WEBINAR: COVID-19 AND IMPACT ON THE US FINANCIAL SYSTEM - Oliver Wyman

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WEBINAR: COVID-19 AND IMPACT ON THE US FINANCIAL SYSTEM Reports from Brazil and Australia August 12th, 2020 Please note that this session was held at a particular point in time (Wednesday, August 12th, 2020, 4pm-5pm EDT), and in light of the rapidly evolving COVID-19 situation, it is possible these discussions are no longer accurate after that date.

CONFIDENTIALITY Our clients’ industries are extremely competitive, and the maintenance of confidentiality with respect to our clients’ plans and data is critical. Oliver Wyman rigorously applies internal confidentiality practices to protect the confidentiality of all client information. Similarly, our industry is very competitive. We view our approaches and insights as proprietary and therefore look to our clients to protect our interests in our proposals, presentations, methodologies, and analytical techniques. Under no circumstances should this material be shared with any third party without the prior written consent of Oliver Wyman. © Oliver Wyman

WEBINAR AGENDA 1 Epidemiological update 2 Macroeconomic outlook 3 Perspectives from Brazil 4 Perspectives from Australia 5 Q&A © Oliver Wyman 3

OUR PANELISTS

Til Schuermann Nuno Monteiro

Partner & Co-Head, Risk Partner, Financial

& Public Policy Services

Helen Leis

Partner, Health & Life Nicholas Tonkes

Sciences Partner, CFA & CIS

© Oliver Wyman 4

01

EPIDEMIOLOGICAL

UPDATE

Helen Leis

Partner, Health & Life

Sciences

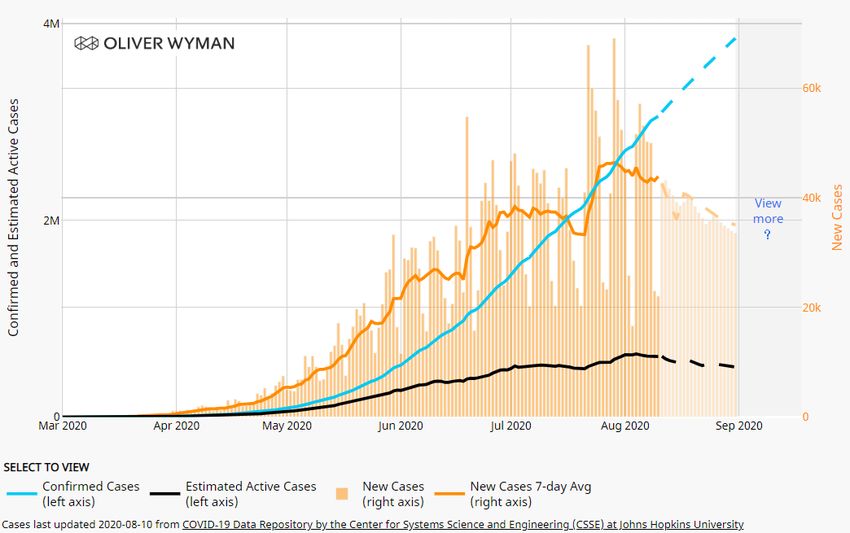

RECENT HOTSPOTS IN THE SOUTH AND WEST ARE BEGINNING TO SHOW SIGNS OF

SLOWING CASE GROWTH WHILE PARTS OF THE MIDWEST HEAT UP

Active cases per million by state

As of August 9th, 2020 Example states

8,000 Forecast launch

7,000

6,000

5,000

4,000

Missouri

3,000 Texas

Illinois

Florida

2,000 California

Indiana

1,000

New York

0

3/1 3/8 3/15 3/22 3/29 4/5 4/12 4/19 4/26 5/3 5/10 5/17 5/24 5/31 6/7 6/14 6/21 6/28 7/5 7/12 7/19 7/26 8/2 8/9 8/16 8/23

© Oliver Wyman 6

DUE TO HIGH ACTIVE CASE COUNTS AND LIMITED TESTING, RISK IS STILL HIGH IN THE

SOUTH AND WEST, WHILE NEAR TERM RISK HAS INCREASED IN THE MIDWEST

Data as of: Legend:

8/4 % Change in new

daily cases (2 weeks)

Circle size: # of active cases

Testing rates 0% or less 1–25%

>10% indicate 26–50% 51–100%

capacity issue,

101+%

suggesting

confirmed case Testing capacity insufficient

growth is to capture true case growth

limited by

tests, not true Fully reopened1

FL2 caseload in Partially reopened

region

Partially reclosed (after

reopening)

South/West Rural States Midwest Northeast/Mid-Atlantic

High Risk Moderate-High Risk Moderate–High Risk Moderate Risk

• 9 of 10 states with highest active cases are in • All fully reopened and fared well for • Cases continue to rise across most of • Generally hit hard by initial outbreak

South (CA is 3rd) multiple weeks the region • Cautiously reopening after case decline,

• Case growth appears to be slowing, but may • Though some case counts are still low, • IL, MO, OH, WI are all in the top 20 though many (NY, NJ, DE) have paused

be a result of limited testing - Several states hotspots like Idaho now in top 10 active states by active cases, signaling reopening plans

(MS, AL, FL, NV, AZ, SC, TX, GA, and AR) have cases/capita potential shifting of epicenter • Pockets of Northeast (NJ, CT, MA, RI) are

positive test rates of >10% • Despite low active case counts, - AK, NE, • Many states (MO, KS, IA, IN, KY, WI, showing signs of outbreak, with 2 week case

• Alternative explanations for slowing growth in SD, MT, WY, and ND have all been MN, OH) have concerning rise in growth >50%

following slides growing for over a month with little signs positive test rates >5%

of slowing down

1. “Fully reopened” defined as when a majority of high risk businesses, including bars, movie theaters, or gyms, have been reopened with indoor service. This chart does not account for regulatory restrictions that may or may not be in place

