Greater Downtown Miami - Mid-Year Residential Market Study Update August 2018 - Prepared for the Miami Downtown Development Authority (DDA) By ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Greater Downtown Miami

Mid-Year Residential Market Study Update

August 2018

Prepared for the Miami Downtown Development Authority (DDA)

By Integra Realty Resources (IRR)

Greater Downtown Miami Mid-Year Residential Market Study Update Prepared for the Miami Downtown Development Authority (DDA) by Integra Realty Resources (IRR) August 2018 For more information, please contact IRR-Miami/Palm Beach The Dadeland Centre 9155 S Dadeland Blvd, Suite 1208 Miami, FL 33156 305-670-0001 dbowen@irr.com

Contents 2 Introduction 4 Greater Downtown Miami Market Submarket Map 5 What’s Changed Since Year-End 2017? 10 Submarket Analysis 12 Resale Condominium Pricing 15 Rental Market Statistics 18 Conventional Apartment Rents 20 Conventional Rental Market Supply 23 Condo Development Process Appendix

Introduction Integra Realty Resources – Miami/Palm Beach (IRR-Miami) is pleased to present the following Residential Real Estate Market Study within the Miami Downtown Development Authority’s (Miami DDA) market area, defined as the Greater Downtown Miami market. This report updates IRR-Miami’s findings on the local residential real estate market through July 1, 2018. Key findings from this mid-year study are as follows: • While everyone wants to see a continued “economic extension” prompted by tax cuts, strong wage growth, and overall positive economic news, Greater Downtown Miami’s new construction market continues to wind down the under-construction inventory of condominiums. The final push of condominium deliveries in Greater Downtown will happen towards the end of 2018, namely in Edgewater and the Arts & Entertainment District. • Condominium rents and velocity year over year experienced normalized increases of 2 to 3 percent on all but the 3-bedroom product. • The continuing story of condo pricing declines is now set squarely in the resale condominium market. While average resale pricing declined again, and may even decline a bit further, the average pricing is quickly nearing the replacement cost threshold. • Newer resales will not retreat as quickly because the sellers are new buyers with a higher average cost basis. As a result, new project sales will be slower overall in the coming 12 to 18 months. This does not portend economic doom despite the market naysayers. • The market champions who believe money will continue to flow into new condo developments against a wall of resale inventory can only credibly make that argument if the development offers something that’s not available in the resale market. • Average rental rates downtown rebounded from a down-year in 2017. This “rent wobble” was largely due to project deliveries in 2017 which needed to stabilize, and the market rents in 2017 reflected increased pre-leasing activity and higher vacancy as projects competed with one another. 2 | Integra Realty Resources

Introduction

• The “rent wobble” of early 2017 could reasonably be expected to occur again in early 2019

following the pending conventional multi-family deliveries expected at the end of 2018.

Year-over-Year rents retreated -1.8% - 3.9% on a price per SF basis for one and two bedroom

units. Studio units were the stand-out winner in 2018 with 16% average rent growth, and new

projects coming to market with smaller average unit sizes and lower overall “chunk rents”

may find similar success.

• While market-makers are plotting how to time the market, the largest fundamental decision

is your own view on the length of continued economic expansion. How long can it last?

How deep will be the retreat?

• The Integra mid-year 2018 report reflects the sum of all hopes (bulls) and fears (bears) in

the market. There are many on both sides. No matter whether you are a bull or a bear, the

condominium development market is standing on solid ground as of midyear 2018.

Respectfully,

Integra Realty Resources (IRR) – Miami/Palm Beach

Anthony M. Graziano, MAI, CRE, FRICS

Senior Managing Director

Dan Bowen

Market Research Analyst

3 | Integra Realty Resources

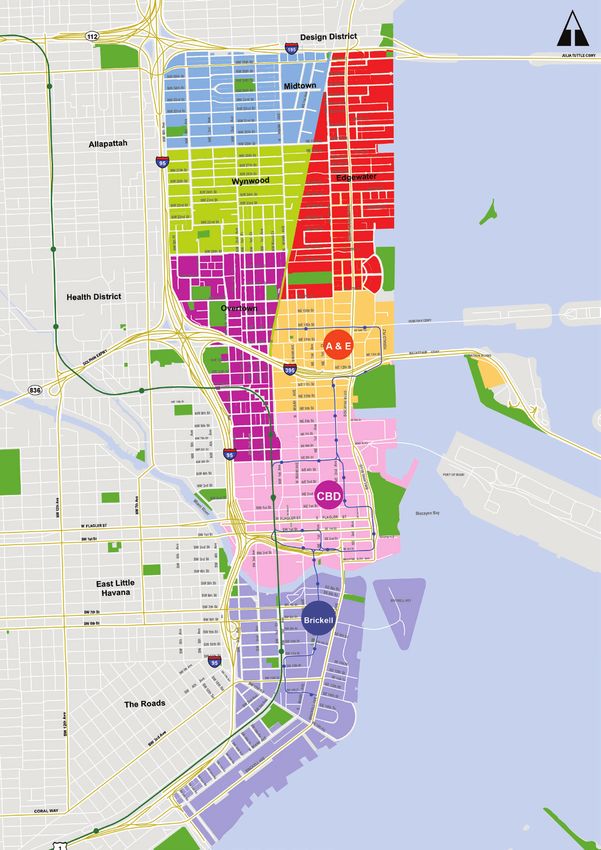

Greater Downtown Miami Market Submarket Map

The map opposite

illustrates the

boundaries of the

Miami DDA, as well

as each submarket

within the Miami

DDA market.

