Integrating energy efficiency and other sustainability aspects into property valuation - methodologies, barriers, impacts

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Integrating energy efficiency and other

sustainability aspects into property valuation

– methodologies, barriers, impacts

Walter Hüttler Christian Schützenhofer

e7 Energie Markt Analyse GmbH KPMG Advisory GmbH

Theresianumgasse 7/8, A-1040 Wien Kudlichstraße 41-43, A-4020 Linz

walter.huettler@e-sieben.at cschuetzenhofer@kpmg.at

Klemens Leutgöb Gerrit Leopoldsberger

e7 Energie Markt Analyse GmbH Dr. Leopoldsberger + Partner

Theresianumgasse 7/8, A-1040 Wien Rheinlandstraße 62, D-60529 Frankfurt am Main

klemens.leutgoeb@e-sieben.at leopoldsberger@leopoldsberger.de

Sven Bienert

IRE|BS Institut für Immobilienwirtschaft

Competence Center of Sustainable Real Estate

University Regensburg, D- 93040 Regensburg

sven.bienert@irebs.de

Keywords

life cycle cost (LCC), economic assessment, energy efficiency • In valuation practice it is the lack of data that sets limits

investments, property valuation, operational cost differences for broad application of the modified valuation approach-

es. Valuers need reliable data bases on reference buildings

(comparables) including also data on energy performance

Abstract and different operational cost categories. Although in gen-

Property valuation is a key driver for the development of the eral property valuation is mostly driven by market forces,

property market. Since energy performance and other sustain- there remains some room for interventions to be set by en-

ability aspects are practically not integrated into standard prop- ergy efficiency policy.

erty valuation practice the market gets very little price signals

valuing highly energy efficient and sustainable buildings. Inten-

sive work in the collaborative EU project IMMOVALUE comes

up with the following results: Introduction: Green buildings ask for green value

The term sustainability becomes fashionable in the real estate

• There is no need for “new” property valuation approaches.

industry and moves from the margins to the centre. A visible

The standard valuation approaches need just a few inter-

sign of this trend is a boom of sustainability certificates for

ventions to enable an improved consideration of energy ef-

buildings, such as BREEAM, LEED, DGNB, HQE and others.

ficiency and other sustainability aspects.

Most of these certificates follow a widespread approach with

• Since for most property markets a direct statistical inter- “green buildings” encompassing the whole range of sustain-

relationship between energy performance and value can- ability aspects such as energy performance (e.g. energy con-

not be observed the analysis of energy cost differences resp. sumption), comfort parameters (e.g. indoor air quality, etc.),

of operational cost differences becomes the starting point. CO2 emissions, reusability of building materials, connection to

Comprehensive and well-structured life-cycle cost assess- local public transport, social impacts (e.g. extended productiv-

ment (LCCA) thus is a key issue for integration. ity), etc. In this context energy efficiency is an essential and

• Several pilot project valuations, however, show that the indispensable feature of a “green building”.

value impact deduced from cost differences is limited. Only This background given real estate industry becomes increas-

very energy efficient and sustainable properties come up ingly interested in the question whether resp. under which

with a premium of 5-10 %. Higher value impacts depend conditions energy efficiency and other sustainability impacts

on an increased market sensitivity towards energy efficiency have an impact on the building value. Is there something like a

and sustainability (i.e. if the markets do not only account “green value”, which is specific for green buildings but which

for cost advantages but account also for better comfort lev- at the same time, is an integral part of the overall market value?

els, for better productivity etc. to be achieved in sustainable What is the correct way to quantify the green value (if existing

buildings). at all)? And are the standard valuation approaches sufficient

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1279

Contents Keywords Authors

5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

for the quantification of green value or do they need adapta- • “Cost is not Value” – The (additional) costs for construct-

tions? ing a green building or upgrading an existing conventional

Starting from these questions the paper develops the follow- property to an energy-efficient building do not necessarily

ing thematic thread: lead to a green value and vice versa. This means that a green

or sustainable property with identical costs of construction

• The first part highlights the crucial role of property valua-

(and land) and identical certification etc. can still have a

tion for resource allocation in construction industry: Why

totally different added value in different locations, just be-

is it necessary to integrate green features into property valu-

cause the willingness to pay revealed by consumers in dif-

ation? And has property valuation the same relevance for

ferent markets might vary substantially.

all building sectors?

Furthermore it has to be mentioned that property valuation

• The second part explains briefly the standard valuation ap-

is more important for certain segments of property markets

proaches: How valuation works today?

than for others. In general, property valuation plays a more

• The third part gives a short summary on actual interna- important role for the commercial building sector than for

tional research on green value: How far have we gone in the housing sector. This is mainly due to the fact that commer-

integrating green value into property valuation? And what cial property markets usually have a higher volatility with more

still needs to be done? frequent transactions. Commercial buildings are increasingly

assumed to be ordinary financial products which are traded ac-

• Chapter four describes in detail how energy efficiency and

cording the rules of financial markets. There are, however, sev-

selected other sustainability issues could be integrated in a

eral exemptions to this rule, e.g. property valuation is a crucial

concrete valuation procedure: How can we quantify green

influencing factor in countries with more frequent changes of

value under the precondition that for most real estate mar-

ownership of single family houses and owner-occupied dwell-

kets we have available only very limited data (opaque mar-

ings, too.

kets)?

