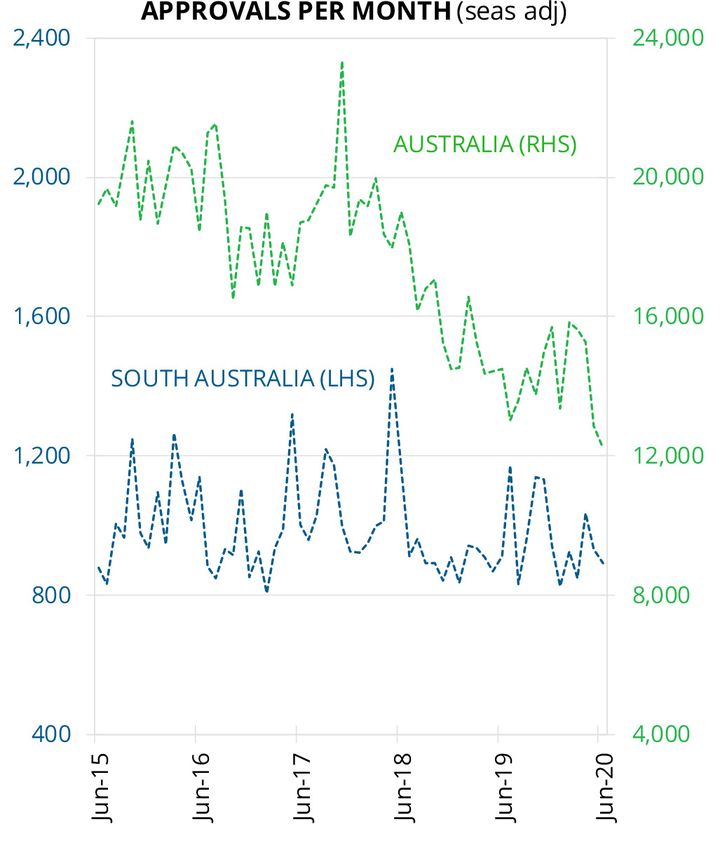

4ABS Building Approvals – June 2020, Cat. No. 8731.0 dwelling approvals was 16.0% lower than a year ago.

data – Analysis by Department of Treasury and • The number of private sector houses approved

Finance for construction in South Australia fell 2.3% in

Note that monthly seasonally adjusted June and was 1.2% lower than a year ago.

estimates show considerable volatility. • Private ‘other’ dwelling approvals in South

• The total number of dwelling approvals in South Australia fell by 10.8% in June and were 16.1%

Australia in June 2020 was 2.4% lower than a year lower than their level of a year ago.

ago (seasonally adjusted). Nationally, the number of

Compared to a

Monthly data (seasonally adjusted) Latest month year earlier

Dwelling approvals (June 2020) 890 -2.4%

• Private houses 648 -1.2%

• Private ‘other’ dwellings1 182 -16.1%

Non-residential building approvals $490.3m +109.0%

Other’ dwellings includes semi-detached, town houses, units, and multi-storey apartments

1

SOURCE: ABS BUILDING APPROVALS DATA

Table 1: Seasonally Adjusted Dwelling Approvals by State

June 20 v June19

(% change)