© Oliver Wyman in those businesses, including mask wearing or capacity constraints. 2: Florida has considered reclosure of a number of risky venues, including bars, gyms, & restaurants, but ultimately decided to only reclose bars; thus, Florida is still 7

considered “fully reopened”

HOWEVER, WHILE THE MIDWEST HAS SHOWN SIGNS OF RISING CASES, THE NEAR TERM

OUTLOOK IS NOT AS SEVERE AS IT WAS IN THE SOUTH IN JULY

Key COVID metrics in Midwest (currently) vs. South (1 month ago)

Midwest (as of 8/9) South (as of 7/9)

States included in set IL, IN, IA, KS, KY, MI, MN, MO, AL, AR, FL, GA, LA, MS, OK, SC,

OH, WI TN, TX

Median mobility 86% of baseline 90% of baseline

Median 2 week case growth 11% 100%

Median active cases per 1M 1810 2400

Median tests per 1M 1940 1920

Median % positive tests 7.5% 11.8%

% of states with mask mandates 80% 10%

• Case growth is much less severe, allowing Midwestern states more time to respond to renewed outbreaks

• Testing is stronger in the Midwest, with similar capacity but lower active cases and % positive rates, though some states (MO, KS, IA) are currently at

high risk from testing capacity strain

• Mask mandates and social mobility are also stronger in the Midwest, hopefully dampening severity of the outbreak

© Oliver Wyman 8EVEN IF HOTSPOT CASES ARE TRULY DECLINING, STATES WILL STILL HAVE TO DEAL WITH

RISING DEATHS FOR THE FORESEEABLE FUTURE There is a ~3-4 week lag between new cases and

associated deaths; deaths in hotspots spiked ~1 month

after cases started rising. Lag is longer now than in early

pandemic due to increased testing catching cases earlier

The effects of the sharply rising case rates throughout the summer are New cases per 1m

still being felt in plateauing/declining hotspots 600

400

Spike begins

• Though new daily hospitalization growth has appeared to slow

down in recent days, the lengthy lag between diagnosis and 200

outcome ensures that hospitalizations are on the rise even in 0

states with clear new case declines May Jun Jul Aug

• This trend is mirrored in deaths (with a longer time lag), as new New hospitalizations per 1m1

25

daily death rate tended to increase throughout July in hotspot 20 Spike begins

states, even as case rates stabilized 15

• Health systems will be dealing with capacity strain for a month or 10

longer after cases peak – this strain will be exacerbated in regions 5

with plateauing (not declining) new daily case rates 0

May Jun Jul Aug

– Plateauing case rates may lead to even higher death rates as a New deaths per 1m

result of sustained demand for beds, ventilators, PPE, or 6

healthcare labor reducing quality of care for the population as a Spike begins

whole; states should strive for clear declines in case rates before 4

relaxing restrictions 2

0

1. New hospitalization data not available in Texas May Jun Jul Aug

© Oliver Wyman Florida Texas 9WE DO NOT YET KNOW IF CASE GROWTH HAS TRULY STABILIZED; POSITIVE TEST RATES

>10% INDICATE A TESTING CAPACITY ISSUE AND LIMIT ABILITY TO ASSESS GROWTH

7-day % positive testing rate

28%

Inadequate % positive rates • Though some states appear to be

26%

improving (AZ, TX), their positive

24%

MS rate is still high enough to limit true

22%

understanding of outbreak scope

20% AL

18%

FL

AZ

• There are currently 14 states with a

16%

ID

KS

>10% positive rate, including 7

14%

SC

TX hotspots that appear to have

12%

MO

AR

declining case rates:

10% % positive rate risk threshold – AL, AZ, FL, ID, KS, SC, TX

8% • While declining case rates and %

6% positives are encouraging, those case

4% rates should be taken with a grain of

2% salt until positive rates are well

05/31 06/07 06/14 06/21 06/28 07/05 07/12 07/19 07/26 08/02 08/09

below 10% in current hotspots

Alabama Florida Kansas Texas Missouri

Arizona Idaho South Carolina Arkansas Mississippi

© Oliver Wyman 10THE MAJORITY OF STATES CURRENTLY DO NOT HAVE ADEQUATE TESTING CAPACITY TO

ADDRESS EXISTING CASE GROWTH

New cases per thousand (including undetected cases) by tests per thousand for each state

As of August 9th, 20201

0.45

Inadequate capacity Handling the surge

Below average testing, above average cases Above average testing, above average cases

0.40 Louisiana

New cases per thousand (7-day rolling average)

0.35 Mississippi

0.30 Idaho Texas

Florida Georgia

Nevada Alabama Tennessee

0.25 Arkansas

South Carolina

Missouri Oklahoma

0.20 Arizona

California

North Dakota

Rhode Island Iowa Nebraska

0.15 North Carolina

Kansas Wisconsin Illinois

Utah Maryland

Montana

0.10 Managing with less Indiana New Mexico Alaska

Delaware

infrastructure Colorado Ohio Michigan District of Columbia

Below average testing, below Massachusetts

0.05 Pennsylvania West Virginia Connecticut

average cases

New Jersey New York Strongest capacity

New Hampshire Maine

Vermont Above average testing, below average cases

0.00

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0 4.2 4.4 4.6 4.8 5.0 7.2

New tests per thousand (7-day rolling average)

Successful responses to COVID rely on quick and accurate testing; Until this issue is resolved, regional and federal responses will necessarily be less

effective

© Oliver Wyman 1. Quadrants determined using the average of state-level new tests per thousand (7-day rolling average) and average of state-level new cases per thousand (7-day rolling average) 11ALTERNATIVES TO COVID-19 CLINICAL PCR TESTING ARE EMERGING THAT HAVE THE

