How Much for a Haircut? Illiquidity, Secondary Markets, and the Value of Private Equity

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

How Much for a Haircut? Illiquidity, Secondary Markets, and the

Value of Private Equity

Nicolas P. B. Bollen Berk A. Sensoy

Vanderbilt University

Ohio State University

LBS (June 2, 2015) How Much for a Haircut? 1 / 32

Motivation

Alternative asset classes are fraught with illiquidity.

Hedge funds; Subscription periods, lockup restrictions.

Perhaps the most important question facing investors: Do returns and

diversification benefits compensate for the special risks and fees?

In private equity funds, liquidity restrictions are extreme.

LBS (June 2, 2015) How Much for a Haircut? 2 / 32

Motivation

Investors (limited partners, LPs) commit capital for 10-12 years to a partnership.

Generally no option to redeem stakes with the fund, instead must turn to the

secondary market, often at a steep discount.

LPs also face uncertainty in the timing of capital calls for investments in portfolio

companies and payoffs from exited investments.

LBS (June 2, 2015) How Much for a Haircut? 3 / 32

Motivation

For these reasons, often argued PE should command a large liquidity premium.

And often questioned whether observed returns are sufficient.

PME around 1.2-1.3 for buyout, about one for VC since 2000.

• Robinson and Sensoy (2013), Harris, Jenkinson, Kaplan (2014), Phalippou

(2014), Higson and Stucke (2014).

Buyout beats public equities by about 20-30% over the life of the fund, VC just

equals.

LBS (June 2, 2015) How Much for a Haircut? 4 / 32

What do we do?

Build a valuation model for PE commitments.

Take the perspective of a risk-averse LP subject to liquidity shocks.

Explicitly incorporate the secondary market, which the LP accesses when a shock

occurs, and uncertain capital calls and distributions.

Err on the side of taking an upper bound perspective on liquidity costs,

equivalently a lower bound on the attractiveness of PE.

Punchline: Even so, PE should be attractive to many LPs at typical allocations

given observed returns.

Not because of returns, especially in VC, but because of diversification

benefits.

LBS (June 2, 2015) How Much for a Haircut? 5 / 32

Institutional background

PE funds are organized as 10-12 year partnerships.

Fund investors = limited partners, LPs. Typically large institutions such as

university endowments.

Fund investors = general partners, GPs. GPs work at/are PE firms, such as

Kleiner Perkins or Bain Capital.

GP fees typically 2% of committed capital (management fee) plus 20% of profits

(carried interest).

LBS (June 2, 2015) How Much for a Haircut? 6 / 32

Institutional background

LPs commit capital at fund inception and do not have the option to redeem their

stake with the fund.

Commitments are not provided to the GP immediately, but are called when the GP

encounters investment opportunities (portfolio companies).

LPs receive distributions (net of carry) when portfolio companies are exited (IPO,

M&A, liquidation)

Liquidity arrangements are a natural consequence of the illiquidity of portfolio

companies.

From an LP’s perspective, it is not the illiquidity of portfolio companies per se that

matters.

LBS (June 2, 2015) How Much for a Haircut? 7 / 32

The model

LP with CRRA utility of wealth.

3 assets: riskfree security, public equity, private equity.

Evolution of private and public equity asset values follows a trinomial lattice in

discrete time.

In keeping with the real options literature.

Distribution of ending asset values is close to a bivariate normal distribution.

For a set of model inputs, solve the model backward for the LP’s t=0 certainty

equivalent (CE).

LBS (June 2, 2015) How Much for a Haircut? 8 / 32The model

We are mostly interested in solving for the expected return on PE assets that

produces the same CE as a benchmark portfolio containing no PE.

From this we back out the fund’s expected net-of-fee return.

Note this differs from the LP’s expected net-of-fee return, for which we can also

solve.

Calibrate certainty equivalents to a 80/20 portfolio of public equity and the riskfree

security.

