The Forestry Market - Forestry investment UK regional markets Carbon offsetting Woodland creation - Savills

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UK Rural - April 2021

S P OT L I G H T

The Forestry

Savills Research

Market

Forestry investment UK regional markets Carbon offsetting Woodland creation

Forestry investment

50%

rise in hectares traded

£205.5m 20,372

UK forestry investment in the Gross area of hectares traded

in the 2020 forest year 2020 forest year in the 2020 forest year

Breaking convention

Forestry now sits at the apex of both climate and land

use policy and continues to attract new interest

This Spotlight on Forestry tracks UK forest not uncommon for forests to sell in excess of existing forests, these sites have few of the

investments during the 2020 forest year 30-70% over the asking price, which ultimately constraints levied on new planting sites, and

(1 October 2019 – 30 September 2020) represents the scarcity value of tradeable therefore offer good opportunities to investors

and shows that interest in the UK forestry forest assets. Asset supply constraints are willing to improve assets over a longer

investment market continues to follow its being matched with an aggressive appetite for timeframe. This is demonstrated by increasing

long-term upward movement. Last year’s managed carbon and timber resources, with prices for secondary or even tertiary forest

Spotlight reported evidence of new buyers owners wanting to report on sustainability property, with the expectation that through

entering the UK forestry market and this metrics of forestry performance in climate focusing on the better soils within a property,

trend has intensified as climate concerns and biodiversity regulation, especially when drainage, species change and improved growth

continue to dominate investment landscapes. considering afforestation projects. The one performance the second rotation over a

The traditional market drivers of capital asset note of warning is that competition is driving potentially smaller net area is likely to

appreciation and rising timber prices have demand in excess of market realities. significantly outperform the first rotation.

not changed, but evolving policy and action The trend towards off-market sales seen For years forest management was about

around the sustainability agenda has shone during the 2020 forest year suggests that the restricting expenditure in a no income

a light on forestry as not only a financial privacy of buyers and sellers and managing environment, but management is now rewarded

investment, but also an environmental one. speculative interest remain concerns. by strong timber prices and capital values, so

This has diversified the investment pool, but additional money spent on scrub clearance,

also focused demand for lesser quality assets for ACTIVE ASSET MANAGEMENT respacing, infill planting, enhanced drainage, etc

re-purposing, and in the more remote areas. As a result of the increasing competition for is not wasted. Improvements in management

During the 2020 forest year the value of the property, there is clear interest in properties don’t just benefit future timber revenues

UK forestry investment market hit a record that were traditionally less popular mainly due though. Microsoft, for example, in its recent

of over £205 million. The main difficulty to location and the expectation of poorer carbon markets report included carbon storage

is predicting where true forestry values lie commercial returns. While never destined to from enhanced forest management projects as

against the market’s return aspirations. It is produce the same output as prime property, as part of its ambitious net positive strategy.

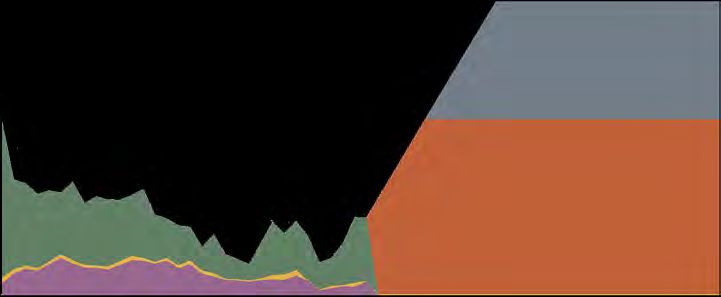

FORESTRY forest hectares sold, however,

Total market area and total market value during 2020, 20,732 hectares

INVESTMENT were transacted, representing a

ANALYSIS rise of 50% compared to the 2019

250 25 (figure 1). Although the number of

The total value of the UK forestry Market value

hectares sold increased during

Value of market transactions (£ millions)

investment market increased from Market area 2020, the demand for forestry still

Market gross area (thousand ha)

200 20

£119 million in 2019, to just over considerably exceeds supply.

