Key Investor Debates Likely to Drive Stocks in the Coming Year - Morgan Stanley

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

January

January 19,19,2018

2018 05:09

05:01 AM AM

GMTGMT

MORGAN STANLEY & CO. LLC

Global Big Debates - 2018 Morgan Stanley Research

EQUITY ANALYST

erteam@morganstanley.com

Key Investor Debates Likely to

Drive Stocks in the Coming Year

Our objective as a Department is to help you, our clients, generate alpha. Today

we publish our 2018 edition of Global Big Debates, in which we highlight the

debates that we believe will shape industries and drive stocks this year. We focus

on debates that are most relevant to investors, that are likely to be settled (or

significantly advanced) in the coming twelve months, or where we have a view

that differs meaningfully from consensus.

This report leverages our edge as a Department – world-class talent, a global

perspective, and a collaborative culture, flexed across a global footprint of over

3200 stocks and dovetailed with first-class economic and strategy insight. In a

MIFID2 world, there will rightly be little value placed on maintenance research –

we will continue to focus on generating single-stock alpha, long-tailed thematic

work cross region, sector and asset class, and further increase our investment in

quantitative research and data.

As always, I welcome your feedback, and thank you for your partnership.

Simon Bound

Global Director of Research

Morgan Stanley does and seeks to do business with

companies covered in Morgan Stanley Research. As a

result, investors should be aware that the firm may have a

conflict of interest that could affect the objectivity of

Morgan Stanley Research. Investors should consider

Morgan Stanley Research as only a single factor in making

their investment decision.

For analyst certification and other important disclosures,

refer to the Disclosure Section, located at the end of this

report.

+= Analysts employed by non-U.S. affiliates are not registered with

FINRA, may not be associated persons of the member and may not

be subject to NASD/NYSE restrictions on communications with a

subject company, public appearances and trading securities held by

a research analyst account.

1

Big Debates: 2018

North America

Autos & Shared Mobility - Auto 2.0 Carve-Outs to Drive Cycle Re-Rating?

Consumer Products - Is US HPC Weakness Temporary, or Secular?

Healthcare / Internet - Amazon's Disruption of Healthcare…What's the Method of

Entry?

Payments and Processing - Is Bitcoin Posing a Threat to Visa, MasterCard?

Semiconductors - Who Will See the Greatest Opportunities in Semiconductor Machine

Vision?

Software - Which Software Companies Will Make Money from Machine Learning?

Telecom Services - Will Bottom-Fishing Be Rewarded in 2018?

Asia / Pacific

EM Equity Strategy - Is it time to rotate out of Tech Hardware/Semis and into later-cycle

plays, like Energy?

Asia ex-Japan Economics - Can the improvement in debt-disinflation dynamics be

sustained?

China Economics - Will there be a growth slump amid policy tightening?

India Equity Strategy - Are Indian stocks too rich to own?

China Financials - Will an economic slowdown pressure bank valuations again?

Europe

Internet - Will Facebook Marketplace Impact European Classifieds?

Leisure - Will US Hotel RevPAR weaken or accelerate in 2018?

MedTech - Turning bearish on hearing aids

Metals & Mining - Structurally higher return on capital in the aluminium industry on

supply side rationalisation

Retail - Will 2018 be the year that H&M (finally) de-rates?

Utilities - Two Stocks that Could Double in 2018

Japan

Japan Economics - Revival of Nominal Growth: Why it Matters for Japan

Japan Internet & Media - Who is most & least threatened in Japan's EC market from

Amazon?

Pharma - Do the major pipeline events in 2018 spell turning points for many companies?

Sumitomo Mitsui FG - Stronger shareholder returns a potential catalyst in light of

finalized Basel rules

Latin America

Latin America Food & Beverage - FEMSA Capital Deployment: Risk or Opportunity?

Latin America Real Estate - Are Malls in Latam Insulated from the Internet?

Latin America TMT - Will AMX's Outperformance Continue?

