INVESTOR PRESENTATION JUNE 2018 - Amazon AWS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

JUNE 2018 INVESTOR PRESENTATION

PLEASE READ THIS PRESENTATION

MAKES REFERENCE TO:

Forward-looking statements

This presentation contains forward-looking statements within the meaning of securities laws. The words “anticipate,” “assume,” “believe,” “pending,”

“budget,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “plan,” “project,” “will” and similar expressions are intended to identify forward-looking

statements. These statements involve known and unknown risks, which may cause SM Energy's actual results to differ materially from results expressed or

implied by the forward-looking statements. Forward-looking statements in this presentation include, among other things, expected Permian Basin

production, expectations about future cost inflation, and the expected benefits from joint venture arrangements. General risk factors include the availability

of and access to capital markets; the availability, proximity and capacity of gathering, processing and transportation facilities; the volatility and level of oil,

natural gas, and natural gas liquids prices, including any impact on the Company’s asset carrying values or reserves arising from price declines;

uncertainties inherent in projecting future rates of production or other results from drilling and completion activities; the imprecise nature of estimating oil and

natural gas reserves; uncertainties inherent in projecting future drilling and completion activities, costs or results, including from pilot tests; the uncertainty of

negotiations to result in an agreement or a completed transaction; uncertainties inherent in projecting the timing and ultimate outcome of litigation; the

uncertain nature of acquisition, divestiture, joint venture, farm down or similar efforts and the ability to complete any such transactions; the uncertain nature

of expected benefits from the actual or expected acquisition, divestiture, drilling carry, farm down or similar efforts; the availability of additional economically

attractive exploration, development, and acquisition opportunities for future growth and any necessary financings; unexpected drilling conditions and results;

unsuccessful exploration and development drilling results; the availability of drilling, completion, and operating equipment and services; the risks associated

with the Company's commodity price risk management strategy; uncertainty regarding the ultimate impact of potentially dilutive securities; and other such

matters discussed in the “Risk Factors” section of SM Energy's 2017 Annual Report on Form 10-K, as such risk factors may be updated from time to time in

the Company's other periodic reports filed with the Securities and Exchange Commission. The forward-looking statements contained herein speak as of the

date of this announcement. Although SM Energy may from time to time voluntarily update its prior forward-looking statements, it disclaims any commitment

to do so except as required by securities laws.

Non-GAAP financial measures: See Appendix for reconciliations

Non-GAAP forward looking metrics: See Appendix for definitions

2

SM ENERGY PREMIER OPERATOR OF TOP TIER ASSETS

FOCUSED ON TWO BASINS IN TEXAS

(1)

• Market capitalization: ~$3.0B

• Production: ~113 MBoe/d; 42%

oil, 41% natural gas, 17% MIDLAND BASIN

NGLs (1Q18) ▪ ~82,500 net acres

▪ 8 Rigs / 4 Frac Crews

• Proved Reserves: 468 MMBoe; EAGLE FORD

▪ ~165,000 net acres

46% proved developed (YE17) ▪ 2 Rigs / 1 Frac Crew

~35%

• Expected 2018 Capital Spend:

$1.27 billion

(1) As of May 31, 2018

3

2017-2019 DRIVING DIFFERENTIAL VALUE

OFF TO A GREAT START IN 2018

“ CASH FLOW GROWTH PER

PREMIER

OPERATOR ~35% CAGR 2017-19

DEBT ADJUSTED SHARE IS

THE METRIC WITH THE

Expected

HIGHEST CORRELATION TO

CASH FLOW

GROWTH INTRA SECTOR RELATIVE

TOP TIER PER DEBT PERFORMANCE”

ASSETS

~35%

ADJUSTED SHARE (1)

– Credit Suisse 12/11/17(2)

(1) See Appendix for Cash Flow per Debt Adjusted Share definition

(2) Betty Jiang and William Featherston, Credit Suisse

4

FIRST QUARTER 2018 HIGHLIGHTS

Cash flow growth, up 30% sequentially

• Rapid margin expansion, highest in 14 quarters

• Big Midland production growth

Operational execution: New wells outperforming expectations

• 19 new RockStar wells average 1,440 Boe/d peak

30-day IP rates (88% oil)

Significant reduction in net debt

• Non-core asset sales year-to-date reduce net debt and

core up portfolio

$792 million $1.6 billion

Non-core asset sales(1) Liquidity(2)

(1) Non-core asset sales in the Powder River Basin, North Dakota and Texas completed through May 2018

(2) As of March 31, 2018; commitment amount as of May 30, 2018

5

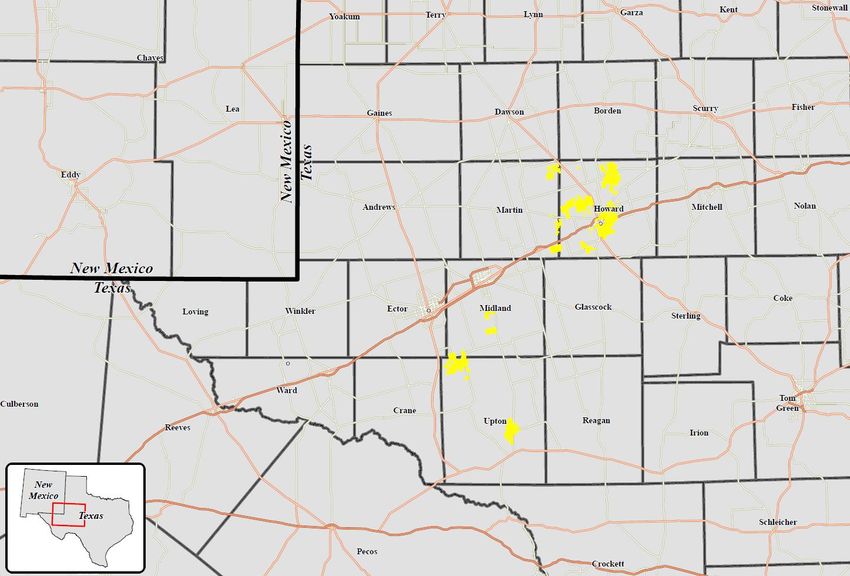

MIDLAND BASIN

EXECUTING ON OUR PLAN

Midland Basin

~82,500 net acres

• 17 net completions in 1Q18

- 15 in RockStar area

RockStar

• 8 rigs currently

• 4 frac fleets operating at high

efficiency

• ~36 net completions expected in

2Q18

Sweetie

Peck

• Focusing on co-development of

intervals

6

MIDLAND BASIN TOP WELL RESULTS

SM RANKS #1 IN REVENUE PER WELL & REVENUE PER LATERAL FOOT(1)

(1) Baird Equity Research 3/28/18 – Joseph Allman 7

2017-2019 PERMIAN HIGH RATE OF CHANGE

EXPECTED BIG PERMIAN PRODUCTION GROWTH & MARGIN EXPANSION

• Permian projected production growth up ~135% 2017-2019

• Company projected cash operating margin up over 45% 2017-2019

Production

(MBoe)

4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18e 3Q18e 4Q18e

Note: 2018 estimated Permian Basin production by quarter based on February 2018 plan, updated for Halff East divestiture.

