Debt Investor Presentation - June 14, 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Debt

Investor

Presentation

June 14, 2019

DISCLAIMER

IMPORTANT: THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS CONFIDENTIAL AND IS TO BE USED FOR

INFORMATIONAL PURPOSES ONLY.

YOU MUST READ THE FOLLOWING BEFORE CONTINUING: Important notice

This presentation (including any oral briefing and any question-and-answer session in connection with it) (the “Presentation”) is for informational purposes only and is provided on a

confidential basis. Disclosure of the information contained in this Presentation to any other person or any reproduction of this information, in whole or in part, without the prior

written consent of Sodexo (the “Company”) is prohibited and is furthermore subject to the terms of any confidentiality agreements entered into. This Presentation is not intended to,

and does not constitute, represent or form part of any offer, invitation, inducement or solicitation of any offer to purchase, otherwise acquire, subscribe for, sell or otherwise dispose

of, any securities. It must not be acted on or relied on in connection with any contract or commitment whatsoever. It does not constitute a recommendation regarding any securities.

This Presentation is only being provided to persons outside the United States in accordance with Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities

Act”). By attending this Presentation or by reading the Presentation slides, you warrant and acknowledge that you fall within this category. No securities of the Company have

been, or will be, registered under the Securities Act.

This Presentation does not purport to be comprehensive or to contain all of the information that a person considering the purchase of the securities or providing any other

indebtedness contemplated by the proposed transactions may require for a full analysis of the matters referred to herein. Any purchase of securities in the offering should be made

solely on the basis of information contained in the offering memorandum to be published in respect of the offering. This Presentation is based on historical information provided by

the Company’s management and advisers or taken from third party sources none of which has been independently verified. There is no guarantee of the accuracy or completeness

of such data. The information contained within this Presentation is subject to change without notice, it may be incomplete or condensed, and it may not contain all material

information concerning the Company’s and its affiliates and/or connected parties.

None of the Company, it subsidiaries, affiliates, associates, or their respective directors, officers, partners, employees, representatives or advisors (collectively, the “Company’s

Representatives”) or any other person makes any representation or warranty, express or implied, as to the fairness, accuracy or completeness of the information contained in this

Presentation or otherwise made available or of the views given or implied, nor as to the reasonableness of any assumption contained in such information, and any liability

whatsoever (in negligence or otherwise) therefor (including in respect of direct, indirect, consequential loss or damage) is expressly disclaimed. No information, or views given or

implied, contained herein or otherwise made available is or shall be relied upon as, a promise, warranty or representation, whether as to the past or the future and no reliance, in

whole or in part, should be placed on the fairness, accuracy, completeness or correctness of such information or views. In particular, past performance cannot be relied on as a

guide to future performance. None of the Company’s Representatives has independently verified the material in this Presentation. Nothing herein should be construed as financial,

legal, tax, accounting, actuarial or other specialist advice.

This presentation has not been approved by an authorised person in the United Kingdom and is for distribution only to (i) persons who are outside the United Kingdom, (ii) persons

who have professional experience in matters relating to investments who fall within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets

Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”); (iii) high net worth entities, and other persons to whom it may otherwise lawfully be communicated, falling

within Article 49(2)(a) to (d) of the Order or (iv) persons to whom an invitation or inducement to engage in an investment activity (within the meaning of Section 21 of the Financial

Services and Markets Act 2000) in connection with the issue or sale of any securities may otherwise lawfully be communicated or caused to be communicated (all such persons

together being referred to as “Relevant Persons”). This presentation is directed only at Relevant Persons and must not be acted on or relied on in the United Kingdom by persons

who are not Relevant Persons. The distribution of this presentation in other jurisdictions may be restricted by law and you should inform yourself about, and observe, any such

restriction.

2 June 14, 2019 – London Investor Presentation

DISCLAIMER

IMPORTANT: THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS CONFIDENTIAL AND IS TO BE USED FOR

INFORMATIONAL PURPOSES ONLY.

YOU MUST READ THE FOLLOWING BEFORE CONTINUING: Important notice

These materials have been prepared by the Company and have not been verified, approved or endorsed by any lead manager, bookrunner, arranger or underwriter retained by the

Company and no representation or warranty, express or implied, is made or given by or on behalf of them or any of its subsidiary undertakings, or any of such person's respective

directors, officers, employees, agents, affiliates or advisers, as to, the accuracy, completeness or fairness of the information or opinions contained in this presentation and no

responsibility or liability is assumed by any such persons for any such information or opinions or for any errors or omissions.

This Presentation is not a prospectus for the purposes of the European Union’s Directive 2003/71/EC, as amended or superseded.

PRIIPS Regulation / Prohibition of sales to the European Economic Area (the “EEA”) retail investors: The securities referred to herein are not intended to be offered, sold or

otherwise made available to and should not be offered, sold, or otherwise made available to any retail investors in the EEA. For these purposes, a retail investor means a person

who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU, as amended ("MiFID II"); or (ii) a customer within the meaning of a customer

within the meaning of Directive (EU) 2016/97, as amended, where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II.

Consequently no key information document required by Regulation (EU) No 1286/2014, as amended (the "PRIIPs Regulation") for offering or selling the securities referred to herein

or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the securities referred to herein or otherwise making them

available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation.

MiFID II professionals/ECPs only target market: The target market assessment in respect of the securities referred to herein has led to the conclusion that the target market of the

securities referred to herein is eligible counterparties and professional clients only (each as defined MiFID II).

This Presentation may include unpublished price sensitive information that may constitute “insider information” for the purposes of any applicable legislation and each recipient

should comply with such legislation and restrictions and take appropriate advice as to the use to which such information may be lawfully put. The Company’s Representatives do

not accept any responsibility for any violation by any person of such legal restrictions under any applicable jurisdictions.

Cautionary note regarding forward-looking statements

Statements in this Presentation describing the objectives, projections, estimates and expectations of the Company and its direct and indirect subsidiaries (collectively, the “Group”)

may be “forward-looking statements” within the meaning of applicable securities laws and regulations. “Forward-looking statements” include, without limitation, statements preceded

by, followed by or including the words “aims”, “anticipates”, “believes”, “could”, “expects”, “intends”, “may”, “targets”, “would” or other similar expressions or the negative thereof.