• The next chapter describes a concrete case study applying

the adapted valuation approach: How does it work in valu-

Short introduction to standard valuation

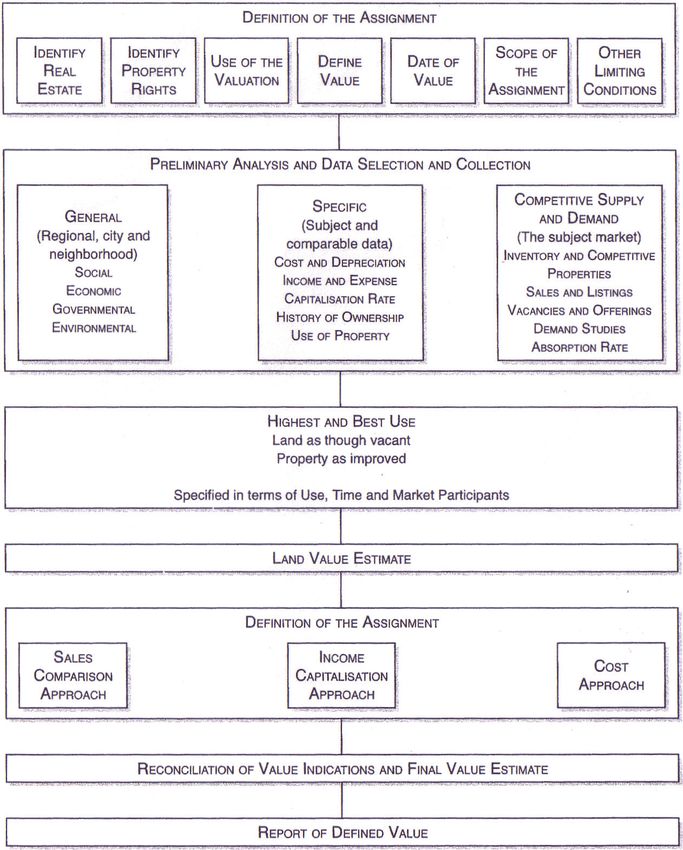

ation practice? approaches

With the exception of some national particularities and dif-

• The concluding chapter presents a summary of main con-

ferent notations, worldwide all valuers use variations of three

clusions: How could energy efficiency policy support mar- basic valuation methods.1

ket players in a widespread application of valuation meth-

ods that integrate green value? • The income related approaches can be differentiated into

the methods of direct capitalization and discounted cash

flow (DCF). The direct capitalization approach uses the es-

The crucial role of property valuers timated achievable market rents less outgoings divided by a

Property valuation can be interpreted as a decisive process cap rate/yield to derive the market value. The DCF approach

for resource allocation. In many cases – but not in all cases in contrast analyses the first 10 years of revenues and costs

– the willingness of an investor to spend (additional) money in detail on a yearly basis and assumes that the property will

to get a (more) sustainable and energy efficient building will be sold after this holding period for a so called “Terminal

be higher if sustainability aspects are reflected in the valuation Value”. The cash flows are calculated in detail for every sin-

result, i.e. if the sustainable building could be sold for a higher gle year of the holding period. Therefore, the valuer must

price. This means that in concrete investment decisions it will estimate rental growth rates, inflation rates, occupancy rates

make a difference if the investor can be sure that the extra etc. on a yearly basis. The essential advantage of the more

quality related to an energy-efficient and sustainable building complex DCF-Approach is that the assumptions are more

becomes visible in the valuation report as a green value in transparent and detailed.

quantitative terms. • In contrast to the income approaches the sales comparison

Before further discussing an integration of sustainability as- approach uses sales data/transaction prices, which are com-

pects into property valuation it is essential to understand two parable to the subject property being valued. In most cases

fundamental principles: the difficulty in applying this approach is the lack of existing

• “Valuers do not make the market”: When doing a spe-

comparable data.

cific valuation they look for market evidence. Speculating • The cost approach is deriving the (depreciated) replace-

what might happen in the future and attempting to price ment costs of the property being valued taking into account

in something that has yet to occur is not useful from the the quality of fittings, the cost level of the region, the age

point of view of a property valuer. Valuers cannot add pre- etc.

miums if the market does not support this premium with

significant evidence. In practice this principle constitutes

the retrospective nature of property valuation: Simply

because of the usual time-lag related to the preparation

of market data property valuation always lags behind the

“real” market. 1. Figure 1: Cf. IVSC (2007), p. 171.

1280 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsPANEL 5: SAVING ENERGY IN BUILDINGS 5-301 Hüttler et al

Figure 1: The Valuation Process.

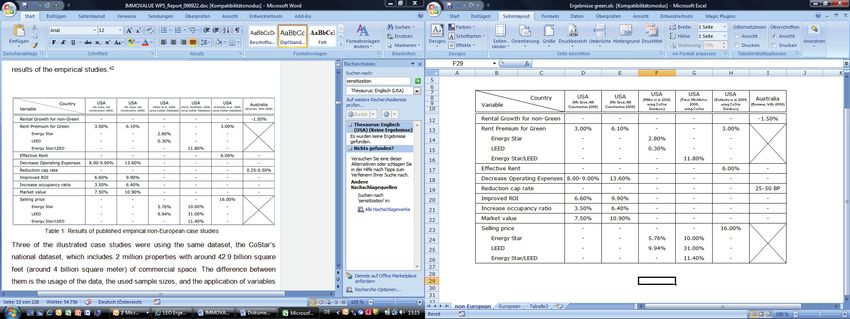

First results of international research on green ples of buildings). Table 1 summarises the quantitative results

value2 of the empirical studies differentiating also between various

factors influencing value (rent premium, improved occupancy

ratio etc.).6

Research on the link between green building features and

A similar approach has been chosen for the so-called eco-

value

logical rent tables which have been developed for the cities

In general, the research on green value is just emerging and

of Darmstadt and Berlin. The approach is based on the rent

it is too early to talk about universally valid conclusions to

tables (so called “Mietspiegel”) which landlords use as legal ba-

be drawn from these first attempts. The first studies looking

sis for fixing net rents. These rent tables are developed with real

for a potential reflection of green building features have been

empirical data updated over the years by surveys. In 2003 and

published for the US and Australia. Some organisations such

once again in 2008 the City of Darmstadt published a particu-

as the Green Building Council of Australia (GBCA)3 or the

lar rent table which takes into account the impact of energy-

New York State Energy Research and Development Authority

efficient characteristics of buildings7. This ecological rent table

(NYSERDA)4 have produced a several case studies to verify

was based on research work implemented by the Institute of

the effect sustainable features on property values. Most stud-

Living and Environment (“Institut für Wohnen und Umwelt”).