8

ROCKSTAR NEW WELL RESULTS

GREAT RESULTS IN MULTIPLE INTERVALS ACROSS ACREAGE POSITION

NEW WELLS AVERAGE 1,440 BOE/D, 88% OIL (10,200’ LATERAL LENGTH)

Fezzik A 2443WA

Fezzik A 2444WA

30 Day Avg Peak Rate:

Guitar North 2850WA

Guitar North 2851WA 1,536 Boe/d

Guitar North 2852WA (89% oil)

Guitar North 2867WB

Guitar North 2868WB

Wiley Bob A 2351WA

30 Day Avg Peak Rate:

Wiley Bob 2352WA(1)

1,607 Boe/d

30 Day Avg Peak Rate:

(87% oil)

941 Boe/d

(90% oil)

(1) 7,708’ lateral length

Lumbergh 2547WA

Lumbergh 2548WA

Lumbergh 2565WB

30 Day Avg Peak Rate:

1,623 Boe/d

Berlinda Ann 2341WA

(85% oil) Berlinda Ann 2342WA

Berlinda Ann 2361WB

Whitaker 22-27 Unit 2251WA

Lumbergh 2527LS Whitaker 22-27 Unit 2252WA

Lumbergh 2528LS

30 Day Avg Peak Rate:

30 Day Avg Peak Rate:

1,305 Boe/d

1,485 Boe/d

(90% oil)

(87% oil)

9

ROCKSTAR NEW WELL RESULTS

NEW WELLS CONTINUE OUTPERFORMANCE TREND

300,000

250,000

Cumulative Production (BOE)

200,000

150,000

100,000

50,000

0

0 30 60 90 120 150 180 210 240 270 300 330 360

Days on Production

Previously Reported Well Avg(1) New Well Avg(2) PEER 1MMBOE

Note: Monthly data normalized to days on production; as of April 26, 2018

(1) Previously Reported Well Average includes all (36) previously reported SM operated wells on production since 11/3/2016.

(2) New Well Average includes 19 new wells that have not been previously reported.

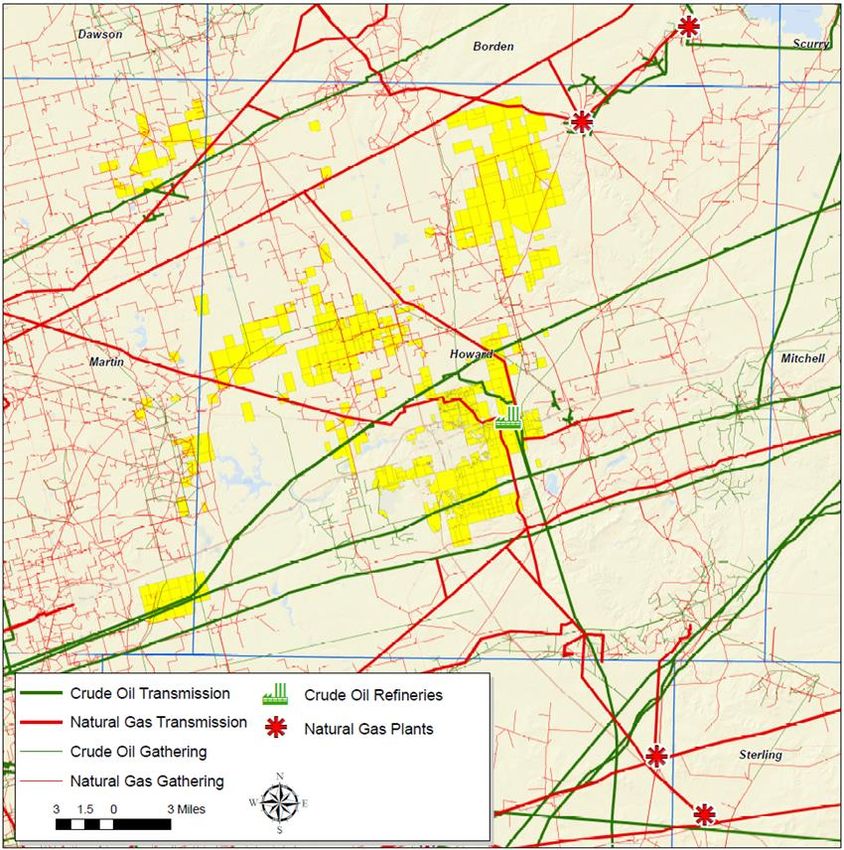

10MIDLAND BASIN INFRASTRUCTURE WATER MANAGEMENT

INVESTING $70MM IN FRESH AND PRODUCED WATER

INFRASTRUCTURE IN 2018

Currently 95%+

Midland water on pipe

Expected cost Accelerates System

savings development control

(LOE + Capital)

11MIDLAND BASIN INFRASTRUCTURE REGIONAL SAND

POSITIVE ARRANGEMENT WITH US SILICA & SANDBOX LOGISTICS

New sand mines

close to SM

operations ~55 miles(1)

>$400K ~48 miles(1)

expected capital

savings per well Lamesa (3Q18)

Crane (1Q18)

(1) Road miles

12MIDLAND BASIN INFRASTRUCTURE TAKEAWAY

MULTIPLE PURCHASERS WITH FT ASSURE RELIABLE SM TAKEAWAY

High quality WTI

Multiple purchasers

Sales at wellhead; used by TX

~90% of oil on pipe with FT; excellent

gathering is firm refineries; SM oil

relationships

37-41 gravity

Permian Basin

Oil Takeaway

13EAGLE FORD

ENHANCING VALUE OF INVENTORY

Eagle Ford

~165,000 net acres

• Up-spacing to improve returns

• Assessing new intervals

• Optimizing completions

JV Area

• Running 2 rigs and 1 frac fleet

• Expect to complete 9 net wells

in 2Q18

14BALANCE SHEET OFFERS FINANCIAL FLEXIBILITY

LIQUIDITY OF $1.6B, INCLUDING $643MM CASH ON HAND(1)

• Rapidly reducing net debt with $792MM non-core asset sales year-to-date

• Net debt:TTM Adjusted EBITDAX 3.3 times at 3/31/18; below 3.0 times projected year-end

• No bond maturities until 2021

• Senior Secured Debt:TTM Adjusted EBITDAX at 0.0 times; max ratio allowed 2.75 times

• TTM Adjusted EBITDAX:Interest at ~4.1 times; minimum ratio required 2.0 times

Debt Maturities(1)

(in millions) $1,500

Borrowing Base: $1.27B(2) $1,250

$1,000

Commitments: $1.0B(2)

$750

$500

$172.5

$562 $500 $500 $500 $250

$345 $395

$0 drawn

$0

2018 2019 2020 2021 2022 2023 2024 2025 2026

1.500%

Coupon 6.500%

6.125% 6.500% 5.000% 5.625% 6.750%

Yield to worst(3) 5.41% 5.41% 5.79% 6.26% 6.48% 6.63%

Initial call date 11/2016 11/2018 7/2017 7/2018 6/2020 9/2021

Initial call price 103.25% 103.06% 103.25% 102.50% 102.81% 103.38%

(1) As of March 31, 2018; borrowing base and commitment amount as of May 30, 2018

