SINGAPORE Q4 2019 - REAL ESTATE TIMES - Soft 2019 economic growth and hopes of market recovery for commercial and residential markets in 2020 ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

REAL ESTATE

TIMES

JANUARY 2020

SINGAPORE Q4 2019

Soft 2019 economic growth and hopes of market recovery

for commercial and residential markets in 2020

ECONOMY

Market commentary In EDB’s 2019 year-in-review announcement in 16 January 2020,

Singapore far exceeded its forecast for investment commitments in

Key economic indicators 2019 by attracting $15.2bn, 39 per cent more than In 2018. The strong

Based on advanced estimates released figures reflect companies’ confidence in Singapore’s fundamentals and

by the Ministry of Trade and Industry on its strategic position at the heart of a growing Asia, with strong value

2 January 2020, the Singapore economy proposition of trust and stability along with sophisticated capabilities

grew by 0.7 per cent year-on-year (y-o-y) of its economy.

in 2019, moderating from the 3.1 per

cent y-o-y growth in 2018 (Table 1). The Table 1: GDP

construction sector had the strongest

performance, growing by 2.5 per cent y-o-y Y-o-y change (per cent)

Selected indicators

in 2019. However, the manufacturing sector Q3 2019 Q4 2019

contracted by 1.5 per cent y-o-y in 2019. Overall GDP 0.5 0.8

Global growth is projected to see a modest Manufacturing -1.7 -2.1

pickup in 2020, supported by emerging Construction 2.9 2.1

markets and developing economies, while Services producing industries 0.9 1.4

growth of key final demand markets for

Singapore such as the US and China is * Based on advanced estimates released by Source: MTI, EDMUND TIE Research

MTI on 2 January 2020

expected to ease amid trade tensions.

Market watchers are cautiously positive on

the possible easing of trade frictions and Table 2: Unemployment rate and fixed asset investments

improvements in global trade in the coming Y-o-y change

quarters. The Ministry of Trade and Industry Selected indicators

Q2 2019 Q3 2019

has forecast Singapore’s GDP growth to range

Unemployment rate 2.2% 2.3%

from 0.5 per cent to 2.5 per cent in 2020.

Fixed asset investments 4.3bn 0.2bn

Notwithstanding the continuing global

trade tensions and economic headwinds, Source: MTI, EDMUND TIE Research

Singapore continued to attract investment

commitment. The fixed asset investment

totalled 8.3bn from Q1 2019 to Q3 2019,

with a greater proportion recorded in H1

2019. The Singapore Economic Development

Board (EDB), with its focus on key priorities

including ASEAN, advanced manufacturing,

digital, innovation and growing new industry

clusters, had planned to attract $8bn to

S$10bn in fixed asset investments in 2019, in

line with previous years.

All monetary values are in Singapore dollars ($)

EDMUND TIE RESEARCH 1

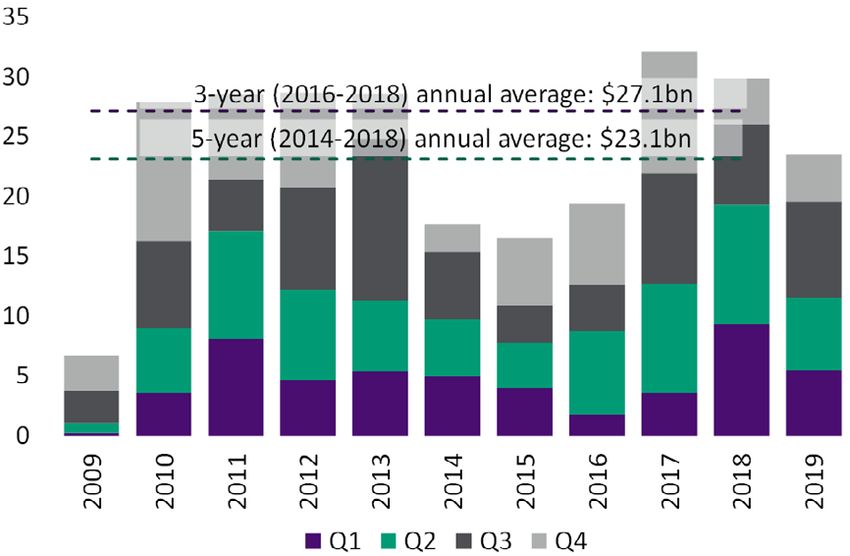

INVESTMENT Investment sales Figure 1: Total investment sales, $bn Against the backdrop of global geopolitical tensions, economic slowdown and business confidence falling to a near two-year low in Q4 2019 (according to the Singapore Commercial Credit Bureau’s Business Optimism Index report released on 16 September 2019), total investment sales value fell 22.2 per cent y-o-y to reach $23.2bn in 2019 (Figure 1). The private sector accounted for the bulk (or 78.1 per cent) of total investment sales value for 2019, with heightened sales activities for commercial assets by local and foreign institutional investors including REITs. Sale of sites sold under the Government Land Source: Various sources, EDMUND TIE Research Sales (GLS) Programme (Table 3) in 2019 was 28.4 per cent lower than in 2018. The decline was attributed to a fall in residential sale sites as property cooling measures and greater investor caution continued to bite homebuyer sentiments. Table 3: Investment sales summary* Key investment sale type 2018 ($m) 2019 ($m) y-o-y change (per cent) Private 22,745 (76.2%) 18,139 (78.1%) -20.3 Residential/Residential mixed-use 11,313 (37.9%) 278 (1.2%) -97.5 Office/Office mixed-use 4,713 (15.8%) 7,798 (33.6%) 65.4 Industrial/Industrial mixed-use 2,835 (9.5%) 3,849 (16.6%) 35.8 Retail/retail mixed-use 1,818 (6.1%) 3,085 (13.3%) 69.7 Hospitality/Hospitality mixed-use 923 (3.1%) 2,547 (11.0%) 176.0 Shophouses 1,143 (3.8%) 581 (2.5%) -49.1 Public (GLS) 7,113 (23.8%) 5,090 (21.9%) -28.4 Residential/Residential mixed-use 6,531 (21.9%) 4,316 (18.6%) -33.9 Office/Office mixed-use 365 (1.2%) Nil Not meaningful Industrial/Industrial mixed-use 154 (0.5%) 211 (0.9%) 36.8 Hospitality/Hospitality mixed-use 62 (0.2%) 562 (2.4%) 800.5 Total 29,858 (100%) 23,229 (100%) -22.2 * Refers to the sale of land, building and multiple units with value above $5 million. It excludes single strata or Source: Various sources, EDMUND TIE Research landed residential units, except for landed sites large enough to be redeveloped into two or more residential units. EDMUND TIE RESEARCH 2

