Sage 300 People Release Notes 20.1.3.0 - Sage VIP Customer Zone

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Sage 300 People Release Notes 20.1.3.0

`

Table of Contents

1. RSA 4

1.1 Tax Tables 4

1.1.1 Income Tax: Individuals and Special Trusts 4

1.1.2 Rebates 4

1.1.3 Tax Thresholds 5

1.2 Medical Scheme Fees Tax Credits 5

1.3 Subsistence Allowances and Advances 5

1.4 Prescribed Rate for Reimbursive

Kilometres 5

2. ETI Changes 6

2.1 Wage test’ and the national minimum wage 6

2.2 Special economic zone (SEZ) 11

3. New UIF and Termination Status 12

3.1 Background 12

3.2 New Termination Reasons 13

3.3 New UIF Status 14

3.4 UIF Exempt 15

4. Foreign Income Alert 17

4.1 Background 17

4.2 Alert 17

5. Variable Remuneration 21

5.1 Background 21

6. Eswatini (Swaziland) 22

6.1 Swaziland Name Change 22

6.2 Eswatini (Swaziland) PAYE5 Tax

Certificate Logo and Header Change 22

7. Namibia 23

7.1 Namibia PAYE5 Report - Spouse

Information 23

7.2 Namibia SSC Form 10 Report - Previous

Terminations 23

7.3 Namibia SSC Form 10 Report –

Remuneration Subject to SSC 23

8. Nigeria 24

Sage 300 People Page 2 of 39

`

8.1 Nigeria Tax Relief Changes Effective 1

January 2020 24

8.1.1 Apply Nigeria Statutory Changes 24

8.1.2 Backdating of PAYE 24

8.2. Nigeria FCT IRS PAYE Schedule 26

8.3. Nigeria FCT IRS Form H1 30

9. Zimbabwe 35

9.1. Zimbabwe P6 Tax Certificate Print per Tax

Record 35

9.2. Zimbabwe ITF16 Print per Tax Record 35

10. Indonesia 36

10.1 BPJS Pensiun Wage Capping 36

11. Skills 37

11.1 Skills Extract filters 37

11.2 Skills Extract Excel 37

11.3 Skills Generic macros 37

12. General 38

12.1 Installer Changes 38

13. Bug Fixes 39

13.1 People Web API 39

13.2 Secure Tax Certificate print 39

13.3 IRP5 export with special character 39

13.4 Payslip Reconciliation Report 39

13.5. Medical Aid Definition set to ‘No Calc’ 39

Sage 300 People Page 3 of 39

`

1. RSA

Note:

The following changes were made in the Sage 300 People application for the

2020/2021 tax year. Please refer to our Budget Speech 2020/2021 summary for further

details or download our detailed guide for everything you need to know about this year’s

changes from our website.

1.1 Tax Tables

1.1.1 Income Tax: Individuals and Special Trusts

Taxable Income Rates of tax

1 – 205 900 18% of taxable income

205 901 – 321 600 37 062 26% of taxable income above 205 900

321 601 – 445 100 67 144 31% of taxable income above 321 600

445 101 – 548 200 105 429 36% of taxable income above 445 100

584 201 – 744 800 155 505 39% of taxable income above 584 200

755 801 – 1 577 300 218 139 41% of taxable income above 744 800

1 577 301 and above 559 464 45% of taxable income above 1 577 300

1.1.2 Rebates

Rebates

Primary R 14 958

Secondary (Persons 65 and older) R 8 199

Tertiary (Persons 75 and older) R 2 736

Sage 300 People Page 4 of 39

`

1.1.3 Tax Thresholds

Age Tax Threshold

Below 65 R 83 100

65 to below 75 R 128 650

75 and older R 143 850

1.2 Medical Scheme Fees Tax Credits

Medical Aid Tax Credits

Main Member R 319

First Dependent R 319

Additional Dependents R 215

1.3 Subsistence Allowances and Advances

Where the recipient is obligated to spend at least one night from his/her usual place of

residence in South Africa an amount equal to the following is deemed to have been

expended for each day or part of a day for –

Article I. meals and incidental costs, R 452;

Article II. incidental costs only, R 139

The rates for foreign travel (travel outside South Africa) will be gazetted soon and can be

found on www.sars.gov.za

1.4 Prescribed Rate for Reimbursive Kilometres

The SARS prescribed rate per kilometre increased from R3.61 to R3.98.

Sage 300 People Page 5 of 39

`

2. ETI Changes

2.1 Wage test’ and the national minimum wage

For an employee to qualify for ETI, he/she must be paid at least the minimum wage

(amongst other qualifying criteria, which is not changed by this amendment).

Before 1 August 2019, an employee could qualify if he/she was paid:

• the minimum wage according to the wage regulating measure, or

• if no wage regulating measure was applicable, R2000 per month for 160 employed

and remunerated hours.

The National Minimum Wage Act became effective on 1 January 2019 with a minimum

wage of:

R20 per hour, R18 per hour for farm workers, R15 per hour for domestic workers, R11 per

hour for workers employed in the public works programme and the minimum weekly

allowances for learners, unless the employer is specifically exempt from the National

Minimum Wage Act (for example, members of the South African National Defence Force),

or the employer is granted exemption from the national minimum wage after successful

application.

Backdating to 1 August 2019, to align the ETI Act with the National Minimum Wage Act,

the minimum wage requirements to possibly qualify for ETI were changed to:

The higher of:

• the national minimum wage, or

• the wage according to the wage regulating measure.

If none of the above is applicable (for example, the employer is exempt from the national

minimum wage after successful application and there is no wage regulating measure), then

R2 000 per month for 160 employed and remunerated hours should be used as the

minimum wage.

Sage 300 People Page 6 of 39

`

Is a wage regulating measure

applicable?

No Yes

No change required. Apply hourly

comparison (i.e. the minimum rate

per hour according to the wage

Does the national minimum wage regulating measure should be

apply to the employer? equal to or more than the

employee's actual wage rate per

hour).

* See note below.

Yes No

Change required. The R2000 rule

no longer applies in this case. The

minimum wage rate per hour No change required. The R2000

according to the National Minimum wage per month rule still applies

Wage Act should be compared to (i.e. R2000 for 160 ordinary

the employee's actual wage rate employed and remunerated

per hour. hours).

