Handling of Unexpected Market Closure Events in MSCI Index derivatives - Webinar February 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Handling of Unexpected Market Closure Events in MSCI Index derivatives Webinar February 2019

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Market disruptions: why does it matter? • If an Equity market is traded via cash market products (Stocks, Baskets, ETFs, Funds) it is generally not a big concern for the investors or the brokers, if those markets are unexpectedly closed for a certain period • The situation is different, if you are investing (or hedging) via derivatives such as swaps or futures. Those products have a fixed expiry date, and therefore a risk for the hedger, that the expiry level is based on a price which is not replicable Risk of a mismatch in the final settlement FSP Futures ≠ FSP Swap price (FSP) • (Total Return) Swaps are bilateral contracts, but are usually based on ISDA agreements. In those agreements, market disruption events for certain markets and their handling are defined in detail • Futures, on the other hand, are standardized contracts, based on rules defined by the exchanges offering the contracts. • None of the exchanges offering MSCI derivatives had clear and transparent rules in the past to detect and correct for market disruptions • These risks can be mitigated - and this is finally happening right now: Eurex announced in December 2018, that as of the March 19 expiry, adjustments will be made to the final settlement price in the case of Market disruptions (see Eurex circular 105/18) www.eurexchange.com 2

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 What is a Market disruption? Not a definition, but the overall idea: A market disruption in the sense of MSCI derivatives is an unexpected closure of a trading venue around the point in time, when the final settlement prices are defined. Hereby, … – … unexpected closure means: trading was supposed to be offered, i.e. no trading holidays announced upfront, but was not possible because of unexpected events like technical glitch of the trading platform, disasters like typhoon, earthquake, flooding leading to a shut-down or an earlier closure of a certain venue – … trading venue is the market place, which is defined by the index provider (MSCI) as the price source for certain stocks in an index. It could be the case that for a certain country (e.g. China), multiple trading venues are defined (HK for HKD-listings / Nasdaq or NYSE for USD-listings (=ADRs)). For the purpose of market disruption definition, the individual trading venues are therefore taken into account separately – … point in time depends on the trading hours of each venue. MSCI defines for each trading venue which stock prices are taken for the calculation of the index close. This is normally the end of day price, or an average price over a certain period. The aim of the market disruption definition is to make sure, that if those prices were not tradable / replicable, the same prices of one of the following days should be taken instead – … final settlement prices for all MSCI derivatives listed at Eurex are usually the index close levels of the third Friday of a month. Only market disruptions influencing those index close levels will be subject to potential adjustments. All standard expiries are checked for potential disruptions, whereas flex products expiring on different days are not checked www.eurexchange.com 3

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 What would we do if a disruption happens? Example: MSCI EM Asia (Eurex code: FMEA / Bloomberg code: ZTWA) No Disruption Disruption (e.g. in Taiwan) 3rd Friday Last trading day for FMEA 3rd Friday MSCI detects a market disruption + informs the relevant exchanges 3rd Friday / ~22:30 CET Standard index close is published Monday after 3rd Friday / Eurex does the Final settlement of expiring FMEA contracts based on Fridays index close ~8:00 CET Monday after 3rd Friday MSCI verifies that Taiwanese market has reopened Monday after 3rd Friday / MSCI calculates adjusted FSP with Equity & FX prices for ~22:30 CET Taiwan as of Monday, and all the rest as of Friday * Tuesday / ~8:00 CET - Eurex publishes the adjusted FSP and initiates correction payments for all relevant expired contracts * - Options moving into-the-money based on the adjustment would be automatically exercised * The above example of a disruption in Taiwan would lead to adjusted final settlement prices for 12 Futures products at Eurex + the related options: • MSCI Taiwan Futures • MSCI ACWI Futures (two versions) • MSCI AC Asia Pacific ex Japan Futures • MSCI EM Asia Futures • MSCI ACWI ex US Futures • MSCI AC Asia Futures • MSCI EM Futures (all three versions) • MSCI AC Asia Pacific Futures • MSCI AC Asia ex Japan Futures Note: Flex contracts (i.e. with expiry date different to the 3rd Friday) are out of scope www.eurexchange.com 4

