US Rare Earths Today: Misconceptions, Dreams and Realities - South Dakota Mines GEOL/GEOE/PALEO Seminar Series April 16, 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

South Dakota Mines GEOL/GEOE/PALEO Seminar Series April 16, 2021 US Rare Earths Today: Misconceptions, Dreams and Realities David R. Hammond, Ph.D. Principal Mineral Economist Hammond International Group

Discussion Topics: ➢ What are Rare-Earth Elements? ➢ Where are they found? ➢ What are they used for? ➢ What are the critical issues? ➢ Who are the US players? ➢ What are the realistic solutions?

Discussion Purpose:

Bring attention to some of the core issues, problems

and realities associated with current US Department of

Defense initiatives to address needed supply of critical

Rare Earth Elements.

Discussion Order:

➢ REE Characteristics

➢ REE Markets

➢ REE Realities

➢ REE Misconceptions

➢ US REE Dreams

3

Rare-Earth Elements:

Lanthanide

Series

4

Rare-Earth Element Oxides:

Total Rare Earth Oxides

TREO

Heavy Rare Earths Light Rare Earth Oxides

HREO OXIDE CRUSTAL LREO OXIDE CRUSTAL

ATOMIC ATOMIC ATOMIC ABUND ATOMIC ATOMIC ATOMIC ABUND

ELEMENT SYMBOL NUMBER WEIGHT OXIDE WEIGHT Oxide/REE (ppm) ELEMENT SYMBOL NUMBER WEIGHT OXIDE WEIGHT Oxide/REE (ppm)

1 Yttrium Y 39 88.906 Y2O3 225.812 1.270 22.0 1 Scandium Sc 21 44.956 Sc2O3 137.910 22

2 Terbium Tb 65 158.925 Tb4O7 747.700 1.176 0.6 2 Lanthanum La 57 138.906 La2O3 325.812 1.173 30

3 Dysprosium Dy 66 162.500 Dy2O3 373.000 1.148 3.5 3 Cerium Ce 58 140.116 CeO2 172.116 1.228 64

4 Holmium Ho 67 164.930 Ho2O3 377.860 1.146 0.8 4 Praseodymium Pr 59 140.908 Pr6O11 1021.448 1.208 7.1

5 Erbium Er 68 167.259 Er2O3 382.518 1.143 2.3 5 Neodymium Nd 60 144.242 Nd2O3 336.484 1.166 26

Pm2O3

6 Thulium Tm 69 168.934 Tm2O3 385.868 1.142 0.3 6 Promethium Pm 61 145.000 337.824 1×10−15

7 Ytterbium Yb 70 173.040 Yb2O3 394.080 1.139 2.2 7 Samarium Sm 62 150.360 Sm2O3 348.720 1.160 4.5

8 Lutetium Lu 71 174.967 Lu2O3 397.934 1.137 0.3 8 Europium Eu 63 151.964 Eu2O3 351.928 1.158 0.9

9 Gadolinium Gd 64 157.250 Gd2O3 362.500 1.153 3.8

5

Rare-Earth Elements Applications: Source: Dudley J. Kingsnorth, 2016, “The Rare Earth Industry in 2016,” Industrial Minerals Company of Australia.

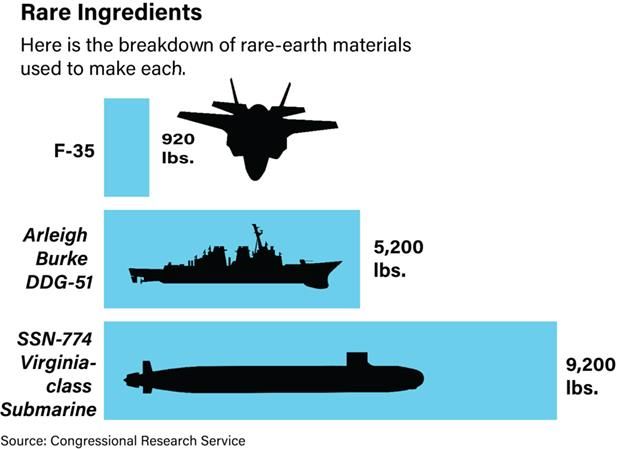

Rare-Earth Elements in National Defense:

