Ride-sharing Profitable or not? - bank DBS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

75

SECTOR BRIEFING

number

DBS Asian Insights

DBS Group Research • May 2019

Ride-sharing

Profitable or not?

DBS Asian Insights SECTOR BRIEFING 75 02 Ride-sharing Profitable or not? Sachin MITTAL Equity Analyst DBS Group Research sachinmittal@dbs.com Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights asianinsights@dbs.com Wen Nan Tan Editor Martin Tacchi Art Editor

DBS Asian Insights

SECTOR BRIEFING 75

03

04 Executive Summary

Can ride-sharing be a profitable model?

09 What is ride-sharing?

Market size

Different ride-sharing models in play

Ride-sharers expanding beyond simple-taxi offerings

Safety is another key appeal of ride-sharing

SoftBank’s role in mediating ride-sharing industry

competition

13 Is ride-sharing a profitable business model?

Understanding the key elements driving profitability

of ride-sharers

Path to profitability of ride-sharers – Line by Line

analysis

17 What does it take to become profitable in

the ride-sharing business?

Confronting arguments against the profitability of

ride-sharing

27 Playbook for smaller ride-sharing operators

30 Regulations: The biggest overhang for ride-

sharers

32 Drawing insights from E-commerce to ride-

sharing

40 Appendix

Key ride-sharers around the world

DBS Asian Insights

SECTOR BRIEFING 75

04

Executive Summary

Can ride-sharing be a profitable model?

From our analysis into the operations of ride-sharers, we found that dominance and scale

are the two key drivers for profitability. Dominance in key cities allows ride-sharers to ease

spending on rider incentives and marketing expenses, without major driver or rider churn.

Scale may entail lower revenue per ride due to expansion outside the major cities but leads to

superior gross margins. Key benefits of scale are lower insurance costs, payment processing

fee and fixed platform operating costs as a percentage of revenue. We believe that ride-

sharers with > 60% market share in their respective countries, including key metropolitans,

should reap benefits of their dominance.

Our key finding is that a region cannot have more than one profitable ride-sharing player.

Ride-sharers operating in the South East Asian region may start to realise scale benefits at

US$1.3-1.7b revenues. This is provided, their expansion plans which typically lead to delays

in reaching profitability, are minimal.

What does it take to build

a profitable ride-sharing

business?

Dominance Scale

Dominance in key markets Scale allows bigger

keeps sales & marketing players to reduce

expenses and rider insurance, payment and

incentives in check fixed operating fee as a

percentage of revenue

Source: DBS Bank

DBS Asian Insights

SECTOR BRIEFING 75

05

Does this mean that smaller operators should just pack up

and leave?

Whilst the path towards profitability for smaller operators remains rocky, we believe smaller

players can co-exist with market leaders with the right strategies in place.

We outline three distinct strategies that smaller players can pursue that could set them on

a path towards profitability:

1. Focus on niche market segments that are typically underserved by bigger operators (Eg.

Ola for Auto-rickshaws)

2. Focus on specific regions / cities to limit competitive play with bigger players to drive

down incentives and marketing expenses

3. Develop an ecosystem of more profitable services leveraging the ride-sharing platform

and the digital follower base

Playbook for smaller

operators

Niche segmental play Selective regional play Ecosystem play

Dominate niche sub- Dominate smaller cities/ Leverage the ride-sharing

segments in ride-sharing regions underserved by platform and user base to

underserved by market leading ride-sharers diversify and venture into

leaders other profitable segments

Source: DBS BankDBS Asian Insights

SECTOR BRIEFING 75

06

Key financial and operational metrics of ride-sharers around the globe

Grab Go-Jek Uber Lyft Ola

Annual rides (in m) 2,409 1,200 5,220 619 1,000

Active Users (in m) N/A 25 91 18.6 N/A

Active Drivers (in m) 2.8 1.0 3.9 1.9 1.0

Annual Revenue (FY19 for Grab) 2,000 N/A 11,270 2,157 318

(in US$m)

Valuation (based on latest 14,000 9,500 85,000 20,696 6,000

funding rounds and latest

market cap for Lyft) (in US$m)

EV/Revenue 7.0 N/A 7.5 9.6 18.9

Total funds raised (in US$m) 8,800 2,000 24,200 4,900 3,800

Source: DBS Bank, Various media reports

Growth in gross bookings likely to remain in mid double

digits for ride-sharers

We are of the view that Ride-sharing is likely to witness a growth trajectory akin to that of

E-commerce in its early days, though profitability is likely to be lower. With penetration of ride-

sharing services still hovering below 1% of total passenger vehicle trips of less than 30 miles,

there is ample headroom for double-digit growth for ride-sharers over the medium term.

Gross bookings and GMV growth comparisons

Source: Companies, DBS BankDBS Asian Insights

SECTOR BRIEFING 75

07

However, the long term profitability of ride-sharers is likely to be lower than that of

E-commerce marketplaces in our view. This is mainly due to:

1. Regulatory concerns about lowly paid drivers may lead to slower growth or even declines

in the take rate of ride-sharers, adversely impacting profitability

2. Lower margin profiles of ride-sharers, given that sales and marketing expenses are borne

by ride-sharers. Ecommerce marketplaces, on the other hand, incur minimal sales and

marketing expenses as most of these expenses are incurred by sellers on their platform

3. Quantum of revenue that can be derived regionally is lower in comparison to E-commerce

as there is a physical limitation on the number of drivers and riders in a region. E-commerce,

on the other hand, holds a much higher ceiling given the ease of scaling up the number

of product and service offerings in a given region

Regulations could Take rates for ride sharers vs. E-commerce

limit any further

improvements in the

high take rates of

ride-sharers

Source: Companies, DBS Bank

Sales and marketing Sales and marketing expense as a percentage of revenue

expense substantial for

ride-sharers but not for

ecommerce players

Source: Companies, DBS BankDBS Asian Insights

SECTOR BRIEFING 75

08

Can Automated Vehicles (AVs) increase the take rate of

ride-sharers?

The take rate of a ride-sharing business is expected to increase significantly when AVs

become common since driver pay is the most expensive element of a ride at present,

accounting for c. 75% of the total fare of a ride. All major ride sharers are in the process

of developing and testing AVs. However, the likes of Waymo (Alphabet’s self-driving arm)

and Cruise (General Motors), that lead the AV race are already trialing ride-sharing services

with their self-driving technologies, which could present a threat to existing ride-sharers.

