SALES TAX HOLIDAY Clothing $100 or Less - TTR

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SALES TAX

When is the tax holiday?

• It begins the last Friday in July each year at

12:01 am and ends at 11:59 pm the following

HOLIDAY

Sunday.

Who can buy tax-exempt clothing?

• Anyone (not just students) can buy clothing

that qualify.

Clothing $100 or Less What’s tax-exempt?

• General apparel that costs $100 or less per item

(shirts, pants, jackets, socks, shoes, dresses,

etc.)

• Items that are normally sold together, such as

shoes, cannot be split up to stay beneath the

$100 threshold.

• More items are listed at www.tntaxholiday.com

What’s still taxable?

• Apparel that costs more than $100.

• Items such as jewelry, handbags, or sports and

recreational equipment.

• Items purchased for business or trade use.

• Please consult our spreadsheets at

Questions? www.tntaxholiday.com for a more

Visit www.tn.gov/revenue comprehensive list of items.

and click “Revenue Help.”

SALES TAX

When is the tax holiday?

• It begins the last Friday in July each year at 12:01

am and ends at 11:59 pm the following Sunday.

HOLIDAY

Who can buy tax-exempt school supplies?

• Anyone (not just students) can buy school

supplies that qualify.

School Supplies and What’s tax-exempt?

• School and art supplies with a purchase price of

School Art Supplies $100 or less per item, such as binders, books,

backpacks, crayons, paper, pens, pencils, and

$100 or Less rulers, and art supplies such as glazes, clay,

paints, drawing pads, and artist paintbrushes.

• Items that are normally sold together cannot be

split up to stay beneath the $100 threshold.

• More items are listed at www.tntaxholiday.com

What’s still taxable?

• School and art supplies individually priced at

more than $100.

• Items purchased for business or trade use.

• Please consult our spreadsheets at

www.tntaxholiday.com for a more

Questions? comprehensive list of items

Visit www.tn.gov/revenue

and click “Revenue Help.”

SALES TAX

When is the tax holiday?

• It begins the last Friday in July each year at 12:01 am

and ends at 11:59 pm the following Sunday.

HOLIDAY

Who can buy tax-exempt computers?

• Anyone (not just students) can buy computers that

qualify.

What’s tax-exempt?

Computers $1,500 • Computers with a purchase price of $1,500 or less.

This includes laptops as well as tablets (iPads, etc.).

or Less • Computers for personal (not business) use.

• More items are listed at www.tntaxholiday.com

What’s still taxable?

• Computer parts, like keyboards and monitors, when

not sold with a CPU.

• Storage media, like flash drives and compact discs.

• Individually purchased software.

• Video game consoles.

• Computer printers and supplies.

• Electronic readers (Kindles, Nooks, etc.) and

personal digital assistants.

• Cell phones, including smart phones.

• Please consult our spreadsheets at

Questions? www.tntaxholiday.com for a more comprehensive

Visit www.tn.gov/revenue list of items.

and click “Revenue Help.”

Sales Tax Holiday Alphabetical Directory: Exempt Items

Tennessee Code Annotated Section 67-6-393

Note: No items used in trade or business are exempt under these provisions.

Item Other Information

Aerobic clothing

Antique clothing (for wear)

Aprons/Clothing shields

Athletic socks

Baby clothes

Baby diapers

Baby receiving blankets

Backpacks

Bandanas

Bathing suits

Belts

Bibs

Binders School supply

Blackboard Chalk School supply

Blouses

Book Bags School supply

Boots, general purpose (winter,

dress, cowboy, hiking)

Bow Ties

Bowling Shirts

Bras

Bridal Gowns and Bridal Veils

Calculators School supply

Camp Clothing

Caps

Cellophane Tape School supply

Chalk School supply

Chef Uniforms

Choir and Altar Clothing

Clay School art supplies are exempt .

Clerical Vestments

Clothing Exempt if $100 or less per item.

Coats

Compasses School supply

Composition Books School supply

Sales Tax Holiday Alphabetical Directory: Exempt Items

Tennessee Code Annotated Section 67-6-393

Note: No items used in trade or business are exempt under these provisions.

Item Other Information

Computers, Notebooks, Laptops, Exempt if $1500 or less. Includes CPU and other bundled

and Tablets components such as speakers, monitor, keyboard, mouse,

cables, and basic software.