NSW -31.7

VIC -11.1

QLD -17.3

SA 2.4

WA -10.1

TAS +3.4

AUS -15.8

SOURCE: ABS BUILDING APPROVALS DATA

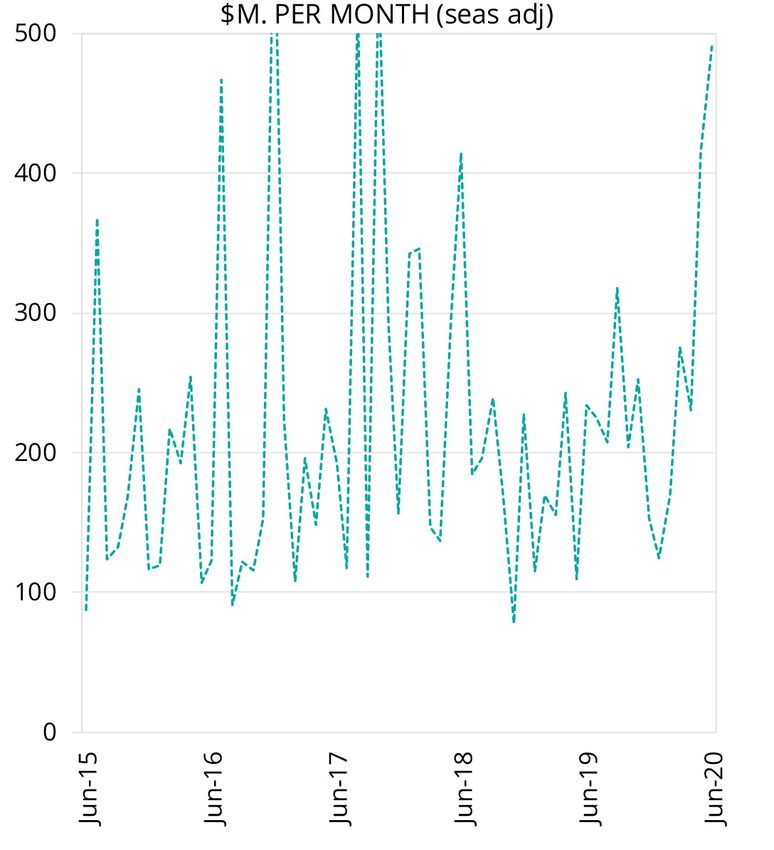

5Chart 2: Total Number of Dwelling Approvals per Month • During June, the value of non-residential building

(Seasonally Adjusted) approvals rose by 18% in South Australia

and was up 109% through the year.

SOURCE: CHART REPRODUCED FROM DEPARTMENT OF TREASURY

AND FINANCE, ECONOMIC BRIEFS.

Chart 3: South Australian Non-Residential Buildings

Approved $M per month (seasonally adjusted)

SOURCE: CHART REPRODUCED FROM DEPARTMENT OF TREASURY

AND FINANCE, ECONOMIC BRIEFS.

6ABS Building Activity Australia – March Quarter 2020,

Cat. No. 8752.0 data – Analysis by CITB

QUARTERLY DWELLING UNIT COMMENCEMENTS ('000)

Chart 4: Quarterly Dwelling Unit Commencements

7 70

TREND

SEASONALLY ADJUSTED

6 60

5 50

AUSTRALIA (RHS)

4 40

3 30

2 20

SOUTH AUSTRALIA (LHS)

1 10

Mar-10

Mar-12

Mar-14

Mar-16

Mar-18

Mar-20

SOURCE: ABS DATA

• During the March quarter 2020, the number of dwelling

unit commencements in seasonally adjusted terms fell

by 1.2% in South Australia, but were 16.7% higher than

a year earlier (nationally, dwelling unit commencements

rose 3.8% but were 1.6% lower than a year earlier).

7Construction Work Done and Construction Work in the Pipeline – March Quarter

2020 – Analysis by CITB

Chart 5: Construction Work Done in the Quarter South Australia ($billion, seas. adj.)

4.0

4.0

3.5

3.5

3.0

Total

3.0

2.5

Total

2.5

2.0

Engineering

2.0

1.5 Engineering

1.5

1.0 Residential

1.0

0.5 Residential

Non-Residential

0.5

0.0

Non-Residential

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

0.0

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

SOURCE: ABS BUILDING ACTIVITY DATA

Chart 6: Construction Work in the Pipeline South Australia ($billion, original)

12

12

10

10

8

Total

8

6 Total

6 Non-Residential

4 Engineering

Non-Residential

4 Engineering

2

2 Residential

0

Residential

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

0

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

SOURCE: ABS BUILDING ACTIVITY DATA

8Other Commentary on Building and Construction

Indicators

Australian Securities and Investments Commission

– Companies Entering External Administration by

Industry

Source: Australian Securities and Investment Commission — ASIC

• The table below summarises the data for construction in South

Australia, by comparing it to all industries in South Australia

and to construction nationally. Insolvencies in construction

in 2018-19 and 2019-20 (YTD) are well below the number in

2013-14. On average, the construction sector makes up around

17% of all insolvencies in South Australia, which is well above

its employment or Gross State Product share (around 8%).

