What's next for the commodities stories? - First State Investments

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

What’s next for the commodities stories?

Joanne Warner Head of Global Resources

Renzo Casarotto Senior Portfolio Manager

What’s happened in resources

Is it over for resources? Source: http://www.theaustralian.com.au/business/markets/stocks-down-as-resources-companies-tumble/story-e6frg916-1226623371985 http://money.msn.com/investing/commodities-crash-recession-looms http://finance.ninemsn.com.au/newsbusiness/motley/8644071/asx-climbs-but-leaves-resources-behind http://www.news.com.au/business/markets/resources-companies-to-weigh-on-asx/story-e6frfm30-1226620458088 http://economictimes.indiatimes.com/markets/commodities/copper-weakens-in-futures-trade-global-cues-subdued-demand/articleshow/19675158.cms 3

Is this the GFC - Mark II?

MSCI sector performance YTD (Rebased to 100)

120

110

100

90

80

70

Dec 12 Jan 13 Jan 13 Feb 13 Feb 13 Mar 13 Mar 13 Apr 13 Apr 13 May 13 May 13

MSCI World Index MSCI World Energy Sector Index

MSCI World Metals & Mining Index MSCI World Health Care Index

MSCI World Financials Index MSCI World Information Technology Index

MSCI World Consumer Discretionary Index MSCI World Consumer Staples Index

MSCI World Telecom Service Sector Index

Source: Bloomberg. 31 May 2013. 4

Chinese GDP - it’s the absolute numbers that count

GDP growth year on year

13.0%

12.0%

11.0%

10.0%

9.0%

8.0%

7.0%

6.0%

5.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

GDP ($US bn)

9,000

8,000

7,000

6,000

$Usbn

5,000

4,000

3,000

2,000

1,000

-

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: Bloomberg , May 2013 & CLSA April 2013. 5

It’s the absolute numbers that count

Chinese oil consumption (million bbls/d)

12.0

11.0

10.0

9.0

8.0

7.0

6.0

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Crude oil processed + net product imports

m bpd

11.0

10.0 Note the continual

9.0 increase y-y,

8.0 despite a notional

7.0 slow down in

6.0 growth rates

5.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009 2010 2011 2012 2013

Source: CLSA April 2013. 6

China’s current five year plan requires more infrastructure

80

70

60

50

40

30

20

10

0

Railway Highway Oil/Gas Pipe Airports

(thousand km) (ten of thousand km) (thousand km) (number of)

Previous five year plan Current five year plan

Source: Standard Chartered Resources, April 2013. 7

US Housing construction ‘upside’

Listed for sale homes per house hold

• Housing inventories at long term lows

• Vacancy rates nearing 2003 levels

• Construction jobs steady but hours up

Homeowner vacancy rate (%) US rental vacancy rate (%)

Source: Bloomberg; US Census Bureau; Stifel Nicolaus report, financial institutions, housing economics

market commentary. As at December 19, 2012. 8

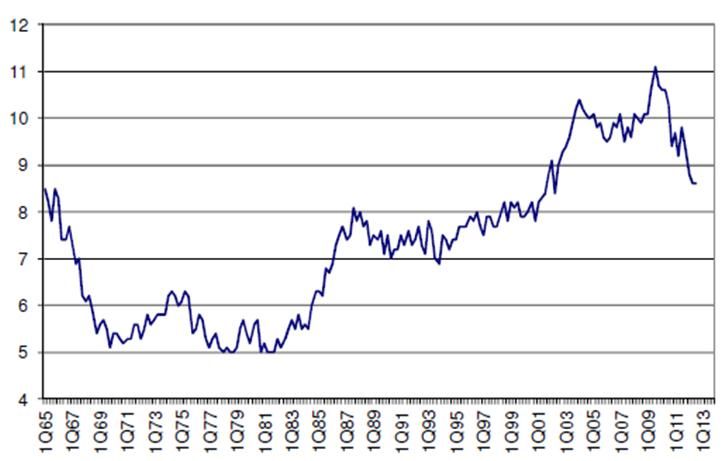

A progressive dividend policy, scope to increase

BHP - Annual dividend (1990-2012), 11.4% CAGR BHP - Dividend Payout Ratio (1990-2012)