2

Contributors

Morgan Stanley & Co. LLC

Thomas Allen, Equity Analyst

+1 212 761-3356 / Thomas.Allen@morganstanley.com

Steve Beuchaw, Equity Analyst

+1 212 761-6672 / Steve.Beuchaw@morganstanley.com

James Faucette, Equity Analyst

+1 212 296-5771 / James.Faucette@morganstanley.com

Colin Fitzgerald, Research Associate

+1 212 296-8052 / Colin.Fitzgerald@morganstanley.com

Simon Flannery, Equity Analyst

+1 212 761-6432 / Simon.Flannery@morganstanley.com

Ricky Goldwasser, Equity Analyst

+1 212 761-4097 / Ricky.Goldwasser@morganstanley.com

Adam Jonas, Equity Analyst

+1 212 761-1726 / Adam.Jonas@morganstanley.com

David Lewis, Equity Analyst

+1 415 576-2324 / David.R.Lewis@morganstanley.com

Cesar Medina, Equity Analyst

+1 212 761-4911 / Cesar.Medina@morganstanley.com

Dara Mohsenian, Equity Analyst

+1 212 761-6575 / Dara.Mohsenian@morganstanley.com

Joseph Moore, Equity Analyst

+1 212 761-7516 / Joseph.Moore@morganstanley.com

Brian Nowak, Equity Analyst

+1 212 761-3365 / Brian.Nowak@morganstanley.com

Rafael Shin , Equity Analyst

+1 212 761-0328 / Rafael.Shin@morganstanley.com

Keith Weiss, Equity Analyst

+1 212 761-4149 / Keith.Weiss@morganstanley.com

3

Morgan Stanley Asia Limited+

Chetan Ahya, Economist

+852 2239-7812 / Chetan.Ahya@morganstanley.com

John Cai, Research Associate

+852 2239-1885 / John.Cai@morganstanley.com

Zhipeng Cai, Economist

+852 2239-7820 / Zhipeng.Cai@morganstanley.com

Jonathan Garner, Equity Strategist

+852 2848-7288 / Jonathan.Garner@morganstanley.com

Julie Hou, Research Associate

+852 2239-1830 / Julie.Hou@morganstanley.com

Derrick Kam, Economist

+852 2239-7826 / Derrick.Kam@morganstanley.com

Lu Lu, Equity Analyst

+852 2239-1568 / Lu.Lu@MorganStanley.com

Robin Xing, Economist

+852 2848-6511 / Robin.Xing@morganstanley.com

Richard Xu, Equity Analyst

+852 2848-6729 / Richard.Xu@morganstanley.com

Jenny Zheng, Economist

+852 3963-4015 / Jenny.L.Zheng@morganstanley.com

Morgan Stanley India Company Limited+

Ridham Desai, Equity Analyst

+91 22 6118-2222 / Ridham.Desai@morganstanley.com

Sheela Rathi, Equity Analyst

+91 22 6118-2224 / Sheela.Rathi@morganstanley.com

Morgan Stanley & Co. International plc+

Miriam Adisa, Equity Analyst

+44 20 7677-8626 / Miriam.Adisa@morganstanley.com

Nicholas Ashworth, Equity Analyst

+44 20 7425-7770 / Nicholas.Ashworth@morganstanley.com

Amy Curry, Equity Analyst

+44 20 7425-6623 / Amy.Curry@morganstanley.com

4

Carolina Dores, Equity Analyst

+44 20 7677-7167 / Carolina.Dores@morganstanley.com

Andrea Ferraz, Equity Analyst

+44 20 7425-7242 / Andrea.Ferraz@MorganStanley.com

Alain Gabriel, Equity Analyst

+44 20 7425-8959 / Alain.Gabriel@MorganStanley.com

Alex Gibson, Equity Analyst

+44 20 7425-4107 / Alex.Gibson@morganstanley.com

Michael Jungling, Equity Analyst

+44 20 7425-5975 / Michael.Jungling@morganstanley.com

Jamie Rollo, Equity Analyst

+44 20 7425-3281 / Jamie.Rollo@morganstanley.com

Geoff Ruddell, Equity Analyst

+44 20 7425-8954 / Geoff.Ruddell@morganstanley.com

Menno Sanderse, Equity Analyst

+44 20 7425-6148 / Menno.Sanderse@morganstanley.com

Morgan Stanley MUFG Securities Co., Ltd.+

Ai Furukawa, Equity Analyst

+81 3 6836-5461 / Ai.Furukawa@morganstanleymufg.com

Yuki Maeda, Equity Analyst

+81 3 6836-8417 / Yuki.Maeda@morganstanleymufg.com

Shinichiro Muraoka, Equity Analyst

+81 3 6836-5424 / Shinichiro.Muraoka@morganstanleymufg.com

Mia Nagasaka, Equity Analyst

+81 3 6836-8406 / Mia.Nagasaka@morganstanleymufg.com

Shohei Oda, Equity Analyst

+81 3 6836-8443 / Shohei.Oda@morganstanleymufg.com

Shoki Omori, Research Associate

+81 3 6836-5466 / Shoki.Omori@morganstanleymufg.com

Tetsuro Tsusaka, Equity Analyst

+81 3 6836-8412 / Tetsuro.Tsusaka@morganstanleymufg.com

Takeshi Yamaguchi, Economist

+81 3 6836-5404 / Takeshi.Yamaguchi@morganstanleymufg.com

Morgan Stanley C.T.V.M. S.A.+

5

Jorel Guilloty, Equity Analyst

+55 11 3048-9620 / Jorel.Guilloty@morganstanley.com

Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V.+

Nikolaj Lippmann, Equity Analyst

+52 55 5282-6778 / Nikolaj.Lippmann@morganstanley.com

6

US: Autos & Shared Mobility

Auto 2.0 Carve-Outs to Drive Cycle Re-Rating?

Morgan Stanley & Co. LLC Adam Jonas

Adam.Jonas@morganstanley.com

Our View Market View

We believe numerous industry actions in 2018 will lead to substantial We think the market still views past carve-outs as occasional one-offs,

reratings across the autos space. As we enter year 9 of the longest mostly concentrated in the US. Traditional, fundamental drivers are of more

uninterrupted auto credit cycle on record, OEMs and suppliers will find it hard focus to investors and they are underestimating the ability of these trends to

to push earnings much higher, leaving them to get creative on expanding the have a substantial impact on stock prices through reratings.

multiple. We expect strategic actions including potential sub-IPO carve-outs

to be a dominant auto theme for 2018.

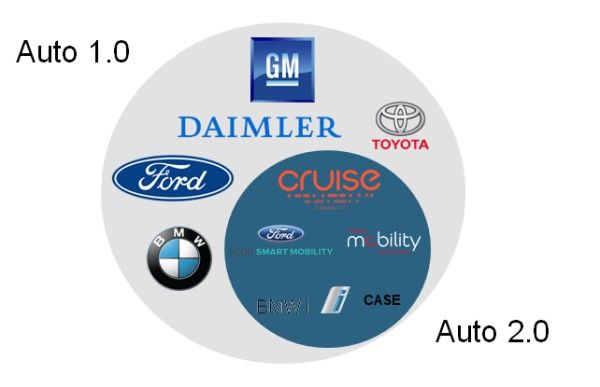

Exhibit 1: Carve-Out City Rationale behind the carve-out thesis: A collision of

unprecedented secular, technological, and regulatory forces has

grabbed the attention of investors and senior leadership teams

across the auto industry. The window of opportunity to reassess

and restructure the business portfolio appears open and under

serious consideration with a number of important precedent

transactions and other precursors having taken place in 2017. We

expect the theme to amplify materially in 2018. The theme of IPO

carve-outs has quickly moved from an issue of tail risk to one of

the single most discussed topics amongst investors today. There is

room to be excited, but there is also room to be skeptical.

We share high-level thoughts on why we expect strategic carve-

Source: Company Websites, Morgan Stanley Research

out activity across OEMs and suppliers to be a key theme:

The auto credit cycle is getting long in the tooth, in our view. As the cycle turns,

auto company financial flexibility and access to capital could be impaired. Autos are

deeply cyclical, and we’re entering year 8 of one the deepest cycles we have

witnessed – uncharted territory on most measures of used cars and auto credit. We

expect a downturn by 2019/2020 so sharp that it necessitates a policy response to

provide a floor around 15mm SAAR. For more on our views on where we stand on

the US auto cycle and US auto credit cycle, see our June 8, 2017 report: Not Cheap

Enough: Lowering US Auto Sales Forecasts, Estimates, and Targets Across the Group.

A chance for Auto 1.0 firms to steal the thunder before potentially important tech

firm entries/IPOs focus on their backyard. OEMs and suppliers have a window into

the venture capital community and, in many cases, have been investing directly in or

partnering with a a variety of Auto 2.0 start-ups. Through these interactions and

partnerships, many of which are quite well developed, we believe the auto

leadership teams have developed a high awareness of the differences in skill sets,

7

access to human talent, and access to financial capital. For more on our views of

the relationship between Silicon Valley and Detroit, please see our March 18, 2014

report: Hyperloop Needed… from Detroit to Silicon Valley, our July 15, 2015 report:

The Mobility Skunkworks Carve-Out? Or our March 15, 2016 report: Update: Motown

Valley: Can GM and Ford Adapt to Shared Autonomous Tech Threat?