Figure 2: Total investment sales by asset type Figure 3: Estimated Residential GLS supply

2018 Retail Mixed Use Hospitality Mixed

Shophouse No. of Dwelling Units

Industrial Mixed 1.7% Use

3.8% 14,000

Use 0.0%

Retail

0.0% Hospitality 12,000

4.4%

3.3%

10,000

Industrial 8,000

10.0%

6,000

Office Mixed Use

1.2% 4,000

Residential 2,000

52.2%

Office 0

H1 2014

H2 2014

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

15.8%

Residential Mixed

Use Confirmed List Reserve List

7.5%

Source: URA, EDMUND TIE Research

Figure 4: Estimated Commercial (excluding Hotels) GLS supply

2019 Sq ft ('000)

Hospitality

4,000

Hospitality Mixed Use Residential

11.3% 2.1% 3,500

16.6%

Shophouse 3,000

2.5%

2,500

Retail Mixed Use Residential Mixed Use

2.2% 2,000

3.2%

Retail 1,500

11.0% 1,000

500

Industrial Mixed 0

Use Office

H1 2014

H2 2014

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

6.8% 26.3%

Industrial Office Mixed Use Confirmed List Reserve List

10.7% 7.3%

Source: URA, EDMUND TIE Research

Source: Various sources, EDMUND TIE Research Figure 5: Estimated Industrial GLS supply

Sq ft ('000)

2,500

2,000

1,500

1,000

500

0

H1 2014

H2 2014

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

Confirmed List Reserve List

Source: JTC, EDMUND TIE Research

EDMUND TIE RESEARCH 3

Table 4: Key private investment sale transactions in Q4 2019 (above $100m)

Tenure/

Development name/location Purchase price Purchaser/investor type

(remaining tenure)

Office/Office mixed-use

99 years $547.5m Fund managed by Angelo Gordon and TCRE Partners

Bugis Junction Towers

(70 years) ($2,200 psf NLA) (Private property vehicle)

Industrial/Industrial mixed-use

99 years $1.576bn Mapletree Commercial Trust (local listed REIT) –

Mapletree Business City (Phase 2)

(76 years) ($1,330 psf NLA) related party transaction

Retail/retail mixed-use

60 years $296m Rock Productions (New Creation Church)

The Star Vista Mall

(48 years) ($1,817 psf NLA) (Private company)

Hospitality/hospitality mixed-use

99 years $475m Hoi Hup Realty Pte Ltd

Andaz Singapore

(91 years) ($1.4m per key) (Private property company)

97 years $163.3m City Developments Limited

Liang Court

(57 years) ($975 psf GFA) (Quoted property company)

Source: Various sources, EDMUND TIE Research

No GLS sites were recorded in Q4 2019.

Sector trends and outlook

• Office sector continued to stand out, increasing 53.5 15.9m visitors in the first 10 months of the year – a

per cent y-o-y in total private sector deals and GLS 2.3 per cent y-o-y increase above the same period

sites. The stronger interest is supported by investors’ in 2018. 2018 recorded a new-high in terms of total

confidence in office space demand and positive visitor arrivals of 18.5m.

outlooks for the sector as viable source of stable

• Residential collective sales remained lacklustre, falling

income-recurring assets.

from 52.2 per cent of total investment sales value in

The largest transaction in 2019 was Chevron House, 2018 to just 16.6 per cent in 2019.

which transacted at $1,025m (or $2,739 psf) to US

The overall investment sales value estimate of $23.2bn

investment firm, AEW from Oxley Holdings. The

for 2019 falls within our previous forecast range of

transaction price represents more than a 35 per cent

$22bn to $24bn. Despite the increase in investment sales

increase in capital value over the $660m that Oxley

for all commercial assets (barring shophouses), overall

Holdings had initially paid to acquire the development

investment sales value posted an annual decline in 2019,

in March 2018. Chevron House is currently undergoing

amid the dearth of residential collective sales. Concerns

addition and alteration (A&A) works to increase the

on the unsold supply glut also weighed on investors’

NLA in the building.

appetite for new residential sites. Along with existing

• Hospitality assets emerged as the next investors’ property cooling measures, residential investment sales

target, with investment sales value increasing 216 per activity is likely to be soft in the near term until we

cent y-o-y in 2019, underpinned by yet another record observe a continuous recovery in new sales momentum

year in international visitor arrivals in Singapore, with in the next three to four quarters.

EDMUND TIE RESEARCH 4OFFICE

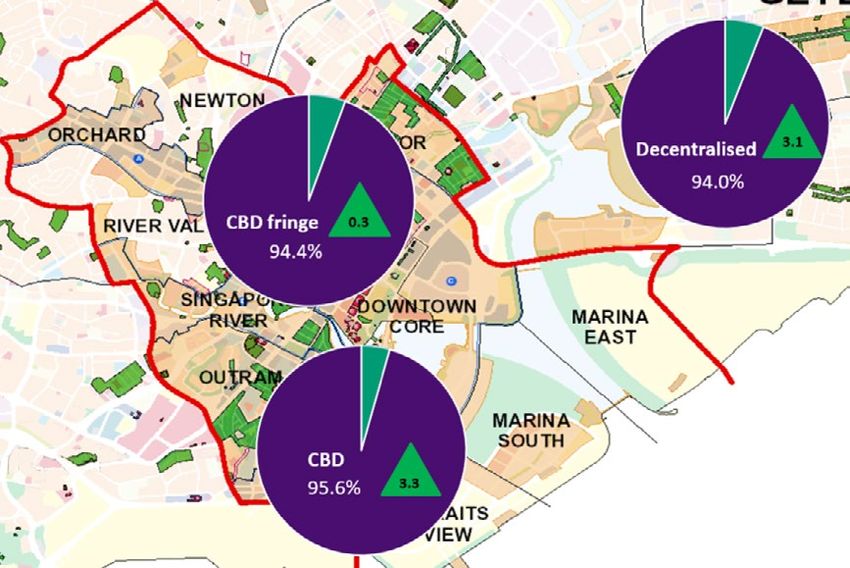

Office demand and occupancy rates Figure 6: Office occupancy rates* and y-o-y percentage point change (in

green arrows) in Q4 2019

• Based on our estimates, occupancy rates

of office developments* island-wide

trended upwards by 2.5 percentage

points y-o-y to 94.9 per cent in Q4 2019.