POTENTIAL TO ALLEVIATE CAPACITY CONCERNS (ONCE SCALED)

Type of test Description Potential future benefit Firms with FDA Emergency Use Authorization (EUA)

Quickly detects protein fragments on or Produce results more rapidly and cheaply • Becton Dickinson (BD) • Quidel

Antigen Testing within the virus; Rapid diagnosis and than PCR tests; are more amenable to POC

relatively cheap use

• Assurance Scientific • Kroger Health

Laboratories • LabCorp

Cheap collection at scale to reduce

• Color Genomics • P23 Labs

Allows for tissue sampling at-home or in a bottleneck at testing sites; if combined

• Compass • Phosphorous

At-Home Collection non-supervised/clinical setting; analysis with high throughput processing, possible

• Everlywell • Quest Diagnostics

still happens in laboratories to rapidly turnaround results for large

• Fulgent Therapeutics • RUCDR Infinite Biologics

swaths of populations

• Kaiser Permanente Mid-Atlantic

States

• Sherlock Bioscience • UCSF Health Clinical

Fast, precise diagnostic capabilities; if

Utilizes CRISPR machinery to detect COVID Laboratories

CRISPR developed for POC use, highly increase

genetic material from tissue sampling

scale and speed of testing

High Throughput Processes large amounts of samples with Sample processing at larger scale than • Color Genomics • Quest Diagnostics

Processing relatively short turnaround other diagnostics • Illumina

Allows for diagnostic testing at or near the • Abbott • Mesa Biotech

POC Molecular Substantially decrease turnaround time for • Atila Biosystems • Privapath Diagnostics

point of care, without delay from sending

Testing results • Cepheid

samples to a laboratory

Experimental technology is also being developed that may increase the scope and timeliness of testing – these new technologies include rapid detection from saliva,

breathalyzers, soundwave detection, or gold nanoparticles. These technologies should not be considered as anything more than experimental without further study.

© Oliver Wyman 12REOPENING SCHOOLS IS A CRITICAL AND HOTLY DEBATED ISSUE – IT LIKELY CAN BE

DONE SAFELY ONLY WHEN COMMUNITY SPREAD IS LOW

• America’s economic system can not function fully without schools, placing economic pressure on reopening

• Pediatric welfare also depends on in-person learning

Reopening schools should be a top priority, but must be done safely – reopening only when community spread is low is the best

way to limit further disruption

• Low community spread mitigates risk from reopening schools

– The U.S. CDC’s official stance is that COVID-19 transmission in schools is not a significant risk when overall

community spread is low2, and independent experts agree7

• However, reopening schools without low community spread or adequate precautions can be significantly disruptive:

– The United States has started to reopen schools in the midst of still rising cases, leading to almost immediate

disruption, including quarantine of hundreds of students and staff in newly reopened districts

– Some districts have been forced to reclose temporarily after only days of in-person operations

Despite previously reported lower severity of illness in children, recent studies suggest that kids can become infected and transmit

the virus at rates similar to adults, especially in children >10

© Oliver Wyman 1. U Chicago, 2. CDC, 3. NYT, 4. NYT, 5. ABC News, 6. IPS News, 7. NPR 13SCHOOLS NEED TO LIMIT THE RISK OF TRANSMISSION ACROSS ALL PHASES OF

REOPENING

Planning for reopening Executing reopening Continuing operations

• When to reopen • Limit importation: The first priority should be to • When to reclose: Schools and the relevant

– Community spread should be low stop cases from entering the school authorities should have a clearly defined response

– Thresholds should be clearly defined and – Health screening paired with testing (health to any positive cases within the student body or

communicated to enable effective planning screening alone unlikely to effectively diagnose staff that includes:

– Generally, epidemiologists agree upon a 5% infection) – Defined threshold of positive cases at which the

positive rate as an adequate threshold for – Strict policies on symptomatic individuals or school recloses

reopening8 close contacts staying home – Clearly defined plan or policy for when to reopen

• For whom to reopen If the virus makes it into a school… – Testing policies allowing for rapid diagnosis

– Several studies suggest transmission is less • Limit transmission: The school environment should • How much to reclose: Plans should consider extent

common among children02

MACROECONOMIC

OUTLOOK

Til Schuermann

Partner, Risk & Public

PolicyLast updated: 8/10/2020

THE US ECONOMY IS EXPERIENCING A SEVERE SHOCK: GDP

The escalation of the COVID-19 crisis has resulted in unprecedented volatility in forecasts

U.S. Real GDP Growth Forecasts – Q3 2020 to Q4 2021 Key observations from estimates

QoQ annualized growth rate, by select economic analysts1

3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

• Q2 2020 was the worst quarter

30

TD on record

Annualized growth rate (%)

25

• Forecast updates for Q3 2020

GS

20 FRBATL (Aug 7)

JPM

have been moving lower (or flat)

15

CBO

BAC FRBNY (Aug 7) over the last month, but still with

DB UBS

MS CBO MS

MS significant uncertainty in

10 GS

MS DB GS DB UBS

UBS GS

CBO UBS GS forecasts

UBS TD TD

CBO TD GS UBS DB

5

MS CBO DB • Key indicators to track include:

BAC JPM JPM MS TD CBO

JPM DB JPM TD

0

– Cycle of opening and closing in

1Q202 2Q203 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

regional economies

Avg -4.8% -33.1% 17.2% 6.5% 5.5% 4.7% 5.3% 4.4%

Max -2.3% -29.0% 28.0% 9.2% 8.0% 6.5% 10.7% 10.4% – Reliance on “smart” mitigation

Min -9.9% -35.0% 10.6% 4.5% 3.9% 3.1% 3.0% 2.7% strategies (e.g., mass testing,

Act. -5.0% -32.9% analytics)