** See note below.

*The National Minimum Wage Act takes precedence over any wage regulating measure.

Therefore, each bargaining council agreement, sectoral determination and collective

agreement had to be updated with the correct minimum wages to be at least equal to or

more than the national minimum wage. It is the employer’s responsibility to confirm the

correct minimum wage be applied and will not be a change in the system. If the employee

is not paid at least the minimum wage, then he/she must be excluded from ETI.

**The National Minimum Wage Act specifies a minimum weekly learnership allowance for

learners. We are waiting for confirmation from National Treasury and SARS whether the

weekly wage (learnership allowance) can be converted to a minimum hourly rate to apply

an hourly comparison (as we do with other wage regulating measures). It is our assumption

that a rate per hour comparison can be applied and seeing that the legislation was only

promulgated on 15 January 2019 (effective August), we are not able to apply a weekly

minimum wage comparison in the system. At this point, it is the responsibility of the

employer to confirm that the learners are paid at least the minimum weekly allowance even

though our systems currently apply a rate per hour comparison.

Sage 300 People Page 7 of 39

`

Note:

The Sage 300 People application will not automatically apply the National Wage Rates,

these rates need to be created manually.

On the Navigation pane:

Expand Parameters

Expand Payroll

Double-click on Min Wage Type

Click on New

Link this rate to the applicable employee

Note:

If the same rate is used for multiple employees in the same company rule then this rate

may be linked on the Company Rule screen and changed individually for employees to

whom this rate does not apply.

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Employee Detail

Click on Detail

Sage 300 People Page 8 of 39

`

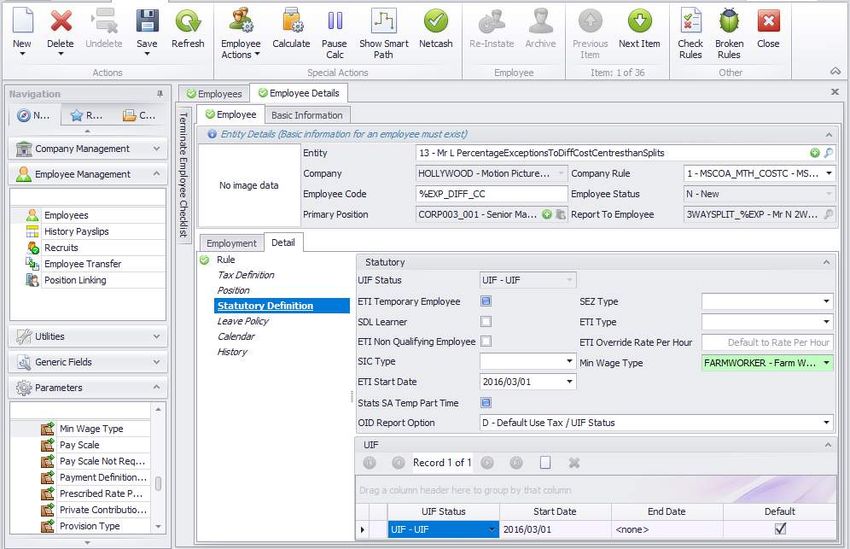

Click on Statutory Definition

Click on Min Wage Type Dropdown

If the employer needs to make backdated adjustments to the system the following reports

and tools are recommended:

• Print the detailed EMP201 and EMP501 from August 2019 to January 2020

• Print the ETI Report under Dynamic Reports from August 2019 to January 2020

• The ETI Take On batch can be used to export, amend and import history ETI

values back into the system

• Rebuild or recreate the Tax Monthly Totals for each period and reprint the

EMP201

Backdating to August 2019:

• ‘Redo’ (backdate) the ETI calculations/criteria according to the new legislation if

necessary, for each month for each employee from August 2019 until

January/February 2020 (depending on when the user will apply the backdate).

Backdating will be necessary if the R2000 minimum wage was applied instead of

the national minimum wage. This means that employees could have qualified who

will not qualify if the national minimum wage is applied

Sage 300 People Page 9 of 39

`

If there are differences for August 2019:

• The new ETI calculated value is less than the original value declared on the EMP201

(ETI Calculated value):

o The employer must make the shortfall payment to SARS using the relevant

month’s PRN number. The employer must also restate the EMP501 (since

an EMP501 reconciliation for that period has already been submitted)

containing the new corrected ETI value. This correction can result in late

payment penalties and interest. The values must also be correct in the

system because the total 4118 value (ETI value on the tax certificate for each

employee) must balance back to the total ETI calculated value declared on

the EMP201’s for the employer to be able to submit their EMP501

reconciliation

o If the new ETI calculated value is more than the original value declared on

the EMP201 (ETI Calculated value):

No ETI can be claimed for a previous 6-month reconciliation period. Since

August 2019 is part of the previous 6-month reconciliation period, the ETI

will be permanently forfeited. The values can also not be adjusted in the

system as the total 4118 value (ETI value on the tax certificate for each

employee) must balance back to the total ETI calculated value declared on

the EMP201’s for the employer to be able to submit their EMP501

reconciliation

If there are differences for September 2019 – January/February 2020:

• The new ETI calculated value is less than the original value declared on the EMP201

(ETI Calculated value):

o The employer must restate the relevant month’s EMP201 with the new lessor

value and make the shortfall payment to SARS. This correction may result

in late payment penalties and interest. The values must also be correct in

the system because the total 4118 value (ETI value on the tax certificate for

each employee) must balance back to the total ETI calculated value declared

on the EMP201’s for the employer to be able to submit their EMP501

reconciliation

o The new ETI calculated value is more than the original value declared on the

EMP201 (ETI Calculated value):

Add the additional ETI value to the current month’s EMP201 as ETI

calculated. The employer has only until the end of February 2020 to claim

the ETI not claimed from September 2019 to February 2020. Any ETI not

claimed for that period (September 2019 – February 2020) after February

2020 will be permanently forfeited as no ETI can be claimed for a previous

6-month reconciliation period. The values must also be correct in the system

because the total 4118 value (ETI value on the tax certificate for each

employee) must balance back to the total ETI calculated value declared on

Sage 300 People Page 10 of 39`

the EMP201’s for the employer to be able to submit their EMP501

reconciliation.