Automobile manufacturers like Tesla have also expressed an interest in offering ride sharing

services through its vehicles as announced recently.DBS Asian Insights

SECTOR BRIEFING 75

09

What is Ride-sharing?

M

ost of us have hailed a cab at least once in our lives. Ride-sharing refers to

the same arrangement, except the “hailing” takes place via digital means

– either via a smartphone application or a website browser. Drivers are also

often freelancers and not dedicated drivers of taxis. Ride-sharing allows users

to hail an array of transportation options, ranking from Limousines, black cars and choppers

to auto rickshaws and motor bikes.

Ride-sharing involves the provision of a taxi-like service via the use of Global Positioning

System (GPS) enabled software, linking drivers and passengers directly without the need

for a dispatch centre. The platforms are account-based, with payments being automatically

processed via the subscriber’s credit card or manually at the end of the trip. Different service

options are typically available, ranging from shared rides with other passengers through to

rides in luxury limousines.

Market size

Ride-sharers primarily target short passenger trips, often of less than 10 miles. Their focus

greatly lies in metropolitan cities of the world, where frequency of rides is usually high and

distance travelled short. According to Uber, ride-sharers can target a market that is worth

as much as US$5.7 trillion in 175 countries across the globe. This is based on 11.9 trillion

miles travelled per year in passenger vehicles, including public transportation miles in all

countries globally.

Potential size of the market up for grabs for ride-sharers

Total Addressable market (175 countries)

All passenger vehicle and public transport trips – 11.9t Miles

Valued at - US$ 5.7t

Trips in public transport– 4.4t Miles

Valued at - US$ 1.0t

Trips in passenger vehicles

– 7.5t Miles

Valued at - US$ 4.7t

Source: UberDBS Asian Insights

SECTOR BRIEFING 75

10

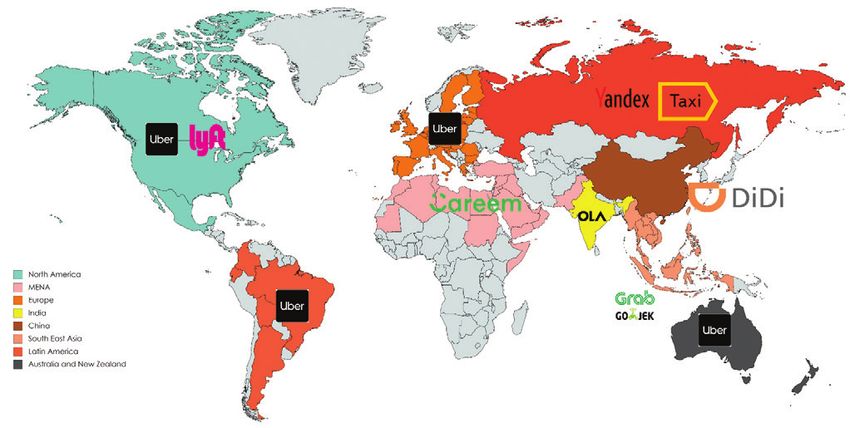

Major ride-sharers around the globe

Source: Mapchart, DBS

Different Ride-sharing models in play

Ride-sharing companies have come up with different models of service offerings to cater to

the requirements of various user groups, targeting high-end, mid-market and budget users

separately.

For instance, Uber, the biggest ride-sharing platform globally, offers premium services through

its service offerings such as Uber Black, Black SUVs and Uber Select. The vehicles offered via

these services are usually black in color, sometimes equipped with personal chauffeurs and

target business customers and high net worth individuals.

Lyft also caters to the premium market through Lyft Lux, Lux Black, and Lux Black XL, where

drivers with qualifying vehicles have the opportunity to earn more by listing their vehicles

under those ranges.

Uber’s mid-market range offerings include UberX and UberXL, which offer everyday rides at

affordable prices. Lyft caters the mid-market through brands Lyft and Lyft XL. These models

target regular customers seeking convenience at affordable prices.

Both Uber and Lyft cater to budget customers. UberPool and Lyft Shared are some of

the examples in this category. Here, drivers cater to multiple customers, who share

destinations that are in close proximity to each other, simultaneously, with a cheaper rate

offered to each customer.DBS Asian Insights

SECTOR BRIEFING 75

11

Ride-sharers expanding beyond simple-taxi offerings

Ride-sharing services have grown rapidly worldwide over the last five years, with companies

such as Uber, Didi Chuxing (Didi), Grab and Ola rising to be among the most prominent. With

ride-sharing turning out to be such a successful venture, most of the ride-sharers are now

expanding beyond ride-sharing, into other adjacent segments like bike-sharing and scooter

sharing, logistics and autonomous driving.

Specifically, Lyft offers an expanded suite of transportation including shared bikes and scooters

for shorter rides and first-mile and last-mile legs of multimodal trips. Lyft has also added

information on nearby public transit routes in selected cities to offer riders a robust view of

transportation options. This multimodal platform better enables Transportation as a Service

(TaaS), which is a viable alternative to car ownership.

Through its New Mobility Solutions offerings, Uber also caters to consumers with access to

rides through a variety of modes, including dockless e-bikes and e-scooters. Uber expanded

into logistics in 2017, introducing “Uber Freight”, connecting shippers with drivers and small

fleets hauling freight via a load-matching mobile app. Furthermore, Uber, Lyft and Didi are all

piloting self-driving projects alongside with manufacturers of automobiles.

Safety is a key appeal of ride-sharing

Ride-sharing services have also instilled confidence in drivers and riders since there is more

transparency and trust through the rating system, where both riders and drivers get the

opportunity to rate their experience on the ride. The two way system holds both riders and

drivers accountable for their behaviour during the ride. Consistently lower ratings could even

result in a ban from the usage of the ride-sharer’s services. Furthermore, in-app safety features

allowing riders and drivers to notify authorities and their friends of any incidents, share their

live location with other users, 24/7 incident reporting and phone number anonymization have

boosted the confidence of riders and drivers to utilise the service even further. This is not to

say that ride-sharing is perfectly safe. Three female passengers using the services of Didi have

been murdered by their drivers over the 2016-2018 period, signifying safety is still a concern in

ride-sharing. However, ride-sharers have utilised technology tools at their best to offer a much

better sense of safety than their traditional taxi-counterparts.

SoftBank’s role in mediating ride-sharing

industry competition

Prominent Japanese investor, SoftBank, has built a stronghold in the ride-sharing market

worldwide, placing the firm within the ranks of the largest investors in all the leading

ride-sharing platforms. Its investments in the ride-sharing industry include Uber (US), GrabDBS Asian Insights

SECTOR BRIEFING 75

12

(Singapore), Didi (China), Ola (India) and Brazil’s 99 (which was later acquired by Didi).