1. JP Morgan (July 31), Goldman Sachs (July 12), Morgan Stanley (July 17), Toronto Dominion (June 17), UBS (July 29), Bank of America (July 31), Deutsche Bank (July 28), CBO (July 2)

2. JP Morgan (April 24), Goldman Sachs (April 29), Morgan Stanley (April 27), Toronto Dominion (April 20), UBS (April 29), Bank of America (April 17), Deutsche Bank (April 28), CBO (April 24)

3. JP Morgan (July 17), Goldman Sachs (July 12), Morgan Stanley (July 17), Toronto Dominion (June 17), UBS (July 29), Bank of America (July 24), Deutsche Bank (July 28), CBO (July 2)

© Oliver Wyman 16Last updated: 8/10/2020

THE US ECONOMY IS EXPERIENCING A SEVERE SHOCK: UNEMPLOYMENT

The escalation of the COVID-19 crisis has resulted in unprecedented volatility in forecasts

U.S. Unemployment Forecasts – Q1, Q2, Q3, and Q4 Key insights

Quarterly unemployment rate, by select economic analysts1

2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21 2020 2021 • Unemployment claims filed since

15

April

start of the COVID-19 lockdown have

CBO

May wiped out the last eleven years of job

Unemployment rate (%)

June DB UBS CBO gains2, 3

JPM CBO DB

10 GS Moody’s

July JPM DB JPM CBO

JPM CBO CBO JPM GS JPM

UBS • Most unemployment forecasts

TD GS DB GS Moody’s

TD TD

DB

GS JPM GS

GS

TD

CBO TD DB CBO assume a steady recovery for 2H20

TD DB TD GS

TD DB and 2021 and appear not (yet) to

5

account for the possibility of

subsequent waves of lockdown

0

Institutional forecast CBO forecast Actual

• Unemployment estimates will likely

3Q20 4Q20 1Q21 2Q21 3Q21 4Q21 2020 2021 be quite volatile for a while

Avg 10.9% 9.3% 8.5% 7.9% 7.3% 6.8% 9.6% 7.8% • Congressional Budget Office

Max 14.1% 10.5% 9.4% 8.6% 8.0% 7.6% 10.8% 8.9% forecasts a slower employment

Min 9.2% 7.9% 7.5% 7.3% 6.8% 6.3% 8.5% 7.0%

recovery than most major banks

Act. 10.2% (Jul)

1. Goldman Sachs (July 12), JP Morgan (July 31), UBS (July 29), Deutsche Bank (July 28), Toronto Dominion (June 17), CBO (July 2), Moody’s (June 22); U.S. Bureau of Labor Statistics. 2. U.S. Bureau of Labor Statistics. 3. Tracking

unemployment forecasts against unemployment reports may be misleading – unemployment reports only record jobless workers actively searching for employment

© Oliver Wyman 17THE ECONOMIC IMPACTS APPEAR TO BE CORRELATED WITH THE STRINGENCY OF

GOVERNMENT RESPONSE

Real GDP Growth vs. Oxford Stringency Index Key observations

All figures Q2 2020 except as noted below

90 • In general, greater government

More Portugal

France Belgium response in the form of behavior

Oxford Stringency Index, Quarterly Average

stringent 80

Mexico Singapore restrictions (“stringency”)

Italy

Spain Canada United StatesIndonesia

United Kingdom 70 corresponded to more adverse

Germany

Austria 60 immediate economic impact

China, Q1 South Korea

50

• However, economic impacts on a

Czech Republic

Sweden specific country likely a

Hong Kong, Q1

40 combination of other factors

30 beyond government response

Taiwan • Improved adherence to public

20

health guidance now could allow

10

for more robust recovery later….

-

-70 -60 -50 -40 -30 -20 -10 0

GDP Growth, QoQ% annualized

Sources: Oxford University, Oxford Economics/Haver Analytics

© Oliver Wyman 1803

REPORT FROM

BRAZIL

Nuno Monteiro

Partner, Risk & Public

PolicyIN BRAZIL, COVID-19 CASES ARE STILL GROWING CONSIDERABLY, WITH ESTIMATED PEAK

OF ACTIVE CASES EXPECTED TO BE REACHED IN AUGUST

COVID-19 in Brazil: Confirmed, Estimated Active, and New Credit market growth and GDP are strongly correlated

August 11th

Credit balance - real YoY growth Market consensus expects GDP

for 2020 to contract at least

GDP - real YoY growth

-5.0% vs. the +2–3% at the

30% beginning of the year

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Government quickly anticipated year-end target risk

free rate (SELIC) decrease, and went below historical

lows to stimulate credit availability by lenders

As the crisis spreads through the real economy, credit will be a central piece to amplify or smooth the recession

Source: Oliver Wyman Pandemic Navigator (https://pandemicnavigator.oliverwyman.com), World Bank data; BCB Séries temporais;

© Oliver Wyman 20COVID-19 CRISIS ARRIVES DURING THE SLOW AND LONG-WAITED RECOVERY AND WILL

IMPACT CREDIT AND NPL VOLUMES

Non-Performing Loans Credit volume outstanding

% of total loans in BRL BN

Early signs of increase in unemployment and Credit was recovering from 2015’s slowdown,

business bankruptcies, as suppressive measures but despite an increased demand from SMEs and

take place, indicate NPLs likely to grow in response individuals it is likely that credit supply will reduce

8 2,000

6 1,500

4 1,000

2 500

0 0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

SME Corporate1 Consumer2 Trend Corporate Consumer Trend

Interest rates • COVID-19 crisis arrives in the arrives during a slow and long-awaited recovery, which is

Interest rates expected to increase as particularly concerning for Retail lenders

% a.a.

investor confidence falls and NPLs grow

50 – Likely NPL increase in vintages that were already originated in growth mode

– Little room to maneuver and avoid/ mitigate credit losses

40

30 • Despite surging demand for cash from Retail clients, we expect (and start to observe) little

20 appetite from lenders in supplying the much needed credit

10

• Individual lenders and the government will have to work together to provide aid and fuel the

0 economy – with the required guard-rails to maintain the stability of the system

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Corporate Consumer Base rate Trend

1. Pessoas Jurídicas, Brazilian term for “legal entities”, includes Corporates, SMEs and individual micro-entrepreneurs (MEI); 2. Pessoas Físicas, Brazilian term for natural person or individual

© Oliver Wyman

Source: Series temporais (Central Bank of Brazil) for total credit (incl. earmarked); Relatório de economia bancária, 2018 (Central Bank of Brazil); Oliver Wyman analysis on illustrative trends

21HOW THE DYNAMICS OF RETAIL CREDIT WILL CHANGE IN BRAZIL?