Note:

The backdating process as explained above was not confirmed by SARS and we

suggest that employers seek advise regarding the backdating directly from SARS.

2.2 Special economic zone (SEZ)

Both the Income Tax Act (ITA) and Employment Tax Incentive Act (ETIA) allows special tax

incentives for companies that operate (carry on a business) within a SEZ. In order to be a

qualifying employee for ETI, certain criteria must be met. One of the criteria is that the

employee must be 18 to 29 years old on the last day of the calendar month, unless the

employee renders services mainly within a SEZ to an employer who operates through a

fixed place of business within a SEZ, then the employee can be any age.

In order to qualify for the tax incentive in terms of the Income Tax Act, the employer must

meet certain requirements, however, before March 2020 the Employment Tax Incentive Act

did not make provision for the same requirements.

From March 2020, in order to ensure that the SEZ policy is applied in a uniform manner in

both the Income Tax Act and Employment Tax Incentive Act,

• the definition of ‘special economic zone’ is amended to align with the definition in

the Income Tax Act, and

• it is clarified that in order to claim ETI for employees of any age due to the SEZ

criteria, the company should be a qualifying company as contemplated in the

Income Tax Act under the SEZ regime and the employee renders services to that

employer mainly (more than 50%) within the special economic zone in which the

qualifying company that is the employer carries on trade.

Sage 300 People Page 11 of 39`

3. New UIF and Termination Status

3.1 Background

Currently employers submit the UI-19 and UIF Submit file (E03 -UIF Electronic

Declaration Specification) to declare employee details to the Unemployment Insurance

Fund.

Therefore, these reports should be aligned, but currently that is not the case.

There are 2 places where the new UI-19 (see attached) and the E03 (see attached) differs

(please see tables below), namely:

• employment status code (reason for termination codes), and

• reason for non-contribution codes

Employment status code (reason for termination codes)

UIF Submit File (E03) UI-19

01 Active

02 Deceased 02 Deceased

03 Retired 03 Retired

04 Dismissed 04 Dismissed

05 Contract Expired 05 Contract Expired

06 Resigned 06 Resigned

07 Constructively Dismissed 07 Constructively Dismissed

08 Employer’s Insolvency 08 Employer’s Insolvency

09 Maternity/Adoption Leave 09 Maternity/Adoption Leave

10 Illness Leave 10 Illness Leave

11 Retrenched 11 Retrenched

12 Transfer to another branch 12 Transfer to another branch

13 Absconded 13 Absconded

14 Business Closed 14 Business Closed

15 Death of Domestic Employer

16 Voluntary Severance Package

17 Reduced Work Time

18 Commissioning Parental

19 Parental Leave

Sage 300 People Page 12 of 39`

Note:

The Sage 300 People application will apply these changes to the UIF export.

3.2 New Termination Reasons

Two new termination reasons are added to the Sage 300 People application, these

reasons are only available to employees linked to a company linked to the tax country

South Africa. These 2 reasons are:

• Voluntary Severance Package

• Death of Domestic Employer

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Employee Detail

Click on Employee

Sage 300 People Page 13 of 39`

When an employee is linked to these termination reason the following code will export in

the UIF Export:

• 16 – Voluntary Severance Package

• 15 – Death of Domestic Employer

3.3 New UIF Status

Three new UIF reasons have been added:

• Parental Leave

• Commissioning Leave

• Reduced Work

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Employee Detail

Click on Detail

Click on Statutory Definition

Sage 300 People Page 14 of 39`

• Click on New

• Create a new UIF transaction

Note:

UIF will still calculate if this status is selected.

When an employee is linked to these termination reason the following code will export in

the UIF Export:

• 17 – Reduced Working Time

• 18 – Commissioning Parental

• 19 – Parental Leave

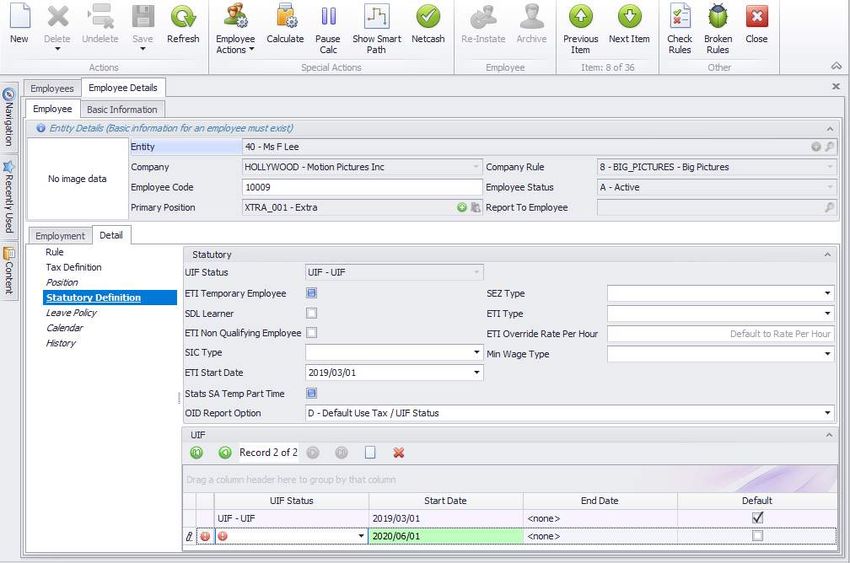

3.4 UIF Exempt

Legislation

According to section 10(1)(o)(ii) of the Income Tax Act, if an employee receives

remuneration for services rendered outside the Republic for or on behalf of any employer,

that remuneration shall be exempt if:

• the employee was outside SA for a period or periods exceeding 183 full days in any

12 month period, and

• for a continuous period exceeding 60 full days during that period of 12 months.

In this case, the remuneration received for foreign services is exempt income and therefore

no longer constitutes remuneration (i.e. not subject to PAYE on the payroll).

Therefore, if the employee receives exempt foreign services income/remuneration, it will

also be exempt for UIF purposes, since the UICA defines remuneration as remuneration

defined in the Fourth Schedule to the Income Tax Act.