The ‘Dyson effect.’ We anticipate more signs of competitive encroachment from

consumer electronics firms (e.g. Dyson) and tech firms (e.g. Apple). In our opinion,

the auto industry presents itself as ripe for redefinition as an electro-driving, mobile

supercomputing ecosystem where firms unfamiliar to the legacy industry can have

significant competitive advantage. The multi-trillion dollar industry size is of such a

magnitude that the multi-hundred-billion market cap club cannot afford to ignore.

For more on Apple in the auto industry see our June 14, 2017 report: Apple, Inc. &

Tesla Motors Inc.: Partners or Competitors? For more on Dyson, see our September

27, 2017 report: Will Dyson Take the Air Out of Tesla's Tires?

The importance of the Model 3 ramp-up as a catalyst. Tesla still faces the

challenge of becoming a self-financing, self-sustaining, profitable organization but

we do expect the Model 3 to be a highly successful car. We believe Auto 1.0

companies will be facing difficult questions about their commercial response and

strategy, particularly as they navigate aligning resources to pursue a future in Auto

2.0 while also providing a landing zone for Auto 1.0. It is our working assumption

that the Model 3 ramp will be successful and may materially change investor

perceptions. For more on Tesla’s Model 3 ramp-up, see our September 26, 2017

report: Tesla Motors Inc.: Prepare for a Big Jump in Teslas on the Road.

The clock is ticking on used car obsolescence. Auto companies are telling investors

and consumers alike that their cars on sale in 3 to 5 years should experience an

unprecedented improvement in propulsion tech, efficiency, connectivity, safety and

automation. This begs the question: Why would one buy a car now? Why not…

wait? For further thoughts on the concept of a 'buyers' strike’ for autos, see our

June 2, 2017 report: Uh Oh... US SAAR Feeling the Osborne Effect? Unintended

Consequences for the Auto Cycle. For more details of our thesis on used car

obsolescence, see our July 18, 2017 video Hyperchat: Video | That Used Car Smell:

Technological Obsolescence is a $2 Trillion Challenge.

Investment significance: While high points of the cycle can bring exciting capital markets

developments and moments of demand pull-forward, we increasingly see OEMs and

suppliers as being in a vulnerable position and reiterate our Cautious view on US Autos

& Shared Mobility. We have UW ratings on 12 out of 25 names under our coverage. FCA

remains our only OW-rated OEM in our coverage with a €16 price target. We rate GM

EW with a $43 base case while our $56 bull case is underpinned by a SOTP valuation

driven by a break-up/Auto 2.0 carve-out scenario.

Our views vs. the prevailing market views.

1. Timing. We expect further industry actions to be imminent. 2018 may be a very

active year for catalysts. The market is more in the ‘one-off’ camp.

2. Breadth. We view "Carve-out city" as potentially a global phenomenon…

particularly in Asia. The market is more focused on US catalysts.

3. Motivation. We believe carve-outs occupy strategic significance at C-level and

8

Board level to attract capital, talent and partnerships – to help learn how to be a

small company again. Our sense is that the market sees this as short-term

opportunism and ‘me too’ category.

4. Stock Impact. We expect ‘carve-out city’ to potentially have a bigger impact on

stock prices than even auto credit/cycle. We have seen re-ratings happening and

have studied them. The market may still be focusing more on fundamental drivers

such as unit volume and residual values.

Exhibit 2: Redefining Value Added in Auto 2.0 ($MM)/Employee

Source: Company Websites, Morgan Stanley Research

A review of the precedents. Auto 2.0 carve-out activity drove material re-ratings

several times in 2017. Delphi’s strong share-price performance in 2017 coincided with

the announcement and execution of its break-up and IPO spin-off into two companies,

Aptiv and Delphi Technologies. Aptiv’s mission is focused on the hardware expertise of

advanced electric vehicles and the software capabilities of automated driving while

Delphi Technologies is more focused on extending the useful life of advanced internal

combustion technology. Investors applauded the disaggregation of the businesses into

two distinct units to help focus resources on their respective end markets while opening

up new strategic opportunities. Last summer, Autoliv shares (covered by Victoria Greer)

saw a material re-rating after it announced plans to separate its active

safety/autonomous driving unit. GM’s stock experienced a material positive inflection as

management began to educate investors on the opportunities inherent within its sum-

of-parts, highlighting the commercial opportunities for Cruise Automation as a

potentially separate entity. FCA’s strong performance in 2017 coincided with increased

market appreciation and management acknowledgement of the ability of key business

units such as Magneti Marelli, and potentially Jeep and Maserati/Alfa Romeo to exist on

its own from under the parent company.

9

Exhibit 3: We believe strategic events across the autos space motivated GM to present Cruise as a

"company-within-a-company"

Source: Morgan Stanley Research, Company Websites

During GM’s recent capital markets day, the entirety of the content presented to

investors revolved around its company-within-a-company Cruise Automation. GM and

its OEM and supplier counterparts are aware of Tesla’s $60bn valuation while burning

billions of cash. They’re aware of Mobileye’s $15.3bn takeout valuation with only 750

employees. They’re also aware of Nio’s (of China) $5bn post-money private valuation

pre-revenues. If GM can assemble even a modest collection of assets, tech, partnerships

and platforms, the market may be prepared to pay many billions for a business that

may otherwise be largely ignored. We also note that GM’s 2nd generation Cruise vehicle

does not have a Chevrolet branding, but it has a pronounced Cruise logo on the sides of

the car. When asked by an analyst if brands matter in this type of network, GM

President Dan Ammann said it was ‘too early for us to have that discussion.’ We found

this very interesting.

Potential Catalysts

Announcements of further spins and carve-outs

FCA investor day in 1H18 - potential strategic action announcements involving

Maserati, Magnetti Marelli, or Jeep

ALV electronics spinoff finalized in 3Q18

This piece was originally published on December 15, 2017; all data are as of that date.

10US: Consumer Products

Is US HPC Weakness Temporary, or Secular?

Morgan Stanley & Co. LLC Dara Mohsenian

Dara.Mohsenian@morganstanley.com

Our View Market View

This is a secular trend driven by two factors. Over the last few quarters US The market consensus view and our covered companies explanation are the

organic sales growth has slowed significantly across household products that the US weakness is more temporary in nature, with numerous short-

companies (HPC). Our view is that this is more a secular trend than a term negative factors cited to justify the slowdown (including unfavorable

temporary issue, driven by longer-term factors, such as brand demand weather, delay in tax refunds in Q1, higher gas prices, Hispanic consumer

fragmentation and competitive pricing with retailer pressure and malaise post elections, and inventory retailer cuts). At the beginning of 2017,

P&G/Colgate increasing promotions to regain market share. Our in-depth many of our covered companies indicated the US weakness was mainly

analysis (below) quantifies these two secular factors, which we believe are temporary due to some discrete factors, as highlighted above. With

the key drivers of the US weakness: (1) brand demand fragmentation, with companies starting to provide 2018 guidance, we believe many of them will

consumers shifting away from large global brands towards smaller local increasingly incorporate secularly slower US topline growth into their

brands; and (2) pricing pressure, with increasing spending from P&G/Colgate messaging, and that there will be a change in tone, with companies

to regain market share, and with pressure from retailers "fighting for survival", acknowledging the pressure points are more structural vs. temporary.

as Amazon and discounters (Aldi/Lidl) gain traction in the US. We run through

these factors in detail in the following section.