7Rare-Earth Elements Consumption*:

(TONS)

(TONS)

(TONS)

*View as order of magnitude only; values lack confidence due to issues with Chinese data used

Source: Dudley J. Kingsnorth, 2016, “The Rare Earth Industry in 2016,” Industrial Minerals Company of Australia.Rare-Earth Element Production Chain:

Mining Concentration Extraction Refining Alloying Fabrication

Rare Earth TREO REO REE REE REE

Minerals Concentrate Oxides Metals Alloys Products

9Principal REE Minerals:

Mineral Chemical Formula (Ideal)

Bastnäesite REECO3F

Paristite CaREE2(CO3)3F2

Synchysite CaREE(CO3)2F)

Monazite (REE,Th)PO4

Xenotime (Y,HREE,Th,U)PO4

Apatite (Ca,REE)5(PO4)3(F,Cl,OH)

Loparite (Na,REE)2Ti2O6

Allanite A2M3Si3O12(OH)

Of Special Mention!

Eudialyte Na15Ca6(Fe,Mn)3Zr3SiO(O,OH,H2O)3(Si3O9)2(Si9O27)2(OH,Cl)2

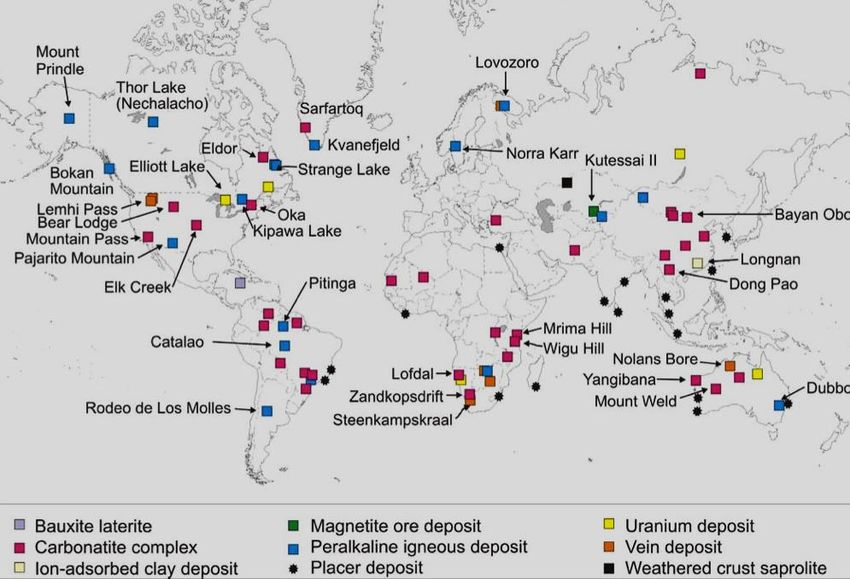

10REE Deposit Types:

Association Example

Lateritic Ion-Adsorption Clays Bayon Obo, China

Peralkaline igneous rocks Bokan Mountain, Alaska; Round Top, Texas

Carbonatites Mountain Pass, California; Bear Lodge, Wyoming

Iron oxide apatites Pea Ridge, Missouri

Pegmatites Spruce Pine, North Carolina; Alces Lake, Saskatchewan

Metamorphic skarn Mary Kathleen, Queensland

Stratiform phosphates Mount Weld, Western Australia

Pelagic muds/Mn nodules Minami Tori Shima, Pacific Ocean

Paleo pelagic muds/Mn-Fe nodules Chamberlin, South Dakota

Paleo placers Witwatersrand, South Africa

Heavy mineral sands Cooljarloo, Western Australia

Fluorine-Fluorite associations Hicks Dome, Illinois

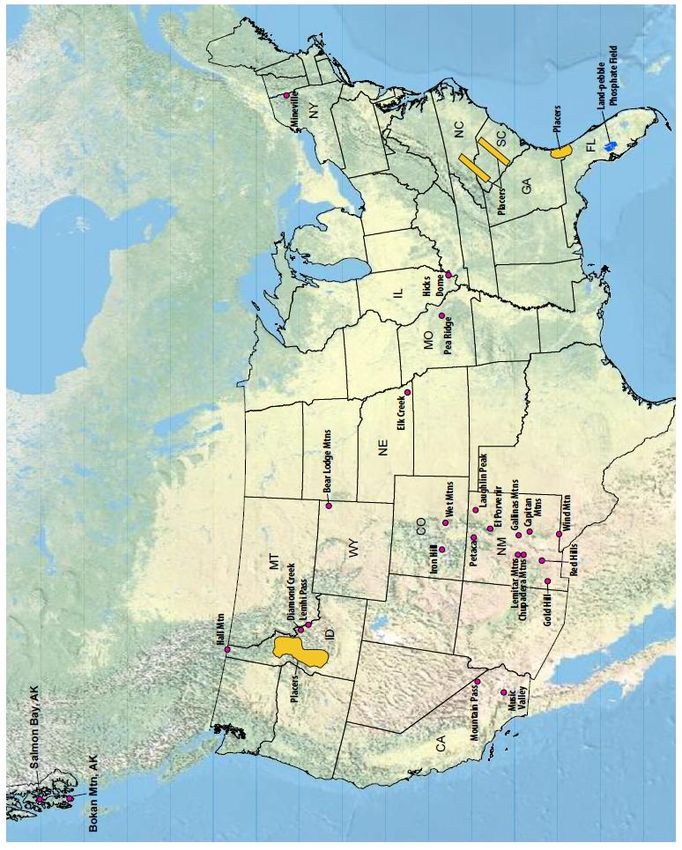

11Rare-Earth Minerals Deposits: Source: www.dggs.alaska.gov/webpubs/dggs/ic/text/ic061.PDF

Rare-Earth Mineralization in the US:

La Paz

Round Mountain

Source: Bradley S. Van Gosen, Philip L. Verplanck, and Poul Emsbo, “Rare Earth Element Mineral Deposits in the United States,” USGS Circular 1454 Ver 1.1, April 2019

13Rare-Earth Minerals Production & Reserves

10 Production quota; does not include undocumented production.

Source: USGS Mineral Commodity Summaries 2021 – Rare EarthsRare-Earth Deposits Reserves & Resources:

Current REO “Posted” Prices:

