Phillip Securities Research Morning Call - StocksBNB

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Phillip Securities Research Morning Call

26th May 2020

Stock Counter Updates Macro/Sector Outlook

IREIT Global Singapore REITs Sector

EC world REIT Singapore Banking Monthly

Propnex Ltd Singapore Weekly

ComfortDelGro Ltd

ThaiBev PLC

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.

Disclaimer

The information contained in this presentation has been obtained from public sources which Phillip Securities Research Pte Ltd (“PSR”) has no reason to believe are

unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in this presentation are based on such

information and are expressions of belief only. PSR has not verified this information and no representation or warranty, express or implied, is made that such

information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in this presentation is

subject to change, and PSR shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or

releases in connection therewith. In no event will PSR be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of

the information or Research made available, even if it has been advised of the possibility of such damages.

This presentation is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of

any particular person.

You should seek advice from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial

situation or particular needs, before making a commitment to invest in such products.

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents. 2

SG Banking Monthly

Building reserves as outlook dims

Tay Wee Kuang

Research Analyst

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.

Singapore Banking Monthly – Neutral (Downgrade)

1Q20 banking results snippet

DBS OCBC UOB

S$mn 1Q20 (YoY) 1Q19 1Q20 (YoY) 1Q19 1Q20 (YoY) 1Q19

4,026 2,490 2,407

Total Income 3,551 2,676 2,406

(+13%) (-7%) (-)

2,470 1,355 1,321

PPOP 2,053 1,556 1,333

(+20%) (-13%) (-1%)

1,086 657 286

Allowances 76 249 93

(+ >100%) (+ >100%) (+ >100%)

1,165 698 855

Earnings 1,651 1,231 1,052

(-29%) (-43%) (-19%)

Banking operations largely unaffected in the quarter

UOB comparable, while DBS saw robust growth across all segments

OCBC largely affected by contribution from GEH

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.

Singapore Banking Monthly – Neutral (Downgrade)

1Q20 banking results snippet

DBS OCBC UOB

S$mn 1Q20 (YoY) 1Q19 1Q20 (YoY) 1Q19 1Q20 (YoY) 1Q19

3,232 2,314 2,362 Regulatory

Cumulative GP 2,947 1,708 2,054

(+10%) (+35%) (+15%) Requirement

CET-1 CAR 13.9% 14.3% 14.1% 9%

Tier 1 CAR 15.1% 14.9% 15.1% 10.5%

Total CAR 16.8% 16.4% 17.2% 12%

NPL Ratio 1.6% 1.5% 1.6% -

NPA Coverage 92% 90% 88% -

Unsecured NPA

173% 234% 206% -

Coverage

LCR 133% 151% 139% 100%

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.

Singapore Banking Monthly – Neutral (Downgrade)

NIM DBS OCBC UOB

(%)

Current 1.86 1.76 1.71

2015 1.77 1.67 1.77

2014 1.68 1.68 1.71

2013 1.62 1.64 1.72

2012 1.70 1.77 1.87

2011 1.77 1.84 1.92

Lending rates under pressure

Current 3M-SIBOR/SOR stands at 0.69% and 0.26% respectively, back to FY13-FY14 levels

Further compression of 10 bps from current levels for FY20

Impact will equate to 5 to 6% impact on NII, which makes up roughly 65% of total income

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Singapore Banking Monthly – Neutral (Downgrade)

Loans growth taper in March to 2.41% YoY

Consumer loans fall 2.43% YoY, in particular housing

and credit card seeing steeper declines

Business loans increase 5.52% YoY, expected to hold up

FY20 loans growth to remain at 2 – 3%, and increased

credit spread may provide buffer to NIM

Loans growth (YoY %)

March 2020 2.41

February 2020 3.05

January 2020 2.97

December 2019 3.08

November 2019 3.10

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Singapore Banking Monthly – Neutral (Downgrade)

SDAV DDAV

YoY (+/-) YoY (+/-)

($mn) (mn)

May (MTD) 1,326 +20% - -

April 1,411 +35% 0.83 -19%

March 2,193 +114% 1.53 +34%

February 1,377 +30% 1.24 +11%

January 1,219 +24% 1.07 +23%

SGX business momentum slowing

Fatigue in derivatives volumes; 35% below average of 1Q20 (1.2mn contracts per day)

