3i Capital Markets Seminar - 18 March 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

3i Capital Markets Seminar 18 March 2021

Action story enhanced by 2020 performance

Action – 3i carrying value, £m1

✓ Discount retail sector has proven resilient during the

pandemic Carrying valuation 4,426

• Increasing customer acceptance of discount retailing

• Evergreen attraction of low price focused SKU model

3,536

✓ Customer value proposition has strengthened

• Core essentials range underpins Action's importance in customers’ day to day lives 2,731

• Maintenance of high sales volumes and superior sales densities

• ASR and digital journey accretive to proposition 2,064

1,708

✓ Outstanding depth of performance across geographies

• Successful scaling of Germany and Poland complements continued strength in

Netherlands and France 902

592

• White space opportunity remains significant 501

280

143

✓ Conviction in enduring compounding benefit to 3i

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 Q3

FY21

(1) 3i financial years

2

Submitting questions

Click here

3

Today’s presenters

Sander van der Laan Joost Sliepenbeek

Chief Executive Officer Chief Financial Officer

Joined in October 2015 Joined in November 2018

30 years of Consumer & Retail experience 20 years of Consumer & Retail experience

Various positions at Ahold (1998 – 2015) 33 years experience in finance, 21 years as CFO

‒ CEO Albert Heijn (2011 – 2015) ‒ CFO Vion (2015 – 2018)

‒ COO Ahold Europe ‒ CFO Van Gansewinkel (2013 – 2015)

‒ General Manager Albert Heijn ‒ CFO C1000 (2009 – 2012)

‒ CEO Giant Food Stores (Ahold USA) ‒ CFO HEMA (2007 – 2009)

‒ EVP Marketing & Merchandising Albert Heijn ‒ CFO Albert Heijn (1999 – 2003)

‒ General Manager Gall & Gall ‒ Various positions at Ahold (1994 – 2007)

4 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Agenda 1. Introduction Simon Borrows 2. Business performance 2020 Sander van der Laan 3. Strategy update Sander van der Laan 4. Financial performance 2020 Joost Sliepenbeek 5. Trading update Sander van der Laan 6. Wrap Up Simon Borrows 5 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Despite the pandemic, 2020 was another year of strong

performance and continued investment for the future

€5,569 (1.4)% €609 164 76%

Million Like-for-like Million New stores Cash

net sales sales Operating opened conversion1)

+8.9% EBITDA1)

+12.4%

+10.4%

normalised

Significant growth and investment in future achieved

despite disruption from the pandemic

6 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Note: all 2020 figures based on 52 weeks unless explicitly referenced to 53 weeks financials 1) Excluding CAPEX for new DCs

Our high growth track record continues

Net sales (€m) Operating EBITDA (€m)

5,569

+24% 5,114 609

+24%

4,216 541

3,418 450

2,675 387

1,995 310

1,506 226

166

2014 2015 2016 2017 2018 2019 2020 2014 2015 2016 2017 2018 2019 2020

Store expansion (numbers) & # countries LfL sales growth (%)

10.4%1)

+ on average 200 p/y 1,716

1,552 7.6%

1,325 7.2% 6.9%

1,095 5.3% 5.6%

852

655 3.2%

514

# of

#4 #6 #6 #7 #7 #7 #8 countries

2014 2015 2016 2017 2018 2019 2020

(1.4%)

2014 2015 2016 2017 2018 2019 2020 2020

normalised

7 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 1) Weeks 12 to 22 and weeks 44 to 52 normalised. Please see slide 51 and 52 for further details

LfL throughout 2020 – strong underlying performance

Period 1 and 2 Period 3 to 5 Period 6 to 10 Period 11 and 12 FY

Lockdown 1 Lockdown 2

Very strong start Store closures and/or All stores open selling full assortment. Supply chain Store closures and/or

assortment restrictions across disruption resulted in some availability issues and assortment

all markets except the NL impact on sales restrictions impacted

FR, BE, AT in P11 and

NL, DE, AT in P12

17.4%

11.0% 11.6% 13.3% 12.2%

8.6% 6.6%

1.3%

(1.4%)

(10.6%) (13.4%)

(19.8%)

(61.2%)

P1 P2 P3 P4 P5 P6 P7 P8 P9 P10 P11 P12 Total

8 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Covid-19 dominated the year

First priority: safety of our customers and employees

Implemented door policy to control customer inflow

Additional store labour and cleaning costs

Strict protocols and measures in place (screens, face masks, safety

vests, sprays, hand gels etc.)

