INDIA'S AIR TRANSPORT SECTOR - THE FUTURE IS BRIGHT BUT NOT WITHOUT ITS CHALLENGES - Global Aviation Summit

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INDIA’S AIR TRANSPORT SECTOR

THE FUTURE IS BRIGHT…

BUT NOT WITHOUT ITS CHALLENGES

January 2019

Preface In a country where train travel has long been the dominant mode of transport, India’s aviation sector has increasingly established itself as a safe, affordable and credible alternative. The number of passengers flown by Indian airlines has more than doubled over the past seven years, compared with just a 6% rise in railway passengers 1. Moreover, as the world’s largest democracy with a population of more than 1.3 billion citizens, India’s potential for further growth and industry development is very clear. Indeed, we expect air passenger numbers to, from and within India to increase by 3.3x over the next 20 years, to more than 500 million passenger journeys per year. This significant expansion is expected to be underpinned by a trebling in the proportion of middle-class households and further increases in time-saving options for air passengers. This highlights the important role aviation can play in connecting the country – both internally and with the rest of the world. This strong growth outlook for air passenger demand will see India overtake Germany, Japan, Spain, and the UK within the next 10 years to become the world’s third largest air passenger market. These are exciting times for the air transport industry in India. Of course, the future will not be without challenges – for those in the industry and policy-makers and regulators alike. These challenges will include making sure that the right type of infrastructure is put into place, at the right time and in the right location to ensure that the demand can be met, as well as ensuring that the regulatory environment is one which successfully fosters a competitive and healthy airline transport sector that will continue to make a major contribution to the Indian economy in the years to come. A robust and financially sound industry is critical to delivering the benefits that aviation can bring – creating jobs, bringing families together, facilitating business, and supporting trade, investment and economic growth. Events such as this Global Aviation Summit 2019 show that the importance of the industry is well-understood in India and underscores the initiatives that are already being taken to position the country for the key role it will increasingly have in global aviation leadership. It is my pleasure to contribute this assessment to the Summit. Brian Pearce Chief Economist International Air Transport Association Geneva January 2019 1http://www.indianrailways.gov.in/railwayboard/uploads/directorate/stat_econ/IRSP_2016- 17/Facts_Figure/Fact_Figures%20English%202016-17.pdf

Table of Contents Preface ................................................................................................................................................................. i India’s air transport industry; a global perspective ............................................................................................ 1 Recent developments ......................................................................................................................................... 1 India’s Domestic air transport market............................................................................................................ 2 India’s International air transport market ...................................................................................................... 5 India’s air cargo market .................................................................................................................................. 7 Business models & industry structures continue to evolve ............................................................................... 8 Financial performance ........................................................................................................................................ 9 The value of air transport to India ....................................................................................................................10 7.5m jobs and a $30bn contribution to GDP ................................................................................................10 Looking forward................................................................................................................................................11 Sound fundamentals point to a bright future ..............................................................................................11 The policy environment matters ......................................................................................................................13 Air passenger forecast scenarios ..................................................................................................................13 National Civil Aviation Policy ........................................................................................................................14 Travel & Tourism Competitiveness ..............................................................................................................14 Ease of Doing Business .................................................................................................................................15 Concluding comments ......................................................................................................................................16

India’s air transport industry; a global perspective

• The Indian air transport sector has shown very strong growth in recent years – particularly on the

domestic market segment.

• In October 2018, the domestic India market recorded its 50th consecutive months of double-digit year-

on-year growth; an outstanding performance and one which is showing no signs of ending anytime soon.

• The air transport market in India employs more than 400,000 people and supports another 940,000

more in the supply chain. Overall the industry contributes some US$35 billion annually to India’s GDP.

• The fundamental drivers of air passenger demand – including population and demographics and

increasing incomes – are favorable and supportive of ongoing growth over the longer-term.

• Over the next 20 years IATA forecasts growth of 6.6% per year on average – the number of annual air

passenger journeys is forecast to increase by more than 414 million over the period, moving to

over570 million journeys in 2037.

• The industry must continue to work constructively with its key stakeholders – including the government

and policy-makers – to ensure that this sizeable increase in demand can be met and to realise the full

benefits that the air transport industry can deliver to India.

Recent developments Figure 2: Annual growth in India’s O-D air

passenger journeys

In 2017, more than 158 million passengers flew on

% growth year-on-year

routes to, from and within India (Figure 1). This 30%

represents an increase of almost 15% over 2016 25%

and is the third consecutive year of growth in the 20%

15%

order of 15-20% per year (Figure 2).

10%

The figures for the 2018 year-to-date suggest that 5%

India is on track to record a fourth straight year of 0%

double-digit passenger growth. -5%

-10%

Figure 1: Total air passenger journeys to, from & 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

within India (annual) 2 Source: IATA

Million pax per year

180

The strong performance of air passenger demand

160

140

growth in India has not been confined to just the

120 past few years, however; the total number of air

100 passengers has more than doubled over the past

80

seven years, from a level of 79 million journeys

60

40

undertaken in 2010.