Table 2: Companies Entering External Administration

SA % of Aus

Construction SA All industries SA Construction Aust % of SA total construction

2013-14 64 393 1,802 16.3% 3.6%

2014-15 47 362 1,591 13.0% 3.0%

2015-16 55 386 1,647 14.2% 3.3%

2016-17 39 311 1,509 12.5% 2.6%

2017-18 57 341 1,354 16.7% 4.2%

2018-19 52 347 1,515 15.0% 3.4%

Jul-May YTD 45 265 1,375 17.0% 3.3%

SOURCE: ASIC

Cordell Construction Monthly – June 2020

• The State Government will match Onkaparinga

Council’s $2.65 million funding to complete the Witton

Bluff Base Trail, a 1.37km cycling and walking track

linking Christies Beach and Port Noarlunga, paving

the way for construction to start in December.

• Walkerville Oval is set to undergo an $11.25 million

redevelopment following the release of plans by

Walkerville Council. The redevelopment will include a two

storey building with a gymnasium, bar, change rooms,

function space, grandstand and new netball court.

• Concept plans have been released for a $32 million

redevelopment of Glenunga International High School. The

upgrade will include a new three storey science and technology

building and double court gymnasium building with a two

storey annex accommodating health and physical education

spaces, change rooms, service learning areas and amenities.

9ANZ-Property Council Survey – September Quarter expectations have deteriorated further over recent months as

2020 businesses reassess the long-term outlook for office space.

Source: Property Council of Australia • The national outlook for construction and forward orders,

• The ANZ-Property Council Survey for the September however, are both now positive and improving, clearly

quarter showed a modest improvement in sentiment helped by the HomeBuilder scheme. In a special question

across Australia’s property sectors, although it remains on the Commonwealth Government’s HomeBuilder

deep in negative territory as COVID-19 and the associated program, respondents within the residential sector were

shutdown of economic activity cuts across the economy. broadly positive about the scheme, with 60% reporting

that it would have a positive impact on their business.

• The impact of COVID-19 is immense. Nationwide, almost

all respondents report being negatively hit. Encouragingly, • While the program looks to have had a material impact on the

60% of businesses expect the impact to improve over the outlook for a majority of businesses in the housing sector,

coming quarter. However keep in mind that this survey closed it will not be a panacea for either the residential or overall

on 1 July, before Melbourne’s shutdown was announced. property markets. And with the outlook still challenging, the

economy is likely to need more stimulus in coming months.

• In the residential sector, overall sentiment remains

negative across all states and territories. Price • In commercial property, sentiment remains deeply

expectations fell further into negative territory, while negative across all sectors except industrial, where

the employment outlook remains challenging. confidence is now back in positive territory. Sentiment

in the office sector declined and was broadly flat in the

• The COVID impact has been widespread across states and tourism sector where confidence is the weakest.

sectors, with residential, office, industrial, retail and tourism

sectors all heavily impacted. Not surprisingly, the tourism

sector has been the hardest hit, although office property

Chart 7: The Year Ahead Expectation for Residential

Construction

SOURCE: ANZ-PROPERTY COUNCIL

10• The improvement in construction expectations is likely to • The national average is currently 76, and has increased by 14

take a little while to feed into residential building approvals. points since last quarter. Importantly, South Australia recorded

An improvement over coming months looks likely, although the biggest quarterly increase of all states in the country.

any recovery will be crimped by the drop in overseas

• South Australians are also the most optimistic when it

migration and an extended period of high unemployment.

comes to the future impacts of COVID-19, with 68 per

• Confidence across South Australia’s property cent expecting things to improve over the next three

sector is slowly returning – and it’s happening at a months, in comparison to 60 per cent nationally.

faster rate than every other state in the nation.

• The State Government performance index enjoyed

• Statewide confidence in South Australia sits at 86 for the a significant increase in South Australia, jumping

September 2020 quarter, lifting 26 points since last quarter. from -1.9 percent to 32.3 per cent – giving the State

Government the second highest confidence rating

in the nation, topped only by Western Australia.

Chart 8: ANZ/Property Council Confidence Survey,

September Quarter

SOURCE: THE PROPERTY COUNCIL OF AUSTRALIA

11Sourceable: Housing Construction Trades Remain in oversupply and in the three months to the end of

Balance – Jul8 28, 2020 June they are now in a marginal undersupply.

