Mighty River Power Capital Markets Day - 2 October 2013 - Amazon AWS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2 October 2013 Mighty River Power Capital Markets Day

CAPITAL MARKETS DAY Disclaimer The information in this presentation has been prepared by Mighty River Power Limited with due care and attention. However, neither the company nor any of its directors, employees, shareholders nor any other person shall have any liability whatsoever to any person for any loss (including, without limitation, arising from any fault or negligence) arising from this presentation or any information supplied in connection with it. This presentation may contain projections or forward looking statements regarding a variety of items. Such projections or forward looking statements are based on current expectations, estimates and assumptions and are subject to a number of risks, uncertainties and assumptions. There is no assurance that results contemplated in any projections and forward looking statements in this presentation will be realised. Actual results may differ materially from those projected in this presentation. No person is under any obligation to update this presentation at any time after its release to you or to provide you with further information about Mighty River Power Limited. A number of non-GAAP financial measures are used in this presentation. You should not consider any of these in isolation from, or as a substitute for, the information provided in the audited consolidated financial statements which are available at www.mightyriver.co.nz. The information in this presentation is of a general nature and does not constitute financial product advice, investment advice or any recommendation. Nothing in this presentation constitutes legal, financial, tax or other advice.

CAPITAL MARKETS DAY Agenda 1.00pm Introduction and Health & Safety 1.15pm Operations 2.15pm Retail 3.00pm Afternoon tea break 3.30pm Metrix 3.45pm Development 4.30pm Capital Management 5.00pm Q&A

CAPITAL MARKETS DAY

Our company and the environment we operate in

> Operate in a competitive and well-functioning market that has led to world-best

outcomes

> for security, level of renewables and resilience to future fuel shocks

> Consumer benefits now occurring from major investments

> Our portfolio well positioned for demand-supply dynamics

> current excess capacity, reflecting flat demand and increased renewable generation

> potential for reduction in excess capacity, as more flexible take-or-pay requirements

lead to further response from fossil fuel generators

> Inherent portfolio advantages mean greater earnings surety under most market

conditions, including weak Waikato hydro conditions

> Multi-brand retail strategy delivers a tailored customer experience through

innovation in an intensely-competitive market

> Metrix, our technology business with unique multiple technology platforms,

provides opportunity for earnings-accretive growth

> Development business continues to position for weak domestic outlook and

medium term economically-viable growth options offshore

> Focus on sustainable earnings and capital management underway and ongoing

CAPITAL MARKETS DAY

Health & Safety

> Health & Safety focus on ‘zero harm’ is an absolute TOTAL RECORDED INJURY

priority FREQUENCY RATE

2.5

> Critical industry opportunity with common contractors

and sub-contractors - StayLive generators’ group 2.0

> Company (and other generators) TRIFR well below

electricity sector averages 1.5

> our TRIFR shows 17% improvement y-o-y; and

59% improvement over past five years 1.0

> Ngatamariki project TRIFR (involving 1 million

0.5

person-hours) of 0.98 vs 3.54 for last major

project (Nga Awa Purua)

0.0

> LTIFR at similar levels for the last 5 years FY2009 FY2010 FY2011 FY2012 FY2013

> Significant and on-going effort into Health & Safety

processes, specific focus to improve critical risk LOST TIME INJURY FREQUENCY RATE

identification, including systems and culture (EMPLOYEES AND ON-SITE

CONTRACTORS)

> Sentenced for ‘near-miss’ incident in September 2013 0.6

> $32,000 for drilling contractor; $16,000 for

0.5

Mighty River Power as principal for failing to

take all practicable steps 0.4

> Judge referenced one-off nature of incident and 0.3

Company’s good safety record and robust safety 0.2

processes

0.1

> early guilty plea from the Company; focus on

capturing learnings and implementing 0.0

improvements in future risk identification FY2009 FY2010 FY2011 FY2012 FY2013

Operations Capital Markets Day Presented by: Fraser Whineray Phil Gibson General Manager Wholesale Markets Manager Operations

OPERATIONS Operations Operations is responsible for: > Managing the generation of electricity to be sold on the wholesale market and to certain large commercial customers > Managing wholesale electricity value and risk position through a range of levers > Operation and maintenance of power stations and upstream fuels

OPERATIONS Market Structure

OPERATIONS

Wholesale/portfolio decisions and governance

Governance – Management/Board

SHORT‐TERM MEDIUM‐TERM LONG ‐TERM

Cover risk and achieve Optimise sales book and Future earnings growth

best value for fuel fuel choices and asset management

Pricing Pricing Pricing

Competitors Competitors Competitors

Dispatch Optimisation

Portfolio net position Portfolio net position

Fuel Value

Outage Planning Asset Management

Outage scheduling

Transmission Plant Mode New Plant

Fuel Fuel Fuel

Decisions made in conjunction with

Decisions made in conjunction with retail Decisions made by Operations

Development

OPERATIONS

Demand and supply

> Excluding industrial, demand flat over last six years

> deindustrialisation trend seen since 2003

> Meridian Tiwai negotiations more positive than expected

> 170MW step down in Meridian contract volume in 2015

> provides clear signal and time for thermal response, including others contracting with Tiwai

> Thermal units in New Zealand are large relative to the total market

> 170MW step-down equivalent to a 15% reduction by the three CCGTs

NATIONAL CONSUMPTION

45,000

40,000 Thermal Generation

35,000 for FY2013

GWh

30,000

25,000

20,000

03 1998

09 1998

03 1999

09 1999

03 2000

09 2000

03 2001

09 2001

03 2002

09 2002

03 2003

09 2003

03 2004

09 2004

03 2005

09 2005

03 2006

09 2006

03 2007

09 2007

03 2008

09 2008

03 2009

09 2009

03 2010

09 2010

03 2011

09 2011

03 2012

09 2012

03 2013

National Consumption Rolling 12 months

National Consumption Excl. Tiwai Rolling 12 months

National Consumption Excl. all Direct Connect Rolling 12 monthsOPERATIONS

Thermal utilisation reducing

> Record level of thermal surplus due to combination of:

> long lead time generation build pipelines

> sustained period of flat to declining demand growth

> Introduction of non-discretionary renewables (geothermal and wind) has led to displacement of

base-load thermals

> Thermal generators’ response constrained by fuel commitments

THERMAL UTILISATION AND CAPACITY, AND GEOTHERMAL CAPACITY

100% 25,000

Thermal and Geothermal Capacities

80% 20,000

Utilisation

60% 15,000

40% 10,000

(GWh)