20% riskfree allocation is a typical fixed income plus cash endowment allocation

(NACUBO, 2015).

Similar results with a 90/10 benchmark.

LBS (June 2, 2015) How Much for a Haircut? 9 / 32Endowment allocations

2014 NACUBO-Commonfund Study of Endowments

Asset Allocations for U.S. College and University Endowments and Affiliated Foundations,

Fiscal Year 2014

Short-term

Domestic Fixed International Alternative Securities/

Size of Endowment Equities Income Equities Strategies* Cash/

% % % % Other

%

Over $1 Billion 13 8 18 57 4

$501 Million to $1 Billion 20 10 20 44 6

$101 Million to $500 Million 27 14 21 33 5

$51 Million to $100 Million 31 18 21 24 6

$25 Million to $50 Million 38 19 18 18 7

Under $25 Million 43 26 14 10 7

Type of Institution

All Public Institutions 18 11 21 46 4

Public College, University, or System 15 10 22 50 3

Institution-Related Foundations 24 13 22 35 6

Combined Endowment/Foundation 21 11 18 44 6

All Private Colleges and Universities 16 8 18 54 4

LBS (June 2, 2015) How Much for a Haircut? 10 / 32The model - caveats/features

Single private equity fund.

Single capital call and single distribution/payoff.

In a portfolio of portfolio companies, not a single one.

Same as Sorensen, Wang, and Yang (2014).

LP horizon is the horizon of the PE fund.

All of these features suggest an upper bound on liquidity costs.

LBS (June 2, 2015) How Much for a Haircut? 11 / 32Model inputs

Time horizon: 12 years.

Riskfree rate: 4%.

Expected return (10%) and volatility (15%) of public equity.

Expected return on PE assets.

Volatility of PE assets: 30% for buyout (BO), 45% for VC.

Correlation between public and private equity: 0.3 for BO, 0.6 for VC.

Implies unlevered BO beta = 0.6, VC beta = 1.8.

LBS (June 2, 2015) How Much for a Haircut? 12 / 32Model inputs

LP risk aversion.

Capital call probability.

GP’s distribution probability. Increasing function of ratio of GP payoff to maximum

possible.

Probability of liquidity shock. Base rate of 1% per quarter, matching disaster

frequency documented in the macro literature.

This increases by 1%age point for each net decrease in public equity value.

If a shock hits, PE must be sold at a haircut that can be large with countercyclical

probability.

Show results for different haircut parameters.

LBS (June 2, 2015) How Much for a Haircut? 13 / 32Why sell?

Have to.

Worried about meeting capital calls on unfunded commitments.

Need to reduce PE exposure to meet allocation targets.

Need to change strategy.

We think of the liquidity shock as a reduced form way of capturing all of these

(countercyclical) effects.

Another possibility: voluntary precautionary sales in anticipation of a future

liquidity shock.

Turns out not to happen unless parameters are extreme.

LPs want to hold to maturity, suggesting that the investment horizon per se is

not a problem given the alternative.