Source: Sourceable • Demand for skilled trades may have eased due to social

• The supply and demand of tradespeople in distancing requirements on site and households not

residential construction remains in balance despite feeling comfortable inviting trades people into their

the coronavirus, the latest data suggests. homes due to the risk of transmitting COVID-19.

• Releasing its latest report, Housing Industry • On the other hand, anecdotal reports suggest that demand

Association said its HIA Trades Availability Index may have increased due to a rise in small renovation activity.

nationally recorded a level of -0.07 in the June With more people working from home, households found

quarter, down from +0,03 in the March quarter. it easier to schedule a skilled tradesperson to complete

smaller jobs as they did not have to take time off work.

• At this level, trades are considered to be in shortage, but

the level of shortage is considered to be moderate. • There was also a reduction in the supply of skilled trades

as some trades people elected not to work during

• All up: seven of thirteen trades examined are in this period due to the increased risk of contracting

shortage: bricklaying, ceramic tiling, carpentry, the virus or due to the closure of schools.

roofing, plastering, other trades and joinery.

• The adverse impact of the COVID-19 restrictions

• Meanwhile, six trades are in oversupply: electrical, general on new home building would not have been a large

building, landscaping, site preparation, painting and plumbing. factor in June. The impacts on new home building

• Trades were in balance across most locations but were were expected to emerge during the September

in shortage in regional South Australia and regional quarter but these are likely to be alleviated due to the

Western Australia and in oversupply in Perth. Australian Government’s HomeBuilder program.

• In March 2020, skilled trades were in a very minor

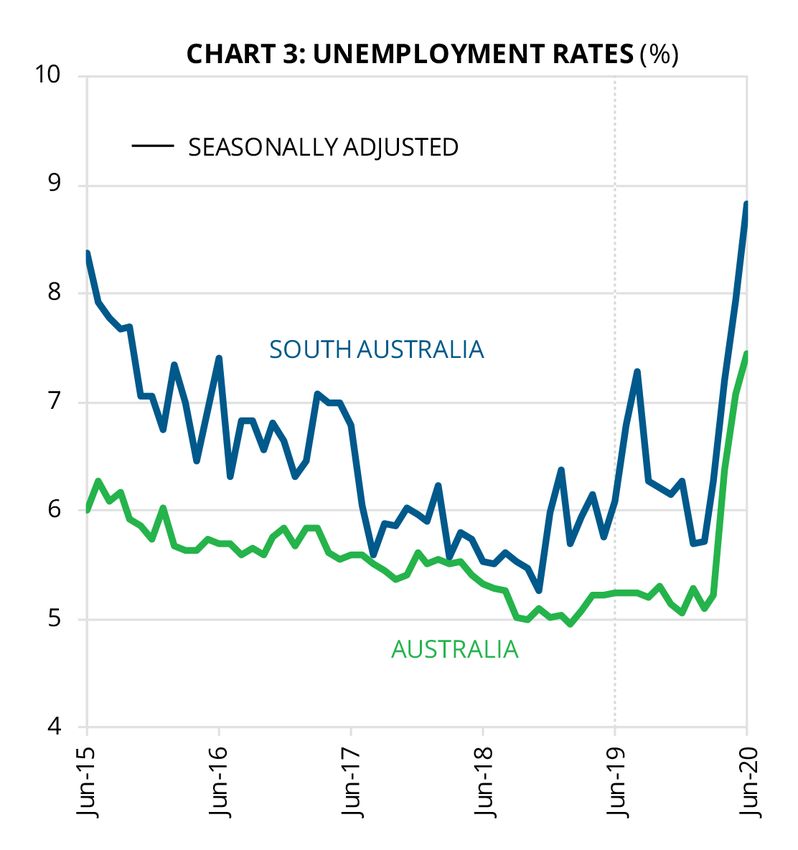

12Employment and Unemployment

ABS Labour Force Australia, June 2020 – Cat. No.

6202.0 (analysis from Department of Treasury and

Finance)

• During June, the unemployment rate was 8.8% in South

Australia in seasonally adjusted terms (7.4% nationally).

• South Australia has the highest

unemployment rate of all the states.

Chart 9: Unemployment Rates (%)

SOURCE: CHART REPRODUCED FROM DEPARTMENT OF TREASURY AND

FINANCE, ECONOMIC BRIEFS.