20% 5,000

0% ‐

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Diesel Capacity Coal Capacity Gas Capacity Geothermal Capacity

Southdown Otahuhu TCC Huntly Main

Huntly 6 Whirinaki e3p

Note: in the above graph thermal capacity is stacked and the geothermal capacity is overlaidOPERATIONS

Thermal response underway

> Contact

> Investment in Ahuroa gas storage facility allows reduced take-or-pay quantities and converts gas supply from base

load to peaking/firming

> Signal to mothball Taranaki CCGT (TCC) from start of 2014 to defer maintenance capex

> Considering disconnection of OTA steam turbine and conversion to OCGT

> Genesis

> Recently announced the second of its units going into storage before the end of 2013

> Only two Huntly 250MW units available from 2014 – expect very low utilisation

> Mighty River Power

> Converted Southdown from base-load to peaking mode from 2003

> Gas supply arrangements reducing during 2014. No gas contracted from 2016

> Earnings from ACOT over winter – offset gas transmission costs

WINTER SECURITY MARGIN ASSESSMENT

Basecase

40%

No new thermal + decommissioning of one CCGT

Energy Security Margin

High Demand

30%

20%

10%

0%

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: System Operator, TranspowerOPERATIONS

What does it all mean for wholesale prices?

> Future wholesale market price outcomes heavily dependent on key drivers of supply and demand

> Futures curves and independent forecasts consistently low for some time

> Market expects some increase over time to wholesale and futures prices

> Current commercial prices would not cover fuel and variable operating cost of thermals

> ASX CAL14 saw $3 lift in response to Contact TCC announcement in August 2013

THIRD PARTY WHOLESALE ELECTRICITY PRICE ASX FUTURES SETTLEMENT PRICE (OTA)

FORECASTS

120 90

110 80

100 70

Nominal Price ($/MWh)

90 60

80 50

$/ MWh

70 40

60 30

50 20

40 10

FY14

FY15

FY16

FY17

FY18

FY19

FY20

0

FY2014 FY2015

Credit Suisse Deutsche Bank FNZC

Goldman Sachs Macquarie UBS As at 30 June 2012 As at 5 April 2013 (date of PFI)

As at 30 June 2013 As at 26 September 2013OPERATIONS

Mighty River Power portfolio dynamics

AVERAGE WHOLESALE PRICE (WKM)

> Traditionally run ‘short’ on an annual

90

energy basis

80

> mean Waikato hydrology and

70

Southdown at circa 30% load

60

> risk managed with additional thermal

$/MWh

utilisation and contracts 50

40

> Portfolio risk assessed by internal VaR

30

model against risk appetite

20

> Actual short position has range driven by 10

high/low inflow scenarios to Waikato 0

Hydro and wholesale prices FY2009 FY2010 FY2011 FY2012 FY2013

> Mixture of sales channels to residential,

SALES PORTFOLIO

commercial and industrial customers

Industrial Commercial Residential

nationwide - spreads exposure to location

risk and portfolio decay/price risk 8,000

7,000

> Current commercial contracts market

6,000

clearing at low/negative margins for risk

5,000

GWh

4,000

3,000

2,000

1,000

0

FY2009 FY2010 FY2011 FY2012 FY2013OPERATIONS

CFD and ASX

INDUSTRIAL CFD SALES

> Industrial Sales CFDs Other Industrial Sales

Kawerau Contract

> Fixed Price Fixed Volume contract, typical in

2,500

Industrial sales channel

2,000

> buyer takes some volume risk compared to 1,500

GWh

FPVV contracts, CFDs normally priced 1,000

accordingly 500

0

> 30% of total sales and 75% of net CFDs FY2009 FY2010 FY2011 FY2012 FY2013

> Inter-generator CFDs

NET INTER-GENERATOR CFD*

> generators use CFDs to manage fuel, plant and

transmission outages 3,000

2,000

> ASX and broker markets provide useful

reference for OTC markets 1,000

GWh

> 15% of net CFDs 0

-1,000

> ASX futures market

-2,000

> exchange traded market for quarterly futures FY2009 FY2010 FY2011 FY2012 FY2013

contracts Buy CFD Sell CFDs

> Mighty River Power participates as a Market ASX CFD

Maker 600

> useful alternative for hedging inter-island risk 400

> 10% of net CFDs 200

GWh

0 Location

Hedging

-200

*Includes VAS on both buy and sell side CFDs

-400

FY2009 FY2010 FY2011 FY2012 FY2013OPERATIONS

How is our portfolio placed to respond to short-term market conditions?

> Base-load geothermal and all-year -round rain-fed Waikato hydro delivers reliable generation compared to other renewable

portfolios

> South Island hydrology is negatively correlated to wholesale price. Taupo inflows are typically not correlated which limits

downside variability but has the opportunity for upside

> Flexible gas generation delivers peaking capacity and hydro firming for dry year risk mitigation (~1000GWh of potential

Southdown)

> All generation located in the central North Island in close proximately to growing parts of the economy – less basis risk

TAUPO AND SI STORAGE PERCENTAGES AND MEANS

100%

90%

Storage Percentage of Average

80%

70%

60%

50%

40% North/South # of QTRs

30%

Wet/Wet 11

Wet/Dry 4

20% Dry/Wet 5

10% Dry/Dry 1

Dry/Dry Taupo storage % SI Storage % Mean Taupo Storage % Mean SI Storage % 80% Mean SI Storage %

0%

Apr-09

Apr-10

Apr-11

Apr-12

Apr-13

Jul-08

Jul-09

Jul-10

Jul-11

Jul-12

Jul-13

Oct-08

Jan-09

Oct-09

Jan-10

Oct-10

Jan-11

Oct-11

Jan-12

Oct-12

Jan-13

Oct-13OPERATIONS

Risk Management Processes

Board

Market and Credit Risk Management Policy

Risk Assurance and Audit Committee

Executive Risk Management Committee

BACK OFFICE

FRONT OFFICE MIDDLE OFFICE

Administration of

Customer and competitor facing Position, Credit and Exposure transactions/cash flows

transactions Control

Transaction

External relationships Reconciliation

Confirmation

Competitor Insight Counterparty Credit Settlement

Accessed Credit

Market Insight Debt Management

Exposure

Offer and Acceptance Policy Compliance EA NotificationMARKET DYNAMICS

Market regulation

> Energy prices for end consumers set by deregulated, competitive market forces

> Deregulated wholesale market based on supply and demand established in 1990s, with full retail

competition from 1998

> Transmission and distribution considered monopoly assets – ownership separation from generation or

retailing businesses and separately regulated

> Independent Regulatory Agencies

> Commerce Commission – competition law and determination of returns for regulated asset base

