Market Update Region MEA - June 2021 - DB Schenker

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market Update

Region MEA

June 2021

Air Freight

Summary

Market Forecast Capacity Carriers

‒ Middle Eastern airlines posted a robust ‒ Cargo capacity ‒ Passenger flights not expected to return

4.4% m-o-m increase in cargo volumes shortage due to lack to pre COVID levels until 2026; more

of passenger aircraft fallout expected

capacity still down

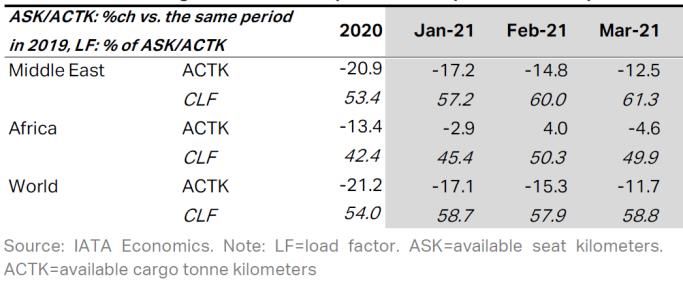

‒ Industry-wide CTKs were up 12.% in April by 14% as compared ‒ African Airlines performed the strongest

2021 compared to the same month in to 2019, despite the of all regions. With CTKs up just over 23%

2019. This strength partly reflects a weak steady growth of compared with pre-crisis level in March

month of April 2019, when the industry freighters 2019 and Middle east carries up 9.1% in

was affected by the US-China trade same period

dispute

‒ After stripping out fluctuations caused by

seasonal patterns, air cargo displays a

steep upward trend, started when strict

lockdowns were lifted in May 2020.

Seasonally adjusted (SA) volumes rose 4.% Rates Jet Fuel

m-o-m in April, the highest growth rate ‒ 2021 rates continue to remain the same as compared to 2020, ‒ Crude oil reaching new heights will have an

since September 2020. SA CTKs are now although still higher as compared to 2018 - 2019 impact on jet fuel prices