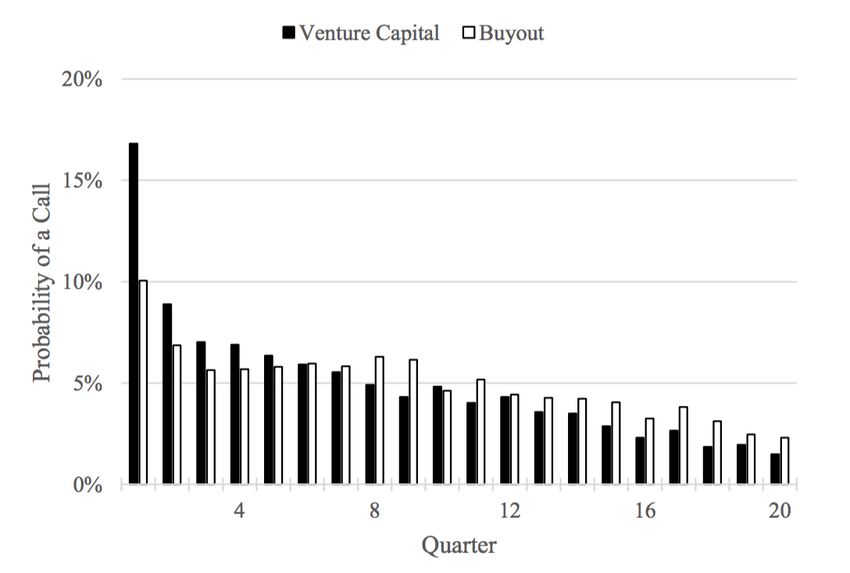

LBS (June 2, 2015) How Much for a Haircut? 14 / 32Capital call probability

LBS (June 2, 2015) How Much for a Haircut? 15 / 32Probability of large haircut

LBS (June 2, 2015) How Much for a Haircut? 16 / 32Risk aversion

LBS (June 2, 2015) How Much for a Haircut? 17 / 32Impact of call/distribution uncertainty

LBS (June 2, 2015) How Much for a Haircut? 18 / 32Impact of call/distribution uncertainty

Uncertain, random calls lower CEs.

Randomness of distributions is outweighed by GP’s strategic distribution timing.