This was greater than the 0.9 percentage

points growth in Q4 2018. In Q4 2019,

occupancy in the Central Business

District (CBD) increased the most by 3.3

percentage points y-o-y to 95.6 per cent

(Figure 6).

• In 2019, co-working and technology

firms remained the major occupiers

of CBD office space despite challenges

faced by selected co-working operators, Central Area

notably WeWork and Wotso. Within the

co-working market segment, there has * In-house estimates of purpose-built office developments and Source: URA, OneMap,

mixed-use premises with NLA of 20,000 sq ft and above EDMUND TIE Research

been consolidation such as the merger

of Collision 8 and Found into Found8. We

observed some co-working operators

expanding into the CBD fringe locations, in

light of the near saturation of co-working

spaces in the CBD. A notable example is

JustCo, which opened its 50,000 sq ft of

space in Manulife Centre and is expected

to house about 1,000 members (Table 5).

Table 5: Key tenant movements in Q4 2019

Building Location Tenant Sector Remarks (space occupied)

Marina Bay Financial

Littler Law New location in REGUS

Centre Tower 3 Marina Bay (CBD)

Asia Square Tower 2 First Abu Dhabi bank Finance Relocation (22,000 sq ft)

9 Battery Road Upgrade Pack Travel technology New location

Raffles Place (CBD)

OUE Bayfront Aramco Oil and Gas Relocation (30,000 sq ft)

AXA Tower Shenton Way/ Cofco Agri Agri-business Relocation (14,000 sq ft)

Robinson Road/

79 Anson Road Tanjong Pagar (CBD) Wan Hai Lines Shipping Relocation (11,000 sq ft)

Millenia Tower CSOP Asset Management Investment New location

Bugis Junction Towers ADMIS Singapore Finance Relocation (10,000 sq ft)

City fringe

Manulife Centre JustCo Co-working New location (50,000 sq ft)

Visioncrest Commercial GFK Singapore Technology Relocation (11,000 sq ft)

The Metropolis Decentralised areas Aedas Architecture Relocation (20,000 sq ft)

Source: Various sources, EDMUND TIE Research

EDMUND TIE RESEARCH 5Rental rates Table 6 : Average monthly gross office rents ($ per sq ft)

Q-o-q

The average gross monthly rents rose across

Location Grade Q3 2019 Q4 2019 change

most of the sub-locations by 0.0 to 1.7 per (%)

cent q-o-q (Table 6). Average CBD rents rose Marina Bay A+ 11.25 – 13.30 11.35 – 13.40 0.8

by 1.3 per cent q-o-q and 7.0 per cent y-o-y

Raffles Place A 9.40 – 11.50 9.60 – 11.70 1.7

for Q4 2019.

CBD A+ 10.10 – 12.10 10.20 – 12.30 1.0

Shenton Way/

Supply pipeline Robinson Road/ A 8.10 – 10.10 8.10 – 10.10 0.0

Tanjong Pagar

B 6.60 – 8.70 6.70 – 8.80 1.7

The total supply pipeline from Q4 2019 to

2023 is estimated to be approximately 4.7m Marina Centre A 8.90 – 10.90 8.90 – 10.90 0.3

sq ft (or 1.1m sq ft per annum). (Figure 7). Beach Road/ A 9.80 – 11.80 9.80 – 11.80 0.2

City Fringe North Bridge

9 Penang Road has obtained Temporary B 6.55 – 8.00 6.55 – 8.00 0.5

Road

Occupation Permit (TOP) in Q4 2019. Global

Orchard Road * 8.55 – 10.60 8.55 – 10.60 0.0

bank, UBS, will relocate its headquarters to

9 Penang Road, relocating from its offices in Decentralised Decentralised

* 5.00 – 7.50 5.00 – 7.50 0.0

One Raffles Quay North Tower and Suntec areas** areas

Tower Five. * Ungraded office space Source: EDMUND TIE Research

** Key purpose-built offices outside of CBD and CBD Fringe

Outlook

The office market is expected to expand in

Figure 7: CBD office development pipeline, million (m) sq ft

terms of footprint and leasing activity, albeit

at a moderated pace in 2020, in view of the

projected modest recovery of Singapore’s

economic growth. Demand for office space

in the CBD will continue to come from the

information & communications and finance

& insurance sectors, supported by the

healthy demand for IT and digital solutions

as well as sustained demand for payment

processing services. Firms providing asset

management and legal services could be

on the lookout for office spaces as inbound

investment to Singapore is expected to step

up on the back of investors’ search for safe

haven investment destinations in Asia. Source: URA, EDMUND TIE Research

EDMUND TIE RESEARCH 6INDUSTRIAL

Market commentary Table 7: Singapore’s NODX and PMI

Key

Key indicators Q3 Nov

economic Key trends

2019 2019

The Non-Oil Domestic Exports (NODX) and the indicators

Purchasing Managers’ Index (PMI) in November • NODX fell by 5.9 per cent in November

2019 showed tentative signs of bottoming out 2019, moderating after the 12.5 per cent

NODX -8.1 -5.9 contraction in October 2019. This was

for the manufacturing sector (Table 7). largely due to the decline in electronics

exports.

Private demand, • The PMI edged up by 0.2 points from

occupancy and supply the previous month to 49.8 points in

November 2019.