around 5% higher than the pre-crisis

August 2018 peak

Market Developments

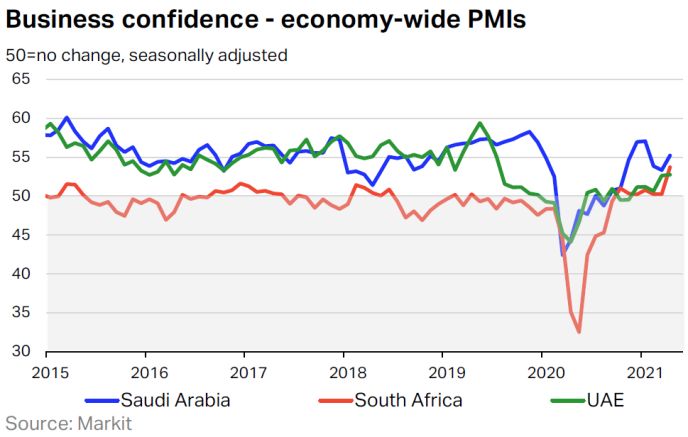

Economic Outlook Economic backdrop

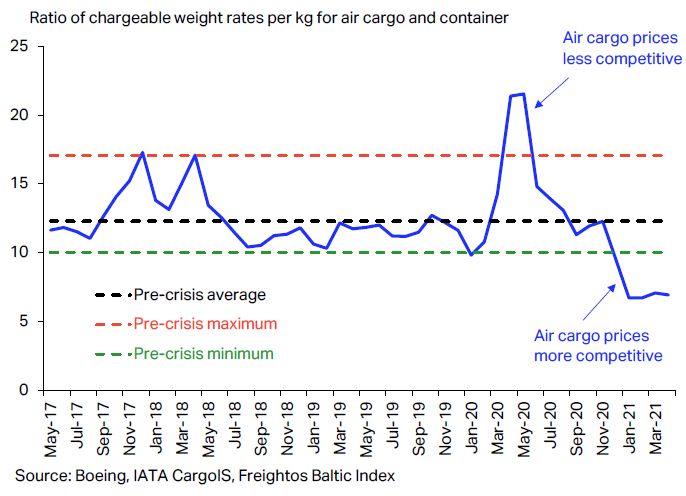

‒ On average, before the crisis, air ‒ The latest PMI results show that

cargo worldwide was 12 times the economic backdrop continues

more expensive than the ocean to improve across the three key

freight. Since April 2020, container economies that we track for the

rates have grown faster, whereas MEA region. In Saudi Arabia,

air freight rates have been stable business activity began to recover

in H2 2020, while South Africa and

the UAE are seeing an economic

expansion now

Capacity Development

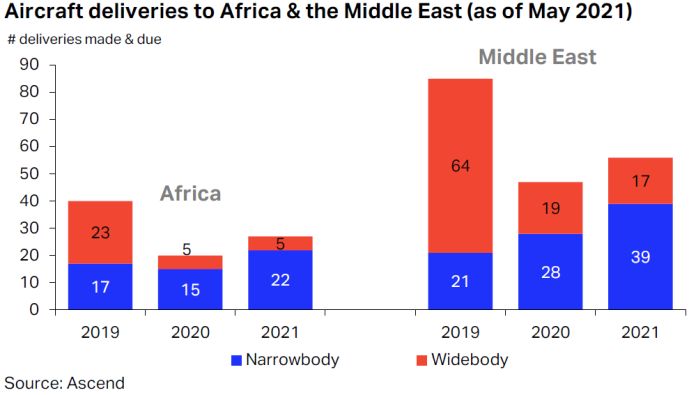

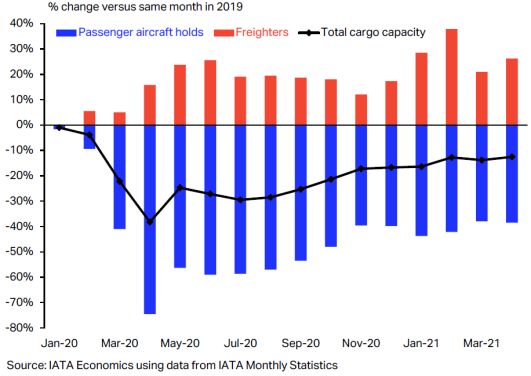

‒ Industry-wide available CTK picked ‒ As of May 2021, African carriers

up by 5.6% m-o-m in March and are expected to receive 35% more

were ~12% below the pre-crisis aircraft deliveries in 2021 vs 2020,

levels while Middle Eastern airlines

should get 19% more deliveries

‒ ACTKs of African and Middle

Eastern carriers were down 4.6% ‒ In both regions, the number of

and 12.5%, respectively deliveries will most likely not reach

The above figures are updated only quarterly

2019 levels

Market Developments

Economic Outlook Economic backdrop

‒ African airlines performed the ‒ The substantial rise in demand for

strongest of all regions, with CTKs logistics benefits all modes of

up just over 23% compared with transport

the pre-crisis levels in March 2019

‒ The increase in demand and

reduction in capacity has disrupted

supply chains across the world,

pushing business to operate in a

just-in-time model

IATA Air Cargo Market Analysis

‒ The Middle East and African carrier’s RPK are posting a weaker outcome as they significantly rely on improvement in international demand

‒ Slow vaccination rate will hinder air travel recovery in Africa, while Middle East RPK will adversely be impacted by travel restrictions and international long-haul routes

‒ In Q1 2021, the airline industry continues to post net losses and looking ahead, the financial performance will vary depending on the size of the domestic market and the

pace of vaccine rollout

‒ Higher fuel surcharges will be a challenge to return to profitability when traffic rebounds

Market Outlook

APAC Americas Europe MEA

‒ Capacity is stable on Lower Deck ‒ Capacity is stable on Lower Deck ‒ Capacity is stable on Lower Deck ‒ Capacity is stable on Lower Deck

but challenging for Main Deck but challenging for Main Deck but challenging for Main Deck but challenging for Main Deck.