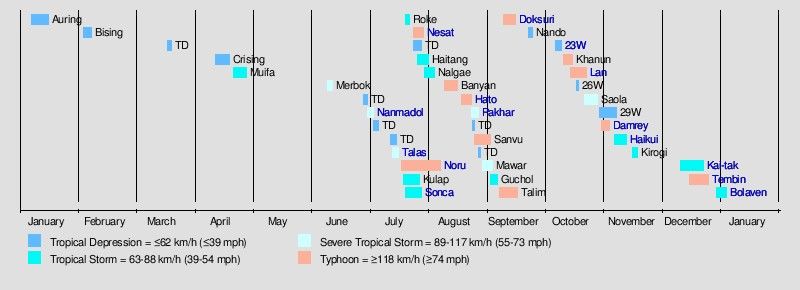

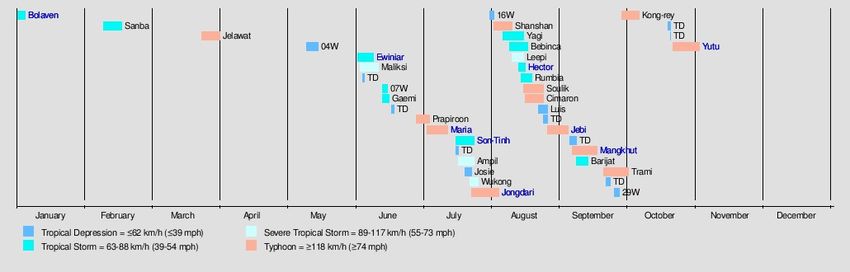

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Market disruptions: Typhoons as main risk • The highest risks for market disruptions are originating from typhoons • Market closures coming from 2017 typhoons are normally short- dated, i.e. one to three days • As shown in the graphs, the Asia-Pacific typhoon season has it´s peak in August / September • The quarterly Sep Futures expiry is therefore the one with the largest risk 2018 www.eurexchange.com 5

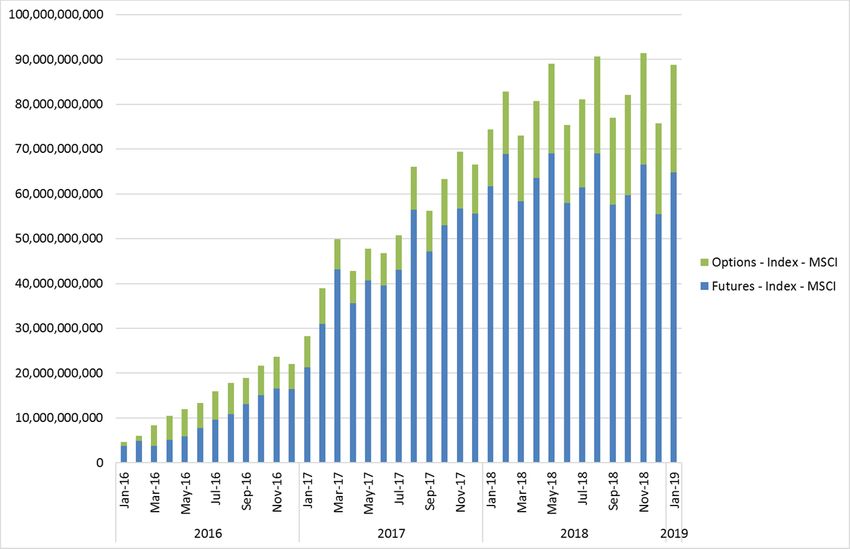

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Why are the new rules introduced for MSCI derivatives? • A first reason – very positive – is the development of the segment. In Q4, 2018, more than 4.5 mn contracts were traded and open interest in notional terms is currently ~90 bn EUR • With this growth, the risk of a financial loss for the banks increases, if there are mismatches between swaps and futures Traded contract in MSCI derivatives at Eurex Open interest in MSCI derivatives at Eurex (in EUR) • A large portion of the open interest is linked to Emerging Markets, where the risk of a market disruption is by far higher, especially in the Asian-Pacific region. More than 70% of the MSCI EM index is Asian-based • By mitigating the risks for the investment banks, who are facilitating the use of MSCI derivatives, the basement for continued growth of the segment is laid www.eurexchange.com 6