A new UIF status has been added, which will result in no UIF calculating for the employee,

this status should be used when an employee is flagged for foreign income and for the tax

record that the employee does not pay PAYE.

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Employee Detail

Click on Detail

Click on Statutory Definition

Sage 300 People Page 15 of 39` Sage 300 People Page 16 of 39

`

4. Foreign Income Alert

4.1 Background

Before 1 March 2020: certain remuneration paid/accrued to a resident employee by any

employer (of private sector companies only) in respect of employment services rendered

for or on behalf of the employer in any country outside South Africa was exempt from

PAYE/income tax if:

• the employee was outside South Africa for a period (or periods) exceeding 183 full

days in any 12 months, and

• for a continuous period exceeding 60 full days in total in that period of 12 months

From 1 March 2020, certain remuneration paid/accrued to a resident employee by any

employer (of private sector companies only) in respect of employment services rendered

for or on behalf of the employer in any country outside South Africa is exempt from PAYE

if:

• that certain remuneration does not exceed one million rand for the tax year, and

• the employee is outside South Africa for a period (or periods) exceeding 183 full

days in any 12 months, and

• for a continuous period exceeding 60 full days in total in that period of 12 months

SARS published an FAQ document and a new Interpretation Note 16 to assist employees

and employers to obtain clarity on certain practical and technical aspects relating to this

amendment.

Resident employees who render services outside of South Africa often find themselves in

a predicament regarding their tax affairs since a double tax situation may arise. In this case,

the employer may (at his/her own discretion) apply for a different basis to calculate the

amount of employees’ tax to be withheld from the employee’s remuneration, taking into

account the potential foreign tax credit which may be claimed on assessment. The employer

will apply for a directive (IRP3(q)). This is not the actual granting of the section 6quat credit

and the employee is still required to submit an income tax return in which the actual foreign

tax credit under section 6quat must be claimed.

For more information regarding the directive application, please click here.

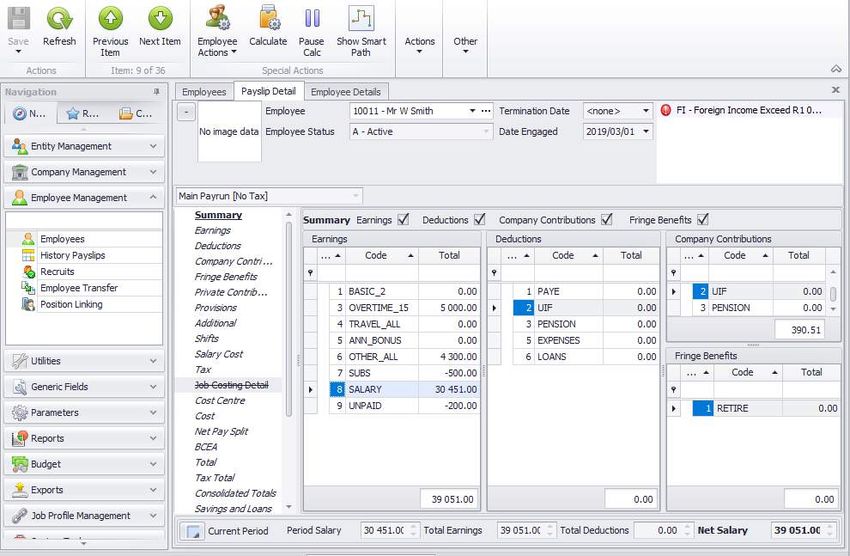

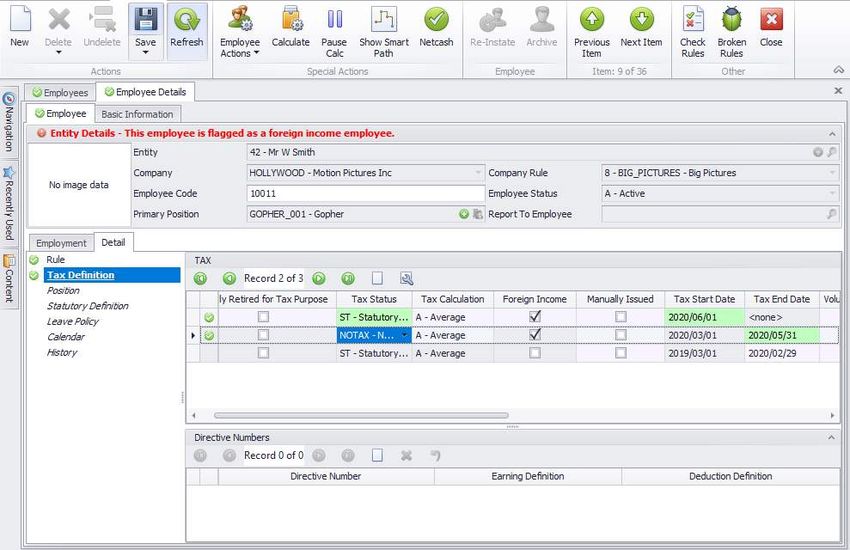

4.2 Alert

An alert has been added to the payslip detail to indicate when an employee, who has

been flagged for foreign income whose PAYE is 0.00’s balance of remuneration exceeds

1 000 000.00. You should then create a new tax certificate, flag it as foreign income but

ensure that the tax status is ST – Statutory Tables.

Sage 300 People Page 17 of 39`

Note:

The Sage 300 People application will not calculate or apply the exemption automatically

due to numerous variables to be taken into account. It will be the user’s responsibility to

apply the foreign employment income exemption on the payroll and report it against the

relevant IRP5 code/s.