20

Indeed, utilising data from the World Bank and

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 ICAO, which measures the number of passengers

Source: IATA carried by airlines based in the particular country,

we can see the growth of the Indian market in a

longer-term perspective (Figure 3, over).

From flying just 16 million passengers 20 years

ago, Indian airlines have seen their passenger

2 Unless stated otherwise, all data in this report are

calculated on an origin-destination (O-D) basis.

1volumes increase more than 8-fold in the period Figure 5: Evolution of market share: Domestic vs

since. Along the way, India has overtaken a host of International

countries, including Germany and Japan, in the 100%

90%

process. 80%

70%

Placed in this longer-term context, the relative

60%

performance of the air transport industry in India 50%

is stark. 40%

30%

Figure 3: Increases in air passenger demand, 20%

10%

1997-2017, selected countries 0%

Passengers carried by airlines based in each country (million) 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

160 DOM INT

UK

140 India Source: IATA

120 Japan

100

Germany Reflecting the relative size of the domestic and

Brazil

80 international markets, the composition of the

Canada

60

Korea current in-service fleet is heavily tilted towards

40 Australia narrowbody aircraft.

20 Spain

France Narrowbodies account for ¾ of the total current

0

1997 2007 2017 fleet, with widebodies contributing a further 10%.

Source: World Bank, ICAO

The remainder consists primarily of turboprops

Returning to more recent outcomes, it is and regional jet aircraft (Figure 6).

unsurprising to note that the bulk of the flights Figure 6: Composition of India’s current aircraft

taken in 2017 were domestic in nature, accounting fleet

for around 62% of the total (Figure 4).

Other*, 14.2%

Figure 4: Composition of 2017 air travel: Domestic

vs International

Widebody, 9.9%

International

38% Narrowbody,

75.9%

Domestic Source: CAPA * incl turboprops and regional jets

62%

The following sections investigate the recent

performance and key developments for the

Source: IATA

domestic and international market segments in

Indeed, the domestic share of total traffic has turn.

been generally increasing gradually over the past India’s Domestic air transport market

decade. From 54.5% in 2007, and notwithstanding

The India domestic market is currently the fastest

some bumps along the way, the domestic share

growing (measured in terms of revenue passenger

has gradually risen to the 61.7% level of 2017

kilometres 3) of the main domestic markets that

(Figure 5).

IATA consistently track around the world.

3Revenue passenger kilometres (RPKs) is a measure of the

volume of passengers carried by an airline. An RPK is flown

when a revenue (paying) passenger is carried one kilometre.

2Over the year to June 2018, the India domestic Figure 9: Annual growth in origin-destination

market has grown by a very strong 17.6%, well passenger journeys – India Domestic

above the industry-wide (domestic markets) pace 40%

% growth year-on-year

of 7.9% (Figure 7).

30%

Figure 7: Comparison of key global domestic 20%

market RPK growth

10%

0%

-10%

-20%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: IATA

While such rapid growth cannot continue

indefinitely, equally, there are no indications that

the performance is likely to come to an abrupt end

Source: IATA

anytime soon.

October 2018 was the 50th consecutive month of Highlighting this point, and the magnitude of the

double-digit growth in India domestic passenger potential growth in the India domestic market, the

volumes, surpassing the four-year milestone. number of domestic journeys undertaken in 2017

In 2017, there were a total of 97.7 million represents just 7.3% of India’s total population.

domestic passenger journeys, up almost The strong demand outcomes over recent years

15 million from 83 million in 2016 (Figure 8). have been partly due to the stimulus of lower

Figure 8: Number of origin-destination air airfares.

passenger journeys per year – India Domestic In real (inflation-adjusted) terms, the average cost

120

Million pax per year

of an India domestic airfare has been trending

100

lower for more than a decade.

80 After rising in 2013 and 2014 which, again, in large

60

part reflects the impact of the market disruption

associated with the demise of Kingfisher, the

40

downwards trend has since resumed.

20

Figure 10: Average India Domestic airfare,

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 adjusted for inflation

Index, 2005=100

Source: IATA 100

90

Growth in the India domestic market has been 80

70

faster than that of the total market depicted 60

previously in Figure 2. 50

40

Following two lean years in 2012 and 2013 (in part 30

reflecting the demise of Kingfisher), growth has 20

10

recovered strongly. 0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

In both 2015 and 2016, India domestic RPKs grew

Source: IATA

by more than 20% and in 2017, although the pace

of growth eased moderately, it still recorded a India domestic passenger demand is also being

very strong 17.6% rate (Figure 9). Growth for 2018 driven in part by rapid expansion in the domestic

is on course to surpass this figure. air network.

