Riviera Investor Presentation August 23, 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Riviera Investor Presentation August 23, 2018

Forward-Looking Statements and Risk Factors Statements made in this presentation that are not historical facts are “forward-looking statements.” These statements are based on certain assumptions and expectations made by Riviera Resources, Inc. (“Riviera” or the “Company”) which reflect management’s experience, estimates and perception of historical trends, current conditions, and anticipated future developments. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond the control of the Company, which may cause actual results to differ materially from those implied or anticipated in the forward-looking statements. These include risks relating to financial and operational performance and results of the Company, continued low or further declining commodity prices and demand for oil, natural gas and natural gas liquids, ability to hedge future production, ability to replace reserves and efficiently develop current reserves, the capacity and utilization of midstream facilities and the regulatory environment. These and other important factors could cause actual results to differ materially from those anticipated or implied in the forward-looking statements. Please read “Risk Factors” in the Company’s Registration Statement on Form S-1 and other public filings. We undertake no obligation to publicly update any forward- looking statements, whether as a result of new information or future events. Reserve Estimates The Securities and Exchange Commission (the “SEC”) permits oil and natural gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves that meet the SEC’s definitions for such terms. The Company may use terms in this presentation that the SEC’s guidelines strictly prohibit in SEC filings, such as “estimated ultimate recovery” or “EUR,” “resources,” “net resources,” “total resource potential” and similar terms to estimate oil and natural gas that may ultimately be recovered. These estimates are by their nature more speculative than estimates of proved, probable and possible reserves as used in SEC filings and, accordingly, are subject to substantially greater uncertainty of being actually realized. These estimates have not been fully risked by management. Actual quantities that may be ultimately recovered will likely differ substantially from these estimates. Factors affecting ultimate recovery include the scope of the Company’s actual drilling program, which will be directly affected by the availability of capital, drilling and production costs, commodity prices, availability of drilling services and equipment, lease expirations, transportation constraints, regulatory approvals, field spacing rules, actual drilling results and recoveries of oil and natural gas in place, and other factors. These estimates may change significantly as the development of properties provides additional data.

Non-GAAP Measures Adjusted EBITDAX The non-GAAP financial measure of adjusted EBITDAX, as defined by the Company, may not be comparable to similarly titled measures used by other companies. Therefore, this non-GAAP measure should be considered in conjunction with net income (loss) and other performance measures prepared in accordance with GAAP. Adjusted EBITDAX should not be considered in isolation or as a substitute for GAAP. Adjusted EBITDAX is a measure used by Company management to evaluate the Company's operational performance and for comparisons to the Company's industry peers. Management also believes this information may be useful to investors and analysts to gain a better understanding of the Company's financial results. EBITDA The non-GAAP financial measure of EBITDA, as defined by the Company, may not be comparable to similarly titled measures used by other companies. Therefore, this non-GAAP measure should be considered in conjunction with net income (loss) and other performance measures prepared in accordance with GAAP. EBITDA should not be considered in isolation or as a substitute for GAAP. EBITDA is a measure used by Company management to evaluate the Company's operational performance and for comparisons to the Company's industry peers. Management also believes this information may be useful to investors and analysts to gain a better understanding of the Company's financial results. PV-10 PV-10 represents the present value, discounted at 10% per year, of estimated future net cash flows. The Company’s calculation of PV-10 herein differs from the standardized measure of discounted future net cash flows determined in accordance with the rules and regulations of the SEC in that it is calculated before income taxes and including the impact of helium, rather than after income taxes and not including the impact of helium, using the average price during the 12- month period, determined as an unweighted average of the first-day-of-the-month price for each month. The Company’s calculation of PV-10 should not be considered as an alternative to the standardized measure of discounted future net cash flows determined in accordance with the rules and regulations of the SEC.

Table of Contents Slides

Riviera Resources, Inc. Overview

Company Overview 5-8

Upstream Asset Overview 9

Proved Reserves 10

Upstream Benchmarking 11-14

Blue Mountain Midstream Overview 15-16

Balance Sheet and Buybacks 17-18

Riviera Upstream Overview 20

Upstream Growth Assets

NW STACK 22-25

Arkoma 26-28

East Texas 29-32

North Louisiana 33-35

Upstream Long Life Low Decline Assets

Hugoton / Jayhawk Plant 37-38

Michigan / Illinois 39

Uinta Basin (Drunkards Wash) 40

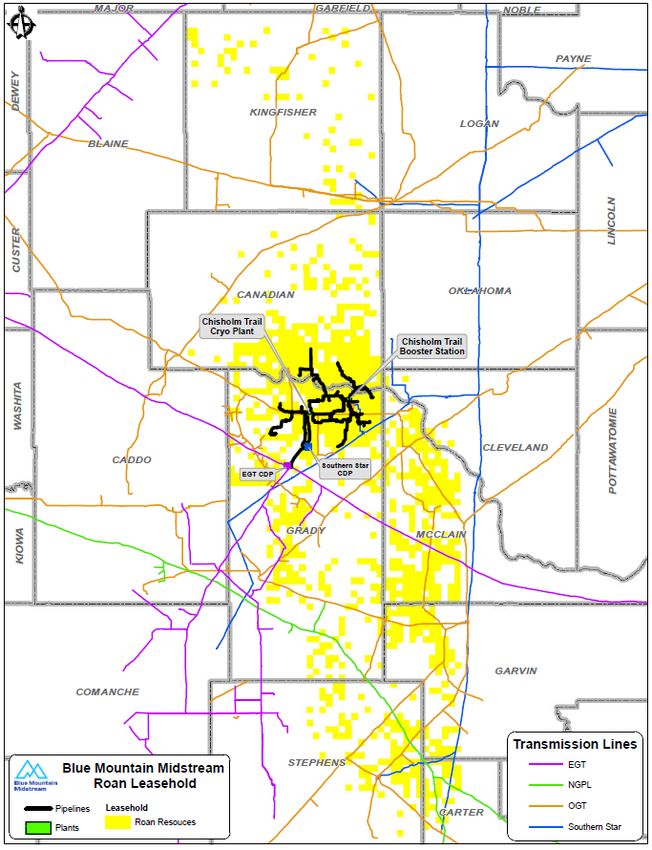

Blue Mountain Midstream LLC (wholly owned subsidiary)

Business Overview 42-45

Operational Overview 46-47

Commercial Overview 48-49

Financial Overview 50-51

Guidance Update 53-56

Commodity Hedge Portfolio 57-58

Capital Structure 59

Leadership 60-61

Riviera Resources – Recent Developments

Riviera Resources (Riviera or RVRA) recently spun-out from Linn Energy, Inc (LNGG) to unlock the sum of the

parts Net Asset Value

Riviera is a newly formed independent company focused on efficiently operating its mature low-decline

production, developing its growth-oriented assets (including Blue Mountain Midstream LLC), and returning

capital to shareholders

Based on recent trading, we believe RVRA is trading at a discount to its sum of the parts Net Asset Value

The Riviera Board approved a $100 million share buyback program

Due to encouraging offset activity, Riviera Upstream is initiating a NW STACK drilling program starting Q4 2018

Blue Mountain is working with Riviera Upstream to provide a midstream solution in the NW STACK

Riviera Upstream is evaluating potential development of its other growth assets, such as Arkoma, East Texas

and North Louisiana

Blue Mountain recently brought a state of the art cryogenic processing plant on-line and is currently processing

~150 mmcf/d

Due to rapidly ramping throughput, Blue Mountain has initiated the engineering and design of a second plant

targeting total throughput of 500 mmcf/d in 2H 2019 to meet projected demand

Blue Mountain has established a stand-alone $200 million credit facility with current capacity of $70 million

LNGG share buyback program has reduced outstanding share count to 76.2 million shares as of the Spin

Transaction

5

Riviera Resources - Overview

Riviera Upstream has 1.6 Tcfe of long life proved developed reserves with a Mid-Year adjusted PV-10 value of $963 million(1)

312 mmcfe/d second quarter 2018 average production

11% base production decline(2) (mature asset base declines: Hugoton 6%, Michigan/IL 4%; Uinta 11%)

15 year proved developed reserves to production ratio

Additionally, Riviera Upstream has a large undeveloped acreage position in several active basins

NW STACK (~60,000 net acres in Core Focus Area), Arkoma (~37,000 net acres), East Texas (~110,000 net acres), North

Louisiana (~100,000 net acres)

More than 900 potential net locations identified with expected internal rates of return (IRRs) >40%(3)

NW STACK operated rig starting in Q4 2018

Evaluating deployment of additional rigs in other growth basins

Blue Mountain Midstream is a growth-oriented midstream business in the heart of the Merge/SCOOP/STACK play in central OK

More than 80,000 acres dedicated to the system

Anchor producer is well-capitalized and currently running 8 rigs

State of the art cryogenic processing plant with current capacity of 150 mmcf/d growing up to 250 mmcf/d in Q4 2018

Initiated engineering and design of a second plant with additional capacity up to 250 mmcf/d servicing the rapidly growing

Merge play

Targeting additional 3rd party gas gathering, crude gathering, terminals and water handling

Strong balance sheet with no debt, up to $495(4) million of available borrowing capacity, and approximately $100 million in

projected cash as of 9/30/2018

(1) YE 2017 proved reserves as of 8/1/18 with updated pricing of $2.85 per MMBtu for natural gas and $65.00 per bbl for oil, and adjusted for basis pricing, including helium revenue, $7.5MM per year of

third party operating margin at Jayhawk Plant (PV-10 of $75MM) and excluding income taxes. See “Non-GAAP Measures - PV-10” for more information.