SDAV fall off peak but remains at heightened level, with institutional clients net selling and retail clients net buying

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Singapore Banking Monthly – Neutral (Downgrade)

1Q20 banking results snippet

DBS Group Holdings Oversea-Chinese Banking Corp United Overseas Bank Limited

ACCUMULATE (Maintained) ACCUMULATE (Maintained) ACCUMULATE (Maintained)

BLOOMBERG CODE DBS SP BLOOMBERG CODE OCBC SP BLOOMBERG CODE UOB SP

LAST TRADED PRICE SGD 19.18 LAST TRADED PRICE SGD 8.49 LAST TRADED PRICE SGD 19.46

FORECAST DIV SGD 1.32 FORECAST DIV SGD 0.56 FORECAST DIV SGD 1.10

TARGET PRICE SGD 20.60 TARGET PRICE SGD 9.14 TARGET PRICE SGD 20.70

DIVIDEND YIELD 6.88% DIVIDEND YIELD 6.60% DIVIDEND YIELD 5.65%

TOTAL RETURN 14.29% TOTAL RETURN 14.25% TOTAL RETURN 12.02%

Reduce Singapore banking sector to Neutral

Earnings impact for FY20 expected to come in at around 20-30%

Revised TP by adjusting NIM compression and increased credit costs

Preference for DBS with stronger business momentum and commitment to stable dividend pegged to

operational performance than targeted payout ratio or CET-1 ratio

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.IREIT Global

Visibility amidst uncertainty

Tan Jie Hui

Research Analyst

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.IREIT GLOBAL

BUY (Upgraded), TP: $0.77, Last: $0.67

+ The Positives

Stable results expected for 1H20; 1Q20 was Sponsors and new strategic investor, AT investments,

minimally impacted by Covid’19. increased stake to show support; IREIT’s non-

100% of rental income has been collected from executive director bought shares from market.

tenants in 1Q20 with no dips in occupancy Tikehau Capital and CDL increased their unitholding to

98% of April’s rents have been collected, with only 29.2% and 20.87%, from 16.64% and 12.52%

2% of arrears coming a handful of tenants from the respectively. AT Investments’ acquired a 5.5% stake.

Spanish portfolio. Mr Bruno de Pampelonne who is IREIT’s non-executive

director purchased 200,000 units of IREIT at S$0.6075.

Proactive asset management mitigated lease break

These transactions are testaments of the sponsors’,

fears of key tenants. investor’s and management’s confidence in IREIT’s

The manager secured a 9-yr future lease with a strong portfolio.

tenant for the entire 2 floors of Munster South building that

will commence on 1 March 2021 post lease break by GMG

on 29 Feb 2021.

WALE of Munster Campus is to increase from 2.9 to 4.1

years, which will help to provide the portfolio with greater

income visibility.

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.IREIT GLOBAL

BUY (Upgraded), TP: $0.77, Last: $0.67

- The Negatives Outlook

Few requests for rental rebates amidst Covid’19

Limited growth expected from CPI-linked

escalations. No requests for rent rebates or deferrals from the German

portfolio, but there are a few requests from tenants in the

Germany’s and Spain’s GDP are expected to decline Spanish portfolio.

by 6.3% and 9.2% respectively in 2020 amidst the

These tenants contribute less than 2% of IREIT’s total

Covid’19 outbreak.

income.

Rental escalations for most of the leases linked with

their nations’ CPI. Office take-up and leasing activity are expected to slow

across both European states

Depreciation of EUR to impact 2020 DPU.

Tenants and investors take on a more cautious approach

IREIT hedges approximately 80% of its income to be

towards relocation and expansion in this economic

repatriated from overseas to Singapore on a quarterly basis, climate.

one year in advance.

We are expecting translation loss to impact DPU by 3-5% IREIT’s portfolio presents defensiveness given that

as EUR generally depreciated against SGD throughout 2019. 95% of the current income stream is locked in till 2022.

0.9% and 2.6% of the leases due to expire and 2.6% and

2.4% eligible for lease break in FY20 and FY21

respectively

Upgraded to BUY with a lower TP of S$0.770.