PMI* 49.5 49.8

• Based on JTC’s estimates (available at the • The electronics sector increased by 0.4

points from the previous month to report

time of this report on 17 January 2020),

a slower contraction at 49.7 points.

island-wide net absorption doubled

q-o-q to approximately 3.3m sq ft in * Reading above 50 indicates an expansion, Source: MTI, Enterprise Singapore,

while below 50 indicates a contraction. SIPMM, EDMUND TIE Research

Q3 2019, while net supply more than

doubled from 1.4m sq ft to 3.3m sq ft

q-o-q.

Figure 8: Occupancy rates of private industrial space by type

• On a quarterly basis, while net supply

100%

for single-user factories (1.1m to 2.3m

sq ft) and warehouses (0.7m to 1.1m sq 95%

ft) increased in Q3 2019, net supply for 90%

multiple-user factories remained in the 85%

negative zone (-22,000 sq ft). There was no

80%

new business park space supply in Q3 2019.

75%

• Occupancy rates of private industrial 70%

space were relatively steady in Q3 2019,

Q3 2010

Q3 2011

Q3 2012

Q3 2013

Q3 2014

Q3 2015

Q3 2016

Q3 2017

Q3 2018

Q3 2019

with slight q-o-q improvements across

industrial types – multiple-user factories

(0.1 percentage points), single-user Multiple-user factory space Single-user factory space

factories (0.3 percentage points) and Business park space Warehouse space

business parks (0.3 percentage points),

Source: JTC, EDMUND TIE Research

except for warehouses which recorded a

figure of -0.5 percentage points (Figure 8).

EDMUND TIE RESEARCH 7• Bollore Logistics has opened a new Table 8: Average monthly gross rents (island-wide)

warehouse facility, Blue Hub (538,195

Q3 2019 Q4 2019

sq ft), following the completion of the Industrial type* Q-o-q change (%)

($ per sq ft) ($ per sq ft)

warehouse in Q3. The facility is fully First-storey:

automated to support the growth 1.70 – 2.00 -0.4

Multiple-user 1.70 – 2.00

of customers in the perfumes and factory Upper-storey:

cosmetics sector. 1.40 – 1.60 -0.2

1.40 – 1.60

• Notable leases secured/expansion Warehouse/logistics 1.50 – 1.70 1.50 – 1.70 -0.8

announcements in Q3 2019 included: High-tech industrial 2.90 – 3.10 2.90 – 3.10 0.3

– Neste, a Finnish energy giant Central region:

4.40 – 4.90 1.2

4.40 – 4.90

announced expansion plans to boost Business park

its Tuas facility capacity from 1m to Suburban areas:

3.50 – 3.80 0.5

3.50 – 3.80

2.3m tonnes.

* In-house estimates of key selected Source: EDMUND TIE Research

– Amazon Singapore expanded its private industrial premises.

warehouse space in Mapletree

Logistics Hub to support its ramp-up

of its retail operations in Singapore. Figure 9: Private monthly industrial gross rents ($ psf per month) by type

– An established global technology, 6

defence and engineering company

headquartered in Singapore has 5

secured over 300,000 sq ft of space

4

in Commodity Hub (under Cache

Logistics Trust’s portfolio). 3

– P-Way Construction and Engineering

2

has secured about 168,800 sq ft of

space at 8 Tuas South Lane, a multiple- 1

user factory.

Q4 2010

Q4 2011

Q4 2012

Q4 2013

Q4 2014

Q4 2015

Q4 2016

Q4 2017

Q4 2018

Q4 2019

Rental rates

First-storey Upper-storey Hi-tech Business park (Central Region)

• Based on our estimates, monthly rental Source: EDMUND TIE Research

rates for multiple-user factories and

warehouse/logistics* moderated in Q4

2019, as industrial demand remained

lacklustre for these sub-sectors amid

weakened manufacturing performance

(Table 8 and Figure 9).

• Monthly rents for high-tech industrial and

business parks reported quarterly increases

due to the limited available supply.

EDMUND TIE RESEARCH 8Supply pipeline Figure 10: Private industrial development pipeline (with planning

approvals and GLS sites which are pending approvals), million (m) sq ft

• From Q4 2019 to 2022, there will be

approximately 26.2m sq ft NLA (or 8.1m sq

ft per annum) in the supply pipeline. This

is significantly lower than the past 3- and

5-year annual average supply (Figure 10).

• There are five business park

developments in the pipeline, totalling

1.4m sq ft, including an A&A to the

existing development at 13 International

Business Park by Pension Real Estate

Singapore Pte Ltd.

• While consultancy firm Surbana-Jurong’s

new campus is due for completion in

2021, tech companies such as Grab Source: JTC, EDMUND TIE Research

Headquarters (317,000 sq ft) and Razer

Headquarters (145,000 sq ft) are due for

completion in 2020.

Outlook

The industrial property market is expected achieve a wider global reach. An example is the Digital and Advanced

to see modest improvements in 2020, Manufacturing Programme launched on 19 December 2019, which

supported by the gradual recovery in allows companies to explore new technologies and undergo training.

the manufacturing sector. Of which, the

Additionally, Singapore continues to invest in infrastructure, partnerships

electronics and precision engineering

and innovation to boost its digital economy. This includes the introduction

exports are expected to improve with

of 5G mobile networks by 2020 to ensure Singapore’s competitive edge

possible easing of US-China trade tensions.

as a trading and connectivity hub. Amid rising labour costs, the use of

Moving forward, the Government has digital tools will also help companies to operate effectively.

introduced various initiatives to assist

With a tapered supply in the pipeline over the next few years,

industrial companies in the upgrading of

occupancy and rental rates are expected to receive some support.