3This is evident both in terms of a strong rise in the Against this backdrop of developments in demand

number of airport pairs in operation within India – and capacity, the India domestic passenger load

these have risen by more than 50% since 2015 – as factor remains elevated.

well as increases in the average frequency of

Indeed, in February 2018, it exceeded 90% for the

flights on each route (Figure 11).

first time ever, hitting an all-time high for the

Both of these factors ultimately translate into time seven global domestic markets 4 that we track each

savings for passengers and therefore have similar month (Figure 13).

stimulatory impacts on demand as reductions in

Figure 13: Domestic India – passenger load factor

air fares.

performance

Figure 11: Components of India’s domestic air 95% % of available seat kilometres Domestic passenger load factors

Domestic India

network growth: new routes vs increased 85%

The shaded area shows the min/max load factor range for

the 7 global domestic markets we track each month.

frequency*

75%

Number of airport pairs Number of flights per week

700 36

65%

34

Domestic routes (# airport pairs in operation), left axis

600 32 55%

Average flight frequency, right axis Failure of

Tōhoku earthquake Kingfisher

30 impact in Japan

45% Airlines

500

28 9/11 SARS impact in China

26 35%

400 2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

24

300 22 Source: IATA

20

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

18

The bigger picture is that the current load factor

Source: SRS Analyser * aircraft >19 seats, at least 1 flight

performance represents a significant turnaround

per week on average from the early-2000s when India regularly posted

the lowest domestic passenger load factor

Overall, India domestic demand (measured by amongst our group of countries, even dipping

RPKs) have grown faster than the corresponding below 50% on occasion.

rate of capacity growth (measured by available

The evolution and maturity of India’s domestic air

seat kilometers or ASKs) in recent years.

transport market can be illustrated by comparing

While the degree of outperformance has the experiences around the time of 9/11 with that

moderated from that seen in late-2014 and early- of late 2014.

2015, annual RPK growth has still exceeded that of

In the former, domestic capacity continued to

ASK growth by 3 percentage points on average

increase even as demand slumped, while in late-

each month over the past two years (Figure 12).

2014 Indian airlines slowed capacity growth to

Figure 12: India Domestic – passenger demand support the load factor even as demand was

(RPKs) and capacity (ASKs) growing strongly.

% year-on-year

60%

In part, this appears to reflect the increasing

50%

40%

influence of competitive (market) pressures over

Revenue passenger kilometres

30% time via a mix of policy, regulatory and industry

20%

developments.

10%

0% Such forces have instilled a greater focus on

Available seat kilometres

-10%

airlines to achieve the load factor levels needed to

-20%

-30%

generate adequate returns for their investors.

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Source: IATA

4

India, China, the US, Brazil, Russia, Japan and Australia.

4Figure 14 puts the strong and sustained growth Figure 16: World’s top ten growth airports 2017 –

performance of the India domestic market into a passengers handled

global perspective.

Since 2014, in terms of RPKs flown India has

overtaken Australia, Japan, Brazil, and Russia – all

of the main domestic markets that we follow, with

the exception of China.

The India domestic market now accounts for

around 1.5% of total industry-wide RPKs and is

larger than all of the domestic markets that we

follow, with the exception of China and the US.

Source: ACI, IATA WATS

Figure 14: Main global domestic air transport

markets, share of industry-wide RPKs

1.6%

% of industry-wide RPKs

India’s International air transport

1.5%

India

market

1.4%

Russia

1.3%

In 2017, around 60 million international

1.2%

Japan

Brazil

passengers flew to/from India, up from 55 million

1.1% in 2016 (Figure 17).

1.0%

Australia Figure 17: Number of origin-destination air

0.9%

passenger journeys per year – India International

0.8%

2010 2011 2012 2013 2014 2015 2016 2017 Million pax per year

70

Source: IATA

60

Furthermore, of the 100 largest domestic city pair 50

routes in the world in 2017, ten can be found in 40

India (Figure 15). 30

20

Figure 15: Largest city-pair routes Within India &

10

their 2017 global ranking

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

#pax 2017 YoY growth Global rank

1 Mumbai-Delhi 5,566,510 1.9% 7 Source: IATA

2 Bangalore-Delhi 3,492,889 -1.5% 20

3 Bangalore-Mumbai 2,716,801 3.0% 35 While the international market has not grown as

4 Kolkata-Delhi 2,153,297 5.6% 52

5 Delhi-Pune 1,997,165 17.5% 63 fast as its domestic counterpart, the sustained

6 Delhi-Hyderabad 1,891,240 3.8% 75 period of robust growth, over a number of years,

7 Delhi-Chennai 1,836,447 -5.4% 80

is still readily evident.

8 Mumbai-Goa 1,748,145 -0.2% 89

9 Mumbai-Chennai 1,717,468 5.1% 91

The 2017 outcomes represents an increase of

10 Delhi-Goa 1,692,230 23.6% 96

10.3% on 2016 and is the third consecutive year of

Source: IATA WATS

double-digit international passenger growth

In a similar way, of the top 10 growth airports in (Figure 18).

terms of passengers handled in 2017, two are

located in India, namely Delhi and Bangalore

(Figure 16).

In terms of global rankings, Delhi is #16 globally in

terms of passengers handled and Mumbai is #29.

5Figure 18: Annual growth in origin-destination pairs has been increasing, so too have the average

passenger journeys – India International number of flights on the international city pair

20%

% growth year-on-year routes (Figure 20).