Corsets and Corset Laces

Costumes, including novelty

chilldren's costumes

Coveralls

Cowboy Boots

Crayons School supply

Diapers - (adult and baby, cloth

or disposable)

Dress Gloves and Shoes

Dresses

Ear Muffs

Erasers School supply

Folders - expandable, pocket, School supply

plastic, and manila

Formal Clothing, purchased

Galoshes

Garters/Garter Belts

Girdles, Bras, and Corsets

Glazes School art supplies are exempt.

Gloves

Glue, Paste, and Paste Sticks School supply

Golf Clothing (caps, dresses,

shirts, skirts, pants)

Graduation Caps and Gowns,

purchased

Gym Suits and Uniforms

Hats, general purpose: cowboy,

baseball, knit

Highlighters School supply

Hiking boots

Hooded Shirts and Sweatshirts

Hosiery

Index Card Boxes School supply

Index Cards School supplySales Tax Holiday Alphabetical Directory: Exempt Items

Tennessee Code Annotated Section 67-6-393

Note: No items used in trade or business are exempt under these provisions.

Item Other Information

Jackets

Jeans

Jerseys, sports

Jogging Apparel

Jogging Bras

Knitted Caps and Hats

Lab Coats

Leather Clothing

Leg Warmers

Legal Pads School supply

Leotards

Lingerie

Lunch Boxes School supply

Markers School supply

Mittens

Neckties

Neckwear, including ties and

scarves

Nightgowns and Night Shirts

Notebooks School supply

Overalls

Overshoes and Rubber Shoes

Pads, sketch and drawing School art supplies are exempt per legislation passed in 2007.

Paintbrushes, for artwork School art supplies are exempt.

Paints, acrylic, tempora, and oil School art supplies are exempt.

Pajamas

Pants

Paper - loose leaf ruled School supply

notebook paper, copy paper,

graph paper, tracing paper,

manila paper, colored paper,

poster board, and construction

paper

Pencil Boxes School supply

Pencil Sharpeners School supply

Pencils School supplySales Tax Holiday Alphabetical Directory: Exempt Items

Tennessee Code Annotated Section 67-6-393

Note: No items used in trade or business are exempt under these provisions.

Item Other Information

Pens School supply

Ponchos

Poster Board School supply

Prom dresses

Protractors School supply

Raincoats, Rain Hats, and

Ponchos

Religious Clothing

Robes

Rubber Thongs, Flip-Flops

Rulers School supply

Running Shoes, Without Cleats

Sandals

Scarves

School Art Supplies Clay and glazes, paints (acrylic, tempora, and oil), paintbrushes

for artwork, sketch and drawing pads, and watercolors are

exempt per legislation passed in 2007.

School supplies Exempt if $100 or less per item.

School Supply Boxes School supply

School Uniforms

Scissors School supply

Scout uniforms

Shawls and Wraps

Shirts

Shoe Inserts

Shoe Laces

Shoes

Shorts

Ski masks

Ski suits

Slacks

Sleepwear, Nightgowns, Pajamas

Slippers

Slips

Sneakers

Socks (including athletic)Sales Tax Holiday Alphabetical Directory: Exempt Items

Tennessee Code Annotated Section 67-6-393

Note: No items used in trade or business are exempt under these provisions.

Item Other Information

Stockings

Suits, Slacks, Jackets, and Sport

Coats

Support Hose

Suspenders

Sweat Suits

Sweaters

Sweatshirts

Swimsuits

Tablet Computer

Tennis skirts, dresses, shoes

Thongs

Textbooks

Ties/Neckwear

Tights

Trousers

T-shirts

Tuxedos, purchased

Undergarments, including

longjohns

Underwear

Uniforms Athletic or Non-Athletic

Veils Veils for general use are exempt.

Vests, except hunting and water

Walking shoes

Watercolors

Wedding Gowns $100 or less rule applies.

Windbreakers

Workbooks

Writing TabletsSales Tax Holiday Alphabetical Directory: Taxable Items Not Exempt

Tennessee Code Annotated Section 67-6-393

Item Other Information

Belt Buckles Belt buckles sold separately are not exempt.

Belts, tool

Boots, ski

Breathing Masks

Bridal apparel, other than gowns

or veils

Briefcases

Cell Phones, including smart

phones

Clothing Accessories or Incidental items worn on the person or in conjunction with

Equipment clothing.

Compact Disks Computer storage media

Computer Software Basic computer software purchased with a bundled system is

exempt. Individually purchased software and upgraded

software purchased with a bundled system is taxable.