Understanding how the COVID-19 crisis will change Retail credit is critical for lenders to address the upcoming challenges, calibrating the credit supply

with a changing demand and adequately responding to government stimulus

COVID-19 crisis has been severing the Credit supply shock

flow of goods and people, hindering With higher uncertainty and complexity in the macro

economies and is in the process of scenario and the emerging real economy crisis,

investor confidence goes down and shift capital to safe

delivering a global recession havens, reducing appetite to lend

Credit demand surge Government stimulus

To provide a safety net to the

Individuals and firms face a economy, Government launches

cash crunch as a result of the stimulus packages that aim to

efforts to limit the spread of mitigate effects of the crisis and

the virus, leading to a strong bridge the mismatch of credit

increase in the need for credit Crisis in the real economy demand and supply

© Oliver Wyman 22CREDIT DEMAND SURGE

Individuals and SMEs will be strongly impacted by this crisis, and will need credit to fulfill their short-term cash flow imbalance during the crisis

# of companies in MM1 # of individuals in MM2

19.2 93.5

- 1.9 Medium and large

0.9

Small

55.1 Formal employee

6.6 Micro

Small business

Level of impact

and entrepreneurs

represent 90% of

total CNPJs, 27% of

GDP and 44%

of total payroll 18.2

Informal employee from

private sector/family biz Informal sector

9.8

represents 41%

Individual

of employed

(MEI) Informal employer/

20.2 population

self-employer

+

Feedback loop between cash crunch on SMEs and individuals – one reinforces the other

1. Data Sebrae as Mar 2020; 2. IBGE as Dec 2019

© Oliver Wyman 23CREDIT SUPPLY SHOCK

Increased credit risk during the crisis is the aggregate factor that strongly contributes to the credit supply shock, but challenges and complexity emerge

for all links in the credit value chain

Credit value chain Key challenges emerging from the crisis

Client acquisition Surge in number of clients seeking credit, favoring large banks that serve as a “first stop shop”, which results in

= Favors the large adverse selection for other players

Change in customer profile, mix, and the new macroeconomic scenario mean that credit models and policies used

Credit decision

during “business as usual” are much less accurate in predicting credit performance – lenders needs a COVID-19

= Less accurate

playbook

Funding Higher uncertainty and complexity causes investor confidence to go down and shifts capital to safer assets,

= More expensive increasing funding costs, with strong impact for fintechs and smaller lenders who are Balance Sheet-constrained

Increase in delinquent volume is driven by constraints in the capacity to repay (rather than unwillingness to pay

Collections

from borrowers), which makes debt collection efforts ineffective – particularly in a moment where “hard”

= Less effective

collection is not advised

Customer service Strong, broad-service digital channels are even more necessary now, given unavailability/sanitary risks of brick-

= More digital and-mortar channels, associated with potential operational challenges to call centers

© Oliver Wyman 24FIRST SIGNS OF COVID-19 IMPACT IN THE CORPORATE CREDIT PORTFOLIO

June 2020 data already showed a considerable impact on the corporate portfolio, with a peak due to FX in March, followed by a relevant decrease in all

lines except working capital

Covid-19 impact on Corporate credit portfolio

Originations: Dec/19 to Jun/20 Balance: Dec/19 to Jun/20 Arrears and defaults: Dec/19 to Jun/20

Indexed Dec/19=100 Indexed Dec/19=100 % of balance

Peak in May

220% driven by FX 40% 2,7% 2,6%

(ACC1 and

200% 35% 2,6%

Export

Financing) 30% 2,5%

100% 2,4% 2,4%

2,3% 2,3% 2,3%

25% 2,4%

80%

20% 2,3%

60% 2,2%

15% 12% 2,2% 2,1% 2,1%

40% 9% 2,1%

10% 2,1%

15%

20%

5% 2,0% 2,0%

0% 1,9%

0% 1,9%

-20%

-25% 1,8%

-5% 1,8% Covid-19 effects on

-40% -10% 1,7% credit quality still not

-60% realized – decrease due

-15% 1,6%

to government stimuli

-80% -20% 1,5% and lower origination 1,4%

-100% -25% 1,4%

Total CC factoring Overdrafts Export financing Arrears 15-90 days

Factoring Working capital ACC1 Other Defaults

1. “Adiantamento de contrato de câmbio” – FX contract anticipation. Source: Banco Central do Brasil; Bank earnings releases

© Oliver Wyman 25FIRST SIGNS OF COVID-19 IMPACT IN THE CONSUMER CREDIT PORTFOLIO

For consumers, there was a fall on credit volumes driven mostly by credit cards, due to lower transaction levels; effects in credit quality still not realized

Covid-19 impact on Consumer credit portfolio

Originations: Dec/19 to Jun/20 Balance: Dec/19 to Jun/20 Arrears and defaults: Dec/19 to Jun/20