15%

Figure 20: Average flight frequencies on

international airport pairs served, selected

10%

countries

Average flight frequencies (per week per int'l airport pair)

5% 14

India

12 12.1

0%

10 Brazil

8.6

-5% China 8.4

8

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

7.1

Source: IATA 6

Russia

4

Contributing to this growth performance, India 2

has steadily increased the number of overseas city 0

pairs served by a non-stop service from the 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: IATA, SRS Analyser

country over time (Figure 19).

In 2018, there are 304 such international pairs, up In contrast to both China and Russia, India is well

from around 230 ten years ago. served by the frequency of flights on the

international markets served.

Figure 19: Non-stop international airport pairs

served, selected countries India has almost four additional frequencies per

1,200

Non-stop int'l airport pairs served week on average between the airport pairs

1030 compared with both Russia and China.

1,000

800

China A choice of flight times is particularly important for

business travelers who value the flexibility the

600

Russia

576

additional frequencies provide.

400

India 304 The bulk of international traffic is to the Middle

200

Brazil 149 East and Asian destinations, with these two

0 markets accounting for around 70% of the total

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: IATA, SRS Analyser share of international traffic from India in 2017

(Figure 21).

In relative terms, the India market appears to have

Figure 21: Share of international traffic by

considerably less international city pairs served

continent, 2017

than either China or Russia. Sth America,

Africa, 2.8%

0.2%

Nth America,

However, Indian travelers have ready access (via 11.6%

the geographic proximity) to the Middle East

super-connector hubs – Dubai, Abu Dhabi and

Doha – that China and Russia do not. Europe, 13.6%

Middle East,

41.5%

This increases the size of the network significantly

for Indian travelers, as well as making India more

accessible for international visitors. As such, it may Asia, 30.3%

go some way to explaining the relatively lower

Source: IATA

number of international city pairs for India relative

to China and Russia. Looking more closely at the composition of

As was the case for the India domestic market, at international travel, at the country-level, the top

the same time as the number of international city

610 international markets account for two-thirds of Figure 23: Top freight country pairs from India,

the total (Figure 22). 2017

Other , 22.2%

The United Arab Emirates (UAE) leads the way,

with almost 20% of the total, followed by Saudi UAE, 28%

Arabia and the United States each with just over

9% market share. Kuwait, 2%

Thailand, 3%

Figure 22: Share of international traffic by country, Germany, 4%

2017

Saudi Arabia, 5%

Qatar, 11%

Singapore, 5%

Other, 32.9%

UAE, 19.8%

Hong Kong, 6% UK, 6% Ethiopia, 7%

Source: IATA

US, 9.3%

Figure 24 depicts the relative market size (in

tonnes) and the annual growth rate of India’s top

Qatar, 2.9% S.Arabia, 9.3% 10 air cargo trading partners.

Kuwait, 3.1%

Malaysia, 3.6% Singapore, 5.4% While the UAE is clearly the largest market by

UK, 5.1%

Oman, 3.9% Thailand, 4.6%

some margin, the fastest growing market was

Source: IATA

Ethiopia, which more than doubled its cargo

tonnage with India in 2017. Kuwait and Thailand

also deserve a mention with growth exceeding

India’s air cargo market 30% for the year for both countries.

While the focus of this paper to date has been on Of the top ten markets, Hong Kong was the only

the air passenger market, it would be remiss to one to see a fall in its cargo tonnage with India in

overlook the air cargo segment. 2017, down a modest 0.3% compared with its

This is particularly the case given India’s 2016 volume.

integration into the global pharmaceutical value Figure 24: Top freight country pairs from India,

chains – a strong growth performer for the air tonnes & annual growth, 2017

cargo segment over recent years.

tonnes %ch

Nonetheless, 2017 was also an impressive year of UAE 292,556 4.7%

growth for the Indian air cargo market. Qatar 113,652 18.2%

Ethiopia 77,626 114.4%

The total cargo tonnage flown from India crossed UK 66,275 16.0%

the one million tonne threshold in 2017, with a Hong Kong 61,460 -0.3%

Singapore 58,146 5.4%

strong, double-digit growth rate of 16.9% 5. Saudi Arabia 52,041 25.6%

Germany 46,583 6.3%

The top ten trading partner countries for Indian air Thailand 32,872 34.2%

cargo account for almost 78% of the total Kuwait 24,576 30.2%

(Figure 23). Source: IATA WATS

The UAE leads the way with almost a 30% market

As was the case on the passenger side, India has

share, followed by Qatar with 11%.

two airports ranked in the global top 10 fastest

growing in 2017, namely Mumbai and Chennai.

These two airports recorded very strong growth of

18.1% and 17.2%, respectively in 2017 (Figure 25).

5

The top freight country pairs cover all scheduled traffic,

excl. integrators. The data are uni-directional in nature.