(2) Borrowing base updated for Divide County asset sale; commitments unchanged 15

(3) As of May 29, 2018WELL HEDGED

PERCENTAGE OF EXPECTED PRODUCTION HEDGED

Production Hedged(1) • ~80% of expected 2Q18 – 4Q18 production volumes

hedged; ~85% of oil volumes, ~65% of gas volumes

(NGLs hedged by product)

• ~75% of expected 2Q18 production volumes hedged;

80% ~75% of oil volumes, ~65% of gas volumes (NGLs

hedged by product)

• ~40% of expected 2019 production volumes hedged;

~50% oil volumes, ~25% gas volumes (NGLs hedged

by product)

Midland-Cushing Basis Swaps

• ~70% of expected 2Q18 – 4Q18 Permian oil

production covered by basis hedges at just over $1/Bbl

70%

• ~45% of expected 2019 Permian oil production

covered by basis hedges

Note: Hedging data as of May 18, 2018; all percentages calculated using mid-point of guidance.

(1) Percentage includes oil swaps and collars, natural gas swaps and collars, and NGL swaps; does not include basis swaps.

16SM ENERGY WHY INVEST IN SM?

OBJECTIVE; DELIVER LONG-TERM GROWTH IN CASH FLOW

PER DEBT ADJUSTED SHARE

• Unique opportunity to participate in competitively high rate of change in oil

production, margin expansion and cash flow growth

• Assets: SM wells ranked best in Midland Basin

• Execution: Exceptional track record; growing inventory

• Rapidly strengthening balance sheet with ample liquidity

• Returns focused: executive compensation tied to returns

25-well cube development; Pads from left to right: Ensign 772, Ensign 769, Trinidad 57, and Ensign 767

17Appendix

18Operational Detail

191Q18 REALIZATIONS BY REGION

Benchmark Pricing

NYMEX WTI Oil ($/Bbl) $62.87

NYMEX Henry Hub Gas ($/MMBtu) $3.00

Hart Composite NGL ($/Bbl) $30.87

Production Volumes Eagle Ford(1) Permian Rocky Mountain Total

Oil (MBbls) 354 3,315 592 4,262

Gas (MMcf) 18,731 5,631 861 25,222

NGL (MBbls) 1,641 5 27 1,673

MBoe 5,117 4,259 763 10,139

Revenue (in thousands)

Oil $19,583 $205,794 $35,683 $261,060

Gas 52,733 24,876 1,500 79,109

NGL 41,770 124 823 42,717

Total $114,086 $230,794 $38,006 $382,886

Expenses (in thousands)

LOE $11,321 $28,292 $10,572 $50,174

Ad Valorem 2,361 4,366 50 6,777

Transportation 45,307 197 1,396 46,900

Production Taxes 1,921 11,359 3,748 17,028

Per Unit Metrics:

Realized Oil per Bbl $55.27 $62.07 $60.27 $61.25

% of Benchmark - WTI 88% 99% 96% 97%

Realized Gas per Mcf $2.82 $4.42 $1.74 $3.14

% of Benchmark – NYMEX HH 94% 147% 58% 105%

Realized NGL per Bbl $25.45 $24.29 $30.36 $25.53

% of Benchmark – HART 82% 79% 98% 83%

Realized per Boe $22.29 $54.19 $49.84 $37.76

LOE per Boe $2.21 $6.64 $13.86 $4.95

Transportation per Boe $8.85 $0.05 $1.83 $4.63

Ad Val per Boe $0.46 $1.03 $0.07 $0.67

Production Tax - per BOE/% of Pre-Hedge

$0.38/1.7% $2.67/4.9% $4.92/9.9% $1.68/4.4%

Revenue

Production Margin per Boe $10.39 $43.80 $29.16 $25.83

Note: Totals may not sum due to rounding and other classifications

(1) Includes nominal amounts of other production and expenses from the region.

202018 PLANNED RIG ACTIVITY AND

COMPLETIONS BY MONTH

14 120

12

100

10

80

Total Net DUCs(1)

Operated Rigs

8

60

6

40

4

20

2

0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Midland Basin Eagle Ford Total Net DUCs

(1) Total Net DUCs counts remove DUCs associated with assets sold.

21NGL REALIZATIONS

• 16% increase in realized price (before hedges) from 1Q17 to 1Q18

• SM NGL price realizations are predominantly tied to Mont Belvieu, fee

based contracts

• Differential reflects NGL barrel product mix, and transportation and

fractionation fees

SM Typical NGL Bbl(1)

1Q17 2Q17 3Q17 4Q17 1Q18 13%

9%

Mt. Belvieu ($/Bbl) $26.74 $24.11 $27.55 $32.12 $30.87 42%

9%

SM Realization

$22.06 $19.71 $22.40 $26.01 $25.53 27%

($/Bbl)

% Differential to

82% 82% 81% 81% 83%

Mt. Belvieu Ethane Propane

Iso Butane Normal Butane

Natural Gasoline

(1) Includes the effects of ethane rejection

222018 ACTIVITY BY REGION

WELLS DRILLED, FLOWING COMPLETIONS, AND DUC COUNT

Wells Drilled Flowing Completions DUC Count

1st Quarter 2018 1st Quarter 2018 1st Quarter 2018

Region Gross Net Gross Net Gross Net

Permian

Sweetie Peck 3 3 4 2 8 8

RockStar 32 30 18 15 54 50

Permian total 35 33 22 17 62 58

Eagle Ford(1) 11 8 5 5 39 33

Rocky Mountain (Divide) - - - - 18 15 (2)

Subtotal Operated Wells 46 41 27 22 119 106

Non-operated Wells(3) n/a - n/a - n/a 1

Total n/a 41 n/a 22 n/a 107

(1) As of March 31, 2018, there were 4 gross JV wells drilled, 0 JV wells completed, and 8 gross JV DUC’s

(2) Expected to be sold during 2Q18

(3) Non-operated activity relates to wells located in the Permian Basin

23LEASEHOLD SUMMARY

PRO-FORMA FOR PENDING TRANSACTIONS

Net

Acres(1) 2Q Sales / Pro-forma

Region 3/31/18 Additions Net Acres

Midland Basin

RockStar 64,855 760 65,615

Sweetie Peck(2) 16,900 - 16,900

Halff East 5,420 (5,420) -

Midland Basin Total 87,175 (4,660) 82,515

Eagle Ford 164,680 - 164,680

Rocky Mountain

Divide 119,235 (119,235) -

Rocky Mountain Other(3) 186,845 - 186,845

Other Areas/Exploration 24,915 - 24,915

Total 582,850 (123,895) 458,955

(1) Includes developed and undeveloped oil and gas leasehold, fee properties, and mineral servitudes held as of March 31, 2018.

(2) Sweetie Peck acreage includes 2,450 net acres of drill-to-earn acreage.

(3) Rocky Mountain Other includes non-core Williston Basin, and other non-core acreage located in North Dakota, Montana, Wyoming, and Utah.