4 | Integra Realty Resources

What’s Changed Since Year-End 2017? T he headline change is the market since Q4-2017 was the completion of 1,145 units at SLS Lux, Aria on the Bay, and Hyde Midtown. This drops the total number of units remaining under construction downtown at 3,849, down from nearly 5,000 units at YE 2017. The development pipeline in Brickell has largely closed out and the last project under construction, Brickell Flatiron, is reportedly experiencing high sales volume. In Edgewater, most of the product under construction, largely comprised of The Related Group’s Paraiso District projects, is pre-sold and slated for delivery in the second half of 2018. This year will also mark the substantial close out of the Arts & Entertainment District when Canvas delivers, further diminishing the construction pipeline across Greater Downtown (Figure 1b). Some developers are reading the tea leaves and trying to be the first project “back” in a submarket when value trends turn upward. In Brickell, Una started taking reservations, while Smart Brickell launched directly into contracts. Okan Tower and YotelPad opened sales offices at their respective sites in the CBD making the submarket one to watch in 2019 (Figure 1a). 5 | Integra Realty Resources

What’s Changed Since Year-End 2017? Figure 1a Greater Downtown Miami Current Growth – Contracts and Reservations Submarket Building Avg. SF Units Status Brickell Una 2,478 135 Reservations CBD YotelPad 563 215 Reservations CBD Okan Tower (former Sterling) TBA 389 Reservations Edgewater Bentley Edgewater Condo-Hotel 905 207 Reservations Brickell One River Point 1,284 350 Contracts Brickell Smart Brickell 632 100 Contracts # in Contracts 350 # in Reservations 596 Figure 1b Greater Downtown Miami Current Growth – Under Construction and Q2 Completions Submarket Building Avg. SF Units Status A&E Canvas 892 513 Under Construction A&E 1000 Museum 5,389 83 Under Construction Brickell Flatiron 1,334 549 Under Construction CBD Paramount Miami 1,793 512 Under Construction CBD Aston Martin Residences 2,000 390 Under Construction Edgewater Gran Paraiso 1,549 317 Under Construction Edgewater Paraiso Bay Tower I 1,360 360 Under Construction Edgewater One Paraiso 1,682 272 Under Construction Edgewater Paraiso Bayviews 1,044 388 Under Construction Edgewater The Edgewater 778 30 Under Construction Edgewater 26 Edgewater 645 86 Under Construction Edgewater Elysee 3,383 100 Under Construction Edgewater Missoni Baia 2,950 249 Under Construction # Under Construction 3,849 Brickell SLS Lux 1,250 450 Complete Edgewater Aria on the Bay 1,317 648 Complete Midtown Hyde Midtown 944 410 Complete # Completed Since Prior Report 1,145 1,103 6 | Integra Realty Resources

What’s Changed Since Year-End 2017?

A s this report was heading to press, Swire announced it was moving forward with plans for two

large Brickell City Centre expansion sites near the river, and whispers of larger plans in Wynwood

began to emerge.

If there is a theme in the first half of 2018, it is that there are two camps of professionals in the market

firmly staked out in their thumbs up or thumbs down position. For lack of a better term, these are the

market’s bulls and bears.

The bears see devastation in the making as we enter a late cycle development period, one of the

longest economic expansions in US history, and few indications that currency and international

demand will return anytime soon.

The bulls believe that Miami has reached critical launch velocity in its downtown urban lifestyle, critical

mass, and residential appeal; and that continued massive liquidity in the equity and debt markets will

remain long-term. The bulls believe that the new Miami developers are emerging that will build without

50% presales, and who will use primarily their own equity with strong private or public balance sheets.

The bears counter this is just a sign of late cycle mechanics that makes the fall even worse.

What the bears cannot deny is that the on-going predictions of the market’s demise do not account for

the declining inventory of new construction being successfully delivered. What the bulls cannot deny

is that even as projects close-out, many units (25%+) immediately return to the market for resale. This

is having a depressing affect on the average resale value and the total resale listing inventory, which is

abnormally high.

What is evident in the composition of the remaining product under construction starting in 2019 is a much

more highly differentiated market, with product offerings in the $350,000 range, to as high as $8 Million.

Instead of shooting for a massive middle-market, the majority of the remaining pipeline will cater to

ultra-luxury, or competitive alternatives for local (primarily domestic) urban dwellers who buy versus rent.

7 | Integra Realty Resources

What’s Changed Since Year-End 2017?