7In terms of global rankings, Dehli and Mumbai For India the growth of the LCC market has been

appear in the list of the top 50 airports for freight significant. In 2004 there were just over 5 million

handled, at #29 and #31, respectively. total LCC seats offered. Incorporating the

schedules data for the remaining months of 2018,

Figure 25: The top 10 growth airports 2017 – cargo

this figure has risen to almost 135 million seats –

handled

an increase of 27x in the 14-year period

(Figure 27).

Figure 27: Increase in the number of LCC seats in

the Indian air transport market

Total LCC seats (DOM+INT)

160,000,000

140,000,000

120,000,000

100,000,000

80,000,000

Source: ACI, IATA WATS 60,000,000

40,000,000

20,000,000

0

2004 2006 2008 2010 2012 2014 2016 2018

Business models & industry Source: SRS Analyser

structures continue to evolve

Even if you consider just the past five year period,

Globally, air transport is a highly dynamic industry

the number of LCC seats in the Indian market has

and in this regard, the industry in India is no

more than doubled, from 64 million in 2013.

different.

One of the key competitors for airlines

As markets evolve and customer demands change,

domestically is the extensive train network in

airlines must constantly review and update their

India. The train system carries more than 8 billion

operations and product offering to ensure that

passengers per year. Many of these will be

they continue to meet the market need.

commuter trips over relatively short distances, for

One important part of this story is the evolution in which air travel is not a viable substitute.

business models and market structures observed

However, a proportion of these train journeys

in the industry, notably the rise of the so-called

could potentially be taken by air; the market

Low Cost Carrier (LCC) business model (Figure 26).

opportunity for an affordable airline alternative is

All told, at the global level, LCCs account for clear.

around 28% of the total number of seats flown.

Looking at the share of LCC seats in the Indian

Figure 26: Proliferation of the LCC model globally market brings to light a number of interesting

observations.

Firstly, around 55% of all seats in the market are

offered by low cost carriers (Figure 28). Focusing

on the domestic market alone, the LCC share of

total seats is almost 70%.

While the share of LCC seats offered on India’s

international routes is much smaller, at just under

25%, this share has risen from essentially zero in

2004.

Source: SRS Analyser

8Figure 28: Share of LCC seats in the Indian air Amongst Indian airlines, there are currently

transport market around 600 aircraft in service. Evidencing the

LCC seats, share of total optimism and positive outlook for the sector, and

80%

70%

providing some insights as to the near-term

60%

INT DOM TOTAL

evolution of the market, some 1123 aircraft are

50% currently on order for India. The bulk of these

40% deliveries are currently slated for delivery to

30% IndiGo – a major low cost carrier (Figure 29).

20%

10%

Figure 29: Aircraft currently on order – Indian

0% airlines

2004 2006 2008 2010 2012 2014 2016 2018

Air India

Source: SRS Analyser

Vistara

Arguably, the emergence of LCCs has facilitated GoAir

the democratization of air travel and fueled

Jet Airways

aviation growth, albeit in various ways across

SpiceJet

different markets.

IndiGo

In emerging markets LCCs have broadened the

0 50 100 150 200 250 300 350 400 450 500

market and allowed more people the opportunity # aircraft

to fly for the very first time. In more mature Source: CAPA

markets, LCCs have deepened the market allowing

people to fly more often.

Given its prevalence, the LCC model cannot be

Financial performance

ignored in any assessment of India’s air transport

Historically, the global air transport industry has

market. However, LCCs aren’t the only way in

struggled to generate consistent profits. Even in

which the industry is evolving.

periods of strong demand, profitability has,

Increasingly, we are seeing a blurring of the historically, proven to be elusive.

traditional distinction between full service airlines

While, as a rule, airlines have been able to pay

and LCCs as each are increasingly adopting

their debts, equity investors typically have not

practices typically the domain of the other,

been adequately compensated for risking their

resulting in a so-called ‘hybrid’ business model.

capital in the sector.

More broadly, there are range of new and

The last three years – and we expect 2018 to be

alternative investment and alliance or partnership

the fourth – have seen a turnaround in this

structures emerging globally which add a new

situation at the global, industry-wide level.

dimension to the industry, as airlines try to find

new and innovative ways to expand their The industry is now generating returns which

networks and their product offering. In some exceed its cost of capital, and delivering a net

global markets, the changing industry structure is profit figure of around US$30 billion per year

one of consolidation rather than expansion. (Figure 30).

These developments can apply to both the

international and domestic markets. Indeed, some

of these new structures and arrangements are

evident in the Indian air transport industry, having

been supported by changes in the regulatory and

policy environment.