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Payslip Detail

Click on Summary

Steps to Follow

Flag a Certificate as Foreign Income

Sage 300 People Page 18 of 39`

If the employee qualifies for foreign income according to the above-mentioned criteria

then do the following:

On the Navigation pane:

Expand Employee Management

Double-click on Employees

Select Required Employee

Click on Payslip Detail

Click on Detail

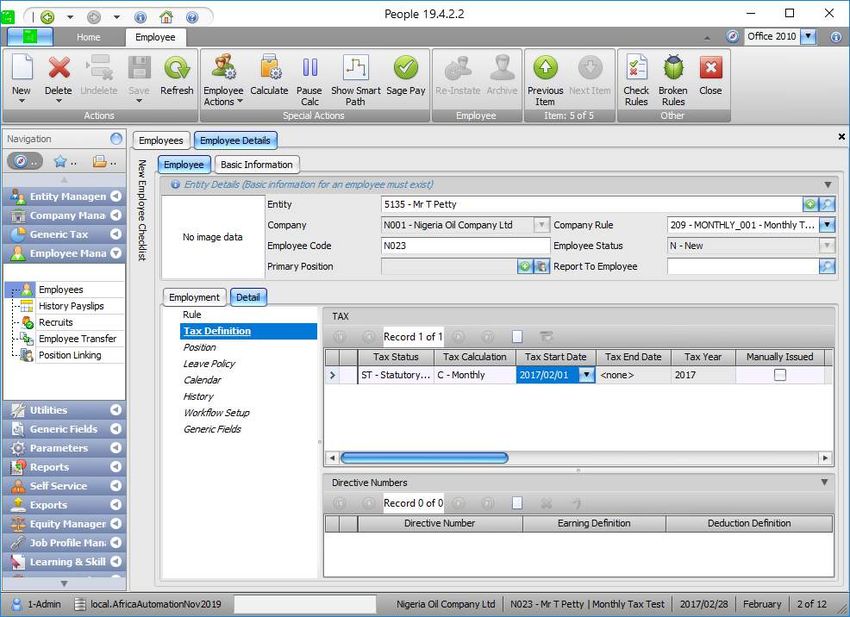

Click on Tax Definition

• Create a new Tax Record with Tax Status – No Tax and flagged as Foreign

Income

• Create a new UIF Record and link it to UIF Status, Foreign Income Exempt

• Once the employee reached the R1 000 000.00

Sage 300 People Page 19 of 39`

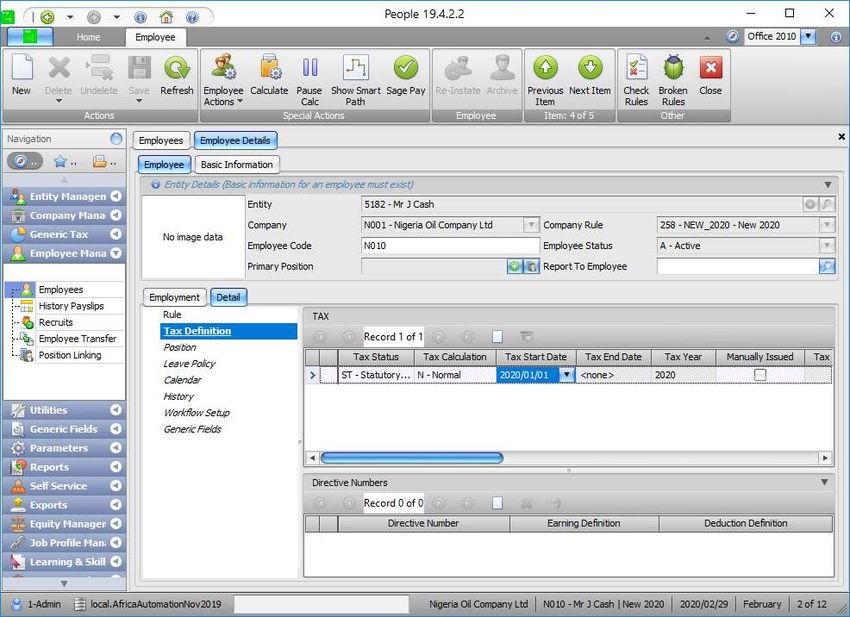

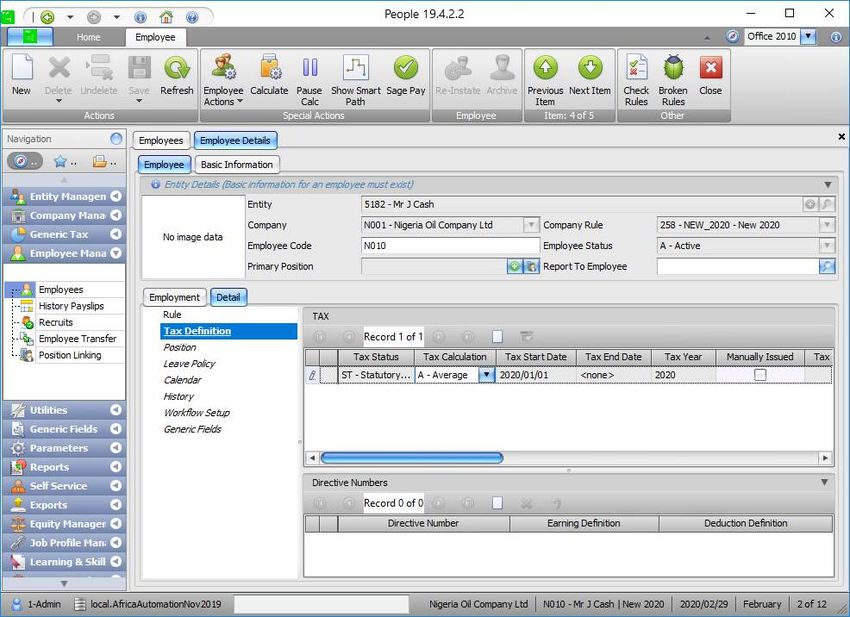

• Create a new Tax Record with Tax Status – Statutory Tables, and flag the

employee as Foreign Income

• Create a new UIF Record and link it to UIF Status, UIF

Note:

The Sage 300 People application will not apply the exemption automatically due to

numerous variables to be considered, for example the qualifying periods, employment

at more than one employer during the tax year, amounts paid/benefits received by

foreign employer etc. You must manually apply the exemption.

Sage 300 People Page 20 of 39`

5. Variable Remuneration

5.1 Background

Remuneration is generally taxable on accrual or receipt/payment, whichever event occurs

first. However, in the case of ‘variable remuneration’, PAYE must be withheld on the date

which the amount is paid to the employee.