> Electricity Authority (EA) is primary regulator of electricity markets - promotes competition in, reliable supply

by, and the efficient operation of, the electricity industry for the long-term benefit of consumers

> Framework has been settled since 1999 after a period of significant reform in mid to late 1990sOPERATIONS

A well functioning market

> Current market structure has led to highly competitive market which has resulted in world-leading

outcomes:

> 1,200MW renewable investment over last 10 years displacing fossil fuel

> best generation projects brought to market first

> security of supply highest for two decades

> retail churn around 20% (second only to Victoria, Australia)

> Initiatives have seen further improvements in wholesale markets

> transmission investment approvals/commisioning

> increased liquidity and price certainty

> Retail markets can benefit from investment in wholesale market

> Electricity Authority survey (February 2013) stated “prices in [this] market reflect the outcomes

expected in a workable market”

EA MARKET PERCEPTIONS SURVEY

Instantaneous Frequency

Retail OTC Futures Spot reserves keeping

2013

2011

Source: UMR research negative positiveOPERATIONS Transmission Pricing Review > The EA announced a new Transmission Pricing Mechanism (TPM) in October 2012 for consultation with proposed implementation in 2015 > The proposal was extremely complex, applied to all transmission (not just HVDC) and was retrospective in nature > Initial consultation attracted strong negative feedback by wide-cross section of submitters > EA has delayed proposed implementation date by one year and intends to release a further series of consultation papers on key elements of the proposal in FY2014 > Ability to recover generator charges key to any new proposal > Any decrease in Tiwai demand would change reallocation/beneficiaries

OPERATIONS Transmission Pricing Review

OPERATIONS

Transmission

> Core infrastructure for electricity markets RELATIVE WHOLESALE PRICE – OTAHUHU

TO BENMORE

> Underpin national competition for customers

5 Bi-pole outages

Transmission upgrades

4 HVDC Commissioned

> Transpower $3.5 billion programme expected to

Location factor

complete in March 2014 3

> North Island Grid Upgrade Programme 2

(NIGUP) providing improved security of supply 1

commissioned in October

0

> Wairakei Ring providing increased transfer

Aug

Sep

Oct

Apr

Aug

Sep

May

Jul

Nov

Dec

May

Jul

Jun

Jan

Feb

Mar

Jun

through central North Island

> High Voltage Direct Current (HVDC) Pole 3 RELATIVE WHOLESALE PRICE – OTAHUHU

TO WHAKAMARU

> HVDC Pole 2 control systems commissioning

underway 1.18

1.16

> lower opportunity for price separation between NIGUP Commissioned

1.14

North and South Islands

Location factor 1.12

> increases South Island generators’ ability to 1.10

compete in wholesale and end-user markets in 1.08

the North Island 1.06

1.04

> reduces risk of retailers competing against

1.02

South Island generators in the South Island

1.00

01 Oct

06 Oct

11 Oct

16 Oct

21 Oct

26 Oct

31 Oct

04 Jan

09 Jan

14 Jan

19 Jan

24 Jan

29 Jan

05 Nov

10 Nov

15 Nov

20 Nov

25 Nov

30 Nov

05 Dec

10 Dec

15 Dec

20 Dec

25 Dec

30 DecOPERATIONS

Reinvestment capital expenditure

> $72 million of reinvestment capital expenditure for

FY2014

> two wells at Kawerau and on-going hydro lifecycle work

> Higher than average reinvestment capital expenditure

for the rest of the decade given the hydro lifecycle

programme

> Arapuni generators - three complete; all four competed

end of 2013

> Ohakuri runners - two complete and all four expected to

be complete at the end of FY2014

> Next phase of programme will focus on Whakamaru

rehabilitation

> Geothermal reinvestment capital expenditure is lumpy

as the sustainable resource is managed

> dynamic system in which we manage around 200 wells

> On-going requirement for make-up wells

> released drilling rig in September on completion of

Kawerau wells

> completion of almost ten years of continuous drillingOPERATIONS

Market Dynamics

> Operate in a highly competitive and well-functioning market that has led to world-best outcomes

> for security, level of renewables and resilience to future fuel shocks

> Our portfolio well positioned for demand-supply dynamics

> current excess capacity, reflecting flat demand and increased renewable generation

> potential for future reductions in excess capacity, as more flexible take-or-pay requirements lead to further

response from fossil fuel generators

> Inherent portfolio advantages means greater earnings surety under most market conditions,

including weak hydro conditions

> Centralised management of wholesale price risk and optimising value across integrated portfolioRetail Capital Markets Day Presented by: Matthew Olde Bryan Dobson Luke Blincoe Acting General Manager Sales, Marketing and Service GM Bosco Connect Retail Manager and GLO-BUG

RETAIL

Retail

> Retail responsible for:

> Marketing and selling electricity to residential and business customers through Mighty River Power’s

consumer brands (Mercury Energy, GLO-BUG, Bosco Connect and Tiny Mighty Power)

> Managing customer segmentation and mix to maximise valueRETAIL

Retail

FPVV BUSINESS AND RESIDENTIAL SALES

6,000

MIGHTY RIVER POWER RETAIL ELECTRICITY

5,000

CUSTOMERS BY BRAND (FY13)

4,000

GWh

3,000

2,000

1,000

-

GLO‐BUG FY09 FY10 FY11 FY12 FY13 FY14 PFI

Mercury

Other Tiny Mighty 16,956 Business Residential

Energy Power

44,504

349,833 16,567 MARKET SHARE OF NATIONAL DEMAND

Bosco

(EXCL TIWAI)

Connect

10,981 40,000

30,000 18% 19% 21% 21% 21% 22%

GWh

20,000

10,000

(note: excludes gas customers) -

FY08 FY09 FY10 FY11 FY12 FY13

Rest of Market excl Tiwai MRP Sales volumes

Source – Transpower information exchange, MRP dataRETAIL

Competitive Landscape

> Retail competition a key focus for the Electricity Authority (EA):