1.4

3.0

1.2

2.5

1.0

2.0

0.8

0.6 1.5

0.4 1.0

0.2 0.5

0.0 0.0

Jan-90

Jan-92

Jan-94

Jan-96

Jan-98

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08

Jan-10

Jan-12

Jan-90

Jan-92

Jan-94

Jan-96

Jan-98

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08

Jan-10

Jan-12

DPS average payout

RIO - Annual dividend (1996-2012), 7.4% CAGR RIO - Dividend Payout Ratio (1996-2012)

2.5 0.7

2.0 0.6

0.5

1.5 0.4

1.0 0.3

0.2

0.5 0.1

0.0 0

Apr-00

Apr-05

Apr-10

Oct-97

Feb-01

Oct-02

Feb-06

Oct-07

Feb-11

Oct-12

Dec-96

Aug-98

Dec-01

Aug-03

Dec-06

Aug-08

Dec-11

Jun-99

Jun-04

Jun-09

Oct-98

Apr-04

Oct-09

May-03

Jul-01

Mar-05

Feb-06

Jul-12

Dec-96

Nov-97

Sep-99

Aug-00

Dec-07

Nov-08

Sep-10

Aug-11

Jun-02

Jan-07

ave payout payout

DPS

Prior to 1995, Rio was operating as two independent businesses CRA and RTZ.

In 2005 a $1.45ps ($1.15ps adjusted) special dividend was declared.

In 2009 no interim dividend was declared.

Source; Goldman Sachs. 9

Where to from here?

Iron ore – is the world too bearish?

China's Iron Ore Imports vs Spot Iron Ore Price

80 250

70

200

60

Million tonnes

US$/tonne

50 150

40

30 100

20

50

10

0 0

2006 2007 2008 2009 2010 2011 2012 2013

China's Iron Ore Imports, Mt Spot Iron Ore, US$/t (RHS)

Source: Morgan Stanley Research, CRU. February 2013. Source: Source: Bloomberg. May 2013. 11Iron ore – why would BHP and RIO talk the price down?

140

120

cash cost of production (US$/t fob)

100

China

80

Australia

Brazil

60

40

20

0

0 300 600 900 1,200 1,500 1,800

cumulative production (Mt)

2013 cash cost curve 50th centile 75th centile

90th centile spot (fines) 3-Jun-13 LT (incentive) price

Source: Metalytics. June 2013. 12So where’s the supply?

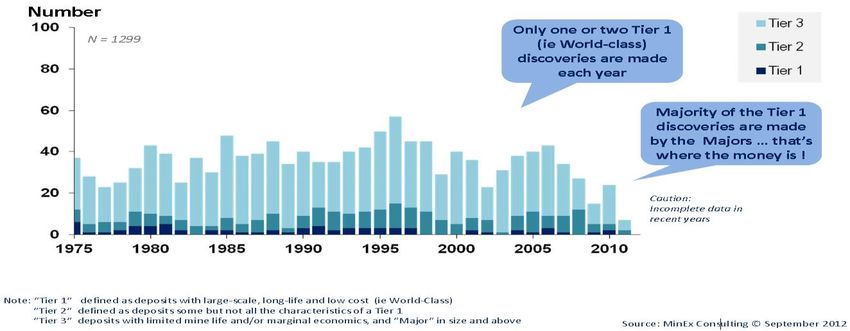

Exploration spend by commodity: 1998-2012 Number of deposits found – by quality

Copper: most of the metal in a handful of deposits

• Exploration spend has increased dramatically

• But why do we keep looking for gold??

• Success rates have declined

• More than half of deposits are being found in high-

political risk locations

• On average it takes 12-18 years from discovery to

first production

Source: MinEx Consulting – presentation to BBY Resources Conference, November 2012. 13Copper: Bingham Canyon – before the pit-wall failure… Source: First State Investment, as at September 2012. 14

And after the pit wall failure April 10, 2013

• Still unknown how much production will be

lost, but early estimates are 100-150kt Cu

• NB: pre-incident estimates were for an

over-supply in the Cu market of ~150kt

this year

• Cost? Equipment alone could be $100m

Source: First State Investments. Rio Tinto May 2013. 15Valuations – but is it cheap?