Indexed Dec/19=100 Indexed Dec/19=100 % of balance

5,6%

5% 12% 5,6% 5,5%

10% 5,4% 5,3%

0% 8% 5,2%

5,2% 5,1%

6% 5,0%

4,9%

5,0% 4,9%

-5% 4% 4,8%

2% 4,8%

2%

4,6% 4,6%

-10% 4,6%

0% 4,4%

4,4% 4,3%

-15% -17% -2% -1%

-4% 4,2%

4,0%

-6% 4,0%

-20% -22%

-8%

3,8% Covid-19 effects on

-25% -10%

3,6% credit quality still not

-12% realized – decrease due

-14% 3,4%

-30% to government stimuli

-16% 3,2% and lower origination

-35% -18% 3,0%

Total Personal loans Others Arrears 15-90 days

Overdrafts Credit cards Defaults

Source: Banco Central do Brasil; Bank earnings releases

© Oliver Wyman 26FIRST SIGNS OF COVID-19 IMPACT ON BANK PROVISIONS AND MARGINS

Large financial institutions have already anticipated some of the expected increase in losses in their provisions

Provisions Financial margin with clients

R$ BN R$ BN

% change % change

Q1’20 / Q4’19 Q1’20 / Q4’19

12 19

11 18

10,4 69% 17,0

17 -6%

10

16 15,3

9

15

8 14

13,0 0%

7 6,7 69% 13

6 6,5 34% 12

5,4

11 11,3

5

4,1 10 9,2 -4%

4 3,9 3,4 15% 9

3 2,7 7,5 -21%

8 8,5

2 7

1T18 3T18 1T19 3T19 1T20 1T18 3T18 1T19 3T19 1T20

Bradesco Santander Itaú BB

Source: Banco Central do Brasil; Bank earnings releases

© Oliver Wyman 27BRAZILIAN BANKS LIKELY TO WITHSTAND SHOCK, WITH HIGH SPREADS SUFFICIENT TO

SUSTAIN CAPITAL RATIOS DESPITE SHARP REDUCTION IN ROE

Starting point Projected impact of pandemic scenarios for major banks

~23% "Smart & Lucky“ scenario "Winter Return“ scenario

Sustainable ROE reduction (%) Sustainable ROE reduction (%)

~18%

0% 5% 10% 15% 20% 5% 10% 15% 20%

0% E2 0%

1% E5 1%

CET 1 Depletion (%)

CET 1 Depletion (%)

E3 E4

2% 2% E5

~6% E1 E2 E3

3% 3%

4% 4% E1 E4

5% 5%

6% 6%

Net interest income

Return on equity

Regulatory capital

(%)

(%)

(%, before tax)

7% 7%

Above Threshold Below Capital Conservation Buffer

Source: Worldbank, Banks’ public fillings, Oliver Wyman analysis

© Oliver Wyman 2804

REPORT FROM

AUSTRALIA

Nicholas Tonkes

Partner, Risk & Public

PolicyMACRO IMPACT: OLIVER WYMAN DEVELOPED 5 POTENTIAL SCENARIOS – OUTCOME

LIKELIHOODS HAVE EVOLVED OVER RECENT MONTHS

Scenarios and likelihoods Observations

March April May June

• Continued downgraded of macro forecasts from March

V shape recovery and April as the pandemic spread and lockdown measures

0 70% 0% 0% 0% intensified

U shape recovery • Economist initially anticipated a V-shape recovery (quick

1 30% 20% ~0% ~0% elimination of the virus) as baseline and U-shape (longer

elimination) as the downside scenario

Vw shape recovery

• Following considerations of potential further outbreaks,

2 0% 35% 60% 70%

seasonality effect and gap from herd immunity, Vw & VW-

shape recoveries emerged as likely options replacing the

VW shape recovery V-shape

3 0% 45% 40% 30%

• The recent flattening of the curve, increase in testing &

L shape recovery tracing capacity, and rapid economic reopening have

4 0% 0% 0% 0% increased the likelihood of a Vw shape recovery

• This in turn, is also reflected in the slight improvements in

Average forecasts (fortnightly)1 09/03 23/03 06/04 20/04 04/05 18/05 01/06 macroeconomic forecasts

GDP growth YoY % 0.1 -1.2 -4.1 -5.0 -5.0 -5.1 -4.2

Unemployment rate % 5.8 6.3 8.3 8.4 8.5 8.2 8.0

Source: AMP, ANZ, CBA, Fitch, JP Morgan, Morgan Stanley, NAB, Oxford Economics, UBS, Westpac

© Oliver Wyman 30MACRO IMPACT: DIFFERENCE BETWEEN SCENARIO 2 AND 3 IS DRIVEN BY THE

EFFECTIVENESS OF CONTAINMENT MEASURES IN SUPRESSING FURTHER OUTBREAKS

Scenario 1 Scenario 2 Scenario 3

Elimination over longer period 2020–21 Additional outbreaks contained in 2020 Additional outbreaks over 2020–21

(U shape) (Vw shape) (VW shape)

Economic impact

Likelihood: ~0% Likelihood: ~70% Likelihood: ~30%

Recovery shape

• 6–12 months: Phased reopening of the economy by • 3–4 months: Rapid reopening of the economy • 3–4 months: Rapid reopening of the economy

sector/region • 4–18 months: Additional wave(s) of virus addressed by • 4–18 months: Additional wave(s) of virus beyond health

• 12–18 months: International arrivals/immigration smart containments system capacity, requiring additional lockdowns

resumes • 12–18 months: International arrivals/immigration • 12–24 months: International arrivals/immigration

• GDP YoY drops 10% and unemployment peaks at 12% in resumes resumes

2020 driven by prolonged restrictions, with rapid • GDP YoY drops 7% and unemployment peaks at 10% in • GDP YoY drops 10% and unemployment peaks at 12% in

recovery in 2021 2020, with slower recovery in 2021 due to outbreaks 2020, with slow recovery in 2021–22 due to further