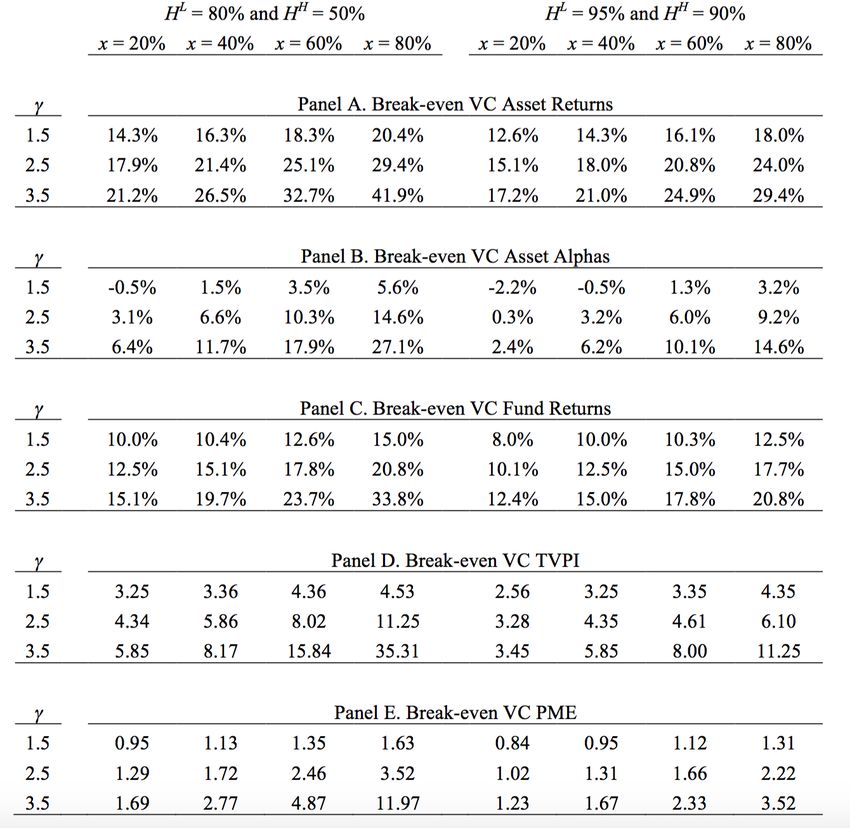

LBS (June 2, 2015) How Much for a Haircut? 19 / 32Breakevens: three assets, VC

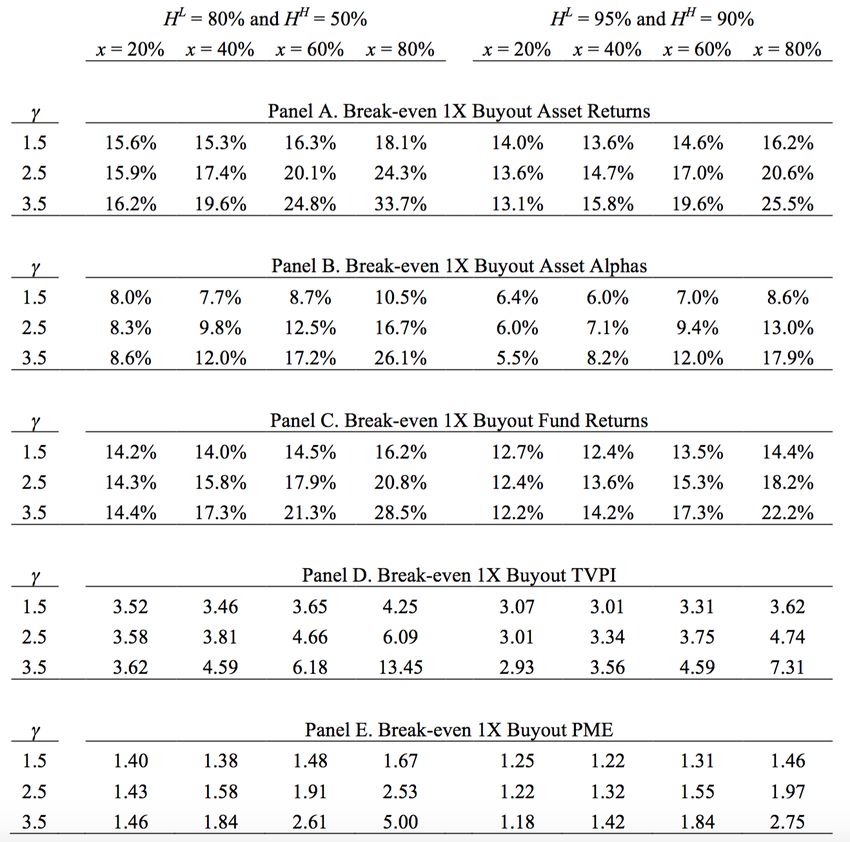

LBS (June 2, 2015) How Much for a Haircut? 20 / 32Breakevens: three assets, BO 1X leverage