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.EC World REIT

Income visibility from master lease

Natalie Ong

Research Analyst

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.EC World REIT

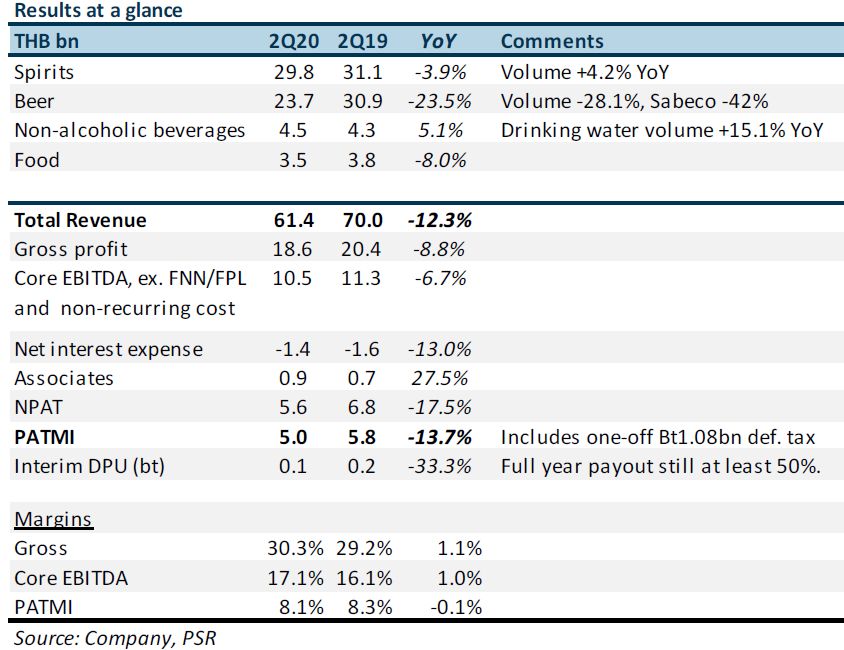

BUY (Maintained), TP: $0.77, Last: $0.68

Results at a glance + The Positives

(SGD mn) 1Q20 1Q19 YoY Comments

Gross revenue 23.5 23.9 -1.4% Lower due to rental rebates of RMB23.7mn High income visibility due to portfolio occupancy

Net property income 21.1 21.2 -0.2% of 99.1% (-0.8ppts QoQ), and WALE by GRI of 3.8

Distributable income 9.8 11.9 -17.9% Lower due to higher interest expense ($9.7mn vs years. 74% of FY20e revenue is secured through 4

$7.0mn) on higher loan quantum, and higher master leases to the Sponsor, with build-in rental

unrealised FX loss ($4.0mn vs $0.9mn) escalations ranging 1% to 3%

DPU (cents) 1.16 1.50 -22.9% Lower payout ratio of 95% (prev. 100%) as DI was

retained for working capital and unforseen Running cost of interest fell QoQ from 4.4% to

contingencies, and 50% of management fees paid in 4.3%. This is likely attributed to ECW increasing

units (prev. 100%) the interest rate hedge in 1Q20 from 72.2% to

Source: Company , PSR 100%

Outlook - The Negatives

Trade receivables ballooned by S$18.8mn (roughly 51%) QoQ, Accretion from the acquisition of Fuzhou E-

indicating that 80% of 1Q20’s revenue of S$23.5mn has not been commerce wiped out. DPU -22.9% YoY in 1Q20

collected - some of the arrears could be attributed to Sponsor, given due to RMB23.7mn of rental rebates granted,

that the Sponsor was responsible for 73.6% of 1Q20’s revenues higher finance expense and 5% retention of

distributable income (DI)

Maintain BUY with lower TP of S$0.77 (prev. $0.83).

