Sohn Conference | April 23rd 2018 - Dylan Adelman The Wharton School - SOHN - Conference Foundation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Sohn Conference | April 23rd 2018

Dylan Adelman

The Wharton School

dylana@wharton.upenn.edu

Introduction Dylan Adelman

dylana@wharton.upenn.edu

Because they wouldn’t let me pitch Zedge.

• Vostok New Ventures (VNV) is an investment holding company

based in Sweden and listed on the Stockholm Stock Exchange.

• VNV has a net asset value of $880M, consisting of a 13.2% stake

in the Russian classifieds website Avito (62.2% of NAV), as well

as other emerging markets companies (31.6% of NAV) and cash.

• VNV is the best way to invest in Avito. Avito dominates the

Russian classifieds market, and is in early stages of monetizing.

Avito can easily grow earnings at 20%+ for the next decade.

• Because of limited visibility into Avito’s financials and VNV’s

NAV discount, Avito is available at just 23.8x 2018E earnings.

• The result: VNV has an expected 10-year IRR of 20%.

2

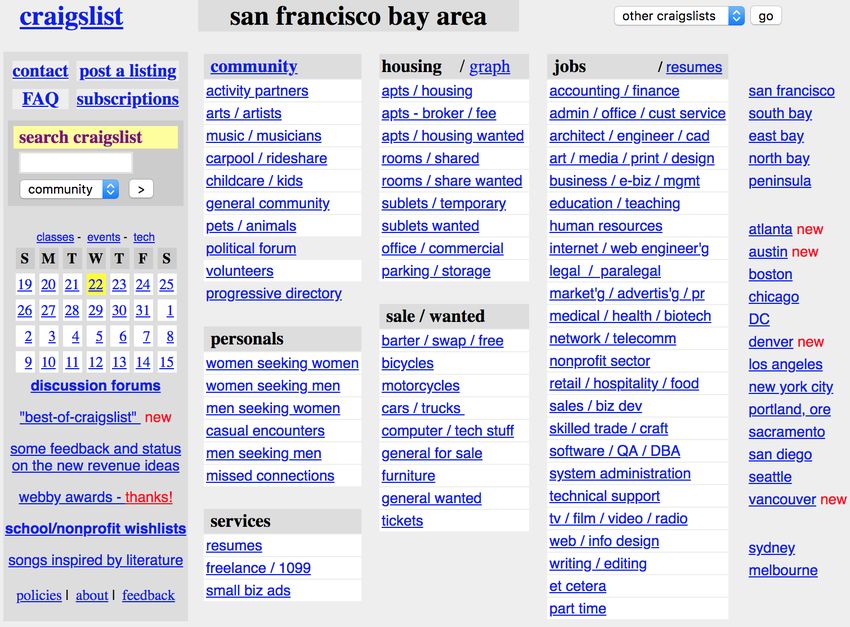

Craigslist Dylan Adelman

dylana@wharton.upenn.edu

Can you spot the difference?

Craigslist in April 2000

?

3

Craigslist Dylan Adelman

dylana@wharton.upenn.edu

Can you spot the difference?

Craigslist in April 2000 Craigslist in April 2018

4

“Every few years, someone in Silicon Valley looks at Craigslist and thinks he or she can do better. All these efforts basically come to naught […] Craigslist pulls in more than $500 million in profit a year without trying.” - Forbes, May 2017

Classifieds Dylan Adelman

dylana@wharton.upenn.edu

The opposite of Bruce Greenwald’s toaster.

What makes online classifieds such a great business model?

The network effect among buyers and sellers Minimal capex requirements at scale because

1 gives a large advantage to the first mover and acquiring new users and raising prices is not

4

ensures that the market is winner-take-all. contingent on reinvestment rates. The result

is a near-100% dividend payout once mature.

The combination of an unregulated natural

2 monopoly and myriad pricing levers results Professional sellers create subscription-like

5

in substantial pricing power over time. recurring revenues via value-added services.