• In seasonally adjusted terms, total employment

in South Australia rose by 11,400 (1.4%) and

rose by 210,800 (1.7%) nationally in June.

• Through the year seasonally adjusted employment growth

was down 4.4% for South Australia and down 4.1% nationally.

• South Australia’s labour force participation rate rose

in June to 61.8% but remains well below its peak.

• Underemployed workers are those who are employed

part-time and who want (and are available for more hours

of work than they currently have. The underemployment

rate in South Australia was 12.3% in June. As a result, the

overall labour force underutilisation rate was 21.1% in June,

up from 15.2% a year earlier (nationally the rate is 19.1%).

13Vacancy Report – June 2020, Australian Government

Department of Employment, Skills, Small and Family

Business

Source: Australian Government

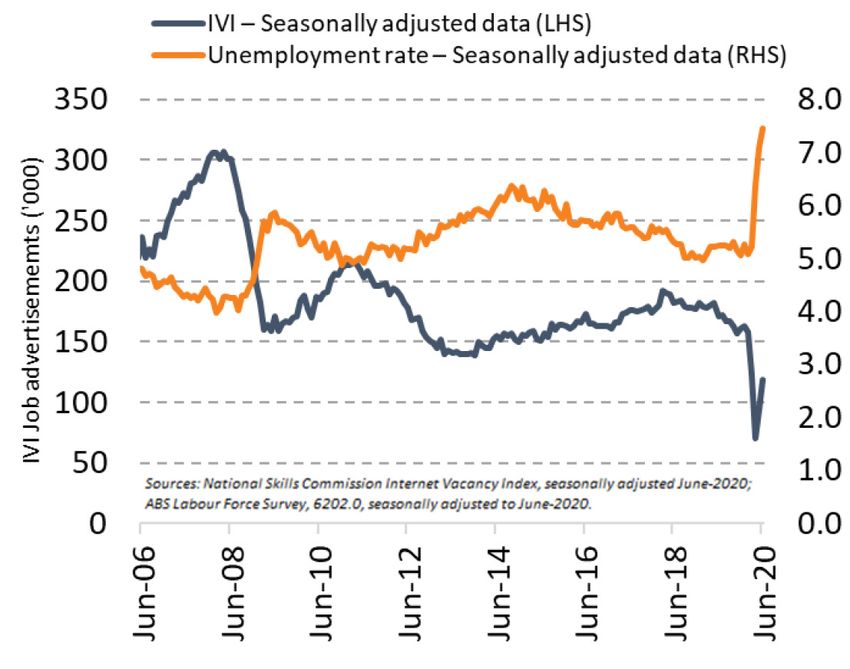

• In seasonally adjusted terms, the Internet Vacancy

Index (IVI) nationally increased by 26.3% (or 24,600

job advertisements) in June 2020. Despite this

increase, job advertisements are 31.0% (or 53,100

advertisements) below the level recorded in June 2019.

• Compared with a year ago, vacancies in

South Australia were down 13.9%.

Chart 10: IVI Change, by State/Territory (%)