ies deal with the different available sustainability certification

Using the relevant information from the energy certificates in

systems like the American LEED, the Energy Star or the Aus-

a hedonic price model the research showed that for the city

tralian Green Star and their impacts on values. In general all

of Darmstadt a statistical proof can be assumed that buildings

they make use of hedonic price models5 (with rather small sam-

that feature good thermal performance were able to achieve a

rental-premium compared to energy inefficient buildings of up

2. A comprehensive overview on recent research on green value is given in the

IMMOVALUE Report D7.2 “Methodologies for Integration of Energy Performance

and Life-Cycle Costing Indicators into Property Valuation Practice” pp 31-40 (www.

immovalue.org) estimates prices (in the case of an additive model) or elasticity (in the case of a log

3. Cf. Bowman, R., Wills, J. (2008). model) for each of them. This information can be used to construct a price index

4. Cf. Institute for Market Transformation (2003). that can be used to compare the price of housing in different cities, or to do time

series analysis (definition according to wikipedia.org/wiki/Hedonic_regression).

5. In real estate economics, hedonic regression is frequently used to cope with the

particularities of a good that is as heterogeneous as buildings. A hedonic regres- 6. Cf. Pitts, J., Jackson, T. (2008), p. 117.

sion equation treats different attributes (or bundles of attributes) separately, and 7. Amt für Wohnungswesen Darmstadt (2003) and (2008).

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1281

Contents Keywords Authors5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

Table 1: Results of published empirical case studies for the US and Australia.

to €0.37/m²/pm8. A similar approach was also implemented for ants evaluated (among other issues) the willingness to pay for

the city of Berlin. environmental/sustainability features of assets12. 70 % of real

For Switzerland the Swiss Center of Corporate Respon- estate investors answered that they are willing to accept higher

sibility and Sustainability (CCRS) established the so called average investment cost of 8.9 % for sustainable buildings resp.

Economic Sustainability Indicator (ESI)9. ESI measures the refurbishment. On the tenants side the answers show that 86 %

long-term risks and chances of a property,10 which may occur are willing to accept higher rents by average 4.5 % if the object

between the date of sale (e.g. end of year 10) and the end of the is perceived as sustainable.

economic lifetime of the building (e.g. year 35 or 40). It iso- The IMMOVALUE project team implemented an own web-

lates and values the uncertainty, which usually is not included based survey to get an overview on the current practice of in-

in the standard valuation approaches11. Five groups of sustain- tegrating energy-efficiency respectively sustainability aspects

ability features have been identified to quantify ESI: (1) Flex- into current property valuation. Furthermore the results of the

ibility and applicability; (2) Dependency of energy and water; survey gave a rough assessment of the valuation experts’ esti-

(3) Accessibility and mobility; (4) Security and (5) Healthiness mation about the future trends with respect to the importance

and Comfort. These features are operationalised and quantified of building certification and sustainability for valuation pur-

through a risk-based weighting model that includes three main poses. The survey was communicated to about 1,000 valuation

elements: scenarios, probabilities of occurrence and dimen- experts. At the end 153 respondents were taking part, mostly

sion. Hence the ESI reflects the property’s future risk, which from Germany, Austria, the UK, Norway, Romania, Sweden,

one should consider when estimating the exit cap rate of the Belgium, and the Czech Republic. Among other results the

DCF-approach. ESI was specified for Switzerland for the mar- survey shows that 93 % of the responding valuers agree or

ket segments of multi-family houses, office and retail spaces. strongly agree that energy-efficient/sustainable buildings will

Table 2 summarizes the results of the Swiss research as well generate a higher market value, but they also assume that the

as the ecologic rent tables for Darmstadt and Berlin. importance of the topic will rise only in the future (2-5 years

from now).

Surveys on the willingness to pay for green features

Besides the research described above, which looks for statistical Conclusions from research results

correlations, there is a second direction of research focussing Even though research on the inter-linkage between sustainabil-

on the attitudes of real industry related to green value. In an ity resp. energy-efficiency and property value is just emerging,

online survey among 40 big real estate companies in Germany, one can already rule out the so called “Null-Hypothesis”, which

Switzerland and Austria the Roland Berger Strategy Consult- would mean that there is no correlation between the properties’

market value and green building features. Market evidence for

8. Knispel, J., Alles, R. (2003), p. 1.

9. Meins, E., Burkhard, H.-P. (2007); Holthausen, N., Christen, P. (2009).

10. Meins, E., Burkhard, H.-P. (2009): p. 4, p. 12.

11. In standard valuation approaches risks are reflected in the yield (interest rate) 12. Roland Berger Strategy Consultants, Nachhaltigkeit im Immobilienmanage-

applied. In practice, however, there is no coherent way how to fix the yield based ment, Kurzfassung, April 2010, http://www.rolandberger.at/media/pdf/Roland_

on a more comprehensive risk assessment. Berger_Nachhaltigkeit_im_Immobilienmanagement_20100413.pdf

1282 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsPANEL 5: SAVING ENERGY IN BUILDINGS 5-301 Hüttler et al

Table 2: Results of published empirical European case studies.

an added value of green buildings is growing due to a number • In valuation practice there are practically no transparent

of recent scientific papers and surveys. markets, which could be evaluated by sophisticated meth-

Although we can assume some market evidence for the im- ods (such as hedonic price models). Usually valuers are con-

pact of energy efficiency and green building features on prop- fronted with opaque markets for which only limited market

erty rents and values valuer need to be cautious in using this data is available. This is even truer when information on

evidence directly in their valuation reports. As regards the energy performance or operational cost is needed.

empirical studies mentioned above it has to be stressed that

– disregarding various methodological deficiencies in some of

Change in gross income as major linkage between

the studies – they all cover only certain regions and market seg-

property valuation and sustainability

ments. This means that their results cannot be simply used for

In contrast to the cost or sales comparison approach, the in-

other valuation contexts. As regards the surveys, they all show

come approach offers a broader range of possibilities for the

an increasing awareness and weight of energy efficiency and

integration of energy efficiency and other sustainability aspects.

sustainability issues among real estate companies. However,

Figure 2 shows the possible “points of contacts” for the direct

one must stress that the results show only intentions and not

capitalization method, which is the most widespread applica-

realised transactions.

tion of the income related approach.