their digital capabilities and facilities to

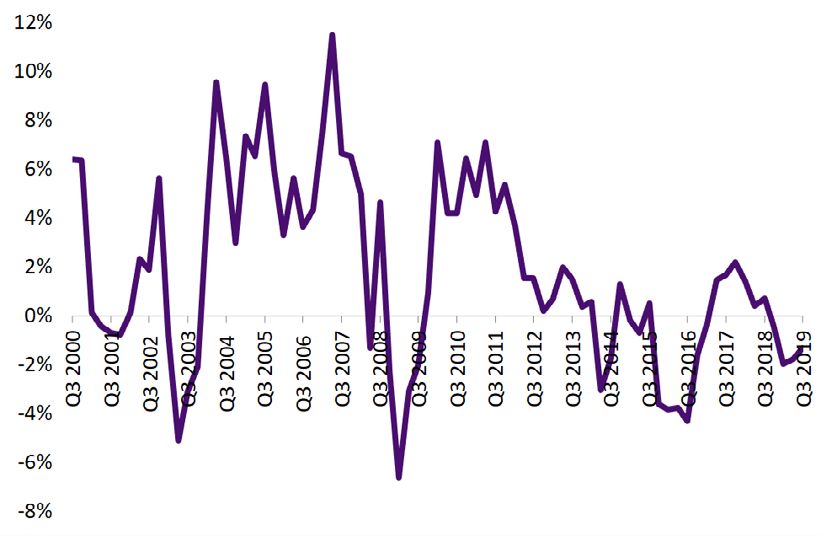

EDMUND TIE RESEARCH 9RETAIL Figure 11: Y-o-y change in retail sales index (excluding motor vehicles)

Market commentary

Key indicators

• Retail sales index (excluding motor

vehicles) trended downwards for the

fourth consecutive quarter by 1.3 per

cent q-o-q in Q3 2019 (Figure 11).

However, the decline in Q3 2019 was

moderated as compared to the -1.8 per

cent contraction in Q2 2019.

Source: Department of Statistics Singapore

• In October 2019, the top three

gainers (on y-o-y basis) were wearing

apparel and footwear as well as the Figure 12: Retail sales index (Oct 2019), y-o-y change

supermarkets, hypermarkets; mini- Wearing Apparel & Footwear 6.6%

marts and convenience stores sectors. Supermarkets & Hypermarkets 1.9%

The furniture and household equipment, Mini-marts & Convenience Stores 0.7%

optical goods and books as well as Computer & Telecommunications Equipment -0.1%

watches and jewellery sectors reported Medical Goods & Toiletries -1.3%

the largest contraction y-o-y in the same Food Retailers -1.8%

month (Figure 12). In terms of the Food Department Stores -1.9%

& Beverage services index, fast food Recreational Goods -2.7%

outlets had the largest expansion of 6.3 Watches & Jewellery -4.2%

per cent y-o-y (Figure 13). Optical Goods & Books -6.4%

Furniture & Household Equipment -7.4%

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

Source: Retail Sales Index at Constant Prices (SSIC 2015 Version 2018)

from Department of Statistics Singapore

Figure 13: Food & Beverage services index (Oct 2019), y-o-y change

Food Caterers -7.2%

Cafes, Food Courts & Other Eating Places 1.6%

Restaurants 4.3%

Fast Food Outlets 6.3%

-10% -5% 0% 5% 10%

Source: Food & Beverage Services Index at Constant Prices (SSIC 2015 Version 2018)

from Department of Statistics Singapore

EDMUND TIE RESEARCH 10• The online retail sales proportion has Figure 14: Retail sales value and proportion of online retail sales

also been on an increasing trend since 4,500 8

the start of 2019 supported by the 4,000 7

growth in e-commerce (Figure 14). 3,500 6

3,000

• Tourism receipts declined by 1.3 per cent 5

2,500

y-o-y to $6.5bn in Q2 2019 and majority 4

2,000

of the sectors reported a decline y-o-y. 3

1,500

Visitors from Mainland China, Indonesia 2

1,000

and India were the top nationalities

500 1

that visited Singapore in Q3 2019. The

0 0

ongoing Hong Kong unrest situation have

2018 Jun

2019 Mar

2019 May

2019 Jun

2019 Jul

2018 May

2018 Jul

2018 Aug

2019 Aug

2018 Mar

2018 Dec

2019 Apr

2018 Feb

2018 Apr

2018 Sep

2019 Feb

2019 Sep

2019 Oct

2018 Oct

2018 Jan

2018 Nov

2019 Jan

also prompted more Mainland Chinese

visitors to visit Singapore.

Retail Sales Value - Estimated (millions) (LHS)

Online Retail Sales Proportion (%) (RHS)

Private demand, Source: Department of Statistics Singapore, EDMUND TIE Research

occupancy and supply

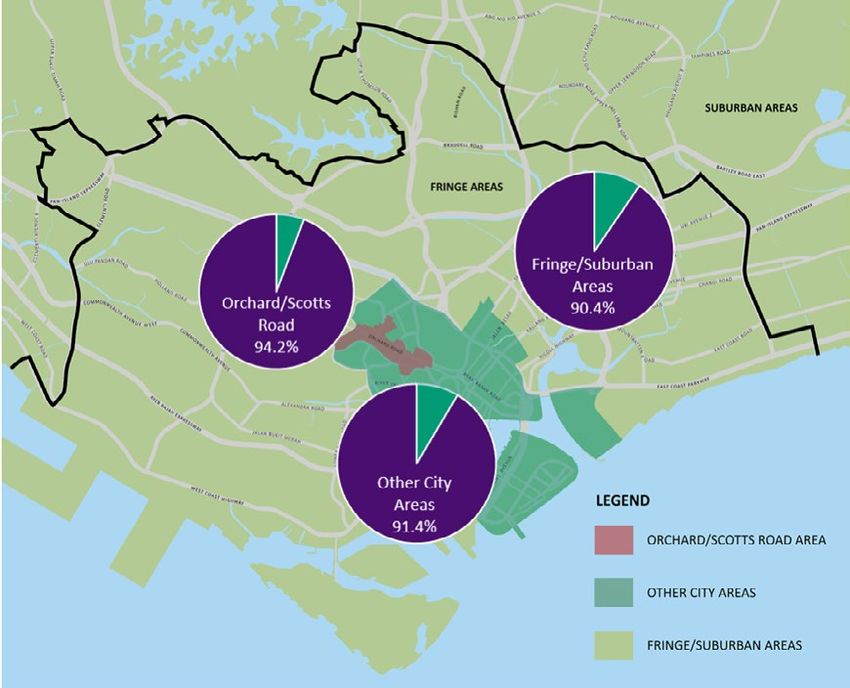

• Based on URA statistics (available at the Q3 2019 with the completion of Paya Lebar Quarter (Phase 2) (NLA:

time of this report on 17 January 2020), 291,000 sq ft) and A&A to the existing podium of China Square

the retail market saw modest demad Central (NLA: 80,000 sq ft).