Softbank’s influence on each ride-sharing company is significant. For example, following its

investment into Uber, SoftBank expanded Uber’s board from 11 to 17 members (including two

directors representing SoftBank’s interest), reduced the voting power of early shareholders,

and limited the influence held by Uber co-founder and former Chief Executive Travis Kalanick.

Softbank’s ambitious plans for the ride-sharing industry was laid out in May 2018 when Chief

Executive Masayoshi Son shared his plans to establish a Visionary Fund to consolidate all its

ride-sharing companies. In total, the Japanese entrepreneur has placed a US$60 bn bet in

more than 40 companies in a bid to steer the US$3 tn global automotive industry1. SoftBank

is now poised to use its influence to broker deals between ride-sharing companies that might

otherwise battle indefinitely, bringing about industry consolidation, as in the case of Grab

acquiring Uber’s South East Asian operations in 2018. This, we believe could fare well for the

bigger ride-sharing operators globally, as Softbank could mediate to limit instances where

bigger players cross paths with each other.

However, the SoftBank portfolio is not without risks, particularly for companies dependent

on the Japanese firm for financial sustenance for years to come. SoftBank faces financial

pressures, including an obligation to pay an annual 7% dividend on a portion of the invested

capital and the firm has already burnt through a significant portion of the Vision Fund. Whilst

this may impose pressure on Softbank’s future investments in the industry, Softbank has

already made its mark as the leader of the ride-sharing industry globally and would be a key

mediator driving rational competition within the industry.DBS Asian Insights

SECTOR BRIEFING 75

13

Is Ride-sharing a profitable

business model?

W

e look into the unit economics of ride-sharing operators, basing our analysis

on recent Initial Public Offering (IPO) filings of Uber and Lyft in a bid to

understand the per-ride profitability of ride-sharing operators on a pure-direct

cost basis at present.

Uber’s ride-sharing business, on a pure-direct cost basis turned positive in 2018

Uber - Ride Sharing (US$) Per Ride Lyft - Ride Sharing (US$) Per Ride

2016 2017 2018 2016 2017 2018

Gross booking per ride 10.78 8.40 7.95 Gross bookings per ride 11.73 12.21 13.00

Driver fees and incentives (8.84) (6.56) (6.19) Driver Incentives (1.46) (1.02) (0.87)

Revenue 1.94 1.84 1.76 Driver Pay (8.15) (8.37) (8.65)

Excess driver incentive (0.26) (0.12) (0.13) Driver pay and incentives (9.61) (9.39) (9.52)

Other cost of revenue (0.87) (0.83) (0.70)

Contribution 0.82 0.89 0.93 Revenue 2.11 2.82 3.48

Operations and support (0.45) (0.31) (0.24) Cost of revenue (1.72) (1.76) (2.01)

Sales and marketing (0.41) (0.32) (0.25) Other adjustments 0.11 0.00 0.01

Driver referrals (0.08) (0.05) (0.02) Contribution 0.50 1.07 1.49

Rider Incentives (0.31) (0.22) (0.22) Operations and Support (0.60) (0.49) (0.55)

Operating Profit/loss before (0.43) (0.01) 0.20 Sales and Marketing (1.47) (1.10) (0.82)

corporate charges Rider incentives (1.20) (0.41) (0.48)

Operating Profit/loss before (2.77) (0.93) (0.36)

As a % of revenue corporate charges

Take rate as a % of gross 18% 22% 22%

bookings As a % of revenue

Excess driver incentive 13% 7% 7% Take rate as a % of gross 18% 23% 27%

Other cost of revenue 45% 45% 40% bookings

Gross Profit Margin 42% 48% 53% Cost of Revenue 76% 62% 57%

Operations and support 23% 17% 13% Gross Profit Margin 24% 38% 43%

Sales and marketing 21% 17% 14% Operations and Support 29% 17% 16%

Driver referrals 4% 3% 1% Sales and Marketing 70% 39% 24%

Rider Incentives 16% 12% 12% Rider incentives 57% 15% 14%

Operating Profit/loss before -22% 0% 11% Operating Profit/loss before -131% -33% -10%

corporate charges corporate charges

Source: Uber, Lyft, DBS Bank

As Uber does not breakdown costs attributable to each of Uber’s segments (namely: Ride-sharing, Uber Eats and Uber Freight),

we have apportioned total costs on the basis of revenue contribution to perform our analysis on profitability per ride. Ride-

sharing accounted for 92%, 87% and 81% of Uber’s topline over 2016, 2017 and 2018 respectively. On a consolidated basis,

Uber generated a profit of US$980m, before corporate charges and depreciation and amortization in 2018. Uber reported

US$3.03b in operating losses over 2018 (vs. US$4.08 in 2017).DBS Asian Insights

SECTOR BRIEFING 75

14

Understanding the key elements driving

profitability of ride-sharers

“I’ve earned US$2on this ride - Uber”

Revenue of ride-sharing companies

is gross bookings less driver fees/

incentives and taxes

“I have US$2 off, so I will pay US$8” “Your fare is US$10”

Incentives are provided to Referred to as “Gross bookings”

riders to improve frequency of this is the total value of all rides

rides and loyalty. This is one of taken through a ride-sharing

thekeydeterminantsofprofitability platform

as rider incentives account for a

significant portion of expenses of ride-

sharing companies and is discretionary

Key operating expenses

Cost of revenue

Includes platform running expenses, insurance and

payment processing fees

Operations and support

Costs involved in providing rider support, driver on-

boarding, driver background checks

Sales and Marketing

One of the biggest line items. Includes advertising and

promotional expenses

Source: DBS Bank

Gross Bookings

Akin to Gross Merchandise Value (GMV) of E-commerce players, Gross bookings refer to the

total value of all rides taken through a ride-sharing platform. This includes the fare of the

ride, applicable taxes, driver fees, tolls, etc. Gross bookings are driven by a combination of

fare set by the ride-sharing company, number of active riders on the platform (penetration

of ride-sharing services) and frequency of use by active riders.DBS Asian Insights

SECTOR BRIEFING 75

15

Revenue and Take Rate

Revenue is defined as the net proceeds realized by ride-sharing companies once the gross

bookings are adjusted for fees and incentives paid to drivers and taxes. Take rate is the

percentage of revenue realized through total bookings.