O n which side do you land? Whichever you are, bull or bear, the fact is that any economic stress

that might cause a mis-step in the new construction market will have almost no impact relative

to the last downturn. By the end of 2018, the total number of units under construction will be less

than 2,500 units city-wide, a pipeline that is less than 10% as large as the pipeline during the last

reversal of fortune.

This extended economic rebound following tax reform, coupled with high liquidity in all sectors,

has mostly absorbed any massive shocks to the development pipeline.

Figure 2

Current Greater Downtown Miami Condo Pipeline – Q2 2018

Submarket Complete Under Construction Contracts Reservations Proposed Totals

A&E 0 596 0 0 2,291 2,887

Brickell 4,939 549 450 135 5,160 11,233

CBD 352 902 0 604 5,838 7,696

Edgewater 1,698 1,802 0 207 1,296 5,003

Midtown 410 0 0 0 0 410

Wynwood 11 0 0 0 448 459

Total (2018 Midyear) 7,410 3,849 450 946 15,033 27,688

Total (2017 Q4) 6,312 5,002 520 344 15,016 27,194

Total (2017 Midyear) 5,180 5,078 1,225 505 14,381 26,369

Figure 2 outlines this continued decline of projects imminently entering the pipeline. This should allow

a 24-36 months stabilization of existing resales, which could bring prices back to equilibrium. Property

resales in newer buildings will be slower than older resales primarily because the seller’s cost basis is

higher. Predictions of deep discounts in resale pricing on newly delivered developer-product abound,

with the potential of bulk offerings continuing to make social media headlines. Nonetheless, no major

announcements on bulk deals are evident.

8 | Integra Realty ResourcesWhat’s Changed Since Year-End 2017?

F rom trough to peak, the market topped out in Q2 2016 with a total of 7,499 units under construction.

We survived the danger-zone of stalled projects, or major pockets of standing developer inventory.

Integra’s estimate of “Proposed” projects counts all announcements, approvals, and conceptual plans

ever put forth for vacant or redevelopment sites in the city. To be sure, there is significantly more to come

in Wynwood and Midtown than currently in the proposed count. However, if this last peak demonstrated

the normalized development pace, Miami has another 2-3 cycles of 6,000 – 8,000 units downtown.

The ”proposed” pipeline as tracked by Integra is not imminent. Many of these projects get tabled or

redesigned through multiple market cycles. This represents the long-term (25+ year potential) of the

by-right landscape downtown, not current proposals that will emerge in the near-term 5-year time horizon.

Figure 3

Greater Downtown Miami Condo Market Size – Q2 2018

Submarket Current Market Current % Potential Long % Growth

Size [1] Growth Growth Term Growth Longterm

A&E 4,052 596 15% 2,291 57%

Brickell 24,782 1,134 5% 5,160 21%

CBD 6,640 1,506 23% 5,838 88%

Edgewater 5,750 2,009 35% 1,296 23%

Midtown 1,388 0 0% 0 0%

Wynwood 111 0 0% 448 404%

Total (2017) 42,723 5,245 12% 15,033 35%

[1] Long-Term Growth is the remaining Conceptual units, net of current growth

[2] Current Growth is all Under Construction, Contracts and Reservations

[3] Long Term Growth: 25+ year potential

Figure 3 outlines the critical mass by submarket. By the close of 2019, the city will have nearly 48,000

condominium units available in downtown plus another 11,500 conventional apartment units (Figure

9a). Despite new activity in Little Haiti, Little Havana, Coral Gables, and Dadeland, a compelling

case can be made that downtown has reached critical residential mass unmatched anywhere in the

county, or region, even accounting for condo units that are not occupied full-time.

9 | Integra Realty ResourcesSubmarket Analysis

A summary of the key changes to date:

Brickell

SLS Lux has been completed, and additional information about Smart Brickell has

allowed us to report a definitive number of condominiums with 100 units currently taking

contracts. Una, a new bay-front project near the Rickenbacker Causeway, has launched

reservations. On the rental side, the Panorama Tower – Florida’s tallest building – has

delivered and is currently in lease-up with its first residents now occupying the tower.

CBD

The Aston Martin groundbreaking in late 2017 was a boost of enthusiasm in an

otherwise quiet market for new groundbreakings. Sitting at the mouth of the Miami

River with Biscayne Bay and Brickell Key views, the power of the Aston Martin brand

will be on display. Following other branded projects in the market, Aston Martin is

targeting an ultra-lux buyer on a prime waterfront site.

Paramount Miami reports stronger-than-projected presales. This ambitious mixed use

project at full build-out could become a new focal point for development in the CBD.

Completion of conventional rental projects X Miami and Muze Met Square is

imminent. Some say the X Miami (formerly Vice) project will test the market’s for

smaller unit size in exchange for a lower “chunk” rent. This will be an interesting

contrast to Panorama finding the highest end of the rental market in the city’s tallest

residential building.

Arts and Entertainment

Square Station, a 710-unit conventional rental, has been delivered, and completion

of the condominium project Canvas is considered to be imminent. Art Plaza also

broke ground on 655 conventional apartment units.