Over the last few quarters we have seen a pronounced slowdown in US organic sales

growth across large cap CPG companies, which we expect to continue in the remainder

of the year. US organic sales growth slowed significantly in 2017TD, with the weighted

average organic sales growth for a key set of companies in the US/North America

declining -0.3%, far below the average of +1.7% in CY16 and +1.2% in 2015 (Exhibit 1).

Exhibit 4: US Organic Sales Growth For Large Cap Companies Has Slowed in 2017TD

Source: Company data, Morgan Stanley Research. It includes PG (US), CL (NA), CHD (Consumer Domestic), CLX (ex- International), UL (NA), and RB (NA).

At the beginning of calendar year 2017, many of our covered companies indicated the US

weakness was mainly temporary due to some discreet factors, including bad weather,

11delay in tax refunds in Q1, higher gas prices, Hispanic consumer malaise post elections,

and inventory retailer cuts. We generally disagreed with our companies explanation of

the slowdown and attributed the US weakness to longer-term secular challenges

including brand demand fragmentation as well as pricing pressure, with increasing

spending given P&G's / Colgate's refocus on market share, and with retailers focusing

more on sharpening pricing to drive foot traffic, to face the competition from Amazon

and the lower-priced German discounters (Lidl/Aldi), as we highlighted in our 06/21 note

(here). As we approach Q4 EPS, with companies starting to provide 2018 guidance, we

believe "fess up" time regarding secularly slower US topline growth is coming for our

companies, as US topline pressure will likely linger into 2018. Below we quantify what

we believe are the two key drivers of the US weakness: (1) brand demand fragmentation,

and (2) pricing pressure.

(1) Brand Demand Fragmentation

We performed a market share analysis using US scanner data to gauge the performance

of large brands across the key categories we track within HPC sector. To select the

largest brands within each category, we used the following criteria: (1) The top number

of brands in each category in order to reach at least 50% aggregate market share; (2) A

maximum of five brands per category. Based on our definition in certain very

concentrated categories we looked at only the top brand (e.g. Gillette in razor blades),

while for extremely fragmented categories (such as cosmetics or shampoo) we looked at

the top five brands.

As shown in the chart below, our analysis highlights how large brands are losing market

share across HPC categories, as demand fragmentation is accelerating with larger brands

suffering from consumers demanding more variety (partially enabled by technology)

and being less willing to pay up for premium branded CPG products. The weighted

average market share of the top brands in the twenty key HPC categories we track

declined by -51 bps YTD in 2017, much worse than +5 bps of market share gains in 2016

and +35 bps of market share gains in 2015. We believe the driver of this phenomenon is

demand fragmentation across categories, which we estimate is responsible for ~50% of

the share loss of large brands, as well as the share gains of private label, responsible for

~50% of the large brands share loss.

Exhibit 5: Large Brands Are Losing Share Across HPC Categories

Source: Nielsen xAOC + C, Morgan Stanley Research

(2) Pricing Pressure

On a reported basis, our HPC companies that break out US pricing

12(Colgate/Clorox/Church & Dwight) have experienced yoy pricing declines for the last

seven quarters. Noticeably, trends have been weakening significantly in 2017, with an

average pricing decline of -2.6% in the first three quarters of 2017 vs. -1.2% in 2016. With

greater competitive pressure in HPC from PG and to a lesser extent Colgate, aggressive

expansion by the lower-priced Lidl and Aldi retailers in the US, and Amazon increasingly

encroaching on traditional retailers, we expect this pricing pressure to continue.

Exhibit 6: US Pricing Has Slowed Significantly in 2017TD

Source: Company data, Morgan Stanley Research

Within this difficult environment, we believe Colgate, Constellation Brands, and Estee

Lauder are the most insulated names from a US slowdown given their more attractive

category (high-end beer for STZ, prestige beauty for EL, oral care for CL) and geographic

skews (high emerging markets exposure at CL). The most at risk names include EW-rated

Procter & Gamble and Clorox, as well as UW-rated Church & Dwight, given their heavy

profit skew to the US and to challenged household products categories.

This piece was originally published on December 15, 2017; all data are as of that date.

13US: Healthcare / Internet

Amazon's Disruption of Healthcare Is a Foregone Conclusion, but

What's the Method of Entry?

Morgan Stanley & Co. LLC Ricky Goldwasser Brian Nowak

Ricky.Goldwasser@morganstanley.com Brian.Nowak@morganstanley.com

David R. Lewis Steve Beuchaw

David.R.Lewis@morganstanley.com Steve.Beuchaw@morganstanley.com

Our View Market View

Our Amazon disruption framework has 4 phases, with retail pharmacy as the Investor opinions vary, with some skeptical that Amazon will enter the drug

most compelling opportunity (Exhibit 7; see our Insight note). Large profit supply chain at all, and others expecting a PBM acquisition or partnership to

pools, low barriers to entry and strategic benefits make pharmacy a natural access the mail order pharmacy market.

starting point. We estimate a $52bn profit pool here, with limited regulatory

requirements and capex. Should Amazon use Whole Foods as a launch pad, The market expects Amazon to enter the drug supply chain within verticals.

it could: (1) drive Prime subscriptions via 55mn+ pharmacy customers; (2) Our conversations with industry participants and investors usually point to

improve returns on its Whole Foods investment; and (3) expand Prime Now. the healthcare system's complexity as a barrier to entry, thinking of the

opportunity through the lens of existing business models.

Pharmacy 2.0. Amazon could leverage Whole Foods' physical retail footprint

combined with an integrated mobile offering and Prime now network to Whole Foods' 466 locations are subscale relative to established pharmacy

create a "hybrid pharmacy" (Exhibit 8). Traditional players' real estate footprint chains like CVS (~9,700 locations) or Walgreens' (~8,100), which have ~48%

may act as an Achilles’ heel. If Amazon can leverage PrimeNow (now in 31 market share combined. Accordingly, Amazon's offering will not be able to

US cities / 18 states) to scale its offering without the same footprint, gain meaningful share.

incumbents may have to rethink their strategies.