24Financial Detail

25OIL AND GAS DERIVATIVE POSITIONS

BY QUARTER THROUGH 2019

Midland - Cushing

Oil Swaps Oil Collars Oil Basis Swaps

Price

Volume Volume Ceiling Floor Volume Differential

Period (MBbls) $/Bbl(1) (MBbls) $/Bbl(1) $/Bbl(1) (MBbls) $/Bbl(1)

2Q’18 1,534 $49.57 1,459 $59.03 $50.00 2,392 ($1.03)

3Q’18 1,769 $49.77 1,948 $58.61 $50.00 3,018 ($1.06)

4Q’18 1,894 $49.87 2,222 $58.44 $50.00 3,327 ($1.08)

1Q’19 442 $50.70 1,865 $61.08 $49.38 1,471 ($1.27)

2Q’19 439 $50.70 1,990 $61.44 $49.66 1,546 ($1.32)

3Q’19 524 $50.70 2,079 $61.51 $48.26 3,113 ($2.75)

4Q’19 535 $50.70 2,092 $61.46 $48.25 3,132 ($2.74)

Gas Swaps Gas Collars

Volume Volume Ceiling Floor

Period (BBTU) $/MMBTU(1) (BBTU) $/MMBTU(1) $/MMBTU(1)

2Q’18 15,712 $2.85 - - -

3Q’18 17,147 $2.88 - - -

4Q’18 18,646 $2.91 - - -

1Q’19 16,979 $2.92 - - -

2Q’19 - - 4,358 $2.83 $2.50

3Q’19 - - 5,066 $2.83 $2.50

4Q’19 - - 4,818 $2.83 $2.50

Note: Includes all commodity derivative contracts for settlement at any time during the second quarter of 2018 and later periods through 2019, entered into as of 5/18/18.

(1) Prices are weighted averages; natural gas prices reflect the weighted average of regional contract positions and are no longer adjusted to a NYMEX equivalent.

26NGL DERIVATIVE SWAP POSITIONS

OPIS MT. BELVIEU

Ethane Purity Propane Iso Butane

Volume Volume Volume

(2) (2) (2)

Period (MBbls) $/Bbl Period (MBbls) $/Bbl Period (MBbls) $/Bbl

2Q’18 915 $10.87 2Q’18 554 $24.94 2Q’18 66 $35.07

3Q’18 1,033 $10.99 3Q’18 610 $24.27 3Q’18 70 $35.07

4Q’18 1,146 $11.18 4Q’18 671 $24.39 4Q’18 76 $35.07

2018 Total 3,094 2018 Total 1,835 2018 Total 212

1Q’19 853 $12.25 1Q’19 440 $26.13 1Q’19 29 $35.70

2Q’19 877 $12.29 2Q’19 348 $28.53 2Q’19 29 $35.70

3Q’19 907 $12.34 3Q’19 360 $28.53 3Q’19 30 $35.70

4Q’19 896 $12.36 4Q’19 355 $28.53 4Q’19 29 $35.70

2019 Total 3,533 2019 Total 1,503 2019 Total 117

1Q’20 275 $11.13

Natural Gasoline Normal Butane

2Q’20 264 $11.13

Volume Volume

2020 Total 539 (2) (2)

Period (MBbls) $/Bbl Period (MBbls) $/Bbl

2Q’18 175 $50.99 2Q’18 84 $35.69

3Q’18 202 $51.13 3Q’18 93 $35.70

4Q’18 208 $50.99 4Q’18 102 $35.70

2018 Total 585 2018 Total 279

1Q’19 48 $50.93 1Q’19 37 $35.64

2Q’19 49 $50.93 2Q’19 38 $35.64

3Q’19 50 $50.93 3Q’19 39 $35.64

4Q’19 50 $50.93 4Q’19 39 $35.64

2019 Total 197 2019 Total 153

(1) Includes all commodity derivative contracts for settlement at any time during the second quarter of 2018 and later periods, entered into as of May 18, 2018.

(2) Weighted-Average Contract Price

271ST QUARTER 2018

SOLID EXECUTION

Production & Pricing 1Q18

Total Production (MMBoe/MBoe/d) 10.1/112.7

Oil Percentage 42%

Pre-Hedge Realized Price ($/Boe) $37.76

Post-Hedge Realized Price ($/Boe) $35.34

$210.2 MM

Adjusted EBITDAX(1)

Costs $/Boe

LOE $4.95

Ad Valorem $0.67

Transportation $4.63

$168.7 MM

Production Taxes $1.68 Discretionary

Production Expenses $11.93 Cash Flow (1)

Cash Production Margin (pre-hedge) $25.83 30% increase

G&A – Cash $2.33 (over 4Q17)

G&A – Non Cash $0.40

Operating Margin (pre-hedge) $23.10

DD&A $12.87

(1) See Appendix for reconciliation of non-GAAP measures

28TOTAL CAPITAL SPEND

RECONCILIATION TO COSTS INCURRED (GAAP)

Reconciliation of costs incurred in oil and gas

activities (GAAP) to total capital spend Three Months Ended

(Non-GAAP)(1) (in millions) March 31, 2018

Costs incurred in oil and gas activities (GAAP): $372.2

Asset retirement obligation (0.9)

Capitalized interest (4.5)

Total capital spend (Non-GAAP): $366.7

Note: Amounts may not calculate due to rounding

(1) The non-GAAP measure of total capital spend is presented because management believes it provides useful information to investors for analysis of

SM Energy's fundamental business on a recurring basis. In addition, management believes that total capital spend is widely used by professional

research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and

production industry, and many investors use the published research of industry research analysts in making investment decisions. Total capital spend

should not be considered in isolation or as a substitute for Costs Incurred or other capital spending measures prepared under GAAP. The total capital

spend amounts presented may not be comparable to similarly titled measures of other companies.

29ADJUSTED EBITDAX RECONCILIATION

Reconciliation of net income (GAAP) and net cash provided by operating Three Months Ended

activities (GAAP) to adjusted EBITDAX (non-GAAP): (in thousands) March 31, 2018

Net income (GAAP) $317,401

Interest expense 43,085

Interest income (849)

Income tax expense 98,991

Depletion, depreciation, amortization, and asset retirement obligation liability accretion 130,473

Exploration(1) 12,411

Abandonment and impairment of unproved properties 5,625

Stock-based compensation expense 5,412

Net derivative loss 7,529

Derivative settlement loss (24,528)

Net gain on divestiture activity (385,369)

Other 7

Adjusted EBITDAX (Non-GAAP) $210,188

Interest expense (43,085)

Interest income 849

Income tax expense (98,991)

Exploration(1) (12,411)

Amortization of debt discount and deferred financing costs 3,866

Deferred income taxes 98,366

Other, net (2,534)

Changes in current assets and liabilities (16,113)