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 MSCI Unexpected Market Closure Indexes methodology The MSCI Unexpected Market Closure Indexes methodology was designed after an extensive public consultation with the investment community The complete details of the calculation are provided in the official methodology book at https://www.msci.com/index-methodology Topics for overview Unexpected Market Closure Event detection Calculation of Unexpected Market Closure Index Level Notes on MSCI Index Level variant calculation Simulated Examples ** Please note that the variant is based on a new calculation methodology and will be provided in addition to other existing index level variants (e.g. net, price, gross) of MSCI Standard and Sector Indexes. There is no change to any existing MSCI Index methodology (calculation). www.eurexchange.com

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Unexpected Market Closure Event detection Unexpected Market Closure Event: Definition An event on a given market (stock exchange) will be considered an “Unexpected Market Closure Event” when all of the below criteria are met • It is a regular business day for that stock exchange • A limitation on trading remains in effect during the half hour period preceding the close of trading for that exchange. – To account for the differences in liquidity patterns across Frontier Markets, the potential limitation on trading is evaluated for the entire period of trading hours for such exchange • Interruption in trading affects at least 50% of the securities (by number) within MSCI ACWI + Frontier Markets IMI constituents listed on that exchange. – To account for the differences in liquidity patterns across Frontier Markets, if such an exchange lists fewer than 5 MSCI ACWI + Frontier Markets IMI constituents, the interruption in trading should affect all constituents listed on the particular exchanges www.eurexchange.com

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Calculation of Unexpected Market Closure Index Level The Unexpected Market Closure Index level for the Daily Total Return (DTR) Index level of a MSCI Index will be calculated as = ( + ) ∗ = ℎ ∗ ℎ ∗ ∗ ∈ , ∈ , = ℎ ∗ ℎ ∗ ∈ , ∈ , t: futures expiry day, t+k: calculation day, V:Stock exchange for security, t+j: reopen after UMCE www.eurexchange.com

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Notes on MSCI Index Level calculation Sat Sun t+5 3rd Friday March, June, Sept, Dec Calculation t t+1 t+k deadline Market disrupted Market reopen This index level variant will be calculated only at the monthly and quarterly expiry dates Index constituent weights are not used to determine Unexpected Market Closure Events This index level variant is only calculated for 5 business days following futures expiry Both prices and FX (4pm WMR) for securities listed on a disrupted exchange are taken from first reopen day of stock exchange after unexpected closure Prices and FX from expiry day are used for securities listed on exchange that continues to be disrupted on 5th business day past expiry in the index variant calculation Corporate actions/dividends are deferred to exchange reopen day www.eurexchange.com

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Simulated Examples www.eurexchange.com

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 Q&A • Thank you for attending! • The recorded version of this webinar will be posted in our website soon. • For more information or additional questions, please contact us at: – Ralf Huesmann: ralf.huesmann@eurexchange.com – Pankaj Parmar: Pankaj.parmar@msci.com www.eurexchange.com 12