(2) Base decline includes both mature and growth assets

(3) Assumed Pricing: $2.85 per MMBtu for natural gas and $65.00 per bbl for oil 6

(4) Includes Riviera Upstream $425 million credit facility, and $70 million of Blue Mountain Midstream LLC $200 million credit facility

Riviera Resources – Sum of the Parts

1 2 3

Balance

Sheet

Current Additional Cash Upstream BMM

Mature / Cash- Future

Growth Assets Acreage Business Credit Credit

Flowing Assets Basins

Dedication Lines Facility Facility

Hugoton NW STACK $200 MM

Michigan Chisholm Trail

Arkoma System Crude credit facility

Drunkards Wash East Texas Gathering / $100 MM with $70MM

Terminals, NW STACK / $425 MM currently

North Louisiana Future projected as of

Jayhawk Plant Water Other credit facility available

Expansions 9/30/18

• 80,000 Acre Dedication

• Current throughput of ~150 mmcf/d

• Proved Developed PV-10: $963 Million(1)

• Initiated engineering and design of 2nd • No Debt

• More than 900 Net Development Locations >

cryogenic plant targeting on-line in 2H 2019 • $100 MM of cash projected as of 9/30/18

40% IRR(2)

• Would increase total processing capacity up

to 500 mmcf/d

(1) YE 2017 proved reserves as of 8/1/18 with updated pricing of $2.85 per MMBtu for natural gas and $65.00 per bbl for oil, and adjusted for basis pricing, including helium revenue, $7.5MM per year of third 7

party operating margin at Jayhawk Plant (PV-10 of $75MM) and excluding income taxes. See “Non-GAAP Measures - PV-10” for more information.

(2) Assumed Pricing: $2.85 per MMBtu for natural gas and $65.00 per bbl for oil

Riviera Resources – Value Proposition

Income Generating Growth Oriented Assets

Assets Requiring Funded by Strong

Minimal Capital Balance Sheet

Northwest STACK

Hugoton Arkoma

Michigan/IL East TX

Uinta North LA

Blue Mountain Midstream

Free Cash Flow

NAV

Returned Through

Growth

Share Repurchases,

Realized

Dividends, and/or

Tenders

Shareholder Returns

8

1 Riviera Upstream – Asset Detail

Proved Developed(2) Proved Developed

Net Production(1) R/P(3)

Reserves PV-10(2)

Upstream Assets Net Acres

(MMcfe/d) (in Years)

(Bcfe) ($ in millions)

Hugoton ~1,100,000 136 842 19 $529

East Texas ~110,000 51 242 13 $137

North Louisiana ~100,000 27 61 7 $78

Michigan / Illinois ~200,000 27 233 23 $85

Arkoma ~37,000 25 111 12 $61

64

NW STACK / other Oklahoma ~110,000 24 7 $51

Uinta ~50,000 22 40 6 $21

Total ~1,707,000 312 1,593 15 $963

(1) Average daily second quarter 2018 actual production

(2) YE 2017 proved reserves as of 8/1/18 with updated pricing of $2.85 per MMBtu for natural gas and $65.00 per bbl for oil, and adjusted for basis pricing, including helium revenue, $7.5MM per year of third

party operating margin at Jayhawk Plant (PV-10 of $75MM) and excluding income taxes. See “Non-GAAP Measures - PV-10” for more information.

(3) R/P is based on proved developed reserves divided by 2018 forecasted production

9

1 Riviera Upstream - Proved Reserves(1)

Total Proved

76% Natural Gas ~1.6 Tcfe of Proved Reserves PV-10 of ~$1.021 Billion

6%

4% 4% 6%

22%

2%

90% 90%

76%

Natural Gas Oil NGL PDP PDNP PUD PDP PDNP PUD

Proved Reserves

as of August 1, 2018 Natural Gas Oil NGL Total PV-10

Bcf MMBbl MMBbl Bcfe ($ in Millions)

PDP 1,115 4 58 1,491 $918

PDNP 96 1 1 102 $45

Total Proved Developed 1,211 5 59 1,593 $963

PUD 54 0 1 60 $58

Total Proved 1,265 5 60 1,653 $1,021

(1) YE 2017 proved reserves as of 8/1/18 with updated pricing of $2.85 per MMBtu for natural gas and $65.00 per bbl for oil, and adjusted for basis pricing, including helium revenue, $7.5MM per year of third

party operating margin at Jayhawk Plant (PV-10 of $75MM) and excluding income taxes. See “Non-GAAP Measures - PV-10” for more information. 101

Riviera Upstream - Benchmarking

Reserve Life

Proved Developed Reserves / Production

(in years)

15

11

10 10

9

8

7

6 6

4

RVRA Company D Company I Company B Company A Company C Company H Company E Company F Company G

Riviera Upstream has the highest ratio of PD reserves to production compared to peers;

To maintain PD reserves, Riviera only needs to replace 7% of its PD reserves annually

Notes:

• Sourced from company 10-K’s and guidance; Proved Developed reserve volumes are from disclosed 2017 SEC reserves; Production is 2018 guidance

• Peers include CHK, CNX, GPOR, LGCY, NFX, RRC, SD, SWN, UNT

111

Riviera Upstream - Benchmarking

PDP Reserve Value vs. Adjusted EBITDAX

7.0x

PDP Reserve Value / Adjusted EBITDAX

(multiple)

4.8x

3.6x 3.5x 3.5x

3.1x

1.9x

N/A N/A N/A

RVRA Company I Company C Company A Company B Company D Company G Company E Company F Company H

Due to Riviera Upstream’s long life reserves, the company should trade

at a higher multiple of adjusted EBITDAX versus peers

Notes:

• Sourced from company 10-K’s and guidance; PDP reserve values are from 2017 10-K filings of SEC reserves. RVRA YE 2017 proved reserves as of 8/1/18 with updated pricing of $2.85 per

MMBtu for natural gas and $65.00 per bbl for oil, and adjusted for basis pricing, including helium revenue, $7.5MM per year of third party operating margin at Jayhawk Plant (PV-10 of

$75MM) and excluding income taxes. See “Non-GAAP Measures - PV-10” for more information; adjusted EBITDAX is 2018 company provided guidance 12

• Peers include CHK, CNX, GPOR, LGCY, NFX, RRC, SD, SWN, UNT1 Riviera Upstream - Benchmarking

Enterprise Value Vs. PDP Reserve Value

Enterprise Value / PDP Reserve Value

(multiple)

2.3x

2.1x

Avg. = 1.7x

1.7x

1.5x

1.4x

1.0x

N/A N/A N/A

Company G Company A Company I Company B Company C Company D Company E Company F Company H

If Riviera Upstream’s enterprise value to PDP reserve value was at the midpoint of peers

(1.7x), it would imply a $1.6 billion valuation for the upstream business only

Notes:

• Enterprise Value sourced from Bloomberg and Yahoo Finance as of 8/16/2018; PDP reserve values are from disclosed 2017 SEC reserves

• Peers include CHK, CNX, GPOR, LGCY, NFX, RRC, SD, SWN, UNT 131

Riviera Upstream - Benchmarking

G&A Vs. Production

G&A / Production

($ / mcfe)

$0.59

$0.52

$0.38

$0.34

$0.27

$0.21 $0.21 $0.22

$0.18

$0.13

Company G Company A Company C Company I Company F RVRA Company B Company H Company E Company D

On a production basis, Riviera Upstream’s G&A is expected to be in-line with peers

Notes:

• Sourced from company 10-K’s and guidance; Riviera G&A is pro-forma for 2019 ($30MM annually); peers’ G&A based on 2018 guidance

• Peers include CHK, CNX, GPOR, LGCY, NFX, RRC, SD, SWN, UNT 142 Blue Mountain Midstream –