Net cash provided by operating activities (GAAP) $140,135

Adjusted EBITDAX represents net income (loss) before interest expense, interest income, income taxes, depletion, depreciation, amortization and asset retirement obligation liability accretion expense, exploration expense, property abandonment and

impairment expense, non-cash stock-based compensation expense, derivative gains and losses net of settlements, gains and losses on divestitures, gains and losses on extinguishment of debt, and certain other items. Adjusted EBITDAX excludes

certain items that we believe affect the comparability of operating results and can exclude items that are generally one-time in nature or whose timing and/or amount cannot be reasonably estimated. Adjusted EBITDAX is a non-GAAP measure that we

present because we believe it provides useful additional information to investors and analysts, as a performance measure, for analysis of our ability to internally generate funds for exploration, development, acquisitions, and to service debt. We are also

subject to financial covenants under our Credit Agreement based on adjusted EBITDAX ratios. In addition, adjusted EBITDAX is widely used by professional research analysts and others in the valuation, comparison, and investment recommendations

of companies in the oil and gas exploration and production industry, and many investors use the published research of industry research analysts in making investment decisions. Adjusted EBITDAX should not be considered in isolation or as a

substitute for net income (loss), income (loss) from operations, net cash provided by operating activities, or other profitability or liquidity measures prepared under GAAP. Because adjusted EBITDAX excludes some, but not all items that affect net

income (loss) and may vary among companies, the adjusted EBITDAX amounts presented may not be comparable to similar metrics of other companies. Our credit facility provides a material source of liquidity for us. Under the terms of our Credit

Agreement, if we failed to comply with the covenants that establish a maximum permitted ratio of senior secured debt to adjusted EBITDAX and a minimum permitted ratio of adjusted EBITDAX to interest, we would be in default, an event that would

prevent us from borrowing under our credit facility and would therefore materially limit our sources of liquidity. In additi on, if we are in default under our credit facility and are unable to obtain a waiver of that default from our lenders, lenders under that

facility and under the indentures governing our outstanding Senior Notes and Senior Convertible Notes would be entitled to exercise all of their remedies for default.

(1) Stock-based compensation expense is a component of exploration expense and general and administrative expense on the statements of operations. Therefore, the exploration line items shown

in the reconciliation above will vary from the amount shown on the statements of operations for the component of stock-based compensation expense recorded to exploration expense.

30ADJUSTED NET INCOME RECONCILIATION

Reconciliation of net income (GAAP) to adjusted net income Three Months Ended

(non-GAAP): (in thousands, except per share data) March 31, 2018

Net income (GAAP) $317,401

Net derivative loss 7,529

Derivative settlement loss (24,528)

Net gain on divestiture activity (385,369)

Abandonment and impairment of unproved properties 5,625

Other, net 807

Tax effect of adjustments(1) 86,710

Adjusted net income (Non-GAAP) $8,175

Diluted net income per common share (GAAP) $2.81

Net derivative loss 0.07

Derivative settlement loss (0.22)

Net gain on divestiture activity (3.41)

Abandonment and impairment of unproved properties 0.05

Other, net 0.01

Tax effect of adjustments(1) 0.76

Adjusted net income per diluted common share (Non-GAAP) $0.07

Diluted weighted-average common shares outstanding (GAAP): 112,879

Note: Amounts may not calculate due to rounding

Adjusted net income excludes certain items that the Company believes affect the comparability of operating results. Items excluded generally are non-recurring items or are items whose

timing and/or amount cannot be reasonably estimated. These items include non-cash and other adjustments, such as derivative gains and losses net of settlements, impairments, net (gain)

loss on divestiture activity, materials inventory loss, and gains or losses on extinguishment of debt. The non-GAAP measure of adjusted net income (loss) is presented because management

believes it provides useful additional information to investors for analysis of SM Energy's fundamental business on a recurring basis. In addition, management believes that adjusted net

income (loss) is widely used by professional research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and

production industry, and many investors use the published research of industry research analysts in making investment decisions. Adjusted net income (loss) should not be considered in

isolation or as a substitute for net income (loss), income (loss) from operations, cash provided by operating activities, or other income, profitability, cash flow, or liquidity measures prepared

under GAAP. Since adjusted net income (loss) excludes some, but not all, items that affect net income (loss) and may vary among companies, the adjusted net income (loss) amounts

presented may not be comparable to similarly titled measures of other companies.

(1) The tax effect of adjustments is calculated using a tax rate of 21.9%, for the three-month period ended March 31, 2018. This rate approximates the Company's

statutory tax rate adjusted for ordinary permanent differences.

31DISCRETIONARY CASH FLOW

RECONCILIATION TO NET CASH PROVIDED

BY OPERATING ACTIVITIES (GAAP)

Reconciliation of net cash provided by operating activities Three Months

(GAAP) to discretionary cash flow (Non-GAAP)(1) Ended

(in millions) March 31, 2018

Net cash provided by operating activities (GAAP): $140.1

Changes in current assets and liabilities 16.1

Exploration(2)(3) 12.4

Discretionary cash flow (Non-GAAP): $168.7

Note: Amounts may not calculate due to rounding

(1) Discretionary cash flow is defined as net cash provided by operating activities excluding changes in assets and liabilities, and exploration (included in

our capital spend guidance). Discretionary cash flow is widely accepted as a financial indicator of an oil and gas company’s ability to generate cash

which is used to internally fund exploration and development activities, pay dividends, and service debt. Discretionary cash flow is presented because

management believes it provides useful information to investors when comparing our cash flows with the cash flows of other companies that use the

full cost method of accounting for oil and gas producing activities, or have different financing and capital structures or tax rates. Discretionary cash

flow is not a measure of financial performance under GAAP and should not be considered as an alternative to cash flows from operating activities, as

defined by GAAP, or as a measure of liquidity, or an alternative to net income.

(2) Exploration expense is added back in the calculation of discretionary cash flow because for peer comparison purposes, this number is included in our

reported total capital spend.

(3) Stock-based compensation expense is a component of exploration expense and general and administrative expense on the statements of operations.

Therefore, the exploration line items shown in the reconciliation above will vary from the amount shown on the statements of operations for the

component of stock-based compensation expense recorded to exploration expense.