Cost of Revenue

Direct costs of revenue largely comprises of insurance expenses (coverage by typical auto-

insurance products cease when passenger vehicles are used for ride-sharing. Hence ride-

sharing companies are required by regional laws to provide insurance coverage to riders/

drivers during service), payment processing fees and platform operating expenses (data

centre hosting and colocation, mobile device and service charges).

Contribution

Gross profit of ride-sharing business after accounting for attributable direct costs.

Operations and support

Expenses involved in providing operational support to riders and drivers, driver onboarding

expenses and expenses related to conducting background checks on drivers.

Rider Incentives

Discounts and promotions offered to riders to keep them on the platform, improve

frequency of rides and attract new riders. Rider incentives are classified under sales and

marketing expenses. Rider incentives typically depend on the competitiveness of the

ride-sharing marketplace and are a key determinant driving profitability of ride-sharing

operators. This is so as rider incentives account for a significant portion of expenses of ride-

sharing companies and is discretionary with ample room to be curtailed depending on the

competitiveness of the marketplace.

Sales and Marketing

Other advertising and promotional expenses involved in promoting ride-sharing services.

The appeal of ride-sharing as a business model is quite clear – the business generates c.

50% gross margins. However, c. 40-50% of revenue is attributed to other direct costs below

the gross margin level with sales and marketing, and rider incentives accounting for the

lion’s share.

Going by the example of Uber, which yielded an operating profit before corporate expenses,

it is evident that once expenses below the gross margin level (particularly sales and

marketing, and rider incentives) are controlled, ride-sharing can turn out to be a profitable

business model.DBS Asian Insights

SECTOR BRIEFING 75

16

Path to profitability of ride-sharers – Line by

Line analysis

Increase gross booking per ride Ride-sharer (US$) 2018 Improving take rate

Fare increases, market share and This would be unsustainable

penetration gains could drive as a higher take rate translates

Gross Bookings 400%

gross bookings up. However, this to lower pay for the drivers,

may require higher S&M and rider Driver pay and 300% which could a). Increase driver

incentives

incentives. Revenue 100%

churn and b). Cause regulatory

concerns

Cost of Revenue 52%

Reduce cost of revenue Lower Ops and Support

There is room to reduce in platform Contribution 48% One of the more feasible

related expenses with economies Operations and 15% ways of improving margins,

of scale, while better negotiated support as with improving volumes

Sales and marketing 20%

contracts with insurance providers and potential digitisation

and payment processors could Rider incentives 13% of customer support, driver

drivedown costs of revenue. Operating Profit/ 0.0% background checks etc, Ops

loss before corporate and support expenses as a %

charges

of revenue has room to come

Lower Sales and Marketing and down.

rider incentives

Most feasible way of arriving

at profitability. However, this

would largely depend on the

competitiveness of the market

place and the market position of

the ride-sharing operator. Lowering

S&M and incentives could also

have a knock on effect on Gross

bookings as frequency of usage

and penetration of ride-sharing

could edge lower once the

incentives are taken out. Source: Uber, Lyft, DBS BankDBS Asian Insights

SECTOR BRIEFING 75

17

What does it take to become

profitable in the ride-sharing

business?

T

he ride-sharing business model is banking on two macro-economic trends: greater

penetration of autonomous vehicles (AV) on the road and lower car ownership to

reach profitability. These two trends go hand-in-hand.

It is estimated that within 10 years of regulatory approval of fully autonomous vehicles (or by

2030) , c. 95% of all US passenger miles will be served by TaaS providers who will own and

operate fleets of AVs resulting in private car ownership estimated to drop by c. 80%2.

The cost of operating a ride-sharing business is expected to dramatically decrease when AVs

become common. This is due to:

1. Currently, the driver is the most expensive element of a ride

2. Autonomous car utilisation could be as efficient as 50%

3. AVs are expected to be able to minimise the number of accidents, which would

decrease repair and insurance costs

The demand for private car ownership is also expected to take an additional hit as the

younger generations are more familiar with subscription services and their disregard for car

ownership as a status symbol. The advent of AVs could create major shifts in the ride-sharing

market, paving way for much better prospects of earnings in the ride-sharing industry.

Drilling down to a more micro-level, we draw cues from our analysis of Lyft and Uber ,

the only ride-sharing companies that have disclosed financial and operational information

publicly. Drawing insights from Uber, the only profitable ride-sharing operation we know of,

we identify a few key elements that could help ride-sharing operators become profitable.DBS Asian Insights

SECTOR BRIEFING 75

18

What does it take to build

a profitable ride-sharing

business?

Dominance Scale

Dominance in key markets Scale allows bigger

keeps sales & marketing players to reduce

expenses and rider insurance, payment and

incentives in check fixed operating fee as a

percentage of revenue

Source: DBS Bank

Market Dominance

A business is said to be enjoying a “network effect” when the product or service it offers

becomes more valuable as more users start using said product / service. Most tech giants in

the world like Amazon, Google and Facebook cite their user networks as the key source of

their competitive strength. This further signifies the importance of the “network effect” for

tech companies.

Ride-sharing heavily benefits from indirect-networking effect. Getting more riders onboard

may not necessarily be beneficial for the riders, as there could be instances where riders

crowd out each other (recall your experience of trying to hail a taxi on a stormy day).

However, the more riders a ride-sharing facilitator has on its platform, the better its ability

to attract a greater proportion of drivers. With more drivers, the user experience of the

rider improves with lower waiting times and limited chances of crowding each other out,

or encountering surge pricing (surge pricing is when the normal fare is adjusted upwards

to reflect the gap in rider demand and driver supply), allowing the ride-sharing facilitator to

attract more riders to its platform. With more riders, driver earnings on the platform also

edge up as the number of trips improve, attracting more drivers to the platform. Hence, first

mover advantage that allows a player to rake up riders and drivers and dominance in the

market a player operates in can be considered critical success factors for ride-sharing players.DBS Asian Insights

SECTOR BRIEFING 75

19

Network effect of ride-sharing platforms

Liquidity Network Effect

More Driver

5 drivers supply

1

More rides Lower wait

4 per hour and

higher earnings $ More

liquidity

times and

fares 2

potential for

drivers

More

3 riders

Source: Uber

In our view, a dominant position in key ride-sharing markets helps the ride-sharer in

two key ways:

1. Minimise rider incentives

A dominant player can minimise its spending on rider incentives, and sales and

marketing expenses. Instead, it can compensate for the lack of discounts and

promotions through a better rider experience (lower wait times, highly rated drivers

etc), lower fares and reduced probability of encountering surge pricing. Second tier

players on the other hand, have to continuously churn out promotions and discounts to

keep riders on the platform and compensate for a potentially poor rider experience.