Amazon will likely acquire a PBM to enter the mail order market. A

Partnership makes more sense than M&A for Amazon in mail order. Mail partnership / acquisition of an existing pharmacy benefit manager (PBM)

order is ~11% of total US scripts and has declined in usage over the last would give Amazon access to long-existing commercial client contracts that

decade as consumer preference has shifted toward interaction with require members to use their PBM mail order pharmacy. As an example,

pharmacists.Whole Foods, Amazon's largest acquisition, at $14bn and came Express Scripts requires that patients use one of its 4 mail order pharmacies

only after 7 years of attempts to enter grocery organically. We do not see vs. the 66,000 in the open retail network. This partnership strategy is most

M&A as likely given Express Scripts (the smallest pubic PBM), has an consistent with Amazon's current business model.

enterprise value of ~$45bn.

In the Life Science Tools and Dental industries, distribution-related

AMZN is already accessing leading Dentsply dental consumables products businesses appear exposed to Amazon in more low-touch commoditized

and has integrations to 50+ practice management systems, granting them a product categories. Across our coverage of Life Science Tools, Dental

way into dental offices. We see downside for margins and multiples from distributors (Henry Schein and Patterson) are most at-risk, given their

increasing competition in what has historically been a profitable oligopoly. historically low price transparency/price increases and relatively high

This is a risk for Patterson/Schein on price/mix, but not for Dentsply/Danaher. margins for distribution businesses. However, the market believes AMZN

lacks key manufacturer products and distributor's practice management

The "clear and present danger" to Medical Devices is overstated. We only see software keeps AMZN at bay.

limited Amazon inroads. Entry through logistics is likely the first step.

Manufacturing may be a second step, commodity-focused, and potentially Amazon's entry into healthcare could be a danger to medical device

years away. We caution that significant barriers for OEMs exist, even for companies. Amazon can disrupt the medical device market through price in

supplies with moderate complexity. the distribution channel and produce commoditized supplies products as a

device OEM.

14We see retail pharmacy as a compelling business proposition for Amazon on three

distinct levels. It is a $52 billion profit pool that parlays nicely with the company's

strategy, giving them: (1) direct access to a large and growing customer base (80% of all

Rx dispensed); (2) an avenue to drive Prime membership growth; and (3) an opportunity

to increase foot traffic at Whole Foods stores. With the highest profits and lowest

barriers to entry, retail pharmacy plays to Amazon's strengths.

Exhibit 7: Opportunities Exist Across the Pharmacy Supply Chain - Retail Pharmacy and Generics

Are the Largest and Most At-Risk Profit Pools

Source: Morgan Stanley Research

Bricks & Clicks – the tech-enabled pharmacy model. With low barriers to entry and

armed with its technological prowess and Prime network, Amazon can to create a new

hybrid pharmacy model, blending its physical retail footprint with an integrated mobile

offering. We envision a world where Whole Foods stores house traditional pharmacies,

consumers' phones become part of the pharmacy real estate, Prime Now delivers

prescriptions to consumer's doorsteps, and telemedicine transports the pharmacist into

a patient's home. This technology already exists - Amazon could adopt and scale these

models by leveraging its existing infrastructure.

15Exhibit 8: The Future of Pharmacy

Source: Morgan Stanley Research, Company data

Potential impact on stocks. Price transparency and lower copays could reduce profits

by ~10% at CVS and Walgreens in 2019, and lead companies to rethink strategies to stay

competitive, as we have already begun to see with the CVS/Aetna announcement.

Exhibit 9: Companies at Risk – MS Estimates

Price Change PE Pre AMZN News On 10/6 Current Change in PE EPS At Risk As a % of Total Earnings

Since AMZN Near-to Near-to mid

Company Threat 2018 2019 2018 2019 2018 2018 mid term Long-term term Long-term

CVS Health -12.8% 13.0x 12.0x 11.3x 10.5x -1.7x -1.5x $0.76 $1.30 11.2% 19.3%

Walgreens Boots Alliance -8.7% 14.3x 13.2x 13.1x 12.1x -1.2x -1.1x $0.60 $0.60 10.2% 10.2%

Drug Retail Avg. -10.7% 13.6x 12.6x 12.2x 11.3x -1.5x -1.3x 10.7% 14.8%

Express Scripts -4.4% 8.2x 7.2x 7.8x 6.9x -0.4x -0.3x $0.00 $1.11 0.0% 12.5%

PBM Avg. -4.4% 8.2x 7.2x 7.8x 6.9x -0.4x -0.3x 0.0% 12.5%

Mckesson -5.9% 12.4x 12.0x 11.7x 11.3x -0.7x -0.7x $1.11 $1.57 8.6% 12.2%

Cardinal Health -16.7% 12.6x 12.5x 10.5x 10.4x -2.1x -2.1x $1.19 $1.39 21.9% 25.6%

AmerisourceBergen -3.4% 13.6x 12.4x 13.2x 12.0x -0.5x -0.4x $0.00 $0.33 0.0% 4.8%

Drug Distributor Avg. -8.7% 12.9x 12.3x 11.8x 11.2x -1.1x -1.1x 10.2% 14.2%

Source: Morgan Stanley Research, Thomson, Company data;

Note: Price Change as of 10/6/2017

Potential Catalysts

A sign post to watch would be Amazon obtaining a license to operate a pharmacy

and starting a pilot in a Whole Foods location.

This piece was originally published on December 15, 2017; all data are as of that date.

16US: Payments and Processing

Is Bitcoin Posing a Threat to Centralized Digital Payment

Solutions (i.e. Visa, MasterCard)?

Morgan Stanley & Co. LLC James Faucette

James.Faucette@morganstanley.com

Our View Market View

The higher structural costs associated with decentralization of a scaled Bitcoin poses a threat to the status quo. The remarkable appreciation in the

payments ecosystem are likely to offset any benefits of security and speed. value of Bitcoin has legitimized the notion that widespread adoption of

Centralized digital payment players can use AI to closely approximate the Bitcoin is likely to happen with time, and better clarity on the regulatory

security benefits while use of blockchain technology within centralized environment will eventually increase investments in Bitcoin payment

ecosystems can help improve speed of transactions where warranted (e.g. applications that could threaten the existing payments ecosystem.

cross-border payments).

Bitcoin's exponential rise in valuation is supporting the

perception of widespread adoption

Bitcoin has been highly topical this past year and as of December 8, the value of a

Bitcoin had soared to ~$16,000, up 1400% YTD and rising 134% in the last month. This

latest wave of value appreciation is being attributed to increasing interest from hedge

funds with supposedly hundreds of millions or perhaps even billions of dollars in

commitment being put into crypto assets by such institutions. At current valuation, all

Bitcoins in circulation add up to an aggregate value of $280bn with ~1000 individuals

owning ~40% of the market, according to a Bloomberg article. Whether or not the

currency is worth what it is trading at is hard to determine given its limited role thus far

in "real" value creation, lack of any fundamental valuation tools, and appreciation that's

not easily attributable to conventional drivers. Nonetheless, the remarkable

appreciation and increasing involvement of institutional money seems to be lending

Bitcoin (and some other crypto currencies) a legitimacy of sorts and supporting the

perception that it could become a widely adopted payments tool in the long run.