These views are based on a number of assumptions and are subject to various known and unknown risks, uncertainties and other facts which in some cases are beyond our

control. Such forward-looking statements are not guarantees of future performance and no assurance can be given that any future events will occur, that projections will be

achieved or that the Group’s assumptions will prove to be correct. Actual results could differ materially from those expressed, implied or projected, and the Group does not

undertake to revise any such forward-looking statements to reflect future events or circumstances.

3 June 14, 2019 – London Investor Presentation

FORWARD-LOOKING INFORMATION

This presentation contains statements that may be considered as

forward-looking statements and as such may not relate strictly to

historical or current facts.

These statements represent management’s views as of the date

they are made and Sodexo assumes no obligation to update them.

Figures have been prepared in thousands of euro and published

in millions of euro.

Alternative Performance Measures:

please refer to Appendix for definitions

4 June 14, 2019 – London Investor Presentation

AGENDA

1. Sodexo at a Glance

2. Fiscal 2018 Highlights

3. H1 Fiscal 2019 Highlights

4. A Solid Business Model

5. Transaction Overview

6. Appendices

5 June 14, 2019 – London Investor Presentation

SODEXO AT A GLANCE June 14, 2019 – London Investor Presentation

SODEXO KEY FIGURES

Sodexo at a glance

€20.4bn revenues

▪ Founded in 1966 by Pierre Bellon and still controlled by

the Bellon family

460,000 employees

19th Largest private

employer worldwide

100 million consumers

served daily

72 countries

€15bn

market Strong Investment

capitalization

Grade S&P “A-/A-1”

April 10, 2019

7 June 14, 2019 – London Investor PresentationOUR MAJOR STRENGTHS

Sodexo at a glance

A unique range of

Significant

Quality of Life Services

Independence market

particularly well aligned

potential

with evolving client demand

A robust

Undisputed

A global network financial model A strong culture

leadership in

covering that allows Sodexo and engaged

developing

72 countries to self-finance its teams

economies

development

8 June 14, 2019 – London Investor PresentationSODEXO’S DEVELOPMENT – MORE THAN 50 YEARS OF HISTORY

Sodexo at a glance

1966 1983 2005 2016 2018

Sodexo 1971 - 1978 Michel Landel Sophie Bellon Denis Machuel

IPO of Sodexo on Paris

founded by International becomes CEO, Pierre becomes becomes third

stock exchange

Pierre expansion Bellon remains Chairwoman of CEO in the

starts 1985 - 1993 Chairman of the Board the Board of Group’s history

Bellon

Service International of Directors Directors

Vouchers 2009

development:

launched Americas, Russia, Sodexo reviews its

South Africa & Asia strategic positioning

1995 1998-2001 2011-2016 2017-2019

2007-2010

Sodexo Marriot Services Puras do Brasil, Refocus on Food:

Gardner Centerplate, US

Acquisitions

US VR Brazil Brazil

Merchant, UK Score Groupe and Crèche Lenôtre, France Morris, Australia,

Partena 2001 Attitude, France Roth Bros, US Novae, AiP, The Good

Sweden Sogeres France Zehnacker, Germany MacLellan, India Eating Company

Wood Dining Services US Comfort Keepers & Motivcom, UK PHS build up:

Circles, US Inspirus US Pronep Brazil, Crèche

RKHS, India PSL, UK de France

the Good Care Group

9 June 14, 2019 – London Investor PresentationINTEGRATED QUALITY OF LIFE SERVICES OFFER

Sodexo at a glance

9 June 14, 2019 – London Investor PresentationA UNIQUE OFFERING: 3 ACTIVITIES TO IMPROVE QUALITY OF LIFE

Sodexo at a glance

On-site Services Benefits and Rewards Personal and Home

Services Services

➢ Foodservices ➢ Employee Benefits ➢ Childcare

o Resident Dining, Retail,

➢ Incentive and ➢ Home Care

Hospitality, Food

Procurement Recognition programs ➢ Concierge services

➢ Facilities Management ➢ Expense Management

o Hard FM: Technical

➢ Public Benefits

Maintenance, Asset, Energy

and Project Management. ➢ Consumer Gifting

o Soft FM: Cleaning, Security,

Front of house, Support

Services.

➢ Integrated services,

combining all of the above

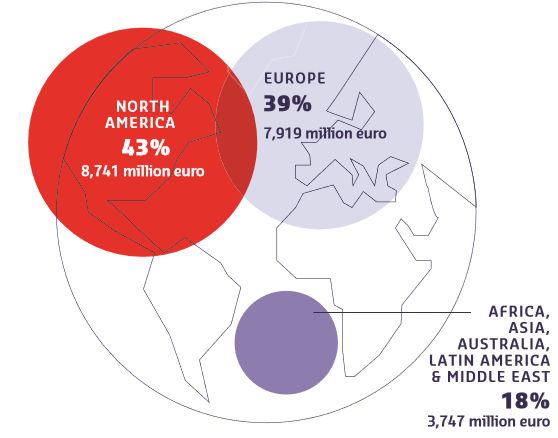

11 June 14, 2019 – London Investor PresentationFISCAL 2018 REVENUE BREAKDOWN

Sodexo at a glance

Distribution

Revenue by segment by geographic region

(1) Including Personal Home Services

11 June 14, 2019 – London Investor PresentationREGULAR AND SUSTAINED PERFORMANCE

Sodexo at a glance

25,000 Revenues (in € millions) Operating Profit (in € millions)

+4.1% CAGR over 10 years 1,200

+3.7 % CAGR over 10 years

20,000

1,000

15,000 800

600

10,000

400

5,000

200

0 0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Operating Cash flow (in € millions) 800 Net Income (in € millions)