9Figure 30: Global airline industry financial Figure 32: Financial performance of selected

performance Indian airlines vs the global industry, EBIT margin

10.0

% revenues

Global commercial airline profitability

US$ billion

40

2013-2018*

8.0 EBIT margin

30 15%

6.0 EBIT margin (left axis)

20 10%

4.0

2.0 10 5%

0.0 0

0%

-2.0 -10

-5%

-4.0

Net post-tax profit (right axis) -20

-6.0 -10%

-8.0 -30

Air India SpiceJet IndiGo

-15%

-10.0 -40 GoAir Jet Airways Industry

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

-20%

2013 2014 2015 2016 2017 2018

Source: IATA

Source: Airline Analyst *data for Indian airlines related to

Unfortunately, for the most part, the airlines in year-ended 31 March, industry data relate to the calendar

India have not yet been able to match this recent year prior

improvement in the industry-wide financial

performance (Figure 31). It is clear that the overall industry in India is not

yet on a sound financial footing and this remains a

Over the period shown, most airlines have work-in-progress for the industry and its key

struggled to consistently generate a net profit stakeholders, including policy-makers.

after tax; the main exception being IndiGo who,

along with GoAir, are the only airlines to have While the industry has demonstrated resilience in

generated profits in each year of the period the face of various shocks and disruption

shown. The recent financial performance of Air (including the global financial crisis and airline

India has been well-documented elsewhere. exits), financial stability is a key factor for the

industry to be able to successfully develop and

Figure 31: Financial performance of selected grow.

Indian airlines, Net profit after tax 2013-2018*

Net profit after tax, US$m

500

300

100 The value of air transport to

-100

-300

India

-500 6.2m jobs and a $35bn contribution to

-700

Air India SpiceJet IndiGo

GDP

-900

GoAir Jet Airways The air transport sector makes a significant

-1100

2013 2014 2015 2016 2017 2018 contribution to the Indian economy (Figure 33).

Source: Airline Analyst * data relate to year-ended 31 March

Analysis undertaken by Oxford Economics shows

In a similar way, many Indian airlines have been that the air transport sector directly contributes

unable to match the global industry performance 404,000 jobs in India. This includes airlines, airport

in terms of operating (EBIT) margin either. operators, airport on-site enterprises such as

restaurants and retail, aircraft manufacturers and

The performance of GoAir and IndiGo are again

air navigation service providers.

notable over the period, as is the improved

financial results of SpiceJet in more recent years. In addition, by buying goods and services from

local suppliers the sector supported another

943,000 jobs across the supply chain.

10Figure 33: The value of aviation in India Looking forward

Sound fundamentals point to a bright

future

IATA’s long-term passenger forecasts for India

highlight the potential for significant growth in air

transport demand over the next twenty years.

A favorable population and demographic profile –

notably a relatively young population – along with

the expected continuation of economic

Source: Oxford Economics, IATA development and growth in household incomes

underpins this very positive long-term outlook.

On top of this, the sector is estimated to have

India’s population is expected to increase further

supported a further 553,000 jobs by paying wages

over the forecast horizon, rising from 1.3 billion

to its employees, some or all of which are

persons currently to 1.6 billion by the end of our

subsequently spent on consumer goods and

forecast horizon (Figure 34).

services and create employment in other sectors

of the economy. This ongoing population increase is expected to

see India overtake China as the world’s most

Air transport brings tourists and investment into populous country within the next decade. Of itself,

India, and helps businesses trade their goods and a growing population will typically have a positive

services around the world. Foreign tourists impact on the demand for air transport services.

arriving by air to India, who spend their money in

Figure 34: India’s population forecast

the local economy, are estimated to have

Population , billion persons

supported an additional 4.3 million jobs. 1.8

1.6

1.4

But it’s not all just about employment.

1.2

1.0

The air transport industry (directly and indirectly)

0.8

is estimated to have supported an $10.4 billion 0.6

gross value added contribution to GDP in India 0.4

while spending by foreign tourists supported a 0.2

0.0

further $21.2 billion gross value added 2006 2011 2016 2021 2026 2031 2036

contribution to GDP. Source: Oxford Economics, IATA

Furthermore, the air transport jobs tend to be In addition to the expected increase in population,

highly productive – not just for their airline India is also forecast to become a richer country

employers but for the economies in which they over the next 20 years.

are employed.

After adjusting for inflation, per capita incomes

The average air transport services employee in are expected to increase to almost US$5,000 per

India generates nearly INR1.3 million in Gross year in 2036, up five-fold since 2006 and more

Value Added annually, which is around 10 times than double the current level (Figure 35).

more than the economy-wide average.

11Figure 35: India’s rising incomes – GDP per capita Figure 37: India’s forecast air passenger demand,

5,000

GDP per capita, real US$ 2017-37

4,500 Million O-D passengers per year

600

4,000

3,500 500

3,000

2,500 400

2,000

300

1,500

1,000 200

500

100

0

2006 2011 2016 2021 2026 2031 2036

0

2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Source: Oxford Economics

Source: IATA/TE

At the same time, the number of middle-class

households in India is expected to continue to The additional 359 million passengers will not be

increase over the coming decades, to around 20% sourced evenly from the domestic and

by 2036, compared with just 2% in 2006 (Figure international segments.

36). Domestic passengers will account for around 63%

Figure 36: Increase in the share of middle class of the total growth over this period, or 228 million

households in India additional passengers.

% share of middle class households

20%

Forecast to rise by a further

Foreign passengers will contribute less to overall

18%

16%

13 percentage points over

the next 20 years

growth, representing 37% of the total market

14% growth, equal to 131 million additional passengers

12%

(Figure 38).