Altogether we can conclude that the research described

The most obvious way to integrate energy efficiency and

above has detected some market evidence for an impact of

other sustainability aspects to property valuation is the adjust-

energy efficiency and other sustainability aspects on property

ment of potential gross income. If tenants have to pay a lower

value, but its results are locally limited and cannot be directly

operational cost (e.g. a lower energy bill) then they might be

used for quantifying the green value of a specific property.

willing to spend the delta on the actual paid rent (here the po-

Therefore there is a need for pragmatic approaches which the

tential gross income).13 The basic hypothesis behind this as-

valuer can use in his daily job.

sumption is the fact that that tenants benchmark their total

occupancy cost rather than just the rental payment. However,

Quantifying green value in the income related tenants will probably bargain. Therefore the reduction in op-

approach for opaque markets eration cost might be only partly reflected in a higher rent for

This background given the IMMOVALUE project team has the landlord (see Figure 3).

developed well working modified valuation approaches that Furthermore, the reduction of non-recoverable operation

ensure the quantitative integration of energy efficiency, life- expenses (the costs that cannot be passed on to the tenant)

cycle cost and partly also other sustainability issues into directly leads to higher net rents for the landlord. In addition

property valuation. The necessary modifications have been the tenants’ willingness to pay higher rents in an energy effi-

developed for all three basic valuation approaches, i.e. for the cient and sustainable building might increase just because these

income related approach, for the sales comparison approach buildings are more “prestigious” whereas rents for buildings of

and for the cost approach. The following chapter, however, a poor energy performance tend to decrease. In this case the

focuses on the income related approach for opaque (non- question is for how long the tenant might want to pay this pre-

transparent) markets for the following reasons: mium, since every new product or idea will lose its “bonus”

over time.

• The income related approach is most commonly applied for

commercial buildings which are probably the sector where

property valuation is most important for resource alloca-

tion.

13. Eddington, C., Berman, D., Hitchcock, D., et al. (2009), p.3

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1283

Contents Keywords Authors5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

Figure 2: Theoretical linkages within the Direct Capitalisation Approach.

Conventional building Sustainable building

Recoverable operating

Recoverable operating expenses

Total occupancy cost

expenses = max. potential = Operation Cost

Reduction in operating exp.

(for the tenant)

rent premium Saving Potential

(OCSP)

rent = gross income to rent = gross income to

owner owner

Comparables (Peer Group) Subject property

Figure 3: Adjustment of gross income through a rent premium based on recoverable OPEX reduction.

Modified income related approach applicable for opaque tainability aspects with the help of a scoring model. This in-

markets dication is expressed through the so-called “Market Adjust-

Starting from the adjustment of potential gross income as a ment Rate” (MAR), which the valuer can use to describe

major leverage for an integration of green value into property the quantity of the markets’ attention and willingness to pay

valuation, the IMMOVALUE project team has developed the for sustainable and energy-efficient buildings. The valuer

so-called WAPEC approach (Weighted Adjustment for Valua- needs to fill in a scoring model that addresses different as-

tion Parameter Effecting Characteristics) as one possible way to pects like price elasticity, economic (market) conditions,

quantify green value in the income related valuation approach consumer awareness, etc. The MAR ranges from “neutral”

for opaque (non-transparent) markets. WAPEC is based on an (0 %) to “high impact” (100 %). It is important to under-

easy-to-handle scoring model giving guidance to the valuer to stand that the developed scoring model is not a complete

process his thoughts regarding the integration of energy effi- and full enumeration of all green aspects. Therefore the

ciency and other sustainability issues into his valuation in a valuer still can adapt and apply the method for every single

structured and transparent way (see Figure 4). green-value-driver.

The approach consists of two parts:

• In the second part the potential rent premium must be as-

• The first part refers to an assessment of the “preparedness sessed by analysing operational cost differences between

of the market” with respect to energy efficiency and sus- the subject property and comparables. This is based on

1284 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsPANEL 5: SAVING ENERGY IN BUILDINGS 5-301 Hüttler et al

the assumption that lower operational costs can be trans-

D eg ree of Market

Influence

ferred to higher rents – but only to a certain degree which is

S ig nific ant Medium Neutral

assumed to be reflected in the MAR. A comprehensive as-

sessment of operational cost for the subject property as well C riteria

1 X C riteria

1 X C riteria

1

as for the comparables leads to the “Operating Cost Saving C riteria

… C riteria … X C riteria

…

C riteria

n C riteria n C riteria

n

Potential” (OCSP) expressed along the lines of the approach

described above: + /-‐ 66-‐100% + /-‐ 66-‐33% + /-‐ 33-‐0%

∑ (OC ) -∑ (OC )

ref, i sub, i

Average Adjus tm ent Market

A djus tm ent

Valuation E s tim ation

P aram eter

(AAP ) rate

(MA R) Adjus tm ent (VE A)

OCSP = i=1 i=1

+ /-‐ …

% x + /-‐ …

% x

rM ×12

+ /-‐ …

%

where:

Weig hted A djus tm ent F actor (WA F )

in

%

OCref operating cost element of a reference building (e.g.