1,200

+6.2% CAGR over 10 years +5.6% CAGR over 10 years

1,000 600

800

600 400

400

200

200

0 0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

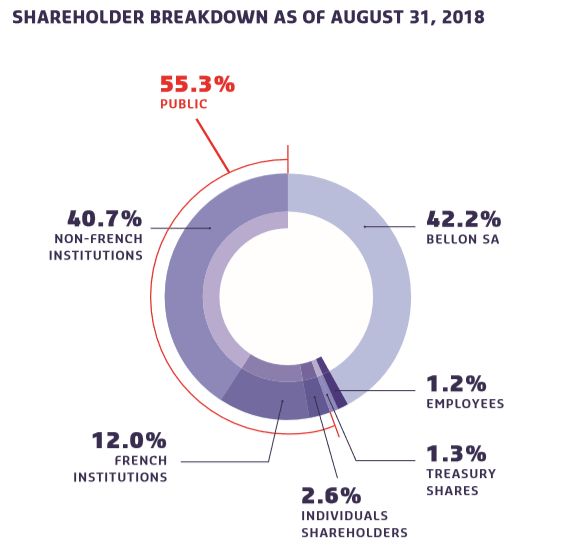

13 June 14, 2019 – London Investor PresentationSHARE OWNERSHIP

Sodexo at a glance

OF WHICH 24% USA

14 June 14, 2019 – London Investor PresentationFISCAL 2018 HIGHLIGHTS June 14, 2019 – London Investor Presentation

FY2018 IN LINE WITH REVISED GUIDANCE

Fiscal 2018 Highlights

Revised guidance FY2018 Results

Organic revenue growth Organic revenue growth

of between 1 and 1.5% at 2.0%

(excluding 53rd week impact) (excluding 53rd week impact)

Underlying operating Underlying operating

profit margin around profit margin

5.7% at 5.7%

(excluding currency effects) (excluding currency effects)

16 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsORGANIC GROWTH IN LINE WITH REVISED GUIDANCE

Fiscal 2018 Highlights

Group On Site Services

FY2018 Q4 Board days shift from Q3 to

+1.9% +3.3% Q4 in Universities in North

Excluding 53rd week Excluding America as expected

53rd week

+2.0% -1.1% +4.5% Good summer tourism

Excluding North America excl. North America in France

53rd week

Benefits & Rewards Services

+1.6%

Published FY2018 Q4

+5.1% +7.6% Brazil pick-up in H2

+2.4% +7.5% India recovery in Q4

Latin America excl. Latin America

17 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsPERFORMANCE IN THE P&L

Fiscal 2018 Highlights

CHANGE

At current Excluding

€ millions FY 2018 FY 2017 exchange rates currency effect

Revenues 20,407 20,698 -1.4% +4.4%

Underlying Operating profit 1,128 1,340 -15.8% -8.6%

Underlying Operating margin 5.5% 6.5% -100 bps -80 bps

Other Operating income and expenses (131) (151)

Operating profit 997 1,189 -16.1% -8.3%

Net financial expense (90) (105)

Effective tax rate 27.1% 31.7%

Underlying net profit group share 706 822 -14.1% -8.6%

Basic Underlying Earnings per Share 4.77 5.52 -13.6%

Group net profit 651 723 -9.9% -4.0%

Basic Earnings per Share 4.40 4.85 - 9.4%

18 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsSOLID CASH FLOW

Fiscal 2018 highlights

€ millions

FY2018 FY2017

Operating cash flow 1,140 1,076

Change in working capital1 221 120

Net capital expenditure (286) (308)

Free cash flow 1,076 887

Net acquisitions (697) (268)

Share buy-backs/ Treasury stock (300) (300)

Dividends paid to parent company shareholders (411) (359)

Other changes (including change in Financial Assets, scope and exchange rates) (316) (164)

(Increase)/decrease in net debt (648) (204)

1 Excluding change in financial assets related to the Benefits & Rewards Services activity (-€228m in Fiscal 2018 and -€134m in Fiscal 2017).

Total change in working capital as reported in consolidated accounts: in Fiscal 2018: -€7m = €221m - €228m and: in Fiscal 2017 -€14m = €120m - €134m

19 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsSTRONG CASH CONVERSION

Fiscal 2018 Highlights

165%

123% 123%

98% 93%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

20 June 14, 2019 – London Investor PresentationROBUST BALANCE SHEET AND RATIOS

Fiscal 2018 Highlights

€ millions

August 31, 2018 August 31, 2017 August 31, 2018 August 31, 2017

Non-current assets 7,944 7,416 Shareholders’ equity 3,283 3,536

Current assets

4,628 4,531 Non-controlling interests 45 34

excluding cash

Restricted cash

615 511 Non-current liabilities 4,330 3,885

Benefits & Rewards

Financial assets

427 398 Current liabilities 7,622 7,419

Benefits & Rewards

Cash 1,666 2,018

Total assets 15,280 14,874 Total liabilities & equity 15,280 14,874

Gross borrowings 3,940 3,500

Net debt 1,260 611

Operating cash totaled €2,680 million1, Gearing ratio 38% 17%

of which €1,987 million related to

Benefits and Rewards Services Net debt ratio 1.0 0.4

(net debt/EBITDA)

1 Cash – Bank overdrafts of €28m + Financial assets related to BRS activity

21 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsFINANCIALS STRICTLY UNDER CONTROL

Fiscal 2018 Highlights

Strong Free Cash Flow Solid Balance sheet Share buyback program

€1.1bn 165% 1.0 38% €300m

FREE CASH FLOW CASH CONVERSION NET DEBT RATIO GEARING

FY18 Net Acquisitions Underlying EPS Dividend maintained

€697m 2.9% €4.77 €2.75 58%

SPEND SCOPE CHANGE DIVIDEND OF UNDERLYING

NET PROFIT

22 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsFIRST HALF FISCAL 2019 HIGHLIGHTS

