Investor presentation - April 2021 - pfandbrief.market

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor presentation April 2021

Leading lender for green

1990 and social infrastructre 4.7million

FOUNDING YEAR CLIENTS

100% subsidiary

of BayernLB

Second largest Local authorities. companies

and retail clients

onlinebank in Germany

Industry Leader in

sustainability

110 billion 77billion

BALANCE SHEET TOTAL CLIENT LOANS

One of the top 20 banks in Germany

in Germany

4.500 954 million

EMPLOYEES NET INTEREST INCOME

Target: Sustainable TechBank

Stable Development. Despite Corona crisis.

Business Results

Continued growth in lending business across Net interest income at previous year's level with

all segments of EUR 7bn EUR 954m

Significant deposit growth of EUR 11.6bn Profit before tax of 249m above expectations

The main driver of the increase in total assets Investments in transformation. digitization and

is participation in the TLTRO programme with restructuring as main cost drivers

EUR 14bn

Risk Ratios

Robust credit portfolio in the environment of the Return on equity: 7.7%

corona crisis due to focus on sectors largely

Cost-Income-Ratio: 61.2%

independent of economic cycles

Equity ratio: 11.6%

Improved risk result compared to the previous year

3 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Corona-crisis impact. Minor.

Germany Business Development

Comprehensive package of measures by the Up to 90% of employees took advantage of the home

German government and federal states to office option in 2020

combat the economic consequences of corona Support of borrowers with the help of promotional

Public authorities and development banks as loans and other tools

financiers and guarantors for many aid Stable core business

programmes

Risk management Credit risk

Operational risks limited by digital mindset and Credit Risk Task Force established to monitor and

appropriate technology and processes manage the Corona crisis

No relevant liquidity effects DKB's business almost exclusively in Germany

Equity exposure in the low three-digit range Only single customer groups affected by Corona

pandemic - including tourism

Bond exposure almost exclusively in LCR-eligible

bonds of core European issuers

4 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Covid-19. Impact scenario analysis.

Loan volume (EUR bn) Corona impact scenario

30

German Savings Banks Association

Housing (DSGV) has published a scenario

24,5 analysis regarding the impact of

Covid-19

20 Local authorities &

social infrastructure Based on economic sectors and

16,8 DSGV industry forecast

Considers supply shortfalls. the drop

Environmental

technologies

in demand and the government

10 interventions

8,9

Food & agriculture Individual clients Impact index (6 = strong impact of

3,8 Energy & supply 2.6 Other corporates

7,2 crisis. 1 = low impact)

(incl. Tourism)

1,3 “Translation” of the impact index into

0 DKB client groups

DSGV

0scale 1 2 3 4 5 6

Source: DSGV and DKB

5 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Agenda.

1 Business model

2 Facts and figures

3 Sustainability

4 Funding

5 Contact

6 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

1

Business model.

2

7 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Ownership structure. Munich. Berlin.

Free State of Bavaria Association of Bavarian Savings Banks

≈ 75 %

BayernLB Holding AG ≈ 25 %

100%

Binding letter of comfort and profit/loss transfer agreement

Real Estate &

Corporates & Markets

Savings Banks/Association

Specialized bank for future Real estate financier in Germany Innovative Tech-Bank with

sectors and chosen markets abroad sustainable focus (#geldverbesserer)

Structuring experts Central Bank of the Bavarian Strong earnings growth planned

savings banks and partner for through targeted doubling of customer

Focused financial markets offer

public business base

8 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Business model. Market leadership.

Infrastructure

48.6

Second biggest

Online Bank in

Germany Financing of services for the

public welfare

Market leader

regarding current

accounts Retail clients

13.8

Biggest renewable

energy portfolio in Projects usually with a

Germany municipal background

Corporate

Market leader in clients

14.0

agricultural

business Loan volume

=

70% of total assets

9 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Business units. Two.