Before 1 March 2020, ‘variable remuneration’ was defined as only:

• overtime

• bonuses

• commission

• an allowance or advance paid in respect of transport expenses such as a travel

allowance

• leave paid out

From 1 March 2020, the following items are added to the definition of ‘variable

remuneration’ and PAYE must be withheld when these amounts are paid to the employee:

• reimbursive travel allowance

• any night shift allowance

• any standby allowance

• certain business reimbursements

Sage 300 People Page 21 of 39`

6. Eswatini (Swaziland)

6.1 Swaziland Name Change

In April 2018, Swaziland’s name was changed to Eswatini. The country code for Eswatini

remained unchanged as ‘SWZ’.

All descriptions in the Sage 300 People application was updated to refer to Eswatini

instead of Swaziland. References to ‘SNPF – Swaziland National Provident Fund’ was

also updated to ‘ENPF – Eswatini National Provident Fund’.

Note:

All codes referring to ‘SWZ’ or ‘SWAZILAND’ remains the same. The statutory reports

will be updated as the new report layouts using the Eswatini detail becomes available.

6.2 Eswatini (Swaziland) PAYE5 Tax Certificate Logo and Header Change

The Eswatini Revenue Authority published a new PAYE5 tax certificate with the new

Eswatini logo and heading details.

Import the new Eswatini generic tax file to ensure that the new PAYE5 tax certificate

report is updated on the Sage 300 People application.

Note:

Before importing the new SWZ-GenericTax.xml file, the Sage 300 People application

must be updated to version 20.1.3.0.

The file must be imported in any pay period before doing any payroll processing, printing

payslips or reports or making any payments.

Sage 300 People Page 22 of 39`

7. Namibia

7.1 Namibia PAYE5 Report - Spouse Information

When the Spouse Entity is added as a Child root and not Parent, the Spouse detail printed

incorrect on the report. The report was updated to print the name of the linked Entity where

the Entity Relationship Type is ‘Spouse’ with the greatest Entity Relationship ID for either

Child or Parent Root.

7.2 Namibia SSC Form 10 Report - Previous Terminations

Employees terminated in a previous period but receives remuneration subject to SSC and

therefore has SSC contributions in the current period, was incorrectly excluded from the

SSC report. This issue was resolved.

7.3 Namibia SSC Form 10 Report – Remuneration Subject to SSC

When a new, active or current period terminated employee has no SSC Remuneration, the

minimum income limit of 300.00 printed on the report in the field for 'Remuneration Subject

to SSC'. The report was updated to print 0.00 instead of 300.00 if an employee's SSC

Remuneration is equal or less than 0.00.

Note:

To update your Sage 300 People application with the above Namibia report changes,

you must import the latest Namibia generic tax file.

Before importing the new NAM-GenericTax.xml file, the Sage 300 People application

must be updated to at least version 20.1.1.0.

The file must be imported in any pay period before doing any payroll processing,

printing payslips or reports or making any payments.

Sage 300 People Page 23 of 39`

8. Nigeria

8.1 Nigeria Tax Relief Changes Effective 1 January 2020

The Finance Act 2019 of Nigeria has been gazetted.

According to Section 27 of The Finance Act 2019, Section 33 of Personal Income Tax Act

has been amended by deleting subsections 4, 5 and 6. The implication for payroll is that

the tax reliefs for disability, children and dependent relatives have been deleted.

The effective date for the Finance Act 2019 is 13 January 2020. However, the gazetted

copy was only made public now in February. Because it is practical to backdate this tax

change, we should apply it from the payroll month of January 2020.

To summarise:

The tax reliefs, employees received for Child Dependents, Relative Dependents and

Disability is not applicable anymore.

8.1.1 Apply Nigeria Statutory Changes

Import the new Nigeria generic tax file to ensure that the tax reliefs are removed for PAYE

to recalculate. This will result in an increased PAYE amount for employees who did receive

the benefit of Child Dependents, Relative Dependents and Disability Relief.

Note:

Before importing the new NGA-GenericTax.xml file please ensure that the Sage

300 People application is updated to at least version 20.1.1.0

The file must be imported in any pay period before doing any payroll processing, printing

payslips or reports or making any payments.

8.1.2 Backdating of PAYE

In the Sage 300 People application, you have the option to link employees to an Average,

Normal or Monthly tax calculation.

If employees are linked to Average or Normal Tax, the PAYE will do an automatic YTD+

recalculation when the new tax file is imported after January 2020 and you recalculate all

your Nigeria company rules.

Sage 300 People Page 24 of 39` If employees are linked to the Monthly tax calculation, the PAYE for previous periods will not recalculate and manual PAYE calculations and adjustment must be done for previous periods. Sage 300 People Page 25 of 39

`

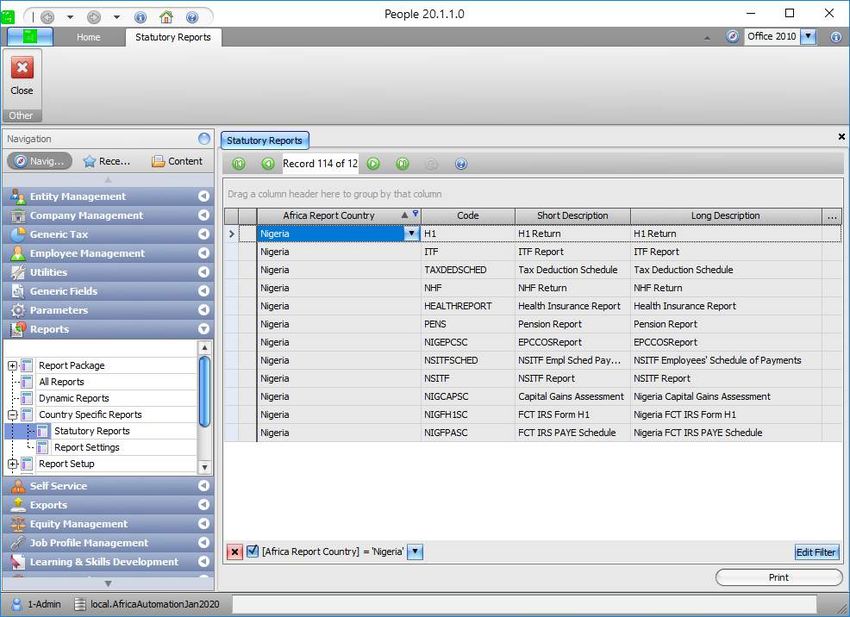

8.2. Nigeria FCT IRS PAYE Schedule

The FCT IRS PAYE Schedule is a monthly tax submission report required for employers

registered for tax in the State of Abuja. The report is a detailed report and must only include

employees whose tax deducted must be declared to the State of Abuja.