Asset-light business model because no assets Recession-resistant business model that meets

3 are required to deliver the services and there 6 the basic need for location-based buying and

is no inventory. Ultra-high return on assets. selling by both individuals and businesses.

Online classifieds are one of the best business models in the world. 6

Classifieds Dylan Adelman

dylana@wharton.upenn.edu

There must be a good election joke here…

7

Avito Dylan Adelman

dylana@wharton.upenn.edu

The best combo of Russia and Classifieds since Trump Tower.

• Founded in 2007, Avito is the third-largest classifieds site in the world after Avito vs. #2 Competitor

Craigslist and 58.com (China). Avito has 70%+ market share in all verticals, in Russia (Page Views)

and is arguably the most dominant classifieds website in the world.

General: 70.1x

• Avito is highly under-monetized. Per-user revenue is by far the lowest for

any major classifieds market, as Avito did not begin monetizing listings until

2012 (versus early 2000s for international peers). Most revenue comes from Services: 71.1x

listing fees and value-added services in a few verticals like jobs and autos.

• In 2017, Avito earned revenue of $269M (32% increase) with an operating Real Estate: 21.6x

margin of 53%. Unique sellers increased by 9% to 47M (⅓ of all Russians).

• Avito’s earnings are a factor of Per-User Revenue × Users × Margins.

Sustained increases in each of these will drive up Avito’s valuation. Autos: 2.2x

How will Avito grow Per-User Revenue × Users × Margins over time? 8Per-User Revenue Dylan Adelman

dylana@wharton.upenn.edu

Even Craigslist is better monetized than this.

• Because Avito was not founded until 2007, it is far earlier Classifieds Revenue/Capita by Country

in the monetization curve than international peers. Avito’s (PPP-Adjusted USD)

current monetization roughly matches peer levels in 2008.

15.9

• Determining revenue/capita potential is difficult because

most peer sites control specific verticals. Very few are the 15.2

dominant classifieds site across every vertical like Avito. In

this sense, Avito is comparable to nationwide aggregates. 12.1

• Peer comparisons adjust for income levels because most 8.7

comparables are in higher-income countries than Russia.

6.3

1.9

How can Avito reach the per-user revenue of more mature classifieds markets? 9“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business.” – Warren Buffett

Per-User Revenue Dylan Adelman

dylana@wharton.upenn.edu

Monetizing like Mugabe.

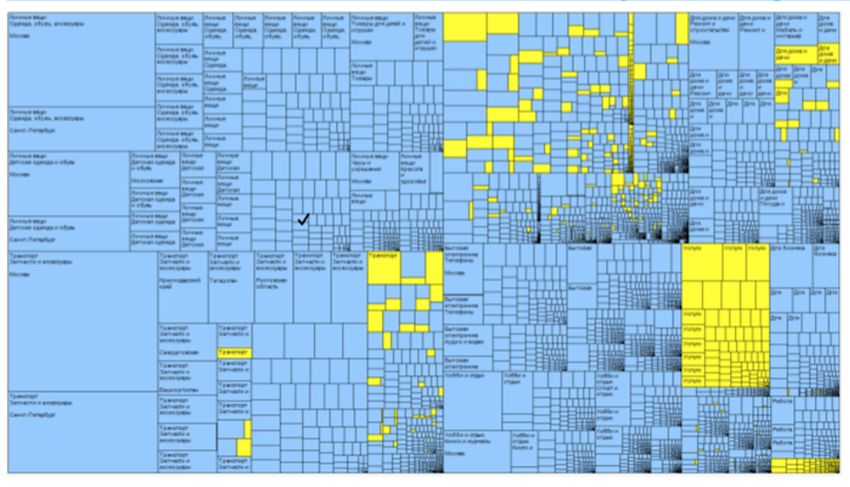

Avito has an enormous runway for monetization:

1

Roll out listing fees to more categories and regions.

Fewer than 5% of categories have listing fees.