26 branches

Business customers Retail clients

across

Germany Online

Infrastructure Corporate clients approach

7.2bn

8.9bn 8.7bn

24.5bn

Energy & New energies

supply 2.5bn

3.8bn Mortgage loans

16.8bn

Housing

Personal loans

2.6bn

1.3bn Food &

agriculture

Local authorities & Individual clients

social Other and other

infrastructure corporates

10 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Customer strategy. Growth. Sustainability.

8m clients until 2024

9,0

8,0

7,0

6,0 Scalability of

lending

5,0 DKB Broker business

4,0

3,0

Increase

2,0 Expansion of profitability

product range

1,0 DKB Cash

0,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

11 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Digitization. Key to success.

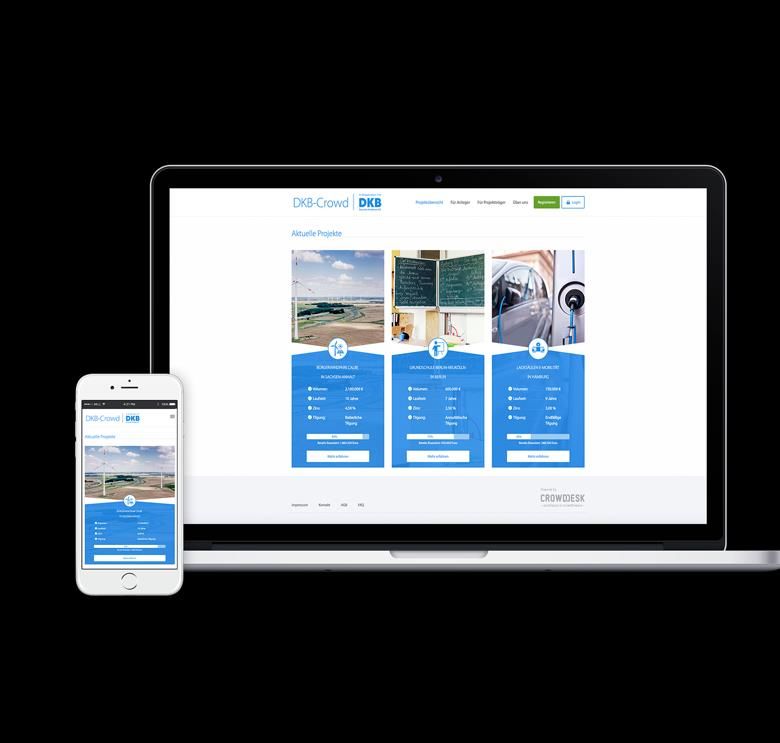

DKB Crowd

Own Fintech

Stake in municipal

funding platform

12 I Investor presentation I April 2021 I IFRS-data as of 31/12/20202 Facts & Figures. 13 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Overview.

Key figures* 2020 2019 2018 2017 2016 2015

Total assets 109.840 m 83.754 m 77.388 m 77.323 m 76.522 m 73.429 m

Customer receivables 76.557 m 69.526 m 65.933 m 64.552 m 63.228 m 61.582 m

Customer liabilities 72.409 m 60.767 m 54.366 m 53.931 m 53.438 m 48.558 m

Net interest income 954 m 954 m 945 m 935 m 795 m 790 m

Profit after tax 249 m 298 m 301 m 263 m 327 m 225 m

Cost income ratio (CIR) 61.2% 56.7% 51.5% 50.8% 45.8 % 48.0 %

Return on equity (ROE) 7.7% 9.5% 10.2% 9.6% 12.4 % 9.6 %

Equity ratio 11.6% 11.1% 11.1% 10.5% 10.0 % 9.1 %

* DKB Group in accordance with IFRS. Angaben in EUR

14 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Business performance. Positive.

Loan volume (EURbn) Customer deposits (EURbn)

+7.1 76.6

65.9 +3.6 69.5 0,2 72.4

0,2 13,8 +11.6

0,1 12,8 +6.4 60.8 4,6

12,4

14,0

54.4 3,6

13,5 4,0

13,2

49,4

40,8

35,0

43,0 48,6

40,2

2,4 2,3 2,5

13,0 14,1 15,9

2018 2019 2020 2018 2019 2020

Infrastructure Corporates Retail Other Infrastructure Corporates Retail Other

Growth was driven by all segments, especially the Exceptional growth in deposits, especially in the retail

customer groups, products: customer segment

- Local authorities & social infrastructure Slight increase in deposit volumes in the corporate

- Housing customer segment

- Mortgage Loans

15 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Earning figures. Solid.