with total net absorption moderating to

• From URA’s estimates, island-wide occupancy increased marginally

374,000 sq ft in Q3 2019, from 888,000 sq

by 0.1 percentage points q-o-q to 91.3 per cent in Q3 2019.

ft in Q2 2019. Net supply was positive in

Orchard/Scotts Road (OSR) Other City Areas 1 (OCA) Fringe/Suburban Areas2 (FSA)

Net • Net absorption reversed from 36,000 sq ft in • Net absorption moderated to • Net absorption moderated to

absorption Q2 2019 to -12,000 sq ft in Q3 2019. 187,000 sq ft in Q3 2019, from 199,000 sq ft in Q3 2019, from

382,000 sq ft in Q2 2019. 469,000 sq ft in Q2 2019.

Occupancy • Occupancy rate declined slightly by 0.1 • Occupancy rate increased by • Occupancy declined slightly by

percentage points q-o-q to 94.2 per cent in Q3 0.9 percentage points q-o-q 0.3 percentage points to 90.4

2019 (Figure 15). to 91.4 per cent in Q3 2019. per cent in Q3 2019.

New • Five Guys (F&B) in Plaza Singapura • Carmen’s Best (F&B) in Capitol • Yun Nans (F&B) in Westgate

Openings • Go Noodle House (F&B) in 313@Somerset Singapore • Sony (technology) in Westgate

(Q4 2019) • Nam Dae Mun (F&B) in 313@Somerset • Asus Experience Store • Don Don Donki (F&B) in Jcube

• Merci Marcel (F&B) in Palais Renaissance (technology) in Bugis Junction • Rabeanco (Leather specialist)

• Social Place (F&B) in Forum The Shopping Mall • Liverpool FC Singapore store in Jewel Changi

• Croquant Chou Zakuzaku (F&B) in Ion Orchard (Fashion) in Bugis Junction

• Style Theory (Fashion) in 313@Somerset • The Whale (F&B) in China

Square Central

• La Mer (Skincare) in The

Shoppes at Marina Bay Sands

Closures • Crate & Barrel (furniture and homeware) • Gudetama Cafe and My • Home-Fix (all outlets)

(Q4 2019) in Orchard Gateway Melody Cafe in Suntec City • Sasa (all outlets)

• Hokkaido’s Bake Cheese Tart (F&B) in

Ion Orchard

1 Other City Areas refer to Downtown Core and Rest of Central Area Source: URA, EDMUND TIE Research

2 Fringe/Suburban Areas refer to Fringe Areas and Suburban Areas (Outside Central Region)

EDMUND TIE RESEARCH 11Rental rates Figure 15: Retail occupancy rates (Q3 2019)

Based on our estimates, island-wide average

monthly rental rates increased marginally by

0.3 per cent to $22.20 per sq ft in 2019. On

a q-o-q basis, rents declined slightly in the

Orchard/Scotts Road subzone (Table 9).

Leasing demand for first storey/prime retail

spaces in other city areas recovered slightly,

as retailers sought prime spaces to capture

higher footfall and visibility.

Amid cautious consumer sentiment, we

observed a slight decline in demand for

upper-floor retail spaces in fringe/suburban

areas, with a 0.7 per cent q-o-q decline in

monthly rentals for the last quarter of 2019.

Source: URA, EDMUND TIE Research

Table 9: Average monthly gross rents ($ per sq ft)

Location Q3 2019 Q4 2019 Q-o-q change

First storey:

34.10 – 39.10 -0.2

34.20 – 39.20

OSR

Upper storey:

13.90 – 18.00 -0.3

14.00 – 18.00

First storey:

16.10 – 21.30 0.1

16.10 – 21.10

OCA

Upper storey:

8.10 – 12.10 -0.1

8.10 – 12.10

First storey:

25.30 – 31.30 0.0

25.30 – 31.30

FSA

Upper storey:

14.90 – 19.90 -0.7

15.00 – 20.00

Source: EDMUND TIE Research

EDMUND TIE RESEARCH 12Supply pipeline Figure 16: Retail development pipeline, million (m) sq ft

The supply pipeline from Q4 2019 to 2022

is projected to be limited comprising some

602,000 sq ft NLA (Figure 16). In Q4 2019, 9

Penang Road in the OSR has obtained TOP,

comprising an NLA of 15,000 sq ft.

Outlook

The retail property market remained fairly

uncertain in view of the soft retail sales

performance, tight labour regulations and

the growing e-commerce industry. Despite

these challenges, the F&B sector is viewed

as the bright spot of the industry as seen

Source: URA, EDMUND TIE Research

from the growth of 4.5 per cent y-o-y in the

F&B services index in October 2019. This is

supported by the many new F&B concepts

introduced in 2019 and some of which have Moving forward, integrating physical brick-and-mortar experience with

attracted visible crowds of customers (e.g. online retailing will be an essential strategy for asset owners and retailers

Shake Shack in Jewel Changi). In H2 2019, to expand their consumer outreach.

various sales events, such as Singles Day and

Black Friday have been introduced, which As a case in point, we have witnessed trend reversal from established

helped to boost retail sales. online retailers – such as Taobao and Love, Bonito – which have moved

into physical retail space for an omnichannel approach. Mall owners,

together with their business partners, are likely to step up their proactive

engagement strategies with retailers and visitors to continously bring

new retail concepts and activities in their retail spaces.

Island-wide overall retail rentals are projected to trend sideways

within the band range of -1.0 to 1.0 per cent in 2020 and the limited

supply pipeline from 2020 onwards will provide some support to rents

and occupancy levels.