ORGANIC GROWTH SLIGHTLY ABOVE EXPECTATIONS

First Half Fiscal 2019 Highlights

Group On-Site Services

H1 FY2019 Continued improvement in North America

H1 FY2019

from +0.2% in Q1 to +2.4% in Q2

+2.8% Business & Administration is growing but

+3.1% still impacted by lower revenues in Govt &

+1.2% +4.1%

North America excl. North America

Agency and high last year comparative base

Organic growth in Energy & Resources

Benefits & Rewards Services

+7.3%

Published H1 FY2019

+10.1% Strong recovery in Brazil

+12.5% +8.2% Solid growth in Europe

Latin America Europe, USA, Asia

24 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsENCOURAGING EVOLUTION OF OSS GROWTH INDICATORS

First Half Fiscal 2019 Highlights

Client retention Comparable unit growth Business development

+40 bps +20 bps +70 bps

97.8%

97.4%

+2.5% 3.0%

+2.3% 2.3%

H1 2018 H1 2019 H1 2018 H1 2019 H1 2018 H1 2019

25 June 14, 2019 – London Investor PresentationUNDERLYING OPERATING PROFIT IN LINE WITH EXPECTATIONS

First Half Fiscal 2019 Highlights

Underlying Operating Profit Underlying Operating Margin

+3.3% At constant rates -20 bps

647

627 6.1% 5.9%

H1 2018 H1 2019 H1 2018 H1 2019

26 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsSOLID FINANCIALS

First Half Fiscal 2019 Highlights

CAPEX up strongly Tax rate in line

€205m 1.9% 70% 28.8% LAST YEAR REDUCED

BY EXCEPTIONNALS

CAPEX CAPEX / REVENUES OF THE INCREASE IS

IN EDUCATION AND SPORTS &

LEISURE

Net Acquisitions Solid Balance sheet

€234m 3.7% 2% – 2.5% 1.3 45%

SPEND SCOPE CHANGE ESTIMATED SCOPE CHANGE NET DEBT RATIO GEARING

FOR FY2019

27 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsPERFORMANCE IN THE P&L

First Half Fiscal 2019 Highlights

CHANGE

At current Excluding

€ millions H1 FY 2019 H1 FY 2018 exchange rates currency effect

Revenues 11,045 10,293 7.3% +6.8%

Underlying Operating profit 647 627 +3.1% +3.3%

Underlying Operating margin 5.9% 6.1% -20 bps -20 bps

Other Operating income and expenses (69) (73)

Operating profit 578 554 +4.2% +4.1%

Net financial expense (54) (44)

Effective tax rate 28.8% 25.9%

Underlying net profit group share 413 397 +4.1% +4.3%

Basic Underlying Earnings per Share 2.84 2.67 +6.2%

Group net profit 364 372 -2.3% -2.6%

Basic Earnings per Share 2.50 2.51 -0.4%

28 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsROBUST CASH FLOW

First Half Fiscal 2019 Highlights

€ millions H1 FY2019 H1 FY2018

Operating cash flow 648 650

Change in working capital1 (428) (402)

Net capital expenditure (205) (123)

Free cash flow 14 125

Net acquisitions (234) (674)

Share buy-backs/ Treasury stock 12 (49)

Dividends paid to parent company shareholders (403) (411)

Other changes (including change in Financial Assets, scope and exchange rates) 32 (43)

(Increase)/decrease in net debt (579) (1,052)

1 Excluding change in financial assets related to the Benefits and Rewards Services activity (+€55m in H1 Fiscal 2019 and €(73)m in H1 Fiscal 2018).

Total change in working capital as reported in consolidated accounts: in H1 Fiscal 2019: €(373)m = €(428)m+ €55m and in H1 Fiscal 2018 €(475)m = €(402)m+ €(73)m

29 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsRETURN TO NORMAL CAPEX LEVEL IN H1

First Half Fiscal 2019 Highlights

€ millions 1.9%

1.7%

1.6%

1.2%

160

1.0%

205

176

125

105 123

51 54 14

30

H1 2015 H1 2016 H1 2017 H1 2018 H1 2019

Free Cash Flow Capex Capex to Sales

30 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsROBUST BALANCE SHEET AND RATIOS

First Half Fiscal 2019 Highlights

€ millions FEBRUARY 28, 2019 FEBRUARY 28, 2018 FEBRUARY 28, 2019 FEBRUARY 28, 2018

Non-current assets 9,147 7,981 Shareholders’ equity 3,9992 3,343

Current assets

5,581 5,207 Non-controlling interests 46 34

excluding cash

Restricted cash

577 495 Non-current liabilities 4,615 3,956

Benefits & Rewards

Financial assets

458 465 Current liabilities 9,055 8,335

Benefits & Rewards

Cash 1,950 1,519

TOTAL ASSETS 17,714 15,668 TOTAL LIABILITIES & EQUITY 17,714 15,668

Gross borrowings 4,753 4,062

Net debt 1,839 1,663

Operating cash totaled €2,914 million1, Gearing ratio 45% 49%

of which €2,171 million related to

Benefits and Rewards Services Net debt ratio 1.3 1.1

(net debt/EBITDA)

1 Cash – Bank overdrafts of €72m + Financial assets related to BRS activity

2 The main impact of IFRS 9 concerns the reevaluation of certain financial assets. Please refer to Appendix 6 for more details

31 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsFISCAL 2019 OBJECTIVES

First Half Fiscal 2019 Highlights

▪ Growth slightly above our expectations in H1 FY19

▪ Continued growth in developing economies

but high comparable base Organic revenue growth

between 2 and 3%

▪ Improvement in North America remains challenging

▪ Some contract exits

Underlying operating

▪ Action plans delivering profit margin

▪ Productivity reinvested in growth initiatives between 5.5% and 5.7%

(excluding currency effects)

32 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsFOCUS ON GROWTH STRATEGIC AGENDA

First Half Fiscal 2019 Highlights

Corporate Services: labor productivity

Synergies benefit Consumers and Clients in France

more than compensated wage increase

▪ Clients choose Sodexo for a combined offer of On site,

Benefits & Rewards Corporate segment North America France

▪ Consumers benefit from a combined Food Services and Hourly cost +3% +2%

Meal Pass offer Hourly productivity +5% +4%

STEP tool building: 6 countries now engaged, with 20 KPIs

Building momentum by expanding offer and

Back to basics principles

bringing healthy & sustainable diets to a wider audience

▪ Unleash is building managerial capabilities to deploy STEP ▪ Opened first Crussh outlet at City, University of

Reasserting the manager role at the center of everything we do London, partnership signed for future development