2. Minimise driver incentives

With higher earnings derived from the platform supported by a higher rides per hour

ratio, ride-sharing operators can also look into the possibility of easing incentivesDBS Asian Insights

SECTOR BRIEFING 75

20

offered to drivers on the platform. However, this would have to be done carefully and

to a lesser degree than minimising sales and marketing, and rider incentives. This is so

as regulatory issues could pop up if driver pay is trimmed substantially. Smaller players

on the other hand, have to compensate for potentially lower hourly earnings of drivers,

by offering higher driver incentives to prevent drivers from churning, which could

exacerbate the situation of these players even further.

Uber has operations across 700 cities, and is a dominant player in most of the markets

it operates in. According to data shared by the company, Uber controls > 65% of ride-

sharing market share in North America, Latin America, Europe, Australia and New Zealand.

This includes major ride-sharing destinations in these markets such as New York City, San

Francisco, London and other key metropolitans. The company also claims to have > 50%

market share in India and Middle East and North Africa (MENA) regions.

We believe Uber’s dominant position regionally and in some of the biggest ride-sharing

markets globally is one of the key forces driving its path to profitability. For instance, sales

and marketing, and rider incentives accounted for only 28% of Uber’s revenues in 2018, vs.

37% at Lyft. This was based on Uber’s statistics, which states that it controls < 35% of the

North American market (Lyft claims to have a market share of c. 39% in North America).

As Uber has secured a critical mass in its key ride-sharing markets in the US, it can secure

customer loyalty through a better rider experience, availability in most major cities vs. limited

availability of Lyft’s services in certain cities. This in turn allows Uber to start trimming its rider

promotions in selected markets in the US without major user churn.

Uber’s strong network effect can also be seen through its operating statistics. Uber riders

on average completed over c. 57 trips annually, c. 70% higher than the average number of

rides of Lyft users. Uber drivers also completed as many as c. 1,338 trips in 2018, almost as

much as 4 times the number of rides completed by a driver of Lyft on average.

Uber’s network effect is reflected in its operating statistics

in m Uber Lyft

Number of riders 91 18.6

Number of drivers 3.9 1.9

Number of rides 5,220 619

Annually

Rides per driver 1,338 326

Rider per rider 57 33

Riders per driver 23 10

Source: Companies, DBS BankDBS Asian Insights

SECTOR BRIEFING 75

21

Furthermore, we believe that Uber’s decision to divest its operations in China and South East

Asia, where it was a second tier player struggling to secure adequate market share, may

have been motivated by the lack clarity on a path towards sustainable profitability.

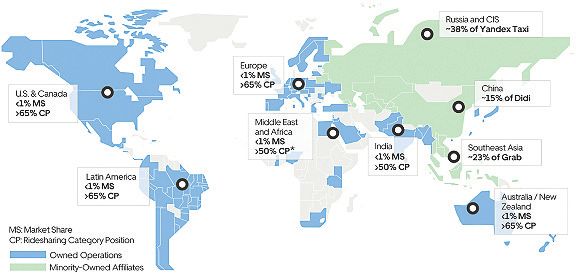

Uber dominates the global ride-sharing market

Russia and CIS

~38% of Yandex Taxi

Europe

65% CP China

US & Canada

65% CP

Middle East

and Africa

50% CP

50% CP

Latin America

65% CP Australia/

New Zealand

65% CP

CP: Ride sharing category position

Owned operations

Minority-owned affiliates

Source: Uber

Whilst it’s difficult to define a level of dominance that allows a ride-sharer to become

profitable, we estimate that at > 60% market share in a country, including the key

metropolitan ride-sharing markets, ride-sharers would start to weave the benefits of the

network effect, allowing the ride-sharer to gradually start curtailing its incentives and

heavy advertising expenses, without major loss of market share. Trimming driver incentives

however, would depend on the regulatory background in the region and would need to be

done at a much slower pace than rider incentives.

However, despite the benefits of the network effect, we believe that the path to profitability

of a dominant ride-sharer would greatly depend on the share of rider and driver incentives.

Dominant ride-sharers with a much greater share of driver incentives than rider incentives

are likely to take longer to reaching profitability, given the slower pace of curtailing driver

incentives vis-à-vis rider incentives, to avoid an increase in driver churn.DBS Asian Insights

SECTOR BRIEFING 75

22

Scale advantage

Scale is another key driver, driving the profitability of ride-sharers. Like in any other industry,

scale allows ride-sharers to realise economies of scale and yield better cost efficiencies. This

in turn allows bigger ride-sharers to realise better margin profiles. Uber for example, enjoys

gross margins of 53% vs. 43% at Lyft, largely stemming from Uber’s ability to realise better

cost efficiencies at a gross margin level and a potentially lower cost structure in markets like

Latin America, India and MENA.

A comparison of Uber’s better margin profiles clearly signifies the importance of scale in ride-

sharing. We believe Uber’s better margin profile is derived from three key sources:

1. Insurance expenses

Insurance is one of the biggest cost items for ride-sharers. Uber uses a small number of

insurance providers (Global insurance giant, AXA for example, provides coverage across

UK, Europe, certain MENA regions and Hong Kong) to provide liability insurance across

the globe. Uber also operates its captive subsidiary for insurance underwriting, in a small

number of markets, allowing Uber to trim its insurance costs even further. Given the

global scale of Uber’s operations, Uber is able to negotiate better terms on insurance

contracts with its key insurance providers, allowing Uber to lower its insurance expenses

as a % of revenue. Furthermore, liability insurance by ride-sharers is not a legislated

requirement in some of the markets (especially emerging) that Uber operates in. Whilst,

Uber provides liability insurance coverage in most of its markets, it is likely that in some

markets Uber incurs no insurance expenses. This should allow Uber to improve gross

margins derived from those regions.

2. Lower payment processing fees

Expansions across the globe is likely to have allowed Uber to secure better terms on

payment processing from global payment processing giants given the higher volume of

transactions. Uber also accepts cash as a mode of payment across 130 cities including

India, Latin America and Africa, which to our understanding are not subjected to any

payment processing fees (Uber’s fee on cash rides is deducted from the fare available

to drivers on rides done through digital means, hence Uber does not incur payment

processing fees on cash rides). News articles suggest that cash rides account for c.

65% of rides in India and c. 25% in Brazil, which should allow Uber to lower payment

processing fees on a per ride basis. Lyft on the other hand is 100% cashless.