We see some value in Decentralization...

Bitcoin is based on a decentralized/distributed ledger, which means that 1) no one entity

controls it and 2) there is no central/concentrated infrastructure to run it. In theory this

has several advantages: (i) Trust:A decentralized system makes it challenging for

participants to collude with one another in order to profit at the expense of others. (ii)

Security: A decentralized/distributed system would be harder to attack or manipulate

given a much higher number of nodes than the typical centralized systems. (iii)

17Efficiency: Ability to participate with unknown parties in theory should remove the need

for intermediaries and lower the cost of transactions. (iv) High network up-times: No

centralized infrastructure reduces the potential for system-wide failures

...But centralized systems for consumer payments are highly

efficient, with formidable cost advantages

Visa and MasterCard run two of the largest centralized consumer payment rails and

offer many (and more) of the same benefits, in our view.

1) Low transaction costs: Given the high fixed cost infrastructure invested upfront, the

per transaction cost of sending money via Visa and MasterCard rails is formidably low

and continues to go down over time.

2) Low incidence of fraud: Visa and MasterCard utilize transaction-based risk scoring

and rule-based technology platforms that offer real-time decisioning tools for fraud

detection and monitoring. By analyzing a wide range of factors like purchasing behavior,

location of purchases, anomaly detection, reputation scoring, and IP address detection,

they are able to quickly determine the chance that an attempted purchase is fraudulent.

There is a wide range of flags that would likely cause a transaction to be denied (e.g.

change in location, shipping address different from billing address, large transaction

made after very small transaction) with the analytics engine constantly fine-tuned as it

incorporates vast amounts of new data every second. On a global basis, card fraud was

5.69bps of total purchase volume in 2016.

Exhibit 10: V and MA total operating costs (which includes several Exhibit 11: Card Fraud on global networks remains manageable even

discretionary investments) are under 10c per transaction and continue as the risk of cyberthreats has grown exponentially

to decline over time Card Fraud in Basis Points

Total Operating Cost per Transaction Processed 14

US Rest of the World

$ 0.12

12

V MA

$ 0.10 10

8

$ 0.08

6

$ 0.06 4

2

$ 0.04

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$ 0.02

2014 2015 2016

Source: The Nilson Report

Source: Company Data, Morgan Stanley Research

3) Network rules solve for trust: Visa and MasterCard network rules guarantee

payments to merchants, while providing consumers with 100% protection against

fraudulent activity or loss of stolen credentials.

4) High bar on Speed: We believe Visa and MasterCard networks in aggregate process

more than 5,000 transactions per second with capacity to process volumes multiple

times that number. Bitcoin in contrast takes 10 minutes to clear and settle a single

transaction vs. Ethereum that takes 15 seconds.

5) Universal acceptance and ease of use: Over their many years of existence, Visa and

18Mastercard have developed acceptance at more than 44mn locations globally, with

expectation for the acceptance network to grow exponentially over the next 5 years as

proliferation of connected devices (mobile, Internet of Things, etc) allows for payments

functionality to be embedded at many new end points.

Decentralization could introduce unsustainable and

unpredictable costs, and has other potential drawbacks

Bitcoin and other Proof-of-Work based distributed ledger systems use electricity. A lot

of it: As the value of cryptocurrencies rise, so does the supply of miners seeking to earn

fees for validating transactions. Bitcoin and most other ledger systems use a "Proof-of-

Work" construct to validate transactions, and as miners compete with each other to

validate transactions, the "hashing" difficulty (i.e. the difficulty of solving an arbitrary

math problem) continues to increase dramatically, and the total effort by all dedicated

mining hardware to solve these hashing problems draws an increasingly massive amount

of electricity.

Exhibit 12: Rising bitcoin price has driven up mining capacity, and concurrently, electricity

consumption

Total Energy Consumption (Megawatts)

3,000

2,500

Electricity Consumption

2,000 of 2 million US homes

1,500

1,000

500

0

11-Apr-11 11-Apr-12 11-Apr-13 11-Apr-14 11-Apr-15 11-Apr-16 11-Apr-17

Note: Energy consumption estimated basedon global mining hash rate multiplied by average Joule/gigahash/s energy usage, which we assume declines linearly from 1.5

in 2014 to 0.2 in 2017

Source: blockchain.info, Morgan Stanley Research estimates

Some inherent disadvantages in the consumer experience: Besides being a more

inefficient use of resources, distributed ledger systems also have clear disadvantages at

the a point-of-sale.

No chargebacks is a positive for merchants, but a negative for consumers: The

existing card payment ecosystem is designed to give consumers the comfort to

transact with merchants they are unfamiliar with – purchase something online, and

if it doesn't arrive or merchant goes bankrupt, consumers can contest the charge

and the card networks will put the onus on the selling merchant and their acquirer.

With a crypto transaction there is by definition no intermediary to work on behalf

of a consumer, leaving the buyer at risk of dealing with a fraudulent merchant.

For merchants, total cost of acceptance is not unequivocally lower: Critics of the

current payment ecosystem cite the ~1-3% merchant discount rate as an

opportunity for disruption by cryptocurrencies, but it's not clear that a distributed

ledger based system can charge less. Merchants that choose to accept

cryptocurrencies can opt to hold the currency, exposing them to fluctuations in

19value, or they can choose to work with a payment service provider or exchange that

converts each transaction back to fiat, exposing them to exchange spread cost.

Further, it remains to be seen how much miners will charge for transaction costs in

an environment where they are not being awarded in bitcoin, as is the case today.

Note that on December 6, Steam, the pre-eminent gaming platform, stopped

accepting bitcoin due to "high fees and volatility."

Long clearing times don't work well for brick and mortar: Proof-of-Work based

cryptocurrencies have transactions that clear on a batch basis, which for Bitcoin

averages to be every 10 minutes. Some cryptocurrencies are designed to clear at a

faster pace (e.g. Ethereum), but even these can be impacted by congestion/capacity

constraints. We find it difficult to expect transaction speeds to match those of card

transactions on a consistent basis.

There are areas of inefficiency/pockets of opportunity for

cryptos.

While cards work extremely well for most point-of-sale transactions, there are areas of

the global payments market that are either underpenetrated or have relatively high

transaction costs that could potentially be undercut. Two examples:

Cross-border money remittance: Global money transfer providers charge

consumers an average of 7.21% of the principal value. A number of free mobile-

based domestic P2P applications exist, but cross-border P2P are likewise expensive.