• HPI drops 20% in 2020 as unemployment peaks and • HPI drops 10% in 2020 as consumer uncertainty is offset outbreaks

foreign demand reduces, followed by gradual recovery in by return to employment, recovery in 2021–22 • HPI drop of 25% in 2020 due to high unemployment peak

2021–22 and consumer uncertainty, slow recovery in 2021–22

© Oliver Wyman 31MACRO IMPACT: IMPACTS ARE HEAVILY INFLUENCED BY THE COVID-19 R0, DRIVEN BY

PATHOLOGICAL & PUBLIC HEALTH CHARACTERISTICS

Vw-shape baseline and VW-shape pessimistic scenarios Anticipated

Return to BAU/ government response

Initial outbreak 12+ months suppression/ containment New normal

5,000 Full lockdown

• The intensity of subsequent lockdowns

required is driven by the R0

4,000 (reproductive rate of the virus)

ACTIVE CASES (#)

• R0 is highly sensitive to the

pathological characteristics of Covid-19 Ban public events

3,000 (e.g. seasonality, herd immunity) and • Resurgence of Covid-19 is more likely

public health characteristics (e.g. scale during winter due to the potential

& sophistication of testing/tracing) seasonality effect of the virus

School closure

2,000 • There is still high uncertainty around • Further advancements in public

the future effectiveness of containment health tools is likely to lead to more

measures despite ongoing effort controlled outbreaks Social distancing

1,000

Self isolation

0

2020 Q1 2020 Q2 2020 Q3 2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1 2022 Q2 2022 Q3 2022 Q4

10 YoY growth QoQ growth

GDP GROWTH (%)

5

0

-5

YoY GDP worsens from 7% to 12% if a

-10

further lockdown is required this year

-15

2020 Q1 2020 Q2 2020 Q3 2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1 2022 Q2 2022 Q3 2022 Q4

Vw-shape VW-shape

© Oliver Wyman 32SECTOR IMPACT: IMPACT ON THE ECONOMY VARIES BY SECTOR, WITH RESILIENCE IN

SOME KEY SECTORS SUCH AS MINING, CONSTRUCTION AND PROF. SERVICES

Australian GVA by Industry, H1-20 impact of COVID-19

$BN

200 Mining

172 Fin services

146 Construction

Healthcare sector 143 Health Care & Social Assistance

has been significantly

impacted by the 137 Prof. Services

replacement of high 112 Manufacturing

margin elective care 104 Public Admin

with lower margin

COVID care 93 Education and Training

93 Transport & Warehousing

81 Retail Trade

74 Wholesale Trade

69 Admin & Support Services

Large (200+ employees) Subsector impacts vary 57 Rental & Real Estate Services

SME (SECTOR IMPACT: THE PACE AND EXTENT OF RECOVERY ALSO DIFFERS BY SECTOR,

LASTING CHANGES EXPECTED IN HEAVILY IMPACTED SECTORS…

Sector recoveries (based on Vw-shape baseline scenario)

Gradual recovery to new

normal as international

borders open and consumer

confidence recovers

Temporary reinforcement

of restrictions during Real estate

second outbreak Healthcare

Construction

Accom. & food

Lifting of restrictions in June and

reopening of interstate borders in Retail Trade

September drives sector recovery Mining

H1-20 H2-20 H1-21 H2-21 H1-22 H2-22

Industry activity w.r.t pre-COVID levels 90% Inflection point

© Oliver Wyman 34STATE IMPACT: IMPACT AND RECOVERIES DIFFER ACROSS AUSTRALIA, DRIVEN BY

SECTOR SKEW TO SERVICES AND FOREIGN DEMAND

Impact of COVID-19 by state

Gross value added $BN, (% of contribution from services sectors)

WA non-service sector QLD swift recovery when interstate

resilience (incl. mining, agri) borders open due to high interstate

reducing impacts tourism

13% of tourism expenditure 19% of tourism expenditure from

from foreign sources foreign sources

27% education expenditure 37% education expenditure from

from foreign sources foreign sources

4.9% in underemployment rate

$308 BN

4.0% in underemployment rate

(76% services)

$235 BN

SA (56% services) NSW recovery prolonged by high

14% of tourism expenditure $90 BN reliance on foreign demand

from foreign sources (83% services) compared to other states

33% education expenditure $508 BN 27% of tourism expenditure from

foreign sources

from foreign sources (88% services)

5.2% in underemployment rate 44% education expenditure from

foreign sources

4.6% in underemployment rate

VIC recovery prolonged by high reliance on foreign demand compared to other states

37% of tourism expenditure from foreign sources $379 BN Impact measure

46% foreign education expenditure foreign sources (88% services) $27 BN High

(78% services)

5.7% in underemployment rate Moderate

1. Underemployment rate increase from March to April, measure used over unemployment rate due to JobKeeper programme artificially lowering the impact on unemployment rate Low

Sources: ABS - Australian System of National Accounts, 2018-19, Gross Value Added (GVA) by Industry, Parliament of Australia, AUSTrade, Victoria University’s Mitchell Institute

© Oliver Wyman 35MAJOR BANKS HAVE INCREASED PROVISIONING (+40% ON AVERAGE) TO ACCOUNT FOR

THE IMPACT OF COVID-19 AND DEFERRED / REDUCED DIVIDEND PAY-OUTS

Impact of COVID-19 on collective provisioning Banks responses

$M

COVID overlay

COVID overlay/ Pre- H1-20 CP post • Decision to payout dividend at 30c per share (vs.