Overview

• Blue Mountain Midstream, LLC (“Blue Mountain”), a wholly owned

subsidiary of Riviera, is a growth-oriented midstream business located

in the heart of the Merge/SCOOP/STACK play in central Oklahoma

• Blue Mountain’s first cryogenic processing plant was brought on-line

in June 2018

– The plant has current throughput of ~150 mmcf/d

– At 250 mmcf/d throughput, plant should generate between

$100-$125 million of run-rate EBITDA

• Blue Mountain recently initiated the design and engineering of a

second cryogenic plant to service its rapidly growing throughput

– Targeting 2H 2019 start-up

– Total processing capacity will increase up to 500 mmcf/d

• Proven management team focused on expanding midstream footprint

by leveraging:

– Existing infrastructure base

– Acreage dedications

– Strong commercial relationships

– Well-funded and active customer base

• Future growth opportunities include:

– Recently approved capacity expansions in Merge play

– Additional business lines (e.g., crude gathering / storage, water

and purity NGLs)

– Extend reach across Merge/SCOOP/STACK/NW STACK plays

• Independent capital structure to self-fund future growth opportunities

either as a part of RVRA or as a stand-alone business

15Blue Mountain Midstream –

Key Statistics

Estimated Operating Margin(1) (in millions) Capital Forecast(2) (in millions)

200 200

$22

175

$32

170

150

140

$18

125

125

$75

MMcf/d

100

$53

75

62

61

50

$6

$53

25 $43

$1 $3 $33

$0

0

Q1 2018 A Q2 2018 E Q3 2018 E Q4 2018 E 2016A 2017A 2018E

Estimated Throughput MMcf / Day - Upper Range Field Cryo I Cryo II

Estimated Throughput MMcf / Day - Lower Range

Plant Operating Margin Estimate - Lower Range

Plant Operating Margin Estimate - Upper Range

(1) Operating margin is all Blue Mountain Midstream revenue less direct operating expenses and does not include G&A

(2) Field includes refrigeration facilities 1 and 2 163 Riviera Resources – Pro-Forma Cash 9/30/18

($ in millions)

$17 ($13)

$301 $301 $304

($50)

$254

($40)

$214 Approximately

76.2 million

shares

($115) outstanding

$85-$100

$100 ($15) $15

$85 $85

LNGG Cash LNGG / RVRA LNGG / RVRA LNGG / RVRA LNGG LNGG Share Working RVRA Projected

Balance Adjusted Severance Capital Cash (1) Repurchase Capital / Cash

6/30/2018 EBITDAX before Spending through Other Balance

Severance Spin-Off 8/7/18 9/30/18 (1)

(1) Prior to the spin-off of Riviera from LNGG (the “Spin-off”), $40 million of cash was remaining at LNGG available for use by LNGG to fund certain obligations of the Company arising

after the Spin-Off and prior to any consolidation with Roan Resources LLC (“Roan Resources”). LNGG will transfer any such remaining cash to Riviera (assumed to be $15MM)

prior to any consolidation of LNGG and Roan Resources.

173 Riviera Resources – Share Buybacks

Through August 7, 2018

LNGG returned approximately $800 million to shareholders

($ in millions)

2018 Open Market

Share Repurchases

2017 Open Market Retirement of Profits and Employee Liquidity

Share Repurchases Tender Offer Interest Shares (1) Program(2) Total

$799

$256

$20

$523 $543

$325

$198 $198

Number of

5,690,192 6,770,833 470,630 6,371,234 19,303,389

Shares

Average Price

$ 34.85 $ 48.00 $ 42.34 $40.18 $ 41.40

Per Share

(1) Class A-2 units of LINN Energy HoldCo LLC held by management retired as a result of common stock repurchases, inclusive of tender offer process

(2) Employee liquidity program repurchases represents 1,331,082 vesting restricted stock units of LNGG (“RSUs”) settled in cash prior to shares being issued, 2,598,663 shares previously issued as a

result of vested RSUs and A-2 units converted to Class A common stock of LNGG and subsequently repurchased 1,837,469 shares of Class A common stock of LNGG retired in open market

purchases, and 604,520 RSUs settled in cash for statutory tax withholdings prior to shares being issued 18Riviera Upstream Asset Overview

Focus on Existing Basins

Riviera Upstream Asset Map

Growth

Mid-Continent 312 MMcfe/d ~1.6 Tcfe 11%(1)

Net Production of ~49 MMcfe/d Second Quarter 2018 Proved Developed Reserves Approximate

NW STACK Net Production 76% Natural Gas Base Decline Rate

• Core acreage position of ~60,000 net acres heavily 22% NGL

concentrated in Blaine, Major and Garfield counties, with

significant offset activity

Arkoma

• ~37,000 net acres, 100% held by production (“HBP”)

with large inventory of remaining horizontal locations

East Texas

Net Production of ~51 MMcfe/d

~ 110,000 net acres HBP

Bossier and Cotton Valley development potential Michigan / IL

Two successful horizontal wells drilled in 2017

North Louisiana Uinta

Net Production of ~27 MMcfe/d

~ 100,000 net acres HBP

Four operated horizontal wells drilled in 2016/2017 with Hugoton

excellent results

Long Life, Low Decline

Hugoton Arkoma

NW STACK

Net Production of ~136 MMcfe/d

Base decline of ~ 6%

More than 3,400 infill drilling locations economic at varying

prices above $3.00 per mcf NLA

Jayhawk Plant derives significant value from helium recovery

and third party processing

Michigan / Illinois ETX

Net Production of ~27 MMcfe/d

Base decline of ~4%

Uinta

Net Production of ~22 MMcfe/d

Base decline of ~ 11%

Non-Operated position

(1) Base decline includes both mature and growth assets 20Growth Assets • NW STACK • Arkoma • East Texas • North Louisiana

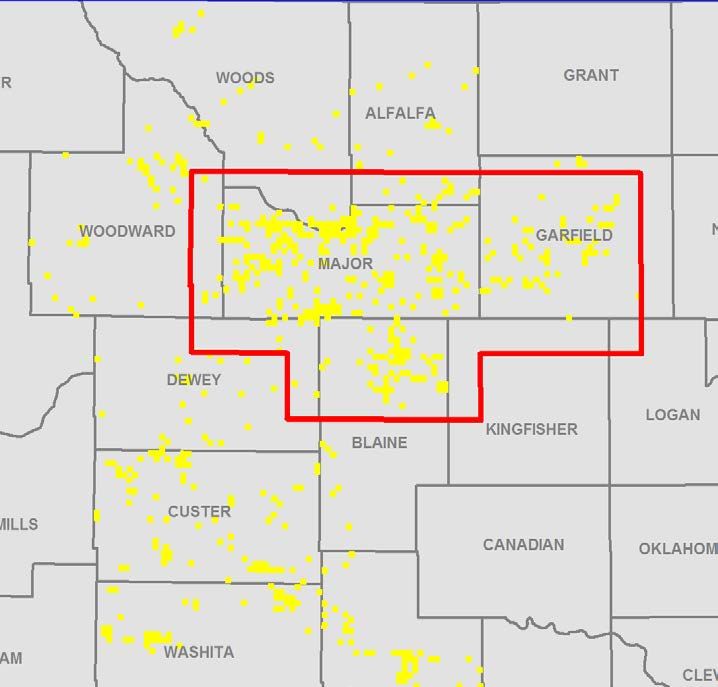

NW STACK - Overview

NW STACK Position

• Approximately 60,000 core net acres within

Riviera’s focus area of Major, Blaine, and

Garfield counties

– Acreage is ~100% HBP and ~75%

operated(1)

– Acreage located in black oil window

– Shallow drilling depths of ~7,500 –

~9,500 feet result in significantly lower

drilling costs than STACK play south of

our core area

– Expected wells costs range from

$3.8MM to $5.8MM

– Potential inventory of >825 net

locations with IRRs >40%(2)

• Additional acreage outside of the core is

being delineated by offset operators

• Riviera has participated in 59 non-operated

wells

NW STACK Core Focus Area

• Plan to initiate operated drilling program in

Q4 2018

(1) Operation control assumed if leasehold >/= 200 acres in a section

(2) Assumed Pricing: Gas: $2.85/Mmbtu; Oil: $65.00/bbl 22NW Stack – Regional Geology Plays & Targets

N GR DPHI S

N

MISS LIME

Osage

NW STACK

STACK Woodford

MERGE S Miss Lime NW STACK NW STACK STACK MERGE

Platform

• Merge to NW STACK is continuous petroleum system

• Massive hydrocarbon column with economic production

throughout

SCOOP – Vertical production from Hunton up through Penn

– Established horizontal success in Meramec and

Osage across core acreage

• Target shallows to the north resulting in higher oil cuts

and lower drilling costs

23NW Stack – Osage

Meramec

Rig Activity

Permit

Analogs

Offset Activity

Hedrick 3-1H (Comanche) Elwell 29-1H (Comanche) Childress 1-26H (Fairway) Newton 1-31H (Fairway) Regier 7-2H (Fairway)

IP30/1000ft:124 Boe/d IP30/1000ft: 229 IP30/1000ft: 82 IP30/1000ft: 189 IP30/1000ft: 91