‒ Rate levels are maintaining the ‒ Rate levels are maintaining the ‒ Rate levels are maintaining the ‒ Rate levels are maintaining the

momentum of 2020 levels momentum of 2020 levels momentum of 2020 levels momentum of 2020 levels

Ex

MEA

‒ Capacity offer is limited ‒ Capacity good/ pricing stable, ‒ Tightening capacity/ pricing might ‒ Capacity is stable on Lower

Exception to South Africa (JNB) increase to South Africa Deck but challenging for Main

‒ The rate level maintains at about Deck

80% above the pre-COVID levels ‒ Space tight and rates high ‒ Supply and demand are stable to

the rest of MEA ‒ Rate levels are maintaining the

Into momentum of 2020 levels

MEA

Ocean Freight

Summary

Market Forecast Space Equipment

‒ Demand From Europe to the Middle East continues to be high; ‒ Further capacity constraints expected due ‒ Equipment shortage prevails in Egypt and Saudi

however, space and equipment allocation from the carriers to MEA is to vessels planned for periodic maintenance Arabia

limited, creating a demand-supply imbalance on this tradelane and/or scrubber installation

‒ Ex Europe and APAC, equipment situation

‒ For the month of June, Europe to MEA tradelane is expected to be high ‒ Carriers are closely monitoring the space remains critical

on utilization. Equipment availability will remain a challenge across agreement. In the case of non-utilization,

Europe (except the UK) the agreed space allocation is scaled down. ‒ We strongly recommend a minimum of four

weeks forecast to secure booking with the

‒ Ongoing issue at Yantian terminal, China, will have a ripple effect on ‒ Although there is a capacity constraint, carrier and to ensure equipment and space

vessel schedule/equipment availability and freight carriers are open to negotiating space at a availability

premium spot rate on certain tradelanes

‒ Schedule adjustments to desired tradeflows in the Far East are

prioritized over the Middle East region

Rates Others

‒ In general, 2021 base contract rates remain significantly higher than the previous year. June onwards, the ‒ For the MEA region, the blank sailings from Europe Asia will

additional rise in Bunker coupled with PSS surcharge is driving the overall rate levels across all tradelanes result in 23% capacity withdrawal, according to various carrier

sources

‒ North and South European ports continue to impose congestion surcharge that was introduced as a result

of the Suez blockage ‒ More than 200k TEUs are currently stuck at Yantian port, China,

working at 30% working capacity only. Each day port will only

‒ Space will be the driving factor in the market and, carriers will prioritize high paying/light-weight cargo accept 5000 TEUs for scheduled vessels to depart within three

days. Congestion is expected to last till June 2021

‒ Considering the shortage of equipment, free time is highly restricted as the carriers would like the

equipment to turn around quicker. The longer free time requests are imposed with a premium demurrage

and detention charges

Market Developments

Bunker Development Freight Rate Development

700 ‒ The VLSFO increased more 4500 ‒ The SCFI index was at USD

600 than 50% from Q4 2020 to Q2 4000 2719 in December 2021 and

500 2021, triggering increased 3500 currently trending at USD 4733

bunker surcharges from the 3000

400

2500

300 carriers 2000

‒ Given the current challenges

200 1500 around equipment and space

100 1000 coupled with an increase in

0 500 bunker surcharge, the freight

0

rates are expected to remain

high till the end of 2021

IFO380 VLSFO ULSFO MGO

Source: Bunker based on 4 ports for IFO380, VLSFO and MGO. Based on Rotterdam for ULSFO Source: SCFI based on 13 ports

Economic Outlook (Annual % change)