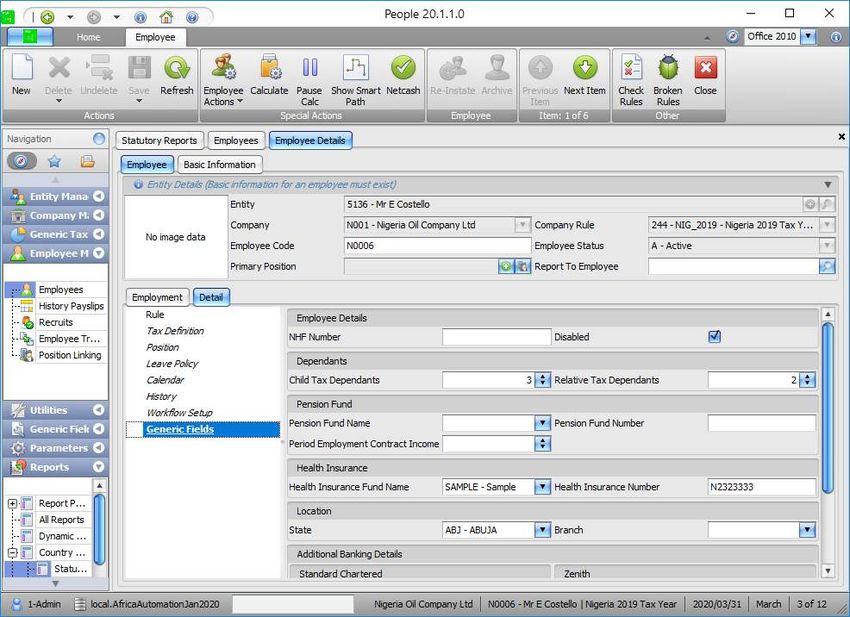

To ensure the correct employees (for the State of Abuja) are included in the report, all

employees in Nigeria companies must be linked to the correct ‘State’ on the Generic Fields

Screen on Employee Detail.

Sage 300 People Page 26 of 39`

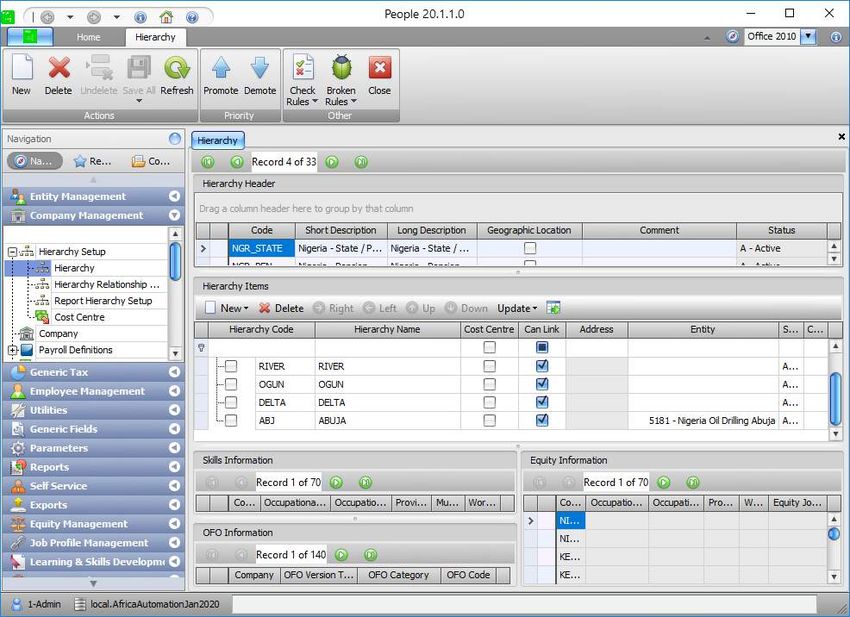

Note:

You have to add the different Nigerian States under Hierarchy Setup to ensure that the

options in the dropdown list in the Generic Field used for ‘State’, is correct.

The option for Abuja must also be linked to the applicable Company – Information Only

Entity if the Company Name, Company Tax Number and Company Address for the

State of Abuja differs from the detail captured on the Nigeria Company Basic

Information Screen.

Sage 300 People Page 27 of 39` The FCT IRS PAYE Schedule Report is available under Country Specific Reports. On the Navigation pane: Expand Reports Expand Country Specific Reports Double-click on Statutory Reports Sage 300 People Page 28 of 39

` When selecting to run the report, there are additional fields and selections on the Report Filter Screen that must be completed to ensure the correct values are included in the report. Sage 300 People Page 29 of 39

`

Field Description

State/Province The dropdown list in this field displays all the Hierarchy Items

linked to Hierarchy Header = NGR_STATE – Nigeria State /

Province.

You must select the applicable Hierarchy item that is used for

the State of Abuja.

Note:

The report will only include employees linked to the selected

Hierarchy Item.

Once you have made the required selections and completed all required fields, click on the

Preview button to run the report.

The report will open in MS Excel. You will be prompted to select the location and save the

report.

8.3. Nigeria FCT IRS Form H1

The FCT IRS Form H1 is an annual tax submission report required for employers registered

for tax in the State of Abuja. The report is a detailed report and must only include employees

whose tax deducted must be declared to the State of Abuja.

To ensure the correct employees (for the State of Abuja) are included in the report, all

employees in Nigeria companies must be linked to the correct ‘State’ on the Generic Fields

Screen on Employee Detail.

Sage 300 People Page 30 of 39`

Note:

You have to add the different Nigerian States under Hierarchy Setup to ensure that the

options in the dropdown list in the Generic Field used for ‘State’, is correct.