Working from home policy in place for all offices

Only essential travel allowed

9 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Covid-19 interrupted our operations,

however business plan not at risk

Scaling down supply chain temporarily interrupted service levels and

product availability

Store expansion and new countries slowed down in first half

Strong focus on cash management

Financial performance remained strong

2023 business plan not at risk

10 ACTION | 3I CAPITAL MARKETS SEMINAR 2021In 2020 we successfully opened 164 new stores, entered

the Czech Republic and added a new DC and a new hub

Opened 100th store in

Opened 9th DC in Poland

Verrières, France +44

+8

1,716 +164 395 101

+42

+7 389

189

+1 +5

9 5

+15

Started operations in

Entered the Czech 69 2nd hub in Wrocław

+42

Republic in Q3

559

11 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 xx # of stores 2020 xx New stores opened in 2020Strengthened our unique customer proposition

Extra large store pilot in Paris Genevieve des Bois Self check-outs well received in NL and BE

Same articles, same prices and same promotions ~50% of transactions shift to self check-out in first 4 weeks

Larger floor plan of 1,600m2 Further improvement in the store operating model

Top sales per week ~€400k

12 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Very strong performance in the Netherlands

Strong LfL P1-P11 of 8.4% (lockdown in second half P12)

Strong brand with 97% awareness and 64% penetration1)

DC Zwaagdijk Upgraded store network

+8 → 8 new stores added Really, Action is the store that the

Netherlands misses the most

→ 28 refurbishments Of all stores that are currently closed due to

395 the lockdown, consumers miss Action the

most. This is evident from a survey by

→ 5 enlargements research organisation Q&A of more than 4,500

Dutch people

Het Parool 12 February 2021, 20:35 (original in Dutch and translated in English)

→ 8 relocations

DC Echt

Total of 107 stores with self-check outs

xx # of stores 2020 xx New stores opened in 2020

13 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 1) Source: GfK dashboard results 2020 and penetration is % clients that purchased one or more products at Action in the previous six monthsFrance is our biggest market with ample

remaining growth potential

DC Moissy Strong LfL of 8.1% in P1-P2 and of 13.1% in P6-P10

DC Verrières

#1 market in sales, store numbers and sales growth

~16,500 employees and ~2.7m customers per week

+42

Total sales driven by expansion and LfL ticket size growth of 12.4%

559 DC Belleville

DC Labastide

DC Ensuès (2022) Hub Martin-de-Crau

xx # of stores 2020 xx New stores opened in 2020

14 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Germany has made great progress in growth

and profit

DC Peine Strong P6-P10 LfL of 19.9%

DC Echt, NL #3 market in sales and store numbers today

83 million inhabitants provide huge potential for continued expansion

+42 Strengthened management team

389 Higher quality of new locations, more focus on urban centres and large cities

3.3

2.8 2.9 3.0 2.9

2.0 1.9

DC Biblis Average sales per store1)

Average sales per new store2)

2017 2018 2019 20203)

xx # of stores 2020 xx New stores opened in 2020

1) 136 stores openedPromising start of click & collect

Successfully piloted in multiple markets Sales development in 2021, NL (€m)

Customer selects store and products on our website

~28% ~31% ~33% ~40% ~46% ~99%

Chooses a pick up time-slot 32.7

11%

Order picked instore by Action employee

Pick up from service counter or outside 15.5

13.9 89%

9.7 10.5 45%

8.8 59%

55%

41%

week 6 week 7 week 8 week 9 week 10 week 111)2)

Sales C&C per week (incl. VAT)

Sales shopping on appointment per week (incl. VAT)

xx Index vs 2020

1) Expected sales week 11 in line with budget 2021 and sales split based on performance 16 March 2021