32Inventory and Returns

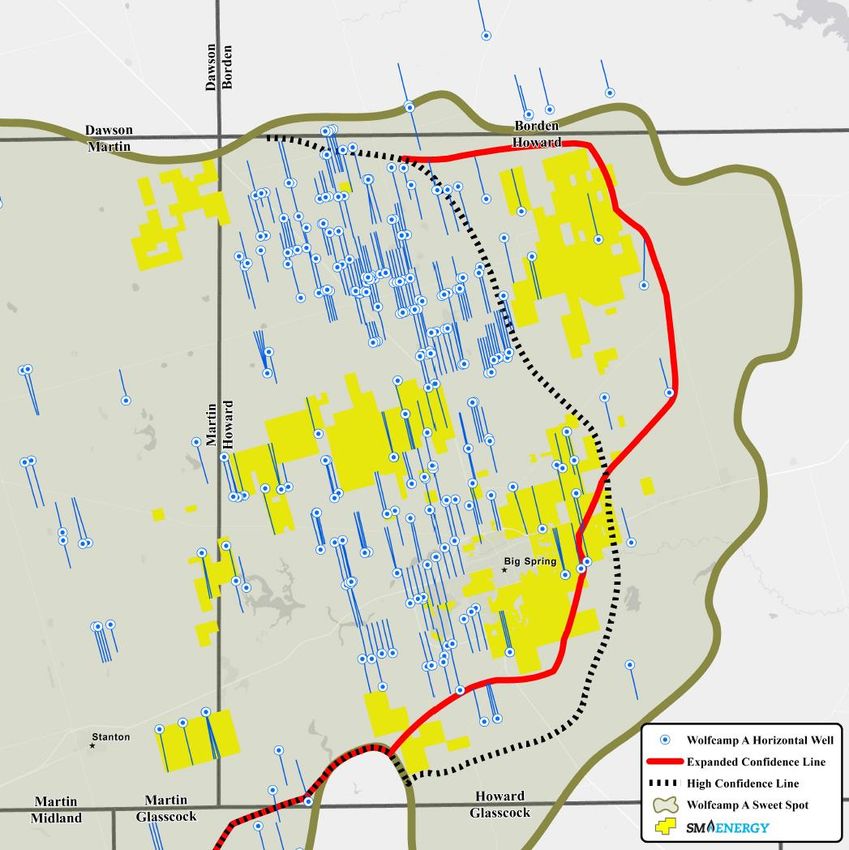

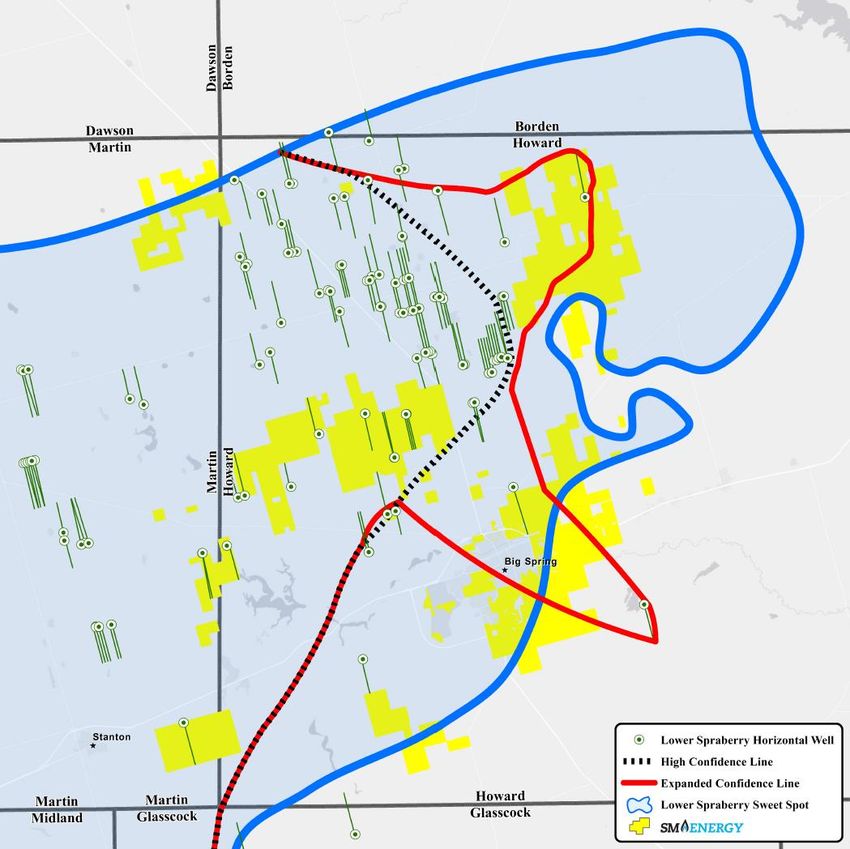

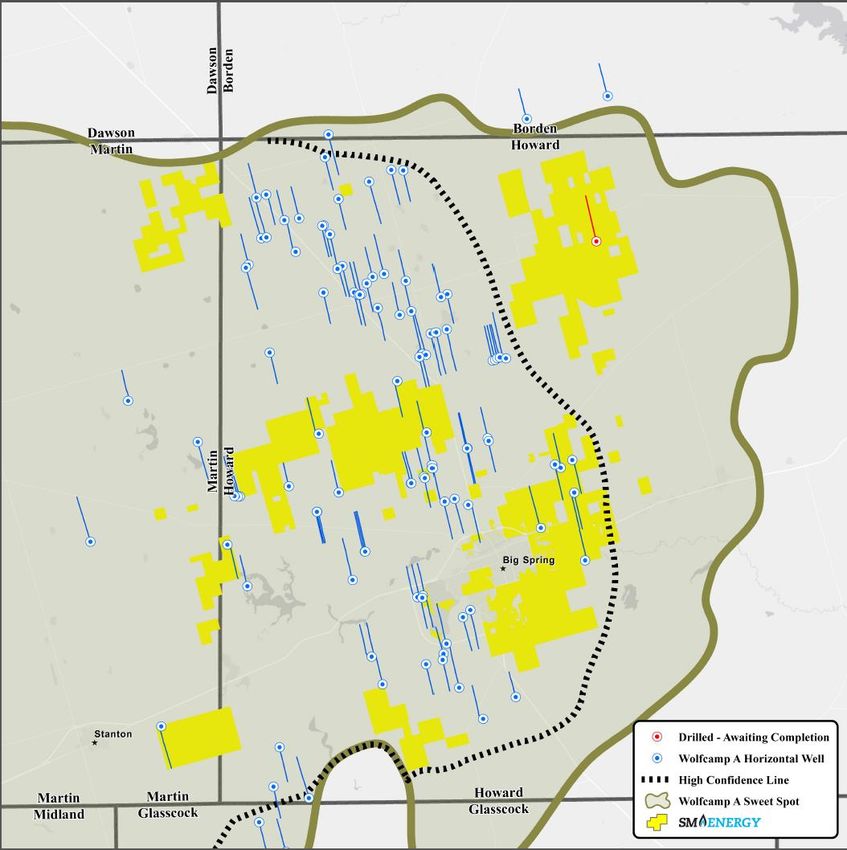

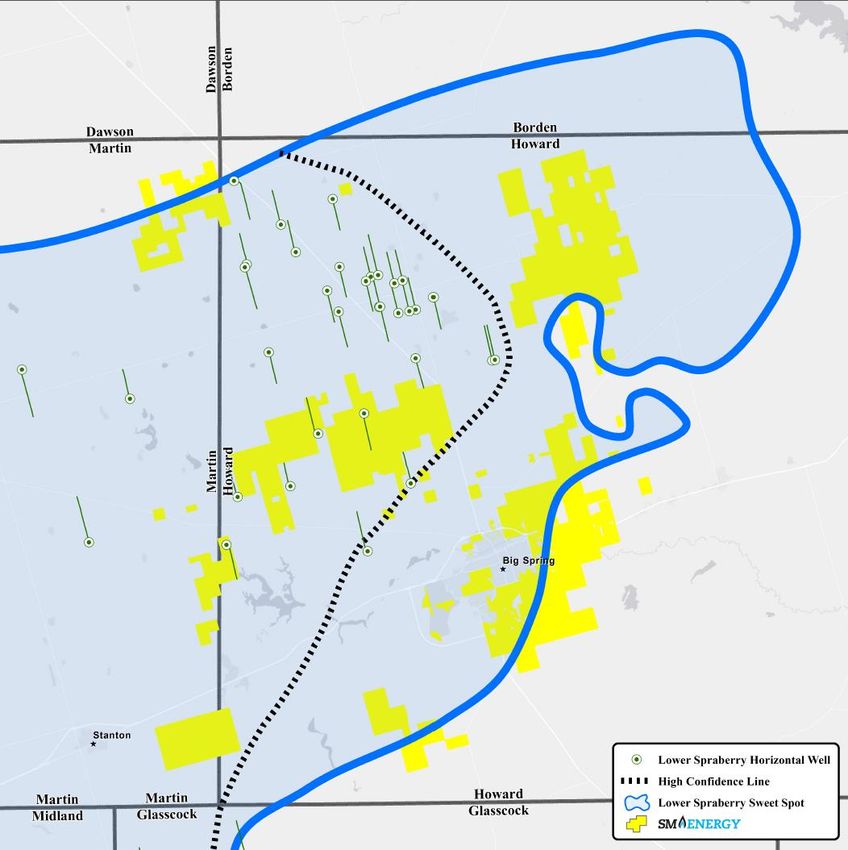

33HOWARD COUNTY WOLFCAMP A

EVOLUTION OF SM SWEET SPOT MAPPING

January 2017 February 2018

Higginbotham Unit B 30-19 1AH Cassidy 26-23 1H

Tall City – 6,397’ Tall City – 7,314’

Hyden 47-38 WA 1H 24hrIP = 403 BOEPD

24hrIP = 398 BOEPD

Grenadier – 9,639’

24hrIP = 848 BOEPD Viper 14-9 1WA

SM – 10,422’

24hrIP = 1,316 BOEPD