Oxide Specification Price (US$/kg) Price Change

Cerium Oxide 99%min FOB China 1.50-1.53 nochange

Cerium Oxide 99.9%min In warehouse Rotterdam 2.30-2.40 nochange

Dysprosium Oxide 99.5%min FOB China 467.00-472.00 nochange

Erbium Oxide 99.5%min FOB China 32.50-33.50 up

Europium Oxide 99.999%min FOB China 31.50-32.50 nochange

Gadolinium Oxide 99.5%min EXW China 33.50-34.00 nochange

Holmium Oxide 99.5%min EXW China 136.20-136.90 nochange

Lanthanum Oxide 99.999%min FOB China 3.80-3.90 down

Neodymium Oxide 99.5%min FOB China 93.50-94.00 down

Praseodymium Oxide 99.5%min FOB China 79.00-80.00 nochange

Praseodymium Oxide 99.5%min In warehouse Rotterdam 74.00-75.00 nochange

PrNd Mischmetal Pr 25%, Nd 75% FOB China 107.50-108.50 nochange

Samarium Oxide 99.9%min FOB China 19.80-20.30 nochange

Scandium Oxide 99.99%min EXW China 856.80-933.30 nochange

Terbium Oxide 99.99%min FOB China 1408.00-1413.00 down

Ytterbium Oxide 99.99%min EXW China 14.80-14.60 nochange

Yttrium Oxide 99.999%min FOB China 6.40-6.50 down

Yttrium Oxide 99.999%min In warehouse Rotterdam 6.90-7.10 nochange

Source: Asian Metals April 14, 2021

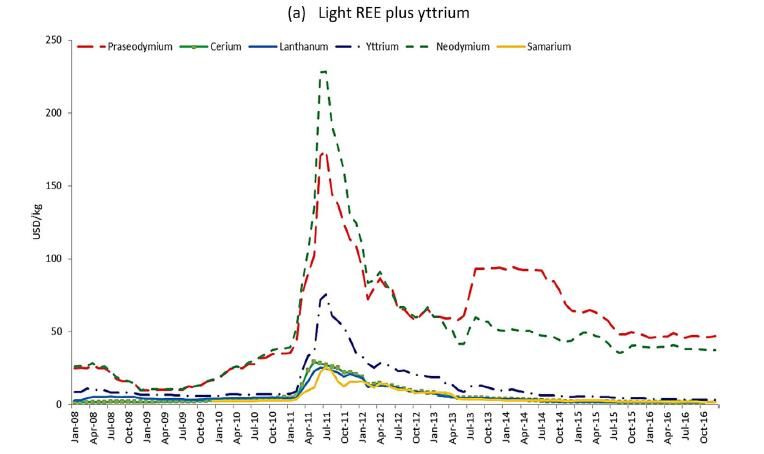

16REE “Market” Prices:

Source: Viviana

Fernandez, “Rare-

Earth Elements: A

Historical and a

Financial

Perspective,”

Resources Policy,

September 2017

17Rare-Earth Critical Issues:

➢ “The Middle East has Oil, China has Rare-Earths”

(Deng Xiaoping, 1992)

➢ Long-term Chinese strategy is to export REEs in value-added products

➢ China now dominates global REE mining, metallurgical processing,

technical research, magnet production, etc., etc. . .

✓ Produces 80% of REE the world’s REE resources

✓ Processes well over 90% of the World’s REOs

✓ Produces 95% of World’s REE metals and alloys

✓ Possesses well over 90% of World REE production capacity and can expand

✓ Holds great majority of modern day REE process & product patents

✓ Increasing imports of REE concentrates and oxides

✓ Increasing investments in REE primary production outside China

✓ Supplies 100% of US defense magnet requirements

➢ China has near total control of global REE supply!

➢ China has 100% control over global REE prices!REE Realities:

1. Global REE industry represents an “imperfect market”

2. REEs are not created equal!

3. The REE Supply Problem is Processing, not Sourcing of REE

containing material!

4. Commercial level REE Processing is very difficult!

5. It will take years to develop new REE mines, processing and

metal fabrication capabilities outside China

6. No major mining companies will get involved with REEs unless

significant by-product from primary production!

19More Realities:

1. China is the major customer for REE resource production since

majority of world's REE metals are produced by Chinese

controlled entities; Chinese companies are aggressively trying

to tie up international REE primary supplies.

2. No matter how great your flowsheet is, you must have tons

AND grade to be an REE supplier that matters; producing small

share of market demand won’t cut it!

3. REE sales will be to intermediate and end-use consumers via

non-transparent bi-lateral long-term supply contracts.

4. The logical potential equity partners for miners & processors

are REE consumers.

5. Lowest possible production costs will be determinant for

consumer partner investment/supply contract decisions.

20REE Misconceptions:

1. I can use market posted prices for my project economics!

2. I can use the REE “Basket” for projecting project revenues!

3. My REE resource can be processed by typical conventional

metallurgical processes!

4. My process chemistry/metallurgy fits theory and works at

bench/pilot scale; it no doubt will work commercially!

5. I have new technology and my costs are going to be lower--see I

proved it in the lab!

6. I can cash-out my project to some big mining company or bring

them in as a venture partner!

Answers: No, No, No, No, No and No!

21So, What is the US Doing About it?

❖ Unfortunately Not Much that has accomplished anything!

• Basically ignored by Clinton, Bush, and Obama Administrations

• DOE university funding grants focused on REEs from coal and AMD over

last decade

• Recently DOE and DOD funding grants for development of process and

metal separation technologies

❖ Critical Materials Institute:

• Government-University-Industry partnership started 2013

• Focused on 34 Critical Minerals/Elements

• Funded by DOE

• Based at the Ames Laboratory, Iowa State University and CSM

• Mission: “To assure supply chains of materials critical to clean energy

technologies – enabling innovation in U.S. manufacturing and enhancing U.S.

energy security.”More Recent Government Actions:

➢ December 2017: Executive Order 13817

➢ August 2018: National Defense Authorization Act—Section 871:

“. . . prohibits sourcing of REM’s from China, Russia, North Korea and Iran . . .”