3. Lower platform related expenses as a % of revenue

Platform related expenses tend to be mostly fixed in nature and hence as operations in

a region expands, platform expenses edge down as a percentage of revenue.DBS Asian Insights

SECTOR BRIEFING 75

23

Uber’s scale allows it Gross Margin and OPS for 2018

to yield better margins

and cost efficiencies

Source: Uber, Lyft, DBS Bank

At what scale would ride-sharers start to see the benefits

of scale?

Uber’s ride-sharing segment attained profitability in 2018, after raking up revenues of c.

US$9.2 bn through c. 5.2 bn rides. Having embarked on an aggressive expansion plan to

expand its reach globally, Uber’s ride-sharing segment is likely to have witnessed delays in

reaching profitability as expansions typically translate to higher sales and marketing, and

operational expenses at the initial stages of entry into new regions. Lyft on the other hand,

is expected to generate an operating profit before corporate expenses from its ride-sharing

segment over the next 2-3 years, with revenues of US$4.5-5 bn, with an annual ride count

of c. 1.1-1.3 bn.

Drawing from our analysis of Uber and Lyft, we believe the scale required to attain

profitability largely depend on two key factors:

1. If the ride-sharer is regional or country specific

2. The expansion strategy of the ride-sharer

Extrapolating from our analysis of Uber and Lyft, we estimate that Ride-sharers operating

in South East Asia may need to generate c. US$1.3-1.7 bn in revenues before reaching

profitability, provided that expansions within the region remain minimal.

In our analysis we assume, to reach profitability outside US, a country-specific operator

would need to rake at least 30 m riders (marginally higher than the rider base of Lyft, when

Lyft is expected to reach profitability), whilst a regional operator may need to secure at leastDBS Asian Insights

SECTOR BRIEFING 75

24

45 m riders (half of the rider base of Uber). We believe that regional operators would need

a higher rider base to reach profitability, as regional expansions remain expensive and such

expansions often tend to encounter greater competitive pressures.

Whilst our analysis is based on a series of assumptions, we do note that Grab, which is on

track to generate revenues of US$2 bn over 2019, is already said to be profitable in certain

mature markets (most mature markets for Grab include Malaysia and Singapore) in the

region in its ride-sharing operations.

Uber’s network effect is reflected in its operating statistics

Scale to profitability Uber Lyft SEA India

Revenue (U$ m) 9,182 4,078 1,729 834

Riders (in m) 91 27 45 30

Rides (in m) 5,220 1,049 1,778 1,192

Revenue per Rider (US$) 101 154 38 28

TAM population(in m) 4,100 328 642 1,339

TAM penetration 2% 8% 7% 2%

Proportion of US fares 25% 18%

Assuming 45m riders to breakeven regionally and 30m riders to breakeven in a given

country. Annual trip count per rider is set at 40.

Source: Companies, DBS Bank

The expansion strategy also comes into play in driving a ride-sharers’ profitability. Typically,

expansions into new cities require heavy marketing and promotional expenses, along with

heavy rider and driver subsidies if the market is already served by a ride-sharing operator.

Operational expenses including insurance and platform related expenses also tend to edge

up at the early stages of entry into new cities. Expanding into new countries tends to be

even more expensive at the initial stages. Whilst expansions and gaining scale is beneficial if

the ride-sharer can secure a dominant position in these new regions, expansions inevitably

would cause delays in the timing of reaching profitability for the ride-sharer.

Confronting arguments against the

profitability of Ride-sharing

Several arguments have been laid out, suggesting that ride-sharing is not a sector prone to

generate sustainable economic profits. We look at some of these arguments in depth and

share our views as to why we think otherwise.DBS Asian Insights

SECTOR BRIEFING 75

25

Multi-homing could lead to a perpetual need for incentives

Multi-homing, refers to a situation in which multiple platforms are simultaneously used

by users, as the cost of switching between platforms remains low or non-existent. For

example, the cost for a rider or a driver of using both Uber and Lyft are bare minimal:

the process is as simple as downloading and registering with the two apps.

Multi-Homing presents a real risk to the platform developer, as users often tend to make

comparisons between the platforms before making their decision of which one to choose.

In ride-sharing this means that riders may choose to go with the platform that gives them

the best discount, while drivers could turn to the platform that allows them to yield the

best hourly pay. When multi-homing is commonly prevalent, it could become challenging

for a platform to generate a profit from its core business as incentives need to be handed

out to platform participants to keep them within the platform.

Whilst, multi-homing remains a reality for ride-sharers, several other industries that

witnessed this effect have successfully transitioned to profitability backed by their

innovative strategies and dominance by a few key players. The E-commerce sector

remains a prime example.

The cost of switching between E-commerce platforms remain as little as searching for

the name of the platform in your web browser. However, Amazon and Alibaba have

managed to emerge as winners in E-commerce regionally, leveraging on their early entry

to the market, dominant network that was hard to be replicated and service innovations

such as “Amazon Prime”, which improved customer loyalty to the platform.

In ride-sharing, the availability of a network itself becomes a key switching cost for

platform participants, allowing the operator with the biggest network to flourish in the

long run. For example, the cost of switching from a first tier ride-sharer to a second tier

ride-sharer for a small discount could be longer wait times or poorly rated drivers, which

may deter users from transitioning between platforms. Ride-sharers have also launched

short-term initiatives such as incentives for drivers that complete a certain number of

trips without cancellations or discounts for riders that complete a certain number of

rides. These could also help ride-sharers improve loyalty and expand on their network

dominance, at which point such incentives can be trimmed down.

Low barriers of entry translate to lower economic profits in

the long run

Ride-sharing industry relies on digital networks where all the core operations are algorithm

driven. The service offering of ride-sharing is also a commodity: The service of taking a

person from point A to point B, and offers little room for key players to differentiate based

on their service offerings. Hence, theoretically a new player with the right algorithm and

enough funds to secure riders and drivers should be able to disrupt the ride-sharing market.DBS Asian Insights

SECTOR BRIEFING 75

26

Why would this not work? Despite the standardized service offering, the network of a ride-

sharer is its key asset and the key barrier to enter the ride-sharing industry. Just like how it

is difficult for a new E-commerce player in China to replicate the buyer / seller networks of

Alibaba, which Alibaba has taken years to develop and invested tons of money in, a new

player would struggle to build a similar network of that of a dominant ride-sharing operator,

making it difficult to compete effectively.DBS Asian Insights

SECTOR BRIEFING 75

27

Playbook for smaller ride-

sharing operators

W

hile dominance and scale remain pivotally important in ride-sharing to attain

profitability, we do believe smaller operators too can share the ride-sharing

pie with bigger operators, with the right strategies in place. In the following

section, we discuss three types of distinct strategies smaller ride-sharing

companies may opt for.