FY20e/FY21e DPU trimmed by 5.6% and 3.9% which translates to

DPU yield of 9.0% and 9.6% respectively

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Singapore REITs Sector

More clarity as the dust settles

Natalie Ong

Research Analyst

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.FTSE REIT Index rebounding faster than STI

Healthcare Hospitality Retail Commercial Industrial Diversified

Covid Drawdown -33.4% -52.5% -38.5% -38.5% -35.9% -38.3%

Price Recovery 54.6% 20.8% 29.6% 37.4% 58.7% 28.7%

Source: Bloomberg, PSR

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.SREIT Dividend Yield at +1.4 s.d. level

Dividend yield: 5.14% FED rate: 0% - 0.25%, after150bps cut

2019 Ave: 4.6%

3M SOR: 0.23% (Sep 2014 lows)

Div. yield spread: 4.42% (+1.4 SD level)

2019 Ave: 2.6% 10YSGS: 0.72%

Source: Bloomberg, PSR

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Impact by Subsector

Impact to landlords vary by:

Hospitality Retail Commercial Industrial

Occupancy:

% Tenants Operating 20% - 25% 10% - 30% 60% - 70% 1. The underlying tenant's reliance

40% - 80%

Property Tax Rebate 100% 100% 30% 30% on the premise to generate

income

Amount of Rental Selectively, Selectively,

NA 2 - 3 months

Rebates Given 0.5 - 1.5 months 0.5 - 1.5 months

2. Degree of business disruption

3Q20: Domestic and amount of rental assistance

Higher vancancy rates, lower rents secures,

Impact 4Q20: rendered

right-sizing of space

International

Source: Respective company announcements, PSR 3. Future demand for space (i.e.

behavioural shifts, ecommerce

and telecommuting)

Source: Bloomberg, PSR

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Implications for S-REITs

Outlook Mitigants

Slower leasing activity, mostly renewals Tenants are locked in by existing leases

Higher vacancy rates Relatively low supply coming online across

the subsectors

Lower rents and/or negative rental

reversions

According to CBRE’s April 2020 cap rate

flash survey, investors are expecting cap

rates for shopping malls to expand up to

30bps while cap rates for logistics and

Grade A office are expected to hold steady

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Retail – Waiting for Phase 2 of lifting of circuit breaker

Retail Rental Index and Occupancy

Occupancy dipped by 0.5ppts while the rental

index fell by 2.3pts

Market expectation for landlord to have more “skin

in the game”

High reliance on premise to generate revenue

Highest amount of rental rebates offered (2 to 3

months)

Rise in vacancy rates, lower rental reversions

Flexible leasing strategies: shorter lease term,

higher risk-sharing

In the long run, higher risk-sharing may increase

the demand as the lower fixed rents makes it

more economically viable for new-to-market

Source: CEIC, PSR brands to give the brick-and-mortar model a go

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Office – Awaiting more clarity from counteracting leasing strategies

Office Rental Index and Occupancy

Occupancy dipped 0.5ppts in 1Q20 to 89.0%,

albeit being 0.8ppts higher YoY

The rental index fell 1.3pts QoQ to 168.7pts

Office prices also showed some weakness,

falling 4.0% QoQ

Low reliance on premise to generate revenue

Potential positives: Lower desk-density and

split office may increase demand, demand for

flex-space

Potential negatives: Risk of rightsizing due to

adoption of telecommuting

Source: CEIC, PSR

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Industrial – Resilient, for now

Industrial Rental Index and Occupancy

Occupancy unchanged QoQ at 89.2%

Rental index for biz parks unchanged while the

multiple and single-user factory and warehouse

index fell by 0.2 to 0.4pts

Low reliance on premise to generate revenue for

business parks

High reliance on premise to generate revenue for

light industrial, hi-spec, factories, warehouse,

data centres

High percentage of tenants operating in premise

during circuit breaker

Risk: Relatively high percentage of SME tenants

Potential positives: Heightened demand for

Source: CEIC, PSR logistic and data centre assets

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Hospitality – Lingering fears will impede recovery

Figure : Office Rental Index and Occupancy

Hotel RevPAR fell by 62% YoY, average

occupancy at 40% for 1Q20

High reliance on premise to generate revenue

Extension of lockdown in other countries and

bans on international visitors keeping occupancy

at depressed levels

Alternative source of income (Block booking by

govt, self-isolation)

Lingering fear and caution even if international

travel bans are lifted, domestic demand to

supplement demand

MICE events, which have been pushed back to

the second half of the year, should help in the

recovery of the sector once event-hosting

Source: CEIC, PSR restrictions are lifted (Phase 3)

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Changes to PSR’s forecasts

Previous New % Previous New % Previous New Target % FY20e DPU FY21e DPU

FY20e DPU FY20e DPU Change FY21e DPU FY21e DPU Change Target Price Price Change Yield Yield