10 | Integra Realty ResourcesSubmarket Analysis

Edgewater

Aria (648 units) has been completed, and deliveries at Related Groups’ Paraiso

projects are expected to complete shortly starting with Paraiso Bay. Despite Related’s

strong record of success in Edgewater, one of downtown’s most notable and active

players is waiting on the sidelines following the completion and close-out of the

majority of its Edgewater portfolio by the end of 2018.

Midtown

Midtown 29 completed in the first half of 2018, and work is ongoing at Midtown 6 and

8, all representing conventional rental product. Condominium Hyde Midtown also

delivered in the current period.

Wynwood

There are currently two ongoing rental developments in Wynwood – Wynwood 25 and

the Bradley (formerly Wynwood 26). There are no condo projects in the pipeline as

Wyn26 has been canceled after the developers reportedly failed to secure financing.

Overtown

Miami-Dade County is currently conducting an RFP for the redevelopment of Block

45, a county-owned parcel centered at 152 Northwest 8th Street near the Historic

Overtown Metrorail station in an area currently dominated by state and county

offices. This development will likely be majority retail and affordable housing but may

contain some market-rate rentals. Sawyer’s Landing (Block 55) is also proposed for

115 units of workforce housing and 220,00- SF retail.

11 | Integra Realty ResourcesResale Condominium Pricing

Figure 4

Average $/SF Sale Price Trend – Greater Downtown Miami Resale Market

$500

$457

$431 $426

$405

$372 $392

$400

$305

$300

$240

$221 $224

$200

$100

0

2009 2010 2011 2012 2013 2014 2015 2016 2017 1H 2018

F igure 5 shows that resale pricing continued to dip slightly in 2018, returning in between 2013-2014

levels on a per square foot (PSF) basis. This appears to be mainly driven by an ever-increasing

inventory of new listings even as sales velocity increases has ticked up in the past year. May and

June of 2018 represent two of the three strongest months since 2015 in terms of sales volume.

This uptick in velocity may be in response to softening pricing, but can also be largely characterized

by the markets’ recognition that pricing is unlikely to fall much below $350/SF which is generally

seen as replacement cost.

12 | Integra Realty ResourcesResale Condominium Pricing

Figure 5

Greater Downtown Miami Condo Listings (Built 2001+) by Month

(Zip codes: 33127, 33128, 33129, 33130, 33131, 33132, 33136, 33137)

Date For Sale New Listing Sold Pended Date For Sale New Listing Sold Pended

Jul-13 1,273 338 164 198 Jul-16 3,032 374 92 86

Aug-13 1,320 333 163 164 Aug-16 2,990 396 105 114

Sep-13 1,424 328 159 145 Sep-16 3,064 457 86 85

Oct-13 1,524 366 130 156 Oct-16 3,121 407 81 77

Nov-13 1,583 306 143 106 Nov-16 3,167 389 88 82

Dec-13 1,591 280 134 121 Dec-16 3,124 353 94 104

Jan-14 1,645 419 108 175 Jan-17 3,198 553 68 90

Feb-14 1,684 375 105 156 Feb-17 3,258 452 85 100

Mar-14 1,822 446 159 157 Mar-17 3,304 530 114 142

Apr-14 1,904 422 148 149 Apr-17 3,264 403 111 109

May-14 1,918 387 144 155 May-17 3,277 467 142 160

Jun-14 1,926 351 146 146 Jun-17 3,251 422 117 120

Average 1,635 363 142 152 Average 3,171 434 99 106

Jul-14 1,939 345 132 120 Jul-17 3,268 440 119 105

Aug-14 1,932 340 118 155 Aug-17 3,317 464 128 118

Sep-14 1,931 356 135 147 Sep-17 [1] 3,264 285 73 62

Oct-14 2,006 410 131 140 Oct-17 3,302 437 95 104

Nov-14 2,078 342 114 104 Nov-17 3,370 473 85 100

Dec-14 2,152 357 124 99 Dec-17 3,408 395 126 106

Jan-15 2,127 399 109 136 Jan-18 3,400 571 91 120

Feb-15 2,146 408 106 153 Feb-18 3,497 500 100 109

Mar-15 2,264 499 140 143 Mar-18 3,542 410 108 135

Apr-15 2,428 518 112 155 Apr-18 3,513 427 139 164

May-15 2,481 413 152 139 May-18 3,518 472 138 160

Jun-15 2,539 452 133 124 Jun-18 3,505 400 109 117

Average 2,169 403 126 135 Average 3,409 440 109 117

Jul-15 2,568 438 130 144 [1] Hurricane Irma.

Aug-15 2,546 410 126 128

Sep-15 2,619 465 136 139

Oct-15 2,726 511 128 108

Nov-15 2,792 396 104 109 Despite recent increases in velocity, Figure 5

Dec-15 2,747 346 126 100

shows the impact that the continued flow of

Jan-16 2,859 536 90 84

Feb-16 2,976 528 83 123 new listings is having on the resale market in

Mar-16 2,980 431 111 121 greater downtown Miami.