Started in March ▪ Partnership with Veggie Grill, the leading US plant-

+500 completed modules so far based restaurant group to grow offer in US college

campuses

Full roll-out from May

▪ Partnership with SaladWorks, the leading US salad-

centric franchise with nearly 100 locations

33 June 14, 2019 – London Investor PresentationH1 FOCUS – HEALTH CARE IN NORTH AMERICA IMPROVING

First Half Fiscal 2019 Highlights

Contract Wins and Retention Organizational transformation Progress in H1 FY2019

▪ On track All growth KPIs improving

▪ Revamped executive leadership ▪ Business development +30bps

team focused on with14 ▪ Comparable unit growth +230bps

seasoned executives selected

▪ Client retention +240bps

for their wealth of healthcare

industry experience: +2.1% organic growth

Reestablishing operational Improvement in labor

excellence to ensure productivity:

repeatability, reliability and ▪ Average hourly revenue +5%

predictability of the outcomes

▪ Average cost of a work hour

Rebooting commercial +3.5%

expertise (Key Account, Significant improvement in

GPO Relationship, Underlying Operating Profit

Technical Sales Support)

34 June 14, 2019 – London Investor PresentationA STRONG BUSINESS MODEL

MEGA TRENDS IN OUR MARKETS

A strong business model

Environmental issues

1 Demographic Shifts

7 and scarcity of resources

2 Urbanization

8 Empowered Consumers

3 Emerging middle class

9 Disruptive Technology

4 Globalization

10 Ownership vs Right of Goods

5 Emerging markets

11 Future of Work

6 Public deficits

36 June 14, 2019 – London Investor PresentationON-SITE ADDRESSABLE MARKET OPPORTUNITIES

A strong business model

€900bn

€320bn €580bn

Total Market Food Market FM Market

Outsourcing rate: 40% 38% 42%

UK: 58%

USA: 55%

France: 44%

China: 33%

Sources: IFMA, Frost & Sullivan

37 June 14, 2019 – London Investor PresentationSIMPLIFY TO GAIN IN FOCUS AND EFFECTIVENESS

A strong business model

Optimize Redesign our “make or buy” Fit for the future

our geographic footprint approach to service

▪ Clarify where we want to be best

▪ Be fully present in up to ▪ Reinforce food DNA in class / best in cost

50 countries ▪ Redesign support functions

▪ Remain strong in integration

▪ Be active for projects to be leaner and more Site/

▪ Focus on high value Contract centric

in another 10 countries FM Services

▪ Cover the rest of the world ▪ Identify 15% savings to be

▪ Subcontract where it makes redeployed in core activities /

through partnerships sense investment for growth

and subcontracting

▪ Streamline the HQ

& Regional organizations

38 June 14, 2019 – London Investor PresentationA CASH GENERATIVE BUSINESS MODEL

A strong business model

Negative Net Assets Consistent Cash Conversion Free Cash

Excluding Goodwill Flow/Net Income

2.0 30.0%

200%

1.5 25.0% 184%

20.6%

19.7%

18.2% 18.6% 175% 165%

1.0 17.0% 17.1% 17.2% 16.4%

20.0%

15.0% 15.0% 15.4% 153%

146%

0.5 15.0% 150%

130%

0.0 10.0% 120% 123% 123%

125%

-0.5 5.0% 114% 98%

100%

-1.0 0.0% 93%

75%

-1.5 -5.0%

50%

-2.0

FY8 9 10 11 12 13 14 15 16 17 18

-10.0% FY8 9 10 11 12 13 14 15 16 17 18

BRS Net assets excluding, goodwill, customer relationships and brands in €bn

OSS Net assets excluding, goodwill, customer relationships and brands in €bn.

ROCE including goodwill

39 June 14, 2019 – London Investor PresentationBALANCED CASH ALLOCATION

A strong business model

M&A

Selective M&A:

CAPEX

▪ FCF Payback ≤ 10 years

Capex to sales at ▪ End ROCE > 15%

~ 2.5% going forward: SHAREHOLDER

RETURNS

▪ Current levels ~1.5-2%

▪ Additional IT Capex at €30 to 50m

per year

Regular Shareholder return:

▪ Centerplate ~5% ongoing

▪ Predictable dividend policy around 50%

of recurrent net income

▪ Opportunistic approach to share buybacks

40 June 14, 2019 – London Investor PresentationACQUISITION CONTRIBUTION

A strong business model

Contribution of all acquisitions*

M&A Activity in H1 FY19

to total growth

Enriching

offers in Switzerland

FY18

Strategic 2.9%

moves in Brazil

Q1FY19 H1FY19 FY19

Estimated

Consolidating

4.8% 3.7% 2 – 2.5%

positions

in the UK in France in the UK

41 June 14, 2019 – London Investor Presentation *Net of sale of activitiesA CASH GENERATIVE BUSINESS MODEL

A strong business model

Solid Debt Ratio

Net debt / EBITDA

2

0.9 1.0

1

0.6

0.5 0.5

0.4 0.4

0.3 0.3 0.3

0.2 0.2

0

FY7 8 9 10 11 12 13 14 15 16 17 18

▪ Prudent historic debt management

▪ Maintain Net Debt to EBITDA target of 1-2x pre IFRS 16

▪ Impact of IFRS 16: work in progress show impact circa €1bn of net debt* from 2020

▪ No risk on covenants

42 June 14, 2019 – London Investor Presentation *Unaudited preliminary assessment excluding concessions – IFRS 16 will only be applicable starting from FY20BREAKDOWN OF GROSS FINANCIAL DEBT: €4,753m*

A strong business model

BY CURRENCY BYBY

MATURITY (€m)

MATURITY

51% €

42% $ < 1 year 1,178

7% other

INTEREST RATE 1-6 years

1,756

21% 79%

Variable Fixed > 6 years 1,819

Blended cost of debt 2.3% at 28/02/2019

* Including commercial paper for an amount of €1,000m

NB: All data as of 28/02/2019

43 June 14, 2019 – London Investor PresentationRATING AGENCIES

A strong business model

Long term Short term Outlook

A- A-1 Stable

Key Strengths Key Risks

Leading market provider of food services, integrated Exposure to economically and geopolitically volatile countries

services, benefits and rewards, and personal home in Latin America.

services.