> What’s My Number campaign impact

> increased liquidity in hedge markets, reduction of basis risk through transmission investment allowing more

flexibility in retailer portfolio mix, and model use of systems agreements

> EA currently reviewing options to reduce participant prudential requirements and further increase consumers’

propensity to compare and switch retailers

> High security margins drive elevated competition levels

CUSTOMER ELECTRICITY SWITCHING RATES BY MARKET

30%

% of annual customer churn

25%

20%

15%

10%

5%

0%

2010 2011 2012

Source – VaasaETTRETAIL

Competitive Landscape

> Mass market switching activity approaching the 2011 peak, especially in Auckland

> Despite being over-represented in Auckland (68% of Mighty River Power customers Auckland-based), retail

book churning below market average

> Grew mass market volume since FY08 ahead of increase in retail competition backed by additional

generation capacity

RESIDENTIAL CUSTOMER SWITCHING IN AUCKLAND MIGHTY RIVER POWER ICPS &

& NZ SHARE OF CONSUMPTION

25% 450

24%

400

350 22%

20%

MRP Market Share %

300 20%

ICP's (000's)

15% 250 18%

200

16%

10% 150

14%

100

5% 50 12%

- 10%

0% FY08 FY09 FY10 FY11 FY12 FY13

Jan-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

May-11

Jul-11

Sep-11

Nov-11

Jan-12

May-12

Jul-12

Sep-12

Nov-12

Jan-13

May-13

Mar-10

Mar-11

Mar-12

Mar-13

Non Auckland

Auckland

AKL Market Churn NZ Market Churn Share of NZ Consumption (excl. Tiwai)

Mercury AKL Churn Mercury NZ Churn

Source: Electricity AuthorityRETAIL

Mass Market Pricing

> Headwinds in mass market pricing due to the supply / demand balance and increased competition

> Headline prices not reflective of offers and discounts offered in the market

> Lines and transmission charges typically make up 40% of end prices

AVERAGE DOMESTIC ENERGY PRICE BY PROPORTION OF MERCURY CUSTOMERS

RETAILER FOR NZ: 2006 - 2013 ON HEADLINE PRICING

2009

18 3%

17

16

15

c/kWh

14 97%

13

12 2013

11

10

May-06 May-07 May-08 May-09 May-10 May-11 May-12 May-13 39%

Contact Energy Genesis Energy

Mercury Energy Meridian Energy

61%

TrustPower Contact Energy Online OnTime

TrustPower Friends Extra

Source: Ministry of Business, Innovation & Employment & MRP Analysis

Non Standard Pricing Headline PricingRETAIL

Contract Market

> Increased market activity evident in the commercial contract and CFD markets

> Successful in increasing commercial book in 2012 before ASX markets fell. Average contract tenure 2.8

years

> Successfully contracted volume ahead of Ngatamariki commissioning

> Recent market pricing not aligned with Company view of return for risk

COMMERCIAL FPVV SALES VOLUMES & PRICING

10.5 800

10.0 700

9.5

600

9.0

Gwh per quarter

500

c / kWh

8.5

400

8.0

300

7.5

200

7.0

6.5 100

6.0 0

Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13

MRP FPVV Commercial Sales Volumes Energy Link FPVV Index ASX OTA

Source – Energy Link, ASX, MRP dataRETAIL

Cost Management

> Whilst acquisition costs correlate to the level of switching activity, underlying OPEX continues to be

actively managed, partially mitigating the cost of increased churn

> Reductions in underlying costs reflect process efficiencies in billing, credit and service functions

RETAIL OPERATING COSTS

100% 25%

90%

% of FY09 Operating & Direct Cost Base

80% 20%

70%

60% 15%

% Churn

50%

40% 10%

30%

20% 5%

10%

0% 0%

FY09 FY10 FY11 FY12 FY13

Acquistion Costs Servicing Costs Mercury Churn %RETAIL

Debt Management and Disconnections

> A sustained focus on credit assessment, WRITE-OFF COST PER ICP (2012)

80

collection efficacy and leveraging prepay

Average write-off per ICP

is resulting in lower bad debt write-offs 60

than industry

40

> Guiding principles for debt management

20

focus on early intervention and

appropriate payment solutions 0

> Mercury disconnection rates are falling

Source – Veda, Electricity Authority

CREDIT PERFORMANCE

0.40% 0.70%

0.35% 0.60%

Net debt write off rate

Disconnection rate

0.30%

0.50%

0.25%

0.40%

0.20%

0.30%

0.15%

0.20%

0.10%

0.05% 0.10%

- 0.00%

FY09 FY10 FY11 FY12 FY13

Net debt write-offs as a % of revenue Arrears disconnection rate - Mighty River

Arrears disconnection rate - Industry

Source – Electricity Authority, MRP dataRETAIL

Consumer Brands

> A multi-brand strategy enables a tailored customer experience and cost efficiency

Brand Established Customers Description Service Experience

1993 350,000 • Mass market, multi‐ • Full‐service call centre

segment • Comprehensive online service suite

• Scale operation • Multiple communication channels

• Increased use of online and email channels for both

marketing and service

2006 10,000 • CBD apartments • Concentrates on low‐cost service channels

• Low cost operating • Delivers better value to both customer and retailer as a

model for low result

consumption, high

turnover segment

2008 17,000 • Smart meter prepay • Online and app‐based self‐service, pay‐service call centre

product available

• Pay‐as‐you‐go • Uses technology including in‐home display and

budget management smartphones to deliver more control to the customer

service • Eliminates credit management cost

2009 17,000 • Regional towns • Full‐service decentralised call centre

• Local presence, • Regional, personalised service proposition

community

engagementRETAIL

GLO-BUG

> GLO-BUG is a smart meter and cloud hosted prepay solution that provides

a range of tools (IHD, smart phone apps, web) to help customers manage

their energy account more easily

> Delivers a socially responsible solution by reducing the total cost of energy

for most credit distressed customers through avoided fees associated with

late payment behaviour

> on average a customer migrating from Mercury to GLO-BUG reduces their total

cost of energy by around $300 on average

> GLO-BUG well positioned to benefit from wider use of credit checking;

Meridian and Mercury refer credit distressed and credit check fail

customers to GLO-BUG

> Recognised industry solution

> transfer of Meridian prepay customer base

> won the Innovation Award at the Deloitte Energy Excellence Awards in 2012

GLO-BUG CUSTOMERS

20,000

16,000

12,000

ICPs

8,000

Includes transfer of Meridian

4,000 prepay customers

-

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13RETAIL

Tiny Mighty Power

> Distributed contact centre in selected towns enables lower operating costs and more effective

engagement through community presence (e.g. Schools programme)