Oldham Trust 40-25 WA 1H

Grenadier – 10,426’

24hrIP = 1,274 BOEPD

Thumper 14-23 1AH

Sabalo – 10,105’

24hrIP = 1,357 BOEPD

Midland 15-10 1WA

Hannathon – 7,726’

24hrIP = 1,259 BOEPD

Broughton Wise 18-19 WA 1H

Grenadier – 7,012’

24hrIP = 875 BOEPD

Morgan Ranch 38-47 1WA

Hannathon – 7,727’

24hrIP = 713 BOEPD

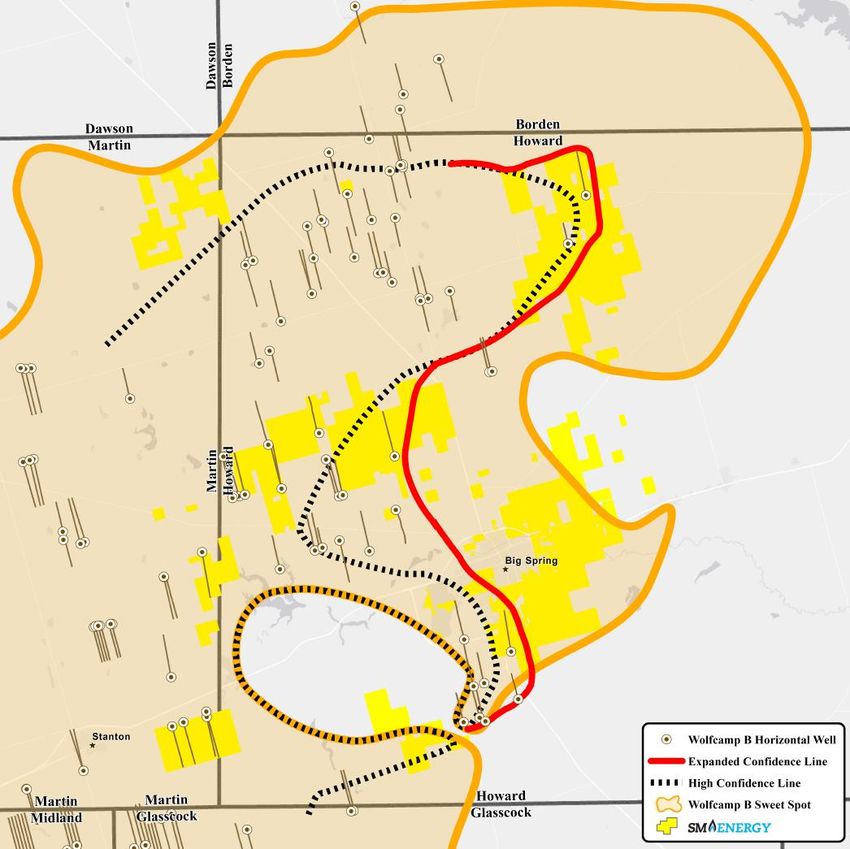

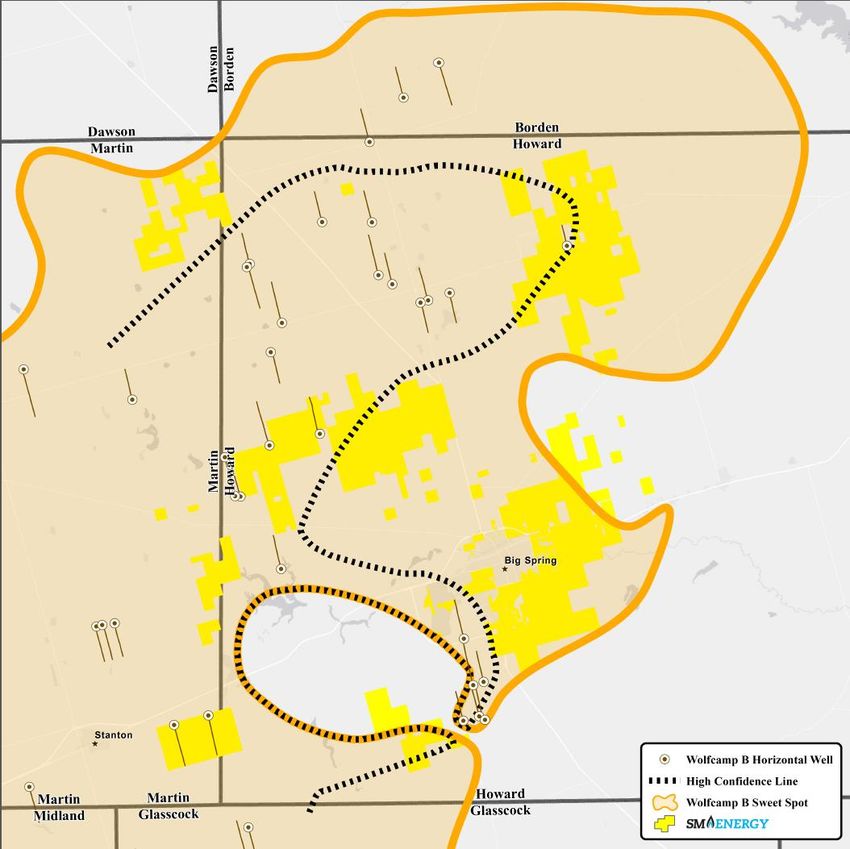

34HOWARD COUNTY WOLFCAMP B

EVOLUTION OF SM SWEET SPOT MAPPING

January 2017 February 2018

Sundown 4566WB

SM – 10,336’