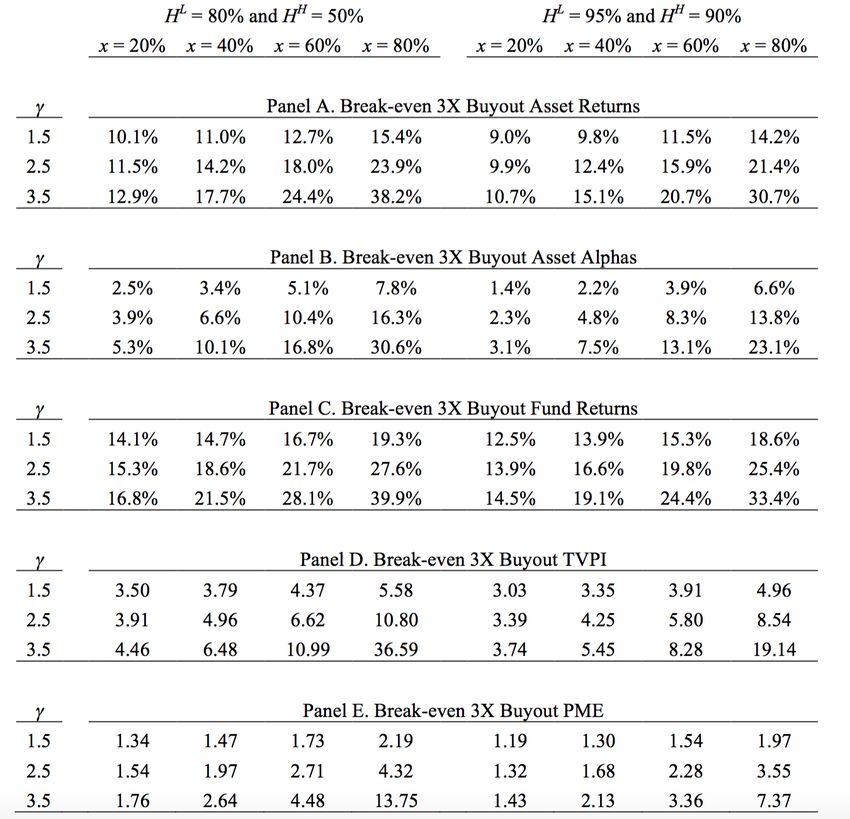

LBS (June 2, 2015) How Much for a Haircut? 21 / 32Breakevens: three assets, BO 3X leverage

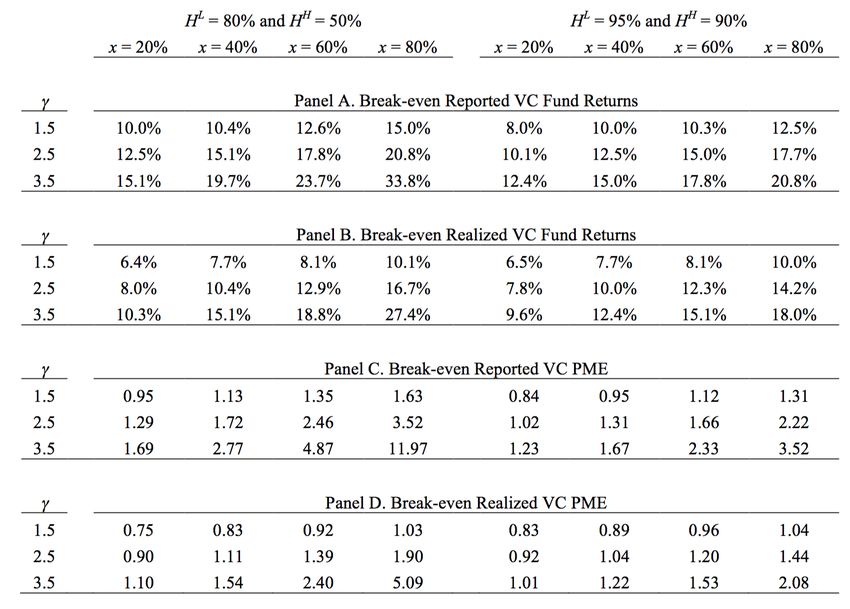

LBS (June 2, 2015) How Much for a Haircut? 22 / 32Required returns

Required returns:

Decrease in the efficiency of the secondary market.

(Generally) increase in LP risk aversion.

(Generally) increase in the allocation to private equity.

Effects mutually reinforcing:

Impact of inefficient secondary markets greater when risk aversion is high

and even more so when the PE allocation is high.

LBS (June 2, 2015) How Much for a Haircut? 23 / 32Required returns

Comparisons to empirical fund returns. PME about 1 for VC, 1.2 for buyout.

Historical performance of PE is sufficient to justify its risks and fees:

At least for relatively risk tolerant LPs at 20%-40% allocations .

Even though assumptions err on the side of an upper bound on liquidity costs.

For instance, allowing for partial liquidations will make PE more attractive.