Oil: 50% Oil: 51% Oil: 56% Oil: 67% Oil: 74%

Shepherd 24-25-1H (Comanche) Martens 5-35 (Red Bluff)

IP30/1000ft: 147 Boe/d IP30/1000ft: 161

Oil: 63% Oil: 66%

Mounds 16-1H (Carrera) Schoeppel 16-2 1H (Chesapeake)

IP30/1000ft: 150 IP30/1000ft: 179

Oil: 61% Oil: 54%

Smart 24-20-17 1H (Tapstone) Gerken 2205 1UMH-33 (Chaparral)

IP30/1000ft: 242 IP30/1000ft: 240

Oil: 37% Oil: 53%

Fenton 17-1H (Corlena) Barbee 2105 1LMH-4 (Chaparral)

IP30/1000ft: 131 IP30/1000ft: 241

Oil: 56% Oil: 68%

Olive Lee 1H-22 (Devon) White Oak 2206 1UMH-36 (Chaparral)

IP30/1000ft: 377 IP30/1000ft: 153

Oil: 20% Oil: 15%

Dennis 28-19-1 1H (Tapstone) Osmus 22&15-20 1H (Chesapeake)

IP30/1000ft: 375 IP30/1000ft: 91

Oil: 15% Oil: 71%

Medill 2015 1-27H (Sandridge) Willamette 30 & 1H (Chesapeake)

IP30/1000ft: 184 IP30/1000ft: 122

Oil: 82% Oil: 63%

Campbell 2015 1-26H23H (Sandridge) Joyce 14-1H (Comanche) Burrell 5-33 MH (Red Bluff) Scheffler 1H-9X (Newfield) Hoskins 5-19-1 1H (Chesapeake)

IP30/1000ft: 98 IP30/1000ft: 94 IP30/1000ft: 185 IP30/1000ft: 163 IP30/1000ft: 204

Oil: 82% Oil: 71% Oil: 56% Oil: 77% Oil: 57%

24

Note: Rig and permit data sourced from DrillingInfo as of August 20, 2018NW STACK - Current Inventory

Type Log NW STACK Inventory

Formations • Base case: 4 wells per section in Meramec and Lower Osage

• Gross locations: ~1,950

• Net locations: ~825

Meramec

• Upside case: 7 wells per section in Meramec, Upper Osage, Lower Osage

• Gross locations: ~5,100

• Net locations: ~2,170

1 Mile

Mississippian

Upper Osage

Base Upside

Case Case

Formation Wells Wells Total

Meramec 4 3 7

Lower Osage

U. Osage 0 7 7

L. Osage 4 3 7

Woodford

Woodford Additional Potential

Hunton

25Arkoma - Overview

Arkoma Position

• Approximately 37,000 net acres mainly in

Hughes and Coal counties, OK

– Acreage is ~100% HBP and ~46%

operated

– Position is fully de-risked in the

Woodford shale with ~420 horizontal

wells drilled on Riviera's acreage

– Base inventory of ~90 net Woodford

locations with average IRR ~30%(1)

– Significant upside in the emerging

Mayes, Caney, and Cromwell plays

• Gas production is very liquids rich with

~27% of revenue coming from NGLs

• Substantial recent offset operations with

~230 horizontal wells drilled since 2015

and 9 rigs currently running in the area

Note: Rig data sourced from DrillingInfo as of July 30 2018

(1) Assumed Pricing: Gas: $2.85/Mmbtu; Oil: $65.00/bbl 26Rig Activity Analogs

Arkoma – Offset Activity Permit

Sherry Pad (BP) Pauline Pad (Trinity Operating) Emma Pad (Trinity Operating) Stewart Pad (BP)

3 Wells drilled in 2015 4 Wells drilled in 2017 2 Wells drilled in 2017 4 Wells drilled in 2017

5,174’ Average Lateral Length 10,298’ Average Lateral Length 7,923’ Average Lateral Length 9,448’ Average Lateral Length

5,802 Mcfd Average Peak IP-30 6,311 Mcfd Average Peak IP-30 6,810 Mcfd Average Peak IP-30 4,621 Mcfd Average Peak IP-30

Ina Pad (BP) Hunt-Garrett Pad (BP)

3 Wells drilled in 2015 3 Wells drilled in 2016

5,646’ Average Lateral Length 8,099’ Average Lateral Length

5,656 Mcfd Average Peak IP-30 8,679 Mcfd Average Peak IP-30

Binns Pad (BP) Sandmann 1H-9X Well (Newfield)

4 Wells drilled in 2017 Drilled in 2015

5,288’ Average Lateral Length 10,709’ Lateral Length

6,995 Mcfd Average Peak IP-30 12,095 Mcfd Average Peak IP-30

Phillips Pad (BP) Payden 1H-12XX Well (Newfield)

2 Wells drilled in 2015 Drilled in 2015

5,927’ Average Lateral Length 10,807’ Lateral Length

6,854 Mcfd Average Peak IP-30 14,856 Mcfd Average Peak IP-30

HB 1-11 Well (Canyon Creek) Ellis Pad (Newfield)

Drilled in 2017 2 Wells drilled in 2015

8,099’ Lateral Length 11,619’ Average Lateral Length

2,876 Mcfd Average Peak IP-30 12,674 Mcfd Average Peak IP-30

LDC Pad (Canyon Creek) Persall 1-8/17H Well (Bravo)

2 Wells drilled in 2017 Drilled in 2017

8,984’ Average Lateral Length 8,934’ Lateral Length

2,607 Mcfd Average Peak IP-30 6,783 Mcfd Average Peak IP-30

Lackey Pad (Bravo Arkoma) Resh 2-8H Well (BP)

2 Wells drilled in 2016 Drilled in 2017

7,515’ Average Lateral Length 5,790’ Lateral Length

2,474 Mcfd Average Peak IP-30 6,524 Mcfd Average Peak IP-30

Bellettini Trust Pad (Bravo Arkoma) Smalley Pad (BP)

3 Wells drilled in 2015 3 Wells drilled in 2015

9,247’ Average Lateral Length 5,555’ Average Lateral Length

4,869 Mcfd Average Peak IP-30 6,945 Mcfd Average Peak IP-30

Ward Pad (Bravo Arkoma) McEntire Pad (Bravo Arkoma) Bowen Pad (BP)

2 Wells drilled in 2016 3 Wells drilled in 2016 3 Wells drilled in 2015

9,883’ Average Lateral Length 9,177’ Average Lateral Length 7,354’ Average Lateral Length

7,619 Mcfd Average Peak IP-30 4,421 Mcfd Average Peak IP-30 6,786 Mcfd Average Peak IP-30

27

Note: Rig and permit data sourced from DrillingInfo as of July 30, 2018Arkoma - Current Inventory