2

Sell professional value-added services (VAS) to

businesses that list multiple products on Avito.

3

Increased third-party advertising, such as the

partnership with Yandex announced in March.

4 Further monetize verticals. Avito’s dominant real

estate subsidiary, Domofond, earns zero revenue. Categories/Regions with listing fees

Categories/Regions without listing fees

5 Increase prices. What alternative do sellers have?

[Data from October 2015]

Avito did not begin monetizing select verticals until 2012, and is 10 years behind its peers on the

monetization curve. Over the next decade, Avito will converge with peers’ 2017 per-user revenue. 11Per-User Revenue Dylan Adelman

dylana@wharton.upenn.edu

Pricing power like Valeant, but without the congressional hearings.

• France has the lowest PPP-adjusted revenue/capita classifieds services Avito Revenue/Capita

among larger developed countries (after Russia). Using France in 2017 (USD) 2017 à 2027E

as a benchmark for the revenue/capita that Avito can earn in a decade, 6.3

Avito will achieve at least 4.9% annual per-user revenue growth.

• This does not include GDP growth, which affects the number of items

sold per user (quantity, not price). Based on OECD projections for the

next decade, Russian GDP growth will be a 2.6% annual tailwind.

• Growth will remain strong in a decade. In 2017, France’s classifieds 1.9

site, Leboncoin, achieved 20% revenue growth with 58% margins, and

is guiding for 15-20% long-term growth. If peers that are more than

a decade further into monetization can still grow revenue at 20%

per year, then estimating 7.5% for Avito is highly conservative.

2018 is just the start. Per-user revenue growth will be at least a 7.5% annual tailwind. 12User Growth Dylan Adelman

dylana@wharton.upenn.edu

How is 10% of the US population still not connected to the internet?

Buyers Sellers

• One proxy is site visits over time. According to • One proxy is listings over time. VNV reported

SimilarWeb, site visits increased by 9% in 2017. that Avito’s listings increased by 18% in 2017.

• Increased internet penetration is also a driver of • Avito’s total number of unique sellers (“listers”)

new buyers. Only 70% of Russians are internet increased by 9% to 47M (that is 1 in 3 Russians).

users, versus 90% in the US/EU. New internet

users in Russia will be a 2-3% annual tailwind. • As a proxy of professional sellers’ advertising

budgets, PwC estimates that Russian online ad

• Russia’s online spending will grow at 18% spending will grow at 21% through 2021.

annually over the next five years (Russian

Association of Communication Agencies). • As of March 2018, Yandex (the Russian version

of Google) is now directing advertisers to Avito.

While precision is difficult, user growth will be at least a 6.0% annual tailwind. 13Margin Growth Dylan Adelman

dylana@wharton.upenn.edu

Is the business quality of online classifieds apparent yet?

• Classifieds businesses naturally expand margins Peer EBITDA Margins (2016)

as they mature due to lower spending on R&D

and marketing, as well as market consolidation. 90.0%

76.4%

• The highest-margin classifieds are those that are

either in control of a massive market (Craigslist 64.2%

in the US) or in control of a highly monetizable

vertical (Rightmove with UK real estate). 60.3%

56.5%

• Avito controls a market size similar to Craigslist

with multiple verticals similar to Rightmove. 52.9%

“We believe that Avito will be able to reach best in 45.0%

class margins of at least 70%.” – VNV, 12/2017 42.2%

How can Avito achieve this margin expansion? 14Margin Growth Dylan Adelman

dylana@wharton.upenn.edu

An undisclosed subsidiary?