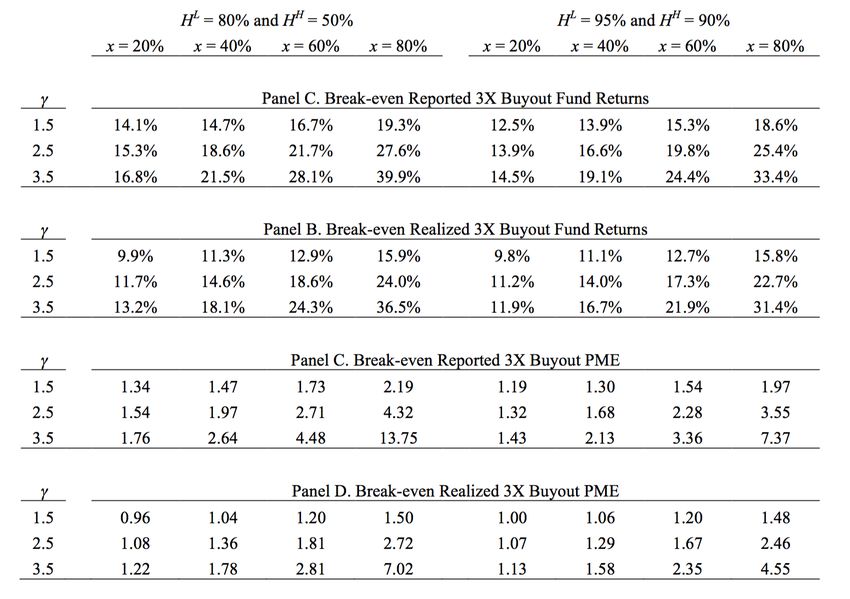

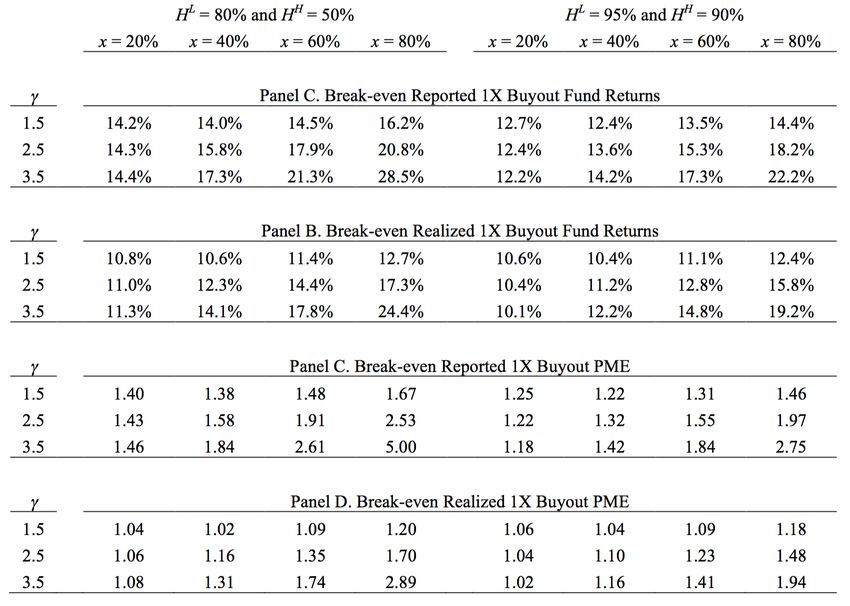

LBS (June 2, 2015) How Much for a Haircut? 24 / 32Hold-to-maturity fund returns vs. LP realized returns

Returns reported in private equity databases and used in all empirical research

are hold-to-maturity fund returns.

They are an upper bound on the expected investment experience of an LP subject

to liquidity shocks that trigger secondary sales.

This wedge is about 1.5-3 percentage points of IRR with efficient secondary

markets.

3-5 percentage points when less efficient.

PME differences are less than the cumulated IRR differences because liquidity

shocks are more likely when public equity values are low.