Playbook for smaller

operators

Niche segmental play Selective regional play Ecosystem play

Dominate niche sub- Dominate smaller cities/ Leverage the ride-sharing

segments in ride-sharing regions underserved by platform and user base to

underserved by market leading ride-sharers diversify and venture into

leaders other profitable segments

Source: DBS Bank

Niche segmental play

Smaller operators can gain dominance in niche sub-segments of the ride-sharing market

that are typically underserved by bigger ride-sharing operators. Ola, the leading ride-sharing

player in India, for example, managed to maintain its leading status in India despite Uber’s

entry and disruption in 2013. This is partially so as Ola focused on three-wheelers (Auto-

rickshaws), one of the most commonly used modes of transport in India. Ola also allowedDBS Asian Insights

SECTOR BRIEFING 75

28

users of its platform to pay by cash, a feature that was not available at Uber until two years

after its entry. This has allowed Ola to retain and develop its market share even further

in India where credit card penetration even in major cities remain below c. 15%3. Auto-

rickshaws contributed c. 15% to Ola’s topline in 20174, just three years after its launch and

Ola enjoys a substantial share of the ride-sharing market in India as a result of its focus on

niche market segments.

Selective regional focus

Smaller players can also choose to focus on smaller regions / cities underserved by bigger

players and limit their competitive play only to such areas. This would provide room for

smaller players to curtail sales and marketing, and rider incentives in these regions and

paving way for margin expansion and profitability.

Ecosystem play

Ride-sharers inherently enjoy a few features coveted by many traditional players in today’s

digital world:

1. Customers connect with ride-sharers purely via digital means, allowing ride-sharers to

collect valuable user data

2. Customers of ride-sharing platforms are often the much sought after millennials and

digital natives that are well versed with technology and are willing to try out new digital

innovations

3. Ride-sharing platforms tend to be highly scalable

Data is the future of TaaS, and small ride-sharers too are poised to benefit depending on

how they manage and share data within the mobility ecosystem. These key features offer a

great avenue for ride-sharers with a sizeable following to leverage their platform to venture

into other more profitable segments such as product distribution for traditional sectors,

offering of data analytics as a service etc that could potentially offset losses from their ride-

sharing business.

Prominent ride-sharers like Uber, Grab and Go-Jek have already started to position

themselves as “Platforms” as opposed to simple-ride-sharing apps.

Uber’s ventures into meal-delivery through Uber Eats and logistics through “Uber Freight”

and Grab’s ventures into payments and banking through Grab Pay and micro-loan facilities

are some of the examples of ride-sharers venturing beyond transport in search of better

profitability elsewhere.

Smaller players like Go Jek have gone even further, positioning themselves as “SuperApps”DBS Asian Insights

SECTOR BRIEFING 75

29

catering to an array of different customer demands. Go-Jek for instance allows users to get

maids, personal stylists, personal massage therapist and even auto mechanics on demand

via its app.

Possibilities remain endless for ride-sharers bold enough to venture beyond their traditional

sector, establish partnerships across sectors and explore possibilities of monetizing their

greatest asset base: the ride-sharing platform.DBS Asian Insights

SECTOR BRIEFING 75

30

Regulations: The biggest

overhang for ride-sharers

R

ide-sharers remain highly vulnerable to regulatory changes. With the uptake

of ride-sharing based on digital means, the number of passengers relying on

traditional taxi services (where you get to the street and hail a taxi passing by)

for their transportation requirements would come down. As this is likely to drive

traditional taxi services out of business, drivers are more likely to sign up with digital

platforms like Uber and Lyft.

Under such circumstances, even though drivers are freelancers and not dedicated drivers

of taxis, they rely on the platform enabler as their employer. Earnings from the ride-

sharing platform becomes the sole source of livelihoods for these drivers, which makes

it increasingly difficult for ride-sharers to improve their take rates (realized revenue as a

percentage of gross bookings) as doing so would translate to lower pay for drivers. News

of poor pay offered by ride-sharing services are plentiful in the media which has caught

the attention of regulators around the globe. Regulators are mulling options ranging from

fixating hourly pay/fees per ride for drivers to drawing regulation classifying drivers of ride-

sharing platforms as employees of ride-sharing platforms.DBS Asian Insights

SECTOR BRIEFING 75

31

Regulatory stance on ride-sharing across the globe

Country Rising concerns Regulatory changes

United States • 18% of Uber drivers in New York City • Minimum wage of drivers of ride-

were eligible for food stamps offered sharers was increased to US$ 17.22 an

to low-income households in 2018 hour vs the current average of US$

11.90 in New York City

• 6 driver suicides were reported from • Issuance of new licenses for ride-

2017-18 sharers has been frozen for a period

of one-year as the Taxi and Limousine

Commission studies the ride-sharing

industry.

Indonesia • Several protests in the country against • Fixed rate bands introduced for

poor pay and low-rates charged by ride-sharers for motorbikes and cars.

ride-sharing companies Motorbike ride-sharing rates should

be between IDR 1,850-2,600 per km

(vs. IDR 1,200-1,400 currently) and car

rates set at IDR 3,500 - 6,000 per km

depending on the zone of operation

• “No-Go” zones for ride-sharers – • Rates are to be reviewed every quarter

Drivers of traditional taxis have set

areas where ride-sharing providers are

not allowed to operate in

United Kingdom • Uber drivers in London, Nottingham • Uber was banned in the city of London

and Birmingham staged a protest and by “Transport for London” in 2017

a strike in 2018 demanding a GBP2 following concerns over failure to

per mile increment and reduction in support government initiatives to

commissions charged by Uber battle crimes in the city through

sharing data and lack of corporate

responsibility

China • Three passengers using the services of • Mandated that driver backgrounds

DidiChuxinghave been murdered by and vehicles should meet standards

their drivers between 2016-2018 established by the Chinese Ministry of

Transport

• Commercial license (which has higher

costs attached to it as opposed to

private vehicles) are now mandatory

for drivers signing up with Didi

Several jurisdictions • In several jurisdictions regulators are

mulling if the drivers of ride-sharing

platforms meet the definition of

“Employees” and if not how the

definitions can be altered

Source: DBS Bank, Various media reportsDBS Asian Insights

SECTOR BRIEFING 75

32

Drawing insights from

E-commerce to Ride-sharing

W

e compare the business models of ride-sharing vs. E-commerce, the most

established disruptive industry globally, to draw key insights over the

trajectory of ride-sharers going forward.