Handling of Unexpected Market Closure Events in MSCI Index derivatives February 2019 © Eurex 2019 Deutsche Börse AG (DBAG), Clearstream Banking AG (Clearstream), Eurex Frankfurt AG, Eurex Clearing AG (Eurex Clearing) as well as Eurex Bonds GmbH (Eurex Bonds) and Eurex Repo GmbH (Eurex Repo) are corporate entities and are registered under German law. Eurex Zürich AG is a corporate entity and is registered under Swiss law. Clearstream Banking S.A. is a corporate entity and is registered under Luxembourg law. U.S. Exchange Holdings, Inc. and International Securities Exchange Holdings, Inc. (ISE) are corporate entities and are registered under U.S. American law. Eurex Frankfurt AG (Eurex) is the administrating and operating institution of Eurex Deutschland. Eurex Deutschland and Eurex Zürich AG are in the following referred to as the “Eurex Exchanges”. All intellectual property, proprietary and other rights and interests in this publication and the subject matter hereof (other than certain trademarks and service marks listed below) are owned by DBAG and its affiliates and subsidiaries including, without limitation, all patent, registered design, copyright, trademark and service mark rights. While reasonable care has been taken in the preparation of this publication to provide details that are accurate and not misleading at the time of publication DBAG, Clearstream, Eurex, Eurex Clearing, Eurex Bonds, Eurex Repo as well as the Eurex Exchanges and their respective servants and agents (a) do not make any representations or warranties regarding the information contained herein, whether express or implied, including without limitation any implied warranty of merchantability or fitness for a particular purpose or any warranty with respect to the accuracy, correctness, quality, completeness or timeliness of such information, and (b) shall not be responsible or liable for any third party’s use of any information contained herein under any circumstances, including, without limitation, in connection with actual trading or otherwise or for any errors or omissions contained in this publication. This publication is published for information purposes only and shall not constitute investment advice respectively does not constitute an offer, solicitation or recommendation to acquire or dispose of any investment or to engage in any other transaction. This publication is not intended for solicitation purposes but only for use as general information. All descriptions, examples and calculations contained in this publication are for illustrative purposes only. Eurex and Eurex Clearing offer services directly to members of the Eurex exchanges respectively to clearing members of Eurex Clearing. Those who desire to trade any products available on the Eurex market or who desire to offer and sell any such products to others or who desire to possess a clearing license of Eurex Clearing in order to participate in the clearing process provided by Eurex Clearing, should consider legal and regulatory requirements of those jurisdictions relevant to them, as well as the risks associated with such products, before doing so. Eurex derivatives are currently not available for offer, sale or trading in the United States or by United States persons (other than EURO STOXX 50® Index Futures, EURO STOXX 50® ex Financials Index Futures, EURO STOXX® Select Dividend 30 Index Futures, EURO STOXX® Index Futures, EURO STOXX® Large/Mid/Small Index Futures, STOXX® Europe 50 Index Futures, STOXX® Europe 600 Index Futures, STOXX® Europe 600 Banks/Industrial Goods & Services/Insurance/Media/Travel & Leisure/Utilities Futures, STOXX® Europe Large/Mid/Small 200 Index Futures, Dow Jones Global Titans 50 IndexSM Futures (EUR & USD), DAX®/MDAX®/TecDAX® Futures, SMIM® Futures, SLI Swiss Leader Index® Futures and VSTOXX® Mini Futures as well as Eurex inflation/commodity/weather/property and interest rate derivatives). Trademarks and Service Marks Buxl®, DAX®, DivDAX®, eb.rexx®, Eurex®, Eurex Bonds®, Eurex Repo®, Eurex Strategy WizardSM, Euro GC Pooling®, FDAX®, FWB®, GC Pooling®,,GCPI®, MDAX®, ODAX®, SDAX®, TecDAX®, USD GC Pooling®, VDAX®, VDAX-NEW ® and Xetra® are registered trademarks of DBAG. Phelix Base® and Phelix Peak® are registered trademarks of European Energy Exchange AG (EEX). The service marks MSCI Russia and MSCI Japan are the exclusive property of MSCI Barra. RDX® is a registered trademark of Vienna Stock Exchange AG. IPD® UK Annual All Property Index is a registered trademark of Investment Property Databank Ltd. IPD and has been licensed for the use by Eurex for derivatives. SLI®, SMI® and SMIM® are registered trademarks of SIX Swiss Exchange AG. The STOXX® indexes, the data included therein and the trademarks used in the index names are the intellectual property of STOXX Limited and/or its licensors Eurex derivatives based on the STOXX® indexes are in no way sponsored, endorsed, sold or promoted by STOXX and its licensors and neither STOXX nor its licensors shall have any liability with respect thereto. Dow Jones, Dow Jones Global Titans 50 IndexSM and Dow Jones Sector Titans IndexesSM are service marks of Dow Jones & Company, Inc. Dow Jones-UBS Commodity IndexSM and any related sub-indexes are service marks of Dow Jones & Company, Inc. and UBS AG. All derivatives based on these indexes are not sponsored, endorsed, sold or promoted by Dow Jones & Company, Inc. or UBS AG, and neither party makes any representation regarding the advisability of trading or of investing in such products. All references to London Gold and Silver Fixing prices are used with the permission of The London Gold Market Fixing Limited as well as The London Silver Market Fixing Limited, which for the avoidance of doubt has no involvement with and accepts no responsibility whatsoever for the underlying product to which the Fixing prices may be referenced. PCS® and Property Claim Services® are registered trademarks of ISO Services, Inc. Korea Exchange, KRX, KOSPI and KOSPI 200 are registered trademarks of Korea Exchange Inc. BSE and SENSEX are trademarks/service marks of Bombay Stock Exchange (BSE) and all rights accruing from the same, statutory or otherwise, wholly vest with BSE. Any violation of the above would constitute an offence under the laws of India and international treaties governing the same. The names of other companies and third party products may be trademarks or service marks of their respective owners. The names of other companies and third party products may be trademarks or service marks of their respective owners. www.eurexchange.com 13

You can also read