“Domofond is still in a development phase and does not generate any significant revenues.” – VNV, 12/2017

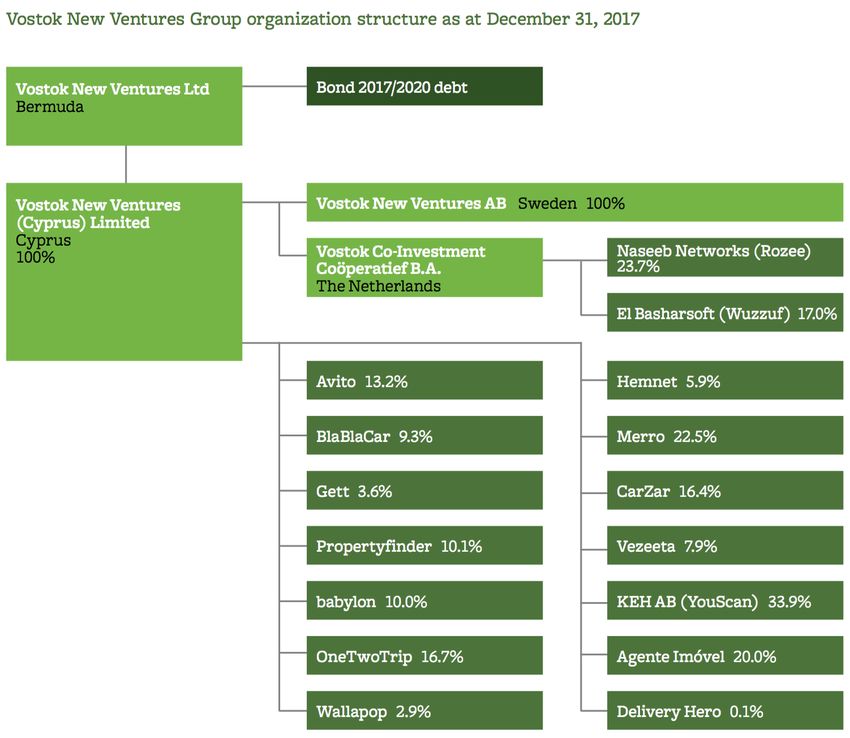

VNV’s Ownership Structure Avito’s Subsidiaries

Acquiring Avito’s financials from the Swedish Companies Registration

Office (Bolagsverket) is difficult, and even these do not fully break out

Domofond. But, they reveal that Domofond is a separate legal entity.

Domofond is likely to be

weighing down Avito’s

margins, but VNV does

not break out its impact.

Domofond is a separate entity, so it must file an annual report with the Swedish government. 15Margin Growth Dylan Adelman

dylana@wharton.upenn.edu

At least it’s not Chewco or Philidor.

Domofond

Domofond offers Avito a clear path for margin expansion:

• Because Domofond is still in the investment stage, it creates

53% of Avito’s product development costs, but no revenues. [ – break – ]

• Domofond produces 11% of Avito’s total expenses. Without

these temporary costs, Avito’s margins would be 5.9% higher.1

Avito

• As Domofond matures and begins to monetize, its margins

will improve and will eventually match (if not exceed) Avito

overall. This is not too aspirational for a real estate vertical.

• Once Domofond begins to follow Avito’s vertical playbook on

monetization, the new revenues and margin improvement will

drive Avito’s overall margins to 70% without any other changes. [Domofond financials in SEK thousands | Avito financials in RUB millions]

1112M SEK = 879B RUB à 879/14968 = 5.9% increase in margins

16Margin Growth Dylan Adelman

dylana@wharton.upenn.edu

More margin expansion than a sell-side report on Tesla.

A few key drivers of margin expansion for Avito: 2017 2027E

COGS 10% 7%

• Decreased sales and marketing (S&M) spending as 6%

Avito’s usage further increases among professional 4%

sellers, and as competitors (i.e. Yandex) capitulate. S&M 19%

9%

• Domofond’s transition out of the investment stage 11%

R&D

will lower product development (R&D) expenses.

G&A 13%

• Lower G&A as a percentage of sales because back

office expenses like labor will increase at a slower 74%

pace once Avito becomes more mature.

Operating 47%

Avito will approach 74% operating margins by 2027. Income

Margin expansion will be a 4.6% annual tailwind.