Prior to drawing parallels between the two sectors, we wish to highlight a few key

differences between the two sectors at their early stages of growth:

1. E-commerce players benefited from much more diverse streams of revenue

from early on

E-commerce players adopted different business models: marketplace and product,

and generated revenues from a portfolio of service offerings including advertising,

sales commissions, listing fees, data analytics etc. Ride-sharers on the other hand

operate on a more uniform business model and generate revenues primarily through

the taxi fares.

2. TAM for E-commerce is much broader

E-commerce could be extended to most retail product categories ranging from books,

consumer electronics and clothing to fresh produceand groceries. TAM for ride-

sharing however is comparatively limited. As mentioned earlier, ride-sharers primarily

target short-distance private transportation needs of users, of which the TAM is

considerably smaller.

However, despite these differences, we believe insights from the more matured

E-commerce segment, would shed some light on the trajectory of the evolution of the

ride-sharing industry.

In the heydays of E-commerce, dominant players like Amazon and Alibaba reported high

double digit growth in the value of goods transacted through their platforms (GMV)

supported by improving penetration of E-commerce and market share gains from smaller

operators. Dominant players like Alibaba still record growth 25%+ growth on a year-on-

year basis on GMV on its Chinese retail platforms.DBS Asian Insights

SECTOR BRIEFING 75

33

Ride-sharers too have witnessed rapid growth since the start of the ride-sharing model

back in 2010. With the penetration of ride-sharers in most markets still remaining below

1%5 of total passenger vehicle trips of less than 30 miles, we believe ride-sharers are set

on a similar growth trajectory to the growth in GMV E-commerce players witnessed in

their early days.

Growth in gross Gross bookings and GMV growth comparisons

bookings going strong

Source: Companies, DBS Bank

When E-commerce was introduced, it offered customers the convenience of shopping

from home, access to a wide range of products unlikely to be available through a typical

retail store and access to similarly priced, if not cheaper, products. These features were key

drivers behind the uptake of E-commerce that set penetration and GMV of E-commerce

on a trajectory of super fast growth.

Ride-sharing, we believe shares most of these features of E-commerce. Ride-sharing offers

customers the convenience of hailing a ride to their doorstep and allows customers to

choose from a variety of riding options that were previously unavailable (Shared rides or

rentable scooters). Ride-sharing also offers their services at a similar price, if not cheaper

to those of traditional private means of transportation such as taxis. We believe these

features of ride-sharers would continue to drive the penetration of ride-sharing over the

medium term, presenting a steady growth trajectory in gross bookings for ride-sharers.

Rising congestion in metropolitan cities around the world, outdating public transportation

infrastructure in major cities, growing proportion of millennials and digital natives entering

the work force, would further support growth in penetration of ride-sharing as a means

of transport, setting the sector on a trajectory of super-fast growth akin to that of

E-commerce.DBS Asian Insights

SECTOR BRIEFING 75

34

However, the quantum of revenue that can be derived regionally is lower in comparison

for ride-sharers in comparison to E-commerce, as there is a physical limit to the number of

drivers and riders that can provide and use ride-sharing services in a given region and the

ride-sharer’s growth in the region is limited by this. The ceiling for growth for E-commerce

players on the other hand, is much higher, as E-commerce platforms can be easily scaled

up to include more products and services.

Regulatory restrictions to limit take rate growth for ride-

sharers

Ride-sharers enjoy much better take rates than their E-commerce counterparts, as GMV,

comprising of the value of all goods traded through an ecommerce platform, often tends to

be significantly higher than gross bookings, which comprises of fare, taxes and driver pay.

Take rate for ride- Take rates for ride sharers vs. E-commerce

sharers is almost

5x higher than

E-commerce

Source: Companies, DBS Bank

However, going forward we believe there is limited headroom for ride-sharers to improve

their take rates substantially. Unlike E-commerce, which remains laxly regulated with

ample head room to improve its GMV take-rate (take rate of marketplace operators

depend on commissions, and the uptake of other services such as advertising, which

remain less vulnerable to regulations), growth in the take rate of ride-sharers is likely to be

capped by regulations.

In E-commerce, sellers on the platform often maintain a presence both online and

offline, and any attempt by the E-commerce platform to improve its take rate, by way of

increasing commissions or rates on advertising for example, are unlikely to significantly

impact the profitability of sellers on E-commerce platforms. Regulatory environment

surrounding E-commerce also is fairly lax, providing ample head room for E-commerce

players to improve their take rates and profitability if need be.DBS Asian Insights

SECTOR BRIEFING 75

35

Ride-sharing on the contrary is quite different. Most drivers on ride-sharing platforms are

dependent on the earnings made through the ride-sharing platform as their livelihoods.

Any attempt by ride-sharers to improve their take rate substantially would come at the

cost of lower pay for drivers, which at some point could be regulated. News of inadequate

pay made by drivers on ride-sharing platforms are plentiful and has caught the attention

of regulators around the globe, who are mulling fixating driver pay rates or contemplating

the recognition of drivers as employees of ride-sharers. Regulations on driver pay could

cap or even reduce the take rate of ride-sharers, impacting revenues and profitability

adversely. A classification or drivers as employees could be even worse resulting in heavy

staff costs for ride-sharers, substantially impacting profitability.

Can Automated Vehicles (AVs) increase the take rate of

ride-sharers?

The take rate of a ride-sharing business is expected to increase significantly when AVs

become common since driver pay is the most expensive element of a ride at present,

accounting for c. 75% of the total fare of a ride. All major ride sharers are in the process

of developing and testing AVs. However, the likes of Waymo (Alphabet’s self-driving arm)

and Cruise (General Motors), that lead the AV race are already trialing ride-sharing services

with their self-driving technologies, which could present a threat to existing ride-sharers.

Automobile manufacturers like Tesla have also expressed an interest in offering ride

sharing services through its vehicles as announced recently.

Progress in the self-driving space is measured by the average number of miles driven

before a manual override by a human driver is required. Waymo is almost 2x ahead of its

closest competitor by that metric.

Milles per manual intervention

Waymo 11,018

Cruise 5,205

Zoox 1,923

Nuro 1,028

Aurora 82

Toyota 2.54

Benz 1.47

Apple 1.15

Uber 0.35

Source: State of California department of motor vehiclesYou can also read