Generation Rent A lifetime of letting? Will rental rungs replace the property ladder?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Generation Rent A lifetime of letting? Will rental rungs replace the property ladder? Perceptions of the first-time buyer market 2014

Generation Rent 2014

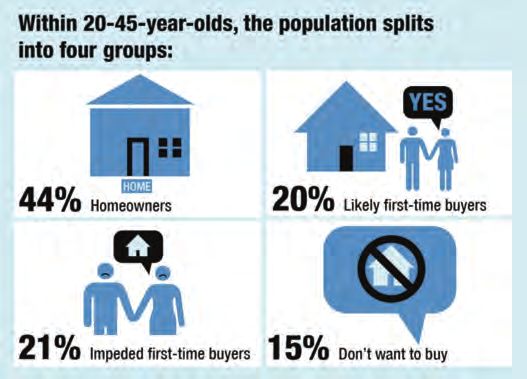

Introduction Who makes up

Generation Rent?

The Generation Rent Report is the definitive annual

research by Halifax, the UK’s leading lender to first-time

buyers, which examines the current perceptions and views

of the first-time buyer market. This is the fourth annual

1.

report and now contains data from interviews with over

32,000 20-45 year olds built up over four years, and over

Plan to buy

3000 parents of 20-45 year olds over the past three years. in the next

5 years...

The global recession which began in 2008 has had a huge

impact on the UK housing market, in particular for first-

time buyers who, facing a difficult mortgage market, high

deposits, poor job security and stagnating incomes, found

it difficult to muster the financial means to get onto the

property ladder. 2.

Our first report in 2011 found that despite a strong desire Would like to buy...

for homeownership, over a third (35%) of 20-45 year olds

could be defined as ‘Generation Rent’ – a group with no

realistic prospect of owning their own home in the next five

years. Three years later, despite the economic recovery

and the implementation of government initiatives such as

‘Help to Buy’, this proportion has not changed, with 36% of

today’s 20-45 year olds falling into ‘Generation Rent’, those

that are either unable to get on the property ladder or those

that have no desire to do so.

This latest report looks back on the past four years to see

what has changed, and the impacts that it may have on the

3.

profile of the housing market overall:

Have no

desire to buy...

The makeup of the UK

housing market?

Over a third (35%) of 20-

45 year olds could be

defined as ‘Generation

Rent’ – a group with no

realistic prospect of

owning their own home in

the next five years.

02

Generation Rent 2014

1. Plan to buy in the next 5 2. Would like to buy...

years... .

Profile: Profile:

■ Younger (52% aged 20-29, mean = 30) ■ Predominantly female (59%)

■ From a middle/high social grade (34% C1, 29% AB) ■ Early 30’s (23% 30-34, mean = 33)

■ Have a higher household income (mean = £33k) ■ From a ‘lower’ social grade (56% C2DE)

■ Have a higher level of savings (mean = £11k) ■ Have a lower household income (mean = £23k)

■ Work full-time (62%) ■ Have lower levels of savings (mean = £3k)

■ Be London-based (27%) ■ Work part-time/be temporarily unemployed (35%)

■ Have grown up in an ‘owned’ home (73%) ■ Have grown up in rented accommodation (36%)

Views: Views:

■ Worried about getting ‘stuck’ renting ■ Worried about future finances

■ 58% agree they’re worried that if ‘I have to rent all my life ■ 60% are worried that if ‘I have to rent all my life I won’t

I won’t be able to retire’ be able to retire’

■ 67% agree renting means they never get to feel like ■ 49% expect to be paying off their mortgage into their

they’re fully settled retirement

■ 67% agree renting means they’re not able to make it feel ■ Feel a social division between those who can/cannot buy

like home homes

■ Think owning is better than renting for all reasons as ■ 78% agree the country is in danger of dividing into two,

above, but more accepting that change is going to between those who can afford a house and those who

happen will never be able to

■ 53% agree it is important for parents to bring up children ■ 65% agree the division between people who can afford

in a home that they own, not rent a house and those who can’t will create long-term social

■ 64% agree buying a home is one of the ways that people problems

take a stake in society ■ Tend to disagree that non-homeowners aren’t willing to

■ 85% agree owning your own home is a good financial make sacrifices. Feel government is not doing enough

investment for the future ■ ‘Only’ 37% agree people aren’t willing to make the

■ 50% agree Britain will become a nation of renters within necessary sacrifices in order to buy their first property

the next generation ■ ‘Only’ 45% agree first-time buyers today are guilty of

trying to find their perfect property rather than adjusting

their expectations to their means

The global recession which began in 2008 has had a

huge impact on the UK housing market, in particular for

first-time buyers.