‒ The outlook for Africa stays strong at 4.9% growth for 2021 and ME at 2.5%. The global economic outlook continues to be strong for 2021, with an average of 6%

‒ Given the V-shaped economic recovery and vaccine developments across the world, air freight and ocean freight demand is expected to further increase during the year

10 7.3

5.2 5 4.8 4.7 4.6 6.1 6

4.9 4.1 4.1 4.1 4.2 4.2 4.3 4 4.4 3.5

3.5

5 2.5 3.4 3 2.8 2.7 2.7 2.2 1.9 1.7 1.7

3.4 3.3 3.3

1.5 1.5 1.6 1.6

0

Africa Middle East Asia and Pacific Europe North America World

-1.9 -1.3

-5 -3.3

-4 -4.1

-5.8

2020 2021 2022 2023 2024 2025 2026

-10

Source: ©IMF, 2021

Main Port Analysis worldwide

Hotspots of Equipment Shortage and Congestion

EU/NCP to FE

Schedules at 32.3%

TAwb/NCP/EC Vessel delay 5.5 days

Schedules at 33% Fewb/NCP

Vessel delay 6.5 days Schedules at 24.4%

Vessel delay 8 days

23,000 TEU backlog

TPeb/WC

Schedules at 22.2%

Vessel delay 10.5 days

‒ Various hotspots of congestion

and equipment shortage last as

an aftermath of Suez canal

blockage, hence impacting the

MEA region

‒ Blank sailings and scrubber

activities are creating a demand-

supply imbalance

‒ Substantial vessel utilization into

and out of the MEA region

continues to drive the ratesMarket Outlook

APAC Americas Europe MEA

Space Space Space Space

‒ Open for most of the destinations ‒ Space is open to USEC ‒ Space crunch remain extreme with all carriers ‒ Mostly open to intra MEA locations

‒ Limited space for ISC ‒ Extremely limited to USWC ‒ Light cargo continues to be prioritized by all

carriers

Rate

Rate

Rate Rate ‒ Remains high due to PSS, in addition to other ‒ Rate to Saudi has been increased almost

‒ PSS maintained by the carriers ‒ Further GRI / PSS expected factors by 70% by all main carriers

Ex ‒ Possible to negotiate rates for bulk spot

bookings

‒ Remain high, especially USWC

Equipment Equipment

MEA Equipment

Equipment

‒ Standard containers are available

‒ MSC / Messina shortage in Saudi Arabia and

Hapag-Lloyd, Egypt

‒ Shortage, as priority given to revenue

generating trades and equipment

‒ Standard containers are available ‒ Options to use NOR available from Europe to repositioning

South Africa

Others

‒ Severe berthing delays in USWC ports Free time Free time

‒ Lack of equipment has curtailed additional free ‒ No additional free time being offered,

time agreements purchase option is also limited

Space Space Space

‒ Extremely scarce ‒ Limited space ‒ Space remains a challenge. Forecasts and

‒ Priority for high paying cargo an optimal usage of given allocation are

Rate very important to manage this situation

Rate ‒ Rates stable

‒ Continue to increase Rate

Into ‒ Premium rate with guaranteed space Equipment

‒ Shortage at certain USEC ports

‒ Hapag has already published GRI for

various lanes ex Europe

MEA Equipment

‒ Severe shortage Equipment

‒ Especially 40ft containers ‒ Hinterland movements are affected, and

shortage of equipment continues

‒ Free time

‒ No additional free time being granted at

destinationsAbbreviations ACTK Available Cargo-tonne Kilometers CTK Cargo-tonne Kilometers ME Middle East MEA Middle East And Africa M-O-M Month-on-month NOR Non Operating Reefers PMI Purchasing Manager’s Index PSS Peak Season Surcharge RPK Revenue Passenger Per Kilometer SCFI Shanghai Freight Index VLSFO Very Low Sulphur Fuel Oil

You can also read