High revenue visibility, with recurring revenue from Exposure to fluctuations in food, commodity, and oil prices,

multiyear contracts and client retention rates above 93%. and salary inflation in emerging countries.

Strong recurring free cash flow, due to low capital intensity, Limited pricing flexibility and modest operating margins in the

structural working capital inflows, and the service-voucher onsite services business.

business’ cash float.

Exceptional liquidity and low interest costs, supported by Reliance on customer prepayments in the vouchers business.

modest financial leverage.

“The stable Outlook on Sodexo reflects our view that the Company will continue to deliver resilient operating performance in

an overall supportive economic environment. Under our base case, we expect S&P Global Ratings-adjusted funds from

operations (FFO) to debt will remain at about 40%, despite our expectation that the Company will continue acquisition

spending while maintaining shareholder remuneration levels.”

44 June 14, 2019 – London Investor PresentationTRANSACTION OVERVIEW

INDICATIVE TERMS AND CONDITIONS OF CONTEMPLATED NEW ISSUE

Transaction overview

Indicative terms and conditions of contemplated New Issue

Issuer Sodexo SA

Issuer rating A- (stable) by S&P

Issue Size GBP £250mn

Use of proceeds General corporate purpose

Issue Type Fixed, annually

Status Senior, unsecured

Tenor 9 years

Settlement date [24] June 2019

Documentation Standalone, Clean up Call 80%, 3M Par Call,

Make-whole call, COC

Law/Listing English Law, Paris Listing

Bookrunners HSBC (B&D), Santander

46 June 14, 2019 – London Investor PresentationAPPENDICES

STRONG INDEPENDENT GOVERNANCE

Sodexo at a glance

Board Audit Committee

▪ Chaired by Sophie Bellon, since 2016 Sophie Stabile, Committee Chair, Independent Director

Emmanuel Babeau, Independent Director

▪ 12 Directors, including two Employee François-Xavier Bellon

Representatives Soumitra Dutta, Independent Director

▪ Of the 10 elected Directors, 6 independent, 6 Cathy Martin, Director representing employees

women, collectively representing 3 nationalities: Nominating Committee

French, American and Indian.

Cécile Tandeau de Marsac, Committee Chair, Independent Director

▪ Luc Messier, Canadian, to be proposed to the Sophie Bellon

AGM in January 2020 as new Independent

Nathalie Bellon-Szabo

Director

Françoise Brougher, Independent Director

▪ Since January 2016, substantial renewal of

Directors and enhanced transparency Compensation Committee

Cécile Tandeau de Marsac, Committee Chair, Independent Director

Françoise Brougher, Independent Director

Philippe Besson, Director representing employees

Sophie Stabile, Independent Director

48 June 14, 2019 – London Investor PresentationAN ENGAGED COMPANY FY 18

Sodexo at a glance

14 years 69% (1) 14.6 34%(2)

As industry leader in the employee average annual hours of targeted

DJ Sustainability index engagement rate training per employee carbon reduction

80.9% 37% 60% 93.8%

employee of women on the of women on the client retention

retention rate Executive Committee Board of Directors rate

ADVOCATE FOR HEALTHY

GROW LOCALLY & INCLUSIVELY TACKLE WASTE EVERYWHERE

LIFESTYLE CHOICES

(1) 2018 employee engagement survey

(2) Absolute reduction in Scope 1, Scope 2 and Scope 3 carbon emissions, compared to a 2011 baseline

49 June 14, 2019 – London Investor PresentationREVIEW OF OPERATIONS

On-site Services

revenues

OSSON-SITE SERVICES H1 FY2019 ORGANIC GROWTH BY REGION

39 %

+3.0% of OSS

EUROPE FY18

45 % NORTH +1.2%

of OSS

FY18 AMERICA

+4.1%

+6.9%

On-site Services

Excluding North America

16 % AFRICA - ASIA - AUSTRALIA

of OSS

FY18

LATAM & MIDDLE EAST

51 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitions56%

BUSINESS & ADMINISTRATIONS – REVENUES On-site

Services

FY18

NON RESTATED ORGANIC GROWTH RESTATED ORGANIC GROWTH

€ millions North America

Organic +0.8%11

-1.3%

Net ▪ Solid growth in Corporate driven by strong comparable

growth acquisition 26%

unit sales and good wins

+1.2% Unfavorable

currency 5,645 ▪ Significant Energy & Resources project work in Q1 last

of FY18

effect year B&A

▪ US Marine Corps renewed with lower comparable

5,295 unit sales

+2.1%1

Europe 48%

▪ Corporate Services helped by solid same site sales

growth driven by cross-selling of FY18

▪ Easier comparable base in Govt & Agency in the UK B&A

▪ Slowdown in tourism in Q2 in France

+5.9%1 Africa, Asia, Australia, Latin America

& Middle East 26%

▪ Strong growth in Corporate driven by

new business and comparable unit sales of FY18

B&A

TOTAL ▪ End of construction projects in Energy & Resources

H1 FY 2018 H1 FY 2019

+2.8%1

52 June 14, 2019 – London Investor Presentation 1 Restated for inter-segment reclassification. Please refer to Appendices.

* Please refer to Appendices for Alternative Performance Measures definitions24%

HEALTH CARE & SENIORS – REVENUES On-site

Services

FY18

NON RESTATED ORGANIC GROWTH RESTATED ORGANIC GROWTH

Organic +1.3%1 North America

€ millions Favorable

Growth ▪ Solid comparable unit growth in Healthcare helped 63%

Net currency

effect by inflation pass-through and cross-selling

+5.6% acquisition

▪ Strong retention to date in Health Care but Seniors of FY18

Health Care

impacted by a significant loss in beginning of the year

2,552 & Seniors

2,359 +1.7%1 Europe

▪ Good growth in Benelux driven by last year wins 31%

and strong same site sales helped by cross selling

▪ Nordics still declining due to negative net lost of FY18

business Health Care

& Seniors

+16.9%1 Africa, Asia, Australia, Latin America 6%

& Middle East

▪ Double digit growth in Brazil, India and China of FY18

Health Care

& Seniors

TOTAL

H1 FY 2018 H1 FY 2019

+2.2%1

53 June 14, 2019 – London Investor Presentation 1 Restated for inter-segment reclassification. Please refer to Appendices