03

Generation Rent 2014

3. Have no desire to buy... Opinions of homeowners.

Profile: Profile:

■ Young (26% 20-24, mean = 32) ■ Predominantly male (53%)

■ From a ‘lower’ social grade (49% DE) ■ Older (57% aged 35+, mean = 35)

■ Have a lower household income (mean = £19k) ■ From a higher social grade (36% AB)

■ Have fewer savings (mean = £3k) ■ Have a higher household income (mean = £40k)

■ Are not likely to be working/students/house person ■ Have higher levels of savings (mean = £16k)

(55%) ■ Work full-time

■ Have been brought up in owned accommodation (49%) ■ Have grown up in an ‘owned’ home (83%)

Views: Views:

■ Do not feel that owning a home is important; renting ■ Think non-homeowners not willing to make sacrifices/

is fine and Britain should lose obsession with home compromises

ownership

■ 54% agree people aren’t willing to make the necessary

■ 23% agree it is important for parents to bring up children sacrifices in order to buy their first property

in a home that they own, not rent

■ 57% agree first-time buyers today are guilty of trying

■ 39% agree buying a home is one of the ways that people to find their perfect property rather than adjusting their

take a stake in society expectations to their means

■ 56% agree owning your own home is a good financial ■ Feel owning your own home is still important, for

investment for the future settling down/taking a stake in society and as a financial

■ 36% agree Britons should lose their obsession with investment

home ownership - we’d be happier as a result ■ 41% agree owning your own home is less important in

■ Do not feel social division between those that can/ life now than it was a generation ago

cannot buy homes. ■ 46% agree it is important for parents to bring up children

■ 57% agree the country is in danger of dividing into two, in a home that they own, not rent

between those who can afford a house and those who ■ 63% agree buying a home is one of the ways that people

will never be able to take a stake in society

■ 45% agree the division between people who can afford ■ 85% agree owning your own home is a good financial

a house and those who can’t will create long-term social investment for the future

problems

■ 66% agree Britain should remain a nation of

■ Tend to disagree that non-homeowners aren’t willing to homeowners and do not think this should, or will, change

make sacrifices. Feel government is not doing enough

■ 41% agree Britain will become a nation of renters within

■ 36% agree people aren’t willing to make the necessary the next generation

sacrifices in order to buy their first property

■ 33% agree the Government is doing enough to support

■ 41% agree first-time buyers today are guilty of trying people trying to buy their first home

to find their perfect property rather than adjusting their

■ 66% agree parents are now expected to help young

expectations to their means

people buy their first home

■ Do not expect support from parents

■ 46% agree parents are now expected to help young

people buy their first home

04Generation Rent 2014

Attitudes to homeownership Barriers to homeownership

and renting

Financial concerns are again cited as obstacles to

While homeownership remains an aspiration for the majority purchasing property. Almost half (48%) of non-owners claim

of 20-45 year olds (85%), there is evidence that attitudes that the biggest reason they are not buying property at

towards renting as a lifestyle option have softened, with the the moment is lack of sufficient earnings, followed by the

proportion of non-owners who don’t want to raise children high level of required deposits (43%). These concerns are

in a rented property falling to 40%, and also the number of particularly acute for women (50% and 46% respectively)

people worried about renting having a negative impact on compared to men (46% and 40% respectively).

their retirement also decreasing by 6% to 51%.

Despite this, saving for a deposit remains one of, if not the,

Almost half (48%) of this year’s respondents agree that most significant barriers to homeownership for first-time

Britain will become a nation of renters within the next buyers, and over half (57%) of those who would like to buy a

generation, with 46% also agreeing that Britain is becoming home admit that while they want to save for a deposit, they

more like Europe, where renting is ‘the norm’. don’t have the spare cash to do so.

The cycle of renting is also perpetuated by the fact that In 2013, increasing house prices meant that the average

people who grow up predominantly in rented accommodation deposit for first-time buyers in the UK increased from

are themselves more likely to rent than buy. 36% of people £28,001 to £30,943. Although deposit sizes as a proportion

that would like to buy but are unable to have grown up in of the total house price have remained stable at around 20%,

rented accommodation. this is still 10 percentage points higher than 2007 (10%)1.

Of those who don’t want to own, over a third (36%) think that On average, non-owners think they can afford to save £31.72

the nation should lose its obsession with homeownership towards a deposit each week. Indeed, 36% say they can’t

and that people would be happier as a result. save anything towards a deposit and would have to rely on a

If this pattern were to continue, then this would suggest that windfall, and another 14% say they could only save between

the people entering the housing market are less likely to want £1 and £10 (compared with 35% and 12% respectively in

to own a home, and are more likely to remain in ‘Generation 2013).