Bank Report date Weighted Base Severe COVID CP COVID 83c in 2019 final)

27 April 807 363 3,827 22% 4,401 • 51% decline in profits to $1.4 BN

• $3.5 BN capital raising to boost Tier 1 Capital to

30 April 1,031 849 3,002 30% 4,501 11.2%

4 May 1,581 291 3,717 44% 5,182

• Decision to defer dividend (vs. 80c paid in 2019

8 May 582 441 941 61% 1,541 final)

• 60% decline in profits to $1.4 BN

13 May 1,500 Not published 31% 6,400

Impairment charge as % of GLA 3Q20 update figures • Decision to defer dividend (vs. 80c paid in 2019

used, reflective of final)

H2-19 H1-20 COVID impacts • 70% decline in profits to $993 MM

+400%

308% 377% • Decision to payout dividend at $1.80 per share

145%

138%

0.80 (vs. $2.50 in 2019)

0.53 0.62 • 8% decline in profits to $2.7 BN

0.49

0.38

0.16 0.13 0.13 0.20 0.16

• Dividend payments to be reviewed as part of the

1 usual year-end process

1. Westpac results includes AUSTRAC charges

Source: Bank annual and interim reports, media reports

© Oliver Wyman 36COVID-19 RELATED PAYMENT DEFERRALS ARE SIGNIFICANT IN SIZE ACROSS ALL MAJOR

BANKS

Loans deferred1 ($B) Total loans ($B) Deferred home loans by LVR

Report

Bank date Home Business Total Home Business2 Total3

14% 8%

27 April 27 17 44 302 174 619 14%

38% 38%

15%

30 April 36 8 44 264 54 661

4 May 39 8 47 497 122 720

40%

33%

13 May 50 15 65 480 141 770

90%

Loan deferred as a % of total loan value Deferred business loans by sector

14% 14%

13%

12% 23% 20%

26%

31%

9% 9%

8% 8% 4%

7% 7% 7% 7%

3%

18% 8%

15% 10%

13%

6% 9% 11%

Property Healthcare Retail & wholesale Construction

Home loans Business loans Total loans Accom/Food Manufacturing Agri Other

Source: Banks’ latest interim reports;

1. Loan deferred are approved figures for NAB, Westpac, and requested figures for ANZ and CBA; assumption that vast majority of deferrals will be approved;

2. Total loans for business excludes corporates and institutional banking and non-Australian entities; 3. Total includes institutional and non-Australian loans

© Oliver Wyman 37ALL MAJOR BANKS HAVE STARTED MOBILIZING THEIR “CUSTOMER IN DIFFICULTY”

PROGRAMME AMID CONCERNS EQUITY VALUES WILL BE DEPLETED

COVID-19 relief provided by Australian banks1 Banks responses

As of 12 June

772,616 For some business owners, the smartest thing for them to do is to

Total number of COVID-19 loan deferrals wind it up now, and walk away with some equity…

(480,727 mortgages and 215,441 business loans) We have begun resourcing "workout" and restructuring

specialists and would be proactively contacting businesses to

help them arrive at the right solution

$234 BN Mark Hand, Head of retail and business banking

Total value of loans deferred

We recognise that customers may require alternative temporary

assistance measures to help them get back on their feet sooner…

$118 BN We are temporarily allowing existing home loan customers to

New business lending apply for a one-year interest only extension or switch if they are

currently making principal and interest repayments without

Benchmarking of number of loans deferred2 requiring a serviceability assessment

K 215 Angus Sullivan. CBA Group Executive

Eligible customers making interest-only payments will be able to

147 71

136 extend that IO period for up to 12 months, while customers

104 42 31 making principal and interest payments will be able to make the

34 switch to interest-only payments for the same period

144

105 105

70

We are adding 500 staff to our support team to help with

the check-in process and will call customers instead of using

digital communications “to gain a deeper understanding of

Business Mortgages their situation”

Rachel Slade, Chief Customer Experience Officer

1. Australian Banking Association, bank loan deferrals commenced 22nd March 2020; 2. Banks’ latest interim reports

© Oliver Wyman 38THANK YOU; POST-WEBINAR LOGISTICS; Q&A

Contact us

Til Schuermann

Til.Schuermann@oliverwyman.com

Helen Leis

Helen.Leis@oliverwyman.com

Nuno Monteiro

Nuno.Monteiro@oliverwyman.com

Nicholas Tonkes

Nicholas.Tonkes@oliverwyman.com

© Oliver Wyman 39READ OUR LATEST INSIGHTS ABOUT COVID-19 AND ITS GLOBAL IMPACT ONLINE Oliver Wyman and our parent company Marsh & McLennan Visit our dedicated COVID-19 website: (MMC) have been monitoring the latest events and are putting https://www.oliverwyman.com/coronavirus forth our perspectives to support our clients and the industries they serve around the world. Our dedicated COVID-19 digital destination will be updated daily as the situation evolves © Oliver Wyman 40

QUALIFICATIONS, ASSUMPTIONS, AND LIMITING CONDITIONS This report is for the exclusive use of the Oliver Wyman client named herein. This report is not intended for general circulation or publication, nor is it to be reproduced, quoted, or distributed for any purpose without the prior written permission of Oliver Wyman. There are no third-party beneficiaries with respect to this report, and Oliver Wyman does not accept any liability to any third party. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been independently verified, unless otherwise expressly indicated. Public information and industry and statistical data are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information. The findings contained in this report may contain predictions based on current data and historical trends. Any such predictions are subject to inherent risks and uncertainties. Oliver Wyman accepts no responsibility for actual results or future events. The opinions expressed in this report are valid only for the purpose stated herein and as of the date of this report. No obligation is assumed to revise this report to reflect changes, events, or conditions, which occur subsequent to the date hereof. All decisions in connection with the implementation or use of advice or recommendations contained in this report are the sole responsibility of the client. This report does not represent investment advice nor does it provide an opinion regarding the fairness of any transaction to any and all parties. In addition, this report does not represent legal, medical, accounting, safety, or other specialized advice. For any such advice, Oliver Wyman recommends seeking and obtaining advice from a qualified professional.

You can also read