16 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

2) From 16 March: max 50 customers per 20 minute timeslot. Initially, only maximum of 8 customers per hour allowedOther notable successes in 2020

Further strengthened our Symphony - expanded KRONOS - 100 % roll out of

digital customer interface functionality of planning our workforce management

software to improve system

availability

Further development of Developed a new opening ESG strengthened including

private label portfolio marketing campaign supporting local healthcare

providers

17 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Agenda 1. Introduction Simon Borrows 2. Business performance 2020 Sander van der Laan 3. Strategy update Sander van der Laan 4. Financial performance 2020 Joost Sliepenbeek 5. Trading update Sander van der Laan 6. Wrap Up Simon Borrows 18 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Sustainability is an integral part of Action’s strategy

Strengthen our

International

I unique customer value II

geographic expansion

proposition

Build a simple, efficient and

III

scalable operating model

IV Make sustainability accessible

V Organisation, people and values

19 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Action’s winning customer proposition and brand appeals

to everyone and is supported by a strong business model…

Brand promise – More than you expect for less than you imagine

150-200 new articles

per week

Quality and Action

6,000 SKUs in Surprising Every day the Weekly Easy

Social Responsibility

14 categories assortment lowest price promotions shopping

(‘ASR’)

Non food discounter

Simple – Efficient – Cost conscious

20 ACTION | 3I CAPITAL MARKETS SEMINAR 2021…with a sustainable advantage and best-in-class unit

economics

Action continues to reinvest in the

customer value proposition

through even lower prices, quality

and continuous surprise

Customer value proposition Competitive advantage

Action’s increasing scale Action’s attractive customer value

enhances profitability and builds a proposition led by low prices,

competitive advantage through quality and surprise drives top line

sheer size, purchasing power and growth

scale efficiencies

Store roll-out & growth Unbeatable financial model

Action’s operating model delivers

exceptionally compelling economics and

cash generation to support store expansion

21 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Strengthen our unique customer value proposition

Strengthen our unique customer value proposition

22 ACTION | 3I CAPITAL MARKETS SEMINAR 2021As a non-food discounter Action offers a surprising

range of c. 6,000 SKUs across 14 categories

Product innovation and quality demonstrated by

Number of SKUs per category ranges between ~100 and ~900

numerous awards

Garden &

Sport Personal care

outdoor

Decoration DIY Pets

Laundry & Toys &

Multimedia

cleaning entertainment

Stationery & Linen Clothing

hobby

Household Food & drink

23 ACTION | 3I CAPITAL MARKETS SEMINAR 2021With a surprising assortment we are able to quickly

meet changing customer demand

Action offers 150-200 new articles per week Does Action have a surprising assortment?

62%

Closest

Coca Cola (375ml) 34%

competitor

€0.73 54%

~1/3 fixed

Closest

35%

competitor

54%

Chocolate Easter eggs

Closest

37%

€1.45 competitor

45%

Closest

~2/3 non-fixed 41%

competitor

Garden hand trowel

52%

€0.89 Closest

38%

competitor

47%

Assortment Closest

Examples 52%

competitor

24 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: GfK report June 2020 and company informationUnbeatable prices are the core element of our customer

proposition

Product types 60% of SKUs below €2 Known for low prices1)

A-brands

92%

~30% ~ 30% ~ 30%

Top scoring competitor 58%

83%

€1.75 €1.49 €1.79 Top scoring competitor 51%

Supplier brands 76%

Top scoring competitor 73%

~ 7%

79%

€2.59 €4.99 €3.99 ~ 3% Top scoring competitor 51%

Private labels 66%

€0-1 €1-2 €2-5 €5-10 >€10 Top scoring competitor 67%

Primary offering 65%

€10.99 €14.79 €1.89 Top scoring competitor 74%

25 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: GfK report June 2020; answers received on the question to participants: to which brand(s) does the statement ‘low prices’ apply?Action brand and format appeals to everyone

Gender Age Brand awareness1)

Female Male 50+ 35-49 18-34

97%

89%

26% 76%

47% 44% 42% 47% 42%

57% 57% 58% 58% 57% 65%

54% 49%

33% 48%

30% 24% 30%

27% 31%

43% 43% 42% 42% 43% 35% 34% 40%

26% 26% 21% 28%

Income Education Penetration1)2)