Rent’, irrespective of changing market conditions, leading to

a longer-term shift in the homeownership profile of the UK.

Barriers to homeownership Plan to buy in Would like to Total

next 5 years buy, but unable

The size of the deposit required 59% 65% 62%

High property prices 55% 52% 53%

Stamp duty 7% 3% 5%

Low income 39% 60% 50%

Lack of job security 27% 26% 27%

Other debts 14% 16% 15%

Extra fees (such as solicitors' fees or mortgage arrangement 17% 14% 16%

fees)

Finding the right property 14% 6% 10%

Not feeling able to apply for a mortgage because they believe 16% 16% 16%

most applications are rejected in today's economic climate

Not knowing how to go about applying for a mortgage 8% 5% 7%

Lenders having unrealistically high expectations of people's 20% 23% 21%

credit histories

Higher repayments from mortgages that have been secured 24% 16% 20%

with relatively small deposits

1

Halifax first time buyer review, 2012, 2013

http://www.lloydsbankinggroup.com/globalassets/documents/media/press-releases/halifax/2014/0401_first_time_buyers.pdf 05Generation Rent 2014

Sacrifices for homeownership Nine-in-ten (90%) young non-owners are prepared to

compromise in order to buy their property – a steady

Only 23% of those who want to buy a home claim to be increase since 2012 (84%). Willingness to compromise is

saving every penny for a deposit and making sacrifices particularly high amongst respondents from London (93%).

to do so. Those who are currently trying to put together a Respondents are most likely to compromise on parking

deposit are more likely to be doing so by making sacrifices (41%) and garden space (41%).

– cutting down on spending on hobbies (35% vs 26%);

going out (49% vs 39%), clothes,(41% vs 30%) or holidays The features that young respondents are least likely to

(36% vs 32%) compromise on are the number of bedrooms (28%) and

having a smaller living area (27%).

20-45 year-old homeowners are far more likely than

potential owners to have lived with their parents for longer

On average, non-owners would be prepared to save up for

(31% vs 15%) or borrowed money from friends/family (23%

a deposit to buy their first home for 5.29 years, down from

vs 4%).

5.41 years in 2013. 40-45 year olds are prepared to save for

This suggests that, for this generation, simply cutting longer than their younger counterparts (5.69 years vs. 4.91

down to save up may not be sufficient to put together years for 20-24 year olds). Following a similar pattern, part

enough money for a deposit on a home, and more dramatic time workers are prepared to save for longer than full time

measures such as moving back home to save on rent or workers (5.29 years vs. 4.95 years respectively).

borrowing money may be necessary.

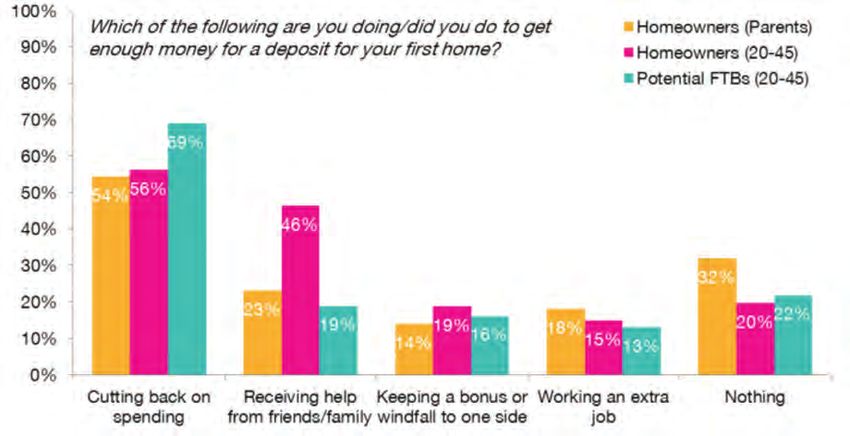

Base: Parents who have ever owned a home; all homeowners aged 20-45; non-homeowners aged 20-45 who would like to buy a home and

want to save for a deposit.