Type Log Arkoma Inventory

• Base case: 5 wells per section in Woodford

• Gross locations: ~230

• Net locations: ~90

Cromwell • Upside: 5 wells per section in Mayes & Caney

• Additional Potential: Cromwell emerging play

1 Mile

Jefferson

Base Upside

Case Case

Caney Formation Wells Wells Total

Cromwell Additional Potential

Caney 0 5 5

Mayes 0 5 5

Woodford 5 0 5

Mayes

Woodford

Hunton

28East Texas – Overview

East Texas Position • Approximately 110,000 net acres

mainly in Limestone, Freestone, and

Personville

Smith counties, TX

– Acreage is ~98% HBP and ~86%

operated

– Significant upside horizontal

development of the Bossier and

Cotton Valley formations

– Significant inventory of >60 net

locations with attractive returns at

current commodity prices

• Recently completed integration of 3D

seismic into Bossier mapping to identify

Overton

additional inventory in the Personville

field

– Bossier well drilled in 2017

yielded excellent results with EUR

~1.5 Bcf/1,000ft

• Overton field is seeing increased

horizontal activity directly offset the

position

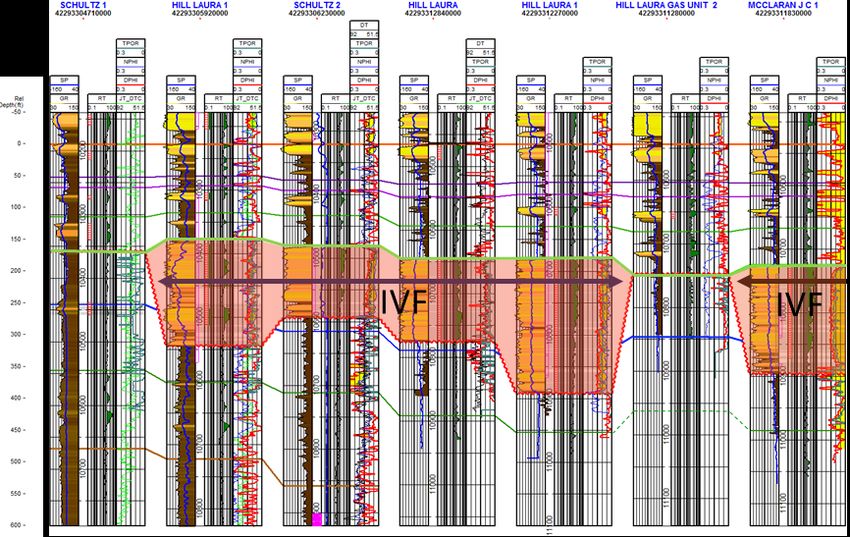

29East Texas – Personville Field

• Bossier target of incised valley fill sandstones Personville Type Log

• 3D seismic tied to well control using waveform modeling combined with

amplitude mapping provide high probability in prediction of IVF sand

presence

Bossier

• Current inventory of 27 net Bossier wells

• Cotton Valley Lime infill horizontal developement provides additional upside

IVF

Bossier – Incised Valley Fill (IVF) Sandstones – Cross Section

Cotton Valley

Lime

Buckner

30East Texas – Overton Field

Type Log

• Overton Field is currently a vertical

producing Cotton Valley field

• There have been 72 offset horizontal

wells drilled in the Cotton Valley Taylor

Sands Taylor L1

Cotton Valley Sands

• Significant amount of offset horizontal

activity generating attractive returns at

current prices Taylor L2

• Approximately 45 net horizontal

development locations identified within Taylor L3

Riviera's acreage position

Taylor L4

• Economics of development benefit from

high liquid yields of approximately 30

bbls/mmcf

31Rig Activity Analogs

Overton – Offset Activity Permit

CV Taylor Sand Gross Isopach Map

McElroy-Swann Moore 1H (Tanos)

Completion Date: 7/3/2017

Peak IP-30: 5.7 MMCFD

LL: 6,737’ Burns 3HR (Valence)

Completion Date: 6/9/2018

McElroy ‘A’- Wilkinson 1H (Tanos) Peak IP-30: Too Recent

Completion Date: 3/23/2017 LL: 5,313’

Peak IP-30: 6.1 MMCFD

LL: 4,803’ Burns-Poole 1H (Valence)

Completion Date: 6/10/2018

Maldonado-Murray 1H (Tanos) Peak IP-30: Too Recent

Completion Date: 3/20/2018 LL: 7,281’

Peak IP-30: 5.8 MMCFD

LL: 4,910’ Burton 2H (Jamex)

Completion Date: 8/3/2017

McElroy ‘A’- Murray 1H (Tanos) Peak IP-30: 4.7 MMCFD

Completion Date: 3/12/2018 LL: 5,636’

Peak IP-30: 3.5 MMCFD

LL: 4,478’ Reagan-Black Stone-Wilkinson 2H

(Tanos)

Pond-Gray 1H (Tanos) Completion Date: 1/3/2017

Completion Date: 6/4/2017 Peak IP-30: 7.8 MMCFD

Peak IP-30: 5.4 MMCFD LL: 6,807’

LL: 3,837’

Steele Gas Unit 1H (Jamex)

Pond 2H (Tanos) Completion Date: 6/20/2018

Completion Date: 5/24/2017 Peak IP-30: Too Recent

Peak IP-30: 7.1 MMCFD LL: 5,943’

LL: 4,950’

McElroy 3H (Valence)

Wilkinson Gas Unit 1H (Jamex) Completion Date: 6/5/2018

Completion Date: 07/17/2018 Peak IP-30: Too Recent

Peak IP-30: Too Recent LL: 7,675’

LL: 6,524’

Cecil Martin Gas Unit 1H (Jamex)

Johnson Gas Unit 2H (Jamex) Completion Date: 8/3/2017

Completion Date: 6/4/2018 Peak IP-30: 6.5 MMCFD

Peak IP-30: Too Recent LL: 6,019’

LL: 6,914’

RVRA’s position has very thick CV Taylor Sand compared to offset results

32

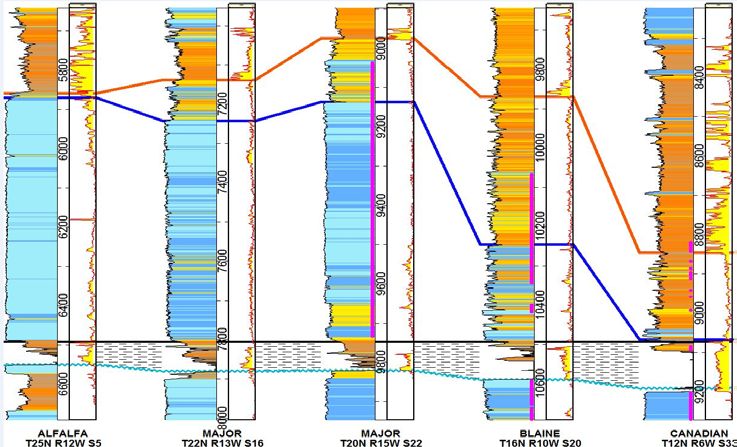

Note: Rig and permit data sourced from DrillingInfo as of July 30, 2018North Louisiana - Overview

North Louisiana Position

• Approximately 100,000 net acres

across northern Louisiana

Ruston Field

– Acreage is ~99% HBP and

~63% operated

• Ruston field is direct offset to

prolific Terryville field

– Significant upside of the

stacked benches of Bossier

(Poole) Sands

– 4 horizontal wells drilled on

Riviera’s acreage with 3

Middle Poole wells average

IRR >100%(1)

– Inventory of ~15 net

locations with exceptional

returns

• Additional upside potential exists

throughout position

(1) Assumed Pricing: Gas: $2.85/Mmbtu; Oil: $65.00/bbl 33North Louisiana - Ruston Field

• Growth faults isolate the sands on downthrown block of faults providing a three way trap

• High maturity of Bossier source rocks provides overpressure reservoir

• Recent development has been horizontal wells targeting the Middle and Lower Bossier

(Poole) Sands, proving dual bench development

• The 4 recent wells drilled on Riviera’s acreage have yielded excellent returns

Upper Poole Sand

– Development downthrown of Terryville Fault with ~15 net remaining locations

– Additional potential upside north of Terryville Fault

Ruston RVRA Operated Horizontal Wells

Middle Poole Sand

J P Graham 2H 2 Alt (RVRA)

Lower Poole Sand

Target: Middle Poole

EUR: 5.4 BCF/1,000’

Elliott Etal 1-11HC 1 (RVRA)

Target: Middle Poole Elliott Etal 1H 1 Alt (RVRA) Carter Etal 6H 1 Alt (RVRA)

EUR: 3.7 BCF/1,000’ Target: Lower Poole Target: Middle Poole

EUR: 1.9 BCF/1,000’ EUR: 3.9 BCF/1,000’

34North Louisiana – Rig Activity Analogs

Permit

Ruston Offset Activity

Lewis 21-16-9 HC 2 Alt (Range) Autry 25-36 HC 3 Alt (Range)

Completion Date: 1/19/2017 Completion Date: 2/7/2017

Peak IP-30: 19 MMCFD Terryville/Ruston Wells Drilled Since 1/2017 & Peak IP-30: 25 MMCFD

LL: 6,522’ LL: 8,026’

Riviera Operated Wells

Standifer 16-21 HC 1 Alt (Range) Autrey 25-36 HC 4 Alt (Range)

Completion Date: 5/28/2017 Completion Date: 2/7/2017

Peak IP-30: 19 MMCFD Peak IP-30: 22 MMCFD

LL: 6,158’ LL: 7,952’

Tatum 19-30 HC 1 Alt (Range) Autry 25-36 HC 2 Alt (Range)

Completion Date: 8/6/2017 Completion Date: 2/7/2017

Peak IP-30: 21 MMCFD Peak IP-30: 24 MMCFD

LL: 4,800’ LL: 7,952’

Tatum 19-30 HC 2 Alt (Range) Elliott Etal 1H 1 Alt (LINN)

Completion Date: 8/6/2017 Completion Date: 7/9/2017

Peak IP-30: 17 MMCFD Peak IP-30: 13 MMCFD

LL: 7,781’ LL: 3,797’

Tatum 19-30 HC 3 Alt (Range) Harrison 7-6 HC 2 Alt (N&G)

Completion Date: 8/6/2018 Completion Date: 10/8/2017

Peak IP-30: 25 MMCFD Peak IP-30: 17 MMCFD

LL: 7,816’ LL: 3,367’

Lamar Dowling 28-33 H 2 (Range) Carter Etal 6H 1 Alt (LINN)

Completion Date: 11/25/2017 Completion Date: 1/3/2017

Peak IP-30: 20 MMCFD Peak IP-30: 15 MMCFD

LL: 8,160’ LL: 4,021’

Lamar Dowling 28-33 H 1 (Range) Christian Etal 5-8HC 1 Alt (N&G)