Apr-16 3,045 469 95 110

May-16 3,041 412 88 136

Jun-16 3,057 454 120 100

Average 2,830 450 111 117 Source: Trendgraphix, compiled by Integra Realty Resources, Inc.

13 | Integra Realty ResourcesResale Condominium Pricing T he average listings per month column (Figure 5) shows the persistently high average asking inventory, and the peaks and valleys of the summer versus winter selling season. Notably, Hurricane Irma severely disrupted deal-flow in September, and disrupted the overall market for six months or longer. Despite a shortfall of 130 sales based on prior year norms, the market sales and pended listings is up YTD over 2017. The listing inventory is not likely to start declining until the balance of the condo construction pipeline delivers, gets relisted, and the market has time to stabilize back to average listing inventory in the 2,800 units per month average. Admittedly, the listing per month also includes condos that are listed for sale or rent, so when rented, these listings come off the for-sale market even though they were not pended and sold. A good deal of this inventory build-up is not solely related to the state of the condo market as much as a weakening of the for-rent market which is exposing buildings to remain in the for-sale listing statistics longer. Unfortunately, the near-term outlook that residents will flock back to the condo rental market en masse represents a pretty strong bet against the quickly expanding conventional rental market. A detailed examination of rental market statistics indicates sufficient vacancy and new product deliveries that support the conclusion that resale listing inventory is not likely to decline anytime soon. The good news is, with very remote chances of major project failures and no significant overhang of developer-owned units following delivery, the private market for condominiums can likely withstand any major price volatility. The smart money is betting that average resale condo pricing may continue its gradual decline with an equilibrium point of $360+/- per SF. We are very near the inflection point without near-term signs of market distress. It’s hard to argue there could be any better time to buy as pricing edges down late cycle. 14 | Integra Realty Resources

Rental Market Statistics IRR’s reporting in Summer 2016 and Summer 2017 provided in-depth analysis of the rental demand and pricing for both conventional rental properties and the shadow rental market comprised of condo inventory available for lease. After decreasing in 2017, condominium rents recovered across most size categories in 2018, although they remain below the 2016 high-water-mark of $2,677 per month. The condo rental market in Figure 6 indicates that average rents are down $50-$100 per month from the high of 2016. This is not such a dramatic shift in rental pricing. On a percentage basis (Figure 6a), condo rental pricing by unit type, excluding 3-bedrooms, experienced a healthy 2%-3% growth in both price per unit and price per SF. The three bedroom units at the top end of pricing ($4,500+ per month) retreated on pricing -5.9% (price per SF); and -1.1% in relative monthly price. Some of this retreat in rents in 2017 and rebound in early 2018 was a result of conventional projects in lease-up coupled with condo inventory delivering, and coming to market for lease. 15 | Integra Realty Resources

Rental Market Statistics Figure 6 Average Condo Leasing Price – Greater Downtown Miami Studio 1 BR 2 BR 3 BR Year Overall $/Unit $/SF $/Unit $/SF $/Unit $/SF $/Unit $/SF 2012 $2,255 $1,421 $2.64 $1,804 $2.33 $2,625 $2.13 $4,340 $2.25 2013 $2,371 $1,504 $2.67 $1,926 $2.30 $2,819 $2.21 $4,427 $2.51 2014 [1] $2,481 $1,632 $2.92 $2,008 $2.48 $2,908 $2.32 $4,346 $2.60 2015 [1] $2,582 $1,698 $3.03 $2,139 $2.62 $3,008 $2.45 $4,773 $2.89 2016 [1] $2,677 $1,683 $2.97 $2,165 $2.66 $3,009 $2.46 $4,675 $2.72 2017 [1] $2,522 $1,628 $2.96 $2,008 $2.49 $2,942 $2.38 $4,573 $2.77 2018 [1] $2,584 $1,661 $3.08 $2,083 $2.57 $2,944 $2.46 $4,521 $2.61 [1] Midyear. Figure 6a Average Condo Leasing Price – Year-over-Year Changes Studio 1 BR 2 BR 3 BR Year Overall $/Unit $/SF $/Unit $/SF $/Unit $/SF $/Unit $/SF 2013 5.1% 5.9% 1.4% 6.8% -1.4% 7.4% 4.0% 2.0% 11.8% 2014 4.6% 8.5% 9.4% 4.3% 7.5% 3.1% 4.8% -1.8% 3.5% 2015 4.1% 4.0% 3.6% 6.5% 5.8% 3.4% 5.7% 9.8% 11.1% 2016 3.7% [2] -0.9% -2.0% 1.2% 1.5% 0.0% 0.4% -2.0% -6.0% 2017 -5.8% -3.3% -0.3% -7.3% -6.4% -2.2% -3.3% -2.2% 2.0% 2018 2.5% 2.0% 4.1% 3.7% 3.1% 0.1% 3.4% -1.1% -5.9% [2] Increase in overall prices reflects larger unit mix (including 4 and 5 bedrooms not reported in detail). 16 | Integra Realty Resources

Rental Market Statistics

W hen looking at condominium rentals within the individual submarkets, we that most (except

for A&E) are performing well; Brickell and Edgewater saw 6%-12% price increases with notable

increases in year-over-year volume. The CBD and Midtown experienced flat or slightly declining

average rents, but also with a large jump in volume of leases.