* Please refer to Appendices for Alternative Performance Measures definitions20%

EDUCATION – REVENUES On-site

Services

FY 18

ORGANIC GROWTH

€ millions Organic Favorable

Growth currency +1.4% North America

Net effect

▪ Neutral net new/lost business from last year 75%

+3.6% acquisition

▪ 1 less working day, more than compensated

2,420 by good retail activity in Universities of FY18

Education

and project work in Schools

2,228 +10.4% Europe

▪ Strong new business and same site sales

in France, particularly boosted 23%

by Yvelines Schools contract start-up in Q2

▪ Strong new business in the UK, of FY18

▪ +2 extra working days in Italy, Education

offset by 1 less working day in France in Q2

Africa, Asia, Australia, Latin America

+10.5% & Middle East 2%

▪ Strong growth in Schools in Asia

still driven by China, Singapore and India of FY18

Education

TOTAL

H1 FY 2018 H1 FY 2019

+3.6%

54 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsSLIGHT DECREASE IN OSS UOP MARGIN

First Half Fiscal 2019 highlights

Underlying Operating Profit Underlying Operating Margin

+1.2% At constant rates -30 bps

581

€ millions 562 5.7% 5.5%

H1 2018 H1 2019 H1 2018 H1 2019

+3.3% At current rates -20 bps

55 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsOSS UNDERLYING OPERATING PROFIT AND MARGIN BY SEGMENT

First Half Fiscal 2019 Financial Performance

Restated

H1 Variation

FY 2019 Constant rate

€205m +1.3% ▪ Weight of US Marine Corps renewal

Business &

Administration ▪ Timing disparity between productivity gains

3.6%* -30bps and investments to accelerate growth

€162m +5.8% ▪ Productivity gains secured,

Health Care deployment of new offers accelerating

& Seniors

6.3%* +20bps ▪ Inflation covered by price increases

€215m -2.0% ▪ Significant start-up costs for Yvelines Schools

Education ▪ Strikes, working days and churn in Schools

8.9%* -70bps ▪ In North America: inflation passed-through in Universities

56 June 14, 2019 – London Investor Presentation * % of revenueREVIEW OF OPERATIONS

Benefits & Rewards

Services revenues

BRSREVENUES BY SERVICE LINE

Benefits & Rewards Services

Employee Benefits Services diversification

€ millions € millions

Organic growth

+11.4%

10.5

Unfavorable

329 currency effect

341 Organic

growth

+5.0% Net acquisition

Unfavorable

84 currency effect 88

H1 FY 2018 H1 FY 2019 H1 FY 2018 H1 FY 2019

▪ Solid growth in Europe ▪ Strong double digit growth in Mobility & Expense

▪ Strong recovery in Brazil ▪ Fast development in Corporate Health & Wellness

▪ Issue volume €6.8bn, +8.1% Organic Growth ▪ Weak start to the year in Incentive & Recognition

58 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsREVENUES BY REGION

Benefits & Rewards Services

Latin America 44% 10.0

FY 18 BRS Europe, Asia, USA 56%

FY 18 BRS

€ millions revenues € millions revenues

Organic growth

+8.2% Net acquisition

Organic growth 10.5 Unfavorable

currency

+12.5% effect

244

Unfavorable

currency effect 229

184 186

H1 FY 2018 H1 FY 2019 H1 FY 2018 H1 FY 2019

▪ Strong recovery in Brazil thanks to growth ▪ Solid growth in Western Europe

in volumes, solid new business wins

▪ Double digit growth in Eastern and Southern Europe

and stabilization of interest rates

▪ Double digit growth in Mexico

59 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsREVENUES BY NATURE

Benefits & Rewards Services

OPERATING REVENUES FINANCIAL REVENUES

€ millions € millions

Organic growth

Net

+10.1% acquisition

Unfavorable

currency effect

17

377 394

36

Organic growth

36 +10.4% 36

Unfavorable

currency effect

H1 FY 2018 H1 FY 2019 H1 FY 2018 H1 FY 2019

▪ Solid growth in Western Europe, ▪ Interest rates stabilizing in Brazil

Double digit growth in Eastern and Southern Europe

▪ High interest rates in Turkey

▪ Strong recovery in Brazil

▪ High float resulting from exceptionally high business

volume in Romania in Q4 last year

60 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsIMPROVEMENT IN BRS UOP MARGIN EXCLUDING CURRENCY EFFECT

First Half Fiscal 2019 highlights

Underlying Operating Profit Underlying Operating Margin

+11.8% At constant rates +30 bps

€ millions 124 125 30.0% 29.1%

H1 2018 H1 2019 H1 2018 H1 2019

+1.0% At current rates -90 bps

61 June 14, 2019 – London Investor Presentation * Please refer to Appendices for Alternative Performance Measures definitionsH1 FISCAL 2019 EXCHANGE RATES

CLOSING CLOSING

AVERAGE AVERAGE RATE RATE RATE

1€ =

RATE AVERAGE RATE H1 FISCAL 19 REFERENCE CLOSING RATE 28/02/19 28/02/19

H1 FISCAL 19 H1 FISCAL 18 VS. H1 FISCAL 18 RATE FISCAL 18 AT 28/02/2019 VS. 31/08/18 VS. 28/02/18

1.145 1.195 +4.4% 1.193 1.142 +2.1% +6.5%

U.S. Dollar

0.887 0.885 -0.3% 0.884 0.858 +4.5% +2.9%

Pound Sterling

4.398 3.864 -12.1% 4.075 4.269 +13.8% -7.8%

Brazilian Real

Note: Reference rate Fiscal 2018 is the average rate for Fiscal year 2018, used for organic growth calculation .