Completion Date: 11/27/2017 Completion Date: 5/7/2017

Peak IP-30: 21 MMCFD Peak IP-30: 20 MMCFD

LL: 8,247’ LL: 6,115’

Barnett 26-35HC 1 Alt (Range) J P Graham 2H 2 Alt (LINN)

Completion Date: 2/27/2017 Completion Date: 8/17/2017

Peak IP-30: 22 MMCFD Peak IP-30: 16 MMCFD

LL: 10,348’ LL: 4,403’

Fallin 23-26-35 HC 2 Alt (Range) Burnett 35-2 HC 1 Alt (Range) Smith Etal 34-3-10 HC 2 Alt (N&G) Elliott Etal 1-11HC 1 (LINN)

Completion Date: 2/18/2017 Completion Date: 2/14/2017 Completion Date: 8/18/2017 Completion Date: 2/20/2016

Peak IP-30: 18 MMCFD Peak IP-30: 29 MMCFD Peak IP-30: 45 MMCFD Peak IP-30: 29 MMCFD

LL: 10,154’ LL: 8,752’ LL: 7,658’ LL: 6,503’

Note: Rig and permit data sourced from DrillingInfo as of July 30, 2018 35Long-Life, Low-Decline Assets • Hugoton – Jayhawk Plant • Michigan / Illinois • Uinta

Hugoton – Overview

• Net Production of ~136 MMcfe/d(1) (66% Natural Gas, 34% NGL) Hugoton Position

• ~1.1 million net acres that are 99%+ held by production(2)

• Very mature, low decline, highly delineated natural gas field

• Focus on Chase and Council Grove formations which produce

significant revenue from NGLs and helium Jayhawk Plant

450 MMcf/d Capacity

• Extensive gathering infrastructure and a significant midstream /

processing investment

• 100% interest in the Jayhawk processing plant with capacity of 450

MMcf/d (currently at ~56% utilization)

• More than 3,400 infill drilling locations economic at varying prices

above $3.00 per mcf

• Estimate a minimal amount of capital to offset base decline

Jayhawk Plant

450 MMcf/d Capacity

Historical Production Trend

180

160 Decline Rate of ~6%

Price Sensitivity

Net Production (Mmcfe/day)

140 Number of drilling locations greater than 20% ROR

120 $2.75

Natural Gas Price ($/MMBtu)

100 $3.00

80 $3.25

Average annual capital of ~$2 million

60

$3.50

40

$3.75

20

0 $4.00

Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Nov-17 Mar-18

0 500 1,000 1,500 2,000 2,500 3,000 3,500

(1) Volumes are average daily second quarter 2018 actual production 37

(2) Acreage as of year end 2017Hugoton - Jayhawk Plant Overview

• Commissioned April 1998 – 100% Riviera owned

• Cryogenic Plant with high NGL recoveries and ethane rejection capability

• Capacity of 450 MMcf/day; current throughput approximately 256 MMcf/day

• Electric driven compression

• Propane fractionator

• Helium Recovery & Nitrogen Rejection capability

• Two NGL outlets: ONEOK & Enterprise

• Residue outlet: Southern Star Central

• Helium outlets: Praxair & BLM Pipeline

• 3rd Party annual Adjusted EBITDA of $7MM - $10MM

Jayhawk Plant Historical Throughput

Berry ~256,000

300,000 XTO / Pioneer separation mcf/d

Hugoton Satanta plant

~170,000

Acquisitions shutdown

mcf/d

250,000

45% of

200,000 total

through

MMcf/day

put

150,000

100,000

55% of

total

through

50,000 put

0

Equity Volumes Third Party Gas 38Michigan / Illinois – Overview

Michigan/IL Position

• Net Production of ~27 MMcfe/d(1) (97% Natural Gas, 3% Oil)

• ~ 200,000 net acres

• Base decline of approximately 4%

• Michigan is a low decline, biogenic natural gas asset

• Illinois is a mature waterflood

Michigan Historical Production Trend

MI

35

Decline Rate of ~4%

30

Net Production (Mcfed)

25

20

IL

15

Average annual capital of ~$1.6 million

10

5

-

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

39

(1) Volumes are average daily second quarter 2018 actual productionUinta – Overview

Asset Highlights Uinta Position

• ~22 MMcfe/day net production(1)

• ~50,000 net acres, majority HBP

• Base decline of ~11%

• Non-operated position acquired through Devon

acquisition in 2014

• Extensive salt water disposal infrastructure

Uinta Historical Production Trend

30

25 Decline Rate of ~11%

Net Production (Mcfed)

20

15

10

Average annual capital of ~$0.166 million

5

0

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

40

(1) Volumes are average daily second quarter 2018 actual productionBlue Mountain Midstream Overview

Blue Mountain History

Key Highlights February 2016 – Executed GPA with Linn Energy Holdings, LLC (“LEH”) and approved

capital for construction of first refrigeration facility with 30 mmcf/d of processing capacity

October 2016 – Capital plan approved, including additional compression and second

refrigeration facility, adding 30 mmcf/d of processing capacity

November 2016 – Second refrigeration facility operational for total processing capacity of

60 mmcf/d

May 2017 – Supplemental capital approved to build Cryo Plant I with 250 mmcf/d of

processing capacity

June 2017 – Start of construction for Cryo Plant I

September 2017 – Amended GPA with LEH, dedicating ~70,000 acres to Blue Mountain

system

December 2017 – Other third-party dedicates ~7,200 acres to Blue Mountain system

April 2018 – Current management team joins Blue Mountain

June 2018 – Start up of Cryo Plant I

August 2018 – Initiated design and engineering of Cryo Plant II

Today Blue Mountain system has more than 80,000 acres dedicated and is currently

processing ~150 mmcf/d of natural gas and 9,800 bbl/d of NGLs

42Blue Mountain Company Overview

• Growth-oriented midstream company focused on

Merge/SCOOP/STACK plays in Oklahoma

• System located in core of prolific Merge play, currently a leading

operating area in U.S.

• More than 80,000 net acres dedicated to system

– LINN Energy’s acreage contributed to Roan Resources is

dedicated to the Blue Mountain system

– Other third-party dedication accelerating growth of business

• Cryo Plant I is catalyst for future growth

– Estimated 2018 exit-rate of 170-200 mmcf/d and expect to

reach full capacity 250 mmcf/d in mid-2019

– At full capacity, Cryo Plant I forecasted to generate

annualized EBITDA between $100-125 million

• Significant growth expected from increased throughout from

current customers and additional third-party volumes

– Initiating design and engineering of Cryo Plant II for up to

250 MMcf/d to meet growing demand

• Commercially focused on diversifying asset and revenue bases

– Crude gathering would provide commodity diversification

– Future expansion into NW STACK with new counterparties

• Connected to major pipelines out of basin to liquid Midwest & Gulf

Coast markets

Current footprint and sizeable dedication provide ample growth opportunities

43Blue Mountain

Executive Management Team

• Most recently served as President, Gas Pipelines & Processing for Enbridge Energy from January 2014 to April 2017

C. Gregory Harper • Formerly SVP of Midstream for Southwestern Energy, SVP and Group President of CenterPoint Energy Pipelines and Field

Services, President & CEO of Spectra Energy Partners, and multiple executive leadership roles for Duke Energy

President and Chief

Executive Officer • Currently serves on the board of Sprague Resources, and has served on the boards of Midcoast Holdings L.L.C., Enbridge

Energy Company, Inc., Enbridge Energy Management, L.L.C, and Spectra Energy Partners

• Over 35 years of energy industry experience with roles ranging from the field to executive leadership

David A. Weathers

• Prior to Blue Mountain, served as Vice President of Business Development for Enbridge’s U.S. Gathering & Processing

Executive Vice President business unit

and Chief Commercial • Former Senior Director for NextEra Energy and held various roles of increasing responsibility for over 20 years with Duke

Officer Energy

Brad D. Reese • Over 36 years of energy industry experience, with over 25 years concentrated in midstream infrastructure development

Executive Vice President • Most recently was President of Enbridge Canadian Gathering & Processing, and served on the boards of Alliance Pipeline and

Aux Sable companies

and Chief Development &

• Prior to Enbridge, held various leadership roles for over 29 years with Targa Resources, Spectra Energy and DCP Midstream

Corporate Services Officer

• Over 36 years of energy industry experience with roles in engineering / construction, operations, and commercial development

Christopher T. Ditzel • Prior to Blue Mountain, served as Vice President of Commercial Operation for Enable Midstream

Chief Operating Officer • Over 28 years served in multiple leadership roles in engineering, operations and business development for Panhandle Eastern,

Duke Energy and Spectra Energy

Noor S. Kaissi • Most recently held numerous finance leadership roles for Enbridge Energy, including Controller of Enbridge’s U.S. asset base