EDMUND TIE RESEARCH 13RESIDENTIAL

Market commentary Figure 17: New housing loans limits granted

$millions

Key economic indicators 14,000

• Based on Q4 2019 Urban Redevelopment 12,000

Authority (URA) flash estimates released

10,000

on 2 January 2020, private home prices

8,000

for the fourth quarter of 2019 reflected

a marginal 0.3 per cent q-o-q and 2.5 per 6,000

cent y-o-y increase. 4,000

2,000

• Private non-landed property prices

declined by 0.7 per cent q-o-q in Q4 0

Q1 2015

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Q3 2017

Q4 2017

Q1 2018

Q3 2018

Q4 2018

Q2 2019

Q3 2019

Q2 2018

Q1 2019

2019, a reversal compared to the 1.3 per

cent growth in Q3 2019. Of which, prices

of non-landed properties in the CCR and Source: MAS (as of 27 December 2019), EDMUND Tie Research

RCR declined, except for non-landed

properties in the OCR, which increased Figure 18: Private homes sales volume (excluding ECs) and URA All

by 2.9 per cent q-o-q in Q4 2019. Residential Price Index

• URA Landed Property Price Index 8,000 160

trended upwards by 4.0 per cent q-o-q in 7,000 155

6,000

Q4 2019, extending from the 1.0 per cent 150

5,000

growth reported in Q3 2019. 145

4,000

140

• Housing loans increased marginally by 3,000

135

3.7 per cent y-o-y in Q3 2019 (Figure 17), 2,000

after four consecutive quarters of decline 1,000 130

amid moderated demand for housing 0 125

Q4 2019*

Q1 2015

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Q3 2017

Q4 2017

Q1 2018

Q2 2018

Q3 2018

Q4 2018

Q1 2019

Q2 2019

Q3 2019

loans since the July 2018 property cooling

measures with further tightening of loan-

to-value threshold for borrowers. Units Sold in Secondary Market (subsale and resale) (LHS)

New Sales Units Sold by Developers (LHS)

• New sales volume is expected to Property Price Index of All Residential Properties (RHS)

outweigh resale volume, including both * Q4 2019 sales volume based on monthly developer sales and Source: URA, REALIS,

resale and sub sale, for the second caveats from REALIS as at 27 December 2019, PPI at Q4 2019 EDMUND Tie Research

consecutive quarter in Q4 2019, albeit based on flash estimate

at a lower new sales volume compared

to the third quarter due to the lower

number of launches for the last quarter

of 2019 (Figure 18 and Table 10).

EDMUND TIE RESEARCH 14Table 10: Non-landed private residential launches (excluding ECs) in Q4 2019 (projects >20 units)

District Launch Initial Indicative

Total Units

Development Developer (market month in sell-down average price

units sold

segment) 2019 rate* (%) ($ psf)

Neu at Novena Roxy-Pacific Holdings Ltd 11 (CCR) 87 October 54 62 2,604

Midtown Bay GuocoLand Ltd 9 (CCR) 219 October 48 22 2,917

Royalgreen Allgreen Properties Limited 10 (CCR) 285 October 42 15 2,743

Midwood Hong Leong Holdings 23 (OCR) 564 October 24 4 1,641

The Iveria Macly Group 9 (CCR) 51 November 13 26 2,643

One Holland Far East Organization, Sino

10 (CCR) 296 November 87 29 2,680

Village Residences Group and Sekisui House

Pullman Residences, EL Development (Horizon)

11 (CCR) 340 November 12 4 2,992

Newton Pte Ltd

Dairy Farm

United Engineers 23 (OCR) 460 November 35 8 1,547

Residences

Sengkang Grand CapitaLand and City

19 (OCR) 680 November 235 35 1,746

Residences Developments Limited

Total units from Q4 2019 launches 2,982

* Estimates analysed from caveats lodged (from REALIS as of 3 January 2020) Source: URA, EDMUND TIE Research

• One Holland Village Residences, • Conversely, resale volume is envisaged to decline to about 2,000

comprising a total of 296 residential units in the last quarter, due in part to the end-of-year seasonal

units within One Holland Village mixed- lull and some homeowners are seen to be holding back their

use development, received positive divestment plans in anticipation of possible return of buyers from

responses with 87 units sold since the the first quarter of 2020.

end-November preview sales launch.

Buyers are observed to be predominantly • Total private homes sales volume for Q4 2019 is projected to reach

locals. The coveted address in prime approximately 4,600 units, higher compared to 3,860 units in Q4

district 10, combined with its integrated 2018.

development appeal in a vibrant location • With these Q4 estimates, we forecast that total sales volume of

are strong selling points for the project. private homes could reach close to 19,000 units for the whole of

• Other integrated developments with 2019, compared to 22,139 units in 2018.

residential units launched in the fourth • In terms of the private residential leasing market, total rental

quarter that saw encouraging responses contracts volume rose by 4.5 per cent y-o-y to reach 27,000

include Midtown Bay and Sengkang Grand transactions in Q3 2019 (Figure 19). The URA Rental Index for All

Residences. Homebuyers are attracted to Residential Property has risen for three consecutive quarters in

the multiple attributes of trade variety, 2019 with cumulative increase of 2.4 per cent from Q4 2018. These

convenience and lifestyle appeal offered trends were supported by the lower number of completed private

by these integrated developments. homes in 2019 and a firmer overall occupancy of 93.9 per cent for

the third quarter. In view of a weakened economic performance

for the second half of 2019 and dimmed job market prospects that

EDMUND TIE RESEARCH 15could have curtailed foreign workforce Figure 19: Number of private home rental transactions (excluding ECs)

growth and accommodation budgets,

we envisage overall private home rental

movement to trend sideways with -0.3

to 0.2 per cent q-o-q change in Q4 2019

(Figure 20).