Figure 4: The WAPEC approach.

average of comparables)

OCsub operating cost element of the subject property

ment cost. All in all we can assume that energy efficient and

i certain operation cost category (e.g. maintenance,

sustainable buildings have lower overall operational cost

cleaning, energy consumption etc.)

than conventional buildings, although this must not the case

rm observable market rent of comparable properties[€/ for all cost items (e.g. shading devices which are necessary to

m² p.m.] keep the cooling demand low might increase maintenance

cost). Therefore we can see life-cycle cost as something like a

The OCSP is expressed in percentage of the ordinary rent

“proxy” for sustainability in economic terms.

which is further used as average adjustment parameter (AAP)

In order to be able to handle the complexity of linkages be-

in the WAPEC approach.

tween building characteristics and operational cost a full life-

All in all the WAPEC approach can be interpreted as one

cycle cost assessment (LCCA) is indispensable. Data for the

of the possible ways which a property valuer can apply if he

LCCA may be:

observes a certain market sensitivity for the additional value

of sustainable buildings and therefore meets the challenge to • Observed cost data from existing buildings: There exist

quantify this green value. for example a few Facility Management cost databases

which include operational cost for a broader set of com-

Need for a comprehensive assessment of operational cost mercial buildings. All these cost databases, however, do

When applying the WAPEC approach as described above it not include enough information on the building itself,

is necessary to go beyond the usually rather rough figures on which makes it practically impossible to draw a link be-

operational costs used in current valuations and come up with tween specific sustainable features of the building and its

solid forecast of future operating cost – differentiated into operational cost.

recoverable and non-recoverable cost. • Calculated cost data: Future operational cost can also be

The operational cost assessment should include at least the calculated if enough information is available on the partic-

following cost items: ular building characteristics. On the market there are avail-

• Building related facility management costs including cost for able several LCCA tools but most of them require a huge

cleaning, inspections, caretaking, management of planned amount of technical building data14. For the Austrian and

service contract etc.; German markets two Austrian real estate consultants – e7

and M.O.O.CON – have developed a LCCA tool that re-

• Utilities – energy, water, sewage; quires only a limited data set: Usually the input parameter

• Regular maintenance cost such as repairs and replacement

used for the calculation of the energy performance certifi-

of minor components; cate and a few additional information on the interior fitting

are sufficient to come up with plausible operational cost as-

• Conversion and back-fitting e.g. in case that a change of the sessments. This tool has also been applied in the case study

customers requires adaptations in the rental object; below15.

• Cost for major refurbishment: In the context of property

valuation this cost elements plays a role mainly in those

cases where a refurbishment is needed because of lacking

functionality of the old system.

14. The IMMOVALUE project has assessed existing LCCA models with respect to

their applicability for a quick and transparent calculation of operational costs of

It is obvious that the single items of operational costs depend buildings (compare IMMOVALUE report D3.2 resp. Appendix to Report D7.2, both

on specific building characteristics: Large window areas will available as downloads under www.immovalue.org).

lead to high cleaning cost, a bad energy performance will lead 15. A comprehensive description of the LCCA tool developed by e7 ad M.O.O.CON

is included in the Annex to IMMOVALUE report D7.2 “Methodologies for Integration

to high energy cost, old buildings will have higher refurbish- of Energy Performance and Life-Cycle Costing Indicators into Property Valuation

Practice” (www.immovalue.org)

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1285

Contents Keywords Authors5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

Table 3. Description of key findings.

Result of modified valuation approach: 17,150,000 €

Rental impact (nominal): Premium of 0,53 €/m² p.m.

Rental impact (percentaged): Premium of 3,74 %

Value impact (nominal): +810,000 €

Value impact (percentaged): Premium of around 5% (of which around 1,4% is direct impact

due to difference in non-recoverable OPEX)

Table 4. Key valuation parameters.

Current gross rental income: The rental income of the subject property due to current tenancy

agreements is calculated with 13.0 €/m² p.m. amounting at a current

gross rental income of 1,138,800 €/a

Non-recoverable Operating expenses: The current annual non-recoverable operating expenses (OPEX)

have been calculated by means of a full LCCA and amount at

20.5 €/m² p.a. The LCCA shows that the non-recoverable operating

expenses of the highly sustainable and energy efficient subject

property is a little bit lower than the OPEX from the comparables (-

2

2.0 €/m p.a.)

Applied yield (term): The applied yield for the term was estimated with 6.6 % and

encompasses adjustments for location, property configurations, and

risks adjustments for expected short-term difficulties in letting high

standard offices (vacancy and collection loss).

Applied revisionary yield: For the period after the expiration of the contract duration a

revisionary yield of 6.5 % was applied to addresses the positive

market expectations due to recovery of the market conditions.

Estimated rental value (ERV): On the basis of the market observation the market rent for

comparable properties ranges between 14.0 and 14.5 €/m² p.m.

Therefore an average rent of 14.2 €/m² p.m. was applied.

Vacancy rate: The current observable vacancy rate of 15 % has been addressed

within the applied yield.

Case Study – “Vienna Offices Building”: Results of the LCCA

Valuation based on a modified income related Based on the data available related to the technical character-

istics of the building a comprehensive LCCA has been con-

approach with a full life-cycle cost assessment

ducted with an integrated LCCA tool developed by e7 and

The following example shows a modified property valuation M.O.O.CON16. Since in the context of the income-related ap-

using the income related approach for an office building in proach only operational cost differences need to be calculated,

Vienna. This office building is not a standard building but it LCCA was limited to operational cost side (including capital

is a very sustainable one with a very good energy perform- repair cost) but did not include the primary construction cost.

ance. Therefore we can observe a remarkable difference in Table 6 summarises the results structured according to dif-

operational cost between the valued building (subject prop- ferent cost categories. Since LCCA usually works on the basis of

erty) and the reference group buildings (comparables). See sqm gross floor area, all results are given for this unit.