• Principal accounting officer for Enbridge Energy Management, Enbridge Energy Partnership and Midcoast Energy Partnership

Vice President of

Accounting and Finance • Prior to Enbridge, held leadership positions with Dynegy, Enron and Arthur Andersen

High-quality executive team supported by accomplished, commercially-focused

technical and financial teams

44Blue Moutain Key Priorities

Cryo Plant I in-service June 2018

Capture incremental third-party volumes to system

Ensure sufficient take-away capacity for system volumes

Design and engineering of Cryo Plant II commenced August 2018

Diversification of products, service offerings, and reach into new basins

Stand-up organization, processes and finances for standalone platform

Blue Mountain team focused on achievable, highly value-driven opportunities

45Initial Blue Mountain System Overview

• 250 mmcf/d of designed processing capacity with Cryo Plant I

• ~87,000 HP of total compression

• 110 miles of gathering pipe

• Supported by dedicated acreage position of more than 80,000 net

acres under long-term contracts

• Interconnections into Southern Star Central, Enable Gas

Transmission and ONEOK Gas Transportation pipelines

• At full capacity, Cryo Plant I forecasted to generate annualized

EBITDA between $100-125 million

Blue Mountain system strategically positioned to capture and provide market

access for producer volumes

Note: Processing capacity, compression and pipeline mileage shown are for fully-built system at year-end 2018 46Blue Mountain Midstream –

Cryo Plant I Update

• State of the art cryogenic processing facility in-

service June 2018

• Initial operating capacity of 150 mmcf/d and

62,000 horsepower of compression now online

• Full 250 mmcf/d to become available by 4Q

2018, with the addition of 25,000 HP of

compression

Forecasted Throughput vs. Plant Capacity

300,000

• ONEOK Hydrocarbon providing NGL 250,000

transportation from the facility 200,000

mmcf/d

150,000

• Facility is fully staffed and operating 24/7 100,000

50,000

0

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

• 80-acre site provides ample space for additional

Forecasted Throughput (Upper Range)

trains to meet growing demand Actuals Through August 2018; Forecasted Throughput (Lower Range)

Plant Capacity

Blue Mountain system built by experience operations staff; focus now

moves to design and engineering of Cryo Plant II

47Merge / SCOOP Play Overview

Active Rigs by Operator in Merge / SCOOP(1) Merge / SCOOP Rig Activity(1)

14 13

12

10

8

8

6

4 3 3 3

2 2 2 2

2 1 1 1 1 1

0

Horizontal Drilling Permits in the Merge(2)

136 125

3

20

20 56

61

35 93

14 69

11

15

2015 2016 2017 2018 YTD

Other Operators LNGG Citizen Roan

Blue chip operators surround premier Merge / SCOOP acreage position

(1) Source: Drilling Info as of August 2018

(2) Source: IHS; 2018 YTD is as of July 2018 48Customer Acreage Dedication

More than 80,000 acres dedicated to Blue Mountain

System

• Roan Resources is anchor producer (1)

– Pure play operator in Merge/SCOOP/STACK

formed by LINN Energy and Citizen Energy

– Largest position in the Merge play

– Producing ~45,000 Boe/d and forecasting

61,000 Boe/d by end of 2018

– Running 8 rigs on dedicated acreage

• Received other third-party dedication in December

2017

– Private company

– Dedicated acreage located in close proximity

to system

– Expect to add 10 new wells to system in 2018

• In active talks to gain additional third-party

dedications

Decision made on Cryo Plant II with up to 250 mmcf/d of addition capacity, based on producer

commitments and anticipated production growth from Roan and other producers

(1) Guidance from Roan Resources Investor Update July 2018 and current production and rig count from Roan Resources 49Blue Mountain Key Statistics

Estimated Operating Margin(1) (in millions) Capital Forecast (2) (in millions)

200 200

$22

175

170 $32

150

140

$18

125

125

100

mmcf/d

$75

75

62

50 61 $53

$6

25

$1 $3

$0

0

Q1 2018 A Q2 2018 E Q3 2018 E Q4 2018 E $53

$43

$33

Estimated Throughput MMcf / Day - Upper Range

Estimated Throughput MMcf / Day - Lower Range

2016A 2017A 2018E

Plant Operating Margin Estimate - Lower Range

Plant Operating Margin Estimate - Upper Range Field Cryo I Cryo II

Blue Mountain systems designed for speed and efficient deployment of capital

(1) Operating margin is all Blue Mountain Midstream revenue less direct operating expenses and does not include G&A 50

(2) Field includes refrigeration facilities 1 and 2Blue Mountain Key Takeaways

Deep Experienced management team in place with proven track record of

Midstream successful execution in midstream energy infrastructure

Expertise

Strong believers in Anadarko Basin and current asset footprint well-

Leading G&P

positioned to capitalize on growth opportunities in prolific Merge/

Position

SCOOP/STACK/NW STACK plays

Strong

Commercial Closely aligned with our key customer – Roan Resources

Relationships

Aggressive ramp up in volumes and EBITDA strengthens cash flow in near-

Financial

term; secured $200 million line of credit with $70 million currently available

Strength

provides funding for growth

Multiple Key focus on securing future growth projects; beginning design and

Avenues for engineering of Cryo Plant II and evaluating other scalable business growth

Growth opportunities

51Financial and Management Update

2019 Guidance to be

2018 Guidance Provided Following

Budget Approval

Q3 2018E Q4 2018E FY 2018E

Net Production (MMcfe/d) 275 – 305 270 – 305 314 – 330

Natural gas (MMcf/d) 225 – 250 220 – 248 237 – 250

Oil (Bbls/d) 1,300 – 1,500 1,300 – 1,500 3,200 – 3,300

NGL (Bbls/d) 6,900 – 7,700 7,000 – 8,000 9,600 – 10,000

Other revenues, net (in thousands) (1) $ 9,000 - $ 13,000 $ 25,000 - $ 31,000 $ 52,000 – $ 63,000

Blue Mountain Midstream business $ 3,000 - $ 6,000 $ 18,000 - $ 22,000 $ 22,000 – $ 29,000

Other $ 6,000 - $ 7,000 $ 7,000 - $ 9,000 $ 30,000 – $ 34,000

Costs (in thousands) $ 48,000 – $ 54,000 $ 47,000 – $ 54,000 $ 223,000 – $ 236,000

Lease operating expenses $ 23,000 – $ 25,000 $ 23,000 – $ 26,000 $ 118,000 – $ 123,000

Transportation expenses $ 19,000 – $ 21,000 $ 18,000 – $ 20,000 $ 77,000 – $ 81,000

Taxes, other than income taxes $ 6,000 – $ 8,000 $ 6,000 – $ 8,000 $ 28,000 – $ 32,000

Adjusted general and administrative expenses (2) $ 22,000 – $ 24,000 $ 15,000 – $ 17,000 $80,000 – $ 84,000

Severance expenses $ 12,000 – $ 14,000 $ 3,000 – $ 5,000 $ 33,000 – $ 37,000

Costs per Mcfe (Mid-Point) $ 1.91 $ 1.91 $ 1.95

Lease operating expenses $ 0.90 $ 0.93 $ 1.03

Transportation expenses $ 0.75 $ 0.72 $ 0.67

Taxes, other than income taxes $ 0.26 $ 0.26 $ 0.25

Targets (Mid-Point) (in thousands)

Adjusted EBITDAX $ 4,000(3) $ 39,000(3) $ 94,000(3)

Interest expense (4) $— $— $—

Oil and natural gas capital $ 16,000 $ 33,000 $ 66,000

Blue Mountain Midstream capital $ 29,000 $ 41,000 $ 160,000

Total capital $ 50,000 $ 76,000 $ 235,000

Weighted Average NYMEX Differentials

Natural gas (MMBtu) ($ 0.47) – ($ 0.38) ($ 0.45) – ($ 0.35) ($ 0.40) – ($ 0.35)

Oil (Bbl) ($ 5.05) – ($ 4.55) ($ 3.00) – ($ 2.70) ($ 4.00) – ($ 2.00)

NGL price as a % of crude oil price 36% – 41% 36% – 41% 34% – 38%

Unhedged Commodity Price Assumptions Jul Aug Sep Oct Nov Dec 2018E

Natural gas (MMBtu) $3.00 $2.82 $2.94 $2.95 $2.98 $3.07 $2.92

Oil (Bbl) $70.58 $67.63 $67.63 $66.94 $66.54 $66.21 $66.51

(1) Includes other revenues and margin on marketing activities

(2) Excludes share-based compensation expenses and severance expenses

(3) Includes a reduction to Adjusted EBITDAX for certain non-recurring G&A expenses, including estimated severance expenses of $35mm, estimated spin transaction costs of $7.5mm, estimated land diligence costs of

$3.6mm, divestiture related expenses of $1.1mm 53

(4) Excludes non cash amortization of deferred financing costsPro-Forma Adjusted Riviera Upstream