The option for Abuja must also be linked to the applicable Company – Information Only

Entity if the Company Name, Company Tax Number and Company Address for the

State of Abuja differs from the detail captured on the Nigeria Company Basic

Information Screen.

Sage 300 People Page 31 of 39` The FCT IRS H1 Form Report is available under Country Specific Reports. On the Navigation pane: Expand Reports Expand Country Specific Reports Double-click on Statutory Reports Sage 300 People Page 32 of 39

` When selecting to run the report, there are additional fields and selections on the Report Filter Screen that must be completed to ensure the correct values are included in the report. Sage 300 People Page 33 of 39

`

Field Description

State/Province The dropdown list in this field displays all the Hierarchy Items

linked to Hierarchy Header = NGR_STATE – Nigeria State /

Province.

You must select the applicable Hierarchy item that is used for

the State of Abuja.

Note:

The report will only include employees linked to the selected

Hierarchy Item.

Once you have made the required selections and completed all required fields, click on the

Preview button to run the report.

The report will open in MS Excel. You will be prompted to select the location and save the

report.

Note:

To update your Sage 300 People application with the above Nigeria reports, you must

import the latest Nigeria generic tax file.

Before importing the new NGA-GenericTax.xml file, the Sage 300 People application

must be updated to at least version 20.1.1.0.

The file must be imported in any pay period before doing any payroll processing,

printing payslips or reports or making any payments.

Sage 300 People Page 34 of 39`

9. Zimbabwe

9.1. Zimbabwe P6 Tax Certificate Print per Tax Record

In August 2019 a new tax table as well as tax credits were announced with an effective date

of 01 August 2019 and therefore no backdating to the start of the tax year was allowed. The

solution was for users to close employees’ current tax record with an end date of 31 July

2019 and then create a new tax record with a start date of 01 August 2019 to correspond

with the two tax tables for the 2019 tax year.

Although ZIMRA did not explicitly say that the employees should be issued with two tax

certificates, the assumption is that each employee should receive two tax certificates. This

is because an employee’s P6 has a serial number which should correspond with the serial

number of that employee’s record on the ITF16.

The existing P6 report was updated to create tax certificates per tax record for the selected

reporting year instead of a tax certificate that uses consolidated tax records for the selected

reporting tax year.

9.2. Zimbabwe ITF16 Print per Tax Record

Due to the two tax tables for the 2019 tax year, ZIMRA now require that employers must

provide two separate ITF16 submission files for the 2019 tax year. One for the period

January to July and the other for August to December.

We changed the existing ITF16 report to create entries in the submission file per employee

tax record instead of consolidated tax records for the selected reporting tax year. This is

also applicable to tax years where there was only one tax table.

If there was more than one tax table in the tax year, then separate submission files will be

created per tax table with the relevant transactions per employee tax record.

If there was only one tax table in the tax year, then only one submission file will be created

but with separate transactions per employee tax record.

Note:

To update your Sage 300 People application with the above Zimbabwe report changes,

you must import the latest Zimbabwe generic tax file.

Before importing the new ZWE-GenericTax.xml file, the Sage 300 People application

must be updated to at least version 20.1.1.0.

The file must be imported in any pay period before doing any payroll processing,

printing payslips or reports or making any payments.

Sage 300 People Page 35 of 39`

10. Indonesia

10.1 BPJS Pensiun Wage Capping

Effective 1 March 2020, the BPJS Pensiun wage capping limit is increased from

Rp 8.512.400 to Rp8.939.700.

Note:

To apply the new BPJS Pensiun wage capping limit, please ensure that you have

imported the latest Indonesia Generic Tax file. Please contact support if you require any

assistance.

Sage 300 People Page 36 of 39`

11. Skills

11.1 Skills Extract filters

The following changes has been made to the existing Skills Extract filter screen:

• Export File name will allow the user to select the expand option and then type the

file name to be created, previously the Excel file had to be saved first to be located.

• Company and Company Rule will allow for more than 250 characters to be selected.

Previously the user received and error if too many Companies or Company Rules

were selected.

• Date Validations will apply as follow:

o “From Date” cannot be after “To Date”

o “To Date” cannot be before “From Date”

• Training and Qualifications will be defaulted as selected as this is primarily why the

extract is used.

• Municipality has been added as a filter

• Workplace has been changed to a multi select filter

11.2 Skills Extract Excel

No changes has been made to the extract file layout, we understand that the file has many

duplicate or un-used columns on it but due to customers custom reports and macros running

on this extract we are unable to change this until we have consulted with all customers on

this process.

11.3 Skills Generic macros

No changes have been made to the Private and Public Skills macros.

Sage 300 People Page 37 of 39`

12. General

12.1 Installer Changes

• 3-Tier configuration has been removed from the Sage 300 People installer.

• Sage 300 People PublicAPI upgrade has been corrected when using the Main

Installer.

• Load Balancer and Throttle Policy values now copy over when completing a

software upgrade.

Sage 300 People Page 38 of 39`

13. Bug Fixes

13.1 People Web API

An error occurred where certain customers received an arithmetic overflow error. This has

now been corrected.

13.2 Secure Tax Certificate print

Previously when printing the secure IRP5 certificate, certain employee’s values where

printed over 2 certificates, but the employee’s information for the second certificate did not

reflect the correct employee’s fixed values. This has been corrected.

13.3 IRP5 export with special character

Previously when an employee had a special character in any text field, the special character

was replaced with a “?”, this has been corrected and the special character will no longer be

converted in the IRP5 Export.

Example:

• Previous Release - First Name: Janè was exported as Jan?

• New Release – Firsta Name: Janè will be exported as Janè

13.4 Payslip Reconciliation Report

The Payslip Reconciliation report did not reflect the correct YTD plus retirement fund fringe

benefit value, this error occurred when an employee had either multiple payruns or a tax

adjustment payslip was created for the employee. This error has been corrected.

13.5. Medical Aid Definition set to ‘No Calc’

When an employee had an active medical aid policy with contribution amounts on the

policy and the calculation status was set to ‘No Calc’ on the medical aid definition line. An

amount still calculated on the payslip. This has been corrected to calculate no amounts

when the calculation status is set to ‘No Calc’.

Sage 300 People Page 39 of 39You can also read