£205.5 million. During 2020,

20,372 hectares were transacted AVERAGE FOREST VALUES

150 15

representing a 73% increase in Analysis of our 2020 database

the value of forestry sold and, shows the average gross forest

according to our research, exceeds 100 10 value increased by 17% to just over

the record in 2015 by just short of £11,600 per hectare. All forests

£60 million, when forest sales were have unproductive areas such as

bolstered by a large portfolio sale 50 5 tracks, rivers, lochs, etc, so it is

(figure 1). important to consider the value of

This report focuses on data the productive area. The average

from all mainstream forestry 0 0 price per net productive hectare

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

transactions and, where we are rose by 11% to £15,000. This

aware, off-market or private reflects all sales over 20 hectares

figure 1 Source Savills Research

transactions. While we make every and covers a wide variation in the

effort to record all forest sales, type, location and size of forest

through our market knowledge have become more widespread suggests the value of sales may be sold. However, closer analysis of of

and networks, it is becoming with our analysis showing private as high as £225 million for 2020. the larger commercial forest sales

increasingly clear that the market sales represented 32% of all sales The remarkable increase in the (>150ha) highlights the strength of

is becoming harder to determine during 2020, compared to 11% in overall value of sales can be partly the upper end of the investment

as some sales are not easily 2019 and 7% in 2017. As a result, attributed to a rise in the total area market, with average gross values

identified or verified through although our database reports of forestry transacted across the at £13,100 per hectare and the

available records. total sales of just over £205.5 UK. In recent years, our analysis average net productive hectare

In recent years, off-market sales million, anecdotal evidence found a relatively even number of rising to £18,250.

savills.com/research 2

Regional market

Although the number of hectares sold increased

during the 2020 forest year, the demand for

forestry still considerably exceeds supply

Higher average yields from younger trees

40%

35%

Percentage of spruce trees

30%

25%

20%

15%

10%

5%

0%

Low yield Medium yield High yield Very high yield

class class class class

Tree age 0-19 years Tree age 20+ years

(second rotation) (first rotation)

figure 2 Source Savills Research

Regional performance

Higher demand for forestry is driving interest in previously unconsidered locations

Average forest values are diverse and factors closely to asset value. Analysis of a forestry benefit from better growing conditions

such as location, accessibility, tree species, portfolio comprising first and second rotation and access to timber markets. However,

average age and timber volume continue to spruce crops indicated that younger timber, during the 2020 harvest year, North

influence the price. However, as demand for less than 20 years old and therefore nearly all Scotland achieved a price of over £16,500

forestry intensifies we are seeing growing early second rotation, recorded a higher average per net productive hectare, which is a

interest in areas that were considered less yield class of 17, compared to a medium yield regional high. North Scotland also reported

attractive in the past, resulting in average class of 13 for timber over 20 years old, which the second largest market share across

forest value growth being strongest across was nearly all first rotation. Furthermore, our Scotland, England and Wales at 28% with

North and Central Scotland. research indicated that 53% of the younger 5,678 hectares transacted.

The growing interest in previously less timber was rated high to very high yield class,

attractive forest properties is also driven by compared to 22% of timber over 20 years CENTRAL SCOTLAND

a realisation that through improvements in (figure 2). This is in part why we are seeing The area enjoyed a significant 24% rise

management techniques, tree stocks, genetics, very strong values paid for younger age profile in the average net productive value to

and precision breeding, the performance of woodlands, with valuations capturing this £16,555 per hectare. Average prices here

forests can be boosted. Improved techniques heightened performance as well as other have been gradually rising and for a second

for tree establishment provide the basis for benefits, such as the smoothed income profile consecutive year recorded the highest number

better performing and faster growing forests. associated with multi-age forests. of forest hectares sold across Scotland,

Foresters are also witnessing longer growing England and Wales.

seasons due to milder UK autumns. NORTH SCOTLAND

Monitoring yield helps forest managers In North Scotland the average price of SOUTH SCOTLAND

understand performance patterns in terms of £8,513 per net productive hectare continues During the 2020 forest year, the average value

growth and productivity, which should link to be lower than more southerly regions that of net productive forest rose by 3% to £15,100

per hectare. This follows a 33% rise in the 2019

forest year and the 2020 data reflects the range

Regional market share and values of prices and properties sold across the region.

The number of hectares transacted reduced

by almost 500 hectares when compared to the

Region Average £ per Number of Market 2019 forest year.

productive hectares share

hectare sold %

ENGLAND AND WALES

● North Scotland £8,513 5678 28% England and Wales continue to benefit

from the highest prices paid per hectare of

● Central Scotland £16,555 7210 35% net productive forest. This year’s analysis

shows a 4% rise in the average value to

● South Scotland £15,100 4000 20%

£17,131. The number of hectares sold in

● England & Wales £17,131 3484 17% England and Wales increased by over 2,000

hectares during the 2020 forest year compared

figure 3 Source Savills Research to the 2019 year.