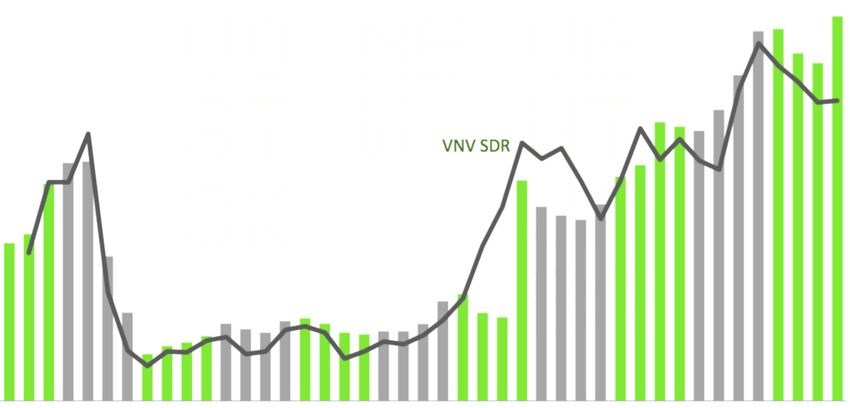

17NAV Discount Dylan Adelman

dylana@wharton.upenn.edu

Somewhere between Murmansk Trawler Fleet and PSH.

Despite its growth prospects, Avito is remarkably cheap when purchased through VNV:

• With a $740M market cap and $880M NAV, VNV trades at a 16% discount to reported NAV. This

is the largest discount to NAV in the last decade. VNV historically trades in line or above NAV, and the

discount is the result of a recent adjustment in the carrying value of Avito (+32% in December 2017).

• After netting out other investments ($300M), VNV’s 13.2% stake in Avito is priced at $440M.

This implies an overall price for Avito of $3.33B. Avito’s 2018E earning are ~$140M.

VNV NAV/Share (Bar)

• Through VNV, Avito is available at only 23.8x 2018E earnings (4.2% yield).

VNV Price/Share (Line)

1810-Year IRR Dylan Adelman

dylana@wharton.upenn.edu

It can’t be worse than shorting PayPal, right?

Revenue/User GDP Growth New Users Margin Growth Earnings Yield Avito

4.9% + 2.6% + 6.0% + 4.6% + 4.2% = 22.3%

This assumes zero

10-Year Average Weight IRR multiple expansion

Avito 88% × 22.3%

= 10-Year IRR = ~20%

Other Investments 12% × 0%

Given that “other investments” have double digit

returns and VNV is reasonably skilled at capital

allocation (proof: Avito), this is an extreme lowball.

Vostok New Ventures will earn a 20% average annual return over the next decade. 19Rightmove Dylan Adelman

dylana@wharton.upenn.edu

A useful parallel for Avito in 2018.

• Rightmove is a UK real estate classifieds site, founded in 2000. After almost

a decade of rapid growth, Rightmove appeared to slow down by late 2007.

• Over the next decade, investors earned 28% per year (on average), including 12/2017

dividends. This was from a base price that was not reached again until 2010. £44.89

“The analogy with Rightmove in 2007 […] still holds very well.

Rightmove tripled revenues during the 10 years following 2007

whilst maintaining world class margins. We believe Avito is on

the same route, possibly even at a faster rate.” – VNV, 12/2017

• Rightmove is still posting impressively strong numbers:

• 14% EPS growth in 2017 with a 30% payout

• 85% of EPS growth from monetization 12/2007 28% 10-year IRR

• Trading at 25.5x 2018E earnings £4.40

20“No formula in finance tells you that the moat is

28 feet wide and 16 feet deep. That’s what drives

the academics crazy. They can compute standard

deviations and betas, but they can’t understand

moats.” – Warren BuffettSpecial Thanks

The Sohn Conference Foundation

Global Platinum Securities

Matt JacksonSohn Conference | April 23rd 2018

Dylan Adelman

The Wharton School

dylana@wharton.upenn.eduYou can also read