> Sustained local presence enables higher market penetration (in the towns) than could be achieved

with the traditional retail approach of one-off acquisition campaign

Area (Market Entry) Market Share %

TINY MIGHTY ICPS

Marlborough (Sep 10) 15.7%

18,000 Whakatane (Jul 12) 14.6%

Waipa (Nov 09) 13.4%

16,000

Wairarapa (Aug 10) 10.7%

14,000 Thames Valley (Sep 10) 3.3%

12,000 Rotorua (Jan 13) 1.2%

Taupo (Jan 13) 1.0%

10,000

ICPs

8,000

6,000

4,000

2,000

-

Nov-09

May-10

Jul-10

Sep-10

Nov-10

May-11

Jul-11

Sep-11

Nov-11

May-12

Jul-12

Sep-12

Nov-12

May-13

Jul-13

Mar-10

Mar-11

Mar-12

Mar-13

Jan-10

Jan-11

Jan-12

Jan-13

Source: Electricity AuthorityRETAIL

Innovation

> Focused on strengthening customer

relationship beyond basic electricity supply: MERCURY ENERGY RESIDENTIAL PRODUCT

> 43k dual fuel customers (since April 2002) PENETRATION

100%

> 35k Star Supporter Club members

donating $850k p.a. to Starship via monthly 90%

bill (since May 2004) 80%

> 36k Mercury Perks members receive 70%

entertainment, travel, food and wine 60%

discounts (since April 2010)

50%

> 95k residential customers on fixed price 40%

contracts (since November 2010)

30%

> 65k GEM users to date, incl. >60% repeat

20%

users (since March 2013)

10%

0%

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13

Electricity only 2 products 3 products 4+ products *

* Products include: Dual Fuel, Fixed Price Contracts, Mercury Perks, Star Supporters Club, Active

GEM usersRETAIL

Innovation

> The Good Energy Monitor (GEM) is delivering increased customer engagement

> Active GEM users display higher level of satisfaction and lower likelihood to switch

CUSTOMER PERCEPTIONS SINCE LAUNCH OF GEM

60%

% of Mercury customers that agree

50%

40%

30%

20%

10%

0%

Innovative and Save energy Leading the way Comes up with Offers Appeals to you Takes away the

Progressive and money new ideas something more hassle

different

Feb-13 Jun-13

Source: Colmar BruntonRETAIL Demo of GEM live $#

Metrix Capital Markets Day Presented by Matthew Olde Tim O’Halloran GM Business Strategy & Solutions GM Metrix

METRIX Introduction > Technology Business > Advanced Metering Infrastructure (AMI) and Services

METRIX

Business model

> Three key components underpin a flexible business model

> buy and deploy AMI or leverage third party AMI

> operate AMI control systems and manage rich information

> deliver AMI services and field services for retailers or their agents

AMI TECHNOLOGY METRIX SYSTEMS CUSTOMERS

P2P AMI

Retailers

Retailers Service

Integration

Distribution

Collector

networks

Field Services

Mesh AMIMETRIX

Client base

> Increased electricity retailer ICP churn provides opportunities for increased deployment

CLIENT BASE JUNE 2013

Contact 13%

Meridian

7%

Glo-Bug Powershop 4%

7%

Other 11% Genesis 3%

Mercury 61% Other 3%

Bosco 1%METRIX

Enabling retailer propositions

> AMI propositions are now coming to life

> Mercury - Good Energy Monitor

> GLO-BUG Prepay/GLO-BUG and IPHONE

> Powershop

> Contact EnergyMETRIX

The AMI market in Auckland

> Metrix has a long heritage in New Zealand’s biggest retail/residential market

> Now 85% deployed with AMI

> Metrix holds 70% market share

> Ongoing deployment programme in Auckland

AUCKLAND AMI METERING MARKETS JUNE 2013

Metrix AMI

AMS AMI

LegacyMETRIX

AMI market nationally

Market structure

> Rollout of AMI is driving market consolidation in electricity metering

> Three AMI providers now deployed 50% AMI

> Retailer-led model

> Beginning to see maturity in service interoperability among the three AMI providers

JUNE 2013

Metrix AMI, 329

Legacy upgrade assigned,

577

Other, 1043

AMS AMI , 505

Legacy upgrade

uncommitted , 466

Arc AMI , 135METRIX

The AMI market nationally

Operating environment

> Expect stabilisation following recent, extensive

changes to the electricity metering regulations

> Significant investment in systems interface

with the Electricity Registry completed

> Compliance deadline of 1 April 2015 rapidly

approaching for Category 1 metering

installations

> all metering installations up to 3-phase 100

Amps require full certification

> Elevated levels of Electricity ICP churnMETRIX Operating statistics > $101m of capital expenditure over the last five financial years > EBITDA doubled from FY2009 to FY2013 Year ended 30 June FY2013 FY2012 FY2011 FY2010 FY2009 Capital Expenditure ($m) 8.4 16.6 33.0 25.8 17.1 AMI 314,586 281,340 240,586 120,877 35,104 Legacy Meters 58,663 84,405 121,726 192,213 279,119 Legacy Meters – 3 phase 23,908 25,673 33,005 33,296 32,542 Load Control (hot water) 270,332 268,163 252,380 227,504 226,239 Pre‐pay 13,586 14,679 15,198 14,765 12,095 Total Assets 681,075 674,260 662,895 588,655 585,099

METRIX

Growth opportunity

Expansion activity

> Deploying AMI into new regions for Mighty River Power

consumer brands

> Providing exclusive AMI services on the Counties Power

network

> Further AMI opportunities available in the market

Capital investment

> Future capex spend depending on growth opportunities

around $20m - $40m p.a.

