Northeast Gas Association 2014 Sales and Marketing Conference Government Initiatives on Natural Gas Expansion - March 14, 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Northeast Gas Association

2014 Sales and Marketing Conference

Government Initiatives

on Natural Gas Expansion

March 14, 2014

State Agencies Involved throughout Gas Expansion Process

Market, Challenges, Policies and

Implementation

Potential Benefits Costs Programs

• Market studies • Customer • Financing • Planning

conversion costs

• Economic • Incentives • Reporting

benefits • Regulatory requirements

policies • Rate design

• Environmental

benefits • Investment

• Economic • Gas supply and

development pipeline capacity

2

Example – Massachusetts Department of Energy Resources

Gas distribution

expansion study

Opportunities

Challenges & barriers

Strategies, policy

options,

rate/regulatory

models

Economic and

environmental

analysis

Collaborative

stakeholder process

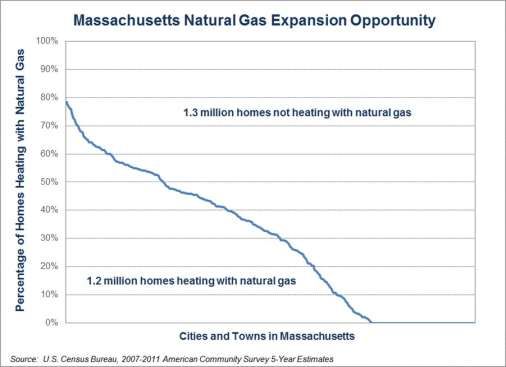

31. Define Market Potential

By regions

Communities

By access

On-main

Off-main

New communities

By end user

Residential

Commercial

Industrial

http://www.rural.palegislature.us/documents/reports/Natural-Gas-Infrastructure-SR29.pdf

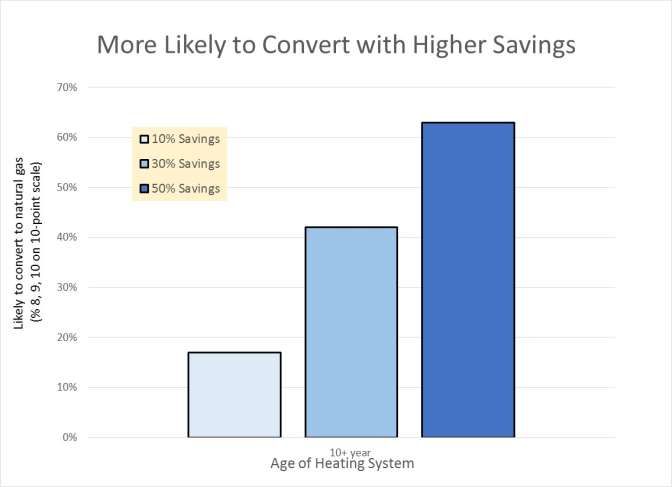

41. Identify Customer Interest

DOER study, 2nd stakeholder meeting

51. Quantify Potential Benefits

Fuel savings

Pennsylvania

• Fuel savings of approximately $1,500/year for converting customers;

• $15.2 million/year of additional GDP; and

• $7.1 million/year of disposable personal income injected into the state economy.

Environmental benefits

Reduce carbon emissions

Economic development

Pennsylvania

• 3,100 additional job-years from 2014 through 2040.

Energy efficiency

62. Identify Challenges to Achieve Benefits

Customer challenges

Upfront cost

• New heating system

• Contributions (CIAC)

Conversion process

• Can be cumbersome

LDC challenges

Policies that prohibit cross-subsidies

Gas supply and capacity constraints

Other challenges

Permits

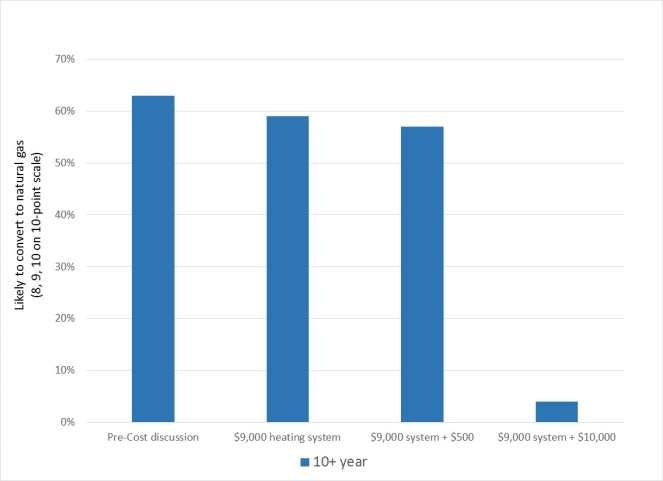

72. Upfront Cost is a Challenge for Off-Main Projects

DOER study, 2nd stakeholder meeting

83. Develop Policies and Programs – Setting a Framework

High

Upfront

Cost

Low High

Access to Natural Gas

93. Develop Policies and Programs – Estimating Impacts

DOER study, 2nd stakeholder meeting

103. Policies and Programs: Financing

Lower upfront cost through financing

No- or low-interest financing options

Financing of equipment costs and/or the CIAC

Repayment through the utility (on-bill repayment), or a third-party bank (loans)