Ascott Residence Trust 8.15 6.87 -15.7% 8.52 8.14 -4.5% 1.53 1.17 -23.5% 7.9% 9.4%

CapitaLand Mall Trust 12.51 10.78 -13.8% 13.11 12.81 -2.3% 2.70 2.22 -17.8% 5.8% 6.9%

Frasers Centrepoint Trust 12.76 9.88 -22.6% 14.14 13.56 -4.1% 3.11 2.22 -28.6% 4.6% 6.2%

CapitaLand Commercial Trust 9.03 7.67 -15.1% 9.20 9.12 -0.9% 2.18 1.74 -20.2% 4.8% 5.7%

Ascendas REIT 16.11 16.74 3.9% 16.25 17.06 5.0% 3.31 3.18 -3.9% 5.5% 5.6%

Keppel DC REIT 7.79 8.99 15.4% 9.50 9.55 0.5% 2.06 2.20 6.8% 3.7% 3.9%

IREIT Global 5.54 5.47 -1.3% 5.58 5.54 -0.7% 0.885 0.77 -13.0% 8.0% 8.1%

EC World REIT 6.27 5.92 -5.6% 6.59 6.33 -3.9% 0.83 0.77 -7.2% 8.7% 9.3%

Source: Bloomberg, PSR, updated 19 May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.PropNex Ltd

1Q20 Results

Earnings almost tripled but outlook cloudy

Paul Chew

Head Of Research

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

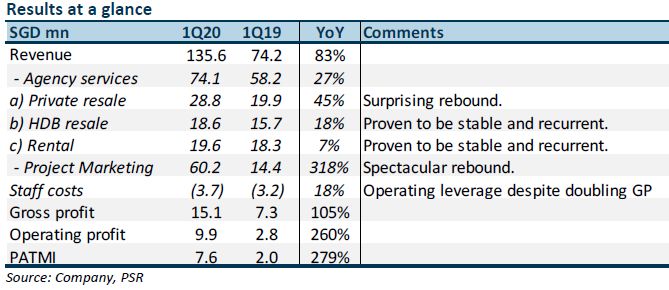

accepts no liability whatsoever with respect to the use of this document or its contents.PropNex (BUY (Maintained), TP: S$0.60, Last: S$0.495)

Positives

• 3x jump in project marketing - 8 to 12 weeks for revenue from the booking

of a new project, the growth this quarter comes from the health project

sales in 4Q19. For the Top 3 selling projects in 1Q20 (The M, Treasures

at Tampines, Jadescape), PropNex market share ranged from 46% to

60%

• Cash keeps piling up - cash from operations increased S$8.7mn in 1Q20.

Capital expenditure was less than S$100k in 1Q20. Net cash on the

balance sheet rose to a record S$89.8mn (~50% market cap).

• Huge operating leverage - Gross profits doubled YoY to S$15mn whilst

staff cost only increased S$560k (or +17.8% YoY). The rise was due to

salary increment and additional 1 headcount to 175.

Outlook:

a. New launches: 1Q20 industry volumes rose 17% YoY to 2149. This will be supportive of 2Q20e earnings. FY20e industry transaction

volumes may drop by around 20% to 7900. These are levels worst than the 12 months post July18.

b. Private resale: 1Q20 volumes jumped 12% YoY to 2080 units. The resale market will be even worst hit than new launch. Without viewing

the units physically, there is a higher risk for the buyer if there are issues with the unit. Resale units are unlike new launches where

developers are reputable and there is the typical 1-year defect liability for developers. Expectations are for at least a 32% decline in

transactions to 6100.

c. HDB resale: 1Q20 volumes rose 22% YoY to 5893 unit and the highest in 9 years (for a March quarter). The circuit breaker will cause

some postponement of purchases in the near-term and overall transaction for FY20e could fall by 10% to 21,500 units.