3

Carbon offsetting

Interest in the UK woodland carbon market has grown

rapidly over recent years, presenting a new potential

income stream for landowners

IMPACT OF CARBON INCOME ON

WOODLAND CREATION MODELS

Model assumptions = 50ha over 80 years

Amenity: England broadleaf

n 100% mixed broadleaf

n Woodland creation and maintenance

grant income

n Carbon price = £25/tonne

n Timber income from selling firewood

= £2,000/year for 40 years

Scotland: mixed

n 50% broadleaf, 50% conifer

n 2 x conifer rotations

n Woodland creation and maintenance

grant income

n Carbon price (from the broadleaf)

= £25/tonne

n Timber yield (from conifer) = £500 tonne/

ha for fell, 40 tonne/ha for thin

n Timber price (from conifer) = £80/tonne

Carbon as a disruptor

for fell, £30/tonne for thin

n Timber income from selling firewood

= £1,000/year for 40 years

Companies concerned about their climate impact are Commercial: Scotland conifer

increasingly looking at woodland carbon offsetting n 100% conifer

The reality of the climate crisis has sparked a risk. The growing demand for accountability, n 2 x conifer rotations

race to net zero emissions across all sectors combined with increasing regulatory baselines n Woodland creation and maintenance

grant income

within the UK. Companies and organisations and the threat of carbon taxes, means that

n No carbon income

seeking to reach zero carbon impact start by companies are starting to address their carbon n Timber yield (from conifer) = £500 tonne/

reducing their procedural emissions and then emissions. This has resulted in a surge of ha for fell, 40 tonne/ha for thin

look to offsetting for any residual emissions. interest in woodland carbon offsetting. n Timber price (from conifer) = £80/tonne

Tree planting offers a nature-based solution for fell, £30/tonne for thin

to carbon offsetting. As trees grow, they CREATING A CARBON OFFSET

sequester carbon through photosynthesis. In order to sell woodland carbon offsets,

This sequestration can be quantified and there are a number of key criteria that Estimated income breakdown over 80 years:

reported as an internal offset or “inset” for need to be satisfied. Firstly, the woodland

land managers, or it can be externally verified creation needs to be verified as a legitimate

and sold to the voluntary carbon market as carbon sequestering project. Within the

an offset. UK, the Woodland Carbon Code is the most

Interest in the UK woodland carbon commonly used scheme to do this. Secondly,

market has grown rapidly over recent years, it is essential that the woodland can prove

presenting a new potential income stream for additionality. This means that the carbon

landowners and generating demand for bare would not have been sequestered in the Amenity: Mixed: conifer Commercial:

broadleaf and broadleaf conifer

planting land. absence of a market for offset credits.

In other words, carbon income needs to be ● Woodland grants ● Woodland carbon sales

DEMAND FOR WOODLAND CARBON a key driver for planting the trees – the project ● Woodland timber sales

There are a number of factors behind the cannot be financially viable without carbon

increasing demand for woodland carbon income. This means deriving carbon income £ Conifer Mixed Broadleaf

offsets. The legally binding net zero emissions from commercial forestry can be difficult

Total

target of 2050 for England and 2045 for to justify. The trees have to be planted on £3,882,210 £2,328,560 £673,535

income

Scotland has put pressure on policymakers new land, and the land manager cannot be

and business to take their carbon impact under an obligation to plant – meaning land Total

£375,100 £457,912 £493,802

impact seriously. This ambition is brought managers cannot sell the carbon from trees costs

to reality through Climate Related Financial grown through restocking (for example, under Net

Disclosure, which is increasingly becoming the conditions of a felling licence). Trees £3,507,110 £1,870,648 £179,733

income

mandatory for all large companies and sequester carbon at different rates depending

financial institutions in the UK, requiring on age and species, therefore woodland carbon (all numbers are based upon theoretical models and assumptions)

them to be transparent about their climate credits can take time to generate. figure 4 Source Savills Research

savills.com/research 4

Woodland carbon

£20.37/t

The average price of carbon from three rounds of England’s

15x

The amount of times the voluntary carbon market needs

Woodland Carbon Guarantee over 2020-21 is £20.37/tonne to scale by 2030 in order to reach net zero in time

Investment potentials Comparative income streams over time

We look at carbon sequestration versus (illustrative – not to scale)

returns from commercially driven forestry

Woodland creation and maintenance grant income

The growing interest in woodland timber remain far more substantial.