High Middle Low High Middle Low 64%

22% 22% 24% 13% 19% 26%

36% 36% 34% 31% 47%

45% 44%

36% 33% 35%

31% 32% 30% 30%

28% 41% 18% 23% 25%

42% 51% 18%

43%

47% 45% 46% 52% 48% 44%

36% 38%

23% 26% 18%

12%

1) For DE, AT, PL the % only applies within catchment area and not national

26 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: GfK report June 2020 2) % clients that purchased one or more products at Action in the previous six months…which generates high sales volumes and density

Examples of high volume items Average sales density (sales / m2) vs. competitors1)2)

Variety of face masks Aluminium foil

(1 – 50 pieces) 2.8x

Price (NL) €1.29 – €4.95 €0.99 Avg. competitors

2.7x

Volume ~76.3m >6.3m Avg. competitors

2020

Kitchen paper Disposable gloves

Price (NL) €1.68 €0.99 2.6x

Avg. competitors

Volume 3.7x

2020 >7.9m >1.5m

Avg. competitors

1) Action floor productivity based on a ‘mature’ set of stores opened before 2017

2) Competitors’ floor productivity based on 2018 public figures combined with total sales surface area figures from Locatus (NL, BE) and

27 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Euromonitor/IGD (FR, DE). Competitor floor productivity on ‘mature’ store set was not possibleFurther strengthening of multiple digital customer

touchpoints

Social media followers

Launch App first in NL… …and launch loyalty

+21%1) +50%1) programme later

2.3m 1.8m

Facebook Instagram

fans followers

Digital Early

Receipts updates

Emails and website

+19%1) +38%1) Seasonal Other

stamp card features

5m 272m

email web Supports in-store experience Drive customers to store with

sessions (e.g. product catalogue & loyalty-based engagement (e.g.

subscrib.

shopping list) stamp card, digital receipts)

28 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 1) Year-on-year growthStrengthen our unique customer value proposition

Make sustainability accessible

29 ACTION | 3I CAPITAL MARKETS SEMINAR 2021During the pandemic

we have been able to

support our customers

with much needed

essentials

Example of an Action ad

in national newspapers in

NL, BE and DE in 2020

30 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Action is already delivering on its ASR strategy

Progress made in plastics Sustainable cotton Sustainable timber

Outdoor planting

plastic accessories

with recycled plastic Action’s sustainable cotton confirmed Action’s sustainable timber confirmed

saving 1,900 tonnes of

virgin plastic at 76% for 2020 at 60% for 2020

OFFICE

HOTEL ROYAL ZIKI MINI MATTERS

Replaced single use plastics ESSENTIALS

Private Label Private Label Private Label

Private Label

31 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Our sustainability strategy focuses on four UN sustainable development goals 32 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Product – achieve 100% supply chain transparency

Safety Social compliance

We ensure all our products are safe and responsibly sourced We strive for 100% supply chain transparency

Technical file transparency/compliance for 100% transparency of entire

full assortment by end 2025 (Product IP) assortment by end 20251)

Full visibility already in place for

direct import

Product & manufacturing

Packaging

We strive to minimise our impact through manufacturing and raw

We aim to optimise our approach to packaging waste reduction

material use

Commit to 100% sustainable Publish Packaging policy and

timber & cotton by 2025 best practice guidelines to total

supply base

Deliver category specific

Circularity plans for entire Deliver 100% recyclable

business by the end of 2022 packaging for entire assortment

by end 20251)

33 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 1) except A-brandsEnvironment - minimise our environmental impact

across the supply chain

Waste management Energy & emissions

We commit to mitigating our waste to minimise our footprint We commit to reducing our energy usage and emissions

Plastic stretch wrap usage on Reduce energy usage per m2 within our

containers reduced by 30% buildings by 15% by end of 2024

Ban on use and sale of single use Ensure 50% of our total energy used is

plastics and disposables replaced renewable by 2025

by bamboo, cardboard,

paper/wooden alternatives Achieve zero gas stores

Environmental footprint Actively contribute to reduction of carbon

We commit to reducing our environmental footprint throughout our emissions of third-party operated transport

operations

Reduce carbon emissions of vehicles (e.g.