Because money transfer transactions occur less frequently than Point-of-Sale

purchases, have higher average transaction values, and need not be instant (10

minute clearing time is probably good enough), we see this as a more suitable

opportunity for cryptocurrencies.

B2B and other large ticket transactions: Cryptocurrency transaction costs tend to

be relatively fixed in nature (apart from "FX" conversion costs), and this positions

cryptocurrency-based payment transactions well for large-ticket transactions

where the variable merchant discount rates charged in the traditional card

ecosystem can seem prohibitive and have gotten pushback.

Incumbents too could use blockchain technology to resolve

some of these issues

Incumbents like Visa and Mastercard can use blockchain technology to build

private/permissioned ledgers (as opposed to public ledgers typically used by

cryptocurrencies), which are used only to drive efficiency. e.g. Visa's B2B Connect

initiative uses blockchain architecture to enable financial transactions on a scalable

private blockchain network of participating banks. This network is being designed to

provide a new real-time payments system for high-value cross-border payments

between participating banks on behalf of their corporate clients.

This piece was originally published on December 15, 2017; all data are as of that date.

20US: Semiconductors

Who Will See the Greatest Opportunities in Semiconductor

Machine Vision?

Morgan Stanley & Co. LLC Joseph Moore

Joseph.Moore@morganstanley.com

Our View Market View

We expect many winners as machine learning redefines machine vision - The market has looked at the large opportunities in cloud, and to some

AMBA and XLNX have the most rerating potential. One of the important extent in cars, but isn't looking at machine vision as a distinct problem. The

ramifications of machine learning is an acceleration in state of the art in early opportunities are dominated by deep learning "training" chips from

machine vision. Machine learning has been seen as important because of its NVIDIA. inference solutions from NVIDIA/Altera/XLNX or systems level

impact on cloud spending for training, But one of the most important implementations such as Mobileye. While those opportunities are exciting,

ramifications of machine learning is an acceleration of "machine vision", or we expect dedicated solutions to emerge.

extracting information from video images - key to self driving cars, but also

automating a wide variety of vision oriented tasks. We see this as creating an Investor concern: The long lead times for fully autonomous vehicles makes

entirely new category of semiconductor products. this a difficult investment thesis. We agree that the extended time frame is

almost undoubtedly true, and we expect investor fatigue to set in when time

The focus thus far has been on programmable solutions, but standardized frames are inevitably delayed. So it's important to focus on not just the end

products will also emerge - Ambarella could be a big surprise. We see a big goal of full autonomy, but on various milestones along the way that will

role for programmable products - notably GPUs from NVIDIA, and FPGAs demonstrate machine vision analytics capability. The extended time frame

from Xilinx - but as machine vision matures, we see standard products for implementation also should lead to room for more standardized, less

solutions as emerging. Mobileye/Intel has an early lead but Ambarella and programmable solutions.

others could emerge with greater than expected opportunity.

Semiconductor machine learning is more important than just the

cloud impact

In 2018, we expect machine learning to start to become a more meaningful accelerant

for most of the semiconductor green shoots that were already in place. Morgan Stanley

thematic reports in recent years have focused on drivers such as Internet of Things,

autonomous driving, augmented reality, and automation, all of which are dependent

upon computers that can extract information from video images.

Until the last few years, solving such problems relied largely on "heuristic algorithms" -

that is, structured software development that teaches algorithms to interpret images

one step at a time. For example, teaching software to do facial recognition by parsing

facial details (how far apart are the eyes, shape of the nose, etc.).

Machine learning has proven to be a substantial accelerant to this process. Machine

learning essentially instead exposes an iterative learning algorithm to data - in the facial

recognition example, a database of facial images tagged to actual individuals - and the

algorithm makes its own determination about how to extract the information.

21Exhibit 13: Machine Learning Image recognition timeline

2012 2013 2014 2015

Krizhevsky

AlexNet enables solution lower Matthew Zeiler and First time that Microsoft wins using

Google wins 2014

Machine learning for errort rate for Rob Fergus from the machine learning an algorithm called

competition with an

the first time to beat Imagenet NYU achieve 11.2% beat humans at "ResNet" and lower

errort rate of 6.7%

other algorithms Challenge to error rate image recognition error rate to 3.6%

15.4%

Source: Morgan Stanley research

Why it matters: The headline application for machine vision is self driving cars, which

certainly has been an investors' focus - we have ascribed $15 bn of value to NVIDIA's

essentially pre-revenue ADAS business, and Intel paid close to that - over 40x revenues

- for the leader in Level 2 driver assistance, Mobileye.

Fully self driving cars are clearly an exciting opportunity, and might continue to drive

strategic activity in the space. But the timeline is very long, as the required technology is

in its infancy.

Perhaps more importantly, solving the video vision analytics problem will have

important ramifications for the surveillance camera market, commercial drones, driver

assistance, medical devices, and robotics/automation. Adding intelligence to cameras can

enable new innovations like the Amazon Go concept store that uses machine vision

(among other technologies) to eliminate checkout, to identify crimes in progress, and to

conditionally record data under certain circumstances.

What are the semiconductor building blocks? Machine vision is in some respects simply

another form of deep learning "inference", which is essentially the classification of the

visual data through application of the neural network database that is "trained" through

the deep learning process. As such, the solutions normally seen for inference are going

to get the early wins for machine vision. But as the end market applications mature and

grow, we would expect to see more specialized solutions tend to dominate.

Microprocessors (Intel, AMD) or applications processors (Qualcomm, Apple): Today, much

of what we would characterize as inference for machine vision is done on various

microprocessors. We expect this to change, over time, as traditional microprocessors are

suboptimal for video data sets (which are highly parallel in nature). But for today, the

dominance of CPUs in cloud and in devices. We also note that many of the early

prototype "self driving cars" are based on large clusters of microprocessors, mostly from

Intel.

Graphics (NVIDIA, Intel Xeon Phi, AMD): Graphics chips are better for video data streams

given the higher degree of parallelism vs. traditional microprocessors. And NVIDIA have

the advantage that most neural networks are trained on their devices. Graphics chips are

also more programmable than custom chips. Still, there are some limitations - we don't

think that the same chip can be optimal for training (double precision floating point

data, highly throughput intensive, insensitive to latency concerns) and inference (8 bit

integer data, not computation/throughput intensive, highly latency sensitive, with

minimal power consumption a key). Still, we do expect NVIDIA to get many of the early

wins due to the company's prevalence in training.

Field programmable gate arrays (Xilinx, Intel/Altera): FPGAs are uniquely well suited to

machine vision tasks, given their high degree of inherent parallelism, lower latency, and

22better power consumption compared to graphics. Ease of use has been a challenge in

cloud, where customers are less familiar with FPGA design, but closer to the edge we

see FPGAs having a strong role, and we think that Xilinx actually has more ADAS

revenue than any other semiconductor vendor. The challenge will be that as volumes

grow and technology matures, there will always be some pressure to move to standard

products which offer lower unit prices (at the expense of design flexibility).