Table 3 and 4 for description of key findings and key valuation Table 7 gives the results for the differences in operational

parameters. cost between the comparables and the subject property after

recalculating the figures of Table 6 to the unit of m2 lettable area

Technical characteristics of the valued property and of which is the usual area unit for property valuation. In addition

comparables operational cost is differentiated into recoverable and non-

In order to be able to estimate the future operational cost of recoverable operational costs. For this purpose it was assumed

the subject property as well as of the comparables, it is neces- that non-recoverable cost consist of 70 % of cost for conversion

sary to know the cost-driving characteristics of these buildings. and backfitting and of 100 % of capital repair cost. All other

Table 5 gives an overview on the technical characteristics of costs were assumed to be recoverable from the tenant.

the property building and of the comparables in the given case

study.

16. A comprehensive description of the LCCA tool developed by e7 and M.O.O.CON

is included in the Annex to IMMOVALUE report D7.2 “Methodologies for Integration

of Energy Performance and Life-Cycle Costing Indicators into Property Valuation

Practice” (www.immovalue.org)

1286 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsPANEL 5: SAVING ENERGY IN BUILDINGS 5-301 Hüttler et al

Table 5: Technical characteristics of subject property and comparables.

comp

1 comp

2 comp

3 com

4 subject

roperty

lettable

area,

m² 20.000 34.000 22.000 20.000 7.300

heating,

c ooling,

ventilation

heat

production district

heating district

heating district

heating district

heating heat

pump

refrigeration vapor-‐compression

vapor-‐compression

vapor-‐c ompression

vapor-‐c ompression

vapor-‐c ompression

refrigeration refrigeration refrigeration refrigeration refrigeration

ventilation ventilation

with

ventilation

with

ventilation

with

ventilation

with

ventilation

with

preconditioning

and

preconditioning

a nd

preconditioning

a nd

preconditioning

and

preconditioning

and

air

de-‐/ humidification air

de-‐/humidification air

de-‐/humidification air

de-‐/humidification air

de-‐/humidification

heat

dissipation radiation fan

c oils radiation

heating fan

coils building

component

activation

cold

dissipation fan

c oils fan

c oils building

c omponent

fan

coils building

component

activation activation

indoor

ventilation ventilation ventilation ventilation ventilation ventilation

renewables

solar

thermal

system -‐ -‐ -‐ -‐ 300

m²

use

of

s olar

thermal

system -‐ -‐ -‐ -‐ hot

water

and

heating

support

PV -‐ -‐ -‐ -‐ 400

m²,

integrated

facade

facade

/

design

type

of

facade glass

a nd

panel

f acade perforated

facade glass

and

panel

facade

glass

and

panel

facade perforated

facade

(80%),

perforated

facade

( 20%)

window

area

s hare 70% 100% 70% 70% 31%

sun

protection none none lamellae

horizontal

none special

c onstructive

overhanging facade

( tilted

forward)

dazzle

protection sun-‐blind sun-‐blind sun-‐blind sun-‐blind sun-‐blind

daylight

control none none none none none

purifier cat

burglar cat

burglar cherry

picker cat

burglar cherry

picker

windows glass

a nd

panel

f acade aluminum

window aluminum

window

(at

glass

and

panel

facade aluminum

window

the

perforated

f acade

(20%))

glazing

thermal

insulation

thermal

i nsulation

thermal

i nsulation

thermal

i nsulation

sun

protective

glass

glass glass glass glass

g-‐value

window 0,65 0,65 0,65 0,65 0,45

u-‐values

[W/m²K]

exterior

wall 0,35 0,37 0,31 0,35 0,11

window 1,7 1,3 1,15 1,7 0,6

ceiling

against

e xterior

wall 0,2 0,24 0,21 0,2 0,09

ceiling

against

unheated

0,4 0,38 0,41 0,4 0,13

building

floor

over

a mbient

a ir -‐ 0,24 0,2 -‐ -‐

Table 6: Operational cost according to cost categories for subject property and comparables (based on a comprehensive LCCA).

Unit: €/m2a gross floor area comp 1 comp 2 comp 3 comp 4 subject

property

indoor cleaning 11,1 10,7 8,6 11,1 10,7

glass cleaning 0,1 0,1 0,1 0,1 0,1

facade cleaning 5,1 3,3 2,1 2,0 1,5

operation 1,4 1,3 1,3 1,4 1,2

maintenance 8,2 9,4 7,9 8,2 8,3

capital repair 12,4 13,6 9,8 12,3 11,3

conversion / backfitting 6,0 6,4 4,2 6,0 4,8

energy and resources 18,7 19,4 15,2 19,2 11,1

TOTAL 63,0 64,2 49,2 60,3 49,0

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1287

Contents Keywords Authors5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

Table 7: Total recoverable and non-recoverable operational costs for subject property and comparables (in €/m2a lettable are; based on a

comprehensive LCCA).

unit:

€ /m²a

lettable

a rea comp 1 comp 2 comp 3 comp 4 subjekt

property

Total recoverable 64,5 64,1 54,3 60,9 48,2

Total non-recoverable 23,0 25,1 18,9 22,9 20,5

average comparables recoverables 61,0

average comparables non-recoverables 22,5

Difference comp to subject property recoverable p.a. 12,7

Difference comp to subject property recoverable p.m. 1,1

Difference comp to subject property non-recoverable p.a. 2,0

Table 8: Summary of valuation calculation for the case study “Office Building Vienna”.

Input Parameter Term Reversion

Lettable Area 7300 m 7300 m

Current Rent 13.0 /m p.m. -

Market Rent - 14.2 /m p.m.

Rental Impact (Wrent) - +0.53 /m p.m.

Estimated Rental Value - 14.73 /m p.m.

Annual Gross Rental Income 1,138,800 1,290,348

Total non-recoverable OPEX p. a. 149,122 149,122

(difference to average non-recov.