All new DCs rated in the top

with alternative fuels for Action fleet)

category by BREEAM or

equivalent standards

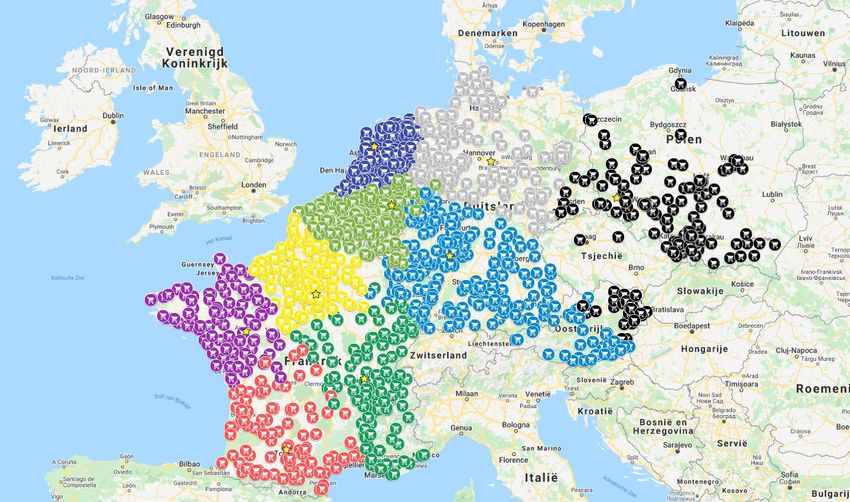

34 ACTION | 3I CAPITAL MARKETS SEMINAR 2021International expansion

International geographic expansion

35 ACTION | 3I CAPITAL MARKETS SEMINAR 2021New store roll-out is the engine behind Action’s growth

story

The reason is simple… … and the economics are extremely attractive

1

One single and successful format 1 year average historical payback on

new store CAPEX

2

Proven to travel across borders All stores opened before 2020 are

profitable1)

3

First class store opening teams & Store expansion self-funding

processes

4

Increasing operating leverage

Massive white space opportunity through size and scale

36 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 (1) Based on store contribution (incl. supply chain costs) FY2020 (including lockdowns)Principle of one format across all countries remains

unchanged

1 1 1

brand store format store operating model

Action name resonates in all languages All stores look the same Same policies

Marketing and packaging is consistent Stores between 700 to 1,100m2 Same ordering systems

and standardised across all countries Over 90% of assortment is the same Same processes

across all stores and countries Same employee training

Same management structure

International expansion of the Focus on simplicity enables Same proven formula applied

brand is seamless rapid new store roll-out to every new store

A simple, repeatable and scalable business model

37 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Continued rapid store roll-out in current markets and

entry in new markets

Population in millions

2020 237 61 47 163

% of store potential

2021

2022

1,716 stores open

FY2020

Existing markets IT ES Rest of Europe

Conservative estimate of white

Rapid expansion in

space potential in new and existing

FR, DE, PL, AT and CZ

markets (in scope) is ~4,800 stores

38 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Czech Republic – roll-out after successful pilot

DC Osla Strong start of our 5 pilots stores

Poland DC Bierun

Poland (2021) Sales growth Czech Republic on average ~30% better than in

Poland1)

Population of 11 million allows for at least 150 stores

Expect to open at least 12 new stores in 2021

No additional supply chain CAPEX

DC Bratislava,

Slovakia (2021)

39 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 1) Based on performance 2020 in weeks since start of pilot in Q3 2020 without restrictionsOpening 5-7 pilot stores in North of Italy in 2021

DC Belleville, France

Lombardy First store planned in Vanzaghello in Q2

(3 stores)