Mining vs MSCI World (P/E 2013 F1)

P/E FY1

30.0

HSBC Mining MSCI World (MXWO Index)

25.0

20.0

15.0

10.0

5.0

0.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Historical and Mean P/E FY1 Ratio (Index 1/Index 2) Relative Valuation

1.80 Mean +/- 1.96 Standard Deviations

1.60

1.40

1.20

1.00

0.80

0.60

0.40

0.20

0.00

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Source: Nomura Custom Products Group – data to 31 May 2013. 16Valuations – but is it cheap?

Energy vs MSCI World (P/E 2013 F1)

P/E FY1

25.0

MSCI Energy (MXWO0EN Index) MSCI World (MXWO Index)

20.0

15.0

10.0

5.0

0.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Historical and Mean P/E FY1 Ratio (Index 1/Index 2) Relative Valuation

Mean +/- 1.96 Standard Deviations

1.20

1.00

0.80

0.60

0.40

0.20

0.00

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Source: Nomura Custom Products Group – data to 31 May 2013. 17The resources cycle

Phase 1

Demand rises

Inventories decline

Supply response lags = higher prices

Governments attempt to raise taxes

Phase 2

Phase 3 High prices encourage new projects

Supply response = demand

Supply is curtailed

Inventories rise = prices fall

Demand normalises

Capital expenditure is reduced

Producers benefit from recovery

18What about agribusiness?

Agriculture: hitting the headlines http://news.nationalgeographic.com/news/2013/13/130412-drought-great-plains-weather-environment/ http://www.reuters.com/article/2012/11/29/usa-drought-idUSL1E8MT5H220121129 http://www.merredinmercury.com.au/story/1433588/hundreds-of-people-gather-for-agriculture-crisis-meeting-in-merredin/?cs=1478 http://www.treehugger.com/climate-change/us-drought-going-get-worse.html http://www.agriculture.com/news/crops/wld-crop-wear-wries-abound_2-ar31103 20

Strong EM wages growth to drive consumption

China wages growth Brazil wages growth

Brazil average monthly wage (BRL)

45,000

40,000

China average wage (RMB)

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

Source: Ministry of Human Resources and Social Security, Nomura, data to Dec 2011.

Bloomberg, CEIC, Nomura, data to 31 May 2012. 21Growing demand for soft commodities

GROWING POPULATION & CONVERGING DIETS INCREASED MEAT

URBANISATION

6.5bn to 9bn by 2050

+ 40kg to 52kg by 2050

= CONSUMPTION

260mt to 470mt by 2050

70% urbanised by 2050

Source: FAO How to feed the world in 2050 report, UN World Urbanization Prospects 2009 revision. 22What does this mean for grain demand?

In 2050 Mt meat required Conversion ratio Mt grain required

Chicken 274 2 549

Beef 70 7 487

Pork 101 4 402

Sheep 25 4 102

TOTAL 470 1,540

mt

+85%

Source: OECD-FAO Agricultural Outlook 2012-2021, FAO how to feed the world in 2050

report. Consumption split is 58% chicken, 15% beef, 22% pork, 5% sheep. 23Middle East, Africa, and Asia consumption rising rapidly World’s Food Surpluses and Deficits Net trade (Million tonnes) Source: The Economist, * Cereals, rice, meals, oils and fed equivalent of meat. 24

The global food challenge… The task: • Increase global food production by 70% • Which requires $US80 billion per annum of investment The challenges: • Resource constraints (land/water) • Environmental pressures • Natural disasters • Productivity growth declining Source: FAO, How to feed the world 2050 Report. 25

How can investors participate in the solution?