> PFI FY14 forecast was $12.8m

> Revenues flow immediately following deploymentDevelopment Capital Markets Day Presenters: Mark Trigg Samuel Moore Dennis Radich GM Development Manager Strategy & Planning Generation Development Manager

DEVELOPMENT

A significant role in both of the Company’s core business strategies

> Maximising the value of the existing business

> Technical Resources Team (Rotorua) provides specialist

technical services to Operations through Geoscience;

Reservoir Engineering; Asset Management; Well Services;

Chemistry

> Securing economically attractive development options

> Business Development Team (Auckland based)

> Chilean operations and development team (Santiago based)DEVELOPMENT

The trend in the domestic market required an adjustment to strategy

> Reset the level of domestic activity

> maintain a small number of long-dated options with sufficient diversity of scale, fuel type and technology

> align the resourcing to match the reduced activity levels

> consider the optimal configuration of existing gas generation

> Increase our focus on existing investments in offshore jurisdictions

> removed the intermediary between the Company and its offshore investments in Chile and California,

enabling significantly greater direct management involvement

> fully controlled entity in Chile

> Board representation, management and technical collaboration in EnergySource (California)DEVELOPMENT

Domestic activity curtailed consistent with demand requirements

> Small focused number of

opportunities being maintained

> wind and geothermal preferred

> Other lesser opportunities

abandoned

> Lower touch/lower cost approach as

we await market recovery

> Significant reductions in resourcing

undertaken or planned

> headcount peaked at circa 150

(inclusive of Chile) during

Ngatamariki construction

> trending towards 90

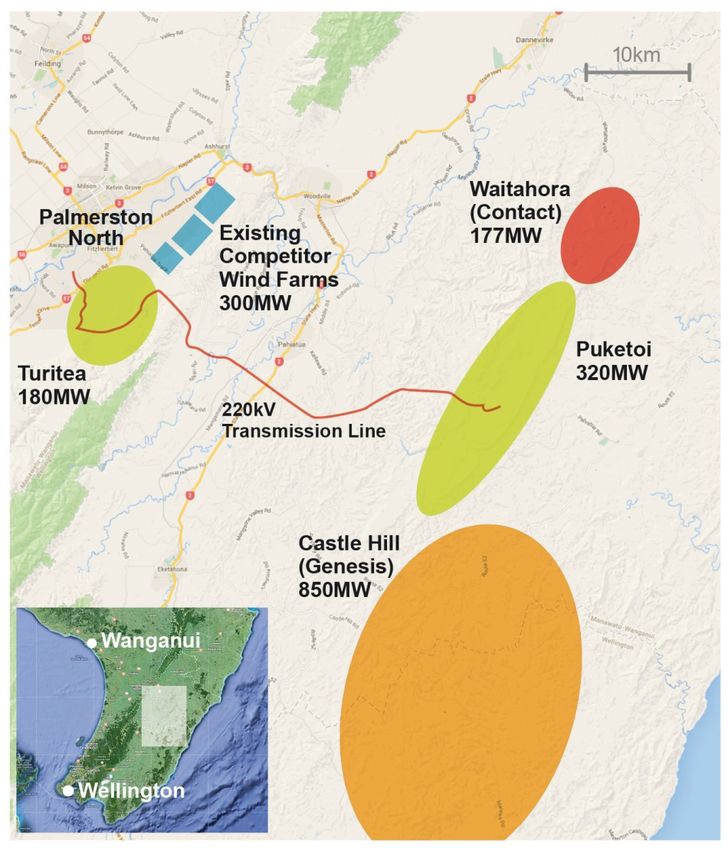

> 2/3 in technical resourcesDEVELOPMENT A strong position in wind has been created > Two very high quality, consented Class 1 (high wind speed) sites South East of Palmerston North > Fully consented 220kV transmission line route to link projects to the Transpower grid > Transmission line consent large enough to accommodate all four wind projects in the area (note Waitahora & Castle Hill consented without transmission) > Staged execution options to meet market opportunities > Also a third (earlier stage) Class 1 site, Cape Campbell, in Marlborough with long-term development rights

DEVELOPMENT

Offshore an opportunity to leverage niche capabilities and create a new growth channel

> The Company has, during the 10 year period of domestic development, built up institutional

knowledge in

> geothermal risk assessment

> development capability

> technical resource capability

> geothermal operations

> The small size of the global geothermal market created opportunity to leverage that strategic

advantage not held in any other fuel sources

> Additional risks in new jurisdictions offset by diversifying existing risks

> soft domestic market with increased regulatory uncertainty

> long term domestic contract price uncertainty

> Route to maintain institutional knowledge in absence of new domestic opportunity

> Consider the programme as a continuous one, not bounded by geography per se

> US-based John L Featherstone plant (HR1) in commercial operation prior to completion of Ngatamariki,

first evidence of that transition

> further Salton Sea (US) development seen as next most likely projectDEVELOPMENT

After five years we have created a platform from which we can control future

direction

> Created the opportunity to consider a number of development options via GeoGlobal Energy (GGE)

that would have been inaccessible otherwise

> Have direct control of those investment opportunities we elected to pursue

> direct investment in EnergySource with a preferred position in John L Featherstone plant

> direct ownership of Chilean entity and resource rights

> financial interest in German assets currently under management control of GGE, but including a repurchase

option (nominal cost) should certain financial criteria not be met by GGE

> Transformed the structure of original investment (designed to meet SOE constraints) to enable

direct management and control

> absorbed the management of the assets / investments into our own development structure with significantly

reduced cost

> closer alignment of incentives between partners

> leverage of existing resources and systems that successfully delivered the domestic programme over the

past decade

> apply patient approach to development as required with full control over capital allocation decisionsDEVELOPMENT

Investment in John L Featherstone has already paid dividends

> Initial USD92m investment

> 20% holding in EnergySource

> preferred equity interest in John L

Featherstone Plant

> post construction refinancing led to lump

sum distribution of USD118m

> Post tax cash flow returns influenced by “flip”

dates

> circa USD1m until tax equity flip forecast in

late 2017

> circa USD4.5m from then until MRP

“preferred” return completed in 2021

> circa USD2m thereafter

> Resourcing

> EnergySource has operational and

development teams based in San Diego

and Salton Sea

> hold one (of three) board seats

> interaction at management and technical

levels giving direct access to information

> Hudson Ranch II

> EnergySource has PPA for a further project

> has additional landDEVELOPMENT

Salton Sea represents a significant opportunity

> Field

> Cal Energy has operated 10 plants with 327MWe US GEOTHERMAL FIELD BY RUNNING

net (340MWe gross) since 2000 CAPACITY

> no make-up wells required to support pressure Geysers

decline (small number due to well condition) Salton Sea

> State Coso

Running capacity

Heber

> ongoing significant retirements of gas plant due to Steamboat

restrictions on ‘Once Through Cooling’ East Mesa

> San Onofre (2200MW nuclear) closure Dixie Valley Additional

resource

> geothermal baseload characteristics / benefits are Blue Mountain

potential

starting to be recognised in context of large Roosvelt

amount of intermittent renewables Puna

> But we are mindful of 0 500 1,000 1,500

MW

> Californian utilities near the 20% Renewable

Portfolio Standards requirements but some way to

Source: Running Capacity: International Geothermal Assn

go to reach 33% requirement by 2020 Database

> longevity of federal tax incentives always Additional resource potential: Western Governors'

uncertain Association Geothermal Task Force Report, Jan 2006

> Future

> Mighty River Power elected not to exercise its option to increase its stake to 33% - value based decision