10%

Risen by 5 percentage

8% points since 2006 Figure 38: Expected increase in Indian air

6%

4%

7% in 2017

passenger demand 2017-37, and DOM vs INT

2% contributions

0%

Passenger flows (million)

2006 2011 2016 2021 2026 2031 2036 400

Source: Oxford Economics 350

300 INT

36.6%

The latest IATA/Tourism Economics (TE) forecasts 250

suggest the demand for air travel to, from and 200

within India – on an Origin-Destination basis – will 150 DOM

63.4%

increase at an average rate of 6.1% per year over 100

the next twenty years. 50

0

India is forecast to gain an additional 359 million Total pax INT & DOM

passengers by 2037, compared to 2017 (Figure Source: IATA/TE

37); an increase of 3.3x the current level.

Of the 6.1% average annual growth in Indian air

This means that, by 2037, there will be almost passenger demand over the next 20 years,

520 million passengers flying to/from and within improvements in living standards (via higher

India each year. incomes) are expected to contribute the major

share, at 5.1 percentage points.

Favourable population and demographic factors

are forecast to contribute 0.6 percentage points to

annual growth. Other factors, mainly future

technological gains, will contribute 0.8 percentage

points per year.

12The modest subtraction from growth (0.5 to maintain their ranking over the forecast period

percentage points) from trade mainly reflects the (Figure 41).

Oxford Economics view that the economy will

The mature air transport markets of the UK and US

become slightly less trade intensive over the

are expected to see the largest decline in rankings,

forecast horizon (Figure 39).

losing 3 places and 2 places to #9 and #6,

Figure 39: Sources of growth in India’s air respectively.

passenger demand, 2017-37

Figure 41: Top 10 Indian air transport markets,

7

%, %age pt Living standards Pop'n & Demog. Technology Trade

2017-37

6 0.8 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

0.6 Dom. India 1 Dom. India

5

UAE 2 UAE

4

S. Arabia 3 S. Arabia

3 6.1

US 4 Singapore

5.1

2 Singapore 5 Thailand

1 UK 6 US

0 Thailand 7 Oman

-0.5

-1 Oman 8 Qatar

Total pax Drivers

Malaysia 9 UK

Source: IATA/TE Kuwait 10 Malaysia

Putting this performance into a global context, the

S

Source: IATA/TE

positive outlook will see India move up from the

#7 ranked largest air passenger market in the

world currently to #3 (behind China and the

The policy environment matters

United States) within the next decade. India will

It is important to note that while the fundamental

hold this position through to the end of our

drivers of air passenger demand provide a

forecast horizon in 2037.

favorable tailwind to growth in the sector, these

Along the way, India will overtake Germany, outcomes are not guaranteed.

Japan, Spain and the United Kingdom (Figure 40).

Demand forecasts can be impacted – either

Figure 40: Top 10 global air transport markets, positively or negatively – by a range of other

2017-37 factors, including the availability of infrastructure

US 1

2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

China and broader government policy decisions around

China 2 US market regulation and liberalization, for example.

UK 3 India

Spain 4 Indonesia Air passenger forecast scenarios

UK

Japan 5

As part of the forecast process, we prepare two

Germany 6 Spain

India 7 Japan

generic global scenarios.

Italy 8 Germany

France 9 Thailand

The scenarios are designed to demonstrate the

Indonesia 10 France possible impacts on air passenger demand of both

S

Source: IATA/TE a more favorable future outcome (where there is

policy stimulus and further air transport market

The composition of the top ten air transport liberalization) and a less favorable future outcome

markets for India show relatively little change over where policies are more restrictive and there is a

the 20-year forecasting horizon. pick-up in protectionism.

Kuwait is set to drop out of the top 10, to be The effect of these two broad scenarios on India’s

replaced by Qatar as the only compositional

air passenger demand forecasts are depicted in

change expected. The top 3 markets (Domestic

Figure 42.

India, the UAE and Saudi Arabia) are all expected

13Figure 42: India’s air passenger demand outlook More recently, a new draft scheme has been

under three scenarios, 2017-37 announced seeking to extend the UDAN

1000

Million O-D passengers per year framework to international routes.

800

Baseline

Travel & Tourism Competitiveness

Policy Stimulus & Market Liberalisation

600

The World Economic Forum’s (WEF) Travel and

Pick-up in Protectionism

Tourism Competitiveness Index provides a

400

framework to assess and benchmark the factors

200 and policies which impact a country’s T&T sector

competitiveness.

0

2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

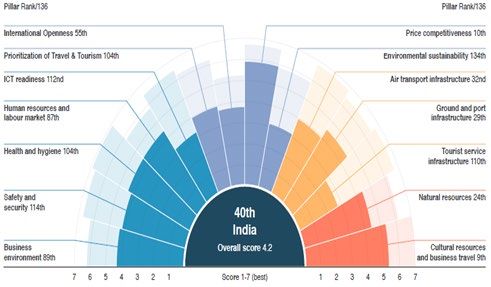

In its latest report, India ranks #40 out of the 136

Source: IATA/TE

countries assessed, a strong improvement of 12

Under the less favorable scenario, India’s air places over the previous survey (Figure 43).

passenger market will still grow, albeit at a slower India’s strengths include its vast cultural and

pace, of 4.9% per year. While this difference natural resources (ranked 9th and 24th,

doesn’t seem significant, it translates to more respectively), and its price competitiveness

than 100 million less passengers per year in 2037 advantage (10th).

than under the ‘constant policies’ scenario.