Population of 60 million, initial focus on North of Italy with 28 million

people

Piedmont

(4 stores) Start up delivered from France, first DC location identified

Local management team in place, GM hired

First store Vanzaghello

under construction Store teams recruited and currently in training

40 ACTION | 3I CAPITAL MARKETS SEMINAR 2021A simple, efficient, responsible and scalable operating model 41 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Action continues to grow its DC network to enable its

store expansion

DC Bierun, PL (2021)

DC Ensuès, FR (2022)

DC Bratislava, SL (2021)

42 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 DCs to open >2020 DCs/Hubs opened in 2020 DCs/Hubs openedDevelopment of Hubs to improve availability and reduce

inventory levels across the chain

A hub enables direct sourcing of containers from Far East

Hubs receive and palletise inventory and supply DCs

Benefits: improve availability and lower inventory levels

Hub I is a multi-site location and Hub II is a stand-alone location

both operated by our logistical service provider Katoen Natie

Direct sourcing expected to increase from ~13% of sales in 2020

to at least 20% in 3-4 years

43 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Organisation, people & values 44 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Further strengthened our management team to support

our ambitions

CEO CFO

Sander Joost

van der Laan Sliepenbeek

Commercial Director Store Director Director

Director HR

Director Operations Supply Chain Technology

Luc De Baets

Hajir Hajji Florian Knauer Joost Bous Jens Burgers

GM start-Up

GM NL GM BeLux GM France GM DE

countries

Pieter Rozendaal Judia Elkadi Wouter De Backer Bart Raeymaekers

Monique Groeneveld

GM Czech

GM Austria GM Poland GM Italy

Republic

Boyko Tchakarov Slawomir Nitek Philippe Levisse

Petr Julis

45 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Executive committee Country General ManagersRoll-out of values across the organisation ensures we preserve our Action DNA 46 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Agenda 1. Introduction Simon Borrows 2. Business performance 2020 Sander van der Laan 3. Strategy update Sander van der Laan 4. Financial performance 2020 Joost Sliepenbeek 5. Trading update Sander van der Laan 6. Wrap Up Simon Borrows 47 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Our repeatable financial model remains unchanged

1 2

• Low SKU count

• New store roll-out and country

expansion • Consistent gross margin across

Clear value Superior store categories

drivers • LfL sales growth economics • All LfL stores profitable

• EBITDA margin

• High sales density

3 4

• Proven

• Low capital intensity Strong

Excellent cash • Consistent

• Negative working capital economic

generation • Predictable

• Fast payback model

• Robust

Delivered with discipline and tight control

48 ACTION | 3I CAPITAL MARKETS SEMINAR 20212020 performance explained

• LfL growth

• Store expansion

Action’s

• Operating leverage

repeatable • EBITDA margin

financial model • CAPEX

• Cash conversion

+

• Impact of 53rd week

• LfL normalisation

2020 additional • Covid-19/social distancing restrictions impact on OPEX

drivers • Germany, Austria and Poland coming of age

• Cash management

• IFRS 16

49 ACTION | 3I CAPITAL MARKETS SEMINAR 2021Continued strong sales and EBITDA growth in 2020 in

spite of the Covid pandemic

Net sales (€m) Operating EBITDA (€m)

8.9% 10.2% 13.8%

5,637 12.4%

5,569

5,114

609 616

4,216 541

3,418 450

2,675 387

1,995 310

1,506

226

166

2014 2015 2016 2017 2018 2019 2020 2020 (53 2014 2015 2016 2017 2018 2019 2020 2020 (53

weeks) weeks)

Operating EBITDA (%) 11.0 11.3 11.6 11.3 10.7 10.6 10.9 10.9

Run-rate EBITDA (€m) 190 265 361 456 509 601 651

50 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company information Note: all 2020 figures based on 52 weeks unless explicitly referenced to 53 weeks financialsFull year reported LfL impacted by lockdowns

Normalisation for weeks 12 – 22

+480bps

→ Only applied for countries which were

10.4 forced to close stores and/or remained

open with limited assortment

→ Includes normalisation for reopening

7.6

7.2 6.9 effect

→ Normalisation based on performance

►6.0% 5.3 5.6

YTD week 11 2020

3.2 Normalisation for weeks 44 - 52

→ Only applied for countries which were

forced to close stores and/or remained

open with limited assortment

→ Includes normalisation for reopening

effect

(1.4)