62 June 14, 2019 – London Investor PresentationIFRS 9

▪ Prospective application from September 1,2018 with no restatement of prior periods

▪ First application net impact as of September 1, 2018 of €404m recorded in equity

▪ Main impact for Sodexo: Need to reevaluate at each balance sheet date some non-consolidated investments

at fair value that were previously accounted for at cost

FAIR VALUE HISTORICAL COST

€ million AT FEBRUARY 28, 2019 PRIOR TO IFRS 9 DIFFERENCE

Bellon SA stake 662 32 630

Other investments 85 27 58

▪ The difference in valuation of the Bellon SA stake of €630m is split between:

• €564m for the first application as of September 1, 2018

• €66m of change in fair value in the first-half

▪ Very limited impact from the new depreciation model on accounts receivables which is based on expected losses:

€21m additional depreciation recorded on September 1, 2018

▪ No impact from changes in hedge accounting

63 June 14, 2019 – London Investor PresentationALTERNATIVE PERFORMANCE MEASURE DEFINITIONS

Blended cost of debt of the prior fiscal year, calculated using the exchange rate for the prior fiscal

The blended cost of debt is calculated at period end and is the weighted year; and excluding the impact of business acquisitions and divestments,

blended of financing rates on borrowings, (including derivative financial as follows:

instruments) and cash pooling balances at period end.

▪ for businesses acquired (or gain of control) during the current period,

revenue generated since the acquisition date is excluded from the organic

Free cash flow

growth calculation;

Please refer to Cashflow position.

▪ for businesses acquired (or gain of control) during the prior fiscal year,

Growth excluding currency effect revenue generated during the current period up until the first anniversary

Change excluding currency effect calculated converting FY 2019 figures date of the acquisition is excluded;

at FY 2018 rates, except when significant for countries with hyperinflationary

economies. ▪ for businesses divested (or loss of control) during the prior fiscal year,

As a result, for Argentine Peso figures for H1 FY2019 and H1 FY 2018, have revenue generated in the comparative period of the prior fiscal year

been converted at the exchange rate of EUR 1 = ARS 44.045 vs. ARS until the divestment date is excluded;

44.302 for FY 2018. ▪ for businesses divested (or loss of control) during the current fiscal year,

Issue volume revenue generated in the period commencing 12 months before the

Issue volume corresponds to the total face value of service vouchers, divestment date up to the end of the comparative period of the prior

cards and digitally-delivered services issued by the Group fiscal year is excluded.

(Benefits and Rewards Services activity) for beneficiaries on behalf of clients. For countries with hyperinflationary economies all figures are converted at

the latest closing rate for both periods when the impact is significant.

Net debt

Net debt is defined as Group borrowing at the balance sheet date, less As a result, for the calculation of organic growth, Argentine Peso figures

operating cash. for H1 FY2019 and H1 FY 2018, have been converted at the exchange rate

of EUR 1 = ARS 44.045 vs. ARS 44.302 for FY 2018.

Organic growth Starting FY19 Venezuela is accounted for using the equity method.

Organic growth corresponds to the increase in revenue for a given period Consequently Venezuela is no longer in revenue.

(the "current period") compared to the revenue reported for the same period

64 June 14, 2019 – London Investor PresentationALTERNATIVE PERFORMANCE MEASURE DEFINITIONS

Underlying Operating profit Underlying Net profit per share

Operating profit excluding other operating income and other operating Underlying Net profit per share presents the Underlying net profit divided by

expenses. Other operating income and expenses include gains or losses the average number of shares

related to perimeter changes and on changes of post-employment benefits,

restructuring and rationalization costs, Acquisition related costs, amortization Underlying Net Profit

and impairment of client relationships and trademarks, impairment of Underlying Net profit presents a net income excluding significant unusual

goodwill and impairment of non-current assets. and/or infrequent elements. Therefore, it corresponds to the Net Income

Group share excluding Other Income and Expense and significant non-

Underlying Operating margin recurring elements in both Net Financial Expense and Income tax Expense.

The underlying operating profit margin corresponds to Underlying operating

profit divided by revenues In the H1 Fiscal 2019, the Underlying net profit excludes from

the Net Income Group share the following items and the related tax impact

Underlying Operating margin at constant rate where applicable.

The underlying operating profit margin at constant rate corresponds to

Underlying operating profit divided by revenues, calculated by converting H1

2019 figures at FY 2018 rates, except for countries with hyperinflationary

economies.

65 June 14, 2019 – London Investor PresentationAPM - FINANCIAL RATIOS DEFINITIONS & RECONCILIATION

H1 2019 H1 2018

Gross borrowings(1) – operating cash(2)

Gearing ratio 45% 49%

Shareholders’ equity and non-controlling interests

Gross borrowings(1) – operating cash(2)

Net debt ratio 1.3 1.1

Earnings before Interest, Taxes, Depreciation and Amortization (EBITDA)(3)

(1) Gross borrowings

Non-current borrowings 3,576 2,978

+ current borrowings excluding overdrafts 1,189 1,095

- derivative financial instruments recognized as assets (13) (12)

4,753 4,062

(2) Operating cash

Cash and cash equivalents 1,950 1,519

+ financial assets related to the Benefits and Rewards Services activity 1,035 960

- bank overdrafts (72) (81)

2,914 2,399

(3)Earnings before

Interest, Taxes, Operating profit 1,021 1,157

Depreciation and

+ depreciation and amortization 347 296

Amortization (EBITDA)

1,368 1,453

66 June 14, 2019 – London Investor PresentationREVENUE BREAKDOWN

REVENUES BY SEGMENT RESTATED ORGANIC ORGANIC EXTERNAL CURRENCY TOTAL

(In millions of euro) H1 FY19 H1 FY18 GROWTH GROWTH GROWTH EFFECT GROWTH

Business & Administrations 5,645 5,295 +2.8% +1.2% +6.3% -0.9% +6.6%

Health Care & Seniors 2,552 2,359 +2.2%1 +5.6% +0.4% +2.1% +8.2%

Education 2,420 2,228 +3.6% +3.6% +1.8% +3.2% +8.6%

On-site Services 10,617 9,882 +2.8% +2.8% +3.9% +0.7% +7.4%

Benefits & Rewards Services 430 413 +10.1% +10.1% +0.2% -6.3% +4.1%

Elimination -2 -2

TOTAL GROUPE 11,045 10,293 +3.1% +3.1% +3.7% +0.5% +7.3%

67 June 14, 2019 – London Investor PresentationThank you

You can also read