Figure 7

Condominium Rental Rates (YTD 2018)

Overall Overall Year-over-Year Total # Leases/ Year-over-Year # of Households

Submarket Asking Achieved Price Change Month Volume Change (2018 est.)

Brickell $3,695 $2,677 6% 236 34% 19,053

CBD $2,887 $2,270 0% 101 44% 8,180

A&E $5,338 $3,213 -17% 10 -35% 8,188

Edgewater $3,334 $2,716 12% 79 84%

Midtown $2,738 $2,442 -3% 18 42% 7652 [1]

Wynwood $2,700 $2,538Conventional Apartment Rents

W ithin conventional rental communities, the picture is generally one of stability. Rent growth

remains below inflation for most property and price categories among class A- and B

communities, with studios and one-bedrooms reporting average rent declines.

In the conventional market, as property technology (#proptech) evolves, the use of daily pricing systems

for apartment projects is creating efficiency in market pricing to more finely tune rental rates based on

availability by unit type and other characteristics. During periods of high vacancy when projects are in

lease-up, these systems adjust pricing to solve for market pricing equilibrium. This partly explains the

2017 dip in conventional rental pricing. A review of the upcoming late 2018 deliveries could have a similar

affect on short-term rents heading into the fourth quarter of 2018.

Figure 8

Overall Downtown Conventional Rental Rate Survey (2,474 Total Units, Class A- and B)

$/Unit Studio 1 BR 2 BR 3 BR

Average SF $/Unit $/SF SF $/Unit $/SF SF $/Unit $/SF SF $/Unit $/SF

Q3 2014 $1,976 638 $1,585 $2.49 864 $1,605 $1.86 1221 $2,106 $1.73 1752 $2,622 $1.50

Q2 2015 $2,121 638 $1,856 $2.91 864 $1,774 $2.05 1221 $2,241 $1.84 1752 $2,707 $1.55

Q2 2016 $2,123 638 $1,937 $3.04 864 $1,772 $2.05 1221 $2,257 $1.85 1752 $2,652 $1.51

Q2 2017 $2,164 638 $1,906 $2.99 864 $1,831 $2.12 1221 $2,274 $1.86 1752 $2,751 $1.57

Q2 2018 $2,175 638 $1,867 $2.93 864 $1,823 $2.11 1221 $2,305 $1.89 1752 $2,752 $1.57

Q3 2014 -

Q2 2015 7.3% 17.1% 10.5% 6.4% 3.2%

% Change

Q2 2015 -

Q2 2016 0.1% 4.4% -0.1% 0.7% -2.0%

% Change

Q2 2016 -

Q2 2017 0.7% -1.6% 3.4% 0.7% 3.6%

% Change

Q2 2017 -

Q2 2018 0.5% -2.0% -0.5% 1.4% 0.0%

% Change

As shown in in Figure 8, the Class A-/B remained relatively steady despite the addition of new Class A

inventory and condo units available for lease. Studio and 1-Bedroom rents retreated modestly,

2 Bedroom average rents grew 1.4% year over year, and 3-Bedroom rents remained level.

18 | Integra Realty ResourcesConventional Apartment Rents

Figure 8a

Overall Downtown Conventional Rental Rate Survey (Class A, Sample Size Varies as Projects are Delivered)

Average # of Studio 1 BR 2 BR 3 BR

Rent Units SF $/Unit $/SF SF $/Unit $/SF SF $/Unit $/SF SF $/Unit $/SF

Q2 2018 $2,175 2,474 638 $1,867 $2.93 864 $1,823 $2.11 1,221 $2,305 $1.89 1,752 $2,752 $1.57

Class A- & B

Q2 2018 Class A $2,466 4,774 510 $1,873 $3.67 845 $2,164 $2.56 1,150 $2,796 $2.43 1,624 $3,916 $2.41

Q2 2017 Class A $2,360 2,349 516 $1,615 $3.13 775 $2,064 $2.66 1,095 $2,711 $2.48 1,437 $3,960 $2.76

Class A Premium

13.4% 25.3% 21.4% 28.8% 53.5%

(%) – PSF

YoY Change

4.5% 17.2% -3.9% -1.8% -12.5%

(% ) – PSF

Studio rents jumped 17.2% on a price per SF basis, one and two-bedroom rents retreated -3.9% and -1.8%

respectively. The largest decline in rents per SF was in the three-bedroom rents, although those units on

average jumped in average size nearly 200 SF as Panorama entered the rent survey results. The survey

uses a rolling sample as new units enter the market, so large swings in average unit size can overstate a

decline on a price per SF basis.

Overall average rents on a gross basis increased 4.5% on average year over year. However, average

weighted price per SF declined by 2.2%. Renters this year will be getting more size for their money.

Class A-/B three bedrooms are a bargain at the moment with an average $2,752 per month, with three

bedroom condo options averaging $4,421, and conventional Class A projects averaging $3,916 per month.