Maintain BUY with higher TP of S$0.60 (prev. S$0.70): Our target price is lowered as we cut FY20e earnings forecast by 19%. We believe

the company intends to position themselves as a high yield paying stock (7%). To maintain dividends at 3.5 cents per annum requires a

payout of S$13mn

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.ComfortDelGro Corp Limited

1Q20 Business Update

Pain everywhere

Paul Chew

Head Of Research

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.ComfortDelgro (Neutral (Downgraded), TP: S$1.50, Last: S$1.54)

Positives

(SGD mn) 1Q20 1Q19 YoY Comments • FCF of S$57.4mn in 1Q20 (1Q20: +S$0.4mn). Operating cash-

Revenue 862.4 947.3 -9.0% flow of $S105.5mn during the quarter was higher than a year

- Public transport 656.3 684.6 -4.1% Bus operations in Singapore were ago (1Q19: S$95.6mn). Turn net cash position of S$26.mn

against the net debt of S$40mn as at end Dec19.

- Taxi 127.8 171.9 -25.7% stable.

Impact from China more significant.

EBIT 55.9 107.4 -48.0% Negatives

- Public transport 33.6 54.9 -38.8% UK swung into a loss.

• Taxi operating profit plunged 92% to S$2.4mn. Rental rebates

- Taxi 2.4 28.2 -91.5% and lockdowns depressed earnings and volumes respectively.

PATMI 36.0 70.4 -48.9% Of the S$116mn of rental rebates to Singapore taxi drivers, we

believe only S$13.7mn was incurred in 1Q20.

Source: Company, PSR

•

Bus operations are not immune. The lower frequency in bus

mileage will impact revenues. The service fee paid by the

authorities is dependent on mileage travelled.

Outlook: Taxi – Comfort taxi drivers will receive rental relief in stages from 13 February onwards. Taxi drivers will also receive 100% rental

waiver from 7 April to 1 June, to coincide with the circuit breaker period. We estimate the rental rebates from Comfort in 2Q20 will be around

S$68.9mn (Figure 2). Taxi operations are expected to be loss-making in FY20e.

Public transport - Public bus and rail ridership was down between 70-75% during the circuit breaker period. Lower mileage operated will lead

to less service fee to be received from the authorities.

Downgrade to NEUTRAL with a lower target price of S$1.50 (prev. S$2.20): Social distancing behavior, working from home and the

decline in tourist will all weight on passenger volumes. Our PATMI for FY20e is slashed by 62%. It excludes the job support scheme to be

received from the government. Bus operations can recover faster as revenue depends on capacity, not passenger volumes. However, rail

and taxi will suffer for a more prolonged period. The unknown for us will be the number of taxi drivers churning out of or into Comfort.

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.ComfortDelgro (Neutral (Downgraded), TP: S$1.50, Last: S$1.54)

Figure 1: Announcements of rental relief for taxis in Singapore by Comfort Figure 2: The S$116mn support from Comfort for taxi drivers

Annc. Comment Driver Total Relief Period Daily rental waiver from Comfort S$mn

Date Relief Cost 13 Feb to 6 Apr S$10 per day x 54 days 5.4

S$/daily S$ mn 21 Feb to 6 Apr S$16.50 per day x 46 days 7.6

13-Feb S$900 rental rebate over the next 3 months 10 9 25 Mar to 6 Apr S$10 per day x 13 days 1.3

This is on top of the S$900 announced by the Government. 10 9 7 Apr to 1 Jun S$103 per day x 56 days 57.7

20-Feb Daily rental rebate of S$16.50 from 21 February to end March. 16.5 10 2 Jun to 30 Sep S$36.50 per day x 121 days 44.2

Followed by daily S$10 rebate for April. 116.1

25-Mar From 25 March to end April, additional S$10 daily rental relief on top 10 1Q20e S$10/day (54days) + S$16.50 (46days) + S$10/day (7days) 13.7

of the current S$36.50, inclusive Government Special Relief Fund. 2Q20e S$10/day (6days) + S$103/day (56days) + S$36.5/day (29days) 68.9

The S$16.50 will be extended to end-April. 3Q20e S$36.5/day (92 days) 33.5

30-Mar Extend the daily S$46.50 rental relief till end-September. 80 116.1

4-Apr All tax rental will be waived from 7 April to 5 May. All 19

22-Apr Extend the full rental waiver from 6 May to 1 June. All 17

Source: PSR, Company

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Thai Beverage PLC

2Q20 Results

Dry spell in watering hole

Paul Chew

Head Of Research

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Thai Beverage

(BUY (Maintain), TP: S$0.82, Last: S$0.67)

Positives

• Margin stable for spirits business despite weaker volumes. Operating

profit for spirits business was flat YoY at TBH6.46bn despite the fall in

revenue. The expansion in margins was due to a 10% YoY decline in

distribution expenses to TBH1.69bn. Spirits PATMI was up 9.5%

Negatives

• Sabeco will remain problematic for a few quarters -volumes punished by

three key events: fake news, decree 100 and Covid-19 economic hit.