Computer Storage Media Computer storage media (diskettes, compact disks), handheld

electronic schedulers, personal digital assistants (PDAs),

computer printers, and printer supplies (printer paper, printer

ink).

Cosmetics

Diskettes Computer storage media

Electronic Readers

Electronic Schedulers School computer supply

Emblems Emblems sold separately are not exempt.

Fabric

Face Shields

Fins, swim

Glasses, safety

Globes

Gloves, protective or welders'

Gloves, sports

Goggles, safety

Goggles, sports

Guards, sports hand, elbow,

mouth, shin

Hair Notions

Handbags

Hard Hats

Hearing ProtectorsSales Tax Holiday Alphabetical Directory: Taxable Items Not Exempt

Tennessee Code Annotated Section 67-6-393

Item Other Information

Helmets

Jewelry

Jump Drives Computer storage media

Leased Items

Maps

Paintbrushes, other Paintbrushes not used for artwork are taxable.

Paints, other Only acrylic tempora, or oil paints defined as school art

supplies are exempt.

Patches Patches sold separately are not exempt.

Personal Digital Assistants (PDAs) School computer supply

Printer Ink School computer supply

Printer Paper School computer supply

Printer Supplies School computer supply

Printers School computer supply

Protective Equipment Items for human wear and designed as protection of the

wearer against injury or disease or as protections against

damage or injury of other persons or property, but not

suitable for general use.

Reference Books

Reference Maps

Rented Items

Respirators, paint or dust

School Computer Supplies Computer storage media (diskettes, compact disks), handheld

electronic schedulers, personal digital assistants (PDAs),

computer printers, and printer supplies (printer paper, printer

ink).

School Instructional Material Reference books, and reference maps and globes. Textbooks

and workbooks exempt under existing law.

Sewing Equipment & Supplies

Sewing Materials Materials that become part of clothing are not exempt.

Shoes, ballet or tap

Shoes, cleated or spiked

Shoulder Pads for Dresses,

Jackets, etc.

Shoulder Pads, sports

Skates, roller and ice

Ski Boots

Skin Diving SuitsSales Tax Holiday Alphabetical Directory: Taxable Items Not Exempt

Tennessee Code Annotated Section 67-6-393

Item Other Information

Smart Phones

Sport or Recreational Equipment Items designed for human use and worn in conjunction with

an athletic or recreational activity that are not suitable for

general use.

Sunglasses

Telephones

Thread

Thumb Drives

Tool Belts

Trade or Business, items used in

Umbrellas

Video Game Consoles

Wallets

Watches

Welders' Gloves

Wetsuits

Yarn

ZippersSales and Use Tax Notice

Notice #21-10 May 2021

2021 Sales Tax Holiday for Food, Food Ingredients, and

Prepared Food

Sales Tax Holiday During the Week of July 30 to • It contains two or more food ingredients

August 5 mixed together by the seller for sale as a

single item; or

Public Chapter 456 (2021), effective July 1, 2021,

creates a new sales tax holiday for the week • The vendor who sells it also provides eating

beginning 12:01 a.m. on Friday, July 30, 2021 and utensils, such as plates, knives, forks, spoons,

ending at 11:59 a.m. on Thursday, August 5, 2021. glasses, cups, napkins, or straws.

During this period, food, food ingredients, and

For examples of prepared food, please see Important

prepared food products may be purchased tax free.

Notice 17-21.

Food and Food Ingredients The most common example of a retailer selling

prepared food is a restaurant.

“Food and food ingredients” are defined as liquid,

concentrated, solid, frozen, dried, or dehydrated Food, Food Ingredients, and Prepared Food

substances that are sold to be ingested or chewed by Purchased Prior to the Sales Tax Holiday and

humans and are consumed for their taste or Received During the Sales Tax Holiday Period

nutritional value. Food ingredients do not include Qualify

alcoholic beverages, tobacco, candy, dietary Sales of food, food ingredients, or prepared food are

supplements, and prepared food. For more also considered exempt if:

information and examples of food and food

• The payment for the food is made prior to the

ingredients, please see Important Notice 17-20.

sales tax holiday period; and

The most common example of a retailer selling food

• The food is received by the purchaser during

and food ingredients is a grocery store.

the holiday period.

Prepared Foods

For example, an individual pays a caterer on June 1,

A food item is considered “prepared food” if it meets 2021 for food that will be served at an event

one of the following qualifications: occurring on August 2, 2021. Because the food is

• It is sold in a heated state or heated by the delivered to the individual on August 2, during the

seller; sales tax holiday, this sale is exempt from sales tax.