LBS (June 2, 2015) How Much for a Haircut? 25 / 32Hold-to-maturity fund reported vs. LP realized returns, VC

LBS (June 2, 2015) How Much for a Haircut? 26 / 32Hold-to-maturity fund reported vs. LP realized returns, BO 1X

leverage

LBS (June 2, 2015) How Much for a Haircut? 27 / 32Hold-to-maturity fund reported vs. LP realized returns, BO 3X

leverage

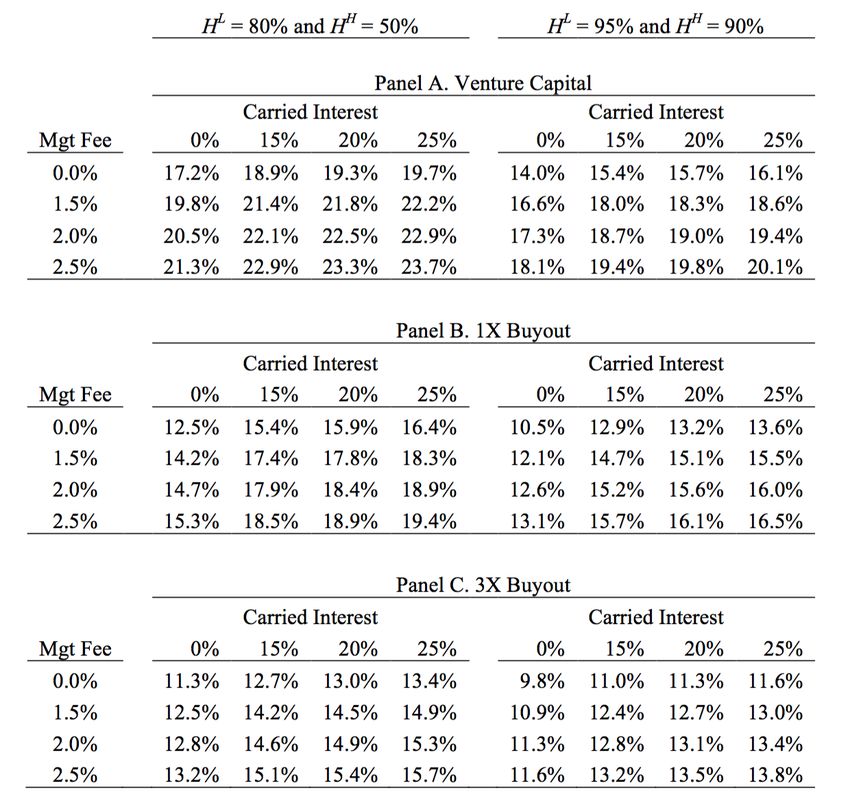

LBS (June 2, 2015) How Much for a Haircut? 28 / 32The Impact of Fees

A perennial debate in private equity is whether observed fees are excessive.

One way to shed light on this is to ask what fraction of the gross value generated

by the fund accrues to the GP through fees.

Relative to a hypothetical zero-fee fund, the standard 2-20 fee structure increases

the breakeven private equity asset return by about 5-6 percentage points, or about

50%.

GP fees capture about one-third of the gross returns generated by the fund.

LBS (June 2, 2015) How Much for a Haircut? 29 / 32The impact of fees

LBS (June 2, 2015) How Much for a Haircut? 30 / 32Optimal allocations

The model can also be used to generate optimal allocation to assets given an

expected return on PE assets.

Here, we find that expected asset returns in the 15-20% range generate

allocations in the 30%-40% range for the most risk-tolerant LPs, and 10%-20% for

more risk averse ones.

Close to the empirical distribution of endowment allocations.

This is true even though the allocation consists of a single PE fund.

LBS (June 2, 2015) How Much for a Haircut? 31 / 32Summary

We present a model of commitments to private equity funds explicitly incorporating

two major sources of illiquidity from an LPs perspective.

Stochastic cash flows and the prospect of secondary sales at a haircut.

The model also naturally embeds the payoff volatility associated with holding a

fund to maturity.

Although our estimates if anything overstate liquidity costs, PE is still attractive to a

reasonable range of LPs at observed returns and allocations.

Casts doubt on claims that PE should command a large liquidity premium.

LBS (June 2, 2015) How Much for a Haircut? 32 / 32You can also read