→ Normalisation based on performance

2014 2015 2016 2017 2018 2019 2020 2020 YTD Q3 2020

normalised

Annual LfL % growth

Average LfL 2014-2019

51 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationNormalised 2020 LfL growth +10.4% versus (1.4%) reported

1 2 3 4

Week 1 – 11 Week 12 – 22 Week 23 – 43 Week 44 – 52

40%

+7.3% (34.9)% +7.4% +12.7% (4.8)% +11.3%

20%

0%

(20)%

(40)%

x.x% Reported LfL

(60)%

x.x% Normalised LfL

(80)%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

week

52 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationStrong LfL growth in all countries between lockdowns

LfL sales growth by geography, week 23 – 43

20.7%

19.4%

14.5%

13.2% 12.7%

11.8%

8.4%

Netherlands Belgium Germany France Austria Poland Total

53 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationStore closures and assortment restrictions in quarters

1,2 and 4

Net sales per quarter (€m)

15.3%

23.3% 1,804

1,541 1,564

9.1% (8.8)%

1,216 1,250

1,184

1,085 1,109

Q1 Q2 Q3 Q4

2019 2020

54 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationStore openings: programme delayed by pandemic,

catch-up in 2021

(1)

244 (2) (3)

6 232 230

11

19

197 32

20

6 16

164

115

141 5

89

1 100 93 44

108

68 15

39

42

80 72

23 31 60 59

25 42

24 18 19

18 18

21 17 13 14 13 12 8

8

2014 2015 2016 2017 2018 2019 2020

Czech Poland Austria France Germany BELUX Netherlands

(1) Net stores added was 243 as a result of one store closing in the Netherlands

(2) Net stores added was 230 as a result of two store closings in the Netherlands

55 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 (3) Net stores added was 227 as a result of three store closings in the Netherlands Source: company informationConsistent margins across all categories

60 %

50 %

40 %

30 %

20 %

10 %

0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Categories

56 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationOperating leverage shows in all countries with Germany,

Austria and Poland coming of age

Average store contribution margin by country P6 to P10 - stores opened before 2019

+100bps +100bps

+60bps +285bps +120bps

+385bps +215bps

# of stores

375 167 288 424 38 25 1,3221)

openedTotal CAPEX development

(In €m)

5.4% (17.5)%

11.3% 210 Lower CAPEX (€37m) versus last year as projects were

199

paused and new store expansion temporarily halted during

179

173 the first lockdown

Lower CAPEX spend per new stores reflects continuous

efforts to reduce €/m2

Continued investment in IT

123

105 Other

98

DC maintenance

71

Store maintenance / RERs

IT

New DC (incl. IT)

2017 2018 2019 2020 Store expansion

58 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationStrong cash flow: 2020 cash conversion of 76%

100% Low capital intensity, negative

700 100

92% working capital and fast payback

86%

600 for new stores lead to strong

77% 76%

73% 75 cashflow, notwithstanding Covid-

500

70%

462 451 19 impact on timing of sales and

58% 419

400 working capital and required cash

50

314 management

300 268

225 223 Cash and cash equivalents end of

200

153 25 week 53 was €590m (excludes

100 €100m unused revolving facility)

0 0

2014 2015 2016 2017 2018 2019 2020 2020 (53

weeks)

Operating cashflow (excl. CAPEX for new DCs)

Cash conversion = Operational cashflow / Operating EBITDA

59 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationOverview of high-level financials

Change 2020 (53 Change

2019 2020

(vs 2019) weeks) (vs 2019)

Net sales (€m) 5,114 5,569 +8.9% 5,637 +10.2%

LfL sales growth 5.6% (1.4%)

Operating EBITDA (€m) 541 609 +12.4% 616 +13.8%

EBITDA margin 10.6% 10.9% 10.9%

Cash conversion 77% 76% 73%

Number of stores (end of

1,552 1,716 +164 1,716 +164

year)

60 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationImpact of IFRS16 on Action 2020 financials

The average lease period of Action’s store portfolio is

RIGHT-OF-USE ASSET AND

EBITDA (€m)1)