Carbon offsetting income

carbon for offsetting and ESG High timber prices and high yields

Timber income

objectives makes forestry an have resulted in exponential value

increasingly attractive investment. growth for commercially driven

Income (£)

Savills Rural Research modelled forestry. It is important to assess

the impact of carbon income on a the relative price of the assets at

variety of woodland creation models maturity, rather than focusing solely

to understand the extent to which on chasing the earlier income streams

carbon is changing forestry market from carbon, which may lead to

dynamics. Our models (figure 4) investment in a lower yielding model.

demonstrate that growing trees for While forestry is not solely about Time

commercial carbon (offsetting) and carbon, the emergence of carbon

growing trees for commercial timber sequestration as a key incentive for figure 5 Source Savills Research

are very different projects in terms of planting is undeniable. As a disruptor

income potential, timescales around carbon boosts a strengthening

return on investment and scheme forestry market, increasing demand Illustrative capital appreciation of each model

design. The need to prove additionality for bare land with planting potential,

means that commercial carbon and and making forestry an attractive Conifer £25000/ha

commercial forestry schemes are asset for its “soft” insetting power. Mixed

increasingly incompatible, as deriving For certain planting schemes such Broadleaf

carbon income from financially viable as lower yielding broadleaf amenity £12000/ha

Capital value (£)

timber production makes additionality woodland, carbon income is becoming £8000/ha

hard to justify. All growing trees a key driver. However, history

sequester carbon, however not all reminds us that focusing on single

£5000/ha £5000/ha

woodland creation models can sell issue drivers has led to regrettable

carbon offsets. Carbon sequestered mistakes in woodland design, such as

can be used as an internal “inset” on monoculture plantations when the

a carbon balance sheet. Figures 5 and sole aim was mitigating income tax. £4000/ha Dip in value is because the impact of traded carbon units on

6 show that although carbon income It is crucial that investors and land the capital valuation of a woodland asset remains uncertain

is an incentive to planting and will managers understand all their drivers Time (80 years)

ease cash flow for certain schemes, at for planting and adopt a long-term,

current carbon prices, returns from balanced approach. figure 6 Source Savills Research

CARBON VALUES

£160

Income from carbon offsets is not linear, as sequestration tCO2e

rates vary depending on age and species of the tree.

Carbon prices within the voluntary offsetting market vary

£75

greatly, from £3/tCO2e to £30/tCO2e. The average price tCO2e

of the mandatory EU Emissions Trading Scheme for April

2020–2021 was £24.41/tCO2e. Research has suggested £50

tCO2e

that carbon should be priced between £40-£100/tCO2e in

order to accurately represent the cost of reaching net zero

by 2050 (2045 for Scotland). For many companies looking 2020 2030 2050

to purchase offsets, the UK provides high quality, verifiable

“charismatic carbon”. Companies value the additional Source LSE, Grantham Institute

benefits UK tree planting can provide such as public

access, biodiversity uplift and species protection. If carbon A report from LSE and

prices rise in line with research predictions, and regulatory Grantham Institute

baselines continue to increase, carbon will endure and grow suggested that shadow

as a dominant force for change within the forestry market, carbon prices consistent

blurring the lines between land use change and viable with net zero would start

investment. However, even with rapid carbon price growth, at £50/tCO2e in 2020,

the high returns from timber are likely to remain the most reaching £75/tCO2e in 2030

substantial income driver for forestry investment. and £160/tCO2e in 2050.