(-14,336 )

OPEX of comparables)

Annual Net Rental Income 989,768 1,141,226

Applied yield 6.60 % 6.50 %

Average residual term of contract 3 years -

Annuity factor

(1+6.6%) 2.43

-1

2.648 -

(1+6.6%) 2.43

⋅ 6.6%

Net Rental Income

Net Present Value (Term) x 2,616,325 -3,022,508

Annuity factor

Net Present Value (Reversion) - 17,557,316

Total Net Present Value 2,616,325 + (17,557,316 – -3,022,508) = 17,151,133

Revised Market Value 17,150,000

Valuation calculation results using the modified income sitivity for operational cost differences and achieves a MAR of

related approach around 50 % due to valuers expectation based on observable

Table 8 summarises the results of the valuation calculation for market conditions and circumstances.

the case study. In a third step we combine the AAP and the MAR and calcu-

The rental impact (VPArent) as given in Table 8 above has late the weighted adjustment factor (WAFrent) as follows:

been calculated as follows:

In a first step the average adjustment factor (AAP) has WAFrent = MARrent · AAPrent · VEA = 50% · 7,48% · 100% +3.74%

been calculated by evaluating the operational cost difference

(OCSP) including only recoverable operational cost. The fol-

Based on the percentage value given in the WAF we can finally

lowing formula has been used:

calculate the absolute rental impact (VPArent):

AAPrent = OCSP =

(OC ) – (OC ) = 61,0 – 48,2 = +7,48 %

ref , i subj VPA rent = WAFrent · rmarket = 3.74% · 14.2 /m p.m. +0.53 /m p.m.

rM ·12 14.2 ·12

Conclusions from the case study

In a second step the awareness of markets for sustainability

The results of the applied modified income related approach

and energy efficiency has been evaluated by using the WAPEC

show that integration of sustainability aspects through a com-

scoring model. In our case study we assume that the property

prehensive analysis of operational cost derives a remarkable

market for office buildings in Vienna has a low to medium sen-

“green value” for a very energy-efficient and sustainable

1288 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsPANEL 5: SAVING ENERGY IN BUILDINGS 5-301 Hüttler et al

building. The higher value comes prevailingly from achievable • Activities to be implemented by the valuers’ community:

rental premiums and partly also from lower non-recoverable The adapted methods need to get well-established and ac-

OPEX. Depending on the observable sensitivity on market cepted in the valuation community. The IMMOVALUE

(MAR) the calculated value impact is between 5 and 10 % not project team has already succeeded to make a first step in

taking into account the potential additional impact of lower that direction since the results and methods developed in

vacancy rates in higher quality buildings. the project are reflected in the actual Guidance Note for

The approach is easy to handle but works only under the the integration of energy performance and LCC into EVS

precondition that the valuer can gain data on operational being prepared by the European Group of Valuers’ Asso-

cost for the subject property as well as for the comparables. If ciation (TEGoVA) which is the publisher of the European

this data is available the required LCCA can be implemented Valuation Standards (EVS). This first steps in reducing the

and delivers reliable and plausible results for the integration of uncertainty through standardisation needs to be contin-

sustainability aspects into property valuation. ued and intensified.

Besides the case study described above, the IMMOVALUE

• “PPP” to be implemented by real estate industry together

project team has assessed and calculated further 14 case stud-

with energy efficiency policy: For a broad application valu-

ies. Altogether these case studies demonstrate that the modified

ers need reliable data bases on reference buildings (com-

methodologies for all three basic valuation approaches work

parables) including not only data on building site, rent level

well. This is mainly due to the fact that they are strongly based

and building equipment etc. but also on energy efficiency

on the usual standard valuation approaches with only smaller

and different operational cost categories. This data bases

adaptations where required.

may be kicked off with policy support using the network

of certification bodies for well acknowledged sustainability

What needs to be done for a market rollout? certificates (such as LEED, DGNB, BREEAM, HQE etc.).

As a summary of this paper – which is based on the overall Since many of these certificates already reward the imple-

results from the IMMOVALUE project – we can conclude as mentation of an LCCA within their criteria sets, the certifi-

follows: cation bodies could also become a cornel for acquisition of

data on operational cost. If this data is then made available

• The value impact which is derived by using the modified - e.g. in a web-based database - valuers could use this source

valuation approaches developed for an integration of en- in their daily valuation work.

ergy efficiency and other sustainability issues must not be

neglected, but is in general limited. Only for very energy • Role for major customers of property valuation: The de-

efficient and sustainable properties the modified valu- mand for the application of adapted methods needs to in-

ation would come up with a premium of 5-10 %. Higher crease by communicating to sellers and buyers of real estate

value impacts would depend on further increased market that the integration of green value in property valuation is

sensitivity towards energy efficiency and sustainability (i.e. possible and might improve their positions. If the demand

if the markets do not only account for cost advantages but side actively asks for adapted valuation reports, the valu-

account also for better comfort levels, for better productivity ers will see an increased necessity to (better) integrate green

etc. to be achieved in sustainable buildings). value in their work. This process could be accelerated if ma-

jor public building owners would become obliged to order

• We can, however, observe an increasing interest of real es- property valuations which actively integrate sustainability

tate industry in energy efficiency and other sustainability and energy efficiency aspects.

issues leading to an increasing willingness to pay for envi-

ronmental features. There is, however, still a considerable • Dissemination and training activities supported by en-

gap between the general acknowledgement of importance ergy efficiency policy: The broader use of the adapted

and the practical application in valuation practice. At the methodologies would by itself support the market sensitiv-

moment, practically all valuation reports deal with the issue ity towards energy efficiency and sustainability. Therefore it

of “green value” only in a qualitative, descriptive way and are is necessary to disseminate the adapted valuation approach-

not able to reflect it in quantitative terms. es in the valuation community, even if the value impact is

not overwhelming at the first glance. In addition, valuers

• In valuation practice it is the lack of data that sets limits for require training which makes them capable to interpret

broad application of the modified valuation approaches. In energy benchmarks, results of LCCA and other technical

most cases data on energy efficiency, LCCA and other sus- characteristics of the building in a correct way.