Which of the following are you doing/did you do to get Homeowners Homeowners Potential

enough money for a deposit for you first home? (Parents) (16-45) Homeowners

(16-45)

Living in lower quality accommodation to save on rent 15% 11% 14%

Cutting down on / stopped going out 43% 39% 49%

Spending less on clothes, toiletries or personal grooming 35% 30% 41%

Going on fewer / cheaper holidays 37% 32% 36%

Spending less on Christmas, birthdays and other special events 24% 22% 31%

Spending less on my hobby / hobbies 26% 26% 35%

Borrowing money from friends or family 9% 23% 4%

Keeping a bonus or windfall to one side rather than spend it 14% 19% 16%

Working an extra job 18% 15% 13%

Living with parents 15% 31% 15%

I'm not doing any of these things 32% 20% 22%

06Generation Rent 2014

Parental assistance The future of the

UK Housing Market

Relying on parents or other family members and friends

for support when getting on the property ladder is now The report highlights a disconnect between the desire and

expected, with 6 in 10 of 20-45 year olds agreeing that perceived ability to buy a home. Although homeownership

support is from family members is now automatically is seen as advantageous by a majority, many of Generation

assumed/ a given to help first time buyers. Rent admit they are not taking the steps they need to

purchase their own home.

Of those that have purchased only 37% of 20-45 year old

homeowners received no help from their parents when Deposit sizes and mortgage accessibility are cited as the

purchasing their home. key barriers to homeownership between those that plan

to buy in the next five years than those who are unable

This is a marked generational shift; while both 20-45 year- to buy. Those that are unable to buy are far more likely

old homeowners and their parents cut back and made to identify low income as one of the top three barriers to

sacrifices in roughly equal measure, this generation of homeownership (60% vs. 39%) unsurprising given their

homeowners is far more likely than the preceding one to household income is, on average, £10,000 lower. This

have lived with their parents for longer (31% vs. 15%) or suggests that if issues of ‘affordability’ continue to worsen,

borrowed money from their friends/family (23% vs. 9%) in then those in ‘Generation Rent’ may be more vulnerable.

order to pull together a deposit. However, it also means that there is more scope for issues

of affordability to impact likely homeowners moving

Government assistance homeownership out of their reach.

Since the last research was conducted in 2013, the

government has introduced the ‘Help to Buy’ initiative to

Implications

try to help first-time buyers onto the property ladder either

This potential, and perceived movement in the UK towards

through equity loans or mortgage guarantees. 17,395

renting is not necessarily viewed as a good thing (only

homes have been bought under the scheme in its first nine

27% agree that Brits should lose their obsession with

months, 88% of which were to first-time buyers2.

homeownership), nor is it viewed as something that will

affect everyone (68% of 20-45 year-olds think the country

When asked, approximately 3 in 10 20-45 year olds thought

is in danger of dividing into those who can afford a house

that government initiatives were working, but the same

& those that will never be able to). 56% of the population

amount felt that it wasn’t, and more (4 in 10) didn’t know.

agree that the division between homeowners and non-

homeowners will create long-term social problems.

48% of 20-45

year olds believe

Britain will

become a nation

of renters in a

generation.

2

https://www.gov.uk/government/news/pm-hails-help-to-buy-success

07Generation Rent 2014

A widening of the existing With current estimates of a housing shortfall and an

estimated 232,000 new homes required each year to meet

wealth gap between demand, the house building industry needs to continue to

homeowners and supply new developments. But changes in the proportion

of people who rent, and the length of time they rent for,

non-homeowners are likely to affect the number and nature of new build

properties, and may lead to fewer homes being built than

79% of 20-45 year olds agree that owning your own home

is necessary. As first-time buyers are regarded as crucial

is a good financial investment for the future. As housing

to the housing market and house building industry to keep

represents a large proportion of Britain’s wealth, accounting

the market moving, any decrease in the number of first

for approximately 60% of the UK’s non-financial assets,

time buyers will have an impact on the funding of new

this could result in a widening of the existing wealth gap

builds. It will also be important that, when planning any new

between homeowners and non-homeowners.

developments, the likelihood of some of it being privately

rented is considered, to ensure the stock is of high quality

Lack of financial resources to support people

and well managed.

during retirement

Any decrease in first-time buyers will have an overall impact

Homeownership has long being viewed as a financial

on the future housing market. First-time buyers are viewed

investment; many homeowners view their home as

as the life blood of the housing market and are key to

a resource that they could potentially draw upon in

getting the market moving. In order for the market to remain

retirement. An increasing rental sector would therefore

sustainable, homeowners need to be able to move up the

mean an increasing proportion of the population would not

property ladder. Without a first-time buyer, many people

have that resource to draw upon in their retirement, with

living in their first home will be unable to move up the

51% of non-homeowners aged 20-45 are worried that if

property ladder and, without this movement, the market will

they rent all their lives they won’t be able to retire.

come to a standstill.

08You can also read