➢ June 2019: “A Federal Strategy to Ensure Secure and Reliable Supplies of Critical

Minerals”

➢ June 2019: “Presidential Determination Pursuant to Section 303 of the Defense

Production Act of 1950” (DARPA Title III)

➢ July 2019: DOD RFI regarding LREE and HREE Separation and Processing

Capability

➢ December 2019: DOD FOA regarding REE Element Separation and Processing

Capability

➢ January 2021: DOD and DOE funding grants

➢ February 2021: Biden administration directive to agencies to critical mineral supply

chains

23Near-Term Global Demand for Critical

REEs:

2020 2025

(mt) (mt)

Total Rare Earth Oxides 200,000 240,000

Assumed US Requirement 60,000 90,000

Praseodymium Oxide 1,000 1,200

Neodymium Oxide 3,500 5,000

Terbium Oxide 150 250

Dysprosium Oxide 500 1,500

Source: D R Hammond projections for relative comparison of upstream mine production purposes only!!!!!

24Current US REE Resource Prospects:

Coal Dream (too low grade & too dispersed)

Coal Waste Dream ( “ “ “ “ “ )

Coal Ash Dream ( “ “ “ “ “ )

Acid Mine Drainage Dream ( “ “ “ “ “ )

Round Top Dream (extremely low grade)

Bokan Mountain Dream (very small resource; low-grade)

Elk Creek Dream (uneconomic, based on Sc)

La Paz Dream (little info, assume is stock play

Hicks Dome Interesting, early stage

Chamberlin Paleo Nodules Very interesting, early stage

Pea Ridge Potential, REE as Fe mine by-product

Florida Phosphates Potential, enormous resource

Bear Lodge Development, large resource, high grade

Mountain Pass Producer (but only LREEs and for China)

25Current US REE Processing Prospects:

MP Materials Mountain Pass, California: Operating but produces LREE

concentrates only which are exported China, new

metallurgical facility promoted, $10 million DOD grant.

Major Problem: Owned by two hedge funds and Shenghe

Resources

Energy Fuels White Mesa Uranium Mill, Blanding, Utah: Operating, now

processing monazite to REE oxide/carbonate, metal

extraction to be done in Estonia, owned by Energy Fuels.

Major Advantage: has radioactive waste disposal permit!

Lynas/Blueline Hondo, Texas: Planned facility to develop new

metallurgical processing technologies for separation of

LREOs, $30 million DOD grant.

Advantage: potential for non-China processing of Mt Weld

concentrates/oxides

Rare Element Resources Upton, Wyoming: Near-term development for process of

Bear Lodge ore to REE oxides; partnership with General

Atomic et al., $22 million DOE grant.

Advantage: has number of permits in hand

26Conclusions:

☼ China controls US’s current/future national defense supply of critical REEs!

☼ There is NO “free market solution” to the US’s REE problem!

☼ Core issue is NOT the need for new REE mines, rather the need for new

REE refining and metallurgical fabrication capacity outside of China!

☼ Government technical & and economic knowledge of mineral resource

production is lacking!

☼ Defense Department officials have little to no understanding of the mining

business in general and the REE value chain in particular!

☼ Junior venture companies will try to capitalize on this lack of understanding

to keep infeasible REE projects going!

☼ High potential US Government will throw buckets of taxpayer money away

to promoters, abetted by political influence and pressures!

DOD needs a fully independent advisory board of experienced resource,

mining, and processing experts for guidance on the optimal (cost & quantity)

sourcing of critical REE supply!

27Realistic Solutions to the Problem:

➢ Government funding, development, and ownership of

central REE separation and fabrication facility?

➢ REE consumer cooperative to create and operate

downstream REE processing, including Defense

Department participation? (e.g., current Rubio Bill)

What’s not realistic is continuing to rely on Chinese

government kindness for finished REE materials, or to

count on Wall Street to bail us out!

28David R. Hammond, Ph.D.