Custom ASICs and application specific standard products (Intel/Mobileye, Intel/Movidius,

Ambarella, Tesla's internal design). As potential volume grows, and time passes enough

for the design cycles to catch up to technology needs, products specifically designed for

machine vision tasks should play a more significant role. Intel has acquired a couple of

the first movers (Movidius in drones/surveillance, Mobileye in cars), which seem

promising. Tesla has made it clear that they are developing their own solution for the

next generation autopilot. Perhaps the greatest rerating potential comes from

Ambarella, who has spent the last 4 years developing computer vision analytics chips to

partner and ultimately integrate with its video processing solutions.

2018 should be a table setting year for these technologies. We don't see much revenue

outside of areas such as surveillance cameras, but when we exit the year we should

have a much clearer picture of which solutions are going to be fundamental building

blocks.

AMBA and XLNX have the most rerating potential in that it is a positive new category.

We would consider the "incumbents" to be NVIDIA in graphics, Xilinx in FPGAs, and Intel

in all product categories, most notably level 2 ADAS through it's Mobileye acquisition -

but as the incumbent, in a category that has some enthusiasm, the bar is higher for stock

rerating. We see the highest rerating potential coming from small cap AMBA, which has

been depressed until recently around hurdles in its video processing products - but we

see the company as emerging as a leader in this category. XLNX also faces the most

investor skepticism, due to the typical life cycle of FPGAs that can see them replaced as

technologies mature - we believe the stock offers upward rerating potential as the

integration of high end CPUs leads to longer duration.

This piece was originally published on December 15, 2017; all data are as of that date.

23US: Software

Which Software Companies Will Make Money from Machine

Learning?

Morgan Stanley & Co. LLC Keith Weiss

Keith.Weiss@morganstanley.com

Our View Market View

Machine Learning enables significantly new functionalities to be automated... Bear Case: Application of Machine Learning technologies still difficult. Most

Machine Learning (ML) programing techniques are unlocking new investors believe the inflection point for ML is still a few years away. The

capabilities for software-based solutions that previously existed only in the training required for computers to understand company and industry-specific

realm of human labor, representing a foundational technology capable of data sets is time-consuming. Significant frictions exist between technology

sustaining massive new market opportunities. vendors who understand how to program the ML algorithms and the end

users who understand the domain-specific problems to be solved and

...with cloud platforms likely the first beneficiaries… Platform vendors like opportunities to be unlocked.

Microsoft Azure have built out machine learning tool sets that abstract the

complexity of the underlying technologies, making them easier to use for data Additionally, the size and transparency of the financial impact to the large ML

scientists. Further, platform vendors like Microsoft present ML driven providers is limited, making it a longer-term trend with minimal impact over

capabilities like Natural Language Processing or Image Recognition as the next year.

application services easily consumed by developers. As seen with prior

cycles of new software capabilities emerging, early consumption likely takes Bull Case: Cloud-Based Applications Vendors Drive Early Value. With both

place in custom-built applications, with the infrastructure platform vendors access to large (and well-understood) data sets and a good understanding of

monetizing the trend first. end-user business needs, Cloud-based application vendors are uniquely

positioned to create value added solutions from the use of machine learning

...and Machine Learning optimizations becoming 'table stakes' for application technologies. In the past, application vendors have upsold analytics and

vendors. Over the past year, most application vendors have begun marketing optimization engines into their installed base, ML will prove no different.

new capabilities and optimizations within their solution portfolio enabled by

machine learning. However, our initial work suggests vendors may struggle to

monetize these machine learning capabilities discreetly. Rather, customers

see them as the continual innovations in functionality that should be included

in a subscription-based application model.

Custom Applications Built First, And Built In the Cloud

We see the Cloud platforms players, not applications, as the early winners in ML with

Microsoft, Amazon (covered by Brian Nowak) , and IBM (covered by Katy Huberty) the

underappreciated leaders. As seen with prior cycles of new software development

capabilities coming into the market, initial utilization likely tilts towards custom-built

solutions versus packaged applications. Thus we see value accruing to cloud-delivered

platforms with machine learning tool sets enabling software developers to more easily

incorporate the functionality into their applications. On the other hand, we see ML-

based optimizations becoming standard across existing application suites, rather than

serving as an area of potential differentiation or additional monetization. As a result, we

see less value accruing to companies like Salesforce.com, Workday and Adobe, who are

24focused on adding machine learning capabilities within existing solutions.

Exhibit 14: Cloud Platforms Bring Together Big Compute and Big Data – A Fertile Environment for

Machine Learning Applications to Propagate

Source: Morgan Stanley

What Is Machine Learning? To be clear, we are not talking about building the

Terminator, nor trying to pass the Turing Test (interactions with computers

indecipherable from humans) – but the ability to develop specific capabilities of human

intelligence within technology driven systems. Traditional programing techniques have

been Deterministic or 'Rules Defined' – each step of the operation and any possible

routes are defined in the program. Machine Learning programing techniques like neural

networks are 'Solution Defined' – a learning system optimizes the program (the

algorithm) to best solve a given task. This solution defined approach has enabled rapid

progress in developing capabilities like Image Recognition, Natural Language Processing

or Motion and Manipulation in software, areas that previously were only the realm of

humans. These capabilities form the foundation for the march towards Artificial

Intelligence.

Why Build it in the Cloud? The training and optimization of machine learning algorithms

requires three core elements; 1) large data sets used to train the system, typically more

data enables better solutions; 2) large amounts of computational power (and often

specialized processors) to run the huge number of iterations necessary to train the

algorithms in a reasonable amount of time; and 3) the data scientists necessary to run

these still-complex systems. Public cloud platforms like Amazon Web Services or

Microsoft Azure offer both a centralized and low-cost pool of storage to host the large

data sets, and bring them together with vast amounts of processing power. Additionally,

all of the Public Cloud giants have hired (and acquired) aggressively to bring machine

learning expertise to their platforms.

Microsoft An Underappreciated Leader in Machine Learning. In attempting to

democratize machine learning, Microsoft’s ML strategy is consistent with its mission to

“empower every person and every organization to achieve more”. Microsoft's approach

looks to monetize machine learning in four broad areas: 1) Agents – using digital

assistant Cortana to facilitate the interactions between individuals and application

services, 2) Applications – instilling machine learning features and functionality into all

their apps, 3) Cognitive Services – bringing the software developer access to machine

learning derived capabilities like Natural Language through easy to utilize application

services, and 4) Infrastructure – building a machine learning tool set within Azure –

25You can also read