5Woodland creation

100

students graduate from higher

900k ha

of woodland to be created by 2050

education forestry courses each year to meet UK net zero recommendations

Future of forestry

With policy drivers and private market demand promoting woodland creation,

we discuss what it will take to significantly increase the nation’s tree planting

The UK government has committed to use (normally farmland) is the core challenge. before ambitious tree planting targets are

ambitious tree planting, promising to reach Land managers need to be committed to long- taken into account. The Institute explained

an annual target of 30,000 hectares of new term change, which means that most tenanted that “the necessary scale of change must be

woodland creation by the end of its term, land is likely to be excluded. A number of reflected in professional delivery capacity

bringing goals in line with the Committee grant schemes exist to incentivise woodland at all levels and in all settings. It will also be

on Climate Change (CCC) net zero creation, and the rising value of forestry crucial to maintain standards to avoid damage

recommendations. The most recent ratified should be a motivator in its own right. to the environment and reputational risk to

UK figures suggest 13,500 hectares were Land use change to forestry is a complex the sector.”

planted in the 12 months to March 2020, with process and can require environmental There are calls to make forestry and

an estimated similar, albeit slightly higher impact assessments in extreme cases. The environmental studies more mainstream

figure to March 2021. This puts current process is also time-consuming and this has at school level, and build on degree

planting rates at 45% of what is required. But, to be factored into appraisals. As a result, the apprenticeships as an opportunity to increase

exactly what is needed if we are to have any process of developing a scheme can take six capacity in the sector and promote diversity

hope of achieving these goals? months to two years depending on scale, and in the workforce. The need for upscaling and

often the net plantable area is only 40% to upskilling is also a great opportunity to forge

LAND AVAILABILITY 60% of the overall area after deductions for links with the wider land use community and

At the highest level, land availability is the safeguarding. draw in career changers from other sectors,

most significant factor for new woodland especially post-Covid-19.

creation. Not only does land need to be LABOUR/SKILLS REQUIREMENTS Approximately 100 students graduate

available, but it also needs to be suitable for Rapid upscaling is needed if the UK is to meet from higher education forestry courses each

woodland development. its tree planting targets. A crucial part of that year across the UK. Work is being done by

Excluding valuable agricultural land upscaling revolves around the labour and devolved governments to develop plans to

and land under protected designations, skills needed to advise, plant and manage new attract talent to the sector, improve skills

the Forestry Commission has identified woodland creation. A Scottish study (2019) and technical knowledge, support education

approximately 3.2 million hectares in England suggested that in order to meet Scotland’s providers and employers.

as favourable for tree planting. A similar share of the 30,000 hectare commitment, Funding from schemes such as the Green

project commissioned by the Scottish it needed an uplift of 29% of the workforce Recovery Challenge Fund and Scotland’s

government estimated there were 2.7 million over 10 years. Estimates based on the Scottish Kickstart programme may help enable

hectares of land with the “most likely potential research and the planting targets indicate the increased employment in the sector. However,

for woodland expansion” across Scotland. shortfall could be as many as 12,500 people in there are no guarantees. Sustained political

Together this represents an extra 24% of England and Wales. will and government commitments will be

the total land mass in Scotland and England The Institute of Chartered Foresters essential in delivering scale, if the UK is

that is suitable for expanding woodlands. believes there is an urgent need for more realistically going to achieve its net zero,

Converting this land from it’s current primary skilled staff in the forestry workforce even biodiversity and planting targets.

Planting progress across UK 24% Current annual planting

Excluding valuable targets

12

agricultural land and

2019-2020

land under protected Scotland

Number of trees planted (000Ha)

12,000ha

designations, the Forestry

Target in 2020

9

N Ireland

Commission has identified 900ha

an extra 24% of the total England

6

land mass in Scotland 5,000ha

and England suitable for

3 expanding woodlands

Wales

2,000ha

0

England Scotland N Ireland Wales

figure 7 Source Forestry Commission figure 8 Source Savills Research

savills.com/research 6Woodland expansion

The industry requires substantial investment if tree

planting is to be delivered rapidly and at significant

scale – trees don’t grow overnight

NURSERY CAPACITY years are good mast (seed production) years. TIMBER

With increasing planting and re-stocking The Forestry Commission recently

MARKET

demand comes even greater demand for announced a potential Nursery Notification

tree seedlings. Tree nurseries have endured Scheme, intended to inform UK seed suppliers A year on from the start

sustained demand increases over the last and tree growers of forthcoming woodland of the Covid-19 pandemic

few years. The nursery sector has struggled creation and restocking projects, in the and we can start to

to anticipate demand for seedlings in what is hope that it will enable them to prepare tree uncover the ways in which

essentially a time-critical operation. Scaling stock accordingly and ensure supply across the virus has had an

up planting stock needs careful planning given the sector. impact on the end users of

the long term nature of these ventures to avoid The forestry sector has not seen such a the timber market. During

under or over supply. rapid demand for upscaling for many years, the pandemic, many home