24hrIP = 1,435 BOEPD

Prichard J 10BH

Legacy – 7,644’

24hrIP = 602 BOEPD

Maverick 0361WB

SM – 10,412’

24hrIP = 1,683 BOEPD Prichard J 9BH

Legacy – 7,641’

24hrIP = 655 BOEPD

International Unit 9H

Callon – 7,579’

24hrIP = 887 BOEPD

Fletch C 1368WB

SM – 10,287’

24hrIP = 1,700 BOEPD

Tubb 1WA

Crownquest – 9,873’

24hrIP = 1,178 BOEPD

35HOWARD COUNTY LOWER SPRABERRY

EVOLUTION OF SM SWEET SPOT MAPPING

January 2017 February 2018

Sundown 4524 LS

Moby Dick 31-30 8SH

SM – 10,352’

Surge – 7,362’

24hrIP = 959 BOEPD

24hrIP = 319 BOEPD

Mr. Phillips 11-2 1SH

Sabalo – 10,047’

24hrIP = 1,032 BOEPD

Papagiorgio 33-40 B1LS

SM – 10,370’

24hrIP = 1,006 BOEPD

Allar LS

Hannathon – 7,580’

24hrIP = 1,135 BOEPD

36MIDLAND BASIN DRILLING INVENTORY

INCREASING INVENTORY AND NPV PER SECTION

4,000

3,500

Average Lateral Average Working

3,000 Length Interest

9,600’ 72%

Drilling Locations

(gross operated)

2,500

2,000

(up 13% from 2016) (up 10% from 2016)

1,500 Economic lateral feet 10% IRR threshold

increased economic locations:

1,000

17% 1,640(2)

~1,250

500

(from 2016) (comparable to peers)

0

(1)

Economic Resource Additional Resource

(1) Economic Resource represents 3P inventory within the confirmed contours and 20% IRR at $60/Bbl oil, $3/MMBtu natural gas, $30/Bbl NGLs

(2) 3P inventory inside and outside the confirmed contours; 10% IRR

37DRILLING INVENTORY

~15 YEARS AT CURRENT ACTIVITY LEVEL

APPROXIMATELY 45 YEARS INCLUDING UPSIDE RESOURCES

Midland Basin and Eagle Ford

6,000

5,000

Drilling Locations

4,000

(gross operated)

3,000

2,000

1,000

0

Economic Resource(1) Additional Resource

Note: Eagle Ford 2017 average lateral length = 9,000’; up 18% from 2016

(1) Economic Resource represents 3P inventory within the confirmed contours for Howard and Martin Counties and 20% IRR at $60/Bbl oil,

$3/MMBtu natural gas, $30/Bbl NGLs

38TOP TIER ASSETS REGIONAL WELL PROJECTED ECONOMICS

RockStar Sweetie Peck

Wells(1) across all intervals (WCA, WCB, LS) in the 2018 drilling program Wells(1) across all intervals (WCA, WCB, LS) in the 2018 drilling program

120% 100%

100%

80%

80%

60%

IRR

IRR

60%

40%

40%

20% 20%

0% 0%

$50 $55 $60 $65 $50 $55 $60 $65

NYMEX WTI NYMEX WTI

Well Cost: $8.3MM Well Spacing: 513’ – 660’ Well Cost: $7.5MM Well Spacing: 660’

Sand loading: 1,900 lbs/ft; Stage Spacing: 167’; Length: 10,000’ Sand loading: 1,900 lbs/ft; Stage Spacing: 167’; Length: 8,333’

Eagle Ford

Wells(1) across UEF/LEF in East, South and North Area in the 2018 drilling program

60%

50%

40%

IRR

30%

1Q18 Average

20%

Mt. Belvieu ($/Gal)

10%

0%

$0.60 $0.70 $0.80

Mt. Belvieu $/Gal

Well Cost: $6.8MM, Lateral Length: 8,800’, Well Spacing: 625’-900’, Sand Loading: 2,000 lbs/ft, Stage Spacing: 150’

Note: well costs include drill, complete, and equip; sensitivities at $3.00/MMBtu NYMEX; Eagle Ford oil flat at $60/Bbl WTI, excludes JV wells

(1) Weighted average by interval 39Maps

40ROCKSTAR OPERATORS

SM Energy

Callon

Encana

Surge/Yantai Xinchao

Diamondback

Oxy

Energen

Endeavor

Sabalo

Grenadier

Note: Peer acreage obtained from 1Derrick

41SWEETIE PECK OPERATORS

SM Energy

Apache

Chevron

Concho

Devon

Diamondback

Discovery

Endeavor

Exxon

Legacy

Oxy

Pioneer

Summit

Note: Peer acreage obtained from 1Derrick

42EAGLE FORD OPERATORS

Dimmit

Maverick

Dimmit

Webb

Area

North

Fasken

Area

East

Area

South

43DEFINITIONS OF NON-GAAP,

FORWARD LOOKING METRICS

The following metrics are forward-looking non-GAAP financial measures. The Company believes these measures are commonly

used in the E&P industry, and other industries, by shareholders, professional research analysts and others in valuation,

comparison and investment recommendations. Certain forward-looking metrics cannot be presented in conjunction with a

reconciliation to the closest GAAP measure, because certain portions of the forecast calculation would are inherently

unpredictable. Accordingly, investors are cautioned not to place undue reliance on these numbers.

1) Projected cash flow per debt adjusted share:

For purposes of forward-looking cash flow from operations, it is not possible to project changes in working capital. The Company calculates

forward-looking cash flow as projected adjusted EBITDAX (reconciled above to GAAP Net Loss and GAAP Net cash provided by operating

activities for actual results) less projected cash interest expense and cash taxes.

The calculation of debt adjusted shares is the sum of average fully diluted common shares outstanding plus the quotient of total principal value

of long-term debt outstanding (including senior notes, convertible stock, credit facility) less cash and cash equivalents divided by the price of

common stock. In the case of the current 2-year plan, the price of common stock used is the closing price at year-end 2017.

2) Capital spend:

For purposes of forward-looking capital spend, it is the sum of projected capital expenditures for drilling and completion of wells, capitalized

geologic and geophysical work, exploration costs excluding dry hole expenses, facilities and infrastructure, allocated overhead and land costs

exclusive of acquisitions.

Capital spend as reported for actual results is reconciled above to GAAP costs incurred in oil and gas activities.

3) Net debt:EBITDAX:

Net debt is total principle value of long-term debt outstanding less cash and cash equivalents. Projected net debt:EBITDAX is projected net debt

divided by projected adjusted EBITDAX. Adjusted EBITDAX is reconciled above to GAAP Net Loss and GAAP Net cash provided by operating

activities for actual results.

4) Discretionary cash flow

Discretionary cash flow is defined as net cash provided by operating activities excluding changes in assets and liabilities, and exploration

(included in our capital spend guidance).

44CONTACT INFORMATION

Jennifer Martin Samuels

Vice President - Investor Relations

303-864-2507

jsamuels@sm-energy.com

45You can also read