The solution: Better agronomic practises

• Increased yields Balanced fertilizer application

• Increased crop intensity Improvements in innovation (i.e. seeds)

• Increased animal intensity Infrastructure investment

• Added acreage Farm economies of scale

26Agricultural value chain

Inputs Farming/ Handling/ Food Supermarkets/

Processors

plantation traders companies consumers

• seed • farm • storage • oilseed • Nestle • Tesco

• crushing • Kellogg’s • Walmart

• fertiliser • forestry/pulp handling

• • biofuels • Kraft • Sainsbury

• machinery • palm oil trading

• marketing • livestock • Waitrose

• paper

Upstream Midstream Downstream

• We invest in the upstream and midstream portion of the agricultural value chain

• Upstream resource owners tend to make the highest margins

Reference to specific securities (if any) is included for the purpose of illustration only and should not be

construed as a recommendation to buy or sell the same. 27Agricultural equity returns versus

agricultural commodity price returns

300

250

+125%

200

150

100

-18%

50

0

DAXglobal Agribusiness Index Rogers International Commodity Agriculture Index

Source: First State Investments, Bloomberg, USD from June 2005 to 30 April 2013;

standardised as at 30 June 2005. 28Valuations – agriculture Agriculture vs MSCI World (P/E 2013 F1) Source: Nomura Custom Products Group – data to 30 April 2013. 29

Valuations – forestry

Forestry vs MSCI World (P/E 2013 F1)

40.0

35.0

30.0

25.0

20.0

15.0

10.0

S&P Timber MSCI World (MXWO Index)

5.0

0.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

2.50

2.00

1.50

1.00

0.50

0.00

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Source: Nomura Custom Products Group – data to 31 May 2013. 30Returns and volatility by equity sector

18.0%

16.0%

14.0% China

Soft Commodity Equities

12.0%

Consumer Staples Emerging Markets

10.0% Global Mining

Return

8.0% Health Care Materials

Consumer Discr

Energy

6.0% Industrials

Utilities Telecom Svc

4.0% Global Bond Information Tech

2.0% Global Equities

0.0% Financials

-2.0%

5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

Risk

Global Mining Soft Commodity Equities Global Equities Energy

Materials Industrials Consumer Discr Consumer Staples

Health Care Financials Information Tech Telecom Svc

Utilities Emerging Markets China Global Bond

Source: Data used from 01 January 2005 to 31 March 2013 in USD. Rimes; First State Investments; Global Mining: HSBC Global Mining Accumulation Index; Energy: MSCI

AC World Energy Index; Materials: MSCI AC World Materials Index; Global Equities: MSCI AC World Index; Global Agribusiness: 75% DAX Global Agribusiness Index & 25%

S&P Global Forestry & Timber Index; Emerging Markets: MSCI Emerging Markets Index. Past performance is no indication of future performance.

31Look beyond the headlines Source: http://www.theaustralian.com.au/business/markets/stocks-down-as-resources-companies-tumble/story-e6frg916-1226623371985 http://money.msn.com/investing/commodities-crash-recession-looms http://finance.ninemsn.com.au/newsbusiness/motley/8644071/asx-climbs-but-leaves-resources-behind http://www.news.com.au/business/markets/resources-companies-to-weigh-on-asx/story-e6frfm30-1226620458088 32 http://economictimes.indiatimes.com/markets/commodities/copper-weakens-in-futures-trade-global-cues-subdued-demand/articleshow/19675158.cms

Disclaimer

Before making any investment decision based upon the information contained in this presentation, you should assess your own

position, and if appropriate, seek the assistance of a financial adviser.

The information contained within this presentation has been obtained from sources that First State Investments (“FSI”) believes to

be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness,

accuracy, completeness or correctness of the information. Neither FSI, nor any of its associates, nor any director, officer or

employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this. It does not constitute

investment advice and should not be used as the basis of any investment decision, nor should it be treated as a recommendation for

any investment. The information in this presentation may not be reproduced in whole or in part without the prior consent of FSI.

This document shall only be used and/or received in accordance with the applicable laws in the relevant jurisdiction.

Please remember that the value of investments and the income from them may go down as well as up and that you may not get

back your original investment. Investment involves risks, past performance is not necessarily a guide to future performance. Due to

the nature of the funds, short-term volatility is expected and your investment should be viewed as long-term. Please refer to the

offering documents for details, including the risk factors.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a

recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First State

Investments’ portfolios at a certain point in time, and the holdings may change over time.

This presentation is issued by First State Investments (Hong Kong) Limited and has not been reviewed by the Securities and

Futures Commission in Hong Kong.

33You can also read