Nurseries also need to be ready to adapt to possibly ever. The turn around needed to owners, bored of staring

the impact of a changing climate on seedling reach net zero emissions by 2050 is at odds at the same four walls and

requirements, as there is likely to be a rising with a sector that has always worked on long with time on their hands,

demand for seeds able to withstand increasing timescales. The industry requires substantial have taken to renovating,

disease and climatic pressure and achieve investment if tree planting is to be delivered with sales of home

desired productivity. Even the collection of rapidly and at significant scale – trees don’t improvement and

gardening products

seed for nursery stock is challenging, as not all grow overnight.

growing by almost 50%

compared to the previous

year (Statista 2020). Much

of these purchases will be

Historical woodland creation across the UK

timber-based building

materials. However,

50 despite the increase in

England Wales Scotland DIY, housebuilding was

UK (minimum) target

halted for the first

UK (upper) target

38 lockdown of 2020,

disrupting demand for

Thousand hectares

timber materials on a

larger scale.

25

Finally, Covid-19 has

resulted in a rapid

increase in online retail –

13 in June 2020 online retail

accounted for a record

33% of all retail sales and

91 local authorities have

0

seen parcel deliveries rise

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

by more than 100% over

the past year (Savills

Research). This is likely to

figure 9 Source Forestry Commission, Carbon brief

have resulted in an

increased demand for

both cardboard and

THE SOCIAL POWER OF FORESTRY timber pallets, critical

to a booming delivery

Forestry is a multi-functional asset, with multiple

logistics sector.

ecosystem services flowing from it, whether it be timber,

Ultimately, promoting a

carbon, flood prevention or public access. Woodlands are

high quality, high demand

increasingly being understood and utilised for their

timber market is a key

holistic value. Forest bathing is a practice garnering

part of the solution to

interest. It originates from Japan and focuses on

increasing tree planting

immersing oneself in woodland as a way to relax, cure

across the UK and in doing

anxiety and improve mental health.

so thereby sequestering

There is more and more science emerging into the

more carbon.

effects of leaf shape, the colour green and the sounds and

smells of a forest and the positive impact that this has on

mental and physical health. Some land managers are

leasing spaces within their woodland for forest bathing

courses to take place, or reaping additional value by

creating commercial forest therapy enterprises. As

society increasingly demands the multiple benefits that

flow from forestry, land managers have the chance to

innovate with service lines and opportunities.

7UK Rural - January 2020 UK Rural - February 2021

Regenerative

S P OT L I G H T

Savills Research

Natural Capital S P OT L I G H T

Savills Research

Agriculture

Carbon Offset Market Biodiversity Net Gain Nitrate Neutrality Rewilding Building resilience Core principles Increasing profitability

1_Savills_Spotlight_NatCapital_10.indd 2 15/01/2020 14:56

UK Cross Sector – April 2021 November 2020

Property

S P OT L I G H T

Savills Research

and Carbon

S P OT L I G H T

Savills Research

Rural Logistics

Measuring risk Green real estate Operational challenges Emissions reduction Urban migration Logistics capacity Rural repurposing

Savills Research

We’re a dedicated team with an unrivalled reputation for producing well-informed and

accurate analysis, research and commentary across all sectors of the UK property market.

To view copies of our previous Spotlight publications, go to www.savills.co.uk/insight-and-opinion/

Analysis methodology: Our research analyses our transactional database of forest sales. This database collates data from all mainstream forestry transactions over 20 hectares in area, and

where we are aware, off-market or private sales. While every effort is taken to ensure all transactions are included within the information presented within this publication, it is very likely that

further sales are reported after our publishing. Therefore, this Spotlight on the UK Forestry Market takes into account all new available information.

James Adamson Nicola Buckingham Molly Biddell

Head of Forestry Investment UK Rural Research Rural Research

+44 (0) 1738 447 510 +44 (0) 7807 999 011 +44 (0) 7866 885 240

james.adamson@savills.com nbuckingham@savills.com molly.biddell@savills.com

Savills plc: Savills plc is a global real estate services provider listed on the London Stock Exchange. We have an international network of more than 600 offices and associates throughout the Americas, the UK,

continental Europe, Asia Pacific, Africa, India and the Middle East, offering a broad range of specialist advisory, management and transactional services to clients all over the world. This report is for general informative

purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. While every effort has

been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form

is prohibited without written permission from Savills Research.You can also read