> discussions are ongoing with partners about alternative mechanisms by which we may increase our

participation

> access to greater acreage of development land would enable participation in huge potential of fieldDEVELOPMENT

Chile overview

Geothermal potential PUCHULDIZA

> Large number of geothermal fields throughout Chile

> Mighty River Power has direct ownership of two of the top

concessions:

> Tolhuaca (central Chile)

> Puchuldiza (northern Chile)

Market potential

SANTIAGO

> Strong growth economy (resources driven)

> Strong electricity demand growth

> Recognized electricity supply challenges TOLHUACA

> Politically stable

> Good regulatory regime and established institutions

> Deep and sophisticated capital markets for infrastructure

investment

> Long term attractive outlookDEVELOPMENT

Chile is a strong demand growth market

TOTAL ELECTRICITY DEMAND

> Average historical electricity demand growth

70,000

rate of >6% p.a.

60,000 1990‐2011 CAGR: 6.4%

> Demand driven both by commodity export 50,000

sector and increasingly by domestic demand 40,000

GWh

(middle class expansion from 1990) 30,000

> Two contracting markets for generators to sell 20,000

10,000

into:

0

> Regulated client (distributor/retailers) tender 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

market

Source: Chilean Ministry for Energy

> “Free client” market for bilateral contracts with

large end users >2MW TOTAL SIC NETWORK GENERATION

60,000

50,000

40,000

GWh 30,000

20,000

10,000

0

Hydro Thermal Other

Source: CDEC‐SICDEVELOPMENT

Supply challenges driving favourable price outlook

SIC SPOT PRICES

> Chile imports about 75% of its total primary

energy supply 400

350

> Beginning in 2004, Argentina curtailed

300

exports of natural gas to Chile 250

US$/MWh

> Base load generation historically dominated 200

by coal and hydro 150

100

> Energy price outlook reflects likely 50

dependence on imported LNG for new 0

(CCGT) capacity 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

> growing opposition to new coal & hydro Spot price at Temuco 220kV node

> some gas-fired plants converted to liquid Source: CDEC‐SIC

fuels REGULATED CLIENT DEMAND

> LNG import capacity constrained 50,000

> Renewables targets increasing* from 10% 40,000

to 20% by 2025

30,000

> Non-conventional renewable energy credits

GWh

available for geothermal generation 20,000

> Generators are paid a firm capacity charge 10,000

for being available

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Contracted volume Regulated client demand

* Passed by Senate; now back with Congress

Source: CNEDEVELOPMENT

World geothermal players are active in Chile

> Large number of exploration concessions have been granted

> Some of world’s largest geothermal companies are present

> All attempting to solve similar issues of bridging geothermal potential with market opportunity

> Starting to see consolidation and exit over time of more speculative resource holders

> Potential for further consolidation of industry as experienced developers optimise portfolios and

speculators exit

> Mighty River Power’s current focus

> de-risking project execution through commercial partnerships

> revenue security (e.g. PPA)

> deepening understanding of resource position

> sizing the local platform to near term activity levelsDEVELOPMENT

Successful geothermal development requires recognition that -

> Patience is necessary

> Successful partnerships require alignment of incentives and preferably

> complementary strategic capabilities

> robust financial capacity of each partner

> Scale becomes valuable to spread technical platform costs

> Risk diversification is valuable

> through multiple fields for resource diversity

> different jurisdictions enable regulatory and pricing risk diversity

> A detailed understanding of market dynamics is important

> a core strength in our home market

> a key strategic capability sought in partners for other jurisdictions

> Staged development is a rational response to long-term resource uncertainty

> Overheads need to be managed through the development cycle2 October 2013 Capital Management Capital Markets Day Presented by: William Meek Tim Thompson Chief Financial Officer Treasury Manager

CAPITAL MANAGEMENT

Capital Structure

Disciplined approach to capital allocation

> Balance sheet consistent with a stand alone

credit profile of ‘bbb’ by S&P (or equivalent)1

> Dividend policy targets dividend yield attractive

to shareholders while cognisant of a sustainable

financial structure

> working capital requirements

> the medium term asset investment programme

> short to medium term risks on earnings

> Focus on maintaining an appropriate portfolio of

high quality investment opportunities

> evaluate against all competing uses for cash

> Capital management is addressed on an on-

going basis by management and the Board

1. Mighty River Power’s BBB+ corporate credit rating reflects S&P’s view that in the

event of financial distress there is a “moderate” likelihood of the New Zealand

Capital

sovereign management

providing as normal

extraordinary support to ensurebusiness

the company’s financial

obligations are met in a timely manner.

practice

2. Free Cash Flow defined as Operating Cash Flow after interest paid and tax less

reinvestment capexCAPITAL MANAGEMENT

Capital Allocation

> FY2014 forecasts reflect full year cash flow

contribution from Ngatamariki

> FY2014 Capex forecast reduced relative to

PFI to be in the range of $125m to $175m

> FY14 PFI forecasts dividend of $182m (13

cents per share)

> forecast Payout 107% of adjusted Net Profit

and 71% of Free Cash Flow

> gross yield circa 8% (fully imputed)

> Modest deleveraging forecast if capex at

low end of forecast range

> On-going focus on sustainable earnings

looking forward driven by:

> normalisation of generation output (average

hydro, full year of Ngatamariki)

> improvements in business wide

effectiveness and efficiency

* Other cash flows from investing and financing activities as disclosed in

Mighty River Powers FY2013 financial results and prospectusCAPITAL MANAGEMENT

Balance sheet management

> Mix of short and long term funding

DEBT MATURITY PROFILE AS AT 30 JUNE

> weighted average maturity exceeding 5 years

350

> $300m of new facilities arranged in FY2013

($200m of bank and $100m of domestic 300

wholesale bonds)

> no maturing facilities in FY2014 (excluding CP) 250

> option to convert RCAF into longer term debt

200

> Liquidity

$m

> $475m of committed but unutilised bank 150

facilities

> $100m of commercial paper outstanding 100

> Cost of Funds

50

> cost of funds likely to remain at current levels

until 2018 due to long term hedging undertaken

0

in 2008 prior to ramp in capex/debt to support

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

geothermal development programme

Financial Years

Drawn Undrawn1

375 100 125 550 260

Facility Type ($m)