Net interest income (EURm) Cost Income Ratio LCR

61,2% 31.12.2020 356%

56,7%

945 954 954 51,5%

31.12.2019 164%

2018 2019 2020 2018 2019 2020

Net profit after tax (EURm)

Tourismus Return on equity Leverage Ratio

10,2% 9,5% 31.12.2020 3.64%

7,7%

301 298

249

31.12.2019 3.71%

2018 2019 2020 2018 2019 2020

16 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Risk and figures. Improved.

RWAs based on SA* (EURbn) Risk result (EURm) Equity ratios (SA*)

10.8% 11.1% 11.6%

69,5 76,6 9.4% 9.3% 9.6%

65,9

- 112

31,5 33,2 33,7

- 56 - 39 9.1% 9.1% 9.1%

2018 2019 2020 2018 2019 2020 2018 2019 2020

Equity ratio

Loan book RWAs Core capital ratio (T1)

Common equity ratio (CET1)

Loan portfolio quality Non Performing Loans Capital measures

0,5%

1,1% Investmentgrade (bis BBB-)

0.9% 0.9% Equity increase of EUR 200

9,9% 0,5%

Non-Investmentgrade (bis BB-) million through capital reserve

Non-Investmentgrade (bis C) allocation by BayernLB

88,6%

Non Performing Loans 2018 2019 2020

* Standardised approach (SA)

17 I Investor presentation I April 2021 I IFRS-data as of 31/12/20203 Sustainability. 18 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Sustainability. A business model.

1996

First wind 2001 2004 2011 2018

turbine Launch of the 2014 First social bond

Establishment of EMAS- Account opening 2016

financed. online bank. DKB STIFTUNG. issued.

Certification process First green bond

becomes 100% issued.

digital.

1998 2002 2009 2015

First public- First day-care

Sustainability Industry

private centre for

management Leader with

partnership children (Kita). 2020

2000 embedded ISS-oekom for 2019

project.

First 2003 directly in the 2013 the first time. 2017

World's first blue

biogas First Board of DKB Bürger- New forms of

social bond

plant. PV plant Management. sparen work through

issuance

financed. scheme. “Projekt Arbeiten

4.0” project.

19 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Sustainability approach. Blue.

Differentiation Blue sustainability

Expansion of the concept

of sustainability Ecological + social

Sustainable Development Orientation towards people's

Goals (SDGs) as a needs

strategic foundation Positioning sustainability in the

Inclusive instead of mainstream

exclusive

20 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Sustainability goals. Ambitious.

Until 2023 Until 2030

the most convincing sustainable Become carbon neutral

product range among the top 20 in our office operations

banks

Until 2050

Until 2030 Meet the 2-degree-goal with

EUR 80bn in sustainable all DKB products

financing

Source: DKB Sustainability Strategy 2019

21 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020SDGs. Mapping.

Signi-

ficant Share of

Sub- Volume Change vs. loan Customer groups according

targets Description in € bn 2018 portfolio to Bundesbank code

Access to financial Private customers, employees,

1.4 services 10.6 bn € +4.5% 15.8% family members & others

Access to

3.8 healthcare 2.6 bn € +13.7% 3.8% Doctors, nursing & hospitals

4.1; 2; 3; Schools, kindergartens,

Access to education 0.8 bn €

77,8%

5 -16.6% 1.2% universities and inclusion

Access to clean

6.1; 3 water 0.8 bn € -3.0% 1.2% Water / sewage, waste

of our customer

7.2; 3; a; Support for Wind, solar, bioenergy, loans (EUR 54.1bn)

b renewable energies 9.9 bn € +0.5% 14.9% hydropower & energy efficiency

have a significant

Access to Public transport, communal & contribution

9.1 affordable housing 16.7 bn € +6.1% 24.8% cooperative housing

Justice & strong Municipalities, foundations, public

16.3; 6 institutions 10.6 bn € +6.5% 15.9% institutions & corporations

17.1 Improve tax levies 0.1 bn € +14.7% 0.8% Tax consultancy

Source: DKB Annual Report 2019 (Data from 31.12.19)

22 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Sustainable performance. Outstanding.