Decree 100 in Vietnam introduced stiffer penalties for drunk driving, ban

advertising of alcoholic beverages (between 6pm to 9pm). This has hit the

on-trade (aka on-premises) (i.e. pubs, clubs).

Outlook: The ban in alcohol sales in Thailand from 10 April to 3 May, will temporarily suppress earnings in 3Q20. Off-trade consumption (i.e.

consumed at home) of spirits contributes approximately 80% of spirit sales and less impacted by Covid-19 social distancing measures.

Maintain BUY with lower TP: We favour THBEV for their dominant market share of around 90% in spirits. It has an unassailable distribution

network in Thailand with 280k direct point of sales presence and another 150k covered indirectly via agents. Another near-term lever to

earning in FY20e will be a cut in advertisement and promotion expenses to defend profitability.

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Week 22 - Phillip Singapore Weekly

Paul Chew

Head Of Research

Phillip Securities Research Pte Ltd

26th May 2020

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Week 22 – Short-term Views Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only. Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

COVID-19: Largest economies trending down

COVID-19 New Daily Cases

120,000

100,000

80,000

60,000

40,000

20,000

0

World Largest Economies ROW

Source: CEIC, WHO, PSR; *Largest economies - US, China, Germany, UK, Spain, Italy, France, Japan, S Korea

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

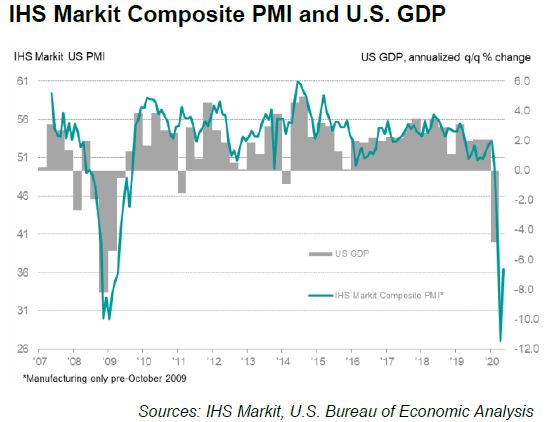

accepts no liability whatsoever with respect to the use of this document or its contents.Economic data – U.S. Flash PMI for April

Source: https://www.markiteconomics.com/Public/Home/PressRelease/63cdd746043d4473bd49c2730287049a

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.SG exports: Surprisingly resilient

Source: CEIC, PSR

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.SIA: April traffic down 99% YoY from 1.78mn to 9.2k

SG: SIA Passenger Carried (YoY) Impact of 9/11 and SARS

70,000 18,000

20% 65,000 17,000

60,000 16,000

0% 15,000

55,000

14,000

-20% 50,000

13,000

45,000

12,000

-40% 40,000 11,000

35,000 10,000

-60% 9/11 = 22 months SARS = 11 months

30,000 9,000

-80%

-100%

US Passengers (000s) - LHS Changi Aircraft Movements - RHS

2006 2008 2010 2012 2014 2016 2018 2020

Source: CEIC, PSR, S$2.68 is cost of MCB if converted to shares after 10 year

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities

accepts no liability whatsoever with respect to the use of this document or its contents.Analysts

Paul Chew, Head of Research

Natalie Ong, REITs | Property

Tay Wee Kuang, Banking & Financial | Healthcare

Tan Jie Hui, Small Mid Cap

Timothy Ang, Credit (Bonds)

Chua Wei Ren, Technical

Siti Nursyazwina, Research Admin

Have an opinion or questions on our reports?

Post them in the comment section of the report!

Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities 38

accepts no liability whatsoever with respect to the use of this document or its contents.Phillip Securities Research Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197501035Z © PhillipCapital 2019. All Rights Reserved. For internal circulation only. Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

You can also read