tainability aspects is very vague. Although prescribed by law

energy performance certificates are still missing for many All in all we may conclude that – although in general property

valuation processes, LCCA is practically not available at all. valuation is mostly driven by market forces – there remains

some room for interventions to be set by energy efficiency

Based on these conclusions we can develop some ideas of a policy. Thus policy can play an important supporting role for a

strategy for market rollout for a (more) widespread integra- better integration of energy efficiency and other sustainability

tion of energy efficiency and other sustainability aspects in issues into property valuation and thus may contribute to an

property valuation practice. The following activities to be im- improved starting position of energy efficient and sustainable

plemented mark the corner-stones of such a strategy and re- properties on the market.

quire efforts from the side of market players as well as from

the side of energy efficiency policy:

ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society 1289

Contents Keywords Authors5-301 Hüttler et al PANEL 5: SAVING ENERGY IN BUILDINGS

References McGraw-Hill Construction (2008), Green Outlook 2009:

Amt für Wohnungswesen Darmstadt (2003), Mietspiegel Trends Driving Change, McGrawHill Publications, New

für Darmstadt 2003 – Zur Berechnung der ortsüblichen York

Vergleichsmiete für nicht preisgebundenen Wohnraum, Meins, E., Burkhard H.-P. (2009), Der Nachhaltigkeit von

Darmstadt. Immobilien einen Wert geben: ESI Immobilienbewertung

Amt für Wohnungswesen Darmstadt (2008), Mietspiegel – Nachhaltigkeit inklusive, Zürich.

für Darmstadt 2008 – Zur Berechnung der ortsüblichen Meins, E., et al. (2007), Der Nachhaltigkeit von Immobilien

Vergleichsmiete für nicht preisgebundenen Wohnraum, einen finanziellen Wert geben – Economic Sustainability

Darmstadt. Indicator (ESI), Center for Corporate Responsibility and

Bienert, S., Schützenhofer, C. and Steixner, D. (2009), Prop- Sustainability (CCRS), University of Zurich, Zürich.

erty Valuation and Energy Performance of Buildings Meins, E., et al. (2008), Der Nachhaltigkeit von Immobilien

– Approaches for integrating Energy Performance into einen finanziellen Wert geben – Minergie macht sich

Valuation Practice, Scientific Paper presented at the Pas- bezahlt, Center for Corporate Responsibility and Sustain-

siveHouse Symposium 2009, Brussels. ability (CCRS), University of Zurich, Zürich.

Bowman, R., Wills, J. (2008), Valuing Green - How green Miller, N., Spivey, J., Florance, A. (2008), Does Green Pay

buildings effect property values and getting the valua- Off?, Burnham-Morres Center of Real Estate, University

tion method right, Green Building Council of Australia, of San Diego and CoStar Group, San Diego.Muldavin, S.

Sydney. (2008), Quantifying “Green” Value: Assessing the Applica-

Eddington, C., Berman, D., Hitchcock, D., et al. (2009), Who bility of the CoStar Studies, San Rafael, California.

Pays for Green? – The Economics of Sustainable Buldings, Pitts, J., Jackson, T. (2008), Green Buildings: Valuation Issues

EMEA ResearchCBRE, London and Perspectives, in: The Appraisal Journal, Spring 2008,

Eichholtz, P., Kok, N., Quigley, J.M. (2009), Doing well by p.115-118, Chicago (Illinois).

doing good? – An analysis of the financial performance of Popescu, D, Mladin, E.C. Boazu, R. Bienert, S. (2009), “Meth-

green office buildings in the USA, RICS Research Report, odology for real estate appraisal of green value”, Environ-

March 2009, RICS, London mental Engineering and Management Journal, Vol. 8,

Fuerst, F., McAllister, P. (2008), Green Noise or Green Value? Issue 3 May/June, pp. 381-386.

Measuring the Price Effects of Environmental Certifica- RICS Valuation Standards Board (2008), Building Sustain-

tion in Commercial Buildings, University of Reading, ability into the Commercial Property Valuation Process,

2008, Reading Valuation Information Paper, No. 14, Royal Institution of

Institute for Market Transformation (2003), Recognition and Chartered Surveyors (RICS), London.

use by appraisers of energy-performance benchmarking

tools for commercial buildings, New York State Energy Re-

search and Development Authority (NYSERDA), Albany. Acknowledgement

IVSC (2007), International Valuation Standards, International The IMMOVALUE project has been carried out within the

Valuation Standards Committee (IVSC), 8th edition, European Commission’s “Intelligent Energy – Europe” Pro-

London. gramme between July 2008 and August 2010 by the following

Knispel J., Alles R. (2003), Ökologischer Mietspiegel - Em- partners: KPMG Financial Advisory Services GmbH (Austria),

pirische Untersuchung über den möglichen Zusam- e7 Energie Markt Analyse GmbH (Austria), Dr. Leopoldsberger

menhang zwischen der Höhe der Vergleichsmiete und + Partner (Germany), Technical University “Gheorghe Asachi”

der wärmetechnischen Beschaffenheit des Gebäudes, Iasi (Romania), SINTEF Stiftelsen for industriell og teknisk for-

Darmstadt. slning ved Norges tekniske høgskole (Norway) and Fachhochs-

Lorenz, D., Lützkendorf, T. (2008a), Sustainability in prop- chule Kufstein Tirol Forschungs GmbH (Austria). The authors

erty valuation: theory and practice, Journal of Property of this paper also would like to thank all the colleagues who

Investment and Finance, 2008, Vol. 26, Issue 6, p.482-521, have contributed to the IMMOVALUE project. All IMMOV-

Emerald Group Publishing Limited, Bingley (UK). ALUE reports can be downloaded under www.immovalue.org.

1290 ECEEE 2011 SUMMER STUDY • Energy efficiency first: The foundation of a low-carbon society

Contents Keywords AuthorsYou can also read