LEASE LIABILITIES (€m) 3.4 years but differs per country

→ Action is desired as a tenant by landlords as it

758 784 drives traffic to the destination

36 782

202 → At the end of a lease Action receives competitive

616 pricing for renewals

IFRS16 impact on other financials 2020:

→ Lease adjustment: €202m (2019: €179m)

→ Depreciation right-of-use asset: €190m (2019:

€170m)

Adjusting items mostly non-recurring cost for long-

Operating Lease Adjusting IFRS16 Right-of-use asset Lease liabilities term incentive plans

EBITDA adjustment items

1) 2020 based on a 53 week financial year

61 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationSummary 2020 financial performance

• Strong normalised LfL growth in all countries between lockdowns

Strong LfL performance

• Product offering tailored to meet changing customer demand

5,569

5,114

• Strong LfL shows operating leverage in all countries

Country EBITDA

• Additional Covid-19 related opex

• Mitigated availability issues over the summer

Supply Chain

• Covid-19 related complexity

2019 2020

+

• Store expansion and projects halted during the first lockdown

541

609 Very strong performance • Strong focus on cash management and stock levels

between lockdowns and • Start-up costs of new DCs and investments in IT

continued investments to • Incremental investments to strengthen capabilities in commercial,

support growth planning, digital, supply chain and support

• Expansion of Czech and Italian team

2019 2020

62 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationAgenda 1. Introduction Simon Borrows 2. Business performance 2020 Sander van der Laan 3. Strategy update Sander van der Laan 4. Financial performance 2020 Joost Sliepenbeek 5. Trading update Sander van der Laan 6. Wrap Up Simon Borrows 63 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Current trading 2021 – situation by country at 17/3/2021

m2 per Shopping by

Country Stores open Click & Collect Assortment

customer appointment

NL 25* n/a* Y All* Full

BE 10 All Y N Full

LU 10 All N N Full

DE 10/20/40** 157 out of 391 N 214 stores Full, 18 stores essentials only***

FR 10 554 out of 572 N N Full

AT 20 All Y N Full

PL 15 All N N Full

CZ 15 All N N Essentials only (~53%)

* As of 16 March: max. 50 customers per 20 minute timeslot

** For fully open stores: first 800m2; 1 customer per 10m2 and above 800m2, 1 customer per

20m2. For Click & Meet stores: 1 customer per 40 m2

64 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company information *** 2 stores closedCurrent trading 2021

Negative LfL sales P1 and P2, turned positive in P3

→ Netherlands, Germany and Czech Republic heavily impacted by store closures

→ YTD LfL week 10 of >25% in Belgium, France, Luxembourg and Poland

Supply chain and DCs are operating well with good product availability

2021 store expansion plan on target with store openings above last year in Q1 so far

Cash and liquidity currently €525m

65 ACTION | 3I CAPITAL MARKETS SEMINAR 2021 Source: company informationAgenda 1. Introduction Simon Borrows 2. Business performance 2020 Sander van der Laan 3. Strategy update Sander van der Laan 4. Financial performance 2020 Joost Sliepenbeek 5. Trading update Sander van der Laan 6. Wrap Up Simon Borrows 66 ACTION | 3I CAPITAL MARKETS SEMINAR 2021

Action is one of Europe’s best retail growth stories…

2020 2023

✓ Action is one of the most successful retail

growth stories in Europe

Sales €5.6bn c.€9.0bn

✓ Action story is stronger from the pandemic

✓ 2023 business plan targets are unchanged

EBITDA €609m >€1bn

# Stores 1,716 c.2,750

# Countries 8 >12

# DCs 9 c.15

673i provides long-term capital backing and strong governance

Governance Long-term vision

3i provides active and responsible governance with a 3i brings an ambitious, growth-orientated long term

focus on the ASR agenda mindset to Action

Investment Values

Prioritisation of investment in Action’s infrastructure 3i leadership protects and supports Action’s customer

continues to drive value creation for all stakeholders values and culture

68Submitting questions

Click here

69Thank you for your attention! Thank you for your attention!

You can also read