Market

Primarily On-Main

Example

Southwest Gas offers a Residential Amortization Program, which allows customers to

pay their CIAC interest-free through an on-bill surcharge. This type of financing is

similar to zone rates.

Many utilities partner with third-party banks to provide low-interest loans for

equipment purchases, such as the HEAT Loan Program in Massachusetts, which

focuses on high energy efficiency boilers and heaters.

113. Policies and Programs (cont.): Financial Incentives

Lower upfront cost through incentives

Rebates, grants, and tax credits

Funding sources from utilities and government agencies

Market

Primarily On-Main

Example

Puget Sound Energy offers up to $3,550 in incentives for customers switching from

the utility’s electric service to the natural gas heating service, along with additional

rebates (up to $800) for installing higher energy efficient equipment.

The conversion incentive amount can be applied to the equipment and installation,

but is limited to 75% of the total cost.

123. Policies and Programs (cont.): Free Service Lines

Lower upfront cost through free service lines

Market

Primarily On-Main

Promotes the connection of Low-Use customers, which increases the likelihood of

that customer’s future conversion to natural gas.

Example

Many; according to AGA study, at least 49 utilities

133. Policies and Programs (cont.): Low-Cost Bonds and Grants

Lower cost of expansion through financial support

in areas where capital is limited or unwilling to invest

Market

Off-Main

Example - North Carolina

LDCs in North Carolina have used $200 million in natural gas bond funds (in addition

to $115 million in expansion funds paid for by all gas customer in the state) to expand

access to the natural gas system in rural parts of the state.

These funds were used to expand service to 31 counties, increasing the total number

of counties in the state with access to 96 (out of 100).

Other States where Implemented or Proposed

ME, NC, PA

143. Policies and Programs (cont.): Zone Rates

Lower upfront cost by spreading expansion costs over a pool of new

customers, and recovering costs over a longer period of time through a rate

surcharge on new customers

Market

Primarily Off-Main

Illustrative Example

Florida Public Utilities Company (“FPUC”) has increased its customer base by nearly

20% since implementing zone rates in 1995.

FPUC’s Area Expansion Program allows new customers that are part of an expansion

project to pay a $5.00 per dekatherm surcharge for 10 years.

Other States where Implemented or Proposed

CT, DE, FL, MN, NY, PA, UT

153. Policies and Programs (cont.): Blended Rate

Lower upfront cost by spreading expansion costs over all customers, and

recovering costs over a longer period of time through a rate surcharge on all

customers

Recognizes the importance of having access to natural gas

Market

Primarily Off-Main

Example

AGL Resources’ Strategic Infrastructure Development and Enhancement (STRIDE)

program in Georgia allows the utility to invest $400 million over ten years in

infrastructure improvements, including expansion to meet forecasted growth.

This program was merged with the company’s existing Pipeline Replacement

Program (which was initiated in 1998) to ease implementation.

Other States where Implemented or Proposed

CT, GA, MN, MS, NC, NE, TX, VT

163. Policies and Programs (cont.): Illustrative Summary

174. Monitor and Track Implementation

Market

Potential

Planning

&

Reporting

Policies and Results

Programs

18Thank You!

Tim Lyons

Partner

Sussex Economic Advisors

802-497-0761

802-598-1651

tlyons@Sussex-advisors.com

19About Sussex

Sussex Economic Advisors, LLC is a management and economic

advisory firm providing consulting services to regulated industries such

as natural gas, electricity, water, and thermal energy distribution.

The firm’s Partners have held senior positions in utility companies, competitive

energy suppliers, management consulting firms, and business-focused

academic institutions.

Our Consulting Staff, Executive Advisors, and Affiliated Experts have

substantial experience and training in matters relating to regulatory strategy

and policy development, gas supply planning and capacity portfolio optimizing,

energy market analysis and assessments, financial and economic analysis,

rate proceedings and regulatory compliance, due diligence and valuation, and

management reviews and audits.

Sussex has a long list of clients including natural gas distribution companies,

electric utilities, combination utilities, electric transmission providers, natural

gas pipeline companies, state agencies, and non-regulated energy market

participants.

20You can also read