Sales of food, food ingredients, and prepared food

where the payment for the food is made during the

Disclaimer: The information provided here is current as of the date of publication but may change as a result of new statutes, regulations,

or court decisions. While this notice is intended to be comprehensive, events and situations unanticipated by this notice may occur. In such

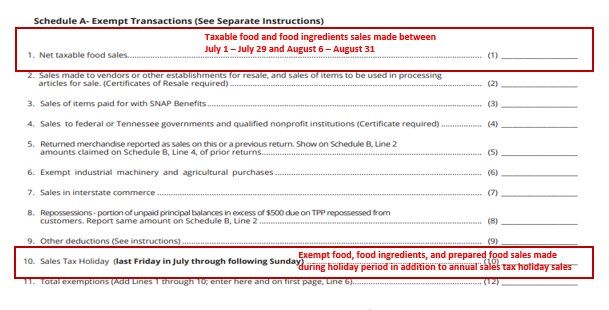

cases you should contact the department or your tax professional for further guidance.sales tax holiday period and the food is delivered 4. Annual sales tax holiday sales of clothing,

after the holiday period remain taxable transactions. school supplies, and computers must also be

reported on the Sales Tax Holiday line,

Reporting Exempt Sales

Schedule A, Line 10.

Proper reporting of sales made during the sales tax

holiday is required of all vendors. For the July 2021 For more information, please see the illustration

and August 2021 reporting periods, sales should be below.

reported as follows:

1. Report all sales (taxable and non-taxable) on,

For More Information

Page 1, Line 1 (Gross Sales) of the sales tax

return. Visit www.tn.gov/revenue. Click on Revenue Help to

2. Sales of exempt food, food ingredients and search for answers or to submit an information

prepared food made during the holiday request to one of our agents.

period must be reported on Schedule A, Line

10 (Sales Tax Holiday). References

3. Taxable sales of food and food ingredients

Tenn. Code Ann. §§ 67-6-102 and 67-6-393. Public

made outside of the holiday period must be

Chapter 456 (2021).

reported on Schedule A, Line 1 (Net taxable

food sales).

Disclaimer: The information provided here is current as of the date of publication but may change as a result of new statutes, regulations,

or court decisions. While this notice is intended to be comprehensive, events and situations unanticipated by this notice may occur. In such

cases you should contact the department or your tax professional for further guidance.Sales and Use Tax Notice

Notice #21-13 June 2021

Sales Tax Holiday for Gun Safes and Gun Safety Devices

One Year Sales Tax Holiday for Gun Safes and Gun Reporting Exempt Sales

Safety Devices

All vendors must properly report sales made during

Public Chapter 592 (2021), effective July 1, 2021, the sales tax holiday. For the July 2021 through June

creates a new one-year sales tax holiday for the 2022 reporting periods, sales should be reported as

period beginning 12:01 a.m. on July 1, 2021 and follows:

ending at 11:59 p.m. on June 30, 2022. During this

1. Report all sales (taxable and non-taxable) on

period, retail sales of gun safes and gun safety

Page 1, Line 1 (Gross Sales) of the sales tax

devices are exempt from sales and use tax.

return.

Gun Safes 2. Sales of exempt gun safes and gun safety

devices made during the holiday period must

A “gun safe” is defined as a locking container or other

be reported on Schedule A, Line 10 (Sales Tax

enclosure equipped with a padlock, key lock,

Holiday).

combination lock, or other locking device that is

designed and intended for the secure storage of one

This exemption will only be available for the one-year

or more firearms.

holiday period. All retail sales of gun safes and gun

safety devices made after June 30, 2022 will be

Gun Safety Devices

subject to sales tax.

A “gun safety device” is defined as any integral device

to be equipped or installed on a firearm that permits

For More Information

the user to program the firearm to operate only for

Visit www.tn.gov/revenue. Click on Revenue Help to

specified persons designated by the user through

search for answers or to submit an information

computerized locking devices or other means

request to one of our agents.

integral to and permanently part of the firearm.

References

Public Chapter 592 (2021). Tenn. Code Ann. § 67-6-

393

Disclaimer: The information provided here is current as of the date of publication but may change as a result of new statutes, regulations,

or court decisions. While this notice is intended to be comprehensive, events and situations unanticipated by this notice may occur. In such

cases you should contact the department or your tax professional for further guidance.You can also read