Principal Mineral Economist

Hammond International Group

2406 Glenhaven Drive

Highlands Ranch, Colorado 80126 USA

mineraleconomics.DrH@gmail.com

303-807-3671

29Supplemental Slides

30Mountain Pass - Producer:

Owner: MP Materials - JHL Capital Group, QVT Financial LP,

Shenghe Resources Holding Co. Ltd.(9.9%)

Deposit Type: Carbonatite with 10-15% Bastnäsite

Resource (5.0% TREO C/O): 16.7 Million mt (P & P)*

In-place TREO Grade: 8.0%

In-place TREO: 1.3 Million mt (83% La and Ce)

Annual Pr Oxide Output: 927 mt (15.4% of 2025 US demand)

Annual Nd Oxide Output: 2,511 mt (16.7% of 2025 US demand)

Annual Tb Oxide Output: Very small production in past

Annual Dy Oxide Output: Very small production in past

Comments: - Currently produces only REE concentrates

- Resource is likely much, much larger than current “reserves”

- Currently produces only REE concentrates which are all

exported to China for processing to metal; this reflects

political strategies, not rational economics!

* 2012 Press Release

31Bear Lodge – Real Potential:

Owner: Rare Element Resources (REEMF:OTC) and General Atomics

Deposit Type: Carbonatite with Bastnäsite

Resource (1.5% TREO c/o): 16.2 Million mt (M & Ind)*

In-place TREO Grade: 8.0%

In-place TREO: 1.3 Million mt

Annual TREO Production: 20,000 mt

Annual Pr Oxide Output: 1,200 mt ( 7.5% of 2025 US demand)

Annual Nd Oxide Output: 4,500 mt (11.3% of 2025 US demand)

Annual Tb Oxide Output: 30 mt ( 4.9% of 2025 US demand)

Annual Dy Oxide Output: 90 mt ( 3.2% of 2025 US demand)

Comments: - Additional inferred resource of 41 Million mt

- Most advanced of publically held US located REE projects

- Entering pilot plant phase with General Atomics

*2014 Feasibility Study and personal communication

32Round Top - Dream:

Owner: Texas Mineral Resources w/ USA Rare Earths Earn-In (OTCQB:TMRC)

Deposit Type: Tertiary peralkaline rhyolite intrusion

Resource: 364 Million mt (M & I)*

In-place Pr Grade: 10.3 ppm (crustal abundance 7.1 ppm)

In-place Nd Grade: 27.9 ppm (crustal abundance 26.0 ppm)

In-place Tb Grade: 3.5 ppm (crustal abundance 0.06 ppm)

In-place Dy Grade: 33.3 ppm (crustal abundance 3.5 ppm)

Annual Mine Production: 7.3 Million mt TPY (20,000 TPD leach feed)

Annual Pr Oxide Output: 70 mt (0.4% of 2025 US demand)

Annual Nd Oxide Output: 182 mt (0.4% of 2025 US demand)

Annual Tb Oxide Output: 24 mt (4.0% of 2025 US demand)

Annual Dy Oxide Output: 207 mt (7.4% of 2025 US demand)

Comments: - Very low REE grades, commercial feasible highly doubtful!

- Projected as a multi-industrial minerals/metals and commodity

chemicals manufacturer, with REEs as by-products

- PEA (2019) claims project will produce 20 products:

Y, Pr, Nd, Sm, Tb, Dy, Lu, Sc and Ga Oxides; Be Hydroxide; U3O8,

Li Carbonate; Al, Fe, Mg, Mn and K Sulfates

*2019 PEA

33Bokan Mountain - Dream:

Owner: Ucore Rare Metals (TSX-V: UCU, OTCQX:UURAF, FSE: U9U)

Deposit Type: Alkaline Igneous Intrusion

Resource (at 0.04 % TREO c/o): 5.8 Million mt (M & I)*

In-place TREO Grade: 0.60%

In-place TREO: 28,000 mt

Recoverable TREO: 22,500 mt

Annual TREO Production: 1,875 mt (1,500 TPD mill feed)

Annual Pr Oxide Output: 71 mt (1.2% of 2025 US demand)

Annual Nd Oxide Output: 274 mt (1.8% of 2025 US demand)

Annual Tb Oxide Output: 12 mt (5.5% of 2025 US demand)

Annual Dy Oxide Output: 83 mt (7.9% of 2025 US demand)

Comments: - Small resource; Dotson Zone geologically constrained

- Adjacent to EPA Superfund site (Uranium)

- Alaska AIEDA commitment of $145 M (but only with a positive

Feasibility Study – that will never happen!)

- 2019 PR claims it will produce the REE “basket” plus Nb, Zr,

Be, Hf, TiO2, V

*2013 PEA plus 2015 Press Release

34You can also read