Industry Leader since 2015

Decile Rank: 1

Peergroup: Financials/ Public & Regional

Banks

Size of peer group: 277 Banks

23 I Investor presentation I April 2021 I IFRS-data as of 31/12/20204 Funding. 24 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Credit. Ratings.

Mortgage

Agency Type of rating Public Pfandbriefe Senior Unsecured

Pfandbriefe

Moody‘s Covered Bond Rating Aaa Aaa

Issuer Rating

A1

(senior preferred)

Junior Senior Unsecured

A2

(senior non-preferred)

Adjusted BCA baa1

Outlook stable

ISS-ESG Sustainability rating - - B- (Prime)

imug Sustainability rating Very positive (A) Positive (BBB) Positive (BB)

25 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Funding. Mix.

2%

4%

Primary funding source, 8%

Customer deposits diversified through all client segments

13%

Development Pass-through and global loans

banks (e.g. from KFW. EIB. Rentenbank) Liabilities**

62%

Since 2006 mainly via Pfandbriefe 11%

Capital markets

Since 2016 Green Bonds

funding Since 2018 Social Bonds

Customer deposits

Central bank operations on an opportunistic basis. Development Banks

Central Bank Participation in TLTRO III with EUR 14bn due to ECB

Capital market

attractive conditions Equity

Other

* Treasury perspective without registered bonds held by non-banks

** In relation to total assets

26 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Funding strategy. Exclusively sustainable.

Focus:

Three Green Bond issuances: Green and Social Bonds

First Senior Unsecured 16%

Green Bond in Germany (2016). Future issuances

further issuance (2017) EXCLUSIVELY in

First Green Bond complaint with 11% sustainable formats

EU Green Bond Standard and As green or social bonds

Taxonomie (2021) or new sustainable bond

formats

73%

Three Social Bond issuances: For both benchmark

First social covered bond (2018) transactions and private

Conventional issues

placements (in progress)

First Blue Social bond (2019) Social Bonds (Pfandbriefe)

First Retail Social Bond (2019) Green Bonds (Sen. Unsecured)

27 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Funding. Volume.

Placement volume (EURm) Maturity profile (EURm)

2500 2000

2000 1500

1500

1000

1000

500 500

0 0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Pfandbriefe Senior unsecured (Green Bond) Social Bond Pfandbriefe Social Bond Senior unsecured (Green Bond)

• Capital markets funding depends on deposit

growth and maturities

• New driving factor: ECB actions, in

particular TLTRO

28 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Green. Bonds.

Renewable energy portfolio: EUR 10.8bn

!

10.000

8.000

6.000

Funding

4.000

2.000

0

Wind Photovoltaik Sonstige

Green

Bonds

2016 500m EUR Senior non-preferred

2017 500m EUR Senior non-preferred

Reporting

2021 500m EUR Senior preferred new

29 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Social. Bonds.

Social Funding

infrastructure

Social

Bonds

2018 500m EUR Social Pfandbrief

2019 Retail Social Pfandbrief

Reporting

2019 500m EUR Blue Social Pfandbrief

30 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Public Pfandbrief. Cover pool. Federal

Republic of

Germany

Municipal 0.2%

service

authorities Federal States

0,0% 9,1%

Cover assets Number Volume

German federal government 6 13

German federal states 109 965 100% German assets

German cities and municipalties 5,383 7,701 High granularity (Ø-Volume: Cities and

Other cover assets 1 1 EUR 1.5m) municipalities

(GER)

90,7%

Total 5,499 8,680

Volumen in EURm

Key figures*

Aaa

Outstanding bond volume (EURm) 4,424.8

Rating over-collateralization Aa1

requirements significantly

Rating Moody's Aaa

exceeded

Over-collateralization required by

1.0%

Moody‘s Collateral score stable on

NPV over-collateralization 98%

low level

Collateral score 2.4%

Collateral Score Rating

* As of December 2020

Source: Moody’s

31 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Public Pfandbrief. Cover pool.