Chart 11: IVI Job Advertisements and Unemployment

Rate, Australia

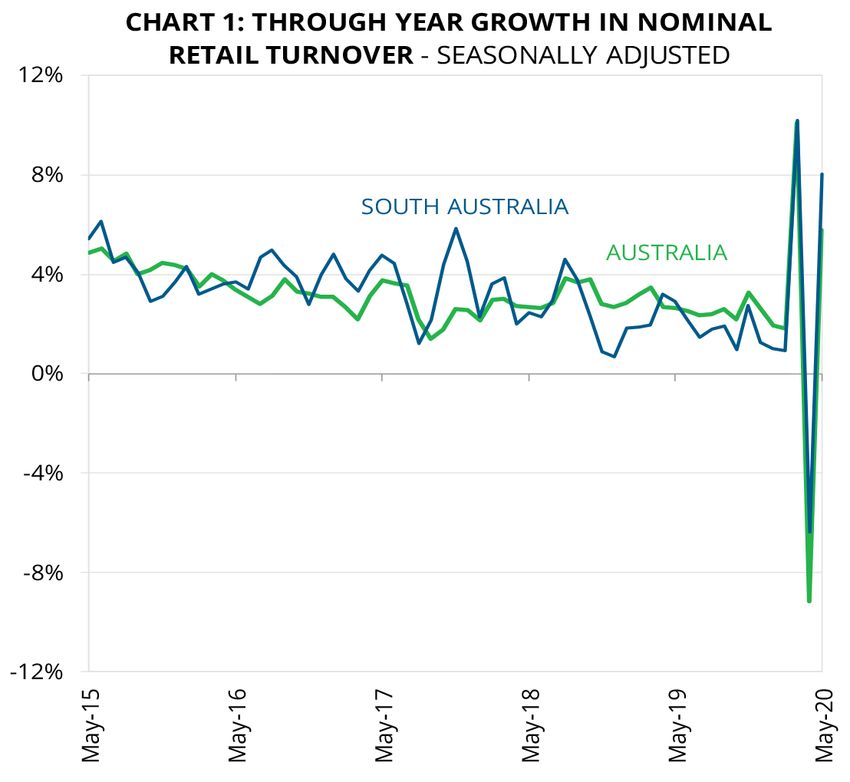

14Commentary on General Economic Conditions

ABS Retail Trade Data – May 2020, ABS Cat. No.

8501.0 (analysis by Department of Treasury and

Finance)

• Due to the impacts of COVID-19 on retail trade,

the ABS has suspended the trend series.

• During May, nominal retail turnover in South

Australia rose by 16% in seasonally adjusted terms

(nationally, nominal retail turnover rose by 17%).

This followed large falls in the previous month.

• Compared with a year earlier, nominal retail turnover was

8.0% higher in South Australia and 5.8% higher nationally

Chart 12: Through Year Growth in Real Retail Turnover –

Seasonally Adjusted

SOURCE: CHART REPRODUCED FROM DEPARTMENT OF TREASURY AND

FINANCE, ECONOMIC BRIEFS.

CommSec – State of the States, July 2020 on relative population growth. But South Australia is ranked

eighth on relative economic growth and seventh on two other

Source: Commonwealth Bank indicators – equipment investment and relative unemployment.

• For the first time since October 2009, Tasmania holds

the mantle of the best performing economy in its own • In terms of construction work, the measure used for

right. Three months ago Tasmania shared top spot analysis was the total real value of residential, commercial

with Victoria. The ACT remains in third spot from NSW and engineering work completed in trend terms in

but both economies have lost ground on the top two. the March quarter. In five of the states and territories,

Queensland is back in fifth spot from South Australia. Then construction work in the March quarter was higher than

follows Western Australia and the Northern Territory. the decade average, up from four in the previous quarter.

• South Australia is now in sixth position on the economic

performance rankings. South Australia is second ranked

15Chart 13: Construction Work Done, Percent Change March Quarter on Decade Average Chart 14: Dwelling starts, percent change March quarter on decade-average SOURCE: COMMSEC, ABS 16

DISCLAIMER

This publication has been produced for general information only

and is not intended to constitute advice. Readers relying on the

content of the publication do so entirely at their own risk.

No warranty (express or implied) is given as to the accuracy or

completeness of information provided. The information may be

true and correct at the date of publication, but this may change

after publication. The CITB is not responsible for providing

updates on such information.

All projections and forecasts are based on assumptions. These

assumptions may not hold true and therefore such projections and

forecasts cannot be relied upon. The CITB is not responsible for

providing updates on such projections and forecasts cannot be

relied upon.

All statements of opinion by the CITB represent the subjective

views of the CITB and the CITB gives no warranty that such

statements are correct. The publication may include statements

of opinion by third parties which do not necessarily reflect the

opinion of the CITB.

All links to third party websites and references to third parties are

included for convenience only and do not constitute endorsement

of the material on those sites, or endorsement of the relevant third

parties and their product or service.

Readers should make their own assessment of all information

provided (including statements of opinion and projections and

forecasts) and consider obtaining independent professional

advice before making any decisions based on such information.

In no event is the CITB (or its trustees, officers, employees or any

related body corporate) liable for any liability, loss, risk or damage

(including incidental or consequential damages) incurred or

suffered (directly or indirectly) out of the use of any information

contained in this publication, whether based on contract, tort or

other legal action.

Copyright in the publication belongs or is licensed to the CITB

and no part of this publication may be used, reproduced or copied

without the CITB’s consent.

17THE FUTURE IS YOURS TO BUILD

You can also read