Outlook

• Notwithstanding the new high pricing set

by new launch projects in 2019 compared

to previous year’s launches, there is

growing acceptance from homebuyers

on the price premium factors accorded

to well-located projects with concepts

* Preliminary estimates of rental transactions in Q4 2019, Source: REALIS,

that appeal in lifestyle and convenience. based on REALIS data as of 3 January 2020 EDMUND Tie Research

The Government’s 2019 Master Plan to

transform various precincts has provided Figure 20: Private non-landed home completions (excluding ECs)

clarity on Singapore’s future property and URA Rental Index

landscape and instilled confidence on

9,000 114

the prospects of residential property 8,000 112

investment. 7,000 110

6,000 108

• The high liquidity in the market, fuelled 5,000

106

by low interest rates, has also supported 4,000

3,000 104

demand for residential property 2,000 102

investment. With limited attractive 1,000 100

options to invest in equities and bonds 0 98

Q4 2019*

Q1 2015

Q2 2015

Q3 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q2 2017

Q3 2017

Q4 2017

Q1 2018

Q3 2018

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2015

Q1 2017

Q2 2018

amid compressed yields and returns,

non-institutional retail investors view

residential property as a possible long- Total Non-landed Completions (LHS) URA non-landed rental index (RHS)

term investment and a hedge against

inflation. For foreign investors, the strong * Based on forecast of -0.1 per cent q-o-q Source: URA, REALIS, EDMUND Tie Research

change for rental index in Q4 2019

Singapore Dollar which has held up well

historically against regional currencies, is • In consideration of a potential recovery in economic outlook with

another attraction. preliminary easing of trade frictions and assuming existing cooling

measures to remain status quo, we could expect private home prices

• The upcoming launches in the first half of

to trend at a steady growth path in 2020, akin to a ‘Goldilocks effect’.

2020, located mainly in the Core Central

We forecast 2 per cent to 4 per cent annual price growth for private

Region, will be closely watched as the

homes for year 2020, with possible price uptick of 0.5 per cent to 0.8

market assess demand conditions and

per cent for non-landed homes in the first quarter of 2020.

sales performance.

EDMUND TIE RESEARCH 16CONTACTS Ong Choon Fah

Chief Executive Officer

+65 6393 2318

choonfah.ong@etcsea.com

PROFESSIONAL SERVICES

Valuation Advisory Property Tax Advisory & Hospitality Property Management

Poh Kwee Eng Statutory Valuation Nicholas Cheng Kwok Sai Kuai

Executive Director Ng Poh Chue Executive Director Executive Director

Regional Head of Executive Director +65 6393 2317 Regional Head of

Valuation Advisory +65 6393 2515 nicholas.cheng@etcsea.com Property Management

+65 6393 2312 pohchue.ng@etcsea.com +65 6417 9229

kweeeng.poh@etcsea.com Heng Hua Thong saikuai.kwok@etcsea.com

Senior Advisor

Nicholas Cheng Research & Consulting +65 6393 2398 Paul Wong

Executive Director huathong.heng@etcsea.com Senior Director

Ong Choon Fah

+65 6393 2317 +65 6417 9225

Chief Executive Officer Tay Hock Soon

nicholas.cheng@etcsea.com paul.wong@etcsea.com

+65 6393 2318 Senior Director

choonfah.ong@etcsea.com +65 6887 0088

tayhs@treetops.com.sg

AGENCY SERVICES REGIONAL OFFICES

Investment Advisory Auction & Sales Business Space & Retail Malaysia

Ong Choon Fah Nicholas Cheng Chua Wei Lin Eddy Wong

Chief Executive Officer Executive Director Executive Director Managing Director

+65 6393 2318 +65 6393 2317 Regional Head of +603 2024 6380

choonfah.ong@etcsea.com nicholas.cheng@etcsea.com Business Space eddy.wong@ntl.my

+65 6393 2326

Edmund Tie Joy Tan weilin.chua@etcsea.com

Senior Advisor Senior Director

+65 6393 2386 +65 6393 2505

edmund.tie@etcsea.com joy.tan@etcsea.com China Desk Thailand

Yam Kah Heng Yam Kah Heng Ong Choon Fah

Senior Advisor Residential Senior Advisor Chief Executive Officer

+65 6393 2368 +65 6393 2368 +65 6393 2318

kahheng.yam@etcsea.com Margaret Thean kahheng.yam@etcsea.com choonfah.ong@etcsea.com

Executive Director

Heng Hua Thong Regional Head of Residential Heng Hua Thong Punnee Sritanyalucksana

Senior Advisor +65 6393 2383 Senior Advisor Chief Operating Officer

+65 6393 2398 margaret.thean@etcsea.com +65 6393 2398 +66 2257 0499 ext 101

huathong.heng@etcsea.com huathong.heng@etcsea.com punnee.s@etcthailand.co.th

Karen Ong

Swee Shou Fern Senior Director Tan Chun Ming

Executive Director +65 6393 2366 Executive Director

+65 6393 2523 karen.ong@etcsea.com +65 6393 2360

shoufern.swee@etcsea.com chunming.tan@etcsea.com

Tan Chun Ming

Executive Director

Regional Investment Advisory

+65 6393 2360

chunming.tan@etcsea.com

Editor: Authors:

Saleha Yusoff Alice Tan Isabelle Seto

Executive Director Senior Director Senior Research Analyst

Regional Head of Research & Consulting Research

Research & Consulting +65 6393 2329 +65 6393 2382

+603 2161 7228 ext 302 alice.tan@etcsea.com isabelle.seto@etcsea.com

saleha.yusoff@etcsea.com

For more information, please contact us at research.sg@etcsea.com.

Disclaimer: The information contained in this document and all accompanying presentations (the “Materials”) are approximates only, is subject to change

without prior notice, and is provided solely for general information purposes only. While all reasonable skill and care has been taken in the production of

the Materials, Edmund Tie & Company (the “Company”) make no representations or warranties, express or implied, regarding the completeness, accuracy,

correctness, reliability, suitability, or availability of the Materials, and the Company is under no obligation to subsequently correct it. You should not rely on the

Materials as a basis for making any legal, business, or any other decisions. Where you rely on the Materials, you do so at your own risk and shall hold the Company,

its employees, subsidiaries, related corporations, associates, and affiliates harmless to you to and any third parties to the fullest extent permitted by law for any losses,

damages, or harm arising directly or indirectly from your reliance on the Materials, including any liability arising out of or in connection with any fault or negligence. Any

disclosure, use, copying, dissemination, or circulation of the Materials is strictly prohibited, unless you have obtained prior consent from the Company, and have credited

the Company for the Materials. © Edmund Tie & Company 2020

Edmund Tie & Company (SEA) Pte Ltd

5 Shenton Way, #13-05 UIC Building, Singapore 068808. | www.etcsea.com | T. +65 6293 3228 | F. +65 6298 9328 | mail.sg@etcsea.comYou can also read