Overcollateralization Distribution of volumes

(EURm) (EURm)

2500

2000

1500

1000

500

0

up to 1 up to 2 up to 3 up to 4 up to 5 up to over 10

year year year year year 10 year years

In circulation Cover pool

32 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Mortgage Pfandbrief. Cover pool.

Thuringia 6%

Baden-Württtemberg 5%

Schleswig Holstein 2% Bavaria 5%

Cover assets Number Volume Saxony-Anhalt 7%

Berlin 11%

Residential loans 33,584 1,805 100% Germany Saxony 11%

Housing-industry investors 3,232 4,958 Very high granularity Saarland 0.4%

Brandenburg 11%

Other cover assets 10 410

Housing-industry investors Rhineland-Palatinate 1% Bremen 1%

Total 36,826 7,173 are mainly residential

Northrhine-Westphalia Hamburg 3%

Volume in EURm property companies 15%

Lower Saxony 5% Hesse 8%

Meckenburg Western

Pomerania 7%

Key figures* Aaa

Aa1

Outstanding bond volume (EURm) 4,283.5 Aa2

Rating Moody's Aaa Rating over-collateralization

Over-collateralization required by requirements significantly

11.5%

Moody‘s exceeded

NPV over-collateralization 66.4%

Collateral score 8.6%

Collateral Score Rating

* As of Dezember 2020

Source: Moody’s

33 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Mortgage Pfandbrief. Cover pool.

Overcollateralization Distribution of volumes

(EURm) (EURm)

2500

2000

1500

1000

500

0

up to 1 up to 2 up to 3 up to 4 up to 5 up to 1 above

year years years years years years 10

years

In circulation Cover pool

34 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020Mortgage. Cover pool.

Type Type. Details

2% 0%

1% 1%

8%

19%

71%

98%

Apartment buildings One- and two-family houses

Residential Commercial Condominiums Office building

Trade building Other (for commercial purpose)

35 I Investor presentation I April 2021 I IFRS-data as of 31/12/20205 Contact. 36 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

Personal.

Uwe Jurkschat

Head of Funding and Investor Relations

Tel.: +49 (0)30 12030-2924

E-Mail: uwe.jurkschat@dkb.de

Anna Stawowy

Funding and Investor Relations

Tel.: +49 (0)30 12030-2910

E-Mail: anna.stawowy@dkb.de

Hannes Merlecker

Funding and Investor Relations

Tel.: +49 (0)30 12030-3317

E-Mail: hannes.merlecker@dkb.de

www.dkb.de

Follow us on

@DKB_deDisclaimer The information in this presentation constitutes neither an offer nor an invitation to subscribe to or purchase securities. It does not represent a recommendation to buy, sell or hold any securities. The information in this presentation is solely intended for informational purposes and does not serve as a basis for any kind of obligation, contractual or otherwise. The presentation may not be copied in whole or in part, distributed, forwarded or sent directly or indirectly by any means to a third party without prior written consent. Statements in this presentation represent solely the opinion of Deutsche Kreditbank AG. All the information contained in this presentation has been compiled with care. However, Deutsche Kreditbank AG does not expressly or silently guarantee the accuracy, completeness or suitability of the information in this presentation for any particular purpose. Deutsche Kreditbank AG assumes no direct or indirect liability from this presentation. Furthermore, investors should bear in mind that statements concerning past performance do not indicate or represent a guarantee of future performance or returns. Deutsche Kreditbank is under no obligation to update or regularly review the information in this presentation. This presentation may be subject to legal restrictions in some jurisdictions. All persons in possession of this presentation are explicitly advised to personally inquire about any restrictions that may apply and to comply with them. The information may not be used in foreign jurisdictions without permission. 39 I Investor presentation I April 2021 I IFRS-data as of 31/12/2020

You can also read