2018 Adjusted EBITDAX Outlook

Adjusted

Riviera

2018 Pro-forma Upstream

Riviera Estimates Guidance

Resources

$140 Guidance

$120

$52

$100

$ in Millions

$80 ($23)

$132

$60 $35

($26)

$94

$40 $80

$71

$20 $45 $45 $45

$0

FY 18 Guidance Pre-Close Adjusted FY18 Operating Implied Riviera Severance Expected G&A Pro-Forma FY18

EBITDAX from Margin from Blue Upstream Pro- Expense Reductions (3) Estimate

Asset Sales (1) Mountain Forma FY 18 E

Midstream (2)

(1) Represents Adjusted EBITDAX before closing for the following: OK Waterfloods closed 2/28/18, TX Panhandle Shallow closed 2/28/18, Permian Conventional W TX closed 3/29/18, Altamont

Bluebell closed 4/4/18, Permian NM closed 4/10/18

(2) Only includes the Chisholm Trail business, and excludes G&A

(3) Further G&A reductions, including Blue Mountain G&A, that will result in a pro-forma run-rate of approximately $30 million annually 54FY 2018 Capital Allocation

Total Capital $235 million

($ in millions)

Drilling = $45MM

Seismic = $ 8MM

Leasing = $11MM

Total = $64MM

Upstream Assets Oil

& Gas Capital (1)

Blue Mountain $64

Midstream 1H'18

$90

Asset Sales (2)

$2

Other P&P / Admin

$9

Blue Mountain

Midstream 2H'18

$70

(1) Assets include Hugoton, Michigan, Uinta, Arkoma, NW STACK, North Louisiana, and East Texas

(2) Asset Sales include Oklahoma Waterfloods and Texas Panhandle closed 2/28/18, Permian Conventional West TX closed 3/29/18, Altamont Bluebell closed 4/4/18, and Permian NM closed 4/10/18. 552018 Capital Bridge – Full Year

($ in millions)

Blue Mountain Midstream Capital Bridge

$160

$32 $160

$120 $8

$120 $120 $128

$80

$40

$0

Prior Guidance Plant 1 Field / Plant 2 Current Guidance

Other (1)

Riviera Upstream Capital Bridge

$80

$4 $1

$60 $14

$8 $56

$8 $48

$40 $75

$40 $40

$20

$0

Prior Guidance NW STACK NW STACK NW STACK Arkoma Non- Other Current

Seismic Leasing Operated Drilling Operated Guidance

(1) Represents acceleration of capital previously forecasted in 2019 to increase plant 1 capacity

56Commodity Hedge Portfolio –

Henry Hub and WTI

Natural Gas Positions Oil Positions

200 191 2000

175 1750

1500

Volume Hedged (MMbtu/d)

150 1500

Volume Hedged (bbls/d)

125 1250

100 $3.02

1000

75 750 $54.07

61

500

50 500

25 $2.89 250 $64.00

0 0

2018 2019 2018 2019

57Commodity Hedge Portfolio –

Natural Gas Basis

PEPL Basis Positions NGPL TXOK Basis Positions

100 25

Volume Hedged (MMbtu/d)

Volume Hedged (MMbtu/d)

20

75

60 60

15

50

10

10

($0.659) ($0.659)

25

5 ($0.185)

0

0 0

2018 2019 2018 2019

Michcon Basis Positions

25

Volume Hedged (MMbtu/d)

20

15

10 10

10

5 ($0.200) ($0.200)

0

2018 2019 58Capital Structure

• Approximately 76.2 million shares issued and outstanding at record date

Common Equity

• Approximately 0.5 million shares of restricted shares(1)

• Interest on borrowings determined by reference to either LIBOR +250 to 350

or ABR +150 to 250, depending on utilization

Riviera Upstream

$425 Million Revolver • $0 million drawn on RBL post Spin-Off

• Redeterminations semi-annually every April and October

Blue Mountain • Interest on borrowings determined by reference to either LIBOR +200 to 300

Midstream or ABR +100 to 200, depending on leverage ratio

$200 Million Revolver • $70 million available post Spin-Off, up to $200 million total availability

(1) Originally granted pursuant to the Linn Energy 2017 Omnibus Incentive Plan and converted to Riviera Resources 2018 Omnibus Inventive Plan at Spin-Off 59Board of Directors

Evan Lederman is a Managing Director, Co-Head of Restructuring and Partner on the Investment Team at Fir Tree Partners. Mr. Lederman focuses on

the funds’ distressed credit and special situation investment strategies, including co-managing its energy restructuring initiatives. Prior to joining Fir Tree

Evan Lederman Partners in 2011, Mr. Lederman worked in the Business Finance and Restructuring groups at Weil, Gotshal & Manges LLP and Cravath, Swaine &

Moore LLP. Mr. Lederman, in his capacity as a Fir Tree Partners employee, is currently a member of the boards of Riviera Resources, Inc. (Chairman),

Director Ultra Petroleum Corp. (Chairman), Amplify Energy Corp., New Emerald Energy LLC, Roan Resources LLC and Deer Finance, LLC. Mr. Lederman

received a J.D. degree with honors from New York University School of Law and a B.A., magna cum laude, from New York University.

Matthew Bonanno joined York Capital Management (“York”) in July 2010 and is a Partner of the firm. Mr. Bonanno joined York from the Blackstone

Group, where he worked as an associate focusing on restructuring, recapitalization and reorganization transactions. Prior to joining the Blackstone

Matthew Bonanno Group, Mr. Bonanno worked on financing and strategic transactions at News Corporation and as an investment banker at JP Morgan and Goldman

Sachs. Mr. Bonanno, in his capacity as a York employee, is currently a member of the boards of Riviera Resources, Inc., Rever Offshore AS, all entities

Director incorporated pursuant to York’s partnership with Costamare Inc., Augustea Bunge Maritime, Next Decade LLC, Vantage Drilling Co. and Roan

Resources LLC.

Phil Brown Philip Brown is a Partner of P. Schoenfeld Asset Management (“PSAM”), where he focuses on credit-oriented investments across various industries.

Prior to joining PSAM in 2009, Mr. Brown held positions at Sun Capital Partners, Inc., an operationally-focused private equity firm, and Buckeye Capital

Director Partners, an event-driven hedge fund. Mr. Brown began his career as an investment banking analyst at Wasserstein Perella & Co.

Andy Taylor is a member of the investment team of Elliott Management Corporation (“Elliott”), a New York-based investment firm, where he is

responsible for various corporate investments. Prior to joining Elliott in 2015, Mr. Taylor held similar positions in BlackRock’s Distressed Products

Andy Taylor Group, R3 Capital Partners and the Global Principal Strategies team at Lehman Brothers. Mr. Taylor, in his capacity as an Elliott employee, is currently

Director a member of the boards of Riviera Resources, Inc., Linn Energy Inc., Roan Resources LLC, Birch Permian Holdings Inc. and Cordero Energy Holdings,

LLC. Mr. Taylor received a B.S. in mechanical engineering from Rose-Hulman Institute of Technology and his M.B.A. with honors from the University of

Chicago.

David Rottino David Rottino is President and Chief Executive Officer and a director of Riviera Resources. Prior to Riviera Resources’ spin-off from LINN Energy, Inc.,

he served as LINN Energy’s Executive Vice President and Chief Financial Officer and as a member of the board of directors. Mr. Rottino has over 25

President and Chief years of total experience and over 20 years of experience in the oil and natural gas industry. Prior to joining LINN in June 2008, he served at El Paso

Energy, ConocoPhillips and Burlington Resources in various finance, accounting and strategic planning roles. Mr. Rottino earned a bachelor’s degree in

Executive Officer business administration from Texas Tech University and an M.B.A. from Texas Christian University.

Greg Harper has served as the President and CEO of Blue Mountain Midstream since 2018. Prior to Blue Mountain Midstream, Mr. Harper served as

Greg Harper President, Gas Pipelines and Processing and as the principal executive officer of Midcoast Holdings L.L.C., an Enbridge Inc. affiliate. Before joining

Enbridge, Mr. Harper served in various Senior Executive positions including Senior Vice President of Midstream of Southwestern Energy Company,

President and Chief Senior Vice President and Group President of CenterPoint Energy Pipelines and Field Services, and President, Chief Executive Officer and Director of

Executive Officer of Spectra Energy Partners, LP. Mr. Harper currently serves on the board of Sprague Resources where he has served as the chair of the audit committee

Blue Mountain since Sprague’s initial public offering in 2013, and previously served on the boards of Midcoast Holdings, L.L.C., Enbridge Energy Company, Inc. and

Enbridge Energy Management, L.L.C. Mr. Harper received his Bachelor’s degree in mechanical engineering from the University of Kentucky and his

Midstream M.B.A from the University of Houston.

60You can also read