RCAF - Undrawn RCAF - Undrawn: CP Cover

1. $100m of outstanding commercial paper deducted from undrawn debt

RCAF - Drawn Wholesale Bonds

2. USD proceeds fully swapped to NZD via cross currency swaps

US Private Placement22CAPITAL MANAGEMENT

Balance sheet management

Cost of Funds INTEREST RATE HEDGING

1400 8.0%

> Term funding and interest rate hedging (swaps)

undertaken prior to undertaking geothermal

7.0%

development programme 1200

> reduce funding and liquidity risk and provide

cash flow certainty in the medium term 6.0%

1000

> most swaps not hedge accounted currently so

Swap Rate (%)

fair value movements recognised through P&L 5.0%

800

> to reduce P&L volatility accounting policy now

$m

requires all new hedges to be hedge accounted 4.0%

> The significant fall in interest rates in NZ (and 600

3.0%

globally) post 2008 has resulted in these

hedges being out of the money 400

2.0%

> FY2013 fair value benefit of $25.6 million

> FY2012 fair value cost of $92.8 million 200

1.0%

> Debt re-financing has negligible impact on cost

of funds excepting credit spread which is largely 0 0.0%

driven by debt market and term

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

> Cost of funds will be higher than benchmark

funding rates until hedges expire in 2018

Debt 10yr IRS (Annual Average)CAPITAL MANAGEMENT

Capital expenditure

> $1.4b invested in geothermal domestically since CAPITAL EXPENDITURE

2006 450

> cumulative revaluations of new geothermal

assets exceed $0.5b at 30 June 2013 400

> Lower capital expenditure forecast on a go 350

42

14

forward basis reflecting no large scale domestic

generation development programme 300

> FY2014F capital expenditure reduced to $125m 38

250 10

- $175m (PFI: $199.1m)

$m

274

> Reinvestment capex $72m (2 new wells at 200 280 44

Kawerau and on-going hydro lifecycle

refurbishment) 150 173 50

225

> $13m for Ngatamariki carried forward from 119

100 53

FY2013

> other capex includes AMI 50

66 74 69 72

> contingent provision capex largely relates to 57

26

offshore geothermal, discussing alternatives at 0

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014F

Energy Source

Potential other new investment Other new investment

Geothermal ReinvestmentCAPITAL MANAGEMENT

Capital Structure

> Mighty River Power Board is committed to maintaining a ‘bbb’ stand alone credit profile

> S&P favour the use of cash flow metrics to assess the financial risk profile of the company

> key comparative measures for Mighty River Power and it’s peers are Funds from Operations (FFO) coverage

and leverage metrics

FFO / DEBT* FFO INTEREST COVERAGE*

50% 7.0

45% 6.5

FFO Interest Coverage (x)

40% 6.0

FFO / debt (%)

35% 5.5

30% 5.0

25% 4.5

20% 4.0

15% 3.5

10% 3.0

2008

2009

2010

2011

2012

2013

2014

2008

2009

2010

2011

2012

2013

2014

Financial Years Financial Years

Mighty River Power Contact Meridian Genesis Mighty River Power Contact Meridian Genesis

> Mighty River Power metrics presently tighter than competitors

> Key credit metrics expected to improve in FY14 due to lift in earnings from removal of one-

off costs and commissioning of Ngatamariki

*Calculated using S&P existing criteria and metric definitions

Source: S&P Credit Reports and Mighty River Power calculations based on publicly available informationCAPITAL MANAGEMENT

Credit criteria

> S&P is currently reviewing the criteria for rating corporate industrial companies and utilities

> stated rationale being to make the ratings process more transparent and comparable across industries and

jurisdictions

> Criteria for intermediate risk, standard volatility unchanged from 2009 core ratios but S&P specifics

to NZ generators historically lower than published ratio bands

> FFO/debt: 30-45%, Debt/EBITDA: 2-3x

> we believe S&P are potentially seeking to pre-empt impacts on ratios when interest rates rise given

currently record low rates globally

> S&P have indicated that the new criteria will likely be in place from the start of calendar year 2014

> consultation was concluded in September 2013

> S&P have indicated that 10% of credits will likely be affected .

> the likelihood of upgrades and downgrades across all S&P credits has been assessed as equal by S&PCAPITAL MANAGEMENT

Sustainable earnings focus

> Weak demand and supply conditions means the company has moved from growth phase to consolidation phase

> potential for demand/supply surprises particularly on supply side reflecting thermal response

> FY2014 EBITDAF guidance confirmed at PFI levels

> generation down over 260GWh against expected levels in Q1 FY2014

> Ngatamariki commissioned and handed over. Generation over Q1FY2014 similar to forecast but income

recognition two months later than expected

> improved LWAP/GWAP ratio due to peakier hydro profile and NIGUP improving location factor between

generation and Auckland.

> FY2014 PFI operating expenditure of $250.5 million

> FY2013 operating expenditure at $318.7 million included $68.7 million one-off IPO and international

geothermal related costs - $250.0 million

> FY2012 operating expenditure of $264.4 million included $10.0 million one off costs - $254.4 million

> Capital markets insights coupled with review processes have identified focus areas to drive sustainable earnings

> in Q4 FY2013 saw $18.4 million savings –two thirds of which are permanent savings

> Group-wide efficiency and effectiveness programme underway to deliver sustainable benefits through time

> rationalisation of suppliers, centre led procurement

> right sizing business for current market environment and activity levels

> consolidation of support servicesCAPITAL MARKETS DAY

Capital management considerations

> Sustained level of elevated reinvestment capital planned – c$10m p.a over rest of the decade

> A lower requirement for domestic growth capex exists but capital required over medium term to

advance international geothermal

> Clarity required around new S&P credit criteria connected to sustainable financial structure

> A number of capital management options exist in absence of growth investments

> change to ordinary dividend: Policy needs to be sustainable and cognisant of rating, working capital

requirements, the medium term asset investment programme and earnings volatility

> special dividend: one-off return of excess capital but cognisant of the above, unimputed if large

> share buy-back: would need to be in the best interests of the company and shareholders

> Dividend policy

> policy expressed as 90% - 110% of adjusted profits cognisant of a sustainable financial structure, working

capital requirements, the medium term asset investment programme and short to medium term risks on

earnings

> FY2014F dividend declared of 13 cents/share. Forecast to be fully imputed –a further 3 cents worth of

imputation credits available as at the end of FY2014

> 71% of free cash flow (FY2013 pay-out was 78% of FCF)

> Capital management outcomes will be announced at ASM (7 November 2013)You can also read