The WEF notes that India continues to enrich its

On the upside, a more favorable policy backdrop cultural resources, protecting more cultural sites

could see air passenger demand for India growing and intangible expressions through UNESCO

at a near-double digit annual pace of 9.1%, World Heritage lists, and via a greater digital

generating an additional 385 million passengers in presence.

2037 compared with the constant policies

scenario. This would take the number of International openness (55th, up 14 places),

passengers travelling to, from and within India by through stronger visa policies implementing both

air to just over 900 million in 2037. visas on arrival and e-visas, has enabled India to

rise up through the global ranking.

National Civil Aviation Policy

In the Indian context, no consideration of the The travel and tourism sector benefited from

policy environment could overlook the recent improvements in India’s transport infrastructure,

National Civil Aviation Policy (NCAP). which the WEF notes has traditionally been a

challenging area.

The 2016 introduction of the NCAP brought a

number of important initiatives and In this regard, it is notable, that the air transport

developments to India’s air transport industry. infrastructure sub-component places India 32nd

currently in the global ranking.

The policy addresses a range of key areas for civil

aviation including airline operations, safety and Figure 43: India’s travel & tourism competitiveness

security, international traffic rights and

maintenance, repair and overhaul (MRO)

operations.

The NCAP aims to make flying more affordable

and convenient to the general population,

including by establishing a regional air

connectivity scheme, the UDAN initiative.

Source: WEF

14Nonetheless, there is always room for A strong and vibrant business environment

improvement which could lift India’s ranking into stimulates employment opportunities, investment

the top quartile of countries. and trade which the air transport sector can both

help to enhance and benefit from.

Within the air transport infrastructure category,

India ranks relatively low (133rd) in terms of The World Bank’s Ease of Doing Business Index is

airport density (the number of airports per million designed to provide objective data for use by

of population) and 108th for the number of governments in designing sound business

departures per 1000 population. regulatory policies.

While health conditions in the country continue to The latest index reveals strong improvement,

improve, the WEF includes India towards the ranking India at #77 of 190 countries, ahead of the

lower end of its global rankings for this indicator South Asia regional average.

(104th).

Key challenges for India highlighted by the World

Similarly, the WEF notes that while India’s ICT Bank include dealing with enforcing contracts and

readiness (112th), security concerns (114th), resolving insolvency.

tourist service infrastructure (110th) and human

Importantly, and as was the case with the WEF

resources (87th) are slowly improving, further

work is required across these dimensions to lift measure discussed above, improvements in the

India’s overall global ranking. broader business environment in India are

underway; India’s ease of doing business ranking

Importantly, the WEF is clear that steps are has risen from #132 just five years ago, clearly

already being taken in the right direction to moving in the right direction.

address the shortcomings and concludes that “the

Indian transport and tourism sector presents

significant opportunities that are yet to be

reaped”.

India’s travel and tourism competitiveness ranking

relative to its Asia Pacific peers is shown in

Figure 44.

Figure 44: Asia Pacific travel & tourism

competitiveness rankings

Global ranking (out of 136 countries)

140

124 125

120

101 102 103

100 94

78 79

80

64 67

60

40 42

40 34

30

26

19

20 15 16

11 13

4 7

0

Source: WEF

Ease of Doing Business

The robustness and efficiency of the broader

business environment is also important – not just

for air transport sector and related parts of the

industry supply chain.

15Concluding comments supporting services, both on the ground and in the

air.

Air transport is the business of freedom. It is so

much more than just moving people and cargo Equally, the broader business and policy

from one destination to another. environment should not place unnecessary

hurdles before the industry which inhibit its

Air transport helps to bring families together, it

growth and development and, in turn, reduce the

supports and enhances business and investment

level of benefits that aviation can deliver to the

decisions, it promotes the transfer of knowledge

nation.

and innovation, and provides opportunities to

study abroad and experience different cultures. There is no doubt that this is an exciting period for

air transport in India.

As this paper has made clear, the future of India’s

air transport industry is bright. And there is a clear mandate for the industry, its

supply chain partners and the government and

However, this does not mean that that the future

policy-makers to all work in a collaborative

flightpath will be without turbulence.

manner, towards the common goal of ensuring

The significant growth potential of the industry in that the benefits that the air transport industry

India will also create challenges – for the airlines, can bring to India are fulfilled.

its industry partners and policy-makers alike – to

ensure that this growth potential can be met.

For example, this will require the right type of

IATA Economics

infrastructure to be put into place, at the right

economics@iata.org

time and in the right place. Infrastructure is not

January 2019

just airports, it includes investment and

16You can also read