19 | Integra Realty ResourcesConventional Rental Market Supply F igure 9a illustrates the current status of Miami’s under construction rental pipeline. The past 12-months, the market has delivered over 2,400 units at Square Station, Solitair, Panorama, 2500 Biscayne, and Midtown 29. Another 1,600 units will deliver in the coming 6-9 months, likely forcing average rental rates to wobble during the lease-up of new deliveries, with a normalized uptick in rents by next Summer. Unlike the condo development market where debt constraints and/or the cost of capital slowed many developers, the market for capital (debt and equity) for new urban multi-family remains robust. Just about the only market indication holding back new multi-family development has been the 2017 rent wobble, and perhaps some discipline on the part of lenders to price risk based on future supply concerns. This story is playing out in many submarkets around South Florida, and in most major markets across the U.S. A housing shortage due to undersupplied single family development continues to provide tailwinds to multi-family housing demand. Large multi-family developers and institutional investors prefer not to build into a wall of new construction deliveries. At the same time, the window is closing for cheap(er) long-term capital, so the race has been on. By the end of 2018, that race in downtown Miami will have largely been won. IRR Miami predicts new construction will slow as new employment growth plateaus. Core population growth will still contribute to new demand, but the structural 7%-9% vacancy in the market is sufficient to absorb near-term (24 month) demand without significant new multi-family construction. Like condominium projects in 2017, next year will be a much harder year to justify new multi-family construction in downtown Miami. Every market could use a pause without a hard reset. As we head into late 2018, the conventional rental development market will have its thumb largely on pause. 20 | Integra Realty Resources

Conventional Rental Market Supply Figure 9a Greater Downtown Miami Rental Pipeline - Under Construction and Complete Projects Submarket Building 2018 Q2 Status # Units Completion Date Arts & Entertainment Art Plaza Under Construction 655 TBD Brickell MaiZon at Brickell Under Construction 262 Q4 2019 CBD Muze Met Square Under Construction 391 Q3 2018 CBD Park Line MiamiCentral Under Construction 816 Q4 2018 CBD X Miami (formerly Vice) Under Construction 464 Q3 2018 CBD Caoba (fka 7th St Promenade) Under Construction 444 Q3 2018 CBD 7th Street Promenade Tower 2 Under Construction 429 TBD Edgewater Biscayne 27 Under Construction 330 Q4 2019 Edgewater Modera Edgewater Under Construction 297 2019 Midtown Midtown East Phase 1 Under Construction 500 TBD Midtown Midtown 6 Under Construction 447 TBD Midtown Midtown 8 Under Construction 387 TBD Wynwood Wynwood 25 Under Construction 289 TBD Wynwood The Bradley Under Construction 175 2019-2020 Arts & Entertainment Melody Complete 500 2016 Arts & Entertainment Square Station Complete 710 Q2 2018 Brickell Solitair Brickell (former Brickell Bayview Center) Complete 438 Q1 2018 Brickell Panorama Complete 821 Q2 2018 Brickell SoMa Complete 418 2015 Brickell Broadstone at Brickell Complete 372 2017 Brickell Brickell View Terrace Complete 76 2016 CBD Flagler on the River Complete 250 2014 CBD Monarc at Metropolitan 3 Complete 462 2015 Edgewater 2500 Biscayne Complete 156 Q2 2018 Midtown Midtown 5 Complete 400 2017 Midtown Eve at the District Complete 197 2017 Midtown Midtown 29 Complete 309 Q1 2018 Total # of Units Under Construction 5,886 Total # of Units Completed YTD 2018 2,434 Total # of Units Completed in 2016-2017 1,545 Total # Units Completed 2014-2015 1,130 Conventional Market Size/Rent Survey 2,474 Total # Units U/C or Proposed 24,110 21 | Integra Realty Resources

Conventional Rental Market Supply

Figure 9b

Greater Downtown Miami Rental Pipeline - Proposed Projects

Submarket Building 2018 Q2 Status # Units

A&E School Board Proposed 1100

Melody II Proposed 630

The Arts Proposed 550

Miami Plaza Proposed 425

Omni Station Proposed TBD

70-90 NE 17th St Proposed 225

Brickell One Brickell II Proposed 500

TBD Allen Morris/Related Proposed TBD

1111 Brickell (Yacht Club Phase II) Proposed 897

Brickell Fire Station Proposed 196

1430 Brickell (TBD) Proposed TBD

Tobacco Road Proposed TBD

El Eden Micro Units Proposed 132

Possible Redevelopment - 1809 Brickell Proposed TBD

Smart Brickell Rental Proposed 89

CBD Luma at Miami World Center Proposed 439

Lynx Tower Proposed 483

Miami World Center Block E Proposed 418

Miami River Village Proposed TBD

Grand Station Proposed 300

Nexus Riverside Proposed 462

Nexus Riverside Central Proposed 900

54 West Flagler Proposed 391

225 SE 2nd St Proposed TBD

M-Tower Proposed 440

Miami Station Tower f/k/a Krystal Proposed 153

200 NMA Proposed 328

533 NE 2 Ave Proposed 150

One Bayfront Plaza (RENTAL) Proposed 1361

400 Biscayne (RENTAL) Proposed 690

Potential Olympia Theater Proposed 300

5 Plaza Proposed TBD

Macy’s Redevelopment Proposed TBD

Knight Center Towers Proposed TBD

2nd & 2nd Proposed 637

Edgewater 1900 Biscayne Proposed 429

1836 Biscayne (Possible Condo) Proposed 352

700 Edgewater Proposed TBD

AR Edgewater Proposed 171

Quadro 3900 Biscayne Proposed 198

Ellipsis Proposed 34

The Village Proposed TBD

Miami 18 Proposed 1400

2000 Biscayne (Rental) Proposed 393

1775 Edgewater Proposed 444

2501 Biscayne Proposed TBD

Modera Biscayne Bay Proposed 296

“25” (RENTAL) Proposed 93

Prince Choice Redevelopment Proposed TBD

Midtown Midtown East Phase 2 Proposed 212

Midtown 7 Proposed 391

Wynwood 2801 NW 3rd Avenue Proposed 264

2110 N Miami Ave Proposed 163

Wynwood Plant Proposed 306

Westdale Wynwood Proposed 202

Wynwood Plant Proposed 306

Wynwood 26 Proposed 176

222 Wynwood Proposed 35

2110 N Miami Ave Proposed 163

Total # of Units Proposed 18,224

22 | Integra Realty ResourcesCondo Development Process Appendix

Proposed Reservations Contracts Under Completed

Construction

The proposed phase The reservations The contracts The Contracts stage The site This is the final

is the initial phase phase is the phase is when the is typically the improvements and stage of the

of the development second phase of initial proposition make-or-break stage vertical construction development

process; a conceptual the development and reservation of development have commenced. process; as the

plan for a new process; the of a completely as the project was At this stage of construction of the

building or project developer and undefined either well-received development, the units is completed,

is initiated by architectural/ development idea by buyers, investors, project has secured CO’s (Certificates

a developer or design team meets the actual and lenders, or sufficient pre-sales of Occupancy) are

property owner. produce additional contracting for sale it was not. If the with significant issued, and the

The developer may renderings and upon the receipt of developer has as a deposits and most closing of the unit

release a press floor plans; the further deposits. sufficient number likely a financing sales are finalized.

release or a news sales centers are The architectural of sale contracts, commitment.

story with an initial opened and the and construction buyer deposits, These projects will

rendering to gauge finishes, amenities, drawings are and a commitment enter the market

the interest in the and features of completed; the for financing, under a reasonably

project, but the the project are developer obtains the project’s definitive timeline

project size may disclosed. The government construction of 24-48 months,

change over time to developer files permitting and will most likely depending upon the

conform to market with the State of approvals. The commence. If the scale of the project

demand and/or as Florida to be able final unit floor project was not and surrounding

site due diligence to take reservations plans are defined well-received, either infrastructure

constrains the and deposits for as the reservations by a lack of pre-sales, requirements.

process. units during this are converted to or insufficient equity

stage. This begins sales contracts from initial investors

the pre-sale phase with additional or debt financing,

during which buyer deposits a project may be

reservations are upon filing of the scrapped, shelved, or

taken. Master Declaration significantly altered

of Condominium. in another future

Changes to these attempt (either later

documents are in the cycle or in the

costly, and therefore next one). Projects

the development which fail the

plan tends to Contracts stage may

be more static move all the way

following this phase. back to Proposed

during this process.

23 | Integra Realty ResourcesDisclaimer & Acknowledgment The information provided herein is for informational purposes. This publication does not render legal, accounting, appraisal, counseling, investment, or other professional advice. Should such services or other expert assistance be needed, it is recommended that the services of a competent person or firm, having access to the details of the situation, be employed. 24 | Integra Realty Resources

Images

Cover: Photo used with permission by Miami DDA.

Page 2: Photo credit: © 2015 IRR-Miami/Palm Beach.

Page 4: Photo credit: © 2015 IRR-Miami/Palm Beach. Map courtesy Miami DDA.

Page 5: Photo credit: © 2015 IRR-Miami/Palm Beach.

Page 10: Brickell, artist’s rendering of Brickell CityCentre used by permission of Swire Properties Inc.

CBD, photo courtesy Miami DDA.

Arts and Entertainment, photo courtesy Miami DDA.

Page 11: Edgewater, photo credit: © 2015 IRR-Miami/Palm Beach.

Midtown, photo courtesy Miami DDA.

Wynwood, photo credit: © 2014 IRR-Miami/Palm Beach.

Overtown, by Ebyabe, Wikimedia Commons.

Page 12: Photo credit: © 2015 IRR-Miami/Palm Beach.

Page 15: Photo credit: © 2015 IRR-Miami/Palm Beach.

Page 18: Photo credit: © 2015 IRR-Miami/Palm Beach.

Page 20: Photo credit: © 2015 IRR-Miami/Palm